Where Are Markets Today?

Both European stock futures and U.S. stock futures are poised to recover on Monday, recovering from the deep losses of last week. S&P 500 futures rose 0.41%, Nasdaq 100 futures rose 0.44%, and Dow Jones futures rose 153 points, or 0.35%. It follows a tumultuous week of trading that saw all three major U.S benchmarks close the week with deep losses, breaking weeks of broadly upbeat action on the broader market. Last week’s dramatic decline was mainly spearheaded by a weak July jobs report that was worse than expected, along with fresh tariffs imposed on some of the major trade partners by President Trump, which fueled inflationary pressures as well as a deceleration of the economy.

The optimistic rally in futures is primarily a result of two things: expectations of potential Federal Reserve rate cuts as well as “buy the dip” thinking from investors. After the weak U.S. jobs data, capital markets have now priced up augmented probabilities of a rate cut later in the month of September, as there are some pundits guessing as much as 100 basis points of cuts over the year. Change of expectations has provided some comfort to equity futures around the world, as that implies relaxing money conditions. The U.S. dollar had dived on the weak job data, but stabilized somewhat, supporting the positive futures action. However, market confidence is still guarded, pending, as investors doubt the credibility of American economic policy. The sudden removal of the Labor Statistics Chief by President Trump, coupled with threats to blow up the Federal Reserve and request imminent rate cuts, has questioned independence of American monetary policy. Trump’s imminent naming of a Federal Reserve Board member has, yet again, questioned political interference on upcoming Fed policies. These questions are generating a confused mood, as investors still doubt the spillover influence of Trump’s economic policy.

Even in Europe, stock futures are showing positive gains, in line with this pattern of cautious optimism. Euro Stoxx 50 futures rose 0.50%, DAX futures rose 0.35%, and CAC futures rose 0.63%. It is a turnaround of a challenging phase in European bourses, when investor sentiment had been dampened by global uncertainties. The weak U.S. jobs report as well as the simmering crisis over President Trump’s tariff policy has raised caution over the economic turnaround across the world. Despite such headwinds, there is the “buy the dip” psychology supporting European futures registering a modest turnaround. With investors remaining cautious over threats to the global economic environment, economic data as well as geopolitical events on the horizon are of keen interest to them to gauge future market momentum.

Major Index Performance as of August 4, 2025

- Nasdaq Composite (QQQ): 20,650.13 (-2.24%)

- S&P 500 (SPY): 6,287.28 (-0.82%)

- Dow Jones Industrial Average (DIA): 43,781.77 (-1.30%)

- Russell 2000 (IWM): 2,166.78 (-2.03%)

The Magnificent Seven and the S&P 500

The “Magnificent Seven” of Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla are softening. A recent sector split places the group averaging more than an 18% correction from recent highs, with Meta and Tesla leading the way lower. That bodes well, of course, for a valuation de-risking, particularly for AI-growth narratives that have gotten unhitched from fundamentals. The S&P 500 still hangs around as tech leadership falters. As nice as energy and industrials are providing some relief, the gauge isn’t going rally on a lasting basis without the return of the participation of its mega-cap core engines.

Drivers Behind the Market Move

Global equity markets are showing signs of recovery today, rebounding from last week’s significant losses. S&P 500 futures rose by 0.41%, Nasdaq 100 futures gained 0.44%, and Dow Jones futures added 153 points, or 0.35%. Similarly, European futures are also experiencing positive movement, reflecting a modest rebound after prior losses. This uptick is attributed to expectations of Federal Reserve rate cuts and a “buy the dip” sentiment among investors. However, market confidence remains cautious due to concerns about the credibility of U.S. economic policy, especially after President Trump’s dismissal of the Labor Statistics Chief and his upcoming appointment to the Federal Reserve Board, which is seen as potentially politicizing monetary policy.

Key Drivers Influencing Today’s Market Movements:

- Anticipation of Federal Reserve Rate Cuts:

Following the weaker-than-expected U.S. jobs report, markets are now pricing in an increased likelihood of Federal Reserve rate cuts, with some analysts forecasting reductions of up to 100 basis points over the course of the year. The disappointing jobs data has led to concerns about labor market weakness and slower economic growth, prompting traders to anticipate that the Fed may need to take more accommodative measures to sustain the recovery. This shift in market expectations has supported equity futures globally, providing some relief to stock prices that were under pressure in the previous week. Additionally, the U.S. dollar, which had been under significant pressure following the job report, has seen some stabilization as investors adjust their expectations of future monetary policy.

- Concerns Over U.S. Economic Policy Credibility:

President Trump’s recent actions have raised significant concerns about the credibility of U.S. economic policy, particularly with his dismissal of the Labor Statistics Chief, which he claimed was due to “manipulated” jobs data. This move has cast doubts on the independence of economic data reporting and added to fears that the administration may further politicize key institutions, including the Federal Reserve. Trump’s upcoming appointment of a new Federal Reserve Board member and his continued influence over monetary policy are fueling concerns that future data releases may be subject to political pressure, potentially undermining the credibility of economic reports. These actions have added uncertainty to the markets, as investors are now questioning whether the Fed will remain independent in its policy decisions. If investors perceive that the Federal Reserve is becoming increasingly politicized, it could lead to volatility in financial markets, particularly if there are shifts in interest rate policy that are perceived to be politically motivated rather than data-driven.

- Global Trade Tensions and Tariff Implications:

The Trump administration’s latest round of tariffs, including a significant 39% tariff on Swiss imports, has heightened worries about rising inflation and potential disruptions to global trade. These new tariffs, which target a broad array of U.S. trading partners, are adding pressure to already strained supply chains and fueling fears of an economic slowdown. As the U.S. pushes forward with its tariff strategy, concerns are mounting about retaliatory measures from other nations, which could lead to further trade conflicts. The market’s reaction has been swift, with European stocks experiencing their biggest daily drop since April 2025 as news of the tariffs spread. Investors are increasingly concerned that the escalating trade tensions will lead to higher inflation, which could force the Federal Reserve to raise interest rates more aggressively, thereby stifling economic growth. Additionally, prolonged trade disruptions could exacerbate global supply chain issues, leading to higher costs for businesses and consumers.

In summary, while markets are showing signs of recovery today, investor sentiment remains fragile due to concerns about U.S. economic policy and global trade tensions. The anticipation of Federal Reserve rate cuts provides some support to equities, but uncertainties about the credibility of economic data and the potential politicization of monetary policy continue to weigh on market confidence. Investors will be closely monitoring these developments in the coming days to gauge the direction of the markets.

Handling Economic Data:

The TRUMP Tweets and Its Implications

President Trump’s recent statements, as well as actions, have also drawn unprecedented volatility throughout the entire financial markets as well as the entire economy. President Trump shocked the nation on August 1, 2025, by firing the Labor Statistics Chief for “manipulated” employment figures, something that undermined the credibility of economic data when confidence in the market had already hit its bottom. The president’s warning of unspecified across-the-board new tariffs as much as 41% on large trading partners, such as India as well as Canada, has added another level of unpredictability, something that has fueled fears of retaliation as well as ongoing interference of the flow of commerce. These statements, as well as actions, suggest that Trump’s combative rhetoric on commerce, as well as that tariffs are going to remain center stage for his economic policy, despite challenges that surround on the international economic horizon.

Trump’s policy and rhetoric of taking the route of tariffs, along with Federal Reserve policy shifts, are changing market expectations. While he is going Fed-bashing, and also asking for rate cuts beforehand, hopes for the central bank going dovish within the next few months are ignited. With the Fed Governor’s resignation leaving Trump with the ability to dictate monetary policy, investors now search for hints of Fed change. If Trump manages to institute lower rates, it will seem benign to equities, but might put bearish pressures on the U.S. dollar. It, however, creates concern over the longer-term effect on inflation, as well as the state of the financial market, with analysts debating whether the move would help or hurt the economy. Additionally, the White House announcement of disbursal of tariff receipts to middle-class Americans obscures Trump’s attempt at framing tariffs as a means of bringing the federal deficit down as well as funding domestic spends. The policy, however, awaits challenge from affected industries as well as trading nations abroad. Geopolitical undertones involving nations like China as well as Russia, for that matter, have only heightened the international trade environment. Aggressiveness by Trump on foreign policy as well as on commerce has remained a primary market sentiment influence. Market participants remain skeptical on the capacity of registering future disruptions, particularly on energy exchanges as well as on technology, which should expect increased regulation pressures as part of the wake of his policies.

Overall, Trump’s latest rhetoric as well as policies are kindling an extremely precarious economic as well as political environment. Market effects in real terms over the near term are clear—increase tariffs at the cost of raising prices to industry as well as consumers, another depreciation of the dollar would be favorable to gold as well as soft commodities. Trump’s impact on the Federal Reserve as well as his current state of trade war has long-term effects, perhaps restructuring the economic system of the globe. Investors must remain on heightened alert, keeping extremely close watch on such moves as they may affect conditions on the markets over the months to come.

Leadership in the Healthcare Industry and Long-Term Trends

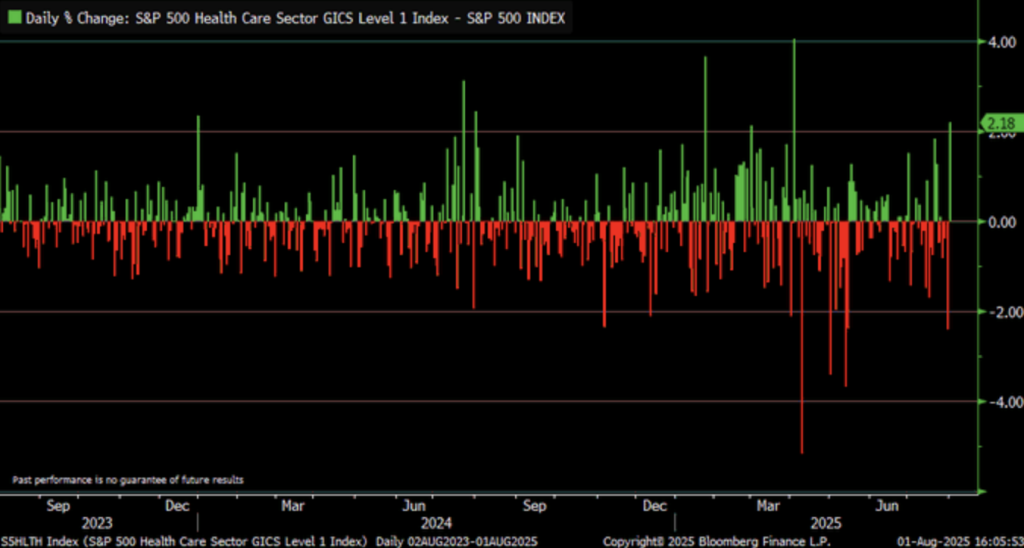

S&P 500 Health Care Sector GICS Index recorded dazzling performance on August 1, 2025, as it outstripped the diversified S&P 500 as the latter recorded its largest one-day gain since April 2024. This gain was largely fueled by the continued rebound of post-pandemic medical demand. Nevertheless, even as the one-off explosion is evidence of the near-term news of innovation or policy rehaul, the analysts need to maintain watchful eyes on the longer-term trend of this performance, as calibrated by the predictions of a 10-12% CAGR of personal care services to 2028, as fueled largely by the continued growth of the home health industry.

Despite the positive short-term trend, historic volatility is a crucial factor in the future of this industry. This sudden drop in the earlier part of 2025, along with prior regulatory impacts like the negotiated drug prices in the Inflation Reduction Act, is indicative of the industry’s susceptibility to policy-induced volatility. Such regulatory advancements continue to fuel investor optimism as well as doubt, shaping the stock price’s stability, and make healthcare shares extremely volatile.

Looking at these dynamics, AbbVie (ABBV) might be referred to as undervalued in the healthcare space, particularly given that regulatory news-driven market responses have likely been skewed towards short-term negativity. Investors must watch the way the stock has been acting versus peers in the industry and closely monitor the policy announcements up ahead, which can provide hints as to long-term growth opportunities. Investors must also track McKinsey’s home health trends and how they can influence healthcare stock valuations.

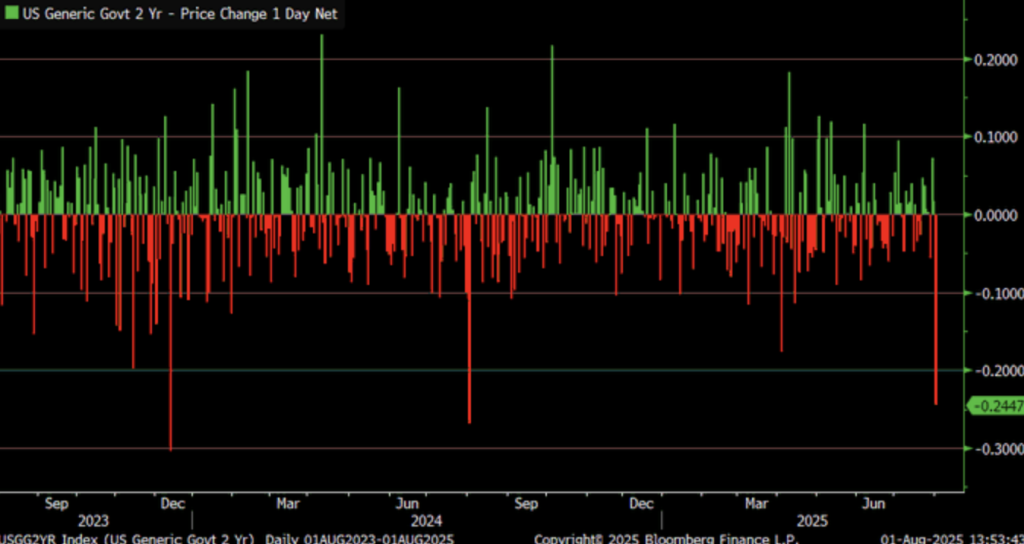

Yield Fall in 2-Year Treasury Suggests Potential Shift in Fed Policy

Aug. 1, 2025, was the last time the 2-Year U.S. Treasury yield declined the most since Aug. 2024, which can herald the prospect of the immediate monetary policy reversal of the Federal Reserve. Such steep falls in the past suggest volatility in the yield is typically occurring before the direction of the interest rates reverses. With the investor clinging to the prospect of the potential reversal by the Fed in lowering rates in the hope of boosting the economy, the fall can be the harbinger of monetary easing hopes due to softening inflation or growth, as was the case in one 2023 Federal Reserve research piece (FEDS Notes).

Yield swings of this type in the past have been harbingers of sizeable turning points in the economy. Such patterns were observed before the 2008 financial crisis as well as in the wake of the 2020 pandemic, in which bond yield surprises were foretelling increased concern about the economy’s health. Better recent GDP news aside, the yield reversal goes against the narrative of healthy rebound in the economy, this time suggesting further deteriorating issues for the psyche of decision-makers.

This comes against the backdrop of the yield curve still being in inversion, as the next moves of the Fed become clearer, the analysts need to wait for the next statement of the Fed for clues on policy decisions that can buttress or detract from the narrative that the economy remains strong.

Extended Unemployment Implies Possible Labor Market Exposure

July 2025 marked the United States witnessing a sudden rise in long-term unemployment (inactive for longer than 27 weeks), rates last seen in early 2022. This contrasts with the storyline of the healthy labor market as well as is of concern for pre-existing vulnerabilities. Long-term unemployment, as viewed from prior chart data issued by the Bureau of Labor Statistics (BLS), has fluctuated reliably between 15-40% of the total in the unemployment since the year 2000, as the recent rises present concern for labor market scarring. This can indicate structural movements in the economy are holding back recovery for jobs for most workers.

Evidence, including the 2021 Journal of Labor Economics report by Autor et al., links chronic unemployment with reduced future employment opportunities. Prolonged unemployment can be part of the explanation for why aggregate labor market mobility is in decline, and it can postpone the reversal of the decline in flagging industries. It’s an indication that the economy will be experiencing some long-term difficulties even when there is short-run job growth.

Meanwhile, Treasury receipts are constant, in spite of this rising jobsless trend, supporting the doubt concerning the real health of the jobs market. Economists question whether tax reform or increased government transfers is maintaining the steadiness of the economy, instead of recovery itself. Fiscal indicators of the U.S. Treasury’s Daily Treasury Statement reveal extended borrowing dependence, which hints toward potential fiscal imbalances even with weak job growth.

ISM Manufacturing Index Confirms Ongoing Industry Weakness

July 2025 dropping of the ISM Manufacturing Index to 48, sub-50 and indicative of contraction, is evidence of the longstanding vulnerabilities of U.S. manufacturing, of the endurance of the 19-month trend of industry softness in the month of May 2024, and the indication that the resulting problems have structural roots, as distinct from the familiar pattern of cyclical softness. Reading is the worrisome context of the longstanding stagnation in the manufacturing sector, which can foretell the possibility of difficulties of systemic character, as distinct from necessarily correctable in the short term in the form of policy.

Whereas new orders rose moderately to 47.1, industry employment dropped to 43.4, showing the gap between low demand and further redundancies. This comes after the end of a 2023 study by the National Bureau of Economic Research that attributed a low level of Purchasing Managers’ Index (PMI) during prolonged periods of industry decline to labor market slack. This gap is also in line with manufacturers facing difficulties in adjustment to unstable circumstances in the economy.

Issued in the face of continued controversy surrounding President Trump’s 2025 economic policies, this information contradicts current market optimism. Resistance to policy, as with the 1784 Joseph II economic reforms, has historically disrupted or even incapacitated economic agendas, potentially creating further turbulence. As these concerns remain, analysts must keep a close eye on subsequent PMI releases as well as policy reforms, as these can signal whether or not the manufacturing economy is moving toward further underperformance.

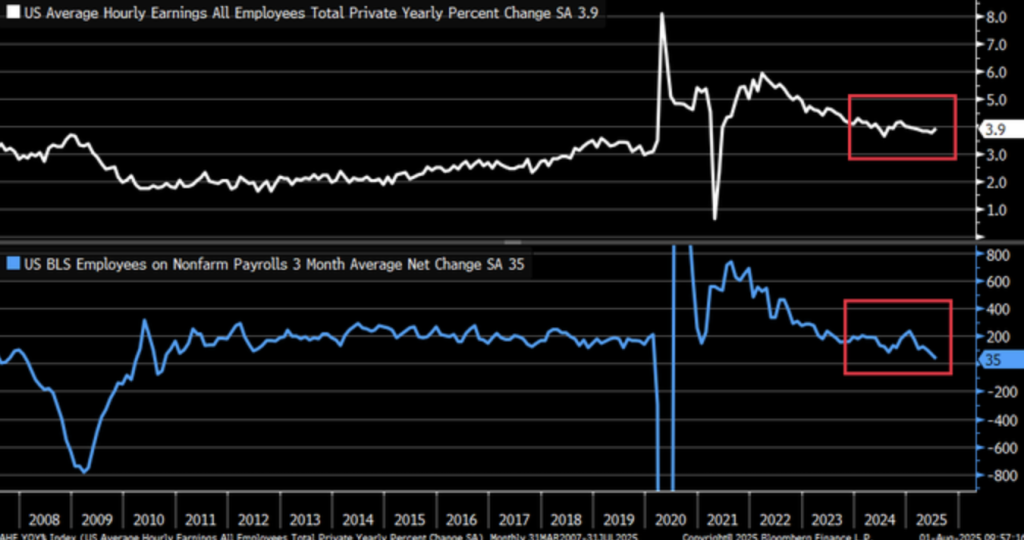

Wage Growth Rebounds Amid Declining Payrolls, Raising Stagflation Concerns

US wage growth is coming back in good form, rising to 3.9% per annum in July 2025, as per Bureau of Labor Statistics (BLS) figures. Such growth is, however, being contrasted against a steep fall in nonfarm jobs growth to just 73,000 new jobs in July. Such a divergence is reflective of underlying weakening in the labor market, with inflationary pressures still prevalent in terms of affecting wage activity. This is a trend that defies the universal assumption of it being a robust post-virus growth and puts the entire US economy in question, too.

National Bureau of Economic Research (2024) analysis, in fact, indicates evidence of continued wage increases without corresponding job growth as a sign of an approaching stagflation, a macroeconomic phenomenon witnessed in the past during the 1970s, wherein there is persistent wage inflation despite stagnant growth in hiring. Persistent wage inflation, while job creation is flat, is a sign of anemic economic foundations wherein living standards increase but employment opportunities lag, leading to decelerated economic growth.

This pattern has echoes from post-2008 financial crisis historical patterns, where payroll softness had signaled more acute post-crisis recessions. In a 2019 Federal Reserve report, caution had been expressed against reading too much strength in wage growth as a signal of healthy economy, as it might just be a sign of economy overheating. Analysts need to remain cautious, observing follow-on labor market releases and inflation patterns to see if dangers from stagflation are going to escalate in the next few months.

Dollar Index’s Fall Reflected the Possible Macroeconomic Shift

On 1 August 2025, the Dollar Index (DXY) dropped by 1.27% to 98.6941, recording the sharp fall after rising 1.98% in the last month. This pattern, as the tradingeconomics.com data indicate, shows likely macroeconomic alterations of long-term impact on the United States’ economic leadership. The DXY is the measure of the U.S. currency against the basket of other currencies, and the recent fall can be a sign of dwindling investor confidence, most probably triggered by rising U.S. debt, which surpassed the $35 trillion limit in mid-2025 as per the Treasury news.

Tends in the past, for example, depreciation of 4.38% in the last year in the DXY, Signal Wider Loss of U.S. Leadership in the Global Arena. Such depreciation would suggest the global reorientation of currencies, whereby rising debt and fiscal imbalances can undermine the dollar’s edge. With inflationary stresses existing already, economists must take particular care in noting the potential of further softness in the dollar fueling these tendencies.

Economic theory, à la the 2021 Federal Reserve study on exchange rates, suggests that the weakening dollar can drive up the cost of import, potentially fueling inflation. The strength, of course, depends upon the post-pandemic resilience of foreign supply chains, but likewise, the increased cost of import can pinch U.S. consumers and businesses, too. Under such circumstances, analysts need to be extraordinarily sensitive to the way currency markets and inflation expectations move in order to measure the effect of the general economy.

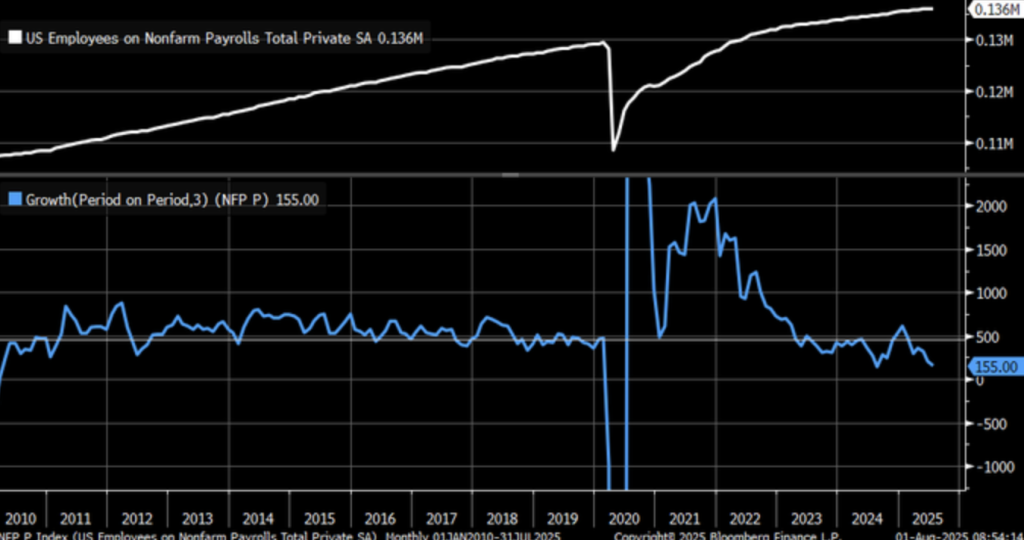

Employment Upturn Remains in Doubt with Tariff Unpredictability

United States private payrolls has been highly volatile, plummeting drastically before rising during the recovery cycle. New data shows the three-month rise of 155,000 jobs, near the August 2024 low, in Bureau of Labor Statistics data. Nevertheless, the disastrous fall in April 2025 to as low as 62,000 new private jobs, well below estimate of 120,000, is bad news for structural weaknesses in the jobs markets. This disastrous fall defies the story of perennial jobs growth, particular in the context of uncertainty about tariffs as well as in the context of policy tilts towards the economy.

Current economic studies by the National Bureau of Economic Research have put more emphasis on nonfarm payroll figures as a reliable indicator of economic performance, since they represent around 80% of workers who contribute to GDP. Correction of payroll figures, such as the 258,000 jobs that have been subtracted in the estimates for May-June 2025, mean one should be careful in understanding short-term employment growth figures. Payroll figure corrections point to the susceptibility of current labor market prospects, which bars one from forecasting sustainable recovery with certainty.

The impact of tariffs, or at least as trade policy evolves, remains a core driver of labors markets dynamics. Fear of negotiations of tariffs along with the subsequent economy implications may also complicate private payroll expansion. Investors must keep a very close eye on developments in U.S. trade policy, at least as the tariffs impact the manufacturing and the services industries, as this can cause additional, albeit greater, movements in job expansion in these coming months.

Wages Increase as Labor Creation Stabilizes

U.S. average hour earnings growth surged to 3.9% year-year in July of 2025, a large pickup from recent trends. Gains were most likely evidencing the flip-flop in the labor market, in particular as the global economy is uncertain. Nevertheless, the advance in wages is at variance with the soft nonfarm payroll growth of only 73,000 jobs and further elevates the risk of the advance in wages taking the lead against employment creation. Evidence of accelerating hours worked at the job as possibly facilitating this trend, against monumental increases in employment, as explained in narrative of this trend.

Although the nominal rise in wages is historic, the real weekly full-time wages had been trailing inflation since 2020, as per the Federal Reserve Bank of St. Louis (FRED). This also means the new rise in wages of 3.9% in nominal terms is also going to fail to advantage the workers in the realm of higher spending capacity, since the increment in earnings is going towards feeding inflation. This discrepancy is one of the strongest and ignored factors in the mainstream economics media, and it deserves the careful consideration of the real impact of rises in wages in improving the standard of living.

Among these tendencies, global pay trend indicators indicate that the U.S. is not the only economy with inflation-adjusted pay freezes. Economists must proceed to keep watch over the pay growth, inflation, and pay rate relationship in order to see the bigger picture of the health of the jobs market. Analysts must qualify the interpretation of the pay growth as proof of the recovery of the real economy without the broader context of the inflationary issues alongside the erosion of purchasing power of the employees.

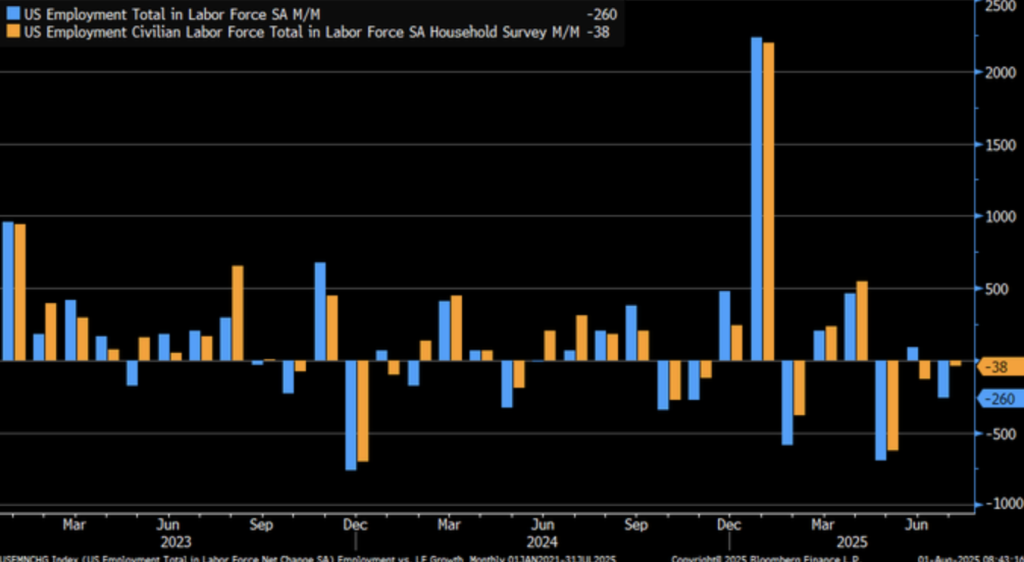

Reduction in the Labor Force During Economic Turmoil and Trade Policy Shocks

The July 2025 U.S. labor report shows a less severe downturn in the labor force, as shown by the orange bars of the chart, though employment, shown by the blue bars, fell emphatically. Fewer than 73,000 jobs were created, much below the projected 110,000, and the 258,000 downward revision in jobs for May and June only increases alarm for the soft nature of the labor markets. The soft employment report in January is a warning sign for the labor force in relation to aggregate labor participation’s steady decline.

This jobs slowdown is in line with broader macroeconomic tendencies, including the 3% Q2 2025 GDP growth as a consequence of the sudden fall in imports largely due to President Trump’s tariffs. Reshuffling the trade pattern the way the GDP growth was boosted but perhaps at the expense of jobs in import-based industries was this shift, the extent of trade policy’s impact upon the labor component, with potential for long-term implications in employment rates as well as industry performance.

The context of the post is also rendered more complicated by the outrage over the August 1, 2025, firing of BLS Commissioner Erika McEntarfer by President Trump on the basis of supposedly fraudulent data manipulation. Economists such as former BLS Commissioner William Beach have attacked the move as undermining statistical integrity, even as no evidence of data manipulation has been discovered after following peer-reviewed statistical procedures. The outrage has the potential to create fear about the transparency and accuracy of labor market data, which can, in turn, influence market sentiment as well as policy-making in the months ahead.

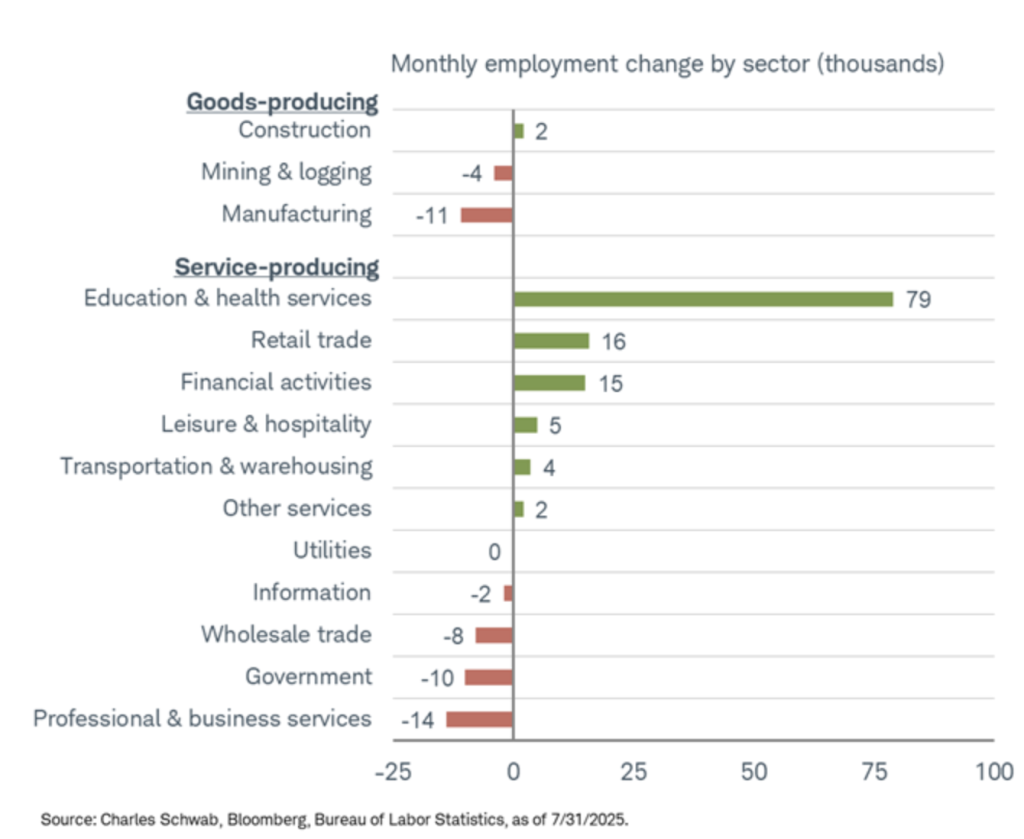

U.S. Shift to Services with Manufacturing Slowdown

July 2025 U.S. jobs report reiterates the same dualism: the colossal 79,000-job increase in the health and educational services, and the 11,000 jobs loss in the manufacturing sectors during the same month. This is the larger pattern of the economy’s shift into the services industries, as the Bureau of Labor Statistics (BLS) indicates the continued growth of the jobs in the health services industries during the last ten years. This is the kind of showing that indicates these structural reorientations in the jobs markets, as the services take the lion’s share in the new jobs creation.

Meanwhile, median hourly earnings increased 3.9% from a year ago to $36.44, once more evidencing the education and healthcare industries taking on jobs that otherwise would have been shed with the contraction of manufacturing industries. This movement is highly likely being fueled by the kinds of global forces as outlined in National Bureau of Economic Research (2023) research reports. Forces of this type are intensifying the displacement of manufacturing employment, but creating new employment in healthcare and education industries, which are less vulnerable to technological upheavals.

Manufacturing job loss is evident in hardship in the 2020 recession, in which 61% of UK Midlands companies actually realized job reductions. This recurring vulnerability, driven by automation as well as global trade arrangements, is contentious for the time of the healthy recovery. While as much services growth is evident, analysts need to monitor the broader picture in the economy since shifting workplace determination implies that recovery is unlikely as well-proportioned or healthy as previously thought.

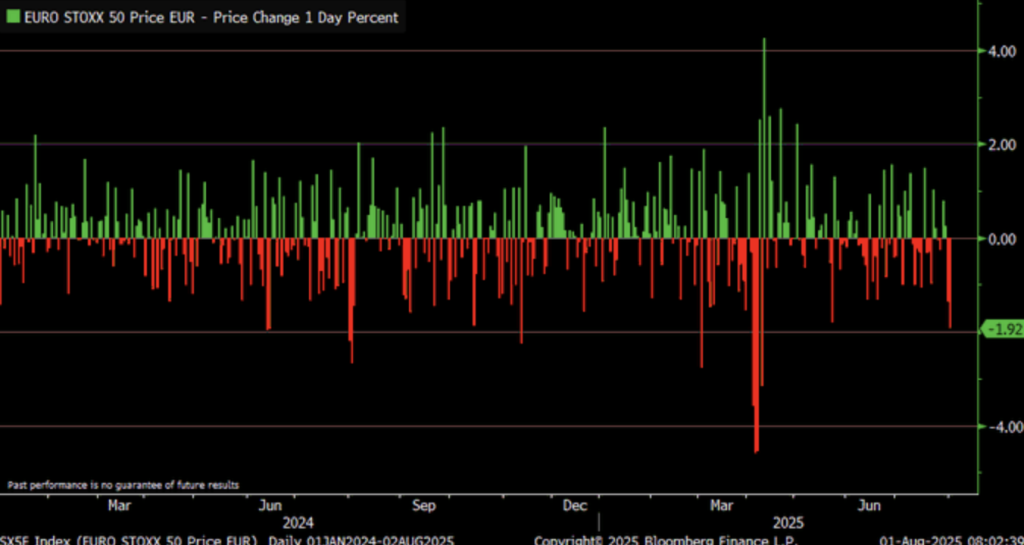

Euro Stoxx 50 Decline Reflected in Tariff Volatility and Trade Tensions

On August 1, 2025, the Euro Stoxx 50 lost nearly 2%, its worst day since April 9, 2025. The decline is due to renewed doubt over U.S. tariff policy following recent shifts in President Trump’s trade policy. Historical stoxx.com and Bloomberg data highlight the importance of the Euro Stoxx 50, an index of 50 large Eurozone stocks and underlying more than €28 billion of ETF assets. Its own volatility is a leading indicator of regional economic well-being, and the decline may be a sign of rising concern over the current trade tensions between the U.S. and its European allies.

The wider European market also shook, as the decline of Stoxx 600 by 2% during the day indicates coordinated market response. This fall is also caused by spikes in bond yields as well as fading investor confidence, widening the exposure of the European economy due to tariff uncertainty. This trend is also supported by evidence in the Journal of Financial Economics, which correlates the policy of tariffs with increased volatility in equity markets. Investors also increasingly worry about the wider effects of trade policy, even further because tariff-based volatility drives stock prices as well as sentiment in the markets. The link of the tariff policy to the performance of the markets is clearly visible as before, drops in tariffs have brought about market rallies. The reverse effect is now being witnessed, with new policy measures as well as fears of rising trade barriers possibly creating concern about the slowdown of the economy. Against these uncertainties, experts need to remain vigilant for releases or policy announcements that can further determine the economic future of the Eurozone as well as the soundness of the equity markets.

Upcoming Economic Events

While the near term might provide potential for short-term relief within the context of the economic calendar, the coming week is brimming with high-impact data, capable of shaping market sentiment for several months ahead. With the high-impact releases of the German Prelim CPI, Core PCE Price Index, Employment Cost Index, through to the Unemployment Claims, in the spotlights, the investor has to be on their toes. Such data shall hold crucial information regarding inflation trend dynamics, labor markets conditions, as well as monetary policy intentions—that influential drivers of global economic sentiment as well as of financial market direction.

Tune in, as this data has the ability to generate the big picture market reactions, which can move anything from cash to stock action. With the next moves of the ECB as well as the Fed under the microscope, the time is now to get ready for the coming flood of information that can re-shape the landscape for the remainder of the year. Watch the calendar-come interesting days ahead.

Earnings

Earnings Review: August 1, 2025

- Exxon Mobil Corporation (XOM)

Exxon Mobil reported Q2 2025 earnings of $7.1 billion ($1.64 per share), surpassing analyst expectations of $1.56 per share. The company achieved record second-quarter production, driven by advancements in the Permian Basin and Guyana. Despite lower crude and natural gas prices, Exxon maintained strong cash flow and returned $9.2 billion to shareholders through dividends and share repurchases. This performance underscores Exxon’s resilience in the face of challenging market conditions, though future performance may still depend on fluctuating commodity prices and geopolitical factors.

- Chevron Corporation (CVX)

Chevron posted Q2 2025 adjusted earnings of $3.1 billion ($1.77 per share), exceeding the forecast of $1.70 per share. The company achieved record production levels, producing 1 million barrels of oil equivalent per day in the Permian Basin. Chevron returned $5.5 billion to shareholders and completed the acquisition of Hess Corporation in July. Despite concerns over regulatory risks and lower energy prices, Chevron’s strong operational performance and growth in its upstream division provide a solid foundation for continued shareholder returns.

- Linde plc (LIN)

Linde reported Q2 2025 adjusted earnings per share of $4.09, beating expectations of $4.03. The company achieved a 6% increase in net income, driven by higher demand in the Americas and operational efficiencies. Linde’s operating profit margin improved to 30.1%, reflecting strong performance in its industrial gases segment. While macroeconomic factors could affect future growth, Linde’s position as a leading industrial gases provider and its focus on efficiency improvements suggest continued positive results.

- Colgate-Palmolive Company (CL)

Colgate-Palmolive reported Q2 2025 adjusted earnings per share of $0.92, surpassing analyst estimates. Revenue for the quarter reached $5.11 billion, driven by strong sales in oral care and pet nutrition segments. Despite the earnings beat, shares declined due to concerns over margin pressures from inflation and tariffs. The company’s efforts to manage supply chain challenges and mitigate cost inflation will be crucial in sustaining growth in the second half of the year.

Earnings Preview: August 4, 2025

- Palantir Technologies Inc. (PLTR)

Palantir is expected to report Q2 2025 earnings with a consensus estimate of $0.14 per share on revenues of $500 million. Investors will focus on the company’s growth in government and commercial sectors, particularly its advancements in artificial intelligence and data analytics. Any positive developments in these areas could signal continued demand for Palantir’s services, though its ability to scale these innovations will be critical to its long-term growth.

- MercadoLibre, Inc. (MELI)

MercadoLibre is projected to report Q2 2025 earnings of $12.01 per share, with revenues around $6.52 billion, reflecting year-over-year growth. Key metrics to watch include performance in Argentina, Brazil, and Mexico, as well as trends in e-commerce and fintech services. Any surprises in these core markets, especially in the face of inflation or political volatility, could have a significant impact on its stock price and future outlook.

- Vertex Pharmaceuticals Incorporated (VRTX)

Vertex is anticipated to report Q2 2025 earnings of $4.25 per share on revenues of $2.91 billion. Investors will focus on the performance of its cystic fibrosis treatments and progress in its drug development pipeline. Positive updates on drug approvals or new indications could further strengthen the company’s position in the biotechnology space, making it a key player to watch for both short-term and long-term growth potential.

- Williams Companies, Inc. (WMB)

Williams is expected to report Q2 2025 earnings of $0.49 per share. Key areas of interest include the company’s natural gas infrastructure projects and its role in the energy transition. Any commentary on expansion plans, especially around renewable energy or carbon capture, could impact investor sentiment, as these initiatives will determine Williams’ future role in the evolving energy landscape.

- Hims & Hers Health, Inc. (HIMS)

Hims & Hers is set to report Q2 2025 earnings, with analysts focusing on its telehealth services growth, customer acquisition strategies, and profitability metrics. The company’s performance in expanding its customer base and increasing its telemedicine offerings will be critical in assessing its ability to scale efficiently in a competitive healthcare market. Any unexpected developments in these areas could provide a boost or challenge to its growth prospects.

Investors should monitor these earnings reports closely, as they may influence market sentiment and provide valuable insights into sector-specific trends and broader economic conditions.

Stock Market Summary – Monday, August 4, 2025

U.S. markets started the week gently, as investors were still apprehensive about latest economic statistics as well as geopolitics. Nasdaq Composite and S&P 500 fell, but the Dow Jones Industrial Average flatlined. Russell 2000 stayed under pressure against economic issues.

Stock Prices

Geopolitical Changes and Economic Trends

Conservative market sentiment is due to various reasons. The US economy had only created 73,000 jobs in July, far less than expectations, which has generated concerns about the state of the labor market. Additionally, President Trump had recently put tariffs on imports from various nations, which has now amplified tension on intercontinental trade as well as created market anxiety. These issues have seen investors turn risk-averse, which has affected the performance of the market.

Today’s Stock News

These 5 Stocks Have the Greatest Chance of the Next Mega-Caps (> $250B+)

While investors continue to look for the next growth icon, there are some firms that are themselves on track to turn mega-cap stock ($250 billion+) themselves. The five most likely contenders are:

- $CRWD | Crowdstrike, the leading cybersecurity player, has gained unprecedented popularity with its security services based on AI. With the security threats posed by cyber attacks increasing continuously across the world, Crowdstrike, being a leading player, has every possibility of becoming a mega-cap player.

- $NET | Cloudflare, a leading cloud security and content delivery company, is expanding rapidly aided by the requirement for rapid and secure online services. Fueling the strong numbers and expanding customer base, it’s headed toward becoming a mega-cap company.

- $AXON | Axon, the public safety technology leader, is continuing to enjoy strong demand for both its cloud-based software and its body-worn cameras. As technology for public safety continues to evolve, the company will join the $250 billion club.

- $MELI | MercadoLibre, the “Amazon of Latin America”, has seen a surge of e-commerce as well as fintech growth. Expanding across all of Latin America, it has the potential to be the continent’s next mega-cap.

- $ARM | Arm Holdings Arm Holdings, the design company of chips, continues to become even stronger as there is growing demand for chips worldwide. Strong market position, along with strategic partnerships, positions it well towards mega-cap growth into the future.

Moreover, $PLTR | Palantir Technologies has surpassed the mega-cap barrier already, while $NOW | ServiceNow is fast approaching $250 billion, but holding its ground still in the enterprise software sector.

The Magnificent Seven and the S&P 500

The “Magnificent Seven” of Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla are softening. A recent sector split places the group averaging more than an 18% correction from recent highs, with Meta and Tesla leading the way lower. That bodes well, of course, for a valuation de-risking, particularly for AI-growth narratives that have gotten unhitched from fundamentals. The S&P 500 still hangs around as tech leadership falters. As nice as energy and industrials are providing some relief, the gauge isn’t going rally on a lasting basis without the return of the participation of its mega-cap core engines.

Major Index Performance as of August 4, 2025

- Nasdaq Composite (QQQ): 20,650.13 (-2.24%)

- S&P 500 (SPY): 6,287.28 (-0.82%)

- Dow Jones Industrial Average (DIA): 43,781.77 (-1.30%)

- Russell 2000 (IWM): 2,166.78 (-2.03%)

Zaye Capital Markets is following closely sector rotation and positioning strategies within the reporting earnings period. Success by leading companies to maintain the earnings momentum despite shutting policy tightening will determine the direction of overall equity markets in 3Q.

Gold Price – Monday, August 4, 2025

Gold prices weakened modestly in the week, with spot gold closing at about $3,351.77 an ounce, down 0.33%. August U.S. gold futures are modestly higher at $3,360.10 an ounce. Gold prices had weakened recently as profit-taking followed a gain that had been driven by weak July U.S. employment growth statistics, which had served to create hopes of a Federal Reserve rate reduction that tends to support gold prices. There was not, however, significant economic data put out today, so market momentum waned, and thus a modest weakening resulted. But nonetheless, the tone of the gold market remains positive, as such current geopolitical as well as economic issues continue to underpin demand for safe havens.

President Trump’s recent remarks, including his imposition of tariffs and his attacks on the independence of the Federal Reserve, also are likely to continue impacting the gold market. His tariffs as well as his policy position on the Fed, including his recent dismissal of the head of the statistics on employment, have heightened market doubts, bringing gold into focus once again as a hedge on possible economic disruption. Although there is little of note on the economy schedule for today, analysts continue to look optimistic on gold’s long-term outlook, with forecasts anticipating possible gains of more than $3,700 an ounce over the next couple of months as investors continue to look for refuge from market volatility as well as economic doubt.

Oil Prices – Monday, August 4, 2025

As of August 4, 2025, Brent crude stands at about $69.01 a barrel, while West Texas Intermediate (WTI) stands at about $66.90 a barrel. Both of these drops are primarily due to a string of increased supplies offered by OPEC+ as well as geopolitics. OPEC+ has agreed to produce another 548,000 barrels a day during the month of August, something that has redoubled fears of oversupply as demand hesitates on a global level. Alternatively, President Trump’s recent levies on some of its biggest trading partners, including India, Canada, as well as Taiwan, still keeps the oil market a contentious space, in that such moves are set to place a stranglehold upon world trade as well as perhaps depress international supplies of oil. The International Energy Agency (IEA) has decreased its worldwide growth for oil demand, as well, as a reference to the danger of such trade antagonisms as well as economic slowdowns.

Yesterday economic data, especially poor U.S. jobs growth data, has put further strain on oil prices as economic growth could slow down. Market participants are afraid that a hurt employment sector may translate into lower energy demand over the coming two months, which puts further strain on oil prices. Markets remain volatility-driven due to aggressive U.S. trade policy by Trump, as well as economic data of weak growth, like economic data. Dynamics of rising OPEC+ production, geopolitics, as well as economic data of growth slowdown, cause market volatility. Oil speculators monitor such events, as drastic changes are possible to prices over weeks to come if there should prove to be either a shift to manufacturing level or a balance shift of geopolitics.

Bitcoin Prices – Monday, August 4, 2025

Bitcoin (BTC) at present changes hands at approximately $114,783, quietly higher than yesterday’s close. The action has come about despite there also existing increased geopolitical tension as well as changes in U.S. economic policy. It has recently had to endure President Trump go on the offensive, including increasing tariffs on trading partners as well as belittling of the Federal Reserve, which has served to increase volatility further into the market. As such, Bitcoin has served as a hedge, as investors have wagered into the currency despite fear of diversion into mainstream financial venues. Where there exists possible diversion into Fed rates, the value of Bitcoin has suffered further impingement from anticipated loose monetary policy, which has served further into its role as an alternate class asset.

Yesterday’s poor jobs report, registering only 73,000 new jobs created in July, further increased concern over the state of the economy as it gave a boost to the popularity of bitcoin amidst times of doubt. Spontaneous institutional buying, including blockbuster announcements such as that of Trump Media acquiring $2 billion worth of bitcoin assets and further institutional uptake of digital assets, has seen added institutional investor demand sustain bitcoin prices, pushing them higher. From here on, bitcoin’s price will depend on forthcoming announcements of economic reports, trade agreements, as well as continued redefinition of the digital asset space by institutions.

Ethereum (ETH) Prices – Monday, 4 August 2025

Ethereum (ETH) was at $3,558.07, 3.25% more than the last close. ETH has moved both ways in the last week, reaching as low as $3,500 before surging. The volatility has been due to the intersection of institutional activity as well as market forces. Ethereum ETFs, such as the iShares Ethereum Trust (ETHA), recorded net inflows of $5.43 billion in July 2025, a 369% increase from June. This trend, however, got disrupted on August 1, as ETH ETFs saw net redemptions of $152 million, breaking a 20-day inflow chain. This is proof of market sensitivity to shifting sentiment, as institutional investors rebalance as macro conditions change.

The whales’ movement still has a significant impact on Ethereum’s prices. Early August 2025, two of the biggest Ethereum whales acquired over $400 million of ETH, booking optimism on long-term asset value despite correction. Other key influencers, however, such as Arthur Hayes, have offered selling pressures through relocating significant ETH volumes on exchanges. Such acts of dual warfare from deep pockets mean that there exists a guarded but optimistic outlook of Ethereum, which signifies that some of them are positioning themselves for long-term gain but some of them are cashing on short volatility. Such acts determine Ethereum’s whole market trend, which means that staying informed on whale action, as well as institutional sentiment, still remains as vital determinants of prices.