Where Are Markets Today?

European and U.S. futures register mixed direction today as markets respond to a mix of regulatory updates and economic concerns. The futures of S&P 500 climbed 0.2%, and Nasdaq-100 futures indicated a 0.3% gain. Conversely, futures of Dow Jones opened down by 57 points, or roughly 0.1%. This mixed market sentiment is largely led by encouraging updates for the technology space on top of wider worries over growing bond yields and economic expansion. The surge in technology stocks, led by Alphabet (Google), climbing over 7% after a positive court ruling for its antitrust suit, is contrasted with flat performance in other industries. By contrast, the overall market remains cautious, pressured down by growing bond yield effects, with 10-year treasury rising to 4.27% and 30-year exceeding 4.97%.

The recent court ruling in Alphabet’s favor, which enabled it to keep its Chrome browser but with limitations on exclusive search arrangements and data sharing, brought optimism to the tech world. It skirted the bottom line for Alphabet, thereby reinforcing confidence among investors in the sector. Further, Apple, whose profit flows from its profitable search arrangement with Google, saw its shares jump by more than 3%. These events have brought a positive trigger for the technologies sector, although market sentiment is bivalent. Market players are equally struggling with the implications of the United States federal appeals court ruling that most of President Trump’s world tariffs are unlawful, a ruling that might shake trade patterns and further increase volatility in markets.

The mixed tone is reinforced by September’s historic weakness for U.S. equities, a month that has averaged -0.7% for the S&P 500 since the 1950s. This introduces a dose of caution for market players, with profit-taking after the summer rally possible. The prognosis for the U.S. economy is mixed with market players considering implications of possible changes in tariffs and a decelerating jobs market. Economic data from yesterday, led by the JOLTS Job Openings release, indicated a tighter jobs market, implying robust American demand, and would be supportive of riskier assets. But uncertainty over trade policy and monetary policy remains overhanging for the broader outlook.

EU equity markets fall on rising bond yields, with European economies’ long-term yields in major world economies like the U.S. and U.K hitting multiyear highs. The Stoxx Europe 600 fell 0.5% in morning trade, with concerns over fiscal deficits and debt issues taking their toll on investor sentiment. Market participants are carefully monitoring upcoming economic indicators like European services figures and U.S. labor market reports to get an idea of how robust the economy is and to predict action from the central bank. A potential rate cut of 25 basis points is on most people’s radars, and it can throw markets a lifeline of sorts in terms of equities. But prior to that economic indicator being released, markets are likely to remain in limbo mode, fluctuating between positive trends for tech to overall economic concerns.

Major Index Performance up to Wednesday, September 3, 2025

- S&P 500: Trading at 6,415.54, down 0.69% on the day.

- Nasdaq Composite: Down at 21,279.63, -0.82%, led down by.

- Dow Jones Industrial Average: Rose 0.2% to 45,295.81, led by advances for bank and energy shares.

- Russell 2000: Flat at 2,352.21, underperforming due to rate sensitivity in small caps.

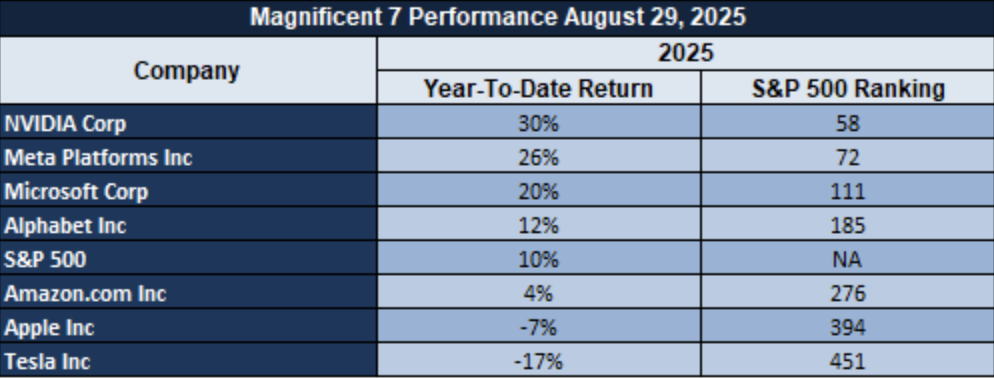

The Magnificent Seven and the S&P 500

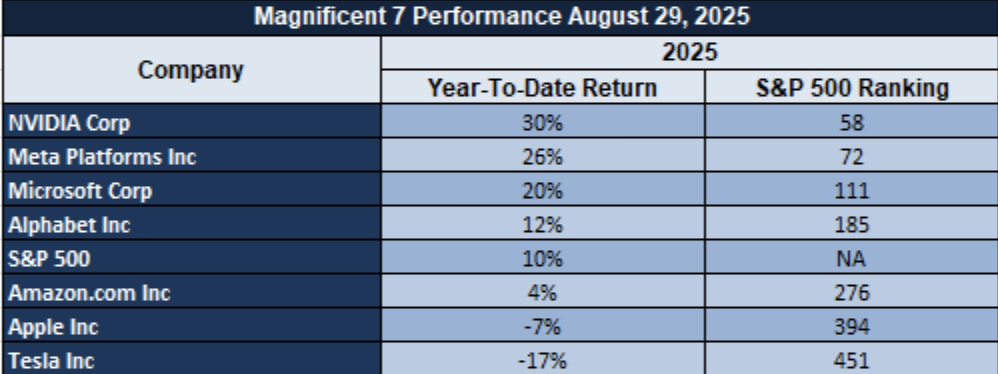

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are looking tired. A recent sector split reveals the cohort to be averaging a more than 18% drawdown from their recent peaks, led down by Tesla and Meta. It’s a sign of valuation rebalancing, particularly in AI-led growth narratives that have gotten ahead of their fundamentals. The S&P 500 continues to struggle with leadership from technology while energy and industrials are providing a little support, but it won’t sustainably rally without new leadership from its major mega-cap stalwarts.

Drivers Behind the Market Move – Wednesday, Sept. 3, 2025

Global markets are off to a mixed start to the day with mixed feedback from recent economic indicators, geopolitical events, and market sentiment. U.S. futures are up on a thin margin with futures of the S&P 500 rising 0.2% and Nasdaq-100 futures rising 0.3%. Futures for the Dow Jones Industrial Average started down by 57 points, or close to 0.1%.

1. Uncertainty over Tariffs and Trade Tensions

A recent ruling by a federal appeals court that most of President Trump’s world-wide tariffs are unlawful has brought uncertainty to the trade arena. Although while the tariffs stand to October 14, in wait of a probable appeal to the Supreme Court, the ruling has unsettled investors and contributed to market volatility. President Trump has said that he plans to take an emergency appeal on the ruling over tariffs, suggesting that the administration is set on continuing its trade policy. These events added to a market cautiousness, with investors considering probable economic repercussions of trade tensions that last.

2. Rising Bond Yields and Inflation Jitters

Global bond markets saw a selloff, prompting higher long-term yields. In the United States, the 10-year Treasury yield has risen to 4.27%, and the 30-year yield breached 4.97%. Correspondingly, in the United Kingdom, long-duration bond yields hit multiyear highs, signaling concerns about fiscal deficits and augmented debt offerings. Rising yields are stoking concerns about inflation and stimulating higher costs of borrowing, and that would affect consumer spending as well as corporate income.

3. Economic Data and Market Sentiment

Markets are looking ahead to next economic indicators, such as the U.S. jobs report on Friday. The report would reflect normalizing labor markets after last month’s disappointing 73,000 jobs growth. European Central Bank President Christine Lagarde is also scheduled to speak, talking monetary policy for the ECB while worries about inflation remain. The two datasets will be integral to informing market perceptions of economic growth and monetary policy action by central banks.

Overall, markets are grappling with a busy agenda of trade policy uncertainty, higher bond yields, and major economic reports. Market players are taking it one step at a time, looking to other events that can provide clearer direction to market action.

Digesting Economic Data

The TRUMP Tweets and Its Implications

Recent comments and actions from the Trump administration can potentially affect many industries, particularly with geopolitical shifts and changes in economic policy. Perhaps most prominent was that of moving the headquarters of the U.S. Space Command to Alabama in order to strengthen military and space-related infrastructure in the state. Such would potentially bring more investment in defense and space companies throughout the area, possible job creation, and federal contracts with potentially lasting regional economic effects. The proposed move comes after greater focus from the Trump administration on beefing up military capabilities and seeing the United States front-and-center of the world space race once again. Defense- and space-related businesses like Lockheed Martin and Northrop Grumman might receive favorable market responses accordingly.

Correspondingly, Trump’s recent comments on the trade climate have generated added uncertainty, specifically with concerns over the current situation of tariffs with China. Although the Trump administration has avoided placing further tariffs on goods from China, throughout negotiations, uncertainty remains, with large implications for trade- and supply chain-dependent industries. Tariffs and trade restriction historically have brought mixed effects to market segments such as technology, retail, and manufacturing, with rising costs potentially being passed to end-consumers, with implications for total spending and inflationary figures. Trump’s comments on his ruling over tariffs, in that he attacked a decision of a ‘liberal court’ and referred to it being a ‘disaster,’ indicate that it is probable that its aggressive posture with China would be maintained by the administration. Repeated trade tensions might produce volatility in markets related to international trade and can potentially result in changes of investor sentiment and movements of market.

Additionally, Trump’s concern about skyrocketing electricity costs, reflected by his energy secretary, betrays growing unease about inflationary forces and their effects upon businesses and consumers. High energy costs are of great concern to businesses that are large users of electricity and fuel, such as manufacturing, logistics, and retail. Their increases could hit profit margins and economic activity hard, driving inflation further and informing Federal Reserve policy for interest rates. Oil giants such as Chevron and ExxonMobil would likely observe their stocks move in response to these concerns, depending upon whether policy standoffs taken by the admin lead to higher or better controlled energy rates. Trump’s latest plans, such as extending the military’s ambit and taking up energy issues, showcase his priority for national security and economic nationalism. While these steps also mirror the larger world problems, namely the effects of the Russia-Ukraine war, continuing to stress world trade and energy markets, uncertainty over these geopolitical and economic matters can trigger further market volatility, with markets like energy, defense, and technology still being center-stage of market responses. Market players must be vigilant and track developments carefully because Trump’s policy, coupled with world events, can send markets to unpredictable places.

U.S. Trade Deficit Widening – Implications for the Dollar

The trade deficit in goods in the United States has jumped sharply to $103.6 billion in July 2025 from $84.9 billion in June of that year. It is indicative of a growing difference between imports and exports that has been encouraged by strong demand for goods like automobiles and electronics from American consumers. With American consumers still encouraging such demand, such a difference is likely to persist. Strong GDP growth of 3.3% in Q2 of 2025 indicates renewed spending and confidence from consumers, widening the trade deficit further. In such a situation, stocks like Apple are attractive, undervalued opportunities. With its strong supply chain that it has around the world and strong persistent demand for its products, it is best positioned to weather trade imbalances that are likely to persist and take advantage of persistent spending from American consumers.

A National Bureau of Economic Research study in 2024 debunks the popular misconception that tariffs are to blame for trade deficits alone. While tariffs are hinted at having a role to play in certain industries, it is actually consumer patterns and macroeconomic forces that would ultimately determine trade deficit direction. American consumer spending, buoyed by stable economic growth, continues to drive the major trade-gap expansion. In parallel, the current-account deficit climbed to $450.2 billion in Q1 of 2025, with a 44.3% surge being recorded. This massive spike is a reflection of how a stronger dollar, having risen 5% across major currencies year to date, has swelled imports’ cost, contributing to further imbalances being recorded. Although tariffs may play a role in affected industries, it would be consumer patterns and macroeconomic forces that would ultimately control trade deficit direction. Tesla, with its strong export prospects and international coverage, continues to be a key stock to focus on in this regard. Looking ahead, further widening of the trade deficit could ultimately place downward pressure on the U.S. dollar’s value. In order to finance growing deficit spending, the U.S. must continue to attract foreign capital, something that could become increasingly elusive should investor confidence deteriorate. A weaker dollar raises import costs, reducing U.S. consumer purchasing power. Analysts should, therefore, watch out for possible currency shifts and their effects on inflation and spending patterns among consumers keenly. Microsoft is one of the few names that stand out in such regard, with its globally extremely diverse revenue base being both a possible currency risk hedge and source of stability in times of uncertainty.

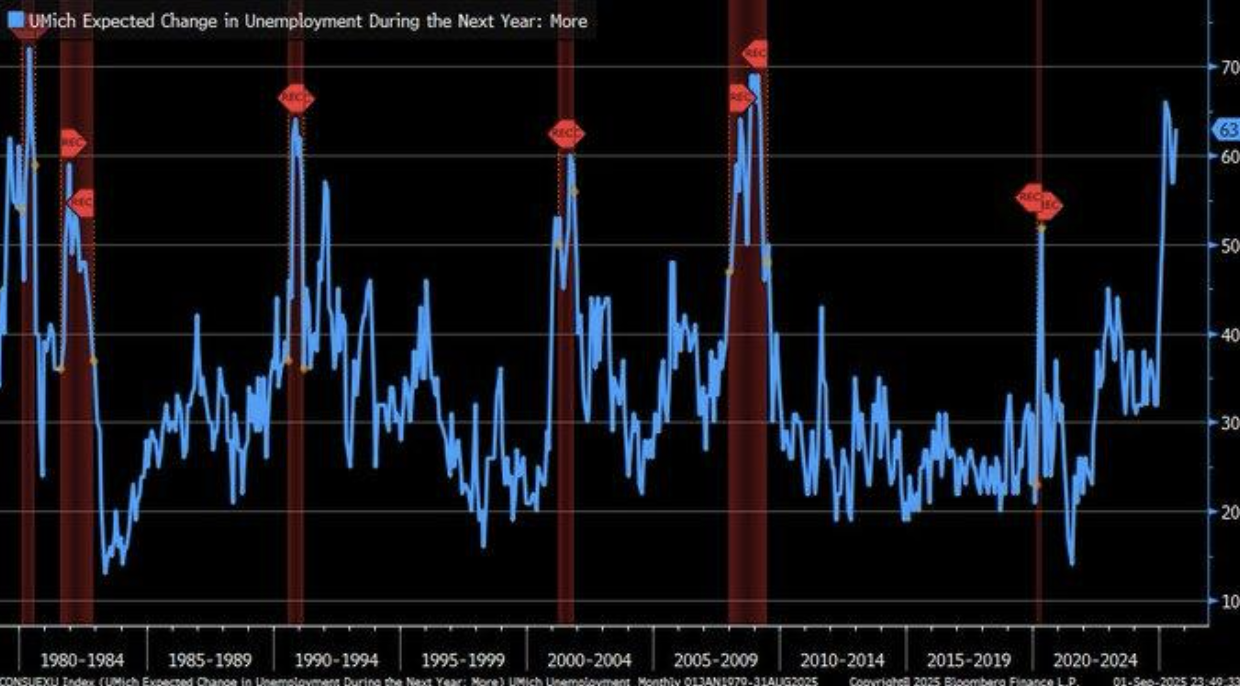

Consumer Sentiment Reflects Economic Uncertainty

In August 2025, consumer expectations of rising unemployment surged to 63%, according to the University of Michigan data, approaching the cycle high seen during the 2008 financial crisis. This sharp increase in unemployment fears signals heightened economic anxiety among consumers, suggesting that sentiment may be influenced by media-driven narratives. Historically, such sentiment shifts have often preceded economic slowdowns, particularly when negative news stories amplify fears of a downturn. As these expectations rise, Meta stands out as an undervalued stock in this environment, given its significant role in shaping consumer sentiment through its platforms.

A study by Alyt Damstra and Mark Boukes (2021) in The Economy, the News, and the Public finds that bad economic news affects public expectations considerably, noting that media-fueled narratives can greatly shape perceptions of the economy (p = .028). It debunks conventional wisdom that sentiment surveys do not predict. With media frequently presenting economic narratives negatively, heightened unemployment expectations by the public might reflect real economic threats in addition to media power to influence consumer behavior. For analysts, monitoring media sentiment in conjunction with economic indicators might offer essential insights into future market directions. Tesla, with its market leadership and innovative edge, might be better equipped to sail through such uncertainty than most. In the past, increases in unemployment expectations tended to precede actual jobs market downturns after a delay, such as with the 2008 recession. The University of Michigan Consumer Sentiment Index has regularly demonstrated a several-month lead interval between increases in unemployment anxieties and subsequent economic downturns. If that tendency persists, then the recent advance would be warning of a recession for late 2025 and would be of great importance for analysts to consider labor market indicators and changes in sentiment. Microsoft, with its ubiquitous presence and multiple revenue streams, might prove to be a relatively safe bet with heightened economic concerns, deriving comfort from stable demand for its cloud platforms and software products.

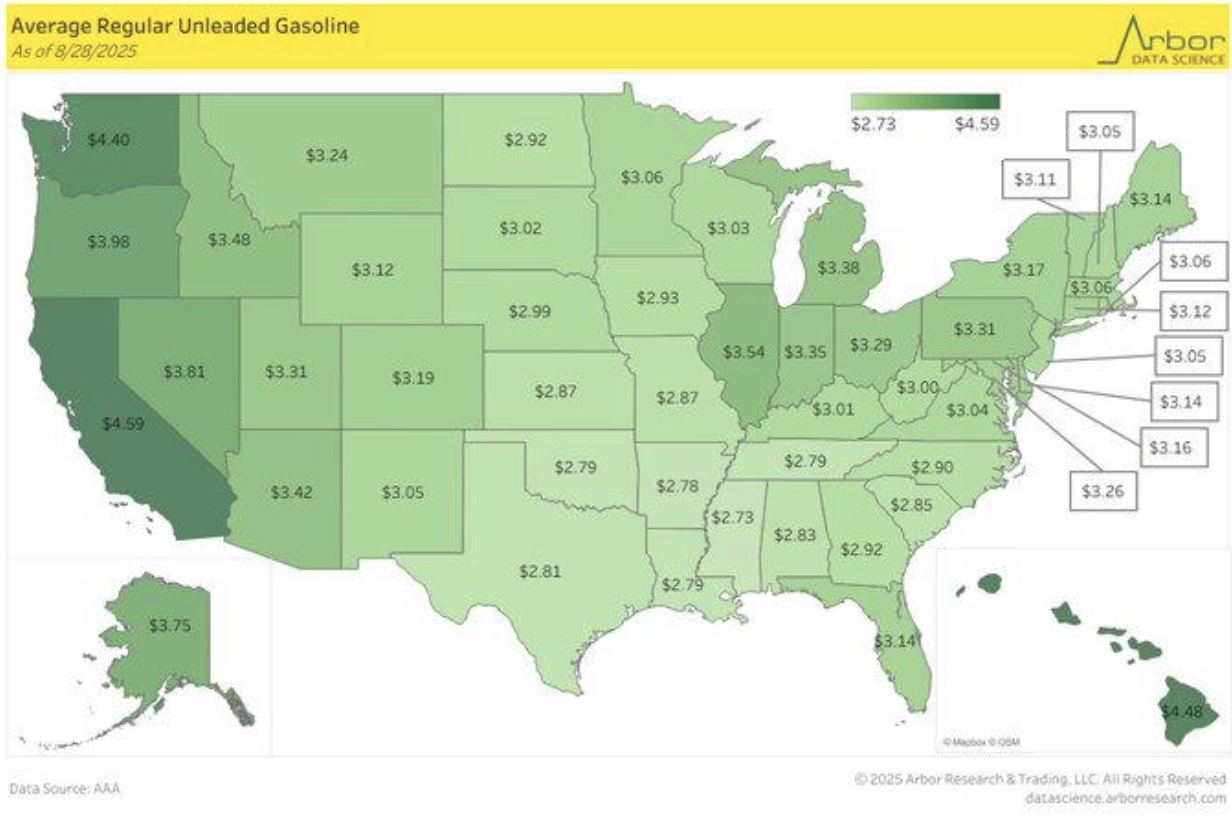

Petrol Prices and the K-Shaped Recovery

California has the highest gas price in the country at $4.59 a gallon in late August 2025, a stark contrast to the national average. Such a spike in price is largely attributable to a mix of state taxes, over 70 cents a gallon, and refining bottlenecks. According to a National Bureau of Economic Research study from 2023, California’s demand for special fuel formulas raises gas prices by 30-40% over national benchmarks. With such hefty costs in consideration, Chevron, California’s most prominent energy market player, might be considered an undervalued stock in such a high-cost market, while it enjoys local demand regardless of tighter margins from higher costs.

Unlike these, states such as Hawaii and Washington face equally elevated gas rates of $4.48 and $4.40, respectively. These are largely due to geographical seclusion and logistics difficulties. In a 2022 University of Hawaii study, it was noted that shipping fees contribute approximately 25 cents a gallon to the gasoline cost, making it costlier for island states to gain access to gasoline. Back on the continent, such states as Mississippi enjoy low rates of $2.78, demonstrating a regional contrast. This difference in price reflects the role of local economic forces, such as infrastructure constraints and geographical location, upon costs for the consumer. Analysts would do well to observe keenly regional differences upon local consumer demand and stock market activity, with that of ExxonMobil potentially gaining from its larger network of distribution. The regional price disparities reflect a broader trend of a “K-shaped” economic recovery, with high-priced states confronting inflationary forces while low-priced states face more modest price increases. Federal Reserve figures from 2021 onwards has shown regional price indices to diverge from one another, contradicting the narrative of a comparable economic recovery from the outbreak. The divergence means thatconsumers from high-priced states could face more economic hardship, with possible implications for spending patterns. For investors, Apple, with its strong presence throughout high-priced regions like California, could face probable spending slowdowns by consumers. Its strong brand identity and product variety can, however, cushion it from these regional changes.

U.S. Personal Savings Rate Decline – Implications for Consumer Behavior

The U.S. personal savings rate has fallen sharply from a record of 33.8% in April 2020 to a level of 4.4% in July 2025, marking post-pandemic change. The decline represents a dissipation of stimulus-fueled savings in response to growing inflation and a consumer spending surge. Based on Federal Reserve (FRED, St. Louis Fed) data, with a recovering economy, consumers have increasingly moved from saving to spending, most likely because of living cost pressures. While overall down, stocks such as Microsoft and Tesla, with returns tied to technology and consumer-demand growth, might still demonstrate strength in response to low consumer savings.

4.4% savings rate matches historic 70-year average but masks massive gaps across income ranges. In a study from the National Bureau of Economic Research released in 2023, low-income households saved less than 2%, while higher-income households saved at 6-8%. The difference reflects uneven economic growth, with higher-income households still being able to save while many low-income households being forced to spend at higher rates. For investors, companies that cater to higher-income households, such as Apple, may still receive robust demand while companies that rely on mass-market popularity may receive sluggish growth because spending behaviors differ. The continuation of a low savings rate regardless of persistent economic uncertainty implies that consumer confidence or necessity spending is playing a key role. The recent base rate cut by Bank of England to 4% in August 2025 reflects a monetary policy direction globally that might also impact U.S. consumer spending patterns. Global economic conditions, such as shifts in interest rates, might be decreasing the motive of U.S. consumers to save, picking up spending further. With ongoing inflationary pressure, Amazon might be a stock to look out for, with its wide consumer coverage placing it in a position to gain from the spending trend that persists, particularly in necessities goods.

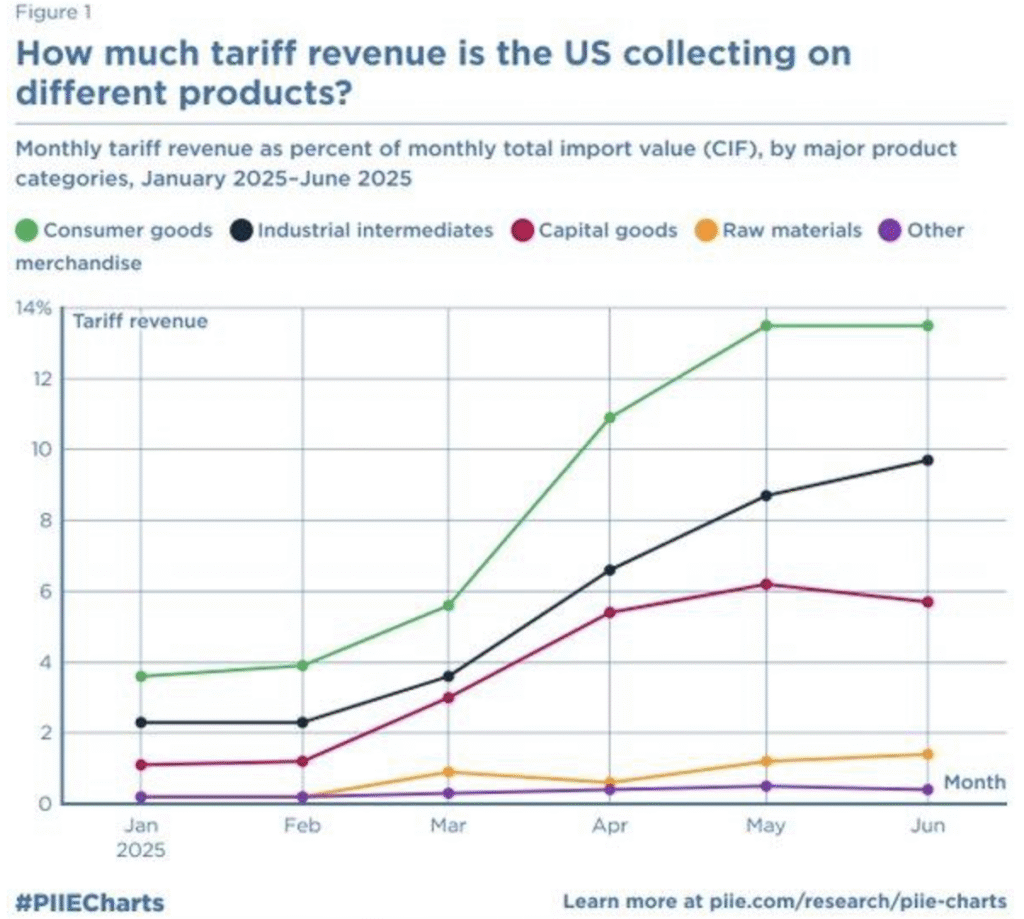

U.S. Tariff Revenue Boom and Consumer Goods Repercussions

During the first half of 2025, U.S. tariff income from imports surged sharply, with consumer goods, like electronics and apparel, earning most of the revenue—up to 14%. The trend reveals the changed policy direction of tariffs in the Trump era that was heavily concentrating on daily consumer imports. Based on Peterson Institute for International Economics (PIIE) data, tariffs for such goods now meaningfully contribute to U.S. treasury revenue, defying conventional wisdom that tariffs serve most to protect American manufacturing. Industrial companies like Apple, depending on U.S. buyers and world supply chain logistics, can feel hurt from these tariffs, primarily if consumer prices increase.

PIIE finds that tariff revenue affects consumer prices after several months because importers absorb the initial cost of tariffs before passing it to consumers. A Federal Reserve Bank of Atlanta study from 2025, with the help of Numerator data, discovered that a 25% increase in tariffs on products from Mexico and Canada saw a 1.63% increase in prices. This implies that although tariffs increase revenue in the United States, their end result on consumer prices spreads out over time and can have huge implications for consumer spending patterns and even inflation. In our case, Tesla can be considered an undervalued stock because it has something to gain from robust demand regardless of possible increases in imported goods costs. Historically, tariffs targeted raw materials and manufacturing intermediates, but newer United States International Trade Commission data show a trend, with imports of consumer goods exceeding manufacturing industries in their fiscal impact for the first time. In January 2025 imports of consumer goods hit $89 billion, marking a paradigm shift in United States trade policy. Analysts would be well-advised to monitor such a shift’s impact upon broader patterns of inflation, particularly across industries that are consumer-facing. Amazon, with its massive coverage of consumer products, would end up with a larger cost of operation because tariffs would permeate its supply chains, but its market dominance would potentially buffer its impact.

Coffee Prices and Supply Chains Disruption

U.S. ground coffee prices jumped 33%, from $6.31 in July 2024 to $8.41 in June 2025. The steep jump is mainly caused by world supply shocks, such as Brazil’s consecutive droughts that cut coffee production by 10-15% annually since 2023, a 2024 USDA report showed. Prices are further pushed up by recent tariffs imposed in September 2025 by President Trump that target major producers of coffee such as Vietnam (46% duty) and Indonesia (32% duty). The tariffs cause supply chain disruptions, contributing to cost pressure already experienced by the coffee sector. Starbucks, highly dependent on coffee imports, can expect its profit margins to be pinched by increased costs, a stock to watch for analysts in view of these disruptions.

Recent reports, like a 2025 KXAN report, find that the tariffs, together with supply shocks, again spawn further cost increases for the coffee market. In contrast to prevailing assumptions that popular inflation remains the sole source of growing costs, a 2023 Agricultural Economics report argues that commodity-specific factors like climate and trade policy account for up to 60% of coffee price fluctuations. This defies simplistic thinking that demand from end-consumers alone is to blame for growing costs. Analysts would do well to consider how such supply chain issues, together with tariffs, can again drive volatility in coffee costs. Companies like PepsiCo, with its large stake in the coffee market through its brands, can potentially reap mixed effects, with growing costs offset with cost-saving measures. The recent increase in coffee prices is also a reflection of a broader trend in coffee production dynamics. With world supply being controlled by mainstream coffee-producing titans like Brazil, recent production setbacks have promoted shifts to other territories for coffee production. In such a situation, analysts must take into account how such changes affect future directions in prices and market flows. With further spikes in price, companies like McDonald’s that derive coffee sales as a large source of revenue can adjust their models of pricing to balance rising costs while ensuring customer demand endures.

US PCE Price Index – Inflation Patterns and their Economic Implications

The U.S. Personal Consumption Expenditures (PCE) Price Index has remained above 2% for 53 months, extending to July 2025, signaling persistent inflation that tests the Federal Reserve’s 2% goal. This over-long inflationary run that began in early 2021 and extends to mid-2025 is indicative of continued economic growth and supply chain bottlenecks. Ever since PCE became the favored inflation indicator for the Fed in 2000, its broader coverage of substitutions has made it a better indicator of inflation than its better-known successor, the Consumer Price Index (CPI), according to Investopedia. In spite of it, however, the ongoing trend of inflation for once indicates economic duress, taking its toll on both end-consumers and businesses. Nvidia, with its vulnerability to technology and semiconductor industries, can be poised to gain from inflation’s ongoing effects on demand for technology and artificial intelligence.

Although PCE Price Index offers a broader picture of inflation by taking substitutions made by people in reaction to price changes into account, recent figures reflect a decline in the chart for 2024-2025, similar to aggressive monetary tightening. In a 2024 Office for Budget Responsibility report, Bank of England increased its base rate to 3.5% to tackle inflationary pressures. It would indicate a possible stabilization phase from these tightening measures that are being matched by similar ones from the United States Federal Reserve, although economic uncertainty across the world might further impact inflationary pressures. Analysts need to watch these interest rate increases carefully to observe their broader market behaviors. A good stock recommendation in such a situation would be that of Apple, since its strong international presences coupled with its premium pricing policy help mitigate inflationary pressures. The PCE metric’s capacity to reflect inflation beyond the core CPI indicator better paints a picture of economic conditions. Even with that clearer picture, however, inflation continues to affect sectors unevenly. Although the downward incline of inflation in 2024-2025 presents a silver lining, continued uncertainty in consumer price volatility remains a major area of concern for companies in all sectors. Tesla, operating in a price-sensitive market, would likely face difficulties in implementing cost increases to consumers without denting demand. Analysts must remain cautious in monitoring PCE together with other measures of inflation to determine if the economy has indeed entered a stabilization phase.

U.S. Labor Market Resilience During Global Uncertainty

Through September 2025, the American labor market remains robust with a 4.2% unemployment rate and a slight 0.2% increase in nonfarm payrolls. These numbers, reinforced with figures from the U.S. Census Bureau’s established surveys, indicate that the labor market remains strong with respect to persistent global economic uncertainties. Although growth in employment endures, significant differences consist of a 62.2% quit rate and a 1.8% depreciation in job openings that might indicate that workers feel either more assured to pursue other jobs or discontent with their jobs. It is in line with a National Bureau of Economic Research study from 2023 that discovered that elevated quit rates are commonly connected to wage growth pressures in strong labor markets. Corporations like Amazon, with large workforces and high turnover rates, must be carefully followed throughout the period because the high quit rate can result in wage competition.

The quit rate and jobs openings reflect a nuanced reality of the labor market, in that while overall growth persists, workers increasingly enjoy greater bargaining power because of tightening labor conditions. The elevated quit rate might reflect wage inflation demands by workers looking for better remuneration or better terms of employment. This has prompted companies to receive increased wage demands across several industries, hiking operating costs for firms. Analysts need to monitor companies that are sensitive to labor costs, like Walmart, because they might find it necessary to revise compensation schemes just to hold on to staff. It is accordingly of importance for gauging future inflationary indicators in the U.S. economy. With a backdrop of a 10.1% year-to-date S&P 500 gain up to September 1, market resilience remains intact according to the labour market figures. Unfortunately, September has historically represented a month of volatility for American equities with average downswings since 1950. This creates uncertainty that disrupts the theme of continuous bullish market trends. By contrast to European markets, with slower rates of labour market improvement and elevated unemployment, American markets still lead the pack. For American investors, while the American equity market might still hold out promise, volatility possible in September cautions prudence. Tesla is something of a possible play, with its diverse market coverage and distinctive business model potentially cushioning risks from possible market volatility.

Shrinking US Factory Due to Tariff Pressures

August 2025 ISM Manufacturing PMI increased modestly to 48.7, its sixth month of contraction for American factories. The reading bucked growth forecasts, further solidifying manufacturing sector distress. New orders did increase to 51.4, however, to signal a possible reversal in spite of contraction. Data shows Trump-era tariffs’ toll that still squeezes U.S. manufacturing, with sharpest impacts accruing to industries depending most heavily on imported raw materials and parts. Industrial giant General Electric might get pricier with rising tariff costs that impact its supply chain, further threatening its own reversal chances in a decelerating manufacturing market.

Historical figures indicate that with a PMI level below 50, economic contraction is ahead, and the increase in the “prices paid” index to 63.7, while employment dipped to 43.8, reflects stagflationary patterns from the 1970s. In that period, supply shocks and accommodative monetary policy propagated inflation without growth to show for it. This situation, described in a 2025 Wikipedia article on stagflation, reflects how tariffs and supply chain shocks are worsening inflationary forces. The increase in consumer prices without manufacturing output growth poses major risks for companies and households alike. Market analysts must watch stocks such as Caterpillar, which are responsive to inflation and broader industrial degrowth. Institute for Supply Management and Washington Post research shows that tariffs and continued supply chain interruptions are behind the manufacturing slowdown, challenging the myth that protectionism fortifies local production. Data reveals that while tariffs might save specific industries, tariffs also increase costs for consumers as manufacturers transfer the cost of tariffs to consumers. Prices go up, contributing to inflation with no resultant economic growth to show for it. Ford Motor, which imports most of its parts, might suffer because costs get transferred to its end-use consumers. Further, analysts must monitor continued trade tensions globally because continued trade war might further disrupt world supply chains and affect U.S. manufacturers and world trade flows.

Upcoming Economic Events

ECB Head Lagarde Testifies, Monetary Policy Report Testimony, JOLTS Job Openings

With further changes to come in the financial landscape, key future events are set to elicit strong market responses that can alter investor attitudes and shape monetary policy from the central banks. With major speeches from ECB President Christine Lagarde, hearings related to recent Monetary Policy Report, and highly anticipated JOLTS job openings scheduled for release, markets are primed for surprises that can impact anything from currency flows to stock valuation. Here’s a rundown of these major events and likely market implications by result:

ECB President Lagarde Responds

ECB President Christine Lagarde’s speeches are never without focus for investors looking ahead to European monetary policy’s future direction.

- If Lagarde is more hawkish, indicating aggressive measures to battle inflation or a potential tightening of rates ahead of schedule, the euro would be strengthened. A strengthened euro might put a squeeze on Eurozone exports and corporate profits but would draw capital flows from those looking for better returns in Europe. Moreover, higher rates might bring up the cost of borrowing, which could weigh negatively on regional growth prospects. Conversely,

- if Lagarde speaks more dovishly, indicating a continued emphasis on economic growth or that rate increases would be slower-paced, look for risk assets to respond positively, with investors looking ahead to a friendly environment for stocks and bonds. The euro might soften on such a move, with dovish signals often leading to discouraging capital flows in. The tone of Lagarde’s speech might send out rippling effects for European stocks, the euro, and risk appetite among investors.

Monetary Policy Report Testimony

Monetary Policy Report hearings are one of the most important windows for gauging the U.S. Federal Reserve’s view of the current economic environment.

- If the real data out of the hearings is indicative of a better-than-expected inflationary scenario or a better economic rebound, expect markets to prepare for tighter monetary policy. The consequence would be rising bond yields as investors price in rising interest rates and would squeeze equity markets, especially growth and technology markets that are sensitive to rising borrowing costs. A bolder tone from the Federal Reserve might also result in a stronger dollar, with capital flowing into dollar-denominated assets seeking better returns.

- If the hearings signal that inflationary forces are easing or economic growth is sluggish, investors might interpret the Federal Reserve’s view as more dovish. A less aggressive course of tightening might fuel a risk-asset rally, sending equities up and bond yields down. This would likely dent the U.S. dollar as low-interest-rate expectations become reality.

JOLTS Job Openings

The JOLTS Job Openings report is one of the most important labor market indicators providing investors with significant insight into job demand strength and possible wage pressures.

- If the actual number of job openings comes out better than forecast, it would confirm persistent demand for labor, showcasing strength in the American economy. It would result in positive market sentiment because investors would consider it proof of a strong jobs market, meaning that consumers are still confident and spending aggressively. Nevertheless, it would also increase worry about inflationary wage pressures because strong demand for employees would drive wages upward, prompting the Federal Reserve to become more aggressive with respect to interest rate policy.

- Conversely, if job openings would disappoint market expectations, it would reflect weakening demand in the labor market, foreshadowing economic activity slowdown and prompting investors to flock to safe-haven assets like bonds, with possible flight to safe-haven defensive sectors like healthcare, utilities, and consumer staples, with growing concerns about economic deceleration. It would depend on how investors weigh their worry about rising inflation with that of decelerating jobs growth to respond to it.

Stock Market Performance

Indexes Recover from Lows of Apr, But Basis of Weakness Is Obvious

The major U.S. indexes have mounted a remarkable comeback since the low of April 8th, 2025, but underneath, stress indicators never really go away. Although the headline returns are encouraging, a closer look at maximum drawdowns and average constituent losses reveals a far more tenuous situation. In our view at Zaye Capital Markets, it further supports attention to selectivity, leadership within sectors, and risk management throughout further market sector rotation.

Below is a more detailed breakdown of recent index-level performance:

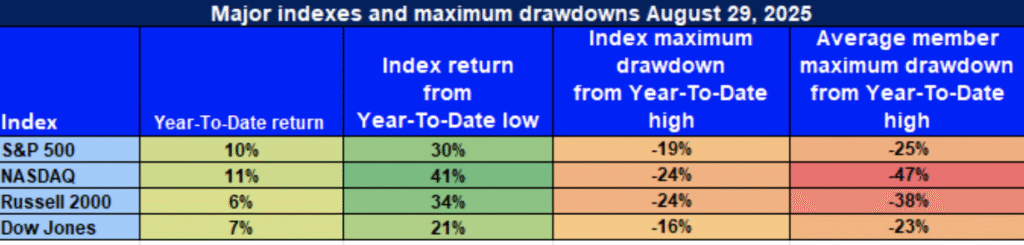

S&P 500: Headline Strength, But Breadth Still Weak

YTD: 10% | 30% Apr low | -19% from YTD high | Avg member: -25%

The S&P 500 has risen 10% year to date and risen 30% from its low in April, showing strength at the headline level. But from its high, the index has fallen 19%, and its constituents, on average, have fallen 25%, indicative of how focused in a select few stocks has the recent rally been. The absence of broader participation in that rally underscores its vulnerability because while strength remains narrowly concentrated among a few heavyweights, it is led most predominantly in specific industries—namely, technology—investors need to be extremely discriminate in their stock selection because other parts of the market can still be struggling.

NASDAQ: Powerful Recovery, but Members Significantly in Red

YTD: 11% | 41% of Apr low | -24% of YTD high | Avg. member: -47%

The NASDAQ is still ahead at the index level, having appreciated 11% year to date and rebounded a stunning 41% from its low in April. But below that, serious internal scarring can be identified. The average constituent of the NASDAQ is down 47% from its high, gaining a glimpse of the losses many technology and growth-sensitive stocks have incurred. While the index has seen a sharp spike in its big names, its overall poor performance remains symptomatic of sector problems, with ongoing concerns over rising rates and valuation stress still being dominant. Here, investors need to look to identify strong growth names in the technology sector, with volatility continuing to plague the overall sector.

Russell 2000: Small Caps Lag Despite Recovery Bounce

YTD: 6% | 34% of Apr low | -24% of YTD high | Avg member: -38% Russell 2000 has risen 6% year-to-date, marking a 34% rally from the lows in April. Even with that gain, however, the small-cap space has stayed very challenged, down 24% from its high and with a 38% average drawdown. The result highlights the continued struggles of small-cap stocks because these players are acutely responsive to macroeconomic downturns like higher interest rates and tighter liquidity. Even with the recent bounce from its low, small caps haven’t fully benefited from broader market upswings, and that divergence represents a warning sign that investors should exercise caution before embracing such exposure.

Dow Jones: Value Bias Exhibits Relatively Stability

YTD: 7% | 21% below low of April | -16% from year high to date | Avg. member: -23% The Dow Jones Industrial Average has exhibited modest strength, rising 7% year-to-date and 21% from its low in April. Its modester 16% drawdown and restricted 23% average member decline indicate that value stocks have offered stability to a certain extent in the face of overall market fluctuations. The Dow’s bias toward value stocks, especially those such as financials, healthcare, and consumer staples, has protected it from the more spectacular fluctuations that are witnessed in growth-biased indices such as the NASDAQ. Even though the performance of the Dow is fairly stable, it is essential to understand that its outperformance to a large extent can be accredited to its defensive bent and concentration on established businesses that offer strong dividends and revenues.

We remain focused on identifying quality sector leadership while being disciplined with risk management. While momentum is gaining strength at a broader index level, missing persistent breadth and continued dispersion of drawdowns are of utmost relevance to watch out for. Due to this ongoing market rotation, it is all the more critical to be vigilant and evidence-based in our investing strategy, with risk management and selectivity in stock picking being the focal points. In the times to come, it’s critical that investors are disciplined, watching keenly which sectors and stocks are actually driving the reversal, and which ones might be lagging behind.

The Strongest Sector in All These Indices

Communication Services Leads the Pack in 2025 Sector Performance

With our progress through 2025, sector-level S&P 500 performance has shown some definitive leadership patterns. Out of 11 sectors monitored, Communication Services was the top-performing sector, outgaining its peers considerably. With its sector experiencing stunning returns for its year-to-date (YTD) period and still taking the lead, it is clear that this sector is being aided by changing consumer behaviors and changing models of business.

Communication Services: Clear Outperformer

YTD: 17.2% | Month-to-Date: 3.6%

Communication Services has recorded a robust 17.2% year-to-date return and a further 3.6% August alone gain, to stand as unequivocal sector performance leader. The outperformance is led by several fundamental factors: a return to digital advertising growth, rising demand for streaming services, and unabated dominance of platform-oriented technology firms across social media, gaming, and content delivery. Key players across the space, such as Meta, Alphabet, and Netflix, have benefited from shifting end-use behaviors and rising expenditure across digital advertising. Overall outperformance betrays market affinity for scalable, high-margin digital business models with exponential growth potential in a growing more connected world. With further innovation and expansion ahead, little sign of slowdown appears for the sector.

Industrials: Quiet Strength Behind the Scenes

YTD: 15.1% | Month-to-Date: -0.1%

The industrials followed suit with a 15.1% year-to-date return, although it has had a minor setback of -0.1% in August. In spite of that minor slip, it remains one of the standout contributors to the S&P 500’s returns in 2025. The industrials category is aided by robust demand for infrastructure, construction, and manufacturing, not to mention governments globally making strides with spending on infrastructure. Its constituent companies such as Caterpillar, 3M, and Union Pacific are among those still riding that tailwind, explaining why it has performed solidly. The recent setback in August, however, implies that the sector is likely going through a spot of consolidation after having performed tremendously over large parts of the year. Analysts would do well to monitor these companies, especially those most dependent on supply chains globally, since supply chain interruptions are likely to affect their near-term growth prospects.

Information Technology: Resilient but Slowing

YTD: 13.6% | Month-to-Date: 0.3% Information Technology remains a strong performer with a 13.6% YTD return, but its rally has slowed of late. The sector saw only a modest 0.3% increase in August that could mark it for a consolidation phase. Although stocks in the space still bask in long-standing themes of artificial intelligence, cloud, and digital transformation, short-term concerns such as elevated interest rates and supply chain issues may be taking their toll on performance. Apple, Nvidia, and Microsoft have stayed resilient, but with further maturity of the space, growth rates may start to decline. The investor must remain vigilant for potential headwinds such as regulatory trouble and increased competition in fundamental markets that can take their toll on sector performance over the short term.

We at Zaye Capital Markets are keen to watch for sector rotation because it provides fundamental insights into directions that investors’ interests are shifting. Leadership for Communication Services reflects investors’ interests in internet platforms and scalable businesses that are set to win out over traditional sectors over the short to medium term. However, industrials and Information Technology cannot be ignored in driving broader market strength, and investors cannot overlook their potential for future growth ahead. By watching for sector leadership and looking at broader market forces, investors can position themselves for upcoming trends for 2025.

Earnings

Earnings Recap: September 2, 2025

- Zscaler Inc. (ZS)

Zscaler delivered impressive fiscal Q4 results, surpassing analyst expectations with adjusted earnings of $0.89 per share and revenue of $719.2 million, marking a 21% year-over-year increase. The company also reported a 32% rise in billings to $1.202 billion. Looking ahead, Zscaler forecasts fiscal 2026 revenue between $3.27 billion and $3.28 billion, exceeding the consensus estimate of $3.21 billion. This upbeat outlook and strong growth in key metrics suggest that Zscaler is well-positioned in the cybersecurity space, which has experienced heightened demand amid growing security concerns across industries. The stock rose 4% in after-hours trading, reflecting positive investor sentiment.

- Nio Inc. (NIO)

Nio reported Q2 2025 revenue of $2.653 billion, a 9% increase year-over-year, though it missed analyst expectations by approximately $102 million. Despite the revenue miss, Nio’s vehicle deliveries were strong, with 31,305 units delivered in August 2025. The company has continued to see solid demand for its electric vehicles, especially in its home market of China. However, the revenue miss raises concerns about profitability and margin pressures, particularly as the EV market becomes increasingly competitive. Investors will closely monitor Nio’s ability to scale production while maintaining margin stability in the coming quarters.

- HealthEquity Inc. (HQY)

HealthEquity reported Q2 FY26 revenue of $325.8 million, a 9% increase from the previous year. Net income rose 67% to $59.9 million, and non-GAAP net income per share increased 26% to $1.08. These results highlight the company’s strong position in the health savings account (HSA) space, which continues to see growth as more consumers take advantage of tax-advantaged healthcare savings options. The positive financial performance and raised full-year guidance indicate a solid growth outlook, positioning HealthEquity as a leader in its niche market.

- Signet Jewelers Ltd. (SIG)

Signet Jewelers reported Q2 FY26 earnings per share of $1.61, surpassing the consensus estimate of $1.24 by 29.8%. Revenue came in at $1.54 billion, exceeding expectations. The company raised its full-year EPS and sales guidance, signaling confidence in continued growth despite macroeconomic challenges. The jewelry retailer is benefiting from strong consumer demand for both engagement rings and luxury items, suggesting that the demand for premium products remains resilient. Investors will be looking for continued strong performance in the second half of the year, especially during the holiday season.

Earnings Preview: September 3, 2025

- Salesforce Inc. (CRM)

Salesforce is scheduled to report its Q2 FY26 earnings after market close. Analysts are particularly focused on updates regarding the company’s AI initiatives and how they are contributing to revenue growth. Salesforce has been heavily investing in AI-powered features across its suite of customer relationship management (CRM) tools. Any developments in this area will be critical for assessing future growth potential. Investors will also be looking for guidance on how Salesforce plans to maintain its growth momentum as competition in the cloud space intensifies.

- Hewlett Packard Enterprise Co. (HPE)

Hewlett Packard Enterprise is set to release its Q3 FY25 earnings after market close. The company has seen strong growth in its server business, driven by the increasing demand for AI-related infrastructure. Analysts will be seeking confirmation of this trend, particularly as demand for high-performance computing (HPC) continues to grow. Any updates on HPE’s full-year guidance will be key in determining whether the company can maintain its strong growth trajectory. Additionally, investors will look for insight into the company’s strategic investments and cost-saving initiatives.

- Figma Inc. (FIG)

Figma is expected to announce its Q2 FY25 earnings after market close. As a leading design platform, Figma has seen substantial growth in recent years. Investors will be focused on revenue growth and profitability, especially given the company’s increased investments in research and development. Any updates on user growth, product adoption, and customer retention will be important for understanding the company’s long-term prospects. Figma’s ability to monetize its platform effectively will be a key area to watch in the earnings report.

- Dollar Tree Inc. (DLTR)

Dollar Tree is scheduled to report its Q2 FY25 earnings before market open. Analysts are expecting earnings per share of $0.40. The company has been facing margin pressures due to rising costs, so investors will be closely watching same-store sales growth, cost management strategies, and any impacts from macroeconomic factors on consumer spending. Dollar Tree’s ability to maintain its value proposition while managing cost pressures will be crucial in determining how the discount retailer fares in a challenging economic environment.

Stock Market Update – Wednesday, Sept. 3, 2025

The American stocks started September’s initial trading week with pressure, indicating investors worry over recent economic reports and geopolitical risk factors. The Nasdaq Composite and the S&P 500 dipped, while the Dow Industrial Average was stagnant. The Russell 2000 was still struggling with economic uncertainty.

Stock Prices

Economic Indicators and Geopolitical Developments

Market nervosity originates from a number of reasons. The American economy generated only 73,000 jobs in last July, below market forecasts, thus creating concerns regarding labor market strength. Additionally, President Trump’s imposition of trade tariffs on imports from other countries recently has elevated trade tensions further, subsequently contributing to market volatility. Such events made investors risk-averse, hence influencing market performance.

Up-to-Date Stock News

- $GOOGL | Waymo Starts to Test in Denver: Waymo, Google’s self-driving spinoff, has started to roll out its self-driving vehicles in Denver, with a launch of full service slated for next year. It is an important step for Waymo to expand its self-driving technology to new markets as it looks to scale up. A successful move would strengthen Alphabet’s leadership in autonomous space.

- $IREN | Bullish Option Interest: Iren (IREN) has caught investors’ attention with strong bullish option interest in the stock. It means that speculators believe there is still room for growth, either with positive sentiment or future news that can propel it further. Analysts would be eager to watch for company-specific events that can drive action.

- $ASML | Largest Winner from $TSM Waiver: The Amsterdam-listed semiconductor equipment maker, ASML, has been considered a largest winner from Taiwan Semiconductor Manufacturing Company’s (TSM) recent exemption on 12/16nm semiconductor technology. The dominance of ASML in the EUV (extreme ultraviolet) lithography market has further enhanced its geopolitical clout, particularly as chip demand for advanced chips grows globally. With its monopoly over EUV machines supply, ASML stands to gain from the continuous effort to miniaturize chip manufacturing nodes, with each step down the curve going through its monopoly. This gives ASML a strategic edge as chip manufacturing rivalry escalates globally.

- $FSLR | Solar Panels, $TSLA | Home Stack, $EOSE | Grid-Scale Storage: It’s all about new innovative collaborations for the future of the energy space with First Solar (FSLR) producing the solar panels, Tesla (TSLA) providing residential power products, and Eos Energy (EOSE) covering grid-scale storage. Together, all three companies are poised to capitalize on rising demand for new renewable infrastructure for energy with all of them playing a part in building out the future of energy transmission, storage, and deployment.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are looking tired. A recent sector split reveals the cohort to be averaging a more than 18% drawdown from their recent peaks, led down by Tesla and Meta. It’s a sign of valuation rebalancing, particularly in AI-led growth narratives that have gotten ahead of their fundamentals. The S&P 500 continues to struggle with leadership from technology while energy and industrials are providing a little support, but it won’t sustainably rally without new leadership from its major mega-cap stalwarts.

Major Index Performance up to Wednesday, September 3, 2025

- S&P 500: Trading at 6,415.54, down 0.69% on the day.

- Nasdaq Composite: Down at 21,279.63, -0.82%, led down by.

- Dow Jones Industrial Average: Rose 0.2% to 45,295.81, led by advances for bank and energy shares.

- Russell 2000: Flat at 2,352.21, underperforming due to rate sensitivity in small caps.

We are monitoring sector rotation and positioning strategies at Zaye Capital Markets with close attention as we move through earning season. Whether top companies can sustain their earning thrust with policy tightening on the horizon will set the direction for broader equity markets throughout Q3.

Gold Price – Wednesday, September 3, 2025

Gold jumped to a record high of $3,541.75 an ounce today from $3,477.54 yesterday after strong demand owing to anticipation of a rate cut by the Federal Reserve. It has been induced by a host of reasons such as a decreasing U.S. dollar, geopolitical tensions, and speculations regarding shifts in U.S. monetary policy. Market indicators are positive for a 25 basis point rate cut by the Fed on September 17, and there is expectation for a bolder 50 basis point cut depending on economic indicators. The depreciation of the dollar by 11% since President Trump’s comeback has made gold increasingly popular with foreign investors, and purchases by central banks, especially from China and India, further solidify it. In addition, Trump’s persistent pressure campaign over the Federal Reserve and its policy orientation creates indeterminacy in the market with investors hedging by switching over to safe-haven assets such as gold. Gold’s recent rally is also motivated by today’s economic releases, like ECB President Lagarde’s speech, Monetary Policy Report hearings, and JOLTS Job Openings report. If these releases give dovish cues, that can help maintain the gold rally because market demand is for loose monetary policy and softer rate hikes. If stronger-than-expected data is released and it shows that the Fed potentially can wait before lowering rates, that can curb the appeal of gold. Amidst prevailing economic uncertainty, like geopolitical risk and central bank activism, gold is still set to be a popular asset in today’s world. For that reason, gold’s price is set to stay on a rising trend because of these macroeconomic considerations and broader risk-off sentiment.

Oil Prices – Wednesday, September 3, 2025

Up to date, Brent Crude is at $68.98 a barrel, while West Texas Intermediate (WTI) is at $65.54 a barrel, up 2% ahead of next week’s OPEC+ meeting. The increase is caused by geopolitical risk and supply concerns, with recent interferences such as Saudi Arabia and Iraq’s suspension of oil sales to a sanctioned Indian refinery. Despite that, however, markets hold back because of continued oversupply and softening demand prospects. President Trump’s recent statements, such as imposing tariffs on Chinese imports and his deployment of his National Guard, bring about further ambiguities. Although directed at internal matters, these can cause instability to world trade and hence impact oil demand. Trump’s trade policy and geopolitical maneuvers can affect oil prices because they bring about disturbances to the world economic landscape, further muddling market prospects.

Yesterday’s economic indicators, led by the JOLTS Job Openings announcement, implied a tightening labor market that would suggest rising domestic demand and buoy oil prices in the short run. However, the recent prognosis of the International Energy Agency foresees an impending oil glut with sluggish growth of world demand and rising supply. Today’s economic indicators, such as ECB President Lagarde’s address and Monetary Policy Report hearings, will be anxiously followed to reflect economic slowdown or dovish monetary policy, offsetting oil demand prospects and placing downward pressure upon prices. Conversely, better-than-expected readings can reinforce confidence in economic growth, buoying oil prices. While these developments are followed by investors, oil prices are still guided by a cautious balance between supply fears and economic sentiment.

Bitcoin Prices – Wednesday, September 3, 2025

Bitcoin (BTC) trades at $111,227.90, rising 1.8% from the prior day. This jump comes after a short pullback to $107,500 earlier in the week, showing ongoing volatility in markets. Commentators are divided on whether or not Bitcoin would reach $125,000 or dip to $100,000 first, with many speculating likely gains to $116,000 should major resistive levels hold. President Trump’s recent comments and geopolitical initiatives, such as his intentions to relocate the Space Command headquarters to Alabama and his cabinet’s stance on Chinese tariffs, may indirectly impact the price of Bitcoin by having world trade and market sentiment implications. Furthermore, concerns of skyrocketing power rates, characterized by Trump’s energy chief, may pressure Bitcoin mining efforts, likely with supply implications for it.

Yesterday’s economic indicators, such as the JOLTS Job Openings report, suggested a tightening labor market that can reinforce Bitcoin’s value proposition as a diverse asset. But the Federal Reserve’s cautious tone regarding rate reductions creates uncertainty, as riskier assets like cryptocurrencies often do better with reduced interest rates. Economic data today, such as ECB President Lagarde’s address and Monetary Policy Report hearings, would prove determinant for market sentiment. Economic slowdown hints or dovish policy would likely curb Bitcoin’s value proposition as a hedge asset, placing downward pressure on prices. Better-than-expected readings, on the other hand, might reinforce economic growth confidence, making Bitcoin a more useful diversification asset for investors.

ETH Prices – Wednesday, September 3, 2025

Ethereum (ETH) was last trading at $4,327.50, down a modest 1.03% from its prior close. Even with that reversal, however, ETH has seen remarkable growth over the last month, rising 25% and hitting all-time high $4,956. Much of that has come from rising institutional demand, led most notably by Ethereum spot ETFs that took in almost $500 million in flows. Institutional demand is likewise helping to entrench Ethereum as a market leader in the realm of cryptocurrencies. Ethereum’s dominance is further augmented by its dominance of the realm of smart contracts, with large projects still building on the chain. A recent whale transaction also saw a whale stake $1 billion in Ethereum, swelling their holdings to 886,000 ETH, valued at over $4 billion. This transaction is a vote of confidence in Ethereum’s future growth prospects.

But even with strong bulls, a recent whale transaction of 3,819 ETH for an average of $4,286 indicates that profit-taking is being undertaken by some investors during the rally. Ethereum ETFs recorded $4 billion inflows in August, showing strong institutional demand, but such whale activity points to caution among some of the largest players in the market. With Ethereum still gaining in value, its price remains subject to market ebb and flow of whales and institutional sentiment. Market investors will keenly watch future economic reports and trends in ETF to determine if such a rally can be sustained or profit-taking takes center stage in the short term.