Where Are Market Today?

US and European futures are down south on Tuesday with investors digesting President Trump’s record-breaking move to oust Federal Reserve Governor Lisa Cook, a move raising alarms of central bank independence. Futures of the Dow were down by roughly 0.15%, while S&P 500 and Nasdaq futures lost 0.23% and 0.35%, respectively. European futures pegged to the Euro Stoxx 50 and Germany’s DAX are no differently softer, a result of spillover of political risk from Washington to global markets. It is as the Federal Reserve prepares to raise interest rates later this month. It has followed a fragile setup, occurring as Wall Street was already falling back on Monday after a stellar bounce last week.

Near-term effects have been seen in debt and currency markets. At night, the dollar index fell 0.3% as investors immediately switched to haven assets, with gold futures 0.3% up in initial trading. Meanwhile, the 2-year Treasury yield fell 4 basis points, reflecting loose policy expectations, and longer-dated yields rose, reflecting fiscal credibility concerns. Overall, the shifts reflect investor anxiety—short-term markets now project in September a cut in the fed funds rate with probability estimates in the 85% area, but faith in Fed independence has been rattled. European markets are also following the U.S.’ lead, with futures indicating softer regional opens. Lower are Euro Stoxx 50 and France’s CAC 40, with investors looking for German Ifo and U.S. consumer confidence later today. It is a weaker dollar that removes the sting from exporters but baser current rhetoric of political meddling in monetary policy distracts from near-term potential. Investors are concerned litigation against Trump’s action will be protracted and deprive the Fed of credibility and undercut market stability.

Meanwhile, U.S. and European futures are shifting defensively heading into a new risk universe of political upheaval, flows to sanctuary destinations, and upcoming economic figures. It’s a two-facet cross: additional volatility to world assets and a more extreme response to upcoming macro releases. On the heels of the “Magnificent Seven” already teetering outright weariness and geopolitical dangers coming under further strain, the session of the day is a step back from euphoria and into a more defensive mindset, putting futures on the defensive both sides of the pond.

Major Index Performance To Tuesday, August 26, 2025

- S&P 500: Current price is 5,842.47, decreased 0.4% today

- Nasdaq Composite: Fell 0.6% to 18,220.78, led by weakness in large

- Dow Jones Industrial Average: 41,182.34, off 0.2%, as defensive shares did not make any gains in a broad-based

- Russell 2000: 2,147.63, flat for the day, and related to rate sensitivity with small-cap stocks.

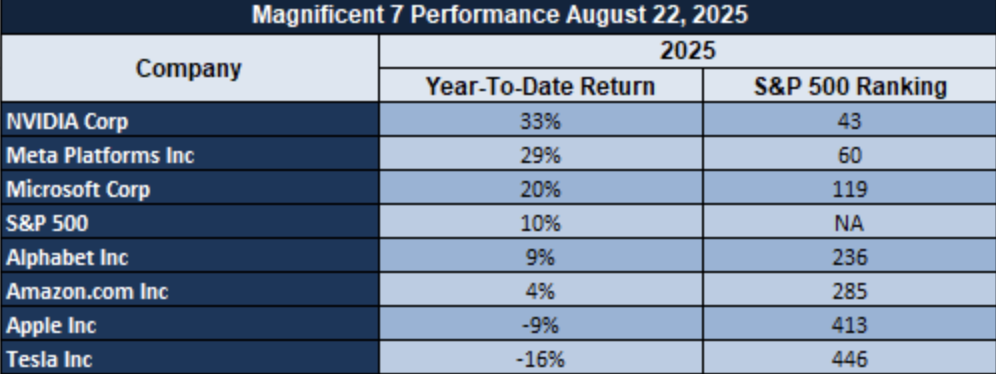

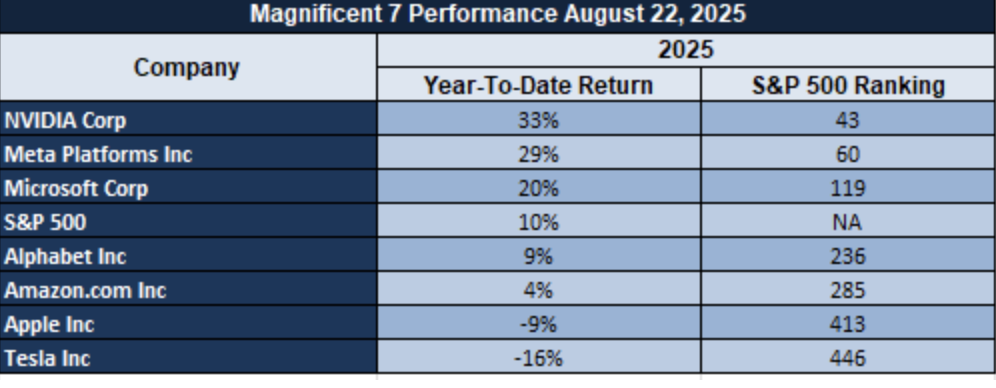

The Magnificent Seven and the S&P 500

The “Magnificent Seven” of Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla remain weak and the group has so far absorbed more than an 18% correction from recent peaks. Tesla and Meta are leading the weakness, a byproduct of valuation correction in growth stocks having gone well beyond fundamentals. Nvidia still has a glow due to dominance from AI but upcoming earnings is sending investors into a tizzy. Without buy support from these megacaps broadly, the S&P 500 is still vulnerable and still living off narrow leadership during periods of mounting volatility.

Drivers Behind the Market Move

U.S. and European markets are experiencing increased volatility today with the intersection of political shocks, economic risks, and macro surprises. The three drivers discussed below are the ones that we see impacting investors’ sentiments:

1. Trump’s Fed Shock: Institutional Confidence Shaken

This historic announcement by President Trump that he has relieved Federal Reserve Governor Lisa Cook of duty has taken markets by surprise and raised serious issues about the autonomy of monetary policy. This action is read by the majority of analysts as politicized—market pricing certainly considers ~83–85% chance of a Fed cut in September, but institutions’ reputation for non-partisanship is eroded, and therefore equity, currency, and debt markets remain volatile.

2. Future Economic Indicators: Consumer Sentiment & Durable Goods Step into the Limelight

Markets are preparing for today’s batch of top releases: Core Durable Goods Orders, Durable Goods Orders, CB Consumer Confidence, and the Richmond Manufacturing Index. Weak numbers there would further push the narrative of a slowing economy and drive investors deeper into rate haven assets like Treasuries and gold. But stronger-than-anticipated numbers might ease concerns and bring some relief to rate-sensitive markets.

3. Ripple Effects Globally: Dollar, Treasuries & Safe Havens Come into Alignment

Following the Fed saga, the U.S. dollar fell back, and particularly the yen and the euro, and short-term Treasury yields fell—emphasizing flight-to-safety mood. Gold hit a two-week high, and Asian shares continued early weakness, reflecting world unease. These three factors—monetary policy political interference, upcoming U.S. data slated to come out shortly, and defensive cross-border flows—are coming together to make a defensive market attitude.

We at Zaye Capital Markets are viewing these forces keenly and think guidance from macro data and central bank guidance will determine whether volatility is subdued today—or hyperbolic.

Digesting Economic Data

The TRUMP Tweets and Their Implications

President Trump’s latest comments featured foreign policy, domestic politics, and corporate M&A and made waves in markets. His comments in Ukraine and NATO suggested a U.S. tone shift, emphasizing personal diplomacy and a departure from monetary commitments to Kiev. Comments such as “we don’t really deal with Ukraine” and “I want war to end” suggest re-focusing U.S. foreign engagement, lifting risk premiums on geopolitical events and welcoming continued inflows into safe-haven vehicles such as Treasuries and gold, and keeping oil markets active in relation to the region’s centrality in world supply chains.

At home, Trump signed law enforcement and crime-related executive actions, including placing a moratorium to Washington, D.C.’s cashless bail and criminalizing the act of flag burning with mandatory imprisonment. Politically significant gestures, these are a hard law-and-order agenda aiming to transmit a sense of control over a situation in the midst of a crisis. Investors view these gestures to add to more unease around institutional capability, just as markets already integrate concerns around the autonomy of the Federal Reserve into his demand for Governor Lisa Cook’s resignation. The tone contributes to more political interference, and correspondingly another hit of risk premium to U.S. assets. Corporate America was no less the target of his remarks, and above all in the Intel deal. By observing that the U.S. government bought an ~$11 billion interest “for zero cost,” Trump positioned such deals as road maps for future industrial policy. He went on to announce “all government stake in Intel goes to the USA,” and forecast this as a national strategic victory.

Though the short-term impact lifted the stock value of Intel, the long-term consequence is the possibility of still more government intervention in corporate ownership of equity. Investors are split: some view this as a stepping stone to long-term industrial competitiveness, while others view the threat of crowding out private capital and politicization of boardroom decisions.

Finally, his remarks concerning South Korea—implying developments there now as a “purge or revolution” and a proposition to do business there—contributes to Asian geopolitical volatility. Likewise with remarks around Israeli attacks within Gaza and a proposition to send U.S. forces domestically “even if governors do not request,” such remarks are of a belligerent but explosive nature. As to markets, such volatility contributes to more challenging planning for investments because policy intent changes so rapidly within foreign affairs, commerce, and domestic law enforcement. Typical of them all is chronically high uncertainty, which usually dampens risk appetites and pushes investors into defensive corners waiting more light to arrive.

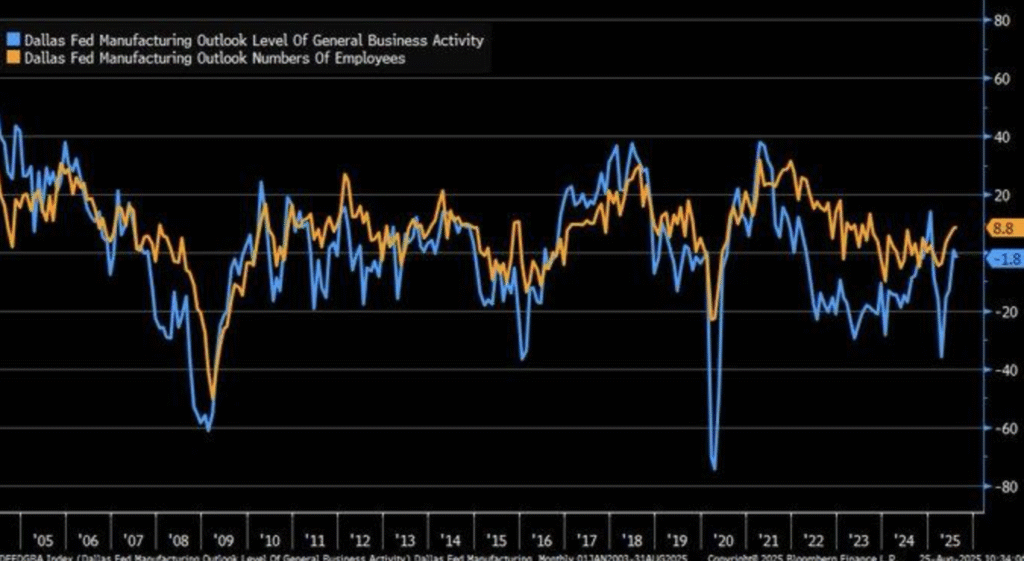

Texas Manufacturing Shows Mixed Signals

The August Dallas Fed Manufacturing Index fell to -1.8 from a previous 0.9 in July and below forecast of -1.7 and a slight Texas factory sector contraction. The index has in the past been exceedingly responsive to world trade flows and changes in the cost of energy and had, in earlier declines in the early 2000s and mid-2010s, hinted at structural strains just below the surface. This most recent fall is another signal that the industrial recovery is tenuous even though other areas of the U.S. economy are strong.

Below the top-line figure, though, the reading are more varied. New orders were assigned to +5.8 and shipments to +14.2 to show strength of demand in the face of weakening sentiment. Employment rose to +8.8 to show producers are keeping labor tight in a quest for stabilisation to occur. But inflation threats remain with prices paid jumping to +43.7 to show gains in recent producer price indices, and to reflect long-standing pressures in supply chains.

From an equity perspective, we view a selective U.S. industrial names to be cheaply priced in the face of solid order books and a possible return to margins in the face of a softening of input costs. Diversified exposure to end-markets away from oil-inspired cycles may be brought into sharper contrast by comparison with more oil-associated demand-exposed comparable. Analysts will want to see if cost inflation again consumes profitability or demand-led tailwinds dominate pricing headwinds, for so will dictate performance within the space from here.

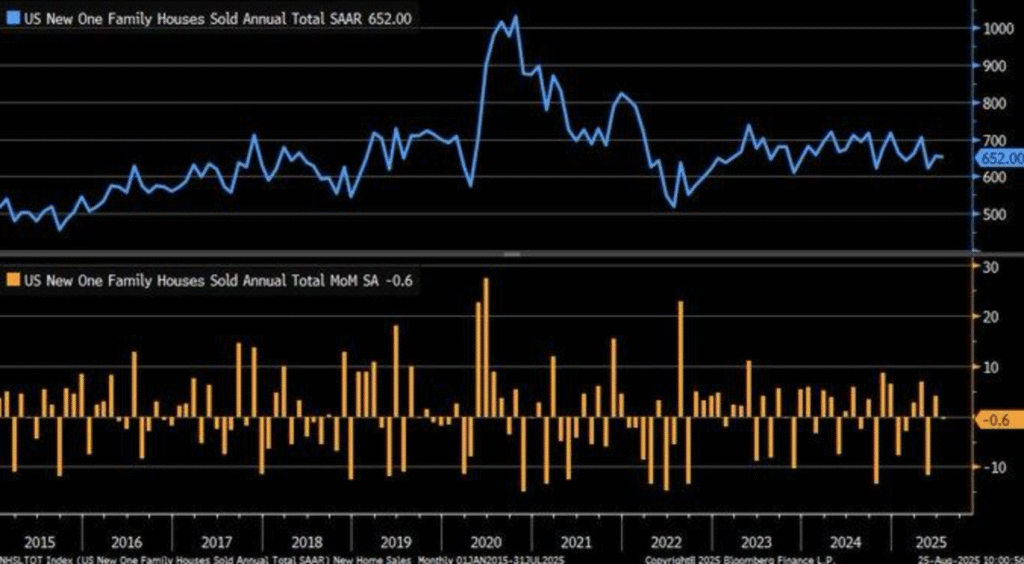

Housing Market Cools Despite Beating Expectations

July U.S. new-home sales reached 652,000 units, a 0.6% decrease from the prior month but above an anticipated 630,000. Although the initial take from the headlines bounce is of a robust market, the particulars are of a moderating housing market. Prices declined 5.9% from a year earlier to $403,800, reflecting the affordability problem with the mortgage rate of just below 6.6%. Builders became more dependent on discounts and inducements to compensate for activity, a pattern characteristic of earlier periods of scarcity of access to credit and elevated lending rates.

The supply side shows an even more urgent issue. Stock levels remained unchanged at 9.2 months, well above the pre-tightening benchmark of 5–6 months and indicative of an overhang which has the potential to put a ceiling on rates in months to come. Persistent higher mortgage rates continue to cap demand, minimizing churn and feeding stockbuilds. This dynamic is a echo of deeper housing structural weakness: affordability limits, increasing input cost pressures and the lagged impact of Federal Reserve policy tightening. Even though demand has not folded entirely, persistent elevated levels of stock make recovery bumpy and subject to another rate shock.

Valuation-wise, U.S. homebuilders are inexpensive relative to their long-term earning power, and most importantly those of sound balance sheet and exposure to the mid-price housing market where demand is relatively robust. We need to be sensitive to whether measures by the Fed over the coming intermeeting period render funding cheaper because this will stabilize volume sales and enable the sector to re-rate higher. But dominance of supply over demand can cap upside via margin compression and adverse pricing pressures and keep housing equities closely aligned with the policy direction of the Fed.

Chicago Fed Index Implies Slowdown

The Chicago Fed National Activity Index (CFNAI) dropped to -0.19 in July, less than a forecast of -0.11 and the fourth consecutive negative reading. Below levels required to signal impending recession, the declining trend is significant because of past experience that a three-month average below -0.70 usually indicates increasing chances of recession. This decline is a signal of slowing momentum throughout the economy and raises doubt about the Federal Reserve’s ability to strike a balance between stimulating inflation and cementing growth.

32 of 85 supporting indicators charted positive contributions and indicated the extent of economic softness. Drag is predominantly from production and jobs categories and assists in confirming the story of industrial and labour markets slowly cooling. While such declines are small in magnitude, the fact that weakness persists in a range of components means the economy is lowering its resilience. The index direction is as it has been in periods in the past when underlying pressures built before turnpoints manifested in headline growth figures.

From an investment perspective, the recent correction provides value plays in the defensive stocks, while some industrials are offering value on valuations grounds now being priced to longer-term earning power. We will be watching closely the follow-on series of employment and production reports to determine if July’s softness is a deeper correction or starts to stabilize in the face of looming monetary policy shifts. CFNAI is again an important leading indicator, and sustained weakness here will be an early indicator of rising systemic risk.

Growth Estimates Signal Potential Slowdown

The most recent economic figures reveal clear downshift in rate, with GDP growth forecasts returning from a previous 2.0% to 0.7%. These updates reflect the effect of trade tensions and doubt around tariffs, which still affect business and consumer sentiment. Confidence indicators declined commensurate with the revisions and reflect households second-guessing expenditure behavior amidst weaker prospects for growth. Overall, these revisions paint a fragile economic situation at a time when global headwinds are still extant.

They are guided by historical precedent. Extended GDP growth declines, and more so when accompanied by softer sentiment and labour indicators, have had a tendency to presage wider downturns within 6–12 months. Previous studies correlating individual quarters’ snap growth declines—like the recent 1.3% rate decrease in annualised Q2 rates—to recession risk are support to the proposition that markets could underestimate the severity of the slowdown. Higher equity valuation and softer real economy indicators result in elevated volatility risk without rapid expectations re-pricing.

On an equity valuation perspective, defensive stocks are still comfortably covered but hopes are in a handful of consumer discretionary stocks which are oversold but still have robust demand profiles. These are trading below their earnables and will benefit potentially if monetary policy is eased to make up for softness in growth. Analysts will need to watch whether such data released onwards again slow down and stabilize around current levels because this will become important when creating positioning across cyclical and defensive allocations. It will also be important to watch developments surrounding tariffs due to the threat of them fuelling or diluting downside risks.

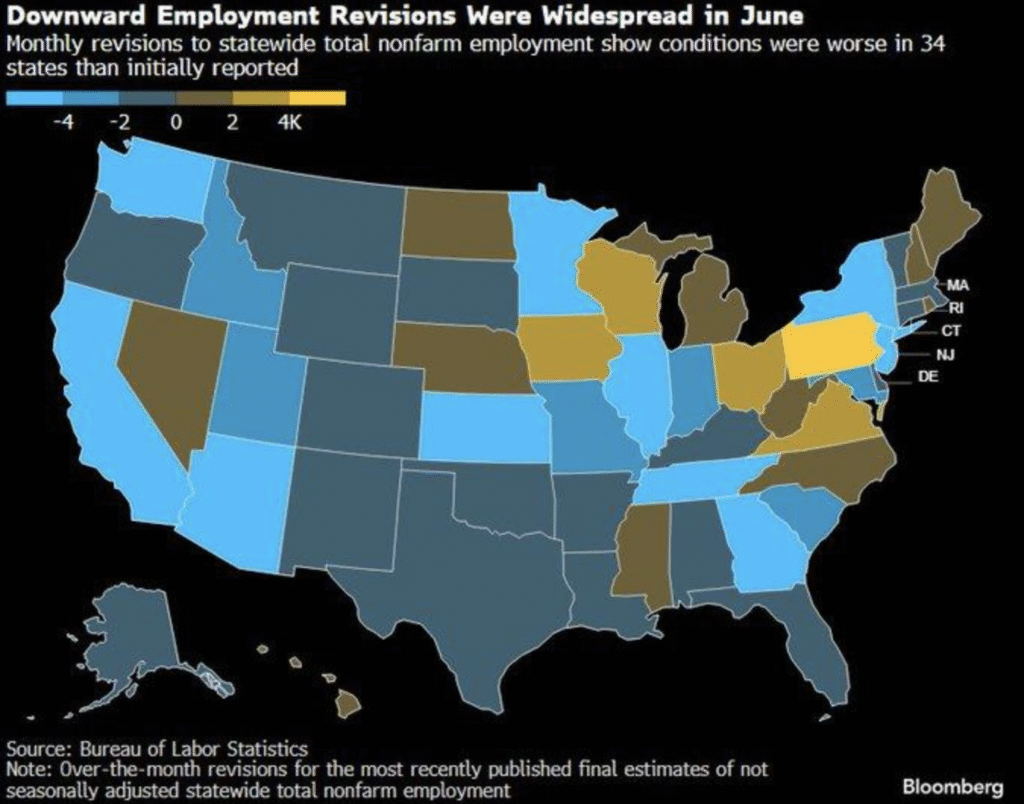

Job Market Revisions Weaken Job Creation Narrative

June 2025 revisions to labor data showed 34 American states collectively reported 258,000 fewer jobs when initially estimated, a softer labor background than initially believed. These are typical revisions the Bureau of Labor Statistics conducts when fresh information is received from businesses and government organizations. The signal to markets is clear-cut: the figures taken face value overstated momentum and subsequent revisions profoundly change perceptions of economy strength when growth driver employment is concerned.

The past record indicates such adjustments are far from trivial. There is an academic paper that has suggested initial estimates of employment growth are being revised by 70% in subsequent months because of seasonals trouble and because of survey data incompleteness. This is suggestive of requiring interpreting early readings with care, since employment rates are prone to drastic revisions. These downward revisions are thus pertinent to interpreting persistence of consumer expenditure, because household incomes and the labour markets continue to be central to the continuation of economic growth.

Revised estimates have also raised political attention, and recent demands for responsibility at statistical agencies a reflection of frustration at the perceived uniformity of economic reporting. For investors, however, concern needs to remain an analytical one: if revised estimates of job growth are too optimistic, the risk is that company profits estimates and policy moves are founded on overly rosy assumptions. We believe some consumer discretionary stocks are value priced, with valuations having already factored in softer demand for labour. Analysts will need to monitor upcoming employment revised estimates, with successive downgrades potentially continuing to dampen market confidence and position into defensives.

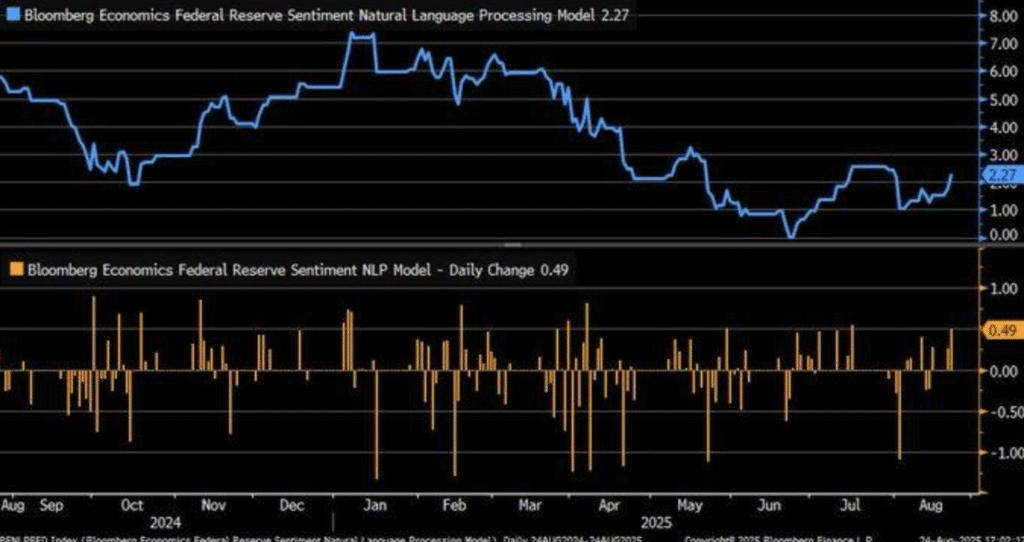

FED Sentiment Model Records Hawkish Shift

The Bloomberg Federal Reserve Sentiment NLP Model increased by 0.49 points on August 22, 2025, the biggest single-day move in 2025. The move came after Chairman Jerome Powell’s Jackson Hole speech, in which repeated reference to price stability signaled a return to inflation fighting at the expense of labour-market worries. For markets, the model reading takes uncertainty out of the equation: direction of policy is tilting hawkish, with implications for yield, equity, and risk appetite.

History’s record is in favor of prudence. Mathematics has calculated that an increase in interest rates of 0.25% typically reduces GDP growth by 0.1% over a year, and illustrates a trade-off in sacrificing growth in order to combat inflation. Powell’s warning is that the Fed will be prepared to tolerate slower growth in order to regain credibility on inflation. The hawkish bias therefore undermines the more dovish market expectation that had ruled out cuts later this year, and poses repricing of rate-sensitive assets.

The usefulness of the model to investors lies in measuring sentiment and not tone interpretation, cutting through Fed messaging speculation. Reflecting a numerical policy change and not verbal subtlety, it is a warning that markets will have to adapt to a more higher-for-longer universe. Valuation-wise, financials with better balance sheets continue to be discounted, as they will benefit from extended higher rates, while growth-sensitive equities will again be on sale. Analysts will have to keep future Fed messaging and economic prints close at hand, as the sentiment model’s present index reflects a clear policy stance change.

Upcoming Economic Event

Core Durable Goods Orders, Durable Goods Orders, CB Consumer Confidence, Richmond Manufacturing Index

Ahead of the next leg of Fed policy markets, week-ahead economic calendars are packed with data points that will swing sentiment and repricing views. As a group, these indicators are a gauge of a primary reading of household sentiment, business expenditure, and the world of manufacturing—all of which will determine whether investors pour into risk or defensives. This is the primer to what’s important and where above- and below-forecast shifts will impact markets:

Core Durable Goods Orders month/month

Core orders are transport-free and are a clean measure of business expenditure across equipment, machines, and technology.

- Better-print is to interpret that companies are willing to incur capital despite high cost of borrowings, a reflection of optimism in the demand outlook down the line. It is then to sustain equities in the industrials and capital goods sectors, and lift Treasury yields with improved growth opportunities through.

- Slower-than-anticipated number, however, will show business expenditure softness and lend support to the easing momentum tale. Markets will subsequently rotate into defensives like utilities and consumer staples, and the dollar can weaken on weak growth prospects.

Durable Goods Orders m/m

The reading in durable goods gauges broad demand among core producers and is most closely linked to cyclical momentum.

- A beat is an indication that commercial and consumer customers are still spending, which will support rallies in cyclicals and push equities higher. Even tighter demand, however, will once more kindle inflation fears of a more pervasive nature, pushing yields higher as investors re-price the Fed’s need to cut rates.

- A miss to the soft side will confirm faltering demand in core sectors such as autos and aerospace, feeding recession fears and flows to Treasuries and gold, with manufacturing-linked equities suffering the worst damage.

CB Consumer Confidence

The US economy is built on consumer confidence and this report will therefore be monitored closely for signals of shifting household opinion.

- Better than forecast will affirm the belief that consumers are still robust and this will boost retailers, discretionary shares, and travel stocks. Strength in confidence, however, can equally fuel inflation concerns should households still spend robustly despite cost of financing that is more expensive.

- Weakness in the print, however, will signal caution and this will mean households cutting back spending because of tighter credit and increasing cost of living. This will weigh down equities overall and fuel safe-haven buying of bonds and the dollar.

Richmond Manufacturing Index

This local measure is a proxy for industry health and is frequently a bellwether of national performance.

- Up surprising here can indicate manufacturing weakness is ebbing and lifts shares of industrials and materials sector. It may also alleviate concern generated by softer regional surveys elsewhere.

- However, a softer-than-anticipated reading will solidify weakness already shown by sector and support risk of recession and drag on cyclicals and highlight defensive exposure.

Collectively, these reports can reboot stories. Better data will sustain hopes of recovery, lifting cyclicals but will make it harder to switch to rate cuts. Low levels will reinforce slowdown fears, ignite safe-haven buying, and drive speculation of easing sooner than anticipated. Analysts’ focus is to monitor not headlines but detail since a mixture of sustained demand and increasing cost is the key driver of markets during the month of September.

Stock Market Performance

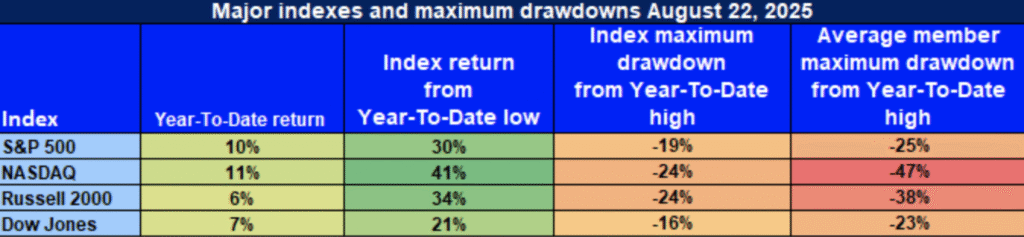

Indexes Bounce Back from April Lows, But Narrow Breadth Indicates Continued Cautiousness

US shares kept returning hard from the April 8 trough, and this year’s performance of the major indices has been solid. But beneath the surface, it isn’t quite so rosy—drawdowns remain gigantic, so strength in the market still remains disproportionately concentrated in the name-brand caps and not diversifying across the board. One reason that even in the midst of double-digit turnarounds, caution remains necessary from an investment perspective is due to the discrepancy between strong headlines and anemic internals.

Below is our detailed overview of recent performance in top indexes:

📈 S&P 500: Headline Gains, Narrow Participation

YTD: +10% | +30% below April low | -19% from YTD high || Avg. member: -25%

The S&P 500 is 10% above 2025, helped along by a 30% recovery from early April. Even so, though, the benchmark is 19% below the high and benchmark member 25% below its high. This again reflects narrow advances, with leadership extremely narrow and concentrated around a handful of leading large-caps, and the overall market still having to come back from lost territory.

🚀 NASDAQ: Tech-Led Gains Mask Fragility

YTD: 11% | 41% below April low | 24% below YTD high | Avg. member: -47%

The NASDAQ is the undisputed winner, 11% up to date this year and 41% from the lows in April. Yet the index is still 24% away from the high, and 47% average member declines are a measure of the extreme bifurcation of the technology and growth stocks. Though megacaps has propelled the index to a fresh high, a titanic percentage of underlying stocks are still in the red and question the sustainability of the move until there is more widespread support.

📊 Russell 2000: Small-Caps Struggle to Regain Confidence

YTD: +6% | +34% below April low | -24% from YTD peak | Avg. member: -38% The Russell 2000 is 6% higher year-to-date and a 34% April increase is a signal of swift in’s and out’s of the small caps. Yet a 24% correction from tops and a 38% collective member fall suggest muted sentiment still. Responsiveness to funding rates and the state of the U.S. economy is still dampening sentiment, a signal of weakness of small-cap reversals in a high-rate regime.

Dow Jones: Comparative Strength through Defense Angle

YTD: +7% | +21% below April low | -16% from YTD high | Avg. member: -23% The Dow has registered a 7% 2025 return, a 21% recovery from its low in April. Its relatively subdued 16% fall from the high of the year implies the safety provided by its defensive tilt, although median constituent declines of 23% reflect even veteran value teams are not exempt from general market stress. Relative strength in the index implies it acts like a kind of safe haven when volatility is high, though breadth is still shallow.

In Zaye Capital Markets, we notice that while indices-level advances are wonderful, successive pullback of mainstream components masks basic weakness. Big rallies will eventually come through by participation in general, and so far as that will not come through, selectivity is the catchword—picking names with solid earning support, healthy balance sheets, and lesser reliance upon speculative flows. Breadth indicators will continue to play a key role in converting recent reversals into a broad-based sustained uptrend in the markets.

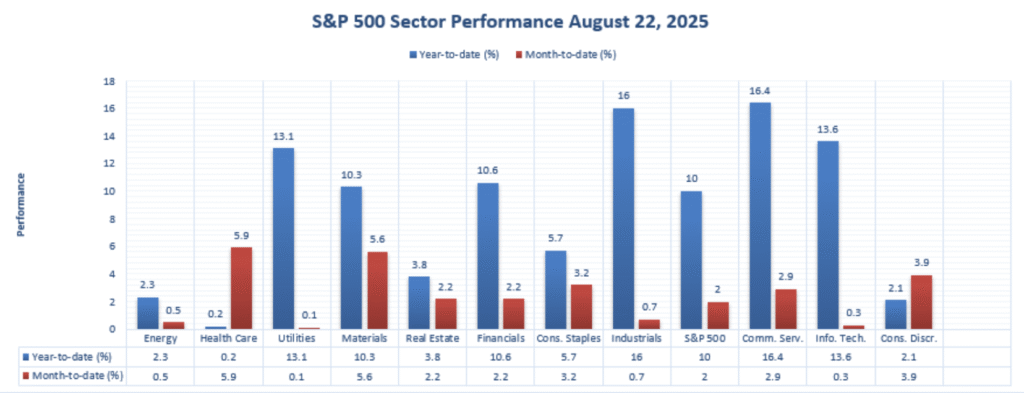

Strongest Sector In All These Indices

Communication Services Take the Lead

Communication Services has so far been the leading sector this year with a return of 16.4% this year and 2.9% so far this month. This has been because of the strength of the sector emanating from sustained demand for internet and digital platforms, media, and communications services. This month so far performance persuades that investors’ sentiment is still robust regardless of general volatility and varied sector participation in other spaces of the overall markets.

Comparing Sector Performance

The other areas remained robust but trail Communication Services. Industrials had a robust 16.0% YTD rise but muted 0.7% MTD growth, which is a slowdown of momentum. Information Technology rose 13.6% YTD but just 0.3% in the previous month, a consolidation of earlier gains. Utilities rose sharply too at 13.1% YTD, but zero MTD gains show defensive flows having stabilized.

What Makes Communication Services Different

The ongoing outperformance of the group is one side of its twin personality: growth potential combined with defensiveness to provide earnings size and resilience. As a contrast to tech, where outperformance is focused in a narrow band of megacaps, Communication Services’ more widely-based source of strength is a better read of healthier participation. Both YTD and recent momentum outperforming all other groups, Communication Services has built the 2025 foundation of performance in S&P 500 and the most unequivocal source of relative strength across the board.

EARNINGS

Yesterday Earnings Recap: August 25, 2025

- PDD Holdings Inc. (PDD)

PDD delivered revenue of CNY 103.98 billion (~$14.5 billion), a 7% year-over-year increase and well above estimates. However, adjusted operating income dropped 21% as higher fulfillment and merchant incentive costs weighed on profitability. Earnings per ADS came in at ~$0.77, significantly below forecasts of ~$2.16, highlighting that while demand remains strong, margins are being squeezed as the company battles competitive pressure.

- HEICO Corporation (HEI)

HEICO posted a record-setting quarter with net income up 30%, operating income up 22%, and net sales up 16%. EPS reached $1.26 versus $0.97 a year ago, supported by revenue of $1.15 billion, a 15.7% increase. The aerospace and defense company continues to benefit from industry tailwinds, with strength in both its flight support and electronic technologies segments. Robust profitability reinforces HEICO’s role as a sector outperformer.

- Semtech Corporation (SMTC)

Semtech reported Q2 FY 2026 revenue of $257.6 million, a 20% increase year-over-year, alongside adjusted EPS of $0.41, both exceeding expectations. Importantly, management has sharply reduced net leverage from 8.8× to 1.6×, improving balance sheet resilience. Strong demand in data center and IoT LoRa segments fueled results, underscoring the company’s strategic positioning in high-growth digital infrastructure markets.

Today Earning Preview: August 26, 2025

- MongoDB, Inc. (MDB)

MongoDB is set to release Q2 FY 2026 results with analysts expecting revenue near $553.5 million, up around 22% year-over-year. EPS is projected in the range of $0.62–$0.66 compared with $0.70 a year ago. Investors will focus on whether revenue momentum can offset near-term margin pressure, particularly as the company continues scaling AI-embedded offerings within its developer ecosystem.

- Okta, Inc. (OKTA)

Okta is scheduled to announce Q2 earnings today, with consensus forecasts pointing to EPS of ~$0.84 and revenue of ~$711.8 million. The identity security provider sits at a critical inflection point as demand for cybersecurity solutions remains strong. Markets will be closely monitoring forward guidance and customer growth metrics to determine whether Okta can sustain momentum in a competitive sector.

- Atour Lifestyle Holdings Limited (ATAT)

Atour reports Q2 2025 earnings before market open, with estimates calling for EPS of ~$0.41 on ~$328 million in revenue. This would represent year-over-year growth of 34% and 32% respectively. The company has built momentum through expansion in managed hotel revenues, and investors will look for confirmation that this trajectory can be maintained amid broader macro uncertainty.

- Box, Inc. (BOX)

Box will release results after market close, with projections of EPS at ~$0.15 and revenue around $290.2 million. While this reflects modest year-over-year growth, the focus will be on margins and forward guidance as competition in cloud content management intensifies. Strong cost discipline and subscription growth will be critical to sustaining investor confidence.

Stock Market Recap – Tuesday, August 26, 2025

U.S. equities began the day under fresh duress as investors weighed political risk against interim earnings catalysts. The Nasdaq Composite and the S&P 500 declined as the tech sector continued to feel pressure, with the Dow Jones Industrial Average and Russell 2000 also declining, as the sensitive breadth of the market continued to set the tone. Sentiment remains skittish as investors weigh the direction of the Fed’s policy against escalating geopolitical risk.

Stock Prices

Geopolitical Trends and Economic Data

Political risk and risk-off macro position are the current drivers of the sentiment in the markets. Trump’s demand for Fed Governor Lisa Cook’s resignation has fueled the fear of independence of monetary policy and equity and bond volatility. But investors are waiting for new prints of consumer sentiment and durable orders that can either solidify the slowdown theme or trigger a near-term relief pop. geopolitical tension is another risk overlay and defensive flows even in a rising yield environment.

Current Stock Updates

The rebalancing into the S&P 500 was newsworthy when Interactive Brokers ($IBKR) took the place of Robinhood ($HOOD) and SoFi ($SOFI), the losing parties being retail-focused platforms. Besides, AI stocks continue to be in the limelight with investors searching into exposure to data centers by revenue. Leader is Nvidia ($NVDA) at 58%, followed by Taiwan Semiconductor ($TSM) and Broadcom ($AVGO) at 15% and 12% respectively. AMD ($AMD), Marvell ($MRVL), Micron ($MU), and Arm ($ARM) complete the roster with much less but increasing roles. This kind of concentration implies that performance in the S&P 500 is correlated to a group of AI leaders, implying that these are more vulnerable to the market should momentum ease.

The Magnificent Seven and the S&P 500

The “Magnificent Seven” of Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla remain weak and the group has so far absorbed more than an 18% correction from recent peaks. Tesla and Meta are leading the weakness, a byproduct of valuation correction in growth stocks having gone well beyond fundamentals. Nvidia still has a glow due to dominance from AI but upcoming earnings is sending investors into a tizzy. Without buy support from these megacaps broadly, the S&P 500 is still vulnerable and still living off narrow leadership during periods of mounting volatility.

Major Index Performance To Tuesday, August 26, 2025

- S&P 500: Current price is 5,842.47, decreased 0.4% today

- Nasdaq Composite: Fell 0.6% to 18,220.78, led by weakness in large

- Dow Jones Industrial Average: 41,182.34, off 0.2%, as defensive shares did not make any gains in a broad-based

- Russell 2000: 2,147.63, flat for the day, and related to rate sensitivity with small-cap stocks.

We are disciplined at Zaye Capital Markets, preferring high-quality stocks with solid balance sheets and predictable sources of earnings. As political anxiety looms over monetary policy steering, the re-shuffling in the S&P 500 inducing shocks, and tech-led dominance under pressure, sector moves and momentum in AI are studied closely to determine to what extent markets are able to stabilize into September.

Gold Price

As of August 26, 2025, gold is at approximately $3,384 per ounce, with SPDR Gold Shares (GLD) at $309.83, modestly down by 0.24%. It is a two-week high in bullion prices amid mild intraday weakness propelled by renewed inflows to havens. Political risk is in the spotlight with President Trump’s firing of a Federal Reserve governor having raised concern about central bank independence and spurred flows into gold. Added to this is his inflammatory comments on Ukraine, NATO, and South Korea, pushing geopolitical risk premiums. With this backdrop, gold is boosted by a weakening U.S. dollar and risk-off tone in equities, spearheaded by mega-cap technology softness.

In the offing are today’s core durable goods orders, Durables headlines, CB consumer confidence, and the Richmond manufacturing index, which are key indicators. Weaker-than-expected prints will build risk aversion again, to the benefit of gold as a hedge to political and economic uncertainty. Upbeat data will contain defensive flows, capping upside gains, as capital will sooner or later move into equities and cyclicals. Weaker economic indicators in manufacturing and confidence yesterday already indicated the weakness in growth again to the benefit of bullion’s stabiliser role in portoflios. Gold’s direction for now still rests still on the tug-of-war of geopolitical tension and coming macro data, ensuring it will stay firmly seated as a haven anchor amidst volatile markets.

Oil Prices

Until 26 August 2025, WTI crude is $64.46 a barrel and Brent $68.47, both off by approximately 0.5% as markets compensate for the risk of oversupply and changing demand prospects. OPEC+, of course, already raised August shipments by 548,000 barrels a day above previous output estimates, and the IEA states world stocks remain high to cap prices even though Goldman Sachs has raised its Brent estimate for the second half of 2025 to $66. WTI, though, is projected by the EIA to average $66 in July and fall to $59 end of year with rising supply building. This shows the fragile equilibrium of the market: supply growth is running a step ahead of flat demand with crude vulnerable to the first whiff of a further rise in output.

Comments from President Trump from urging direct diplomacy in Ukraine to growing criticism of South Korea piled on geopolitical risk that normally benefits oil, but weakness in economic data is moderating that impact. Yesterday’s weakness in confidence and manufacturing readings contributed to demand concerns, prompting defensive action on energy markets. End-of-day data tomorrow—the durable goods orders, consumer confidence, and Richmond Manufacturing Index—will be interesting; softer prints will have a potential to ignite the demand slowdown theme, pulling oil lower, while strong ones will support sentiment. For now, oil ranges in an unruly world marked by oversupply, political risk, and data-led demand to the safest haven with prices somewhere in the middle of structural barriers and episodic flows.

Bitcoin Prices

The cryptocurrency is currently at $109,895, losing close to 3% of value on the second day after it moved from an intraday high of $113,364 to an intraday low of $108,951. Recent weakness follows a “whale” liquidation of around 24,000 BTC that suddenly pulled the exchange rate from an area around $117,400 to an area around $111,200, sucking the momentum out from a strong summer-month rally. Institutional investors like Strategy Inc. are still accumulating aggressively—adding more than 3,000 units this week and taking holding above 632,000—yet the overall marketplace is nervous. Technical charts are now trending bearish, and here the cryptocurrency is being propped up just above a critical support area around $110,000. President Trump’s recent remarks on Ukraine diplomacy, NATO cooperation, and geopolitical tensions in south Korea are set to add weight to the argument of Bitcoin’s safe haven status; but here such headlines were dominated by the liquidity impact from concentrated on-chain selling and left sentiment on tenterhooks. Wednesday’s weaker U.S. consumer confidence and manufacturing numbers continued to erode risk appetite and solidify bearish pressures in already anxious crypto assets after a dovish message from Fed Chairman Powell earlier in the week. Such reports corroborated fears that weaker growth would put a lid on speculative assets, and Bitcoin traded to that risk-off script. Near week-end, today’s U.S. durable goods orders, Richmond Manufacturing and CB consumer confidence will be crucial in dictating near-term flows. Weaker-than-expected readings could stimulate fears of weakness in demand and bring down Bitcoin as investors seek refuge in traditional haven assets such as gold and U.S. Treasuries. Better-than-expected readings, on the other hand, will indicate strength in the U.S. economy and potentially stabilize sentiment and propel fresh inflows into cryptocurrencies. Until then, however, Bitcoin is stuck in a precarious balancing act of whale-spurred technical pressures, macroeconomic risk from data, and geopolitical noise—keeping volatility high and leaving it extremely reactive to forthcoming headlines.

ETH Prices

Ethereum is currently at $4,408, down by some 7% so far today after falling from an intraday high of $4,754 to an intraday low of $4,330. The correction follows a liquidation frenzy which rolled over more than $838 million of leveraged exposure of which the ETH component was approximately $296 million. Although the deep correction has indeed taken place, Ethereum is still more than 30% higher this year and a reflection of the underlying strength and structural integrity of its ecosystem. Meanwhile, this past week’s breakout to a four-year high of virtually $4,954 was supported by optimism regarding Fed policy signals and increasing institutional adoption, but the deep correction again highlights how exposed ETH still is to general macro stress and liquidity shocks.

Institutional flows and whale movements continue to dictate Ethereum’s destiny. One such whale recently exchanged nearly $2.6 billion of Bitcoin for Ethereum, building up around 473,000 ETH before unwinding positions to take profits, yet still dictating $108 million of spot buys. In the meantime, a $1.25 billion staking deal for ETH has constricted circulating supply, and is an affirmation of long-term dedication by large holders. Of note, record one-day spot ETH ETF inflows in excess of $1 billion are an affirmation of expanding institutional adoption. These drivers seem to imply that while ETH remains vulnerable to near-term volatility from macroeconomic data and liquidations, structural demand from whales, staking, and ETF inflows are cementing the place of Ethereum as a pillar digital currency, and will recover as soon as risk sentiment stabilizes.