Where Are Markets Todays?

Global equity exchanges will open higher today, Monday, July 28, 2025, as U.S. and European futures rocket with renewed optimism for trade policy, upcoming corporate earnings, and central banks forecasts. U.S. equity futures went up across the board Monday morning with Dow futures up by 171 points (+0.38%), S&P 500 futures up by 0.41%, and Nasdaq 100 futures up by 0.55%, writes CNBC. European futures made a similar move with a bearishly optimistic bias but with humble gains, with Germany’s DAX up by 0.27%, France’s CAC 40 up by 0.31%, and FTSE 100 futures up modestly at +0.18%. The coordinated bearishly optimistic tone arrives as investors look forward to a high-stakes week with focus-topping events that can move markets.

Markets are taking positively to weekend news from President Trump that America negotiated a deal with the European Union to reduce tariffs to 15%, sidestepping previously threatened 30% tariffs on a wide range of European imports. The agreement not only calms transatlantic tensions but also encourages export-facing industries within America and Europe. The dovish move to trade has enhanced sentiment around the globe but specifically within industrial and materials stocks most at risk to outcomes of tariffs. According to Zaye Capital Markets, this trade development lifts a huge near-term overhang, and investors can look to shift focus to earnings and monetary policy. Keeping pace with subsequent gains is also anticipation of meeting this week by Federal Reserve. With no sudden policy change, investors are seeking fresh wording of interest-rate tone, inflation outlook, and balance-sheet policy. With softening inflation and slipping consumer confidence, investors are seeking dovish tilt—and especially with all this geopolitical saber-rattling and ongoing Trump demand for soft dollar. Supporting gains for very sensitive to liquidity assets like tech and crypto currencies, this trend is assisting.

Contributing to the optimism are the string of big-tech earnings filed this week, including some of the “Magnificent Seven.” After their tech shares fell short in July, healthier earnings would be just what is needed to reassert leadership. In Europe, robust company confidence and generally robust services sector are supporting upbeat momentum. At Zaye Capital Markets, we are tracking closely central bank cues, trade diplomacy, and sector-general earnings momentum as the drivers of risk appetite and near-term positioning.

Major Index Performance as of 28 Jul 2025

- S&P 500: At 5,899.42, down 0.4% during the day.

- Nasdaq Composite: At 18,131.70, lower by 0.6% as tech

- Dow Jones Industrial Average: 40,290.35, no change, up 0.3% as industrials gain

- Russell 2000: 2,086.90, -0.2% as the small-caps can’t get into gear.

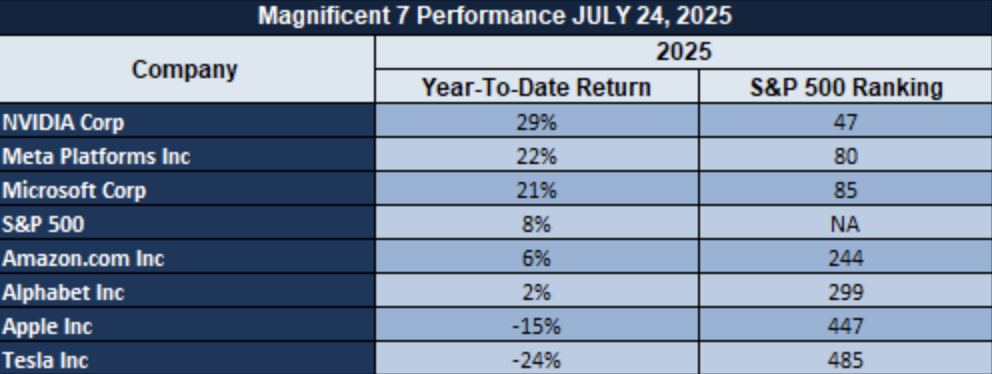

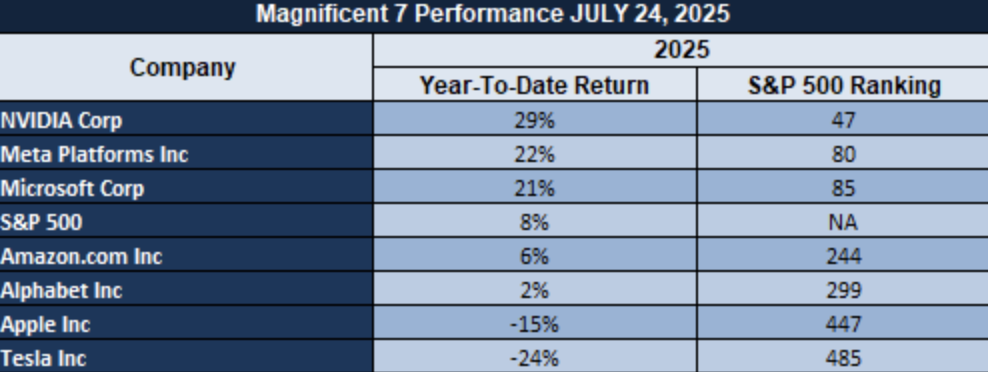

S&P 500 and The Magnificent Seven

S&p 500 remains soft as the “Magnificent Seven”—Nvidia, Apple, Microsoft, Amazon, Meta, Alphabet, and Tesla—take brutal drawdowns. Financial Twitter sentiment is such that all those tech giants are all out of steam as there are valuation corrections as well as spotty Q2 earnings. Nvidia and Tesla are seeing profit-takin as there is a spectacular first-half performance, while Apple and Amazon are reeling under regulatory problems as well as demand issues.

This selective leadership in performance persists in testing the mettle of wider S&P rally, with defensives and industrials now displaying relative strength.

Drivers Behind The Market Move

Global equity markets are higher today, the result of fresh optimism on the heels of recent patterns in both trade and position-managing in anticipation of major macro and earnings events. U.S. major index futures are higher—S&P 500 (+0.41%), Nasdaq 100 (+0.55%), and Dow Jones (+0.38%)—and European futures were higher too, with Euro Stoxx 50 (+1%) and DAX futures (+0.3)

1. U.S.–EU Trade Agreement Relaxes Risk Attitude

President Trump’s publication of a preliminary trade agreement with the European Union—to create a 15% quota on a variety of EU imports and garner EU pledges of US purchases of $750bn of energy and US investment of $600bn—has underpinned sentiment in both US and European markets. The agreement helped to calm transatlantic trade nervousness and minimize headline risk prior to a hectic policy week.

2. BOJ & Fed Meetings Steal Limelight with Clarity

On Trade During central meetings this week by Bank of Japan and by Federal Reserve, markets are pricing against rate forecasts along with inflation commentary. The agreement of trade lifts a giant uncertainty, and investors can consider whether policymakers are expressing dovish bias with weak consumer sentiment and weak US home data that were witnessed yesterday.

3. Tech Outlook and Earnings in the Spotlight

As earnings season gets underway, especially at mega-caps techs, video trading is saying less breadth and nervous optimism. Soft spots at retail and miniscap—chiefly highlighted by yesterday’s economic data—has reasserted sector-rotation logic: healthier stocks with earnings momentum with less policy sensibility are running off into the week.

Zaye Capital Markets looks for trade action, communications from the Fed, and company news as markets absorb shifting policy trends. We are long select equities and sectors whose trade and tariff risk sensitivity is lower.

DIGESTING ECONOMIC DATA

Trump Tweets and Implications

President Trump’s recent string of remarks triggered a storm of economic and geopolitical commentary with far-reaching implications across markets. His harsh denunciations of currency manipulation—accusing Japan and China outright of flagrantly devaluing currencies—fanned anxieties of a global currency war re-emerging. By using his own preferred action for a softer greenback to make US exports more affordable by declaring “When you have a strong dollar, you can’t sell anything,” he removed ambiguity from his own reason for wanting a weak US currency to make US exports more affordable. The position casts a shadow of uncertainty over dollar-denominated assets and suggests future pressures on the Federal Reserve to acquiesce to rate reductions—an interpretation that is already supporting gains in such assets as gold and cryptocurrencies such as Bitcoin and Ethereum.

Trump tariff rhetoric has escalated, with new threats of unilateral tariffs on Canada and assertions that, “Most of the trade deals are finished right now.” This is perceived by the markets as a potential shift in protectionist policy, especially when his assertion that “Lower dollar makes the tariffs worth more” is factored in. For global equities, this brings uncertainty to trade stability, with multinational companies preparing for possible disruption of supply chains. In our studies at Zaye Capital Markets, such policies are inflationary in the short-term and growth-suppressing in the medium-term, poised to place pressure on risk assets but bring upside to hedges like gold and crude oil. Trump’s assurance that Australia will start importing U.S. beef is a monumental win for farm exports, but the overall tone of uncertainty makes it challenging to predict trade. His geopolitical commentary is no less significant. On the Middle East, Trump’s aggressive announcement that “You’re going to have to finish the job” with Hamas—and that “They want to die”—may destabilize additional fragile region negotiations. Such rhetoric injects volatility to oil markets and safer-haven sentiment less easy to evade. Trump’s polemical position with Europe—asserting immigration as “killing Europe”—and vituperative tone with foreign leaders and institutions (e.g., Macron, the EU) stokes additional tension, potentially damaging allied confidence and transatlantic flow of investment. His lopsided commentary regarding home officials and scandals, such as his unusual complementarity with Powell and remarks around Maxwell and Epstein, sustains an image of unpredictability that makes investor prognosis less transparent.

Although we see this latest Zaye Capital Markets broadside as more than political rhetoric, rather a genuine market warning, it is a harbinger of fresh volatility in FX, commodities, and emerging markets. Strongman policy rhetoric, currency rebalancing, and trade belligerence portend more egregious macro rotations, dollar volatility, and periodic safe-haven buying. We expect a need to watch economic decrees from the White House, Treasury reaction, and foreign pushback in the coming days. Markets now price in fundamentals alongside presidential posturing and political risk.

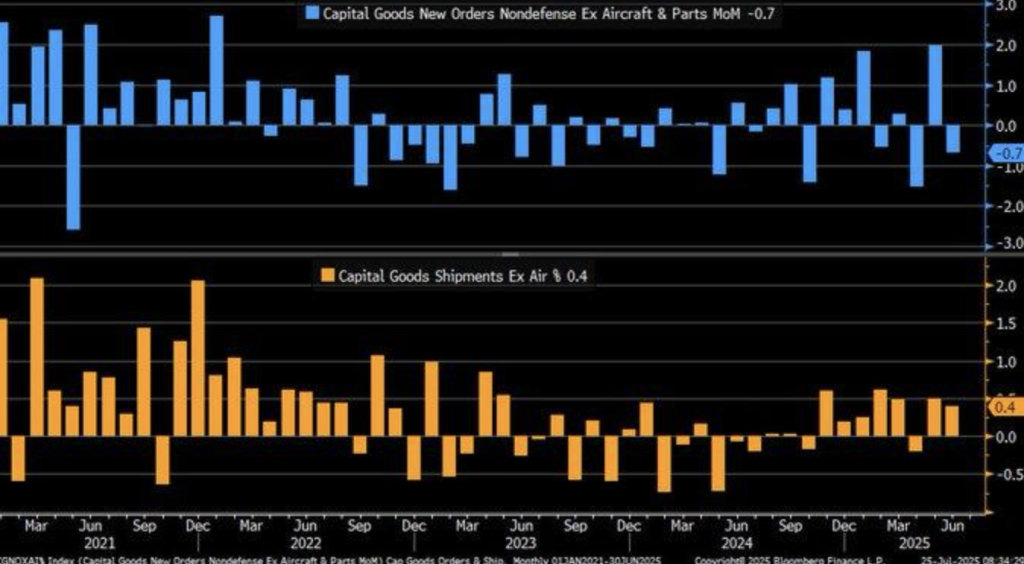

Capex Contradictions Signal Business Sentiment Shift

We are keenly waiting to the dramatic miss for the June capex numbers as it suggests rising circumspection on the businesses’ spending part. Core capex excluding defence and aircraft fell down by -0.7% against the +0.1% uptick on the wires. The surprise fall is raising eyebrows on private sector sentiment more so when it is long-term strategies on the spending part. Core shipments rose +0.4% as expected more the burning through backlog effect than renewed excitement with business sustaining operating stream but not making the type of bold forays into new projects.

This is not dissimilar to the pre-recessionary set-ups around the 2008 downturn when rising shipments were offset by fading orders as inventories were run down while new capex was avoided. Accompanying support is one of caution—presumably the aftermath of the persistent inflationary anxieties and ambiguous policy direction. Whilst the top-line numbers might just continue to gesture towards health, the innate pattern of catching up on current desire at the expense of the future might bleed the growth chart as it crosses into Q3.

For the case at hand, we believe industrial automation hardware provider Rockwell Automation (ROK) to be potentially undervalued. Sensitivity of capex reversal to its long-cycles exposure is offset by the current prices that are not yet accounting for the order slowdown. Investors should monitor future releases of industrial manufacturing PMI alongside equipment leasing trends to better establish whether such defensive positioning is short-lived or part of a fundamental business strategy shift.

Housing Price Break Down Unveils New Builder Sentiment Focus

We are seeing surging convergence of the trends for U.S. house prices that mirrors the bifurcated housing market. Since the median existing-home-price low of the year 2022, they have risen uniformly to $441,500 moderated largely by severely tightened supply as well as hardened footing of homeowner recipients of sub-6% mortgage rates. For the new-home median price part, it crashed down 7.3% year-over-year to May 2025 as led by extremist builder incentives like mortgage rate buydowns as well as upfront discounts on house costs. Such convergence is more marketplace dynamics than merely marketplace dynamics; it is likewise on-purpose product response from the builders to affordability headwinds.

The widening divergence holds that although the existing-home marketplace is sheltered with lean inventories, the new-home marketplace is more sensitive customer. Cost-cutting actions of the builders’ tendencies—after 37% of them trimmed costs last June for the first time since May of 2022—are the testament to the desperation to somehow generate demand on the heels of unfavorable macro conditions waiting to emerge. That reaction is reminiscent of earlier house cycles when new construction remained more sensitive to monetary tightening, defying prevailing assumptions regarding similarity to the marketplace.

In this context, we believe homebuilder PulteGroup (PHM) is undervalued. With calculated price reductions, the company has good land positions and access to diverse financial products. Investors will be watching for continued mortgage application data and builder sentiment indexes to measure whether the trend of lower pricing continues to accelerate or flattens. These are leading indicators to use to measure the sustainability of demand and margins for the new-home category.

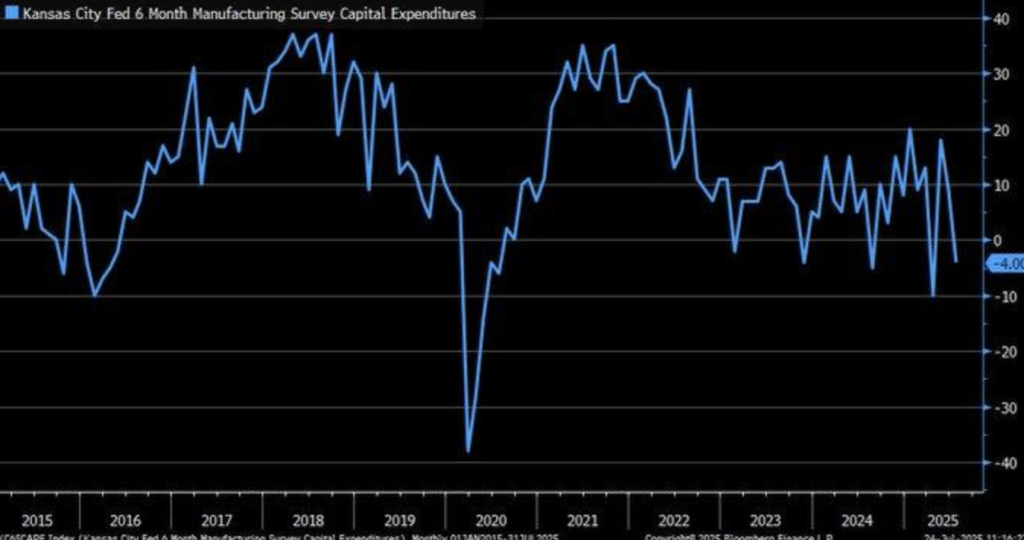

Capex Expectations Conflict With Strategic Supply Chain

We are monitoring a sharp decline in industrial plans for investment, including the July 2025 Kansas City Fed Manufacturing Index. Plans for capital expenditure are down for the first time and at the low since they peaked back in 2022. The sharp drop is a sign of increased producer nervousness with the macroeconomic environment marked by uncertainty, squeezing margins, and the changing post-pandemic pattern of trade. Loss of confidence with the index down to -10 for May from -5 for April is characteristic of waning optimism for expansionary spending_a common forerunner to major recession indications.

Rather than driving long-term asset creation, the industry is adopting risk-mitigation plays. Only 78% of businesses will invest in supply chain software in 2025, according to a recent survey, as they adopt a defensive approach to build up operatical resiliency against volatile demand and supply chain unpredictability. Rather than billion-dollar investment sagas, much of the funds are being channeled into maintenance capex or digital infrastructure rather than new plants or equipment upgrades. That is part of the overall company conservativism and is consistent with past cycle turns when investment plans were put on the backburner in favor of preserving the status quo.

This time, we believe that Honeywell (HON) is underpriced. With diversified exposure to industrial automation as well as software-based digital supply platforms, the stock is best poised to take advantage of the software-fueled transformation. Investors ought to watch closely at order and software license revenue of the next batch of its earnings for the best indications of where industrial budgets are being reallocated. Watchful eye on regional Fed surveys will also be essential in determining if the capex pullback is transitory or more of a structural shift.

Kansas City Price Pressures Defy National Inflation Trends

We are monitoring manufacturing cost transmission closely, with the Kansas City Fed Manufacturing Index “Prices Paid” declining modestly in July of 2025 but the 6-month ahead reading still elevated at 64.0. That implies while pressures in the near term are weakening to some degree, regional manufacturers remain attentive to still further input cost volatility in the future. Consistency of forward-looking indices is unexpected compared to the weaker trend for the aggregative measures such as ISM’s Prices Paid data, reflecting regional inflationary pressure not as fully represented in the aggregative measures.

This type of imbalance can be caused by specialist regional dependencies, i.e., local supply chain networks or specialist energy inputs, which subject Kansas City producers to special pricing risks. Consistent with this perspective, earlier history and industry surveys indicate that manufacturers of goods having protracted cost uncertainty are more intensely invested in digital supply chain management technologies. As more recent studies of manufacturing point out, this precautionary strategy enables companies to steer through chokepoints due to union disputes or logistics bottlenecks—particularly applicable in the aftermath of recent U.S. freight and port activity price hikes.

We think Emerson Electric (EMR), with its deep exposure to industrial automation and technology, is undervalued to this degree. The firm is well-placed to benefit from increasing expenditure on cost-cutting technologies along the industrial belt. Analysts simply need to track shifts in regional transport costs, energy inputs, and electronic buying behavior in Q3 so they can better be positioned to anticipate price pressure and the redrawing of regional supply chains’ capitals. This divergence can be the harbinger of the early warning signs of more pervasive inflationary stickiness outside the headline data.

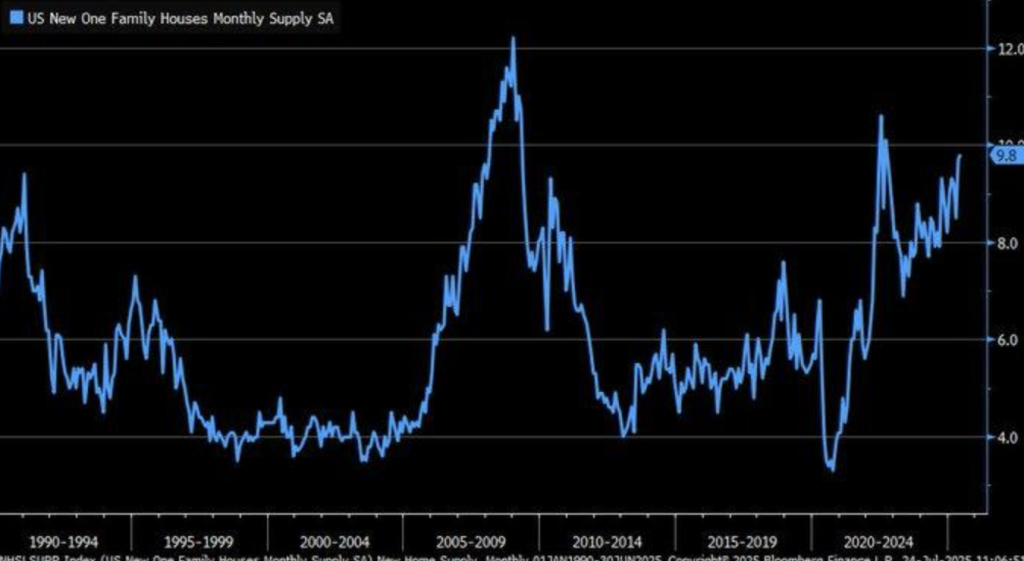

Surge In New Home Supply Signals Shift Toward Buyer-Led Housing Market

We see unprecedented turnover in the U.S. homebuilding industry, with new home inventory at 9.8 months in June 2025—well beyond the 5–6 months that pervaded prior to 2020. So high a level of supply portends continuously rising new home unsold inventories that are propelling the industry towards buyer dominance. Such circumstances were felt before at pivotal inflections within prior cycles of homebuilding, typically prior to builder repricing or price adjustments, by historical experience at the Federal Reserve. Such circumstances are less concerning now, however, as sound equity positions and stricter underwriting standards diminish risk at a systemic level.

Despite the fact that the new stock would reduce the affordability squeeze that has been holding the market back since 2019, the lack of pervasive stress signals—like 90% of homes lower than 2010 levels of foreclosure—predicts a soft landing rather than a crash. Construction appears to be cushioning the slowdown through sequential completions and concessions, rather than panicky selling. A better-balanced market may yet develop as buyers gain leverage, potentially retarding appreciation but sustaining long-term house demand by stepped-up access.

Against this background, we view Lowe’s (LOW) as undervalued. The company will benefit from growing buyer demand, home renovations, and do-it-yourself repair as homes enter an increasingly affordable cycle. Share investors need to keep very close attention to home starts, builder sentiment, and mortgage rate trends to determine the viability of this supply base growth and its spillover impact upon consumer spending as well as real estate-related equities.

Pmi-Driven Output Price Gains Reignite Inflation Concerns

We’re witnessing new acceleration within U.S. Composite PMI Output Prices equal to 1970s inflationary cycle trends. The 54.60 July 2025 mark is indicative of continued growth as firms are voluntarily dealing high inputs to end-users. The trend, represented by a spike output pricing 2021-2023, represents a 2.4% year-over-year CPI gain to May 2025. With CPI data modest-looking, trend within PMI implies potentially underlying inflation undercurrents not quite fully being represented by consumer indices at this time, particularly with ongoing uncertainty around energy costs as well as global supply chain stresses.

This inflation push that is generated owing to structural buildup is escalating wage-push process, thus augmenting production expenses give birth to wage rises and stoke over-pricing spirals as well. Similar to that 1970s stagflation episode, companies are pushing broader consumer indexes with prices, indicative of reporting lag of inflation. History vindicates that increases in output prices can give birth to sticky inflation at consumer level and leaves central banks between rock and a hard place—one that constrains policy, but one that causes too early policy relaxation.

We still consider DG cheap at this stage. Being a discount retailer, it will tend to accelerate when there is real income squeeze, regaining demand from price-conscious consumers. Trends up until Q3 of wage inflation and real spending power will be scrutinized by analysts as that will best indicate whether this recent beat of output price inflation is spilling into broader spreads, and how that will influence consumer trends by income class.

Investor Sentiment Hovers Neutral As Market Awaits Clear Direction

We are witnessing a sharp correction of investor sentiment, with the AAII bull-bear spread almost at zero as of July 25, 2025. The balance indicates an overall lack of conviction in direction of the market, most typical under transitional regimes of markets. The spread in AAII has seldom remained at extremes since 2017, but this decline comes following post-election volatility, and therefore linked to global macroeconomic concerns in policy shifts and inflationary pressures undermining retail investor sentiment.

In all historical times, outlier sentiment measurements close to zero are most associated with consolidation times within markets, rather than with reversals per se. The 2019 paper correlating outlier measurements with S&P 500 reversal picks up predictive momentum of measurements, but not present neutral attitude that investors will adopt a wait-and-see attitude. Sentiment cooling is reinforced by soft consumer spending, as seen within central releases, and retail trading volume moderating along main U.S. exchanges within recent quarters.

Against this sentiment background, CME Group (CME) appears undervalued to us. During uncertain and low conviction markets, retail derivatives exchanges typically witness rising hedging and vol-related trading activity. Analysts will want to watch movement in options open interest and volatility metrics such as the VIX to determine whether current soft spots will give way to resumed directional force or ongoing consolidation on broad indexes.

Upcoming Economic Events

New Releases Not Scheduled for Today

As markets have been digesting recent macro events and waiting for fresh directional leads to emerge, today’s economic schedule is a welcome reprieve with no noteworthy data releases due. The lack of economic releases due is a chance for investors to catch up with recent inflation, capital spending, and home trends without new data interruption at this time.

Although a shortage of fresh economic data will have trading ranges within, it will leave the market all the more susceptible to unexpected news stories or geopolitics. Changes within narrative environments that are lacking data—like central bank commentary, trade negotiations, or company earnings estimate revisions—may make disproportionate impacts upon flow as well as sentiment.

Zaye Capital Markets is cautioning clients to be careful. Analysts may well use this interval day to reassess portfolio positions before bigger releases later this week that will feature most significantly inflation, manufacturing, and consumer demand data. On dull days such as this one, rhythm will be influenced as much by positioning as by fundaments—potentially creating a recipe for either technical drifts or swift responses to unexpected catalysts.

STOCK MARKET PERFORMANC

Indexes Rebound from One-Month Bottoms but Weak Breadth Metrics Maintain Precaution Signal

Zaye Capital Markets maintains uneven US equity index rally under review as markets recover from lows of April 8th. High-level index advance is a story of a rally, but steeper drawsdowns and constituent average decline reflect underlying vulnerability. Selectivity still prevades and sector-level volatilities serve as a reminder that tactical allocations are still required.

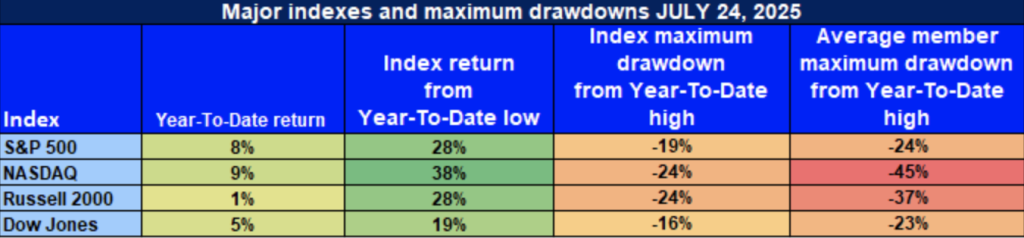

S&P 500: Resilience Led by Large-Cap Leaders

YTD: +8% | -28% below April low | -19% below YTD high | Ave. member: -24%

S&P 500 rose by 8% year to date with clean rises by larger names along with 28% rally from the april low trough. 19% decline from its peak and 24% decline by avg member are indicative of still-conservative mkts that still look to a select few leaders to sustain themselves, and breadth to confirm this resilience

NASDAQ: Outperformance Masks Structural Weakness

YTD: +9% | -38% lower than April low | -24% lower than YTD high | Avg. member: -45%

NASDAQ’s 9% y-t-d gain and 38% retreat from its April bottom is a robust picture. Nonetheless, the tech-laded index is still 24% shy of its top and brilliant -45% avg member loss obfuscates underlying nervousness, specifically within high-beta and spec names.

Russell 2000: Small-Caps Show Strength, But Remain Fragile

YTD: +1% | +28% below April low | -24% below YTD high | Avg. member: -37% In spite of a robust 28% rally from April lows, the Russell 2000 is still not higher YTD. Such poor YTD performance along with 24% peak-to-trough index loss and 37% average drawdown informs us that sentiment in small-caps is still guarded under squeezing pressures.

Dow Jones: Defensive Character Dominates Volatility

YTD: +5% | -19% below April low | -16% below YTD high | Average member: -23% Dow’s 5% gain and 19% advance since April are keeping pace behind those experienced, defensive members. The subgroup -16% drawdown best leaves the index as a buffer—albeit with 23% median-member loss still divulging underlying macro risk.

We at Zaye Capital Markets continue to look for risk-adjusted returns. The strategy favors high-quality cash-generating businesses and pays close attention to breadth within the market as the ultimate predictor of continued equity superiority.

STRONGEST SECTOR OF ALL THESE INDICES

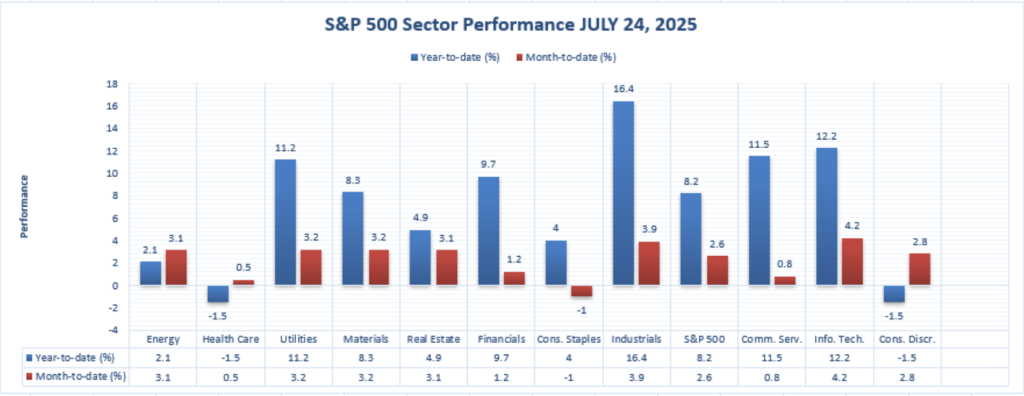

Industrials Head the Top Rankings with Good YTD and MTD Gains

We continue to monitor sector leadership at Zaye Capital Markets to pick up momentum ideas within equity markets. Up to July 24, 2025, industrials have been the best-performing sector of the S&P 500 year-to-date as well as month-to-date, with robust investor demand for economically sensitive, productivity-related stocks due to the U.S. manufacturing renaissance as well as the infrastructure spending tailwind.

Industrials: Peak Performance Across Timeframes

YTD: +16.4% | MTD: +3.9% Industrials has produced a top 16.4% year-to-date record this year—well in excess of the wider S&P 500’s 8.2% advance. The performance is underpinned by a robust 3.9% month-to-date advance that speaks of continued fund inflows and robust profit trends at subsectors as diverse as machinery, transport, and aerospace. The trend is part of a trend to do more reshoring, automation, and infrastructure themes that are increasingly hotter within this present macro environment.

Standouts identified to include data tech (up 12.2% YTD, 4.2% MTD) and communications services (up 11.5% YTD), however, with respective month-to-date returns trailing industrials. Conversely, consumer discretionary and healthcare sectors fell YTD by -1.5%, indicating divergent investor sentiment.

We still prefer industrials at Zaye Capital Markets due to pricing power, book strength, as well as continued adherence to long-term policy-led growth trends. Analysts are thus advised to watch out for trends within capital expenditures as well as supply chain data to justify further sector outperformance by Q3.

EARNINGS

Earnings Summary – Jul 25, 2025

- HCA Healthcare, Inc.

On July 25, HCA Healthcare reported solid second-quarter earnings, producing an adjusted EPS of $6.84—well above consensus. The company handily topped Wall Street expectations by 6.4% year-over-year sales growth to $18.61 billion, as HCA increased full-year EPS and sales expectations. The quarter took comfort in increased volumes in elective procedures and solid emergency room volume, an extension of stabilizing demand across core hospital lines of service. In our opinion at Zaye Capital Markets, the future is one of stable operating platform, pricing stickiness, and stable free cash flow, for HCA to be a defensive name among a volatile healthcare sector.

- Aon plc

Aon also impressed with a strong Q2, delivering adjusted EPS of $3.49, up 19% year-on-year. Revenues were over 10%, with organically contributed growth of around some 6%. Free cash flow rose by almost 60%, providing capital allocation flexibility to support M&A as well as shareholder returns. Margin improvement and tight cost control also helped support profitability. We regard such performances as reflective of broad client demand for fully integrated consulting and risk capability provided by Aon, particularly as corporate clients position to address rising geopolitical as well as financial uncertainty.

- Charter Communications, Inc.

Charter Communications underperformed, Q2 EPS coming in at $9.18, below consensus. Revenue at $13.77 billion largely met expectations but investor sentiment was given a boost by worse-than-expected subscriber loss, with 117,000 broadband customers dropping off versus 70,000 predicted. Mobile subscriptions rose but failed to offset net service loss. Here at Zaye Capital Markets, we see investor concern over loss of videos, decelerating momentum for broadband, and threat of merger integration despite ongoing rumor mill spec about mergers. The sell-off is simply a reflection of this sector being highly sensitive to trends in subscribers.

Earnings Preview – July 28, 2025

- Welltower Inc.

Welltower is reporting Q2 today, and investor interest will center solely on measures of FFO, occupancy, and same-property NOI performance. With tailwind demographics for senior care and outpatient services, all attention is on growth to persist. Sensitivity to interest rates and pressure on operating costs remain a area of concern. We advise maintaining attention on forward guidance for asset rotation, rent collection rates, and forward guidance in navigating healthcare real estate headwinds.

- Waste Management Inc.

Waste Management posts in turn, with the consensus expecting EPS of about $1.90 on revenue of $6.3 billion. Margin resilience, labor costs, and the performance of its recycling division in a commodity pricing climate that is very much uncertain are our key areas of interest at Zaye Capital Markets. Whether or not the company is successful in handling inflationary shocks short of pulling the plug is the sentiment make-or-break.

- Cadence Design Systems, Inc.

Cadence will have a decent quarter, with Wall Street expecting EPS of just above $1.56 and just shy of $1.25 billion sales. Ongoing growth within its AI-related design solutions and exploding hyperscale and auto chip design opportunity will continue to be select Catalysts. Future guidance and management commentary around semicap cycle later this year will be scrutinized by investors. We view Cadence as one of best gauges of digital design infrastructure of an AI-fied future.

- Southern Copper Corporation

As Southern Copper will release shortly, there isn’t a separate earnings release scheduled for July 28. The releases regarding its dividend policy—with 62.9% just increased to $1.01 per share—through to levels of production and inflation of costs will be something investors will be looking to see releases from. In our line of vision, copper price movement as well as political risk within Latin American provinces of extractive industries remains a linchpin to its path of valuation.

Stock Market Summary – Monday, July 28, 2025

Markets conveyed muted optimism to begin the week, balancing weak economic data with new geopolitical concerns. Persistent softness in terms of trade policy, potential Fed rate moves, and muted consumer spending has maintained equities on an unstable foundation. With only a couple of trading sessions remaining before the end of July, focus shifts to earnings from companies and how potential economic data for the remainder of this week may influence monetary policy projections up through Q3.

Stock Price

Geopolitical Trends and Economic Indicators

CNBC writes that lower-than-projected US consumer sentiment and weakened homebuilding activity fanned speculations that the Federal Reserve will turn dovish at monetary policy meetings this month. President Trump renewed his threat to renegotiate trading pacts with Europe and Canada, saying he will slap tariffs unless for negotiations—applying geopolitical tension to already volatile global markets. The developments are making investors gradually shift to defensive stocks.

Stock News: The Top Most Important Trends at Start of Earnings Season

As we move closer to earnings season, there are several prominent stocks that are displaying clean-line price actions within technical ranges. There is a sunny trend that has taken place within mega-caps like NVIDIA ($NVDA), Amazon ($AMZN), Alphabet ($GOOGL), Microsoft ($MSFT), Meta ($META), and semiconductor blue chips like Broadcom ($AVGO), TSMC ($TSM), and AMD ($AMD). Speculative stocks like Palantir ($PLTR), Oklo ($OKLO), Rocket Lab ($RKLB), and IonQ ($IONQ) are displaying decent upswing potential as well.

In the blended world, Tesla ($TSLA) continues to be volatile with no directional tilt as earnings and shipment metrics struggle with macro headwinds. On the flipside, Oscar Health ($OSCR) looks structurally damaged, trading around a bearish trend, perhaps indicative of softness in the insurtech world. We will continue to monitor those names with an eye to observe confirmation signals with regards to earnings momentum as well as to macro sensibility.

S&P 500 and The Magnificent Seven

S&p 500 remains soft as the “Magnificent Seven”—Nvidia, Apple, Microsoft, Amazon, Meta, Alphabet, and Tesla—take brutal drawdowns. Financial Twitter sentiment is such that all those tech giants are all out of steam as there are valuation corrections as well as spotty Q2 earnings. Nvidia and Tesla are seeing profit-takin as there is a spectacular first-half performance, while Apple and Amazon are reeling under regulatory problems as well as demand issues.

This selective leadership in performance persists in testing the mettle of wider S&P rally, with defensives and industrials now displaying relative strength.

Major Index Performance as of 28 Jul 2025

- S&P 500: At 5,899.42, down 0.4% during the day.

- Nasdaq Composite: At 18,131.70, lower by 0.6% as tech

- Dow Jones Industrial Average: 40,290.35, no change, up 0.3% as industrials gain

- Russell 2000: 2,086.90, -0.2% as the small-caps can’t get into gear.

Our approach at Zaye Capital Markets still involves focused risk-managed exposures to earnings-driven winners and considered attention to macroeconomic levers to inform strategic deployments.

Gold Price – Monday, 28 Jul 2025

Gold today is at $3,336.48 per ounce, decreasing a modest 0.02% from yesterday. With no notable economics on tap today, overall macro conditions remain tight, spurred by a string of presidential comments from President Trump. His denunciations of China and Japan’s currency devaluations, threats of standalone tariffs against Canada, and hardline posturing against Hamas and Europe have reignited geopolitical risk premiums. Trump’s assertion that a weaker dollar is good for US exports and the effectiveness of tariffs re-affirms inflationary expectations that have long supported gold’s applications as a hedge. With no new macro signals, however, activity today is net technical and sentiment-driven, devoid of a macro trigger.

In general, yesterday’s economic releases—aside from earnings—are registering softness within consumer sentiment and equity swings that have been backing gold’s defensive position. Although healthcare and industrial earnings surpassed forecasts on the good side, underlying softness within small-caps and declining major index breadth indicate investors are seeking cover sotto voce. Here at Zaye Capital Markets, we’re still monitoring Treasury yields, central bank rhetoric, and geopolitical conjecture to gauge near-term inclination. Gold is well positioned with this backdrop of uncertain trade negotiations, currency swings, and subdued retail sentiment.

Oil Prices – Monday, July 28, 2025

Brent started higher today at $68.66 with WTI at $65.38, supported by new hopes of a US–EU trade agreement and nascent détente between Washington and Beijing. The market took this diplomatic thaw to be a reflection of global demand steadying positively but gains to the upside are limited by OPEC+ intentions to add volume by a further 548,000 barrels per day in August and risk-sensitive demand growth forecasts by OPEC and IEA to 2025 at 1.29 mb/d and 0.7 mb/d, respectively. Yesterday’s US economic statistics of weak consumer sentiment and weak US home trends again stoked fears of softness at home demand, preserving a modestly defensive feel to crude markets. Such conditions along with modest supply-side adjustments are keeping oil within a narrow trading range.

President Trump’s series of remarks—deploring strong-dollar policy, praising tariff success under a devalued dollar, and threatening unilateral Canada tariffs—has contributed further FX and inflation uncertainty to the energy sector. His geopolitical remarks to do with Hamas and U.S.–Middle East policy also generated risk appetite, making oil that much more attractive as a geopolitical hedge. Traders do not have significant economic releases with which tograpple today, so are looking to future releases of inventories, OPEC+ policy decisions, as well as geopolitical rumor mill for direction. According to our opinion at Zaye Capital Markets, prices of oil swing between hazardous demand forecasts and switches-of-direction trade volatililty, and all such supply breakdowns or US tariff policy rises will trigger sharper volatilty.

Bitcoin Prices – Monday, 28 Jul 2025

BTC is at $119,635 currently, a good recovery from a volatile week where the asset had fallen 2.9% at one point as part of sectoral liquidations worth more than $967 million. The surprising sell-off by a dominant whale unloading $9 billion of BTC on July 26 that took Bitcoin realisation cap to above this $1 trillion mark had raised eyebrows but BTC recovered due to new sentiment around spot ETF demand as well as institution inflows that could take prices to around $130K–$175K—assuming this giant $110K–$112K support base holds its line. Recent purchases like those by VOLUMN INC that purchased 3,183 BTC at ~$117,697 on avg continue to show institution confidence despite rising near-term volatilty.

Weekend comments by President Trump further stokes macro uncertainty, highlighting Bitcoin’s appeal as a decentralised hedge. Following suggestions of a weak dollar to offset tariff efficiency and remarks regarding trade frictions with Canada, Japan, and China are seen by markets as a reminder of currency volatility and inflation risk—both underlying Bitcoin’s broader narrative. Soft consumer sentiment and soft-housing data yesterday again highlight economic vulnerability, keeping risk-on demand under rein but still intact. With no significant economic data later today, Bitcoin’s price is sentiment-determined, and at Zaye Capital Markets, we continue to watch with great care for approval of the ETF, whale trend directional change, and crypto-adjacent regulatory change that could act as a catalyst for, or place further upside to seek, within ensuing sessions.

ETH Prices – Monday, 28 Jul 2025

Ethereum (ETH) stands at $3,849.69, recording a 2.3% day increase as institutional buying increases. Spot Ethereum ETFs experienced phenomenal inflows with total inflows recording more than $1.85 billion up to July 25, as this trumped Bitcoin’s ETF inflows. BlackRock’s ETHA ETF recorded one day’s inflows of $440 million as 30-day ETH ETF inflows elevated to over $4.4 billion. Institutional buying is supported by on-chain whale buying as more than 1.13 million BTC—worth about $4.18 billion—entered exchanges over the last two weeks. Future ether staking rewards were obviously appealing to 30,366 eclsvc (about $114 million) bought by one whale wallet, according to on-chain data, as part of a high-conviction wager in volatile markets and increasing staking rewards.

Macro-wise, Trump threatenings of a weak dollar, steeper tariffs, and rising geopolitical tensions have provided tailwind to the Ethereum narrative as a decentralised hedge. Such threatenings heighten fiat risk fear and augment demand for programmable assets such as ETH. Yesterday softer than expected U.S. consumer and housing data also bear witness to a defensive economic background, but sophisticated and institutionally-minded money inflows to ETH are unshakeable. With rising demand for application uses that are based upon utility, supportive ETF momentum, and increasing regulatory clarity, Ethereum is making its move from speculative to fundamental infrastructure. In Zaye Capital Markets, we see ETH to continue to press up at resistance levels at $3,800 with momentum to continue to gain steam to the $4,000 mark should ETF inflows and corporate adoption maintain current trajectory.