Where Are Markets Today?

As of today, U.S. stock futures are indicating a modest upward movement. Futures tied to the Dow Jones Industrial Average have risen by 84 points, or 0.19%, while S&P 500 and Nasdaq 100 futures have both climbed 0.2%. This follows a volatile session on Thursday, where the Dow saw sharp swings, ending the day down by 224 points, or 0.5%. While the Nasdaq Composite showed resilience with a nearly 0.4% gain, the broader market remains cautious amid the mixed economic signals. Investors are awaiting further clarity on the U.S. trade policies and Federal Reserve stance to guide their investment strategies moving forward.

In European markets, stock index futures are also showing positive movement. The Euro Stoxx 50 futures are up 0.95%, while the DAX and FTSE 100 futures have gained 76 points and 0.32%, respectively. This upward momentum comes after a period of uncertainty, where European markets also felt the impact of global trade tensions. The rise in futures could reflect investor optimism following President Trump’s announcement of a potential trade deal with China, though concerns remain over the newly implemented tariffs, particularly with India. The European markets are closely monitoring these developments, as they could have significant implications for the broader market.

Two key factors are influencing the current positioning of both U.S. and European futures. First, President Trump’s new “reciprocal” tariffs, which took effect on August 7, 2025, have added to market uncertainty. While some sectors, particularly those benefiting from the tariffs, initially saw a boost, broader market sentiment remains cautious. There is concern that these tariffs may provoke retaliatory actions and could further disrupt global trade, which may weigh on investor confidence. Additionally, these tensions could lead to increased inflationary pressures, especially in industries reliant on imports from affected countries.

Second, the Federal Reserve’s potential shift towards a dovish monetary policy is contributing to market optimism. President Trump has expressed support for rate cuts based on economic forecasts, and the nomination of Stephen Miran to the Federal Reserve is seen as a move towards a more accommodative stance. This shift has led to expectations that the Federal Reserve will cut rates by 25 basis points, which could provide additional support to equity markets. As a result, U.S. and European futures are poised to open slightly higher, though the overall market sentiment remains cautious as investors await clarity on trade and economic policies.

Big Picture Index on Friday, August 8, 2025

- Nasdaq Composite: Up at 21,242.70, 0.1% higher for the day.

- S&P 500: Down 0.4% on the day at 6,339.39.

- Russell 2000: 2,147.63, lower by 0.3 on the day.

- Dow Jones Industrial Average: 41,182.34, down 0.2% on the day.

The Mag 7 and the S&P 500 Index

“Big 7″—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—albeit having good runs in the past years, present difficult days ahead of them. The current analysis accounts for these stocks having registered colossal drawdowns with the average drop being more than 18% from the current highs. That has been on account of factors like the revenues missing the targets along with the letdowns with the huge investments put on artificial intelligence, so far, without returning the value proportionally.

Drivers Behind the Market Move – Friday, August 8, 2025

As of Friday morning, U.S. and European markets are poised for modest gains, influenced by recent economic data, President Trump’s trade policies, and expectations of Federal Reserve rate cuts. Here are the key factors driving market sentiment today:

1. Implementation of New U.S. Tariffs

President Trump’s new “reciprocal” tariffs, which took effect on August 7, have introduced uncertainty into the markets. While certain sectors, like semiconductor companies, initially rose on the news, broader market sentiment remains cautious due to concerns over potential retaliatory measures and the impact on global trade. These developments have led to increased risk aversion among investors, impacting market performance.

2. Expectations of Federal Reserve Rate Cuts

The recent weak U.S. economic data, including disappointing jobless claims, has heightened expectations that the Federal Reserve may lower interest rates. President Trump’s expressed support for rate cuts, along with the nomination of Stephen Miran to the Federal Reserve, suggests a shift towards a more accommodative monetary policy. This has led to optimism in the markets, as lower rates could stimulate economic growth and support equity prices.

3. Mixed Corporate Earnings and Sector Performance

Corporate earnings have been mixed, with some sectors outperforming while others lag. For instance, technology stocks have gained, driven by optimism over tariff exemptions for companies investing in U.S. manufacturing. However, healthcare stocks have underperformed, with companies like Eli Lilly reporting disappointing results. This divergence highlights the sector-specific impacts of current economic policies and market conditions.

In summary, while markets are showing positive movement, investors remain cautious amid trade policy uncertainties and mixed economic signals. The direction of future market performance will depend on the resolution of these issues and the effectiveness of monetary policy adjustments.

Digesting Economic Data

TRUMP Tweets and Their Implications

President Trump’s recent remarks again provided a boost to market sentiment with far-reaching implications for the US economy as well as the global markets. With his noteworthy statements, Trump clearly asked for a dramatic shift towards aggressive US trade policy, especially against India, where he has decided to increase tariffs on the nation’s import against its relentless importation of Russian oil. The action has triggered higher concern in new geopolitics tensions with the possibility to damage global supply chains as well as greater inflation risks. The threat of increasing tariffs on India, the world’s largest tariff nation, is likely to trigger retaliatory action, further escalating trade threats as well as causing volatilities in commodity prices, especially oil. Increasing tariffs would force US manufacturers to pay more for input, driving the cost for end-users higher, thus triggering inflationary pressure.

Additionally, the Chinese trade remarks by Trump, particularly the upbeat tone towards reaching a trade agreement with President Xi, created mixed signals. Positively, the possibility of a trade agreement has been buoying market sentiment, with some analysts positing the likely agreement may serve to de-escalate tensions and stabilize market conditions. On the other hand, the ambiguity regarding Trump’s approach to global trade, coupled with the necessity of adding tariffs as a negotiating tool, has continued to inject volatility into financial systems. The Chinese remarks by Trump also imply there shall be more developments on the trade agreement side to drive market movements further, with particular sectors sensitive to trade flows, for example, technology and manufacturing sectors, being most likely to bear the brunt of the anxiety. Trump’s wider remarks, like criticism of JPMorgan or action against those he feels have unfairly discriminated against him, also help to support his hardline against corporate power and thus affect market sentiment in the financials and banks space. Although what he has to say on the Federal Reserve—support for lowering interest rates—is also in market consensus, it injects another dose of uncertainty. Whether or not Trump’s team continue to make the case for easy money will continue to elicit further market response, not least in the bond space, where the threat of softer rates will see yields fall back and risk assets, not least equities, get a boost.

Moreover, Trump’s tweet hinting at the potential opening of the US 401(k)s to investments in crypto and private equity provides a glimpse of a possible US financial regulation change that will have a strong lasting impact on the cryptocurrency market. Opening these types of investments to retirement accounts by Trump would unleash a new institutional capital wave into cryptocurrencies, which could raise demand and prices for assets like Ethereum and Bitcoin. While these shifts have promise in the long term, the underlying vagueness concerning Trump’s intentions to regulate as well as pressure he applies on the Federal Reserve policies keeps the market on the brink of optimism, with investors closely observing him for the next move to make.

Fast-Rising Trends in CPI: An Indicator of Re-emerging Inflationary Pressures

Core Goods Consumer Price Index (CPI) has erratically risen during the last few years with a steep rise during the initial quarter of the year 2021, a fall thereafter, and the latest rise. The trend thus would seem to indicate the continued pressure of disruption of world supply chains. By reporting a 2.7% year-on-year CPI rise for the month of June 2025, global inflationary pressure, however, remains higher than desired. The continued uptrend could be signaling inflation risks, higher than initially anticipated, with repercussions for potential monetary policy.

There was the research by the Federal Reserve last 2023, citing the aggressive interest hike to curb goods inflation after the 9.1% CPI peak last June 2022. The newest hike of the CPI, however, comes after the prevailing geopolitical risks, including the air strikes by the nation of Israel on the nation of Iran, further straining the world’s global supply chains as well as commodities. Such actions could even derail program to stabilize inflation and further complicate future policies.

The recent trend witnessed since mid-2024 defies the existing hope for cooling inflation. With UK CPI increasing by 3.6% in June 2025, the world’s inflationary environment continues to remain uncertain. Analysts need to track geopolitical events in real time, as they could further intensify price pressures in the next few months. Undervalued Stock: As inflationary pressure increases, commodity-linked stocks, including energy and materials, could offer opportunities for undervaluation, with geopolitical risks set to increase demand for safer assets. Analysts need to track interest rate expectation changes and commodity price action.

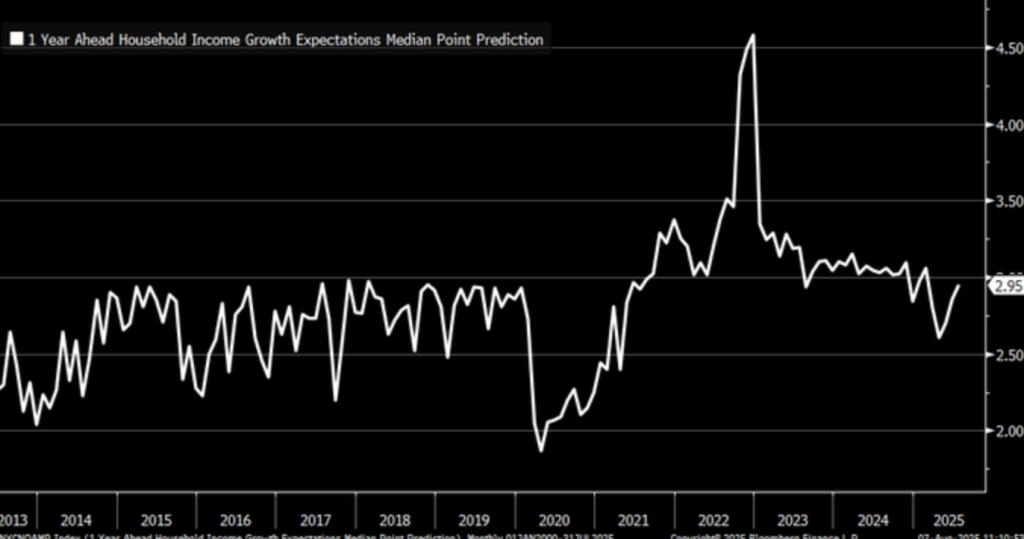

Income Growth Expectations: Converging Trends Amidst Economic Uncertainty

Chart by New York Fed of sudden jump in one-year-forward projections of the growth of household income to 4.5% by mid-2021 from 2.5% by July 2025 reflects the financial stress on the household sector. The decline reflects rising inflation pressure along with rising economic concerns, particularly by the low-income community and the elderly. Although there seemed to be optimism in the first years of the recovery, the decline in the expectation of the growth of income is the reflection of the more cautious consumer approach.

The Federal Reserve Bank of New York’s January 2023 Survey of Consumer Expectations documents a steep 1.3 percentage point decline in anticipated income growth from January to February, with the sharpest declines from lower-income and older survey participants. The survey identifies income inequality not reflected in broad economic estimations, as they continue to bear the brunt of price hikes as well as inflation pressure disproportionately, relative to the broader general population.

US Bank Asset Management Group studies focus on the importance of pre-inflation income growth to maintain consumption spending steady. Yet the prior decline in income projections, alongside small July 2025 reversals against the increase in import prices and tariff risks, can be future points of weakness for consumer spending. Undervalued Stock: Consumer staple firms, especially those with necessary products, will be potential future leaders to undervaluation because the firms will hold up better to thrive under economically challenging times. The analysts would be well-advised to monitor income growth disparities compared to emerging consumer confidence trends with focus on measuring potential impacts to discretionary spending.

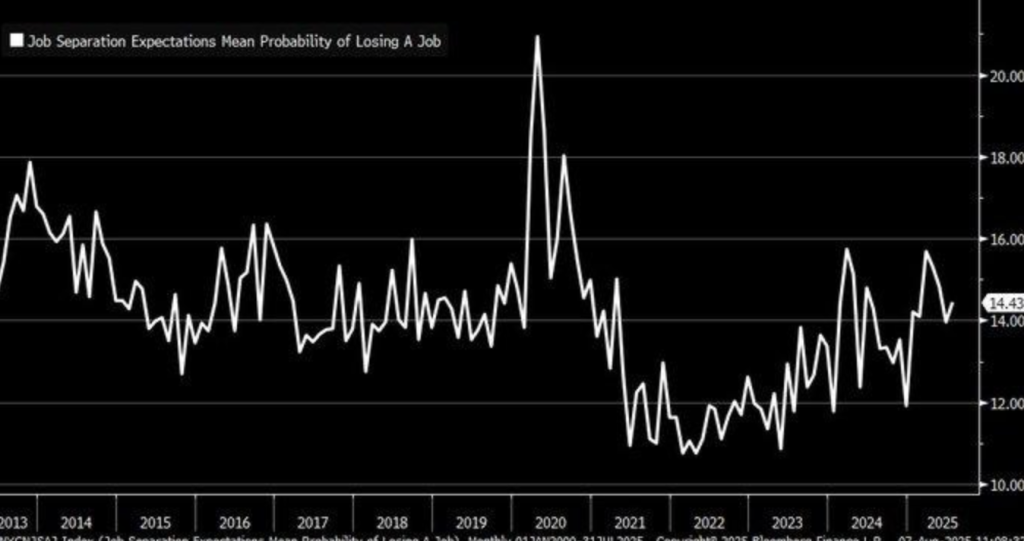

Rising Fears of Job Loss: Transient Disruptions or Structural Patterns?

The New York Federal Reserve graph shows steep jump in future possibility of losing a job, to 14.43% by July 2025, from 11.9% by December 2024. Against level payroll employment of a mere +73,000 by July 2025, it is an indication of rising economic uncertainty. Against earlier estimates, including the 2017 McKinsey report estimating the increase in jobs based on the increase in automatons up to 2030, indicating current fears may be exposing short-term tight market dislocations instead of long-term change.

Such increased likelihood of losing a job could be owing to the current world supply chain disruption or increased fray over AI-to-job replacement, for instance. The renewed discussion on automation, as well as new-tech innovation, has made workers anxious about the future of their jobs. Specifically, low-skilled workers with low incomes could be the most vulnerable, with the NY Fed statistics indicating increased fear among them.

Displaced workers were highlighted by The Review of Economic Studies, 2020, to forfeit 13-25% of pre-displacement earnings in six years, once again placing monetary burdens on the consumer. Undervalued Stock: Those shares relating to re-skilling/re-training of employees with the advent of automation, or relating to build-out of the space of AI, would be the opportunities of undervaluation. Volatility of the job market itself, and the journey to automation, would be the disruptors of disruption to find, with hints on how industries are evolving to such fluid dynamics.

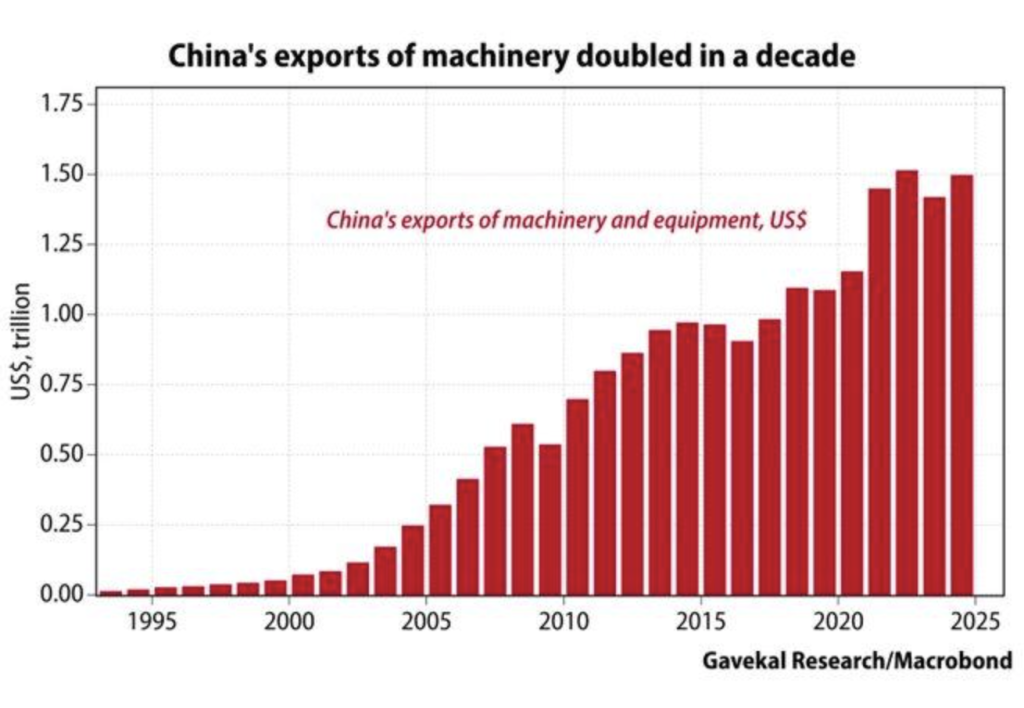

China’s Export Boom: Strategic Changes with Implications for the World Supply Chain

The chart with Gavekal Research/Macro bond data illustrates Chinese exports of machinery and equipment increasing from virtually zero for 1995 to more than $1.5 trillion by 2025. Phenomenal growth has been induced by accession to the World Trade Organization (WTO) by China in the year 2001, boosting the productive capacity of the nation and adding the nation to the global trade community. Chinese industrialism has made the nation the hub of the world’s supply chains, but concerns about the sustainability of export-led growth with increasing geopolitical tensions prevail.

Through government subsidies as well as titanic investments for infrastructure, Chinese manufacturing production became the most likely to compete with the existing markets like the United States, based on a 2019 paper by the Journal of Economic Perspectives. Its export-oriented strategy, however, has been viewed to present risks for over-reliance on external demand together with risks for disruption to the world’s supply chains. Trade disputes with the United States, specifically, together with increasing costs can challenge the extent of the export strategy of China.

While patent infringement cases dominate, in Lexology review for 2022, China’s export miracle consists of high-tech machinery in contradiction of its thesis producing low-quality products. Customs data shine light on increased integration of authentic and counterfeit products, behind the nation’s spectacular growing economic growth. Undervalued Stock: World trade-related companies or companies with association supply chains related to Chinese exports of equipment and machinery can be undervalued, especially those having diversified bases of supply to prevent likely disruption. The future will call for analysts to observe keenly policies of Chinese trade with respect to risks of association supply chains as leading indicators.

U.S. Productivity Growth: Surprise Rebound Despite Fears of Global Slowdown

US nonfarm business sector productivity rose to 1.3% year-over-year in Q2 2025 from 1.2% previous quarter reading in Q1, the Bureau of Labor statistics reported. The reading came after surprise 3.0% increase of the GDP growth after previous 0.5% fall in Q1 2025, revealing the strength of the economy with all concerns over global slow down. Expansion of the productivity, measured as output per hour, reflects the potential strength of the level of efficiency of the labour force but sustainability remains doubtful.

Historically, U.S. productivity growth decelerated below 2% after 2000, defying expectations of declining productivity from automation. Multifactor productivity growth accounted for only a relatively weak 0.4% per year in GDP growth, a 2019 NBER working paper reports, emphasizing the productivity growth as anemic compared to automation growth. The boost in productivity can be a short-run spike due to short-run causes such as reduced imports and a spike in consumer spending, the BEA’s advance estimate indicates.

While the recent productivity bounce is heartening, analysts need to exercise caution because there has not been enough long-term data to indicate this trend will extend. The mixed signals of the data in recent quarters and the arguments afresh regarding labor mix and productivity measures are a pointer to the fact that caution could be warranted. Underappreciated Stock: Consumer discretionary and technology-based companies are likely underappreciated, especially those that have gained from reduced import dependency and improved domestic consumption. GDP growth and consistent productivity momentum monitored by analysts would aid an assessment of the economy’s health.

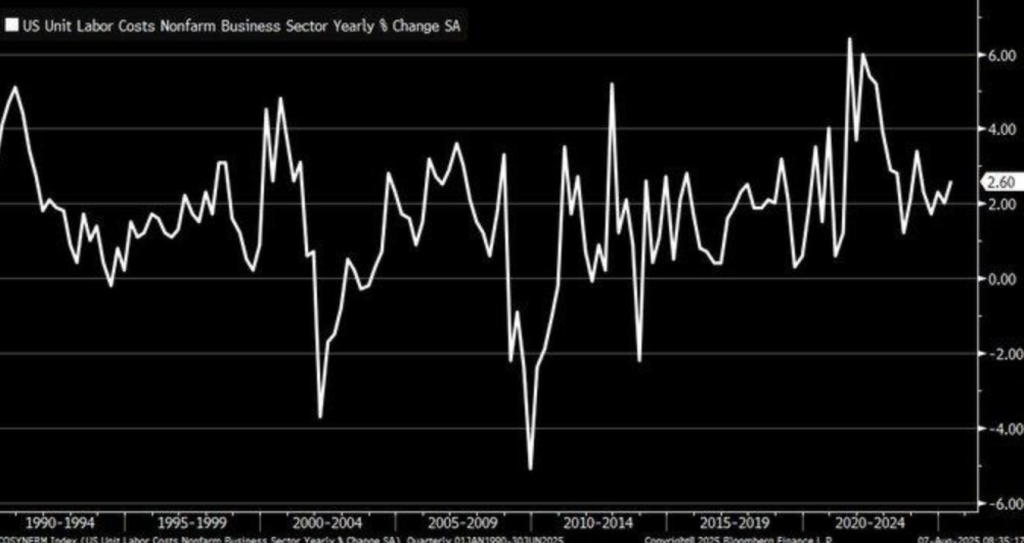

Rising US Unit Labour Costs: Inflation Pressure Ahead?

U.S. nonfarm business unit labor costs recovered to +2.6% year-over-year for Q2 2025, indicating increasing costs to labor, which would be a negative to inflation containment. The increase specifically follows the decline during the 2020 pandemic recession, mirroring the adjustment for the costs to labor with the changes for the economic environment. In the rise for the costs to labor shown by changes for wage rates and productivity, the rises could indicate following inflation forces, making it harder for the Federal Reserve to keep inflation contained.

A sustained rise in unit labor cost produces inflationary pressure, a study in the 2023 Journal of Economic Perspectives contributes. The recent rise in labor cost could presage rises in price levels generally in the future, if firms transfer the added cost to customers, particularly if the rise in wages surpasses the rise in productivity. The trend so far is for inflation to be more entrenched, further contributing to the cloudiness in the economic environment.

Historically, times of rising unit labors costs happened under the limits of the restrictive labor market, as following the 2009 rebound. The current global supply chain disruption, though, amplified by the 2025 due to the geopolitical conflict, could take this tendency beyond the normal cycle of the economy. Undervalued Stock: Industrials and commodities stocks might be undervalued, as rising labors costs and supply chain pressure could push the cost of inputs higher, and benefit those companies supposed to benefit from rising prices. The analysts need to track the trend of the labors costs and the geopolitical factors in order to assess the risk of inflation.

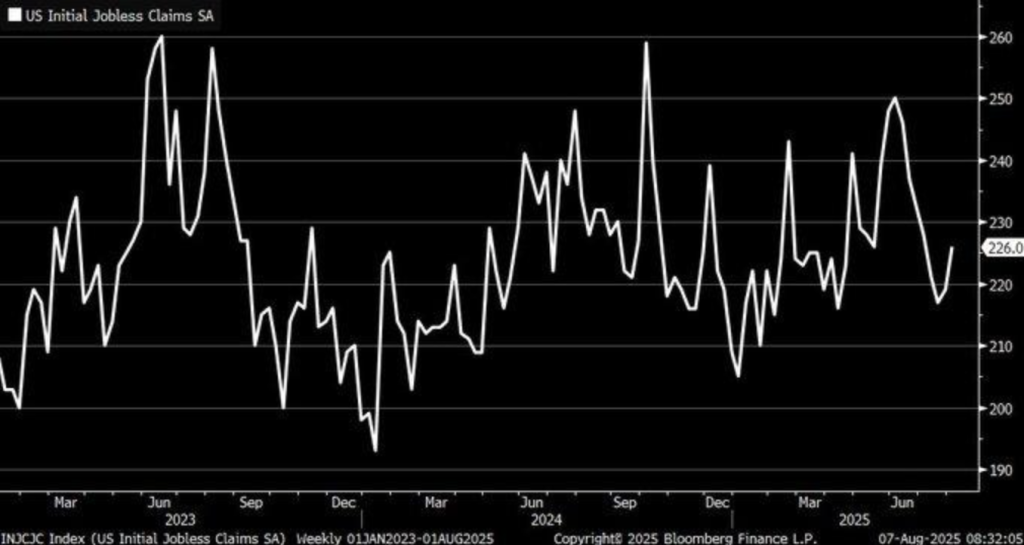

US First-Time Jobless Claims Rise: Recession Risk or Temporary Volatility?

US first-time unemployment benefits soared to 226,000 in the first week of the month of August 2025, from 219,000, and providing a possible leading indicator of a recession. The surge comes after the 2023 National Bureau of Economic Research report linking increased claims to recession risks. While the surge served to fuel panic, whether this represents the start of the overall slump or the temporary dip within the otherwise robust labour market remains to be established. The experts must watch these indicators for clues regarding the more structural slide.

It is contended that the theory supporting the word “Trumpcession” is President Donald Trump’s economic policy, or rather tariffs and trade wars, is perhaps impacting the unemployed claims. Such positions do not, however, rely on peer review academic pieces throughout the year 2025 as the immediate consideration. The argument of tariffs, although paramount, comes second to other forces of the macroeconomy, including global supply chain dislocation with the re-structure of the labour market.

Historical volatility in jobless claims, according to the U.S. Department of Labor, implies the four-week average of claims (recently near 223,000) is a steadier indicator than the weekly series, which can experience notable short-term volatilities. It highlights the need to take the longer perspective before making conclusions from individual points of data. Undervalued Stock: Defensive sector companies, for instance, utilities sector companies and consumer staples sector companies, could be undervalued since they tend to be less exposed to economic deceleration. The analysts ought to monitor the trend of the labor market as well as the impacts of tariffs with a view to gauging the wider risks of a recession.

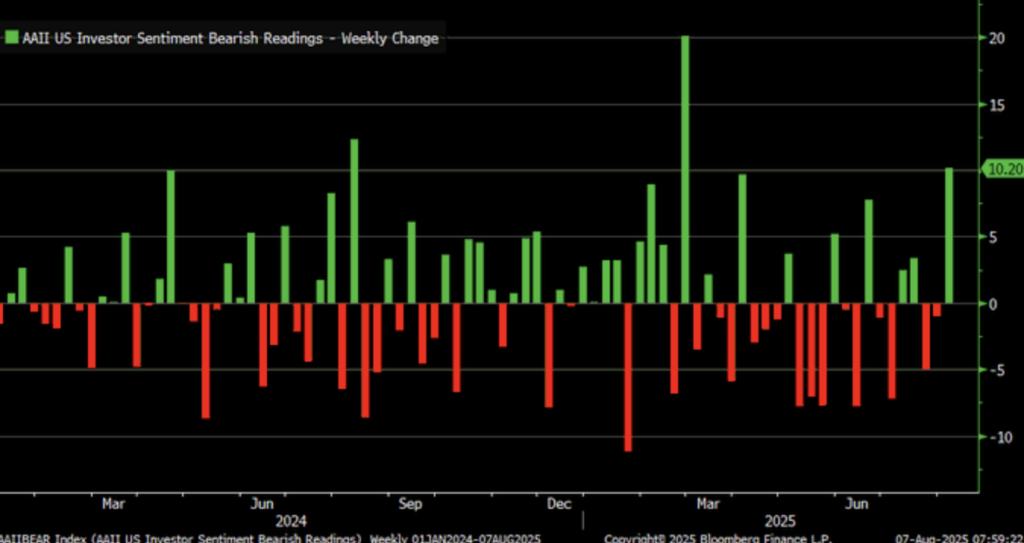

Rush to Bearishness: Signals for Reversals or Temporary Downturns?

American Association of Individual Investors (AAII) sentiment survey release captures a surprise rise of 10.2 points for bearish sentiment, the biggest since February 2025. The rise captures heightened skepticism following a burdensome year, further driven by mid-2025 Eastern European geo-political tensions, which shook global markets. The surprise increase for negative sentiment captures investors’ positioning ahead of further market volatility with the potential reversal on the cards. In this instance, the experts will have to keep a constant eye on investor sentiment as a possible catalyst to wider market correctives.

Historical AAII data exhibits bearish sentiment averaged 30.5% since 1987, with acute spikes on most occasions prior to market corrections. Extreme sentiment changes, writes a 2019 paper by the Journal of Financial Economics, coincidentally happen to be followed by short-term S&P 500 corrections of 5-10%, and may be an early signal for a downturn. History has been consistent with this, with sentiment changes being the prime culprit behind causing sell-downs. Green sentiment peak observed on late July 2025, as compared to prior dips, is an abrupt reversal of investor sentiment, likely because of skepticism on Federal Reserve policies. Current real-time market commentaries, e.g., on TradingView, have characterized skepticism towards the interest rates posture of the Fed alongside inflation, likely because of this abrupt reversal of sentiment. Undervalued Stock: Defensive stocks, particularly involving the utility sector alongside the consumer staples sector, end up being undervalued opportunities among investors, given the fact these categories of companies outperform those involving cyclical sectors during market corrections. The policies of the Federal Reserve need to be closely observed because the short-term trend of the market will most likely be dictated by them.

Loss of US Market Share: Changes in World Market Trends

The chart shows US market cap to global market cap touched 46.8% in February 2025, but thereafter it declined dramatically. That proved correct a 2024 Journal of Financial Economics paper citing overvaluation risk for US technology shares. Because of the monolithic dominance of the performance by the technology sector, broader valuation gain by this sector has caused broader volatilities, observing the latest downslide of US market dominance.

This US market cap loss is only part of the larger rebalancing of world economic power. Data in February 2025 by Visual Capitalist show how Chinese market cap of $15.6 trillion and Indian market cap of $5.2 trillion now exceeding the UK market cap depict the world economic landscape shifting. The emerging markets continue to pick up steam, especially those emerging from Asia, and the US could lose its relative market dominance. These shifts could re-shape the world investment capital allocation, even influencing the global money flow.

Most recent cracks within the U.S. labor market, along with fresh tariffs introduced under the administration of President Donald Trump, published by The New York Times in 2025, may have hastened the decline of the market share of the United States. Such disappointments suggest the possibility of the loss of investor sentiment towards American equities, given the further rise of global markets, particularly Asian markets. Undervalued Stock: Opportunities may arise with the possibility of the correction of American technology stocks translating to global opportunities, specifically within emerging market ETFs or Asian investments, as these become increasingly dominant within the global market environment. Geopolitical events as well as repercussions brought by tariffs must be monitored by analysts to find the trajectory of the market.

Upcoming Economic Events

While the calendar of today’s economic releases might seem a bit quiet, there is every good reason to keep waiting for releases next week, with a flood of important information set to emerge, the potential to change market sentiment, included. Ahead of future releases, with prime economic releases as well as central banks releases, it is the releases for next week that might come with the feeling of clarity investors are looking for. Whether it’s through the reading on inflation, the releases on the employment, or the geopolitical releases, the stage is now set for market-moving information to come out. Keep on your toes, stay on full attention—next week’s releases might be the determinants of the next month, with plenty of potential for course correction. Focus on the horizon, with the macroeconomic environment remaining fluid.

Earnings

Earnings from 07-Aug-2025

- Eli Lilly and Company (LLY)

Eli Lilly’s Q2 2025 performance exceeded expectations, with adjusted earnings per share (EPS) of $6.31, surpassing the forecast of $5.60. The company’s revenue reached $15.56 billion, a 38% year-over-year increase, driven by strong sales of its diabetes and oncology therapies, including Mounjaro and Zepbound. However, the oral obesity pill, orforglipron, underperformed in clinical trials, causing a significant 14% drop in stock price. Investors should keep an eye on the development of new treatments and any potential delays or setbacks related to Lilly’s clinical trials.

- ConocoPhillips (COP)

ConocoPhillips reported strong earnings in Q2 2025, with adjusted EPS of $1.42, exceeding estimates of $1.38. Revenue was driven by higher energy prices and increased production, with production rising to 2.39 million barrels of oil equivalent per day. The company also announced the sale of Anadarko Basin assets for $1.3 billion, ahead of its $2 billion asset-sale target. Investors should monitor the company’s capital discipline strategy and any changes in energy price dynamics, especially in light of global market conditions.

- Brookfield Corporation (BN)

Brookfield’s Q2 2025 performance saw strong revenue of $18.08 billion, though its EPS slightly missed expectations at $0.88. The company continues to benefit from growth in its asset management and real estate sectors, driven by strong demand for infrastructure investments. Notably, the company announced a three-for-two stock split, which could provide added investor appeal. Investors should track the company’s acquisitions and divestitures, as they could impact its earnings trajectory in the coming quarters.

- Constellation Energy Corporation (CEG)

Constellation’s Q2 2025 earnings were strong, with adjusted EPS of $1.91, up from $1.68 year-over-year. Revenue increased by 20.54%, largely driven by increased electricity demand and higher energy prices. The company’s renewable energy initiatives continue to gain traction, and it signed a 20-year deal with Meta for the full output of the Clinton Clean Energy Center. Investors should watch for updates on Constellation’s renewable energy strategy, as it could significantly influence future growth.

- Motorola Solutions, Inc. (MSI)

Motorola Solutions reported a solid Q2 2025, with EPS of $3.04, a 17% increase from the previous year. Revenue rose by 5%, totaling $2.8 billion, driven by strong demand in its communications infrastructure business. The Software and Services segment grew 15%, and the company raised its full-year revenue and operating cash flow outlook. Investors should focus on the company’s continued expansion in public safety and communications, particularly in government contracts, which could drive future revenue growth.

- Monster Beverage Corporation (MNST)

Monster Beverage’s Q2 2025 results exceeded expectations, with adjusted EPS of $0.51, up from $0.41 year-over-year. Revenue rose 11.1% to $2.111 billion, driven by strong sales in international markets, particularly in Asia. The company’s Monster Energy Drinks segment saw an 11.4% increase in sales on a foreign currency-adjusted basis. Investors should monitor consumer trends in the energy drink market, as well as Monster’s product diversification and any potential competition from new entrants.

- Warner Bros. Discovery, Inc. – Series A (WBD)

Warner Bros. Discovery reported impressive Q2 2025 results, with adjusted EPS of $0.63, significantly beating analysts’ forecast of a $0.12 loss. Revenue grew 1% year-over-year to $9.81 billion, driven by strong performance in its studios division and successful movie releases. Streaming revenue also grew 9%, with an addition of 3.4 million subscribers. Investors should focus on subscriber growth and content strategy in the streaming segment, as these will be key drivers of the company’s future performance.

- Rocket Lab Corporation (RKLB)

Rocket Lab’s Q2 2025 earnings showed a loss of $0.13 per share, wider than the $0.08 loss in the previous year. However, revenue rose 36% to a record $144.5 million, driven by increased demand for satellite launch services. The company raised its revenue forecast for Q3 2025, expecting between $145 million and $155 million. Investors should focus on Rocket Lab’s contract wins and new partnerships, as these will be crucial in expanding its market share in the growing satellite industry.

Earnings Due 08-Aug-2025

- Summit Therapeutics Inc. (SMMT)

Summit Therapeutics is set to release its Q2 2025 earnings today, and investors will be focused on updates related to the company’s clinical trials, particularly in its muscular dystrophy program. Any advancements or delays in regulatory approvals could significantly impact the stock, especially if the company is progressing toward pivotal milestones or if new treatment data emerges.

- Lamar Advertising Company REIT (LAMR)

Lamar’s earnings will provide insight into trends in the outdoor advertising market, particularly in digital billboards. Investors should keep an eye on revenue from digital ad space and any commentary on the outlook for the advertising market, especially given current market conditions and the potential impact on ad spending.

- Plains All American Pipeline, L.P. (PAA)

Investors will be watching Plains All American’s earnings for updates on its energy infrastructure, including pipeline capacity and disruptions. Focus will also be on pricing trends within its transportation segment and the outlook for U.S. energy exports, as these are key factors influencing the company’s earnings potential moving forward.

- Freedom Holding Corp. (FRHC)

Freedom Holding’s earnings will offer insights into its financial services growth in Eastern Europe and Central Asia. Investors should look for updates on regulatory changes and new product offerings, as these could significantly impact the company’s margins and growth trajectory in these regions.

Stock Market Commentary – 8 August 2025

U.S. equities today are contending with a challenging environment, with the most recent economic data, international politics, and corporate quarterly results all contributing. The S&P 500 Index and the Dow Industrials continue to decline, but the Nasdaq Composite continues to defy the downtrend, driven by a rally in the technology sector.

Stock Prices

Economic Indicators and Geopolitical Developments

Investor sentiment is being driven by a close cluster of major issues. President Trump’s unexpected ratcheting up of the tariffs has brought the disruption risk themes for global supply chains along with inflation pressure themes. The tariffs, implemented on the 7th of August, pushed the average American import duty to the centennial high, impacting a few of the trading partners.

And the nomination of Stephen Miran to complete the remaining term of Federal Reserve Governor Adriana Kugler has sparked discussion on the future direction of the course of the U.S. money policy. The nomination of Miran, coupled with rumors the Denver-based Fed Governor Christopher Waller is the clear frontrunner to succeed the expiring term of Chairman Jerome Powell, has placed the interest rate course and independence of the Federal Reserve into question.

Recent Stocks News

The stock market keeps changing in response to evolving economic realities, and some industries are experiencing dramatic developments:

- Tesla (TSLA) has been sailing through choppy waters with the 24%-decline from the high, driven by a receding appetite for electric vehicle demand in the top markets.

- Microsoft (MSFT) has suffered a small blow due to skepticism about how rapidly it will continue to expand its cloud computing, with competition within the sector still increasing from Amazon and Google.

- Apple (AAPL), while reporting a robust earnings report, is under growing pressure for its dependence on high-margin iPhone sales, with investors worried these could peak in the next few quarters.

The Mag 7 and the S&P 500 Index

“Big 7″—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—albeit having good runs in the past years, present difficult days ahead of them. The current analysis accounts for these stocks having registered colossal drawdowns with the average drop being more than 18% from the current highs. That has been on account of factors like the revenues missing the targets along with the letdowns with the huge investments put on artificial intelligence, so far, without returning the value proportionally.

Big Picture Index on Friday, August 8, 2025

- Nasdaq Composite: Up at 21,242.70, 0.1% higher for the day.

- S&P 500: Down 0.4% on the day at 6,339.39.

- Russell 2000: 2,147.63, lower by 0.3 on the day.

- Dow Jones Industrial Average: 41,182.34, down 0.2% on the day.

We’re keeping a close eye at Zaye Capital Markets on the changing economic landscape, specifically the implications of trade policy as well as changes within the leadership within the Federal Reserve, set to influence market dynamics in the weeks ahead.

Gold Price – Friday, 8 Aug 2025

Gold is now priced at $3,389 an ounce, with fairly moderate increases from previous sessions. Such increase is spurred by the mix of geopolitical turmoil, including the previous announcement by President Trump to increase tariffs on importation coming from India and other countries, and the prevailing inflation concerns. The dovish sentiment for the Federal Reserve, together with the possibilities for cutting interest rates lowered the expense of keeping non-yielding assets such as gold, making the latter even more attractive as a safe-haven. All these cumulatively led to the increase of the gold price, with the expectation to continue the run, considering the prevailing economic environment.

The economic reports on yesterday also worked to fuel the gold bullishness. US jobless claims increased to 226,000, higher than anticipated, and indicating underlying labor market weakness. That, along with the Federal Reserve’s indication of a coming interest rate reduction, has worked to make the attraction of gold as an inflation hedge and as a hedge against economic uncertainty more appealing. With inflationary pressure still building, particularly against the backdrops of trade tensions and weakness in the labor market, gold is still set to be an excellent beneficiary. We at Zaye Capital Markets pay close attention to these trends, as they work to play a very important role in sentiment on investing in gold and other precious metals.

Oil Prices – Friday, August 8, 2025

Oil prices have been volatile recently, with Brent crude trading at around $66.40 per barrel and West Texas Intermediate (WTI) at $63.82 per barrel. The price fluctuations are largely attributed to the latest developments in global trade and geopolitical tensions. President Trump’s announcement of raising tariffs on Indian goods, which directly impacts oil imports, has sparked concerns about a slowdown in global trade. This move could lead to retaliatory actions, which in turn may disrupt oil supply chains and raise inflationary pressures. Additionally, OPEC+’s decision to increase oil production could further dampen upward price movements, as concerns about oversupply in the market grow.

The recent rise in jobless claims has contributed to a bearish sentiment, signaling a potential weakening in the U.S. economy. This has added downward pressure on oil prices as investors price in reduced demand for energy. On the flip side, expectations that the Federal Reserve may lower interest rates could support oil prices in the short term, as lower rates tend to boost economic activity and demand for energy. OPEC’s actions, coupled with geopolitical risks and fluctuating global demand, make the oil market highly sensitive to economic data. Investors should stay alert to further announcements and data releases, as these could significantly impact oil price movements in the coming weeks.

Bitcoin Prices – Friday, Aug 8, 2025

Bitcoin was at $116,900, a sharp jump from this week’s previous highs. The rally has been led by a series of variables, the latest of which is President Trump’s executive order for retirement 401(k) plans to invest in other assets, including cryptocurrency, last week. The policy move is claimed to release the enormous institutional buying, with the potential to open the floodgates of the $43 trillion US retirement market to crypto assets, too. Bets on a Federal Reserve interest rate reduction, after softer-than-expected jobless claims, were driving the euphoria of Bitcoin, with the interest possibility for non-yielding assets, including Bitcoin, declining. With the chances of a 25 basis points interest rate reduction by the September meeting of the Fed, interest has moved sharply for Bitcoin as a safe-haven asset.

Yesterday’s economic reports, such as the rise in jobless claims, triggered a change in sentiment, increasing wagers on a more dovish monetary policy by the Fed. The renewed attention has been caused among risk assets, including Bitcoin, since investors seek alternatives to traditional fiat currencies. Moreover, the institutional investors’ hope to soon receive the green light for a Bitcoin ETF continues to increase the credibility and exposure of Bitcoin, driving institutional demand. As the world continues to witness the outlines of rising geopolitical risk coupled with economic uncertainty, the asset continues to be in vogue for investors looking to wager against inflation as well as financial distress.

Ethereum (ETH) Prices – Friday, 8 August 2025

Ethereum (ETH) is trading at $3,889.21, up slightly by 0.0597% from the previous close. The momentum on the price side is indicating the formation of a range of consolidation after a humongous upswing in the last month. The last upswing for the ETH price has been induced by the culmination of several factors, resulting in increased institutional demand along with favorable regime on the regulation side, the major among them being the signing of the GENIUS Act, favoring stablecoins on the Ethereum chain. Such positive clarity on the regulation side has increased the confidence among investors, resulting in fresh highs for ETH. Secondly, the last whale jump has shown humongous faith for the long term for the case of Ethereum as one of the major whales transferred $86 million worth of ETH out of FalconX, showing strategic repositioning.

Ethereum’s market forces continue to be controlled by institutional investors, with various firms, the prime example being SharpLink Gaming, raising the percentage towards ETH. Whale trading continues to be a crucial factor, further supporting the bullishness. These shifts help signify Ethereum continues to be on the rise, with real momentum being generated from whales and institutional investors. With the retail investors also getting interested along with institutional investors, the increasing momentum is extremely likely, with the increasing interest for decentralized finance (DeFi) adoptions and the dominance Ethereum has achieved in the cryptographic space.