Where Are Markets Today?

Global markets received a better boost today following President Trump having unveiled overnight a “massive trade deal” with Japan. S&P 500 futures gained 0.10%, Dow futures increased by around 70 points or 0.16%, and Nasdaq futures remained in the flatline area. In Europe, the Euro Stoxx 50 futures rose 1.1%, indicating positive sentiment regarding the risk assets. On the heels of the close at the 11th record high in 2025 by the S&P 500 following morning pressure from decliners in the semiconductor stocks sent the Nasdaq into the red area. Investors are factoring the impact from the revived trade optimism against prevailing fears over the regulation on the AIs and the earnings from the techs as well.

President Trump’s 15% bilateral tariff Japanese trade deal seems to have calmed some protectionist jitters in the market. It provoked a night-time equity rebound in Asian markets spearheaded by a greater-than-3% rise in the Nikkei, and then a revival of risk appetite in the major equity indices. The potential for a similar deal in the EU and China has deepened expectations for a more benign global trading landscape. The futures relief rally is particularly dominant against the backdrop of political uncertainty as Trump’s remarks at the same time targeted Federal Reserve head Powell and surveyed sweeping presidential action. However, there are still cautious undertones too. With the lead U.S. tech players in Tesla and Alphabet unveiling earnings today, the traders will wait and see before they react how the Magnificent Seven will perform under the earnings squeeze. Moreover, Existing Home Sales data later in the day will arguably influence bond yields and provide the lead-in for Fed guidance in response especially from the sluggish manufacturing sentiment and treasury yield slump the previous day. The traders watch how the interaction between the consumer-side data and Trump’s fiscal plan within the tax reforms and home sales evolves.

Based on Zaye Capital Markets, the futures morning performance reflects a tactical rally rather than a structural breakout. As much as the near-term sentiment has been positive on the back of the US–Japan trade agreement, conviction on earnings, independence of the central bank, and the broad policy agenda of the Trump administration will continue to remain pivotal. Meanwhile, we continue to favor selective exposure on areas of trade tailwind exposure alongside monetary stability and AI monetization—albeit with caution in the face of volatility triggered by policy action.

Major Index Performance through July 23, 2025

- Nasdaq Composite: 20,974.17 (-0.3%)

- S&P 500: 6,309.62 (unchanged)

- Russell 2000: 2,248.76 (+0.8%)

- Dow Jones Industrial Average: 44,502.44 (+0.4%)

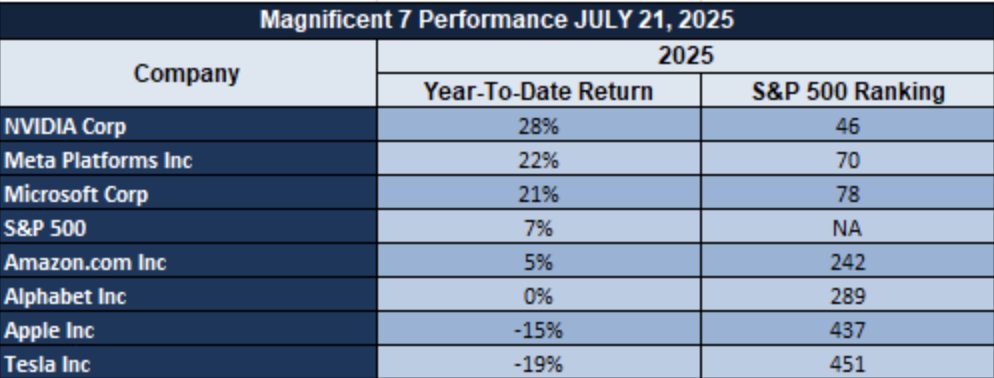

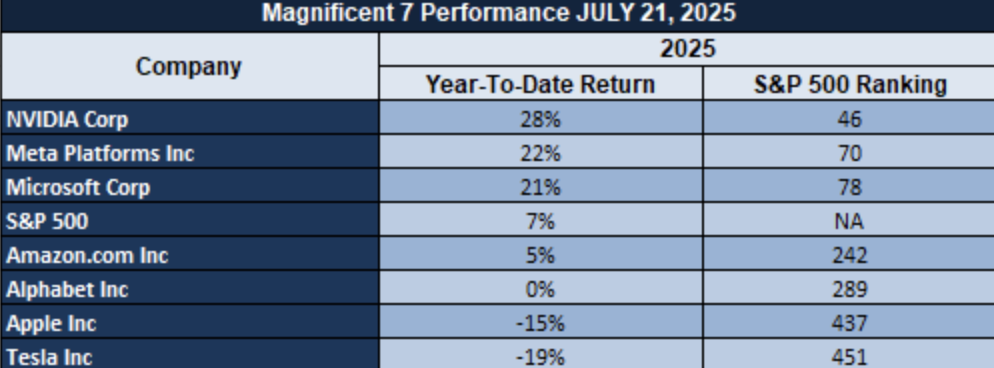

The Magnificent 7 & S&P 500

S&P 500 still leads at the top fueled by the tech-heavy Magnificent Seven—but increasingly discretionarily. Nvidia, Meta, and Microsoft are leading the index on the back of AI infrastructure scale and monetization momentum. Meta particularly enjoying bullish sentiment in balancing superintelligence ambitions with platform-wide AI revenue growth. Apple and Alphabet are still star underperformers, lagging the S&P 500 by up to 20% and 14%, respectively. Tesla also underperforms but Elon Musk’s bold pivot towards AI compute—550K GB200/GB300 Nvidia chips coming into production over the next year and a five-year goal of 50 million H100-equivalent units—sets up a high-risk, high-capital AI war that can remake Tesla’s future trajectory.

Drivers Behind the Market Move

- Stunning U.S.–Japan Trade Accord

President Trump’s revelation of a “massive” US-Japan trade arrangement—at a two-way 15% tariff and a $550 billion bilateral investment agreement—has shifted mood in global markets. Japanese equity futures increased ~3%, and European futures jumped ~1.1%, since there is ever-growing hope more of the same is in the offing with the EU and even possibly China. The surprise breakthrough has removed the heat from the trade scare and the green light for a near-term risk asset pickup.

- Federal Reserve & Trump’s Fed Bashing

Trump’s fresh attack on Fed Chair Powell as a “numbskull” and his statement that he would be replaced in eight months has introduced fresh uncertainty into U.S. monetary policy. Supporting yesterday’s weak manufacturing report and sliding Treasury yields, the market is now doubting the extent of additional rate cuts. Further, this dynamic would benefit defensive exposure in weak points across the cycle while extending compression in bond yields.

- Information On Housing And Tariff-Connected Inflation

The next Existing Home Sales release—along with data revealing single-family home building activity dipping to the 11-month low despite the elevated mortgage rates and tariffs—ramp up the focus on consumer well-being and inflation risk. A soft housing release would confirm slowdown fear, driving housing-connected equities and lending into long-duration positions. A robust reading would temper some of the bearish macro story.

From the perspective of Zaye Capital Markets, current market drivers are a mix of spot relief on the back of trade developments, continued uncertainty at the Fed level, and macro data to confirm or refute the growth story. Investors have to watch closely policy headwinds, yield bias, and home sales for direction on near-term positioning.

Digesting Economic Data

The TRUMP Tweets and Their Implications

President Trump’s latest sequence of announcements on policies—itself both through formal statements and social assurances—has caused a spurt of volatility in the financial markets, re-centering investor sentiment in general. His announcements ranged from a synchronic promise of exemption from capital gains tax on the sale of homes, 19% duty on Filipino shipments, and a broad 15% trade deal with Japan. Touted though they were as pro-growth initiatives, these re-directions in trade are indicative of a shift towards bilateralism and protectionism and re-activate fears on retaliatory pressure on American exports and inflationary headwinds—especially on consumer staples, housing, and industrial inputs. Such announcements are even influencing equity risk premiums and currency market positions.

As compelling was the threat Trump made he could oust Federal Reserve Chairman Jerome Powell in eight months and called him a “numbskull.” Such talk—and frequent Fed-bashing—heightens worries about central banks’ independence. The specter of politicized behavior at the Federal Reserve could induce bond market strife, further volatility amid the anticipation of the direction of rates henceforth, and instigate a new bid into hedging products such as gold and cryptocurrencies. Already we witness gold support at $3,400 and Bitcoin above $119,000 as option positions repriced in anticipation of prospective institutional dislocation. For the tech and artificial intelligence sector, Trump’s promise to sign the executive orders at the coming AI summit and rescind previous Biden administration orders has stoked controversy over the regulation of theartificial intelligence domain. His announcements indicate central American leadership on theAI front to be the course on the policy work which may help defence technology, cloud computing infrastructure, and chipmakers. Those actions may induce regulatory backwash from global stakeholders andreticent regulators apprehensive of the U.S.-faced standardisation. In the marketplaces, that has been instrumental in speculation inflows into the highest-capAI plays and into theNvidia-linked assets, and assisted the current drive into theAI monetisation by the platformMeta.

Lastly, Trump geopolitics continue confused—tempting the US towards UNESCO for being “woke,” and then suggesting a China visit is “not too distant” and rancorage in commerce is losing steam. Such conflicting signals negate certainty for multilateral co-op model-building and world capital movement. Investors in the case are offered this type of lone trade intervention and choosy diplomacy in the form of an even defense-oriented, agile position-taking approach. At Zaye Capital Markets, we’re advising clients to emphasize hedging FX exposure, building protection on exposures long in tenure, and paying close attention to policy moves in traditional and digital venues.

Richmond Manufacturing Slump Exposes Fragile Regional Baseline

July 2025 Richmond Fed Manufacturing Index fell back to -20, pleasantly above projections and one of the deepest one-month dives in years. Sub-indicators—- new orders at -25, shipments at -18, and hiring at -16—-all confirm the finding regional manufacturers are slowing on multiple fronts. The dive defies the national picture with impunity— a 0.1% increase in U.S. manufacturing activity in the prior month had projected stagnation. So vast a regional miss means the external headwinds–such as changing trade currents–maybe particularly punishing the Mid-Atlantic corridor.

Global trade riffs—new tariff threats—have placed significant stress on regional manufacturing centers dependent on world border inputs and export markets. The wide U.S. production platform is sending calming indications, though regional levels of exposure to global value chains and political tensions in the Richmond region are inspiring downside risk. Richmond’s index has been a solid leading indicator of the wider industrial softness in the aggregate when declines are caused by imploding order books and payroll softness.

In our opinion, Caterpillar (CAT) is currently selling at a discount to its intrinsic value, a function of overdone regional pessimism due to its diversified international exposure and long-cycle project backlog. Analysts will have to look to future data from the Dallas and Kansas City Feds to determine whether July’s surprise is an anomaly or proof of a trend. In our opinion at Zaye Capital Markets, look cross-regional divergence and how trade policy continues to propagate within the mid-sized industrial ecosystems.

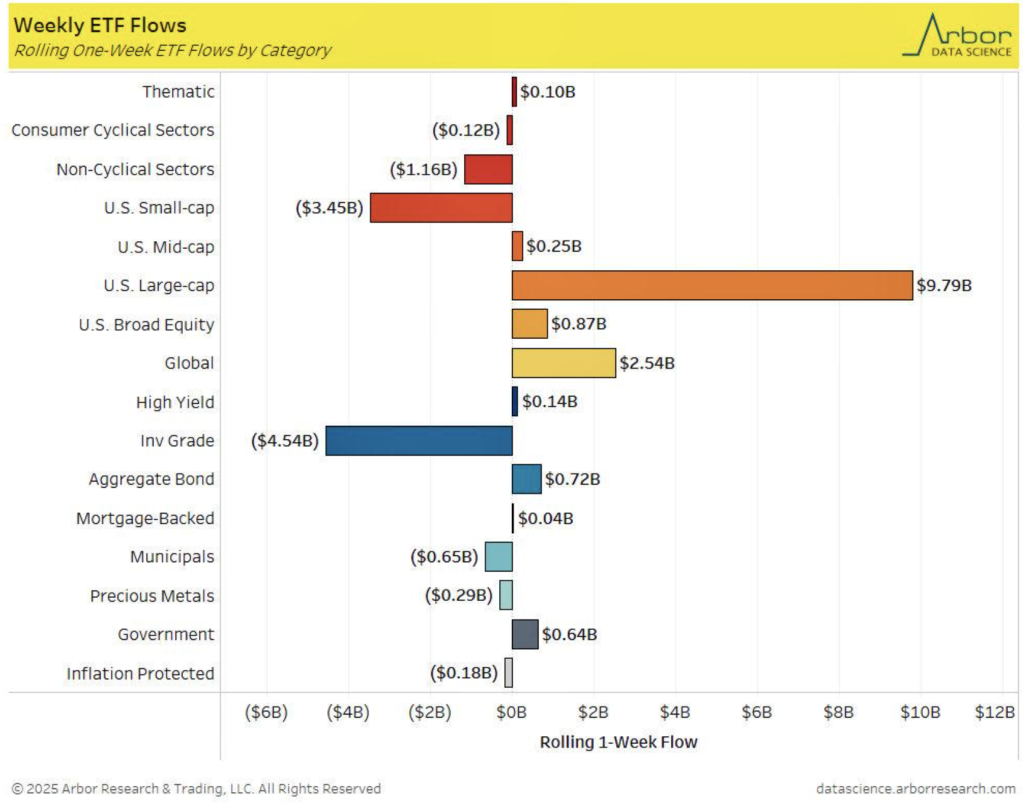

Large-Cap Etf Inflows Signal Flight To Safety As Policy Drives Rotation

A record $9.7B influx into U.S. large-cap ETFs in the last week suggests investors’ appetite for safety despite the ongoing macroeconomic agitations. That comes after the Federal Reserve dovish turn in the fourth quarter 2024 when the lending rates were tightened and rallied capital-starved companies with stronger balance sheets. That was preceded by redemptions from the small-cap ETFs of $1.1B, and the investment-grade bond funds lost $5.4B—the more widespread risk-off sentiment with focus on the rate sensitivity and the credit exposure.

Involved is a selective capital migration process more reminiscent of previous Fed-induced risk splits. Gilt-edges hurt by the more costly refinancing cost and rate-sensitive debt profile continue harming until the monetary easing path gains traction. Redemptions from bond funds may foreshadow waning yield appeal or equity inflows into so-called safety stocks. The market is reading cues—not risk-motor chases but redefinition by the measures of liquidity, size, and operating leverage, particularly in the large-cap builds.

We consider Etsy (ETSY) our value play in this regard, intimidated by volatility short but likely to recover in the event cuts in rates alleviate pressures on costs and spark spending by consumers. Weekly ETF flow potentially can go alongside Fed forward guidance and compared regional central bank sentiment—especially tighter-biased ECB—to gauge relative allocation of capital. We at Zaye Capital Markets still concentrate on adaptive allocation strategies where monetary policy is the key variable in asymmetrical rotation in the markets.

Food Price Normalisation Includes Disinflaton Pockets In The Volatility Of The Commodities

Global ag prices are re-balancing with FAO reading in June 2025 that sugar prices fell 5.2% from previous spurt on pandemic-caused dislocation and geopolitics. Meat prices hit new highs on back of tardy restoration in supplies but overall picture is towards a gradual disinflationary correction at the world level especially in the grain and softs complex. With improved monsoon progress in India and Thailand in the last few days crop yield prospects improved and supported this downside movement in major ag inputs.

This ‘rolling over’ of the inflation within food is more than just seasonal dynamics. It is reflective of regional price stabilisation factors where supply side relief within the main production countries is overtaking prior shocks. USDA 2.9% 2025 food price increase forecast—the lowest since pandemic highs—suggests inflation is becoming more and more segmented. Investors will see this represents a narrowing in the width of inflation but by no means a complete reversal where some segments continue to sharpen divergence.

We believe Archer-Daniels-Midland (ADM) is undervalued since prices today do not capture gains from hardening commoditiy processing and distribution margins, particularly in stabilised input conditions. Care should be exercised on weather-risk fluctuations in crop estimates and monthly release of prices by the FAO. In Zaye Capital Markets, we believe disinflationary tailwinds in food can underpin bottom-line support in agribusiness stocks hitherto afflicted with surges in input prices.

Leading Indicators Edge Higher, But Growth Signal Remains Ambiguous

The Conference Board Leading Economic Index (LEI) diffusion reading reached 40% in June 2025 from the low in April of 15%. Although this indicates expanding components gaining traction, the reading remains far from the 50% level in the past that has been correlated with macroeconomic wellness. Below-50% six-month LEI diffusion readings before the current episode have been accompanied by below -4.1% growth rates and continued on to trigger recessions. Current readings once more point to a soft environment and offer little more than a cautious recovery at best.

Structural vulnerabilities remain in spite of progress. Factors like interest rate spreads and equities’ performance have been volatile, while others like new orders and consumer confidence still remain below their pre-crisis levels. Even though rising diffusion trends can be attributed to markets as a reverse head-and-shoulders signal at the bottom, long-term studies discover that reliability in the LEI becomes thinner in extended low-growth regimes—possibly exaggerating recoveries’ short-term momentum.

We think the stock is undervalued at this level considering the cyclic stock and the strength in holding the way through the downside with positive free cash flow culture. You will need to wait until the next prints on jobless claims and new orders manufacturing for more validation on macro turning points. At Zaye Capital Markets, we do recommend over-reliance on the LEI for directional conviction and diversification into stocks exhibiting elastic cost structures and defensible margins.

Fed’s Restrictive Rate Policy Puts U.S. in Solitude in World Money Cycle

New forecasts have the U.S. Federal Reserve maintaining rates over 2% up until 2027—the reverse in extreme form from fellow central banks already in easing form. The longer flat range is a sign indicative of continued inflation fears most especially price accelerations from trade observed in the Fed minutes from the 2025 June meeting. At odds with the ECB and SNB in shifting ahead of the slowdown in demand, the Fed stance is a reflection on the cautious attempts at credibility maintenance against homegrown cost surges from the policy on tariffs.

Such divergence has long-term implications. The currency markets have already responded accordingly, with the Swiss Franc advancing to a 20-year peak against the US dollar in defiance of zero-bound rates—a vindication of the fact that differential rates are the only source of FX strength. Contrastingly, dollar softness stems from investor nervousness prior to fiscal guidance, prevailing trade imbalances, and jitters related to the change in political leadership. Delay by the Fed also has the risk of policy lags lingering post-inflation-containment phase and damaging capex and consumer lending at a time when growth slowdown is a reality.

We continue to believe Home Depot (HD) is underpriced here in that investor rate-scepticism of rate-related housing headwinds overlooks the leverage in the company’s balance sheet and long-cycle consumer stickiness. Investors will need to keep the next Fed Summary of Economic Projections and ECB statement synchronization closely for clues on relative macro exposure. Our view at Zaye Capital suggests there is room in funding resilient companies, most particularly companies positioned to benefit when the Fed finally looks abroad at convergence trends in easing.

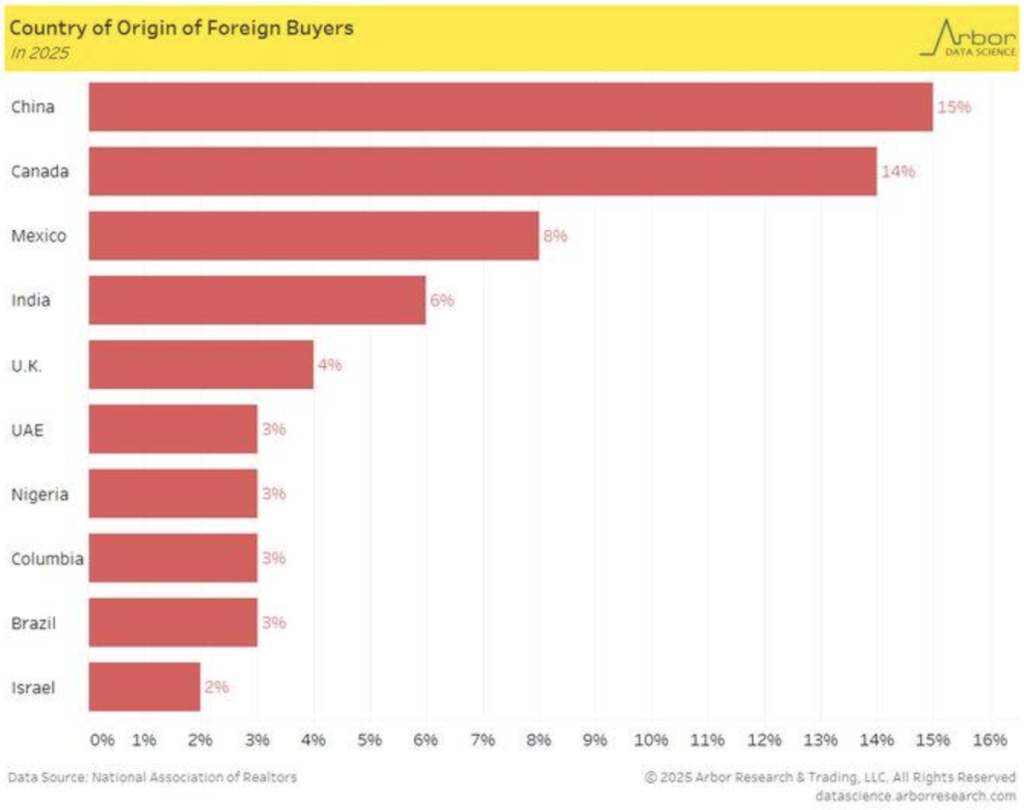

Chinese capital reasserts influence in u.s. Housing amid global rotation

Chinese purchasers are once more the largest foreign group among American residential property buyers and represent 15% of the overall foreign transactions, the 2025 National Association of Realtors said in the latest report. Such a reversal, representing $13.7 billion in property buying, represents a steep 44% year-over-year gain in foreign home buying. Differing from the prior year’s Canadian pattern, such a drastic reversal into the opposite direction represents repositioning in concert with currency shifts and Chinese outbound capital flows resuming after regional policy changes and economic nervousness.

The implications of these trends reach the price trends of metropolitans in the world’s largest metros, since peer-reviewed literature often attributes foreign investment to locally rising real estate prices in metros that have the best demand conditions. To boot, whether “Chinese” purchasers are mainlanders, expats, or naturalized Americans makes the matter more complex. However, the scale and speed of this rellocation confirm structural global imbalances, especially in light of persisting US affordability challenges and policymakers’ consideration of restricting foreign investment control.

We find Zillow Group (ZG) to be undervalued on these grounds of web market leadership and ability to capitalize on overseas buyer demand streams in high-data home categories. Treasury and legislative discussions around issues of foreign ownership restrictions and altering terms of housing credit are issues of interest from the analysts’ side. From our side of Zaye Capital Markets, we anticipate selective real property and proptech equities to capitalize on this renewed capital inflow, particularly in supply-restricted urban corridors.

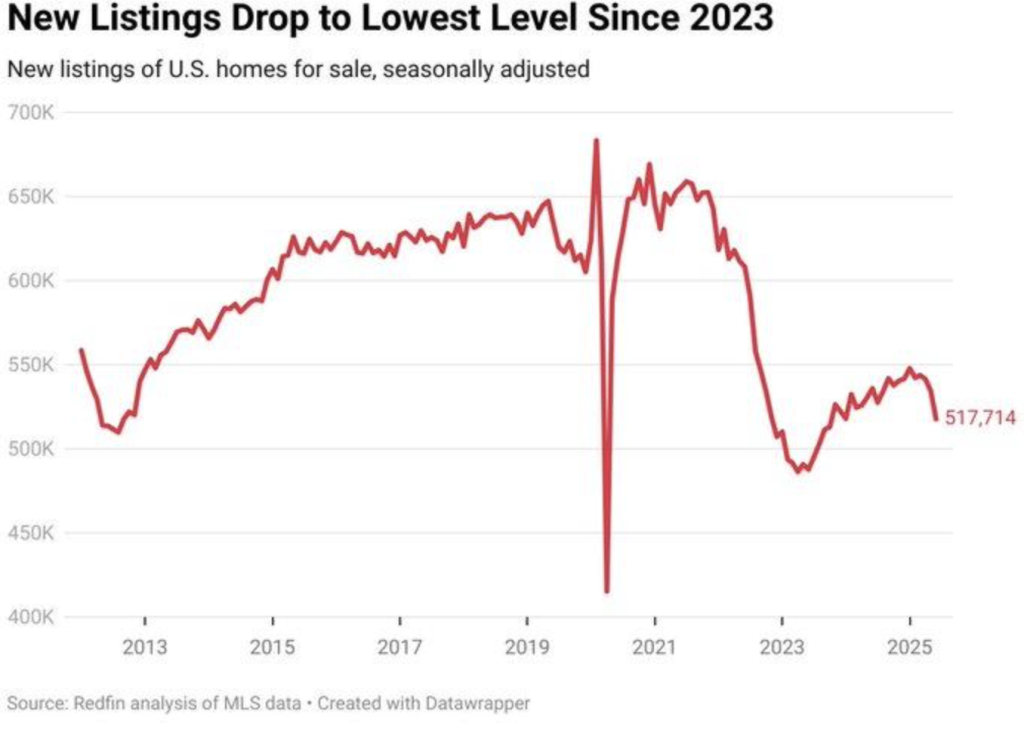

HOUSING INVENTORY DROPS TO MULTI-YEAR LOWS AMID CREDIT TIGHTENING PRESSURES

U.S. home inventory fell to 517,714 in 2025, the lowest since 2023 levels despite a 3.2% inventory drop in June alone, the most recent Redfin statistics indicated. The resulting inventory decliner is predicting increasing pressures from increasing mortgage rates as locked-in homeowners at beneficial earlier rates resist selling. Such structuralgridlock increasingly tightens housing supplies and lowers marketplace fluidity and potentially portends even wider economic exposure on the ongoing softening in new home and resale activity.

The trend is a mirror for earlier indications seen before the 2007–2009 housing-led recession, when falling inventory covered underlying market distress. In contrast to the subprime crisis, however, the risk of today is due to credit cost increases and access to capital constraints, rather than default contagion. Across the world, the UK Office for Budget Responsibility estimates mortgage rates to reach 4.7% by 2028—implying higher borrowing costs might be a structural feature, not a cyclical blip, aggravating affordability and inventory shortages for advanced economies.

We think Lennar Corp (LEN) is too cheap considering especially its scalable model business, land banking stock, and adjustable-for-demand-build-rates. Future shifts in mortgage applications, housing commencements, and lending criteria should be watched by analysts for signs of.systemic stress or policy incursion. Select homebuilders and the modular building group are positioned for relative outperformance compared to the group as the industry readjusts back towards longer-term normalisation of rates and changes in housing demand dynamics, says Zaye Capital Markets.

Upcoming Economic Events

Existing Home Sales

With the market heading into the climactic phase of economic clarity, the coming week holds major data revealing the robustness of the American consumer and the resilient nature of the virus-led recovery in the housing market. While the rates are steep and the supplies shallow, Existing Home Sales can influence risk taking in all housing, credit, and consumption markets. Here are what we must look out for and how the numbers can influence market action:

Existing Home Sales

This housing gauge is a real-time reading on American consumer expenditure and mortgage affordability.

- A beat in the real Existing Home Sales reading from projections will likely be celebrated as evidence of fortitude in the face of increasing borrowings expense. That beat will re-ignite the housing shares, raise the yields on Treasuries, and quell speculation over forceful cuts in interest rates by the Fed. Fix-it home and building product shares will pick up speed as well given bets on steady homeowner relocations and credit availability.

- But a disappointing sales outcome will be interpreted by the market as confirmation the housing market is stressed. A miss on the downside may even seed a more general risk-off rotation—particularly in conjunction with soft consumer sentiment—on homebuilders and switch investors into defensives. That should reheat easing speculation by the Fed, sending yields downward and providing near-term support for growth-sensitive rates instruments.

At Zaye Capital Markets, we will monitor trends in mortgage applications and stockpiles closely in trying to gauge whether this is a fleeting slowdown or more structural.

STOCK MARKET PERFORMANCE

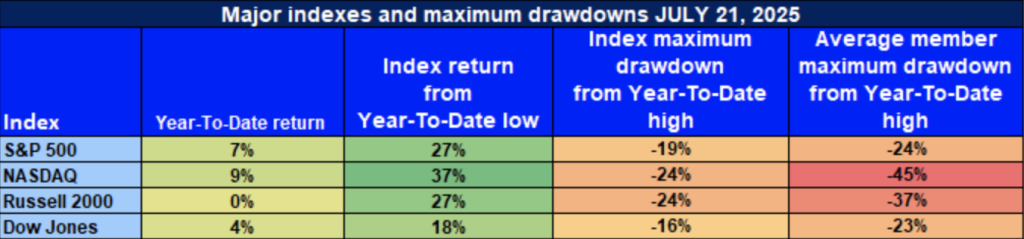

Indexes Bounce Back from April Low, But Breadth Indicators Sound Cautious Sound

U.S. equity markets posted respectable recoveries from the April 8 lows but year-to-date performance remains unbalanced by benchmark. Index advances conceal volatility underneath and declining breadth and average member drawdowns reveal structural stress underneath. At Zaye Capital Markets, we still examine internal index health for evidence of durable participation.

Below is our summary of the previous week’s performance on benchmark indexes:

S&P 500: Resilient Top-Line Gains Bely Wider Damage

YTD: 7% | -27% from April low | -19% from YTD high | Av. member: -24%

S&P 500 has recording a satisfactory 7% YTD gain and 27% retrace from the early April bottom. However the 19% peak-to-trough loss and 24% average member selloff indicate thin strength by a mere handful of leaders propelling the rally on dwindling underlying breadth.

NASDAQ: High Beta Performance, Deep Member Losses

YTD: +9% | -37% from April low | -24% from YTD peak | Avg. member: -45%

The NASDAQ still leads on a 9% YTD gain and exceptional 37% comeback in April. But the extreme 45% average membership drawdown betrays concentration risk and questions the staying power in growth-driven rallies.

Russell 2000: No Year-To-Date Gains in Spite

YTD: 0% | +27% vs. the April low | -24% compared to the YTD high | Avg. member: -37% While the small-cap Russell 2000 has increased 27% from the lows, it’s unchanged year YTD, though unimpressed in the broader small-cap rally. A 24% index decline and 37% average constituent drop mirror growing exposure in economically sensitive sectors.

Dow Jones: Equilibrium With Modest Recovery

YTD: +4% | +18% below April low | -16% from YTD peak | Avg. member: -23% The Dow Jones is very stable with a 4% YTD and a contained 16% drawdown from highs. But these types of average member losses of 23% affirm underlying stress, even from the more defensive sectors of the market.

We are selective at Zaye Capital Markets. Although headline indexes are reassuring, the broad-based scatter in performance in the constituents suggests more selective approach in quality name stocks with decent earnings and defencive balance sheets.

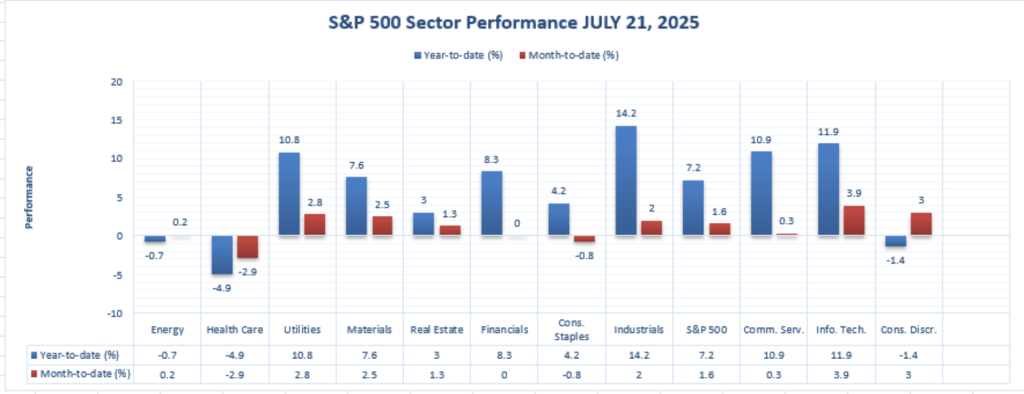

THE STRONGEST SECTOR IN ALL THESE INDICES

Industrials Drive Forward as Larger Market Momentum Approaches

If we break performance across the S&P 500 into sectors, there is definitely a theme out there—Industrials are driving the pack. Up 14.2% year-to-date, they lead all others, alongside the growth-sensitive Information Technology (+11.9%) and Communication Services (+10.9%) groups in the process. That surge is partly the result of robust demand across defence, manufacturing and logistics sectors on the strength of beneficiary effects of reshoring initiatives and government related infrastructural expenditure.

While others like Utilities (+10.8% YTD) and Financials (+8.3% YTD) have held out, Industrials show the very combination of sustained outperformance and rate hike defense that we have been expecting. Even in the month-to-date picture, the sector contributed 2.0%, behind only Information Technology (+3.9%) and Utilities (+2.8%), once again showing sustained rotation leadership.

For Zaye Capital Markets, Industrials represents the best-of-breed position in the space of volatility-rate sensitive investors and policy-change. Relative leadership in humble drawdowns and stronger pipeline orders in the order book reinforces our confidence in believing Industrials are in the most well-placed and intrinsically supported cycle in evidence today.

EARNINGS

Earnings Recap – 22 July 2025

- Coca-Cola Company (KO)

Coca-Cola had a decent Q2 beat on earnings with net income up 58% to $3.8 billion and adjusted EPS of about $0.87–0.88, coming in above estimate. Revenue grew about 1%, with 6% pickup in pricing/mix, but volume declined 1%. The business improved the margin by about 34% through premium product placement and cost control. Operating cash flow was dented by the large acquisition-related payment. The earnings showed the strength at Coca-Cola in resisting macro headwinds through pricing strength and great brands despite concerns over FX sensitivity and liquidity fluctuations.

- Philip Morris International Inc

Philip Morris let down the market, the shares declining 8.4%, on below-estimate revenues and underwhelming Zyn nicotine pouch sales. Expansion in smokeless categories proved too little to overcome overall softness in the market even as continued spending in the lower-risk product categories continues. The miss was the result of softness across core geographies and uncertainty around the pace of conversion by consumers away from traditional products. Investors will be seeking updated guidance and the business model for penetration in emerging markets.

- RTX Corporation

RTX beat earnings forecasts by a narrow win but cut guidance in the negative half-turn, forcing a soft correction by close to 1.6%. With defence-related backorders staying rock solid, cost inflation and doubts over programme execution guidance caused nervousness. Investor interest over RTX’s cyclic sustainability of its margins and principal contract order sequencing despite persistent input inflation in the business is gathering.

- Texas Instruments Incorporated

Texas Instruments beat on the upside reporting $4.45 billion revenue up 16% and $1.41 in earnings per share. Even though management cut Q3 profit forecast on more conservative examination of demand environment, this was in spite of the beat. Company’s aggressive spending with a $60 billion capex in fab facilities helps the long-term picture but could compress the margins in the short term. More Demand Visibility in price trends and inventories is desired by the analysts.

- Intuitive Surgical, Inc.

Post-market results for Intuitive Surgical were strong operating traction with 8% growth in EPS and 17% revenue growth guidance. The business strength comes from the growth in procedure volume internationally and base growth in robotic surgical systems. Investors focus on the growth in recurrent instruments and accessories revenue and growing adoption in emerging regions.

Earnings Preview – 23 July 2025

- Alphabet Inc (Google) Class C

All will center on the profit of Alphabet today compared with the estimate of $2.17 in EPS and $93.7 billion in revenue. Investment analysts will most look at the performance in the underlying ad business, growth in the cloud business, and trends in monetization in YouTube. Discussion on the cost of building the AI and blending lines will attract the most attention. Ad slowing indicators or compression in the cloud on the margin will temper enthusiasm.

- Tesla, Inc

Tesla is reporting earnings with an estimated EPS of $0.44 on revenue of almost $22.7 billion. Look for vehicle delivery, gross margin per vehicle, and China and North America pricing strategy. Since competition in global EVs is increasing and cost-cutting is being experienced, investors will be keen to understand how Tesla’s market share is being sustained while it remains profitable when battery input prices are volatile.

- T-Mobile US, Inc

The T-Mobile earnings focus today will involve subscriber growth, churn level, and 5G network monetization. Stable service revenue will be forecast by analysts and talk regarding potential growth in the future in the ARPU and the latest in a string of in a string of spectrum deals synergies. Investor sentiment will depend on pricing model and retention in a communications competitive environment.

- International Business Machines Corporation

IBM report will show the sustained momentum in the hybrid cloud and the AI businesses, the offsets to the slowdowns in the legacy business. Points of emphasis will be the software renewals, gross margin outlook, and execution in the global markets. Investors will look for the vision on the monetization opportunities for the business in AI and efficiency programs as IBM becomes a new business whose solutions will resonate with the new businesses.

- ServiceNow, Inc

ServiceNow will release earnings where the specifics will get combed through for growth in subscription revenue, ARR, and Customer additions. Since spending by the enterprises has softened up, the most important commentary will be on retention rates and deal size. Investor attention will focus on strength in spending budgets on digital and if macroheadwinds are diminishing plans to buy.

- AT&T INC.

Performance at AT&T today will look into the future performance trends in broadband and wirelss by measuring the increase in the subscriber additions and the generation in the free cash flow. With the business performing on the back of heavy debt levels and capex needs the investor will look at how efficient it is at generating growth despite paying the dividend. Infrastructure Investment Direction And Pricing Tactics will figure prominently.

Stock Market Recap – Wednesday 23rd July 2025

Markets face macroeconomic indicators-high-stakes cocktail and Q2 earnings strength and fresh geopolitical flare-ups. With the Federal Reserve in inaction even as inflation stickiness risk and trade policy concerns are back in the consideration picture, sentiment within the investor realm remains in harm’s way. Treasury yields have fallen on a reading on temperate growth prospects, and the equity picture is still unevenly biased—pretty much by the large-cap techs.

Stock Prices

Economic Indicators & Geopolitical Environment

July Federal Reserve minutes once more hinted at restraint against inflation by resisting commitment towards deeper rate cuts despite soft wholesale data. At the same time, geopolitical tensions are escalating with anticipation building towards fresh developments on tariffs in significant trade channels. Such triggers in conjunction with earnings swings kept major indices in narrow bands as risk sentiment becomes cautious.

The Magnificent 7 & S&P 500

S&P 500 still leads at the top fueled by the tech-heavy Magnificent Seven—but increasingly discretionarily. Nvidia, Meta, and Microsoft are leading the index on the back of AI infrastructure scale and monetization momentum. Meta particularly enjoying bullish sentiment in balancing superintelligence ambitions with platform-wide AI revenue growth. Apple and Alphabet are still star underperformers, lagging the S&P 500 by up to 20% and 14%, respectively. Tesla also underperforms but Elon Musk’s bold pivot towards AI compute—550K GB200/GB300 Nvidia chips coming into production over the next year and a five-year goal of 50 million H100-equivalent units—sets up a high-risk, high-capital AI war that can remake Tesla’s future trajectory.

Stocks Update

- $META is actively funding superintelligence development and has been showing stellar performance in the monetisation of AI in the ecosystem, positioning the stock for gains.

- $RKLB (Rocket Lab) was requested to bid on possible future Golden Dome launch contracts and now directly competes with SpaceX—a flip of the script on the commercial space race.

- $TSLA / $NVDA: Tesla has officially announced it will enable 550,000 Nvidia GB200 and GB300 devices in the coming weeks and xAI will enable 50 million H100-equivalent GPUs over the next half-decade—the total cost will be roughly $1.25 trillion, marking unprecedented large-scale private spending on the development of AI.

Major Index Performance through July 23, 2025

- Nasdaq Composite: 20,974.17 (-0.3%)

- S&P 500: 6,309.62 (unchanged)

- Russell 2000: 2,248.76 (+0.8%)

- Dow Jones Industrial Average: 44,502.44 (+0.4%)

At Zaye Capital Markets, we remain selective amid policy noise and narrow market leadership. We favour quality names with pricing power, exposure to AI or energy, and recommend holding defensive positions while hedging rate and geopolitical risks.

Gold Price – Wednesday, 23 July 2025

Gold is higher at $3,435.50/oz in August futures, spot prices around $3,423.44/oz, holding firm just below the $3,450 resistance level. The market is kept neatly in balance by increasing political volatility. President Trump’s recent outbursts-threats at removing Fed Chair Powell from office, adding 19% tariffs on the Philippines, signing universal AI executive orders and eliminating capital gains tax on house sales–have sparked the policy uncertainty pushing gold to safe-haven status. His message he will sign a US-Japan trade agreement and dovish remarks on China is brooding some geopolitical risk. Existing Home Sales later today will be sentiment pivot; a soft read will see gold break out above resistance on renewed growth worries, while a beat will have the potential cap near-term gains by sparking risk appetite.

Gold’s bullishness is still supported by the decaying yield environment and soft downside surprise in manufacturing data from the previous day vindicating dovish sentiment bias but failing to raise red flags on inflation. Cautious guidance from the Fed and the latest in crypto regulatory saga and debate on role of the AI in policy is spinning hedging demands on systemic level. From Zaye Capital Markets’ perspective, gold convincingly holds above the $3,400 level and macro crosscurrents like political volatility and slowing housing turnover will persist and keep it a defensive asset in the near term.

Oil Prices – Wednesday July 23 2025

Oil prices jumped this morning with Brent at roughly $68.92 and WTI at $65.64 in the wake of a new US–Japan free trade pact and a 1.6 mm barrel drop in US inventories in a shocking about-face, marking firmer-than-forecasted demand. The IEA and OPEC redrew conservative demand growth estimates—700,000 bpd and 1.29 mm bpd correspondingly—but yielded to stronger-than-anticipated Asian consumption in the first half of 2025. Such supply-demand dynamics are keeping oil steady in a $65–$70 bracket, and US Energy Secretary commentary on newly added Russian sanctioning is providing a geopolitical premium. More dovish West yields and dovish US economic data yesterday provided tailwind for oil as the markets backed off aggressive near-term Fed hiking risk, and inflationary demand stress was maintained.

And in the meantime, President Trump’s recent statements are creating waves in the energy markets. His revelation of 19% Philippine import tax, large Japan trade deal, and potential Chinese de-escalation fueled concerns over future demand and inter-global trade flow—triggering mild safe-haven crude flow. On watch is today’s Existing Home Sales reports: a solid reading will allay oil’s rise by supplying evidence of economic resilience and rate expectations; while a soft reading will revive growth concerns and support prices as investors go into defence mode. At Zaye Capital Markets we remain moderately upbeat on oil short term, with structural inventory drains and geopolitics conflict playing to defend prices above the mid-$60s even despite cautious organisational expectation.

Bitcoin Prices – Wednesday, July 23, 2025

Bitcoin stands at $119,214 today and reached intraday highs at $120,256 and lows at $116,751 as institutional and policy support for the asset gains in earnest. Later today, the White House will release the US government’s first crypto policy report ever in the form of suggestions for a strategic Bitcoin reserve and the regulating the stablecoins. The release comes on the back as PNC Bank collaborates with Coinbase in a bid to facilitate crypto-trading and as JPMorgan considers crypto-backed lending—programs which strive towards making Bitcoin a regular in traditional finance. Trump Media’s latest revelation of a $2 billion Bitcoin bet has generated even more bullish sentiment, taking BTC even more into the mainstream limelight. The developments show a large-scale adoption wave gathering steam as the players in the market increasingly consider Bitcoin both store of value and institutional asset.

President Trump’s spate of statements—including calling for the removal of Powell to the release of new tariffs and AI administrative decrees—have enlivened economic volatility into the broader macro environment. Nevertheless, pro-crypto commentary from his administration, such as earlier attempts at creating a Strategic Bitcoin Reserve, has given Bitcoin the proprietary tailwind for gains. Yesterday’s dovish economic data and moderate Treasury yields have solidified BTC’s non-correlated hedge status in the face of slowing macro growth. With today’s Existing Home Sales data being processed by the markets, any suggestion at economic cooling within the week can supply more bullish momentum behind Bitcoin’s current rally. In the opinion of Zaye Capital Markets, BTC remains within the confines of a policy-revaluation cycle where geopolitical volatility and institutional onboarding continue to affect its position in diversified portfolios.

ETH Prices – Wednesday, 23 July 2025

Ethereum stands at $3,742.54, back a bit from an intraday peak at $3,767.95. While there has been some token price weakness, institutional buying remains steadfast, led by U.S. spot ETH ETFs, which in just this month have seen inflows exceed over $3 billion by themselves and set a new single-day record of $726 million. Whale on-chain inflows are adjusting for this unprecedented demand increase, as over 681,000 ETH (~$2.57 billion) have been aggregated since July 1 and $117 million of leverage-aided whalebuys via Aave in a mere five days. Profit-taking is in evidence—the most prominent being a whale unloading 8,005 ETH for roughly $30 million in profits—but accounts over 10,000 ETH are up by nearly 4%, revealing continued confidence on the whales’ part in the face of current RSI reading near 85, indicative of near-term overboughtness.

Institutional building, ETF inflows, and whale purchases are continuing to underpin Ethereum’s growing role in decentralized finance and broader builds in the portfolio. Yesterday’s dovish US data and declining yields offered crypto instruments a little more upside room to maneuver, and housing figures today will set the tone in the rates space and short-term digital token inflows. At the same time, progress on crypto regulatory themes—the White House crypto paper coming soon—the list goes on—is settling Ethereum in the bigger cycle revaluation on the back of policy moves. Our view at Zaye Capital Markets is Ethereum remains inherently well-supported longer term but in the shorter term charts most likely temper into the $3,400-$3,600 range before a potential breakout towards $4,000+ in Q3.