Where Are Markets Today?

U.S. and European futures are stable this morning as investors adopt a cautious stance ahead of a pivotal week in central bank policy. In the U.S., futures remain near the flatline as market participants anticipate that the Federal Reserve will reveal its hand with a 25 basis point rate cut, reducing the funds rate to about 4.00-4.25%. Though the cut in itself is anticipated, attention will be more intently on the new dot-plot of the Fed as well as Chair Jerome Powell’s press briefing, in terms of providing clarity as to whether further easing will be in store ahead of year-end. In Europe, futures of Germany’s DAX futures are slightly higher, while the FTSE is mixed, in a show of caution ahead of later this week’s meeting of European Central Bank policymakers, who are expected to maintain rates steady.

The flat performance across both regions highlights the delicate balance between optimism in certain sectors and broader macroeconomic caution. In the U.S., enthusiasm remains concentrated in technology and artificial intelligence leaders such as Nvidia and Meta, which continue to attract investor flows and provide support to the Nasdaq and S&P 500. However, this optimism is offset by signs of weakening labor market momentum and inflation readings that remain sticky, leaving investors uncertain about how aggressive the Fed’s rate-cutting cycle might ultimately be. In Europe, sentiment has been further dampened by last week’s credit downgrade of France by Fitch, underscoring fiscal challenges and debt sustainability concerns across parts of the eurozone. These developments have reinforced a more defensive tone, preventing futures from rallying despite global liquidity expectations.

Careful positioning also captures investors’ current sensitivity to geopolitical risks. The White House acknowledged that Trump will sit down with European leaders to talk about Russia-Ukraine tensions, a reminder that rising tensions could hit markets via energy, defense, andcurrency avenues. Meanwhile, Trump’s more general remarks about tariffs, tough foreign policy, and desired cuts in U.S. interest rates further cloud the global economic background. Investors don’t want to take big risks in this setting until there is clearer guidance about central bank intentions. The ECB, in particular, has a delicate balancing act to accomplish, as weak signals about growth must be matched against entrenched inflation, so there is little leeway for policy misfires. Ahead, subdued tone in futures indicates that markets are preparing for a critical mid-week pivot. If the Fed gives indications of cuts beyond the anticipated 25 basis points, risk assets might gather steam, especially in growth-sensitive areas. If, however, Powell gives a cautious or subdued prognosis, equities might struggle to continue gains, prompting investors to swing into defensive areas or safe-haven assets. Likewise, if the ECB gives voice to this cautious tone and focuses more on inflation risks versus concerns over growth, European equities might underperform. At this juncture, the clustering of U.S. and European futures around the flatline shows a market that is waiting for central banks to initiate the next directional move.

Major Index Performance at Monday, September 15, 2025

- S&P 500: Closed at 6,584.29 on September 12, 2025. (F

- Nasdaq Composite: Closed at 22,141.10 on September 12, 2025. (The

- Russell 2000: 2,397.06 as of September 12, 2025.

- Dow Jones Industrial Average: Closed at 45,834.22 on September 12, 2025.

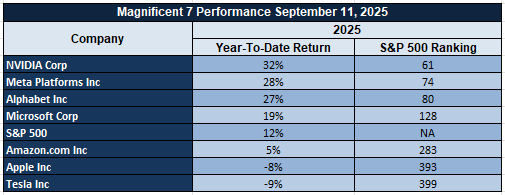

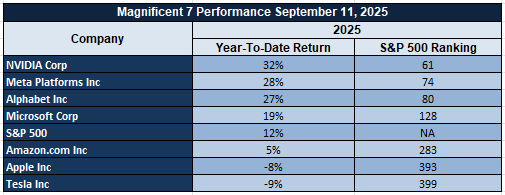

Magnificent Seven and S&P 500 Index

In the background, as the S&P 500 continues to rise near historical highs led by advances in large-cap technology, the Magnificent Seven come under further pressure. The group’s valuations are being questioned as recent behavior appeared out of whack relative to normalized earnings acceleration and fundamental economics. The group is being pushed back by overvaluation signs as much as by concerns about sustaining expansion, leading investors to be cautious about further advances without more substantial underlying data.

Drivers Behind the Market Move – Monday, September 15, 2025

When global markets open up again Monday, September 15, 2025, investor sentiment is shaped by a mix of economic data, central bank action, and political events. While European futures are slightly positive, U.S. futures remain flat as investors hedge ahead of this week’s Federal Reserve policy meeting. Traders are looking at whether that closely expected 25 basis point cut by the Fed will be followed by further easing, as well as whether geopolitical risks intersect with central bank action.

1. Economic Data Influences Fed Outlook

Recent U.S. data is still mixed. Inflation is still sticky, with August CPI up 2.9% year over year, while core inflation stays above 3%. Meanwhile, weekly jobless claims reached 263,000, a portent of worsening labor conditions. Both of these data support the thesis that this week the Fed will unveil a 25 basis point cut, but both leave unclear how soon more cuts will arrive. In Europe, a hold in ECB rates is expected after President Lagarde’s emphasis last week that the Eurozone economy is “in a good place.” This central bank positioning divergence is affecting futures, with U.S. being cautious and Europe a bit more optimistic in tone.

2. Trump’s Remarks Create Policy and Political Uncertainty

President Trump’s latest statements are introducing fresh volatility into the market background. Pressure on the Fed days ahead of its meeting by calling for reduced interest rates, as well as remarks regarding tariffs, foreign policy stiffness, and commitment to NATO, underscore persistent geopolitical risks. His renewed commitment to building out domestic energy and manufacturing capability also suggests a protectionist bent that could raise sector-specific concerns. Investors are paying close attention to them as possible harbingers of shifts in U.S. policy that could percolate into equities, commodities, and currencies.

3. European Markets Consider Fiscal Stress and Geopolitics

Futures in Europe are trading modestly higher, although market sentiment is still weak. Last week’s rating of France’s credit by Fitch again brings into focus fiscal issues in the eurozone, while concerns regarding energy security due to the conflict in Russia-Ukraine remain a dampener in outlooks. Investors are also focused today’s data and ECB releases that could establish the tone of region’s growth path. If there are signs of strength in consumer spending or factory activity, then sentiment could stabilize, although geopolitical risks and fiscal imbalances pose still persistent risks.

Both U.S. and European futures show a balancing act among central bank support, political risk, and weak economies. Until this week, both marketplaces will be looking for a lead from the Fed and ECB, so volatility should continue to be high, as investors scrutinize each data offering and political message closely for signals about what lies ahead.

Digesting Economic Data

The TRUMP Tweets and Its Implications

President Trump’s comment frenzy in the past 48 hours is testament to the far-reaching impact of his remarks across markets and policy anticipations. On economic issues, Trump has taken responsibility for what he terms the “best stock market ever” while at the same time calling forth lower interest rates from the Federal Reserve. Such statements contribute to market volatility by throwing doubt over possible political interference in monetary policy, especially as investors are currently walking a tightrope balancing cooling inflation against slowing growth. His focus on tariffs and presidential power over them injects further unpredictability into a trade policy that has in the past been a catalyst in equity, currency, and commodity market swings.

On the geopolitical side, Trump’s pledge to dig in his heels over foreign policy, ratification of sit-downs with European leaders over the Russia-Ukraine conflict, and caution over global flashpoints highlight his intention to maintain national security as a key focus of his administration’s agenda. Remarks on partnership with NATO and preparedness to send in the National Guard to several U.S. cities show an increase in focus both on homegrown security threats as well as global security risks. Those signals increase the geopolitical risk premium, often prompting flows into safe-haven assets like gold and the U.S. dollar, while at the same time stoking volatility in risk-sensitive assets like equities and oil. His comments that India and Russia are lost to China’s orbit also show a possible realignment of alliances, which in the longer term could reshuffle trade as well as energy flows. Beyond capital markets, Trump’s mention of homegrown energy production, factory resilience, and infrastructure innovation—an initiative to deploy test fleets of flying air taxis, for example—demonstrate an administration that is focused on driving key sectors of the economy. While such moves might muster enthusiasm in aerospace, defence, and energy shares, such initiatives also underscore an activist policy approach that might induce sectoral volatility. His renewed focus on more aggressive Chinese economic pressure, coupled with immigration raids and industrial policy, signals a move towards protectionism that might have ripple effects across global supply chains and trade-exposed industries. Investors should, therefore, take this combination of industrial policy and trade ambiguity with sensitivity in terms of looking at cyclical sectors as well as at global integration-dependent companies.

Lastly, Trump’s remarks about domestic turmoil—ranging from allegations about Chicago’s circumstances being “worse than Afghanistan” to repeated statements about requiring National Guard deployments—constitutes yet another layer of political risk that market participants can’t overlook. Such remarks, in combination with previously declared investigations by him into individuals such as George Soros under potential RICO charges, enhances the risk of political turmoil within the country bleeding over into financial marketplaces. The more extensive implications are that while investors react favorably in initial response to his market-supportive speeches regarding stocks, as well as his market-supportive speeches regarding interest rates, surrounding uncertainty regarding tariffs, international policy, and national security might cause volatility across asset types. At Zaye Capital Markets, in our view, investors will need to compensate both for price potential of pro-growth measures as also for downside risks associated with policy unpredictability, as such dynamics will continue to be a predominant market driver over ensuing months.

Retail Frenzy and the Meme Stock Resurgence

Since early April 2025, the UBS Meme Basket has gained by almost 64%, much more aggressively than defensive sectors like U.S. consumer staples, up 4.6% in the same time frame. The dramatic deviation illustrates renewed retail investors’ enthusiasm for speculative plays, fueled by word-of-mouth campaigns in social media that propel prices substantially above fundamentals. The historical track record, with earlier 2020-2021 spurts, indicates that meme movements could expand valuations by up to 50% above intrinsic value, emphasizing that sentiment, not earnings, typically determines short-term performance. The resilience of this retail-led upsurge should be evaluated by analysts, especially in value-sensitive sectors. Conversely, consumer staples continue to appear undervalued, representing a possible opportunity to reallocate to cash-flow stable businesses underappreciated in this rotation.

On a macro level, this speculative assets surge is in direct contrast to persistent consumer durability in staples. Returning grocery volume growth in 2025, after missing it in 2020, shows continued confidence in core staples despite investors’ pursuit of high-beta names. The disconnect in consumer behavior and market speculation also feeds concerns about equity market stability at a higher level. Liquidity and volatility can be stoked by retail enthusiasm, yet it also brings downside risk as sentiment shifts. Traders should keep a close eye on trading volumes, short interest, and social sentiment gauges, as any reversal of narrative could precipitate sudden selling in such high-beta names. In the meantime, staples and utility companies with robust business models may continue to offer a speculative unwind hedge. Twice over, there are implications for retail investors: although meme stocks yield spectacular short-term profits, they leave portfolios vulnerable to higher volatility and drawdowns as soon as momentum dips. For institutions, increased weight of such names in volumes makes portfolio benchmarking harder, at times requiring unpleasant decisions about whether to pursue momentum at the cost of sacrificing discipline. In the near term, opportunities lie in underappreciated financials and a few consumer discretionary names, in which valuations remain squeezed relative to earnings potential. Analysts should keep a close eye on conditions in credit, spending data by consumers, and shifts in sentiment that might send capital back out of speculative buckets and into fundamentally robust sectors with durable growth.

Upcoming Economic Events

Empire State Manufacturing Index, ECB President Speech by Lagarde

With markets preparing for a critical week, focus will be completely centered on U.S. regional manufacturing data and an important policy guidance by Europe’s highest monetary official. Both of these events could impact global risk appetite, currencies, as well as rotation of sectors in equities. Here is our what to watch and how market reaction will take place based on results.

Empire State Manufacturing Index

The Empire State Manufacturing Index gives a timely indication of conditions in the New York district, and it’s often seen as a leading indicator of more general U.S. manufacturing trends.

- If in fact the actual number prints higher than expected, it would be a sign of healthier factory activity and strength in industrial demand. That could boost cyclical sectors such as industrials and materials, also fan speculation that the Federal Reserve might resist sharp rate cuts, and in turn lift Treasury yields as well as support the U.S. dollar.

- If, though, the reading prints softer than expected, it would be evidence of persistent softness in manufacturing, reinforcing argument in favor of policy easing. Markets would take it as a risk-off flow back into bonds and defensive equity plays such as utilities and staples.

ECB President Lagarde Speaks

European monetary policy guidance is key as investors seek whether the European Central Bank will continue its cautious stance or offer more accommodation.

- If Lagarde strikes a hawkish tone, emphasizing inflation risks and warning against widespread appetite for cutting rates, it will see a strengthening of the euro, with European financials and banks benefiting due to expected stiffer margins. Equity markets more broadly, however, could take a blow under tighter policy prescriptions.

- If, though, Lagarde’s remarks are dovish, approaching risks of growth and leaving easing prospects alive, it should weaken the euro while lifting risk sentiment across European equities. Defensive shares could underperform in such a scenario as investors seek out growth-sensitive names.

Stock Market Performance

Indexes Bounce Back From April Lows, But Breadth Still Tenuous

At Zaye Capital Markets, we remain focused on U.S. equity markets as it displays robust recoveries versus that of April 8 low. Still, while headline advances prevail, index-level declines and average constituent softness denote a beneath-the-surface absence of widespread participation.

Our current update of major index activity by recent data is as follows:

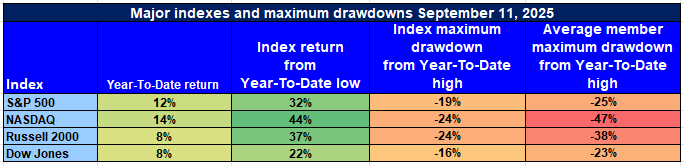

S&P 500: Strong Rebound; Narrow Leadership Persists

YTD: +12% | Low: April 8th Low: +32% | Drawdown from YTD High: -19% | Avg. Member Drawdown: -25

The S&P 500 continues to post big gains, ahead 12% this year and 32% from the April low. But after a 19% index-level loss and 25% average member decline, this is a market being driven by a clique of standout shares.

NASDAQ: Tech Momentum Outshines, But Volatility Lingers

YTD: +14% | Low Since April 8 Low: +44% | Drawdown from YTD High: -24% | Avg. Member Drawdown: -47%

NASDAQ outpaces key indexes this year, jumping 44% from April lows. However, a 24% index-level decline and sobering 47% mean member pullback highlight extreme concentration risk and high volatility in the technology space.

Russell 2000: Small-Cap Resurgence, But Fragile Foundation

YTD: +8% | Low: April 8 Low: +37% | Drawdown from YTD High: -24% | Avg. Member Drawdown: -38% The Russell 2000 is rebounding by 37% so far, though year-over-year advances continue soft at 8%. Repeating 24% index-level corrections and sharp average member losses continue to keep small-cap sentiment soft.

Dow Jones: Relative Stability, But Still Low Participation

YTD: +8% | Low: April 8 Low: +22% | Drawdown from YTD High: -16% | Avg. Member Drawdown: -23% Dow’s defensive slope is manifesting in an 8% YTD rise and lowest drawdown among indexes. However, a 23% average member decline indicates persistent stress in value names.

Zaye Capital Markets remains selective, betting on fundamentally sound names while also being critical of market breadth and volatility more broadly.

Earnings

Yesterday’s Earnings (12-Sept-2025)

- OFS Credit Company, Inc. (OCCI)

OFS Credit reported its Q3 2025 results for the quarter ended July 31, 2025. Net Investment Income (NII) rose to $6.1 million, or $0.22 per common share, up roughly 17% from the prior quarter. However, core NII, adjusted for certain non-recurring items, declined to $8.5 million ($0.31/share) compared to $9.2 million previously, reflecting some margin pressure. Net Asset Value (NAV) per common share slipped slightly to $6.13 from $6.17, largely due to distributions exceeding earnings, though investment gains offset part of the decline. The portfolio’s interest income yield stood at 14.38%, with certain new investments delivering yields above 19%, signaling high-risk/high-return positioning.

- Golden Matrix Group, Inc. (GMGI)

Golden Matrix’s most recent update showed a weak performance, with Q2 2025 earnings per share of −$0.03, missing forecasts that expected near break-even. Revenue came in at approximately $43.25 million, also below expectations. The combination of revenue shortfalls and negative earnings highlights ongoing operational headwinds, with the company under pressure to deliver growth and margin improvement in a competitive gaming and digital content landscape.

- Quantasing Group Ltd. and Barnes & Noble Education, Inc. (BNED)

For QuantaSing Group Ltd. and Barnes & Noble Education, no updated results specifically dated 12 September 2025 were released. However, Barnes & Noble Education’s next earnings release remains scheduled around mid-September, which means markets are awaiting confirmation of trends in campus retail, textbook rentals, and digital learning demand.

Earnings on 12 September highlighted both resilience and vulnerability. OFS Credit showed healthy income growth but also signs of margin pressure and NAV erosion, while Golden Matrix underscored weakness in revenue momentum. With smaller names like QuantaSing and BNED pending updates, investors should remain cautious, tracking whether upcoming releases show improving fundamentals or continued strain.

Today’s Earnings (15-Sept-2025)

- Dave & Buster’s Entertainment, Inc. (PLAY)

Dave & Buster’s will release its Q2 2025 results today after market close. Consensus expectations point to earnings of $0.92 per share and revenue of about $562.78 million. Investors will focus on same-store sales performance, the balance between food, beverage, and entertainment revenues, and any margin pressure stemming from labor and input costs. Guidance on cash flow generation and debt management will also be critical, especially against a backdrop of softer discretionary spending.

- Rezolute, Inc., Radiant Logistics, Inc., and LightPath Technologies, Inc.

These three companies are also scheduled to release earnings today, though detailed market estimates have not been widely published. For Rezolute, investors should watch updates on its clinical pipeline progress and R&D expenditure trends. For Radiant Logistics, freight demand, cost controls, and margin resilience will be central themes, given the cyclical nature of logistics. LightPath Technologies, meanwhile, will be watched for developments in optical components demand, revenue diversification, and gross margin stability as competition in photonics intensifies.

Earnings scheduled for 15 September place Dave & Buster’s in the spotlight, with markets expecting solid revenue performance but wary of potential margin erosion. For smaller firms such as Rezolute, Radiant Logistics, and LightPath Technologies, the focus will be less on near-term earnings and more on strategic progress, cost discipline, and sector-specific demand signals that could shape their trajectory through the rest of 2025.

Stock Market Summary – Monday, Sept. 15, 2025

U.S. shares started Monday in quiet mode as investors made preparations in advance of this week’s Federal Reserve policy meeting. Skepticism about how much in rate cuts there will be, coupled with stretched valuation in the growth sector and mixed signals in the economy, is tempering acceleration following recent sharp gains by mega-cap tech.

Stock Prices

Economic Signs and Geopolitical Events

Up next will be the Fed meeting, which will be in focus and is set to offer guidance about the timing as well as extent of rate cuts. Softer labor market numbers as well as fears about slow growth keep raising expectations of a dovish mistake by the Fed. Trade policy, however, remains a potential wild card: new U.S.-China official-level discussion has cooled some of the heat out of tensions, though risks around tariffs persist.

Latest Stock News

One of the large ETF managers, responsible for a $40 billion asset base, warned that over-exposures by the market to so-called “Magnificent Seven” tech giants—such as Microsoft, Nvidia, Amazon—is creating concentration risk. He pointed out that the seven now represent more than half of the weight of the Russell 1000 Growth Index, and challenged investors to take notice of underweights in small-cap techs and defensives.

Magnificent Seven and S&P 500 Index

In the background, as the S&P 500 continues to rise near historical highs led by advances in large-cap technology, the Magnificent Seven come under further pressure. The group’s valuations are being questioned as recent behavior appeared out of whack relative to normalized earnings acceleration and fundamental economics. The group is being pushed back by overvaluation signs as much as by concerns about sustaining expansion, leading investors to be cautious about further advances without more substantial underlying data.

Major Index Performance at Monday, September 15, 2025

- S&P 500: Closed at 6,584.29 on September 12, 2025. (F

- Nasdaq Composite: Closed at 22,141.10 on September 12, 2025. (The

- Russell 2000: 2,397.06 as of September 12, 2025.

- Dow Jones Industrial Average: Closed at 45,834.22 on September 12, 2025.

We remain risk/reward focused in mega-caps relative to more cyclical market exposure. Appropriate valuation inflections, earnings durability, and Fed direction will determine whether market breadth expands or further contract.

Gold Price

As of today, gold is at USD $3,637.60 per troy ounce. First, Trump’s recent remarks—particularly discussion of investigating Soros (potential legal/RICO claims), digging in his heels over foreign policy in a tense global environment, as well as advocating for reduced interest rates—combined with geopolitical tensions (e.g., European leaders meeting, war-themed diplomacy) in such settings, gold benefits as a safe-haven asset. The market perceives higher risk due to political interference in institutions (up to and including the Fed), tariff and trade policy uncertainty, and elevated global tensions; all of these work to undermine confidence in fiat assets and support gold demand. With market participants in this scenario already forecasting reduced rates (or at least a dove-like bias) by the Fed, the expense of carrying non-yielding assets such as gold becomes increasingly non-penal, bolstering its allure. Accordingly, Trump’s combination of policy and rhetorical risks is driving gold up.

Second, there are key data releases in the Empire State Manufacturing Index and speech by ECB President Lagarde. If the Empire State Index prints softer than anticipated, that would be suggestive of slowing U.S. manufacturing/weaker growth, typically bullion supportive (through reduced real interest rates and softer USD). However, a stronger print could take away some of gold’s gains if investors assume that the Fed will remain hawkish for longer. Speech by Lagarde—depending on whether she indicates tightening or not—has the ability to affect risk sentiment in Europe and impact relative strength/weakness of both dollar and euro, which in turn affects gold. Data that emerged yesterday (e.g. weak labor market/ inflation signals, mixed earnings) has already been sufficient to instill cautious market sentiment, prone to drive investors to move into safe-havens. Net impact is that gold currently shows widely supportive fundamentals, and gains possible if economic surprises remain weak and political risk remains high.

Oil Prices

Brent crude is currently trading around USD $67.02 per barrel, with U.S. West Texas Intermediate (WTI) at around USD $62.77 per barrel, reflective of a market subjected to both the push of higher supply as well as the pull of geopolitical risks. On the supply side, world oil output will increase by around 2.7 million barrels per day in 2025 due to OPEC+ additions to production as well as higher output by the U.S., Canada, Brazil, as well as Guyana. Yet, concurrently, demand growth will maintain modest figures of around 700,000-740,000 barrels per day, leaving the market at risk of surplus. The supply-demand mismatch usually induces downward pressure, yet geopolitical happenings are thwarting a steeper decline. Recent Ukrainian drone strikes against Russian infrastructure—in this case, major export terminals like Primorsk as well as refineries like Kirishi—have added a significant risk premium into the market by placing Russian crude as well as fuel flows at risk. This indicates proof of a fine balancing act wherein over-supply concerns act upon fundamentals, while disruption by geopolitical occurrences as well as infrastructure risks functions as a balancing agent that maintains prices more elevated. Trump’s latest comments introduce further complication. Sanction pressures against Russia, NATO reaffirmations, and vows to remain strong in foreign policy increase supply uncertainty, as any measure that cuts Russian export availability could compress margins. Meanwhile, Trump’s call for softer monetary policy feeds oil indirectly by easing the commodity-sensitive dollar and improving commodity allure. Yesterday’s softer U.S. labor numbers and mixed inflation signals, though, raise doubts over growth acceleration, fuelling concerns of weakening demand. This balancing act of supply expansion, softer demand prospects, and geopolitical tensions accounts for oil price action’s rugged texture. In the days ahead, today’s events will prove critical: should the Empire State Manufacturing Index exceed expectations, stronger industry activity could assuage concerns over weakening demand, sending oil potentially downside as focus shifts back towards oversupply. Conversely, a disappointing read would fortify slowdown fears, strangely bolstering prices as investors believe dovish monetary conditions will remain accommodative. ECB President Lagarde’s speech could also prove critical—hawkish rhetoric could stiffen the euro and harden the U.S. dollar, taking oil downside, while a dovish tone could lift risk appetite and commodity price pressures. Under current conditions, oil stays in a range, with market players balancing the fragile equilibrium of oversupply fundamentals against elevated geopolitical tensions.

Bitcoin Prices

Bitcoin currently trades at around USD $115,374 per coin, remaining just above the $115,000 level after touching on lower levels briefly, and stays around 92% higher year-over-year. The strength indicates wider risk-on sentiment across global markets despite a small 0.5% decline compared to Monday. The asset remains flipping back and forth across key support at $114,000 and around $116,200–$116,800 resistance zones, as market participants keep a close eye on whether there will be continued strength at such junctures ahead of key economic releases. Market structure remains underpinned by robust fundamentals: blockchain data firm Glassnode indicates that more than 82% of Bitcoin supply is now illiquid, citing squeezed circulating float, while futures open interest has shot up to $18 billion, as of Tuesday, highest since March, in a signal that institutions are taking part. Meanwhile, family offices as well as funds are diversifying into Bitcoin and hard assets, as Goldman Sachs research cites rising allocations, while Coinbase sees inflows from European investors at a new high. The moves suggest that Bitcoin is being increasingly seen as a strategic asset class instead of being treated as a speculative toy. Meanwhile, corporate participation remains to support confidence, with MicroStrategy reaffirming it will not shed holdings, now over 240,000 BTC, and as per Ark Invest’s Cathie Wood, who termed it her highest conviction long-term bet. Trump’s comments are also feeding directly into the Bitcoin narrative. His vow to stand firm on foreign policy amid intensifying global tensions, renewed rhetoric on tariffs, and pledges to pressure the Fed for lower interest rates add layers of uncertainty that often boost Bitcoin as a hedge against political and policy volatility. The geopolitical backdrop—including White House confirmation of meetings with European leaders on the Russia-Ukraine war and talk of targeted tariffs—creates risk factors that undermine confidence in fiat systems, encouraging flows into decentralized assets. Yesterday’s softer economic data, including weaker labor indicators and mixed inflation readings, has reinforced expectations that the Federal Reserve will lean dovish, lowering the opportunity cost of holding non-yielding assets such as Bitcoin. This macro environment, coupled with Trump’s political stance, enhances Bitcoin’s appeal as both a hedge and a growth-oriented alternative store of value. Looking ahead, today’s Empire State Manufacturing Index and ECB President Lagarde’s speech could drive near-term volatility. A stronger manufacturing print may revive growth expectations and temper Bitcoin’s upside as liquidity assumptions shift, while weaker numbers would bolster the slowdown narrative and further fuel demand for Bitcoin as a hedge. Overall, Bitcoin’s trajectory sits at the intersection of macro policy expectations, institutional adoption, and political uncertainty, keeping it firmly in play as one of the most closely watched risk assets in the current cycle.

ETH Prices

Ethereum (ETH) is currently trading in the $4,400–$4,460 range, with the latest tick at $4,460.89, reflecting a 2.6% intraday gain. This move underscores a broader rebound across digital assets as institutional demand regains strength. Key technicals show support consolidating around the $4,200–$4,300 zone, while resistance is clustered near the $4,800–$5,000 level, an area ETH has tested multiple times but not yet managed to break through decisively. This structure suggests that a sustained push above $5,000 could unlock fresh upside momentum, but failure to breach may trigger consolidation. Importantly, institutional flows are proving pivotal in price direction. Recent reports highlight more than $638 million in net ETF inflows, reversing weeks of weakness, which signals growing appetite from traditional finance channels. At the same time, the narrative of ETH as the backbone of decentralized applications, DeFi, and tokenization remains intact, ensuring that interest extends beyond short-term speculation into structural allocation by both retail and institutional players.

Whale activity is also providing an essential backstop for Ethereum’s price. In recent sessions, whales accumulated more than $204 million worth of ETH as the asset rebounded above $4,400, with on-chain data showing that large holders increased their balances by roughly 14% over the past five months despite volatility. This steady accumulation reflects confidence in ETH’s medium- to long-term prospects, reinforcing the view that downside risk is being absorbed by well-capitalized investors. However, flows via ETFs reveal a split picture: while recent days have brought heavy inflows, earlier in September Ethereum ETFs suffered $787 million in outflows, reflecting fragility in sentiment. The tug-of-war between whale accumulation, ETF flows, and broader macroeconomic pressures—such as interest rate policy and regulatory uncertainty—will determine whether ETH can sustain this rebound. If institutional inflows persist and whales continue to absorb supply, ETH could mount a sustained challenge of the $5,000 resistance zone. Conversely, renewed outflows or macro headwinds could keep the asset locked in consolidation.