Where Are Markets Today?

U.S. and European stock futures began the week on a stronger note, with both regions factoring in mild increments. Dow futures rose more than 100 points in early morning trade before stabilizing around 20 points above, as S&P 500 and Nasdaq-100 futures inched into positive territory. European bourses also indicated a higher opening at the start of the day, paving the way for a positive Monday opening. The overriding driver has been Friday’s disappointing August payrolls release, revealing a mere 22,000 jobs added against 75,000 forecast, cementing expectations that the Federal Reserve will turn dovish and cut rates sooner, as opposed to later. This dovish turn in policy expectations is injecting a sense of support within risk assets internationally, while, at the same time, dampening yields and value in the U.S. dollar.

The potential for softer monetary conditions has been among the most powerful drivers underlying sentiment in both European and U.S. futures today. Markets now are factoring in all but absolute certainty on a 25-basis-point cut at the September FOMC meeting, and increasingly speculative talk of a steeper 50-point cut. This, as a negative for equity investors, means cheaper funding and potentially improved resilience in the area of earnings, especially in rate-sensitive growth and technology shares. European traders are in sync with the same narrative, considering how Fed easing could buttress world demand while offset domestic political risks, including strains in France and eurozone fiscal disagreements. Beyond the monetary backdrop, incoming catalysts are injecting further momentum into futures. Anticipation for Apple’s iPhone 17 launch this week has helped lift sentiment around technology shares, particularly given the outsized influence of mega-cap names on broader U.S. indices. In Europe, the resilience of exporters and industrials, coupled with an improvement in risk appetite tied to stabilizing energy markets, has bolstered futures pricing. Investors are leaning into these events as potential short-term boosts to momentum, though they remain mindful that macro volatility could resurface quickly if inflation surprises on the upside later in the week.

At Zaye Capital Markets, we interpret the current positioning as cautiously optimistic. Rate-cut hopes and tech catalysts are enough to support a firmer open, but the underlying fragility of labor data and persistent geopolitical risks continue to cap enthusiasm. For now, the futures rally reflects a balance of short-term optimism against long-term caution, with investors awaiting inflation data and central bank commentary to validate whether this momentum can translate into a sustained trend. Until then, discipline remains key, with quality names and defensive balance sheets better positioned to withstand any sudden reversal in sentiment.

Major Index Performances – Monday, September 8, 2025

- S&P 500: 6,472.4, down 0.3% on the day

- Nasdaq Composite: 17,860.6, down 0.5%

- Dow Jones Industrial Average: 45,499.0, up 0.2%

- Russell 2000: 2,377.7, up 0.5%

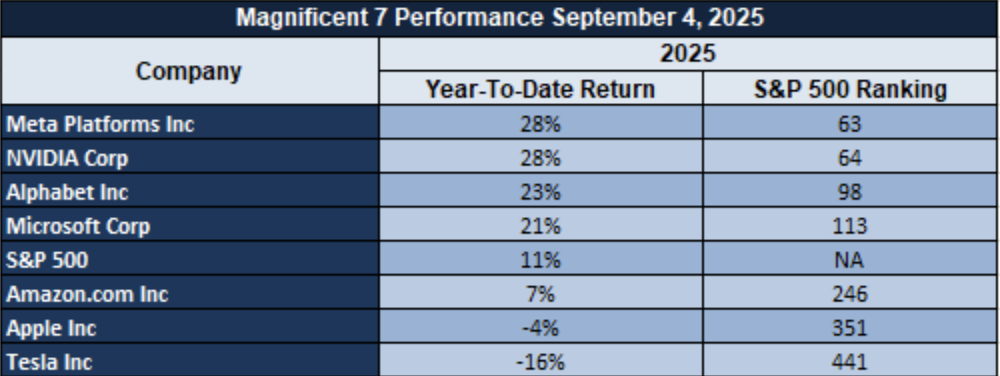

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—the Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla stocks—stay on a selling binge, with the lot in general trading down double-digit percentages from recent highs. Tesla and Meta remain the leaders in decline as valuations are adjusted on account of softer demand cues. This narrowing leadership is sustaining weakness in the larger S&P 500’s momentum, and defensives and selective cyclicals are left offering support. Absent buying participation by these mega-cap stocks, up legs are set to be feeble and spotty.

Drivers Behind the Market Move

Markets are currently balancing a batch of macroeconomic data, geopolitical risks, and monetary policy expectations. The three most influential drivers currently impacting both European and American markets are as follows:

1. Weaker Labor Market Brings Rate Cut Hope Back

Last week’s U.S. employment report delivered a major blow to market optimism, with just 22,000 jobs added versus the 75,000 forecast, and June revised into contraction (the first since late 2020). The unemployment rate climbed to 4.3%, its highest since 2021, reinforcing the view that the Federal Reserve will deliver a rate cut at its September meeting. Futures markets are now pricing in near certainty of a 25 basis point reduction, with a decent probability of a 50-point move. This spike in dovish sentiment has lifted both U.S. and European equity futures, depressed bond yields, and buoyed safe-haven assets like gold.

2. Geopolitical Risk and Trade Policy Risk

Trump administration commentary and executive moves ranging from immigration enforcement and defence rebranding through heightened rhetoric on Russia, China, and sanctions has ushered in a new era of geopolitical unpredictability. This environment begets volatility in cross-border capital flows and increases bets on strategic sectors, namely defence, energy, and safe-havens. Political fragmentation remains a reason for investors to be cautious, especially as inflation and policy decisions on the horizon are front and centre, and headline risk continues as a big wild card.

3. Data on Inflation in Sight and Global Fragility

In the near term, markets are in suspense ahead of this week’s inflation reports—expectations are for CPI advancing ~0.3% MoM and ~2.9% YoY, with the core maintaining close to 3.1% levels. These are decisive data points; if they come in on the upside, it can upset the narrative of a rate cut. In Europe, political tensions in Japan and France continuing to worsen, combined with disinflationary pressures, provides a degree of added precariousness. With no big economic data coming out today, sentiment is being influenced by anticipation and headline risk as much as new data.

Zaye Capital Markets considers the market’s recent move a delicate rally–guided by dovish policy expectations but tempered by political and data risks. The big question ahead: will fresh inflation data reinforce the dovish shift or pull the carpet from under cautious optimism?

Digesting Economic Data

The TRUMP Tweets and Their Implications

The spate of recent commentary and policy initiatives by the Trump administration presents a mixed picture of both domestic and foreign priorities, with widespread implications for markets and investor sentiment. Domestically, the news of intensified workplace immigration raids in the aftermath of the Georgia Hyundai sweep, along with the dismantling of the White House peace vigil and court challenges by National Guard deployments in Washington, signifies a shift back towards more forceful enforcement policy and concentration of executive authority. These actions, though politically expressive, can spark home-bred tensions, as witnessed by the opposition to Guard deployments, and potentially generate waves in industries dependent on immigrant workers. The emphasis on closing labor supply could put a squeeze on wage dynamics, complicating the Federal Reserve’s equation on inflation and jobs.

On the geopolitical front, Trump’s sharp remarks on India and Russia drawing closer to China, combined with his vow that Europe must stop purchasing Russian oil, reveal an intensifying stance against adversaries and a demand for stronger alignment from allies. The threat of a second phase of Russia sanctions, alongside rhetoric branding India and Russia as “lost to China,” signals a deepening of U.S. strategic confrontation. This stance not only reshapes global trade flows—particularly in energy—but also raises volatility across commodities markets, where oil and natural gas prices are sensitive to such geopolitical fault lines. Investors should monitor these developments closely, as policy-driven shocks to supply chains often generate both sector-specific risks and broader safe-haven demand for assets like gold. No less compelling are Trump’s moves renaming the Department of Defense the “Department of War” and hinting at a sterner communications approach to U.S. national security. Such a shift in terminology, while rhetorical, implies a tougher tone in foreign relations. His “last warning” issued to Hamas, tabling sanctions over Ukraine, and scheduled meetings with European leaders all fall into a script of rising world tensions. Such news for markets increases the chances of outperformance in the defense sector, yet also raises investor unease regarding geopolitical divisiveness and potential drag on world growth. The end result is a scenario in which volatility spikes are increasingly likely, driving tactical opportunities yet posing challenges to long-term allocation plans.

Lastly, Trump’s domestic communication—brushing off the Epstein scandal as a “Democrat hoax,” support of RFK Jr.’s vaccine position, and reasserting the independence of the Federal Reserve through his economic point person—emphasizes the politically charged surroundings within which economic policy is playing out. Even as bullish commentary on Fed indepedence soothes certain investors, the larger dynamic of executive audacity and divisive stands could maintain sentiment on shaky ground. Through the lens at Zaye Capital Markets, we interpret these moves as reinforcing a two-track risk narrative: near-term lifts on defense-related equities and commodities, but longer-term doubts on consumer confidence, labor markets, and international trade flows. The important point for investors remains balancing optimism in policy-sensitive sectors with defensive stands in assets such as gold and high-quality equities, as volatility emerges as a lasting characteristic in the existing milieu.

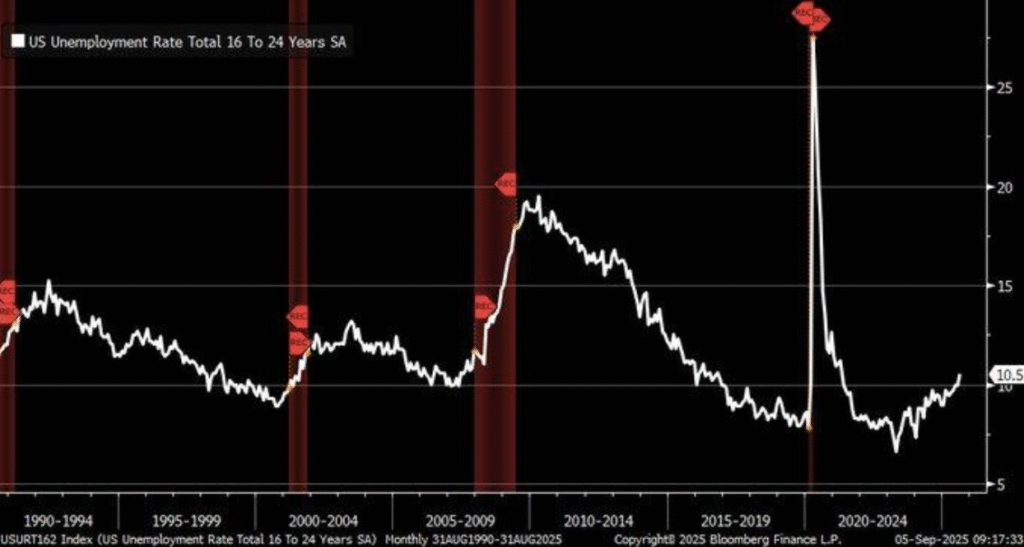

Youth Unemployment Soars as Tariff Pressures Meet Labor Market Easing

The latest labor market figures highlight a critical strain on younger workers, with the unemployment rate for 16–24 year-olds climbing sharply to 10.5% in August, a level not seen in years. Payroll growth added only 22,000 jobs, far below forecasts, underscoring how cyclical weakness is being reinforced by structural disruption. AI automation continues to reshape the landscape for entry-level positions, while the impact of heightened tariffs weighs heavily on corporate margins and investment appetite. These dynamics illustrate how economic policy and technological change are combining to create headwinds for new entrants to the workforce, threatening long-term productivity if participation rates decline further. Historical data shows that youth employment has always been sensitive to broad policy direction, and the current spike points to a deeper imbalance in how the economy is absorbing its youngest labor force.

At Zaye Capital Markets, we interpret this development as something more than a transitory swing. Higher import tariffs—at 50% on essential goods—are restricting supply chains, inflating costs on producers, and leaving companies reluctant to add payrolls. The added dimension is the diminished inflow of high-skilled labor associated with immigration barriers, thus indirectly hampering the pace of innovation and hiring in tech-intensive sectors. When combined with the disintermediative impact by automation in displacing routine and starter work, the end product is a bifurcated employment scenario in which young workers enjoy fewer avenues. The potential implication on consumer resilience flows from diminished disposable income in the age cohort having a direct impact on discretionary spending and youth-dependent sectors. The inter-play between policy constraints and technological diffusion is transforming labor market resilience both in the near term and on a longer, structural foundation.

From a market positioning perspective, we find industrials as having high risk with their sensitivity to tariffs and trade tensions, leaving room for yet lower revisions in earnings forecasts. Consumer staples, in contrast, remain cheap compared with broader indices, and they offer resilience in a world in which wage-sensitive consumption is coming under stress. The sectors enjoy stable demand and offer defensive cover as volatility grows in relation to uncertainty in the labor market. Analysts need to be monitoring the coming inflation releases and productivity numbers in assessing whether policymakers are ready to cut conditions aggressively in order to rebalance. A decisive move in policy could change sector perform quickly, and disciplined positioning is therefore necessary. Until then, our opinion is that defensive positions are tilted towards consumer staples within caution on industrials, as it is the most efficient hedge against higher youth unemployment and its spillovers into the economy.

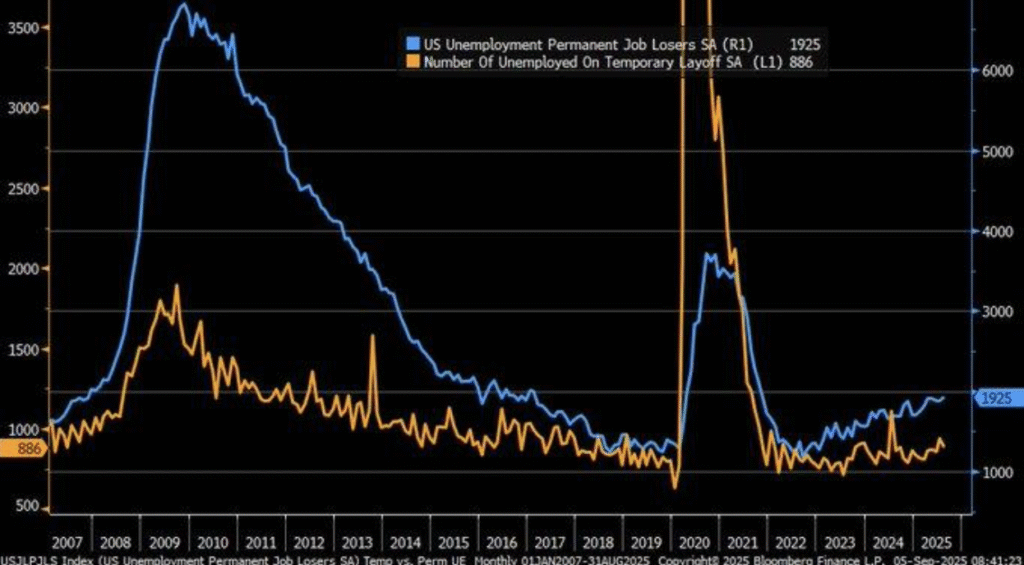

Rising Permanent Job Losses Signal Structural Strain on U.S. Labor Market

The most recent employment data indicate a troubling shift in labor market trends. August 2025 data report a steep increase in permanent job losers, reaching 1.8 million, while temporary layoffs kept trending down. This breakdown signals an economy in the midst of exiting cyclical softness and entering structural adjustment, with less likelihood of workers being recalled and more likely being long-term losers. Unlike temporary layoffs, which tend to reverse themselves rapidly as conditions come into balance, permanent losses drain both labor force participation and wage growth potential, a drag on consumer demand. History hammers home the implication of the shift: earlier cycles, and especially 1980s recessions, were characterized by bulges in permanent job losses as tentative predictors of deeper downswings, complicating hopes for a smooth “soft landing.”

At Zaye Capital Markets, we believe that this increase in permanent unemployment is a caution flag signaling that existing labor softness won’t be corrected by classical cyclical recoveries. Higher borrowing costs, trade dislocation, and growing automation are driving a rebalancing of workforces instead of cyclically driven retrenchments. When companies make permanent cutbacks instead of quick furloughs, it usually signifies strategic moves to rationalize operations, shift supply chains, or automate jobs. Such developments make labor market recuperation pace slower and more variable, and lower household confidence and consumption. Further confounding the equation are data constraints—dwindling survey response rates, as in other economies, make a possibility that statistical estimates undershoot true levels of latent labor displacement. Accordingly, real-time barometers such as payroll tax receipts or wage data are deservedly close attention in order to gauge the actual magnitude of faltering momentum.

From a market point of view, this shift into structural unemployment causes sectoral dispersion. Industrials and discretionary stocks associated with income-sensitive spending are still weak, with valuation levels showing a higher potential downside if labor participation continues to decline. Defensive stocks, on the other hand, look undervalued, especially in consumer staples and healthcare, which have fixed demand as households come under income stress. Analysts, in our opinion, need also to focus on productivity data and lead wage indicators since they will help resolve whether companies’ cost-cutting efforts are capable of maintaining margins despite falling labour utilisation. Positioning towards undervalued defensive stocks, in our opinion, remains the cautious approach, providing stability as the economy adjusts towards a labour market shock whose persistence could be greater than first thought.

Market Reprices Fed Path as Weak Labor Report Boosts Odds of Deeper Cuts

Market expectations shifted sharply following the release of the August jobs report, with the CME FedWatch Tool now assigning a 12% probability of a 50 basis point cut at the September FOMC meeting, up from zero just one day earlier. The driver was a notable miss in payroll growth, with only 22,000 jobs added against expectations of 75,000, pushing the unemployment rate to 4.3%. This weakness has forced investors to reassess the likelihood of a more aggressive policy response. The shift reflects growing concern that slowing employment momentum will weigh on household spending and confidence, particularly when paired with evidence that permanent job losses are rising, suggesting structural vulnerabilities beneath the surface.

At Zaye Capital Markets, we view this repricing as an important signal of investor psychology but caution that it may overstate the immediacy of a larger cut. The Federal Reserve’s recent commentary highlights its awareness of rising labor risks, yet history suggests it rarely opts for an outsized move unless conditions deteriorate further. Research linking past rate hikes to employment slowdowns supports the case for easing, but policymakers must balance this with their inflation mandate. During the 2008 financial crisis, rapid 50 bps cuts failed to prevent recession, illustrating the limitations of monetary policy in offsetting structural imbalances. Today, tariffs remain a lingering factor, as elevated trade barriers restrict supply chains and push input costs higher, complicating the Fed’s ability to deliver a smooth policy pivot. The interplay of weaker labor conditions and sticky inflation creates a narrow window for action, forcing the Fed to weigh risks on both sides of its mandate.

From an investment standpoint, the surge in expectations for deeper cuts should not be viewed solely as a bullish impulse. Lower rates may support liquidity, but structural headwinds, including tariff-driven cost pressures and slower hiring capacity, present challenges for cyclical sectors. Industrials and consumer discretionary remain vulnerable if household demand falters, while defensive positioning appears more attractive. We continue to see consumer staples and healthcare as undervalued relative to broader benchmarks, offering resilient cash flows in a fragile macro backdrop. Analysts should track both inflation releases and forward-looking jobless claims data, as these will determine whether markets are prematurely pricing a more dovish Fed path. In our view, stability lies in disciplined allocations toward defensives, while remaining cautious on sectors reliant on aggressive policy support for earnings growth.

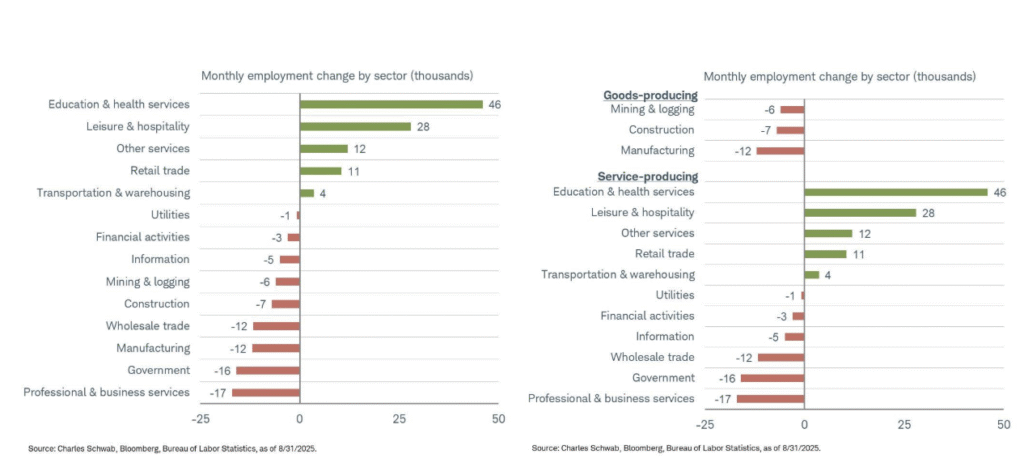

Sector Divergences Highlight Uneven Labor Market Resilience

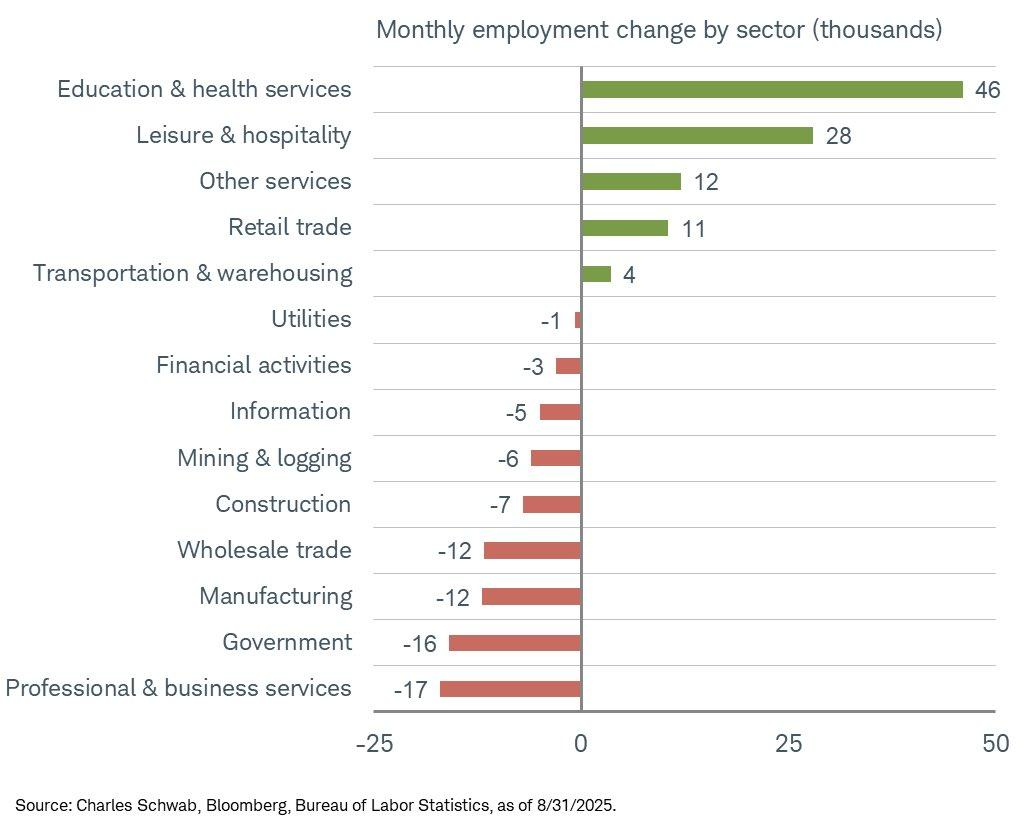

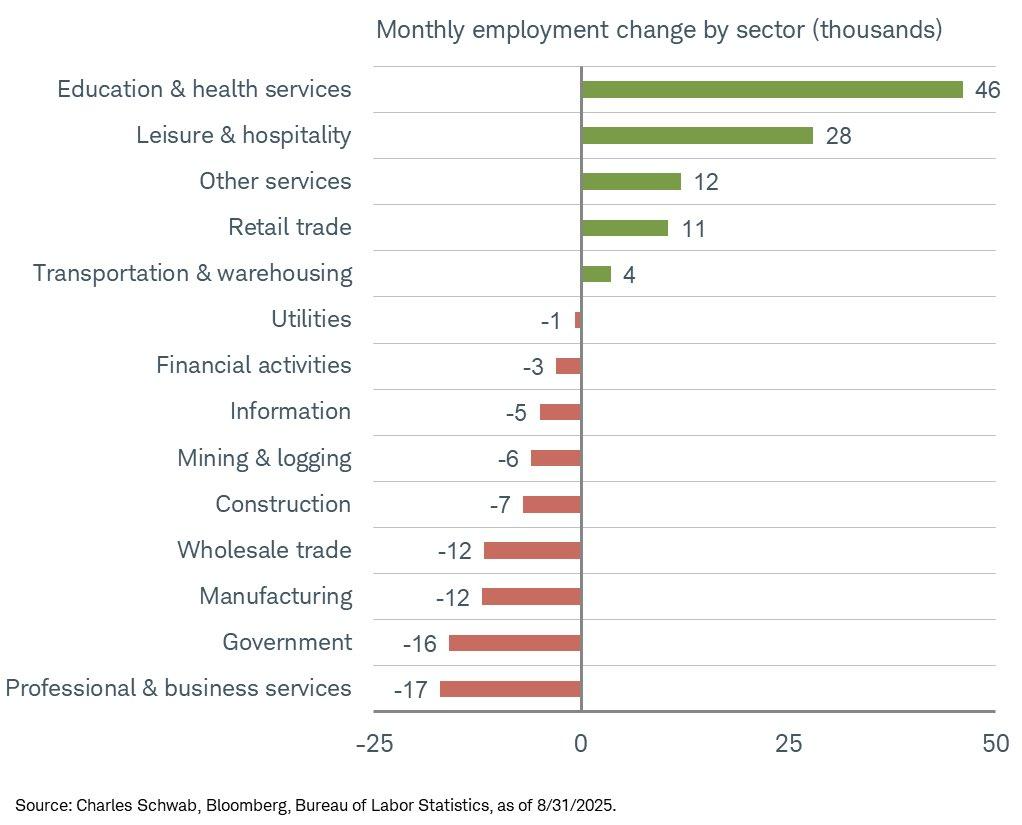

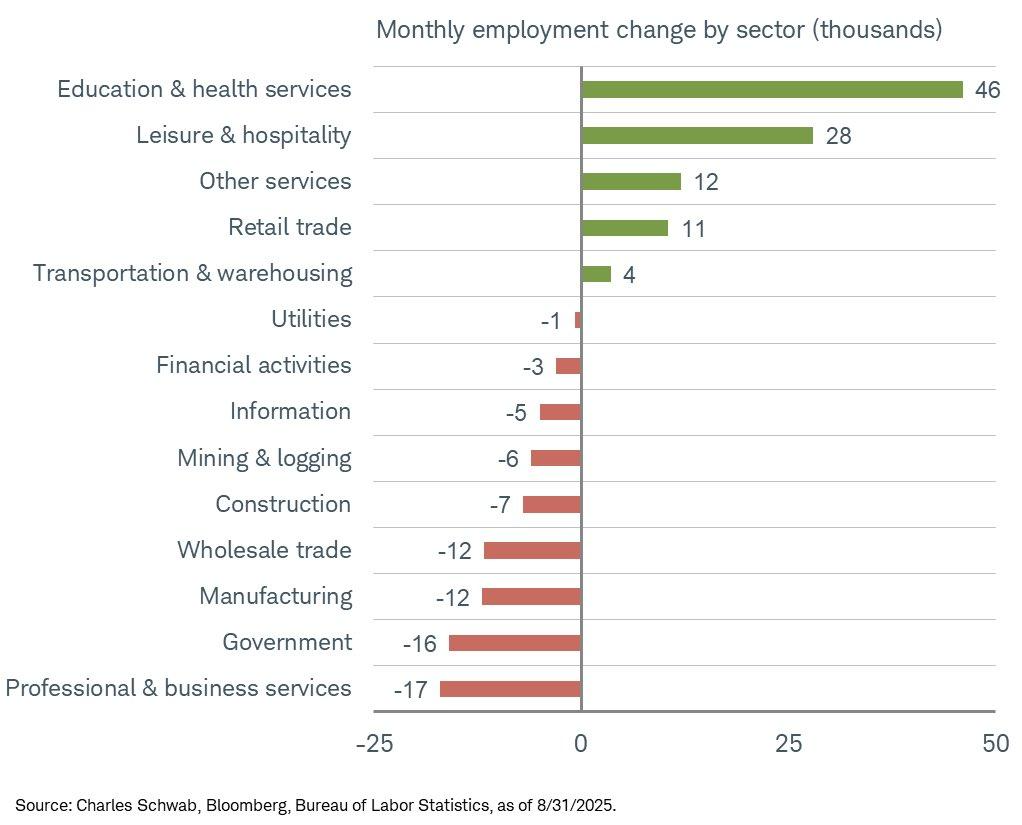

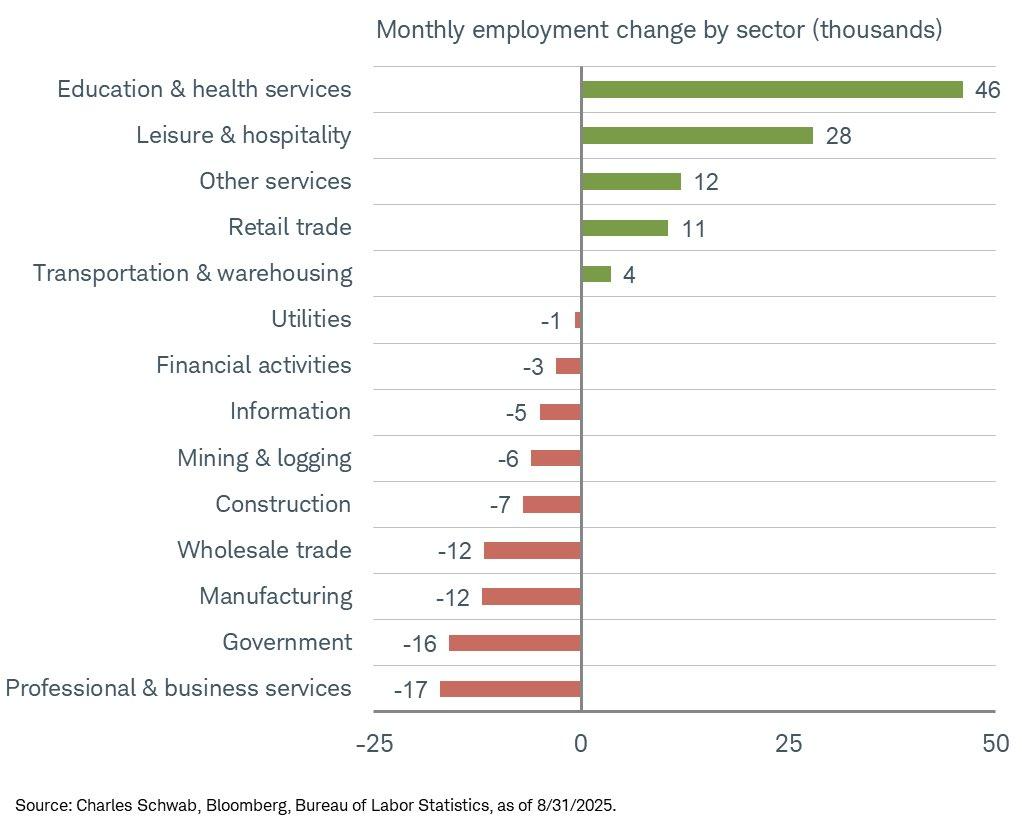

The August employment report showed a sharp discrepancy within industries, highlighting how policy changes and demographic developments are restructuring the labor market. The overall nonfarm payrolls increased by only 77,000, well below the consensus 140,000, and clearly indicating a slowdown in hiring pace. Goods-producing sectors shed 25,000 jobs, accounting for the impact of tightening trade settings and swelling input costs, and government payrolls shrank by 16,000 under budget constraints. Private education and health services, on the other hand, added a healthy 46,000 jobs on the back of underlying demand forces, and leisure and hospitality added 28,000 jobs. Such uneven spread points up the contradictory nature of the current labor market: strength in demographically and services-led sectors, and vulnerability in cyclical and policy-manageable industries.

In Zaye Capital Markets’ opinion, the divergence represents an early sign of structural labor market realignment and not plain volatility in the near term. Healthcare and education enjoy secular tailwinds in the form of aging populations, increasing demand for specialty services, and a labor-intensive model of delivery less vulnerable to automation. This strength contrasts starkly with manufacturing and goods-producing industries, in which higher tariffs and cost pressures compress margins and support slower hiring. Compounding the impact are tougher immigration dynamics, which hamper access to skilled manpower in industries dependent on diversified workforces. The outcome is a bifurcated labor market, with defensive industries growing while cyclical industries draw in their horns, and raising more general concerns regarding the economy’s ability to achieve balanced growth. From a market point of view, this deviation provides a case in point for sector selectivity. Industrials are vulnerable to policy shocks and set to encounter additional headwinds if restrictions on trade increase, placing their valuations in peril. Conversely, healthcare looks cheap compared to its defensive capability and durable growth profile, providing compelling long-term opportunities. The ability of the sector to grow despite conditions of macro weakness provides a primary anchor point for portfolios in uncertainty. Strategists need to be attentive as to whether education and healthcare maintain their leadership in coming data releases, as it would build a case for a defensive lean in portfolios. Currently, we regard healthcare as the sector most capable of surviving policy-induced volatility, while caution is still justified in goods-producing sectors sensitive to trade and budgetary constraints.

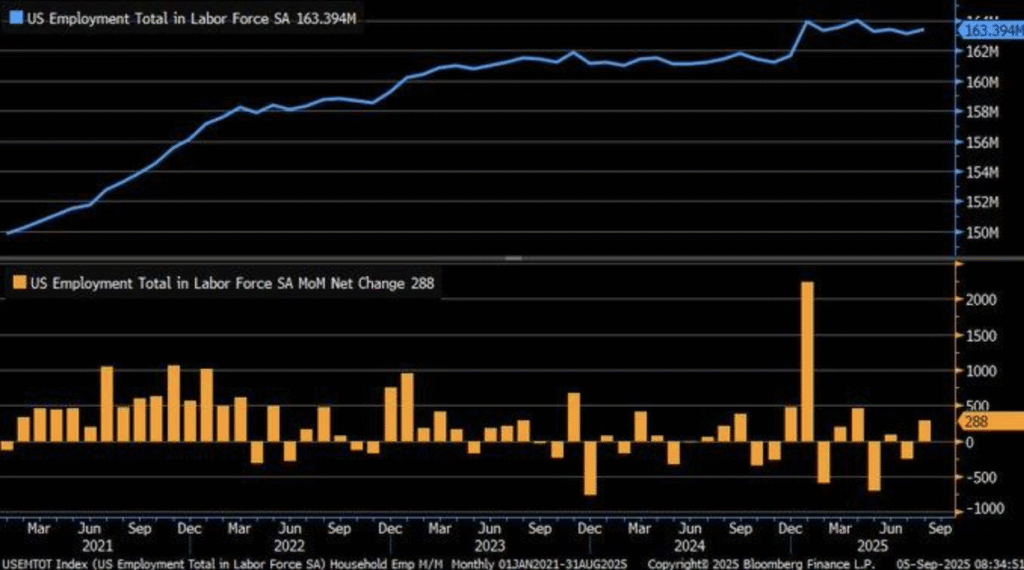

Household Survey Signals Job Recovery but Raises Questions on Reliability

August labor market data revealed a dramatic rebound in the U.S. household survey, showing a net employment gain of 288,000 after a decline of 260,000 in the previous month. This reversal points to a possible improvement in labor market sentiment and participation, suggesting that some of the recent weakness may have been overstated. Yet, the household survey’s strength contrasts sharply with the establishment survey, which recorded only a modest 22,000 increase in nonfarm payrolls. The divergence between the two datasets underscores the challenges of measuring labor conditions accurately, especially at a time when the economy is adjusting to structural pressures from automation, trade disruptions, and shifting workforce participation trends.

At Zaye Capital Markets, we view this discrepancy as a reminder of the complexities in interpreting labor market data. The household survey often captures employment trends not fully reflected in business payrolls, such as gig economy and informal work, which may be expanding as younger and displaced workers seek alternative income streams. However, history shows that these gaps frequently narrow following BLS benchmark revisions, with volatile swings often smoothed out in subsequent releases. With the unemployment rate steady at 4.3%, the household survey surge may represent an outlier rather than a durable turning point. As such, while the report offers a temporary boost to sentiment, it does little to dispel concerns about the broader slowdown evident in payrolls and job quality indicators. Analysts must therefore weigh the optimism of headline gains against the structural fragilities that remain embedded in the labor market.

From a sector standpoint, the divergence reinforces the importance of selectivity. If the household survey’s strength is partly driven by gig or informal employment, it suggests upside for technology platforms and service providers that benefit from flexible labor demand. Still, the sustainability of these jobs remains uncertain, leaving traditional growth sectors vulnerable to disappointment when revisions occur. By contrast, healthcare continues to look undervalued relative to its stable demand base, offering defensive insulation while other sectors face volatility from data noise. We believe analysts should focus on forthcoming revisions and high-frequency indicators, such as tax receipts and jobless claims, to confirm whether household survey gains are durable or simply statistical noise. Until then, disciplined positioning into defensive sectors remains the prudent approach while maintaining cautious exposure to cyclicals sensitive to shifting data narratives.

Payroll Miss and Rising Jobless Rate Reprice the Growth Narrative

The August nonfarm payrolls rose by a paltry +22,000 relative to expectations around +75,000, as earlier months were revised down 21,000 and the unemployment rate gained 4.3%. Since April, headline employment has really leveled off, and it is characteristic of a labor market decelerating, as opposed to plateauing. We believe it is a late-cycle indicator: slower hiring, softer wage growth in average hourly, and smaller breadth in industries are all consistent with muted demand and tightening budgets at corporations. Elevated trade tensions and higher input costs remain negative on goods-producing sectors, and selective hiring in services continues more focused on balance-sheet-strengthening and productivity as opposed to headcount growth.

As we weigh the policy outlook, we find a rate-cut expectations tug-of-war against lingering structural headwinds. Slower payroll has been a harbinger before softer output, and the combination of weak job formation and rising unemployment casts doubt on the idea of robust underlying growth. Tariffs implemented in recent years have increased effective costs, squeezed margins, and subdued capex—impacts that do not undo easily through monetary easing only. Against our background, the probability distribution around near-term growth is tilted lower unless productivity does accelerate or rebuilding in stocks surprises on the upside. This makes a case for caution in cyclicals most vulnerable to real-income sensitivity and external demand, and a close eye on changes that would add to a downgrading in the employment landscape. From a positioning perspective, we prefer high-quality defensives with price power and cash-flow transparency that are less vulnerable to input price volatility. We believe Procter & Gamble (PG) is undervalued compared with its defensive earning profile and ability to insulate against input price volatility, and it is a candidate to gain ground if wage growth and hours worked continue to decline. Analysts should monitor: (1) payroll and household-survey revisions; (2) employment cost index and average weekly hours in confirmation of cooling in labour; (3) ISM employment sub-indices and jobless claims in more up-to-date inflections; and (4) inventory/sales ratios and import prices in ascertaining tariff pass-through. Unemployment rising another notch without compensating increases in hours or productivity would confirm a defensive tilt, while a hint at labour utilisation improvement would warrant selectively adding cyclical exposure again.

Breaking Down the Economies Data: Export Growth Eases, Trade Deficit Widens

U.S. export growth fell to 3.4% year-over-year in July 2025, down significantly from close to 10% in April, highlighting the increasing squeeze on external demand. The associated trade deficit broadened to $78.31 billion, reporting weaker shipments overseas in a world of geopolitical stress, macroeconomic variability, and supply-chain reshaping. History suggests export cycles turn down following big shocks—the 2008 financial shock, say, through pandemic-related dislocation—and the recent fall indicates external demand is decelerating anew. With foreign purchasers retarding orders and logistical complexity increasing, U.S. exporters are facing headwinds both increasingly structural and less reversible.

At Zaye Capital Markets, we take this trend as an early indicator of trade fragmentation’s economic toll. Exporting has grown more responsive to policy changes, as tariffs and regulatory friction increase barriers that formerly less restricted goods faced. Analysis has cited the increasing intricacy of trade since 2023, as supply lines are rerouted, compliance costs increase, and local protectionism limits the ability of American firms to compete externally. The end outcome is margin pressure on goods sectors, especially industrials and capital equipment exporters, as they face softer demand while input costs persist at higher levels. That puts a dent in the tale of external strength propelling the American economy and increases the potential for spillovers into hiring, spending, and earnings. For positioning, we are selective on industrials and export-dependent cyclical companies, whose valuations look sensitive if the slowdown in export growth continues. Conversely, we believe healthcare is cheap on a relative basis in the existing climate, enjoying consistent domestic demand and low exposure to trade disruptions overseas. The defensive earning stream of healthcare provides insulation as export-facing business industries endure volatility from changes in trade policy. Analysts need to be alert for updates to export growth data, currency news, and leading indices of world demand—like PMI export orders and shipping lines—as a guide as to whether the slowdown turns out transitory or turns into a more fundamental drag. A clear cut further decline in export growth would make the case for a defensive bias, while a stabilisation would enable selective reinvesting in cyclical exporters.

Tech Layoffs Emphasize Structural Shift Towards Automation

Recent data shows U.S. tech job cuts accelerating, with 81,972 job losses among 189 companies in 2025, signaling an industry-wide move towards optimization. This is continuing a streak of downsizing that began in 2022–2023, as firms accommodated post-2020 shifts in demand and rebalanced workforces in alignment with the quickening pace of AI rollouts. Assumptions in history that technology was a reliabled job creator are coming into question, as job reductions persist through leading companies and echoing through the supply chain as a continuum. Unlike cyclical retrenchment, the new wave appears supported by a continuing productivity drive, recasting employment dynamics and investment themes in the sector.

At Zaye Capital Markets, we take these developments as evidence of a structural readjustment as opposed to transitory weakness. Analysis posits AI potentially automating 15% or so of world work hours, and firms are racing to implement this potential. The outcome is less headcount demand in repetitive professions and greater need in distinctive skill sets in AI design, cybersecurity, and higher-order engineering. The transformation, as an investment implication, changes the frame on technology exposure: no longer does hiring growth in the classical sense remain the primary driver in sector growth as optimization on the margin and productivity improvement gain the upper hand. Politically sensitive, the moves are in line with previous patterns in which disruptive innovations in the labor force alter composition before driving longer-term economic efficiency. For positioning, we remain selective. High-growth tech reliant on headcount expansion faces margin headwinds as AI reduces the value of labor-intensive models. By contrast, firms providing AI infrastructure and automation solutions appear undervalued, given their central role in capturing efficiency gains across industries. This includes companies in semiconductors, enterprise software, and cloud services that enable automation adoption. Analysts should monitor forward guidance on capex, productivity trends, and labor costs within earnings reports to assess whether tech’s margin expansion can offset employment reductions. We see the present moment not as a cyclical setback but as a redefinition of the sector’s growth drivers, reinforcing the need for disciplined allocations toward undervalued enablers of automation while maintaining caution on labor-heavy models.

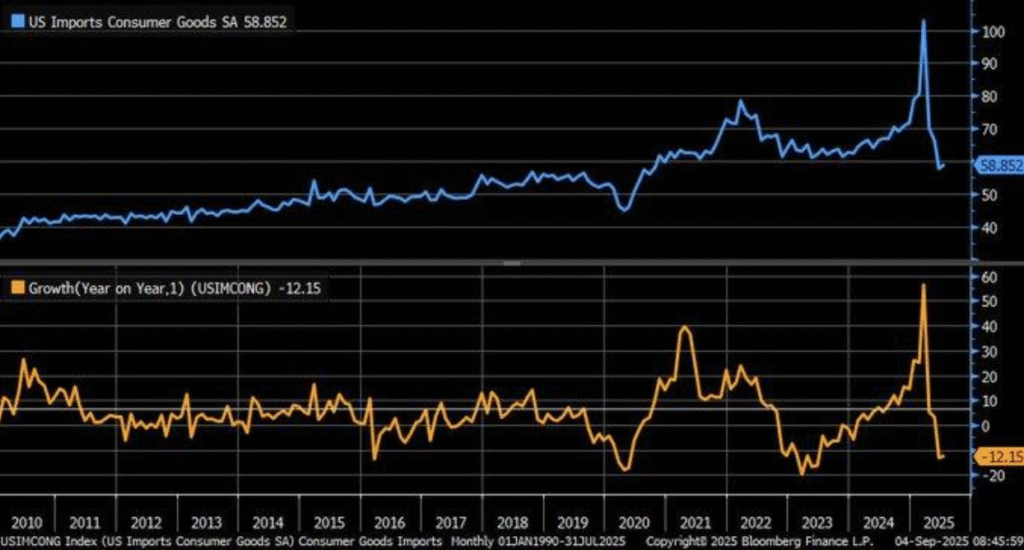

Consumer Goods Imports Fall As Constraints On Spending Rise

U.S. imports of consumer goods fell 12.2% on a year-over-year basis in July 2025, evidencing growing pressures on household demand and portending fissures in the post-2020 recovery story. The fall is consistent with expectations of slower consumption, including a 5% holiday period spending decline as mounting tariffs and higher living expenses whittle down buying power. Imports of consumer goods are still lower than pre-2020 peaks, emphasizing households are retrenching not merely at the margins, but in a manner that hits world supply lines. The 2024 analogue, in which discretionary spending surged among young generations, shows how sentiment can swing quickly if inflationary pressures and higher borrowing costs prevail in household calculus.

At Zaye Capital Markets, we believe this trend is an indicator of a broad rebalancing in consumer demand. Gen Z, having boosted spending by 37% in 2024, is now slashing budgets by nearly a quarter in 2025, as surveys illustrate younger groups now value frugality over discretionary spending. This is consistent with Federal Reserve work showing younger households are more sensitive to inflationary shocks, characteristically cutting discretionary spending and building cushions of liquidity. Such revisions have both near-term implications, as well as implications in medium- and long-horizon consumption dynamics, as younger groups tend to be leaders in goods segments from fashion through electronics. The decline in imports thus reflects both softer cyclical demand as well as larger structural trade frictions, exacerbated by regimes of tariffs and supply-chain bifurcation. From a sectoral angle, it requires caution in discretionary retailing and import-dependent industries, which are set to come under sustained pressure on earnings if belt-tightening by households persists. Consumer staples, on the other hand, are viewed as cheap, with their predictable demand template and partial immunity from trade turbulence providing stability to investors. Those companies having diversified supply lines and price power are well equipped to handle changed priorities by the consumer, though cyclical sectors fare poorly. The analysts need to track high frequency data points like credit card spending, shipping, and retail revisions in sales in order to assess if the slowdown in imports continues into the holiday period. Ongoing contraction would add weight to the argument in favor of overweighting in defensives, while a freeze in imports could mark a bottoming process in discretionary industry segments.

Upcoming Economic Events

As we step into a fresh trading week, the economic calendar opens on a quiet note with no major data releases scheduled for today. This calm provides markets a chance to digest recent volatility in labor reports and wage data before attention shifts toward the key indicators due later in the week.

At Zaye Capital Markets, we view these pauses as valuable moments for investors to reassess positioning and sharpen focus on the data that truly moves policy expectations. The absence of immediate catalysts today means price action will likely be driven by technical flows and sentiment around broader macro narratives, particularly expectations for Federal Reserve policy.

Looking ahead, critical updates on employment, wages, and consumer demand will soon provide sharper direction for markets. We encourage investors to stay tuned, as the upcoming releases will not only test the “soft landing” narrative but also define the path of interest rates heading into the remainder of the year.

Stock Market Performance

Indexes Bounce Back from April Lows, But Breadth Continues Rough

U.S. equity indexes have fashioned decent recoveries off the April 8 low, yet the repetition of steep drawdowns and weak average member activity continues to betray underlying weakness. Even as encouraging headline data emerges, breadth still remains meager and volatility continues to be the hallmark of underlying market temperament.

Here is our summary on the recent performance through major indexes:

S&P 500: Headline Strength, But Constituents Lag

YTD: +11% | -30% below April low | -19% below YTD peak | Avg. member: -25%

The S&P 500 demonstrates healthy progress on the 11% year-to-date advance and 30% April bottoms-up rally, yet a 19% correction from the annual high and average participation losses of 25% underscore the fact that larger participation has been restrained.

NASDAQ: Growth Rebound Masquerades Over Deeper Loss

Year-To-Date: +12% | -42% below April low | -24% below YTD peak | Average member: -47%

The NASDAQ takes the lead on paper, up 12% in 2025 and 42% since April bottoms. But dramatic 24% index-level drops from tops and 47% average member drawdown bare all in how lopsided profits are and how vulnerable the tech-heavy index remains in disguise.

Russell 2000: Small-Cap Volatility Persists

YTD: up 7% | -35% below April low | -24% below YTD peak | Avg. member down -38% The Russell 2000 has regained 35% from April lows but remains up only 7% on the year-to-date. 24% decline from all-time highs and 38% average member decreases validate perpetual pressures on smaller, less-liquid stocks vulnerable to macro headwinds.

Dow Jones: Resilient But Not Immune

Year-to-date: +7% | -21% below April low | -16% below YTD peak | Member average: -23% The Dow Jones, as defensively constituted, was up 7% this year and 21% off April lows. Its fairly modest 16% drawdown is a bullish indicator, but average losses among members of 23% demonstrate that value-weighted ingredients are under intense pressure too.

At Zaye Capital Markets, we remain selective, as ever, and prefer balance-sheet stability, sustained earnings, and defensive exposure, while paying close attention to market breadth in confirmation of a more durable advance.

Strongest Sector Among All These Indices

Communication Services Tops YTD and MTD Charts

From our reading of the most recent sector tape, Communication Services stands as the undisputed winner within the S&P 500 world–+22.5% year-to-date, +4.5% month-to-date–ahead of the S&P 500 itself (+10.5% YTD, +0.6% MTD). While some cyclical groups have achieved double-digit YTD advances, month-to-date breadth is confusing, with numerous sectors down. Leadership is narrow in our estimation, and we shall be examining if follow-through widens by more than a few leaders.

Sector scoreboard (YTD | MTD):

- Communication Services: 22.5% | 4.5% ← both horizons’ strongest

- Industrials: 14.6% | -0.5%

- Information Technology: 14.0% | 0.4%

- Financials: 11.6% | 0.1%

- Utilities: 9.9% | -0.7%

- Materials: 9.3% | -0.9%

- Consumer Staples: 4.1% | 0.2%

- Consumer Discretionary: 3.3% | 1.7%

- Energy: 3.3% | -1.5%

- Real Estate: 2.3% | -1.3%

- Health Care: 0.0% | -0.4%

- Contextual Index:

- S&P 500: 10.5% | 0.6%

As a group, we consider the present configuration leadership-biased: Communication Services anchors itself firmly on top (+22.5% YTD, +4.5% MTD), and multiple sectors register negative MTD prints despite robust YTD gains. We’ll look to see if leaders’ momentum continues and laggards recover sufficiently to enhance breadth overall.

EARNINGS

Yesterday’s Earnings (September 5, 2025)

- Ermenegildo Zegna N.V.

Ermenegildo Zegna reported first-half 2025 revenues of €928 million, down 3% year-on-year, with organic revenues easing 2%. Despite softer top-line performance, profitability improved, with net income rising to €47.9 million from €31.3 million a year earlier. Adjusted EBIT came in at €68.7 million, reflecting strong margin discipline. For investors, this shows resilience in the luxury segment, where tighter cost controls offset revenue headwinds.

- ABM Industries Incorporated

ABM Industries posted fiscal Q3 2025 revenue of $2.22 billion, up 6.2% year-on-year, surpassing consensus expectations. However, earnings per share fell to $0.82, below estimates near $0.95, marking an 18% miss. Management announced a $35 million restructuring plan and a $150 million share buyback program, aiming to mitigate margin pressures. Investors will focus on whether these initiatives restore profitability momentum in coming quarters.

- Pro-Dex, Inc.

Pro-Dex released fiscal Q4 2025 results showing revenue of $17.5 million, up from $15.0 million a year ago. Still, earnings per share were $0.36, falling short of consensus (~$0.47) and representing a 23% miss. Margins contracted, with gross margin dipping to about 20%, raising concerns about cost management. The market reaction was modestly negative, with shares sliding following the release.

- Kewaunee Scientific Corporation

Kewaunee Scientific did not release results on September 5. The company’s fiscal Q4 2025 earnings had already been announced in June, with the next scheduled report expected on September 10, 2025. Investors are awaiting updates on order backlogs and margin recovery when those results are released.

Today’s Upcoming Earnings (September 8, 2025)

- Casey’s General Stores, Inc.

Casey’s will report earnings after the market close, with consensus expecting earnings per share of $5.04–$5.05 on revenue near $4.48 billion. Investors should watch for sustained strength in foodservice and same-store sales, as well as any guidance on store expansion and operating margins, which have been key drivers of valuation.

- National Beverage Corp.

National Beverage is also due to release results today, with analysts forecasting EPS around $0.60 and revenue near $346 million. Investors will closely monitor margin trends, particularly for the LaCroix brand, as competition in the flavored beverage category remains intense. Forward guidance will be critical in determining whether the company can stabilize valuation pressures.

- Planet Labs PBC

Planet Labs is set to report before the market open, with analysts projecting EPS of −$0.06 to −$0.08 on revenue between $65.9 million and $67.7 million. The company’s recent €240 million German contract has raised expectations, and investors will be focused on whether bookings and guidance suggest accelerating adoption of satellite data solutions.

- Yext, Inc.

Yext’s earnings are scheduled for release later this week, with consensus expectations of $0.12 EPS and revenue near $111 million. Key investor focus will be on recurring revenue growth, the monetization of AI-enabled search products, and management’s outlook for adjusted EBITDA. Sustained top-line growth remains essential for maintaining investor confidence in a competitive digital services market.

Stock Market Overview – Monday, September 8, 2025

The US equity markets started the week hesitantly as investors weighed pessimistic labour data released during the previous week against burgeoning expectations of Federal Reserve interest-rate reductions. The S&P 500 and Nasdaq Composite fell as tech leadership softened, but the Dow Jones and Russell 2000 showed selective resilience in defensive and small-cap comebacks. Overriding sentiment remains frail, restrained by macro uncertainty and persisting geopolitical tension.

Underlying Sentiment Economic Factors and Geopolitical Trends

Markets are still processing the August jobs report, reporting a paltry 22,000 jobs added after 75,000 prior expectations and unemployment up at 4.3%. This confirmed bets on near-term easing by the Fed but also triggered fears of growth slowdown. Politically, a new Trump administration immigration enforcement, legal challenges in National Guard deployments, and increased chatter on Russia, China, and Europe are unsettling. The lack of big data today leaves markets vulnerable to headlines and position-taking ahead of Fed anticipations.

Stock News Update

- AI execution gap: Those reporting clear AI monetization are beating, and those without are incurring steep drawdowns.

- Energy and Industrials mixed: Volatility in input costs and trade friction are limiting rallies.

- Quality tilt: Investors are rewarding balance-sheet discipline and punishing thin-margin growth stories, maintaining narrow leadership.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—the Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla stocks—stay on a selling binge, with the lot in general trading down double-digit percentages from recent highs. Tesla and Meta remain the leaders in decline as valuations are adjusted on account of softer demand cues. This narrowing leadership is sustaining weakness in the larger S&P 500’s momentum, and defensives and selective cyclicals are left offering support. Absent buying participation by these mega-cap stocks, up legs are set to be feeble and spotty.

Major Index Performances – Monday, September 8, 2025

- S&P 500: 6,472.4, down 0.3% on the day

- Nasdaq Composite: 17,860.6, down 0.5%

- Dow Jones Industrial Average: 45,499.0, up 0.2%

- Russell 2000: 2,377.7, up 0.5%

At Zaye Capital Markets, we are selective, looking for balance sheets of quality and sustained flows of earnings. Breadth remains mediocre and mega-cap leadership tenuous, and investor discretion is required as markets grapple with policy uncertainty and geopolitics headwinds.

Gold Price

The gold continues to be exchanged at all-time highs, spot selling at barely over $3,600 an ounce as of Monday, September 8, 2025. The resilience in the metal mirrors a alignment of macroeconomic and political trends fueling risk aversion and buttressing bullion’s status as a store of safe-haven assets. Geopolitical risks remain center stage following a spate of commentary from the Trump administration, ranging from new sanctions in response to Russia and demands on Europe to stop buying oil from Moscow, through stepped-up pressures on China and a refranchising of the U.S. Defense Department as the “Department of War.” Coupled with these are homegrown uncertainties, including lawsuits over National Guard deployments and demonstrations in Washington, D.C., which heighten perceptions of political uncertainty. With no compelling economic data scheduled today, markets are forced to swallow these developments, lifting gold as a defensive shield against policy uncertainty and possible changes in international alignments. Periods in the past in which heightened geopolitical commentary was combined with policy uncertainty have paved the way for sustained demand in gold, and today’s is no exception, as investors weigh potential currency uncertainty and equity fragility against the defensive allure of the metal. The weak labor data from yesterday provided a new catalyst, reinforcing the case for higher gold prices on a macroeconomic basis. Nonfarm payrolls added a meager 22,000 in August, well short of the 75,000 anticipated, as unemployment inched up to 4.3%, and earlier months were revised down by 21,000. These readings, in addition to highlighting job creation stagnation since April, add weight to the belief that the Federal Reservewill be compelled toward easing sooner than later. Lower borrowing costs lower the opportunity cost of ownership in gold and more typically make the buck weak, both conditions which add luster to bullion. At Zaye Capital Markets, we interpret the existing scenario as a twin driver in gold: political strains fuel immediate safe-haven interest while worsening labor conditions nudge monetary policy toward accommodation. The end product is an environment in which the metal profits both from stagflationary uncertainty and cyclical weakness, maintaining it close to all-time highs. With sentiment turning decisively in favor of security and maintenance of liquidity, we believe that gold remains well supported, especially if forthcoming data does nothing to reverse the script on economic momentum slowdown.

Oil Prices

The oil markets began the week under fresh volatility, with Brent crude oscillating around $65.50 a barrel, as supply expansion and cooling demand expectations fought a tug-of-war. On the supply front, OPEC+ reiterated plans to unwind earlier production cuts gradually, injecting around 137,000 barrels a day from October, as the International Energy Agency targeted 2025 world supply growth coming in at a 2.5 million-barrel-per-day pace. Meanwhile, the IEA cut world demand growth estimates by half, citing disappointing consumption in major economies including China and Europe, in a scenario it estimated at 680,000–700,000 barrels a day. This dynamic implies that despite supply-side optimism being firm, the demand scenario is downshifted, setting the stage for an oversupplied market and limiting price upswings. Political risk has also appeared on the scene: Trump’s caustic commentary on India, Russia, and China, and efforts to redefine U.S. defense policy and broaden sanctions, have added a new layer of geopolitics uncertainty. Such commentary typically constructs a temporary risk premium in oil, as markets calculate potential interferences in trade flows and energy routes, but whose impact was masked by the overarching supply growth and muted demand narrative. Investor sentiment was also dampened by yesterday’s weak U.S. labor data, reporting only 22,000 jobs added in August versus expectations of 75,000 and unemployment up to 4.3%. For oil, it reinforced the impression that domestic demand growth is sliding, and increased the likelihood of Federal Reserve interest rate cuts that would soften the dollar yet signify softer consumption trends. With no major-picture economic data on the table today, we are in a holding pattern, waiting later inflation releases that could shift monetary policy expectations and, by extension, world demand outlooks for energy. At Zaye Capital Markets, we view the existing atmosphere as a tug-of-war game between bearish fundamentals—as driven by supply overhangs and softer employment data—versus geopolitical noise that produces a spurt or two of support. Until demand indicators make a decisive breakout above recent downtrend lines, larger-picture remains negative and suggests oil struggling to establish a durable rally, sustaining volatility in a heightened range and position-taking tilted towards defensive modes.

Bitcoin Prices

Bitcoin kicked off the week unchanged, oscillating within the $111,188 band, maintaining its ground in the $110,000–$113,000 corridor following a turbulent period during which Ether spearheaded losses within the crypto complex. Long-term holders remain on an accumulation binge, as evidenced by on-chain data, with illiquidity reaching all-time highs, a reflection of conviction in the asset’s store-of-value properties despite weakening short-term flows. Technical levels pinpoint important support levels bunched up around $108,250, $104,250, and $97,050, offering cushions against steeper routs, while resistance is closer to $116,963, a potential destination for profit-taking. Meanwhile, buying interest from corporate treasuries and institutional vehicles continues patchy, with Asia-biased flows decelerating and average purchase sizes falling by over 80% relative to earlier in the year. Reflecting the phase of consolidation, the discrepancy points up the diametrically opposing dynamics of structurally underpinning long-term support and disintegrating speculative momentum. For traders, the narrow range is a case of a balancing act in positive network fundamentals and macro-driven caution. Macro and geopolitical currents are heavily shaping sentiment. A barrage of Trump administration headlines—from intensified immigration raids and lawsuits over National Guard deployments, to sharp warnings on Russia, China, and rebranded U.S. defense policy—has injected political volatility that traditionally supports Bitcoin’s safe-haven narrative. At the same time, Bloomberg reports linking Trump’s family to crypto ventures, alongside news of corporate vehicles multiplying around Bitcoin-treasury strategies, highlight the political and institutional entanglement increasingly anchoring BTC’s ecosystem. Yesterday’s disappointing jobs report—only 22,000 added versus 75,000 expected, unemployment rising to 4.3%, and prior revisions cutting momentum—intensified bets on Fed rate cuts, which weaken the dollar and enhance Bitcoin’s relative appeal. Yet the absence of major data today leaves the market consolidating, as traders await inflation releases later in the week to gauge the Fed’s urgency. In this environment, Bitcoin benefits from geopolitical risk and monetary easing narratives, but until clear catalysts break the stalemate, price action is likely to remain range-bound, with volatility clustered around key support and resistance levels.

ETH Prices

Ethereum currently hovers around $4,307 today, oscillating steadily despite larger crypto markets remaining volatile. Spot ETH ETFs have been a lead source of flows in recent months, with August reporting nearly $3.95 billion in net inflows, temporarily eclipsing Bitcoin-linked funds and confirming investor interest in diversifying outside BTC. Early September, however, has seen a bit of slowdown, with outflows reaching close to $135 million, a reflection on tactically timed profit-taking and rotation into Bitcoin during ETH’s recent hot streak. Unsurprisingly, whale activity has reversed supportively as well: three new wallets collectively scooped up around $148.8 million in ETH on recent dips, while an existing Bitcoin whale made a forceful switch, adding 96,859 ETH totaling $435 million into their account. This activity shows how well-heeled investors are positioning into Ethereum at significant support levels, a reflection that they perceive existing prices as attractive entry points into longer-term accumulation. On-chain data confirms growing illiquid supply as well, reinforcing the narrative that ETH is getting transferred off exchanges into long-term storage—a structural bullish indicator, despite price action feeling range-bound in the near term. Geopolitics and macroeconomic currents are adding further complexity to Ethereum’s outlook. The Trump administration’s sweeping policy actions—ranging from intensifying immigration raids to new sanctions discussions with European allies—are contributing to a risk-off global narrative, one that often channels investor attention toward decentralized assets as hedges against policy unpredictability. Yesterday’s disappointing U.S. labor data, with just 22,000 jobs added against forecasts of 75,000 and unemployment rising to 4.3%, bolstered expectations that the Federal Reserve will lean more dovish in the months ahead. Historically, easier policy weakens the dollar and strengthens the case for alternative assets, giving Ethereum a macro tailwind. While near-term ETF outflows and technical resistance levels cap upside momentum, the combination of whale accumulation, long-term holder conviction, and policy-driven uncertainty is quietly reinforcing Ethereum’s investment case. We at Zaye Capital Markets believe this consolidation period may serve as the foundation for ETH’s next leg higher, as structural demand from institutions and on-chain participants eventually outweighs the tactical selling pressure seen in recent sessions.