Where Are Markets Today?

We at Zaye Capital Markets see U.S. equity futures modestly lower to flat and European futures slightly softer to start Monday, September 22, 2025. The U.S. pullback follows record closes and reflects profit-taking plus policy ambiguity after the recent 25bp cut—traders want clarity on the pace of additional easing and on this week’s inflation cadence, so index futures are marking time rather than extending highs. In Europe, futures mirror the caution amid sticky inflation in the bloc and the translation of U.S. rates guidance into a choppy dollar/euro dynamic, which complicates the outlook for exporters and keeps risk appetite contained.

For the United States, two drivers account for why futures come in this direction. One, policy direction: markets are divided on how soon further reductions could come, and today’s central-bank commentary can spark real yields and the USD—important drivers of long-duration tech and cyclicals. Two, positioning and valuation: following through on an impressive rally to new highs, leadership convergence and over-stretched multiples provide little wiggle room for disappointment, and as such, tactically reducing on data and Fed commentary as opposed to chasing. At this stage, earnings micro-catalysts in large-cap tech and finance remain swing factors, most notably in areas where associated capex and margin stories surrounding AI links are most stretched. For Europe, two drivers dominate in the softer tone. Firstly, ECB–Fed divergence risk: if America becomes more reliant on easing and core euro-area inflation persists, European curves and FX can stay volatile, hurting cyclicals and export-sensitive benchmarks. Secondly, combination of growth and energy: spotty industrial pace and dependence on energy/import prices keep risk premia solid, supporting a defensive mindset in futures in front of this week’s domestic data. The currency climate adds another factor—any increase in the euro against peers can put stress on external competitiveness at just the time order books and pricing power remain shaky in prime centers.

risk from an American FOMC voter and chief of the Bank of England can swing front-end rates; hawkishness (emphasis on sticky services inflation) would likely cap futures through higher real yields and a stronger dollar, while dovishness (labour downside risks, patience) would stabilise the tape and support duration-sensitive areas. Near-term, we’re following breadth, earnings-revision momentum, and factor leadership: broadening beyond mega-caps would cause dips to be bought; not broadening leaves futures at risk of further de-rating on macro surprises.

Major Index Performance — Today (Mon, Sept 22, 2025)

- Nasdaq Composite: previous close 22,631.48; initial response relatively softer.

- S&P 500: previous day’s closing 6,664.36; preliminary indications near unchanged to slightly down.

- Russell 2000: last close 2,471.96.

- Dow Jones Industrial Average: last close 46,315.27.

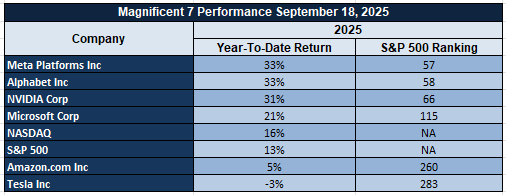

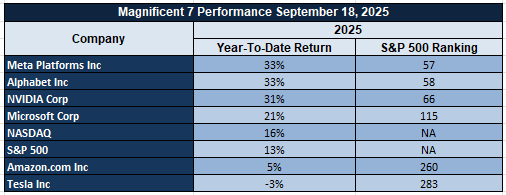

The Magnificent Seven and the S&P 500

We’re witnessing increased attention on the mega-cap group driving the index. Many members are navigating double-digit down swaths from recent highs as (i) elevated real yields test long-duration cash flows, (ii) tariff/export restrictions muddy demand and supply chains, (iii) AI capex comes to earth vs. steeper comps, and (iv) regulatory chatter diminishes optionality in advertising, app stores, and data platforms. Until breadth recovers, the S&P 500 is vulnerable to multi-compression on macro surprises.

Drivers Behind the Movement in Market

We at Zaye Capital Markets see today’s sentiment as being influenced by podium risk, geopolitics, and positioning after last week’s records. In U.S. and European futures, they’re fading strength and waiting for new cues on rates, the dollar, and earnings durability—yet commodities (specifically, gold) display persistent risk premium at/in cycle highs.

- Policy podium risk (today):

A keynote speech by one of the critical US rate-determiners and commentary by the head of the UK central bank keep front-end rates, the dollar, and duration in focus. A hawkish bend—focus on sticky services prices inflation or reluctance to ease further—would tighten financial conditions and strain long-duration equities; a dovish move—labour risk, patience—would relax the dollar impulse and support rate-sensitives. Europe echoes this theme in terms of ECB/BoE-Fed divergence risk and currency sensitivity for exporters. (Dates firmed on official calendars.)

- Geopolitics and the “Washington tape”

The latest set of statements from President Donald Trump—covering security posture (Afghanistan/Bagram), maritime interdictions, prosecutorial moves, platform governance, and leader-level engagement with China and Turkey—adds headline and policy uncertainty. Markets typically price this as modestly wider risk premia (energy, FX, and haven assets) with direction set by whether talk translates into tariffs/sanctions or de-escalation. Any tangible thaw in U.S.–China engagement supports cyclicals and supply-chain equities; escalation sustains a defensive bias. (Recent futures softness aligns with this caution into event risk.)

- Inter-asset confirmations (yesterday → today)

As futures retreated after last week’s rally to records, data-dependence vs easing hopes weighed on traders; meanwhile, gold swung near all-time highs, in tandem with policy-cut expectations and geopolitical hedge-ing. That mix favors a higher-volatility, event-driven regime: risk assets stall on hawkish indicators, and havens gain as uncertainty grows. We watch for this Tuesday’s speeches and this week’s inflation print to know if breadth can bounce back—or if the market remains narrow and responsive to macro surprise.

Digesting Economic Data

The Twitters of Trump And Their Implications

We at Zaye Capital view the security-related messages—claims of retaking control of a critical overseas air base, announcements of maritime interdictions, and threats related to Afghanistan— as adjuncts to the geopolitical risk premium. In financial markets, this combination usually raises event risk in energy transit and defense supply chains, pushes crude volatility, safe-haven demand (gold, high-grade duration), and the dollar’s bid higher. The policy vector makes a difference: if this signal presages wider security stances or sanctions dynamics, we would expect steeper term premia and tighter global financial conditions; if they prove episodic without new policy bites, the effect is more headline-centric and fleeting.

A second thread focuses on institutions and legal architecture: exhortations to increase prosecutions of political opponents, personnel shifts around prosecuting authorities, developments in litigation, and discussion of information limitations for the press. Markets value this as governance risk—fat-tail risk to increase equity risk premia, bolster volatility, and take a toll across multiple expansion where discretionary regulation is an important input (platforms, financials, health-adjacent services). Credit channels also experience it in the form of increased risk compensation, especially at the long end if investors require extra carry for variability of rule of game. The tape on diplomacy suggests an alternative direction. Hints of trade progress, an imminent White House meeting with one of China’s biggest regional leaders, an unusual congressional overture to China, and scheduled head-of-state meetings broach the chance of incremental thaw. For risk assets, that’s positive if it means fewer tariff jolts, more stable export controls, and clearer channels for tech and supply-chain cooperation. Platform governance developments surrounding one of China’s largest short-video operators—accompanied by news of an American operating model—reduce, but don’t do away with, ad- and data-driven equities’ regulatory overhang. At the same time, guidelines on skilled-worker visa fees ease frictions in talent pipes, slightly bullish for margins in tech and services.

Multilateral optics and domestic signaling round out the picture: UN-week choreography, health-policy teasers, and cultural-political endorsements add noise that can move intraday positioning absent hard policy. Our base case is a higher-volatility regime with a modestly elevated equity risk premium until diplomacy produces tangible de-escalation or, conversely, security rhetoric crystallizes into enforceable measures. Positioning wise, we stay barbelled—owning durable cash-flow defensives and selective cyclicals with backlog visibility—while managing headline risk across FX (USD sensitivity to policy tone), rates (term-premium swings), and commodities (geo-linked energy spikes).

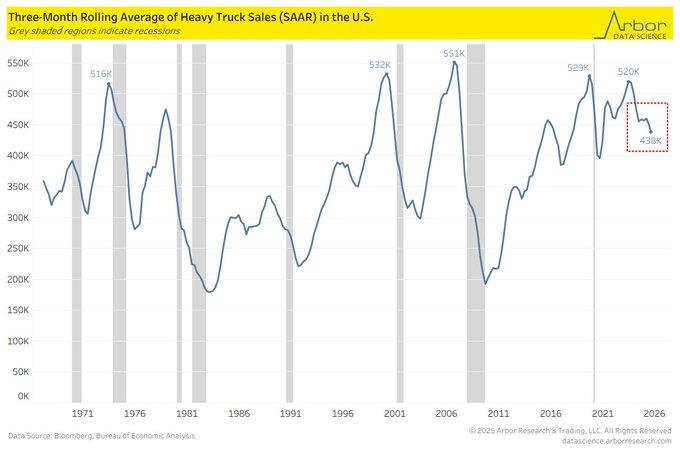

Heavy Trucks Indicate Larger Late-Cycle Softness

We at Zaye Capital Markets watch U.S. heavy truck sales (SAAR) decline to ~438k in August 2025 from north of 500k earlier this year—a rapid, across-the-board retrenchment in one bellwether for goods appetite, freight capacity, and industrial capex. The six-month decline, in combination with roughly mid-teens year-over-year contraction, suggests trepidation at the freight carriers as spot rates trail, used-equipment prices re-price, and financing expenses—although moderating—remain above pre-cycle standards. In the past, such air pockets clustered around late-cycle slowdowns; today, services sector buoyancy and government sector expenditures act as buffers to the overall economy, but the goods side most definitely de-risks.

Our read: three intertwined pressures are at work. First, demand: inventories are leaner but not yet restocking aggressively, keeping order books choppy and backlog-to-build ratios drifting lower. Second, margins: fuel spreads and wage inflation squeeze operating leverage just as price discipline tightens, lifting break-even miles and discouraging fleet renewals. Third, capital: tighter credit boxes and softer collateral values raise required returns on new tractors, extending trade-in cycles. A durable turn would feature firmer spot/contract rate convergence, rising used-truck auction clears, sequential improvement in Class-8 net orders (ex-cancels), and stabilization in equipment-loan delinquencies.

From an equity perspective, we prefer balance-sheet strength and aftermarket mix in anticipation of clearer restock. Undervalued stock: CMI—diversified powertrain and components, scale in parts/service, and optionality in next-generation propulsion can fill trough earnings and enable multiple resilience into a volume re-acceleration. What analysts need to watch: monthly Class-8 orders vs. cancellations, OEM backlog lead time, used-truck price indices, ATA tonnage and intermodal loads, diesel crack spreads, and credit metrics across equipment ABS. Corroboration across these indicators would confirm base-building in freight, constrict capacity, and position for operating leverage on the next up-cycle.

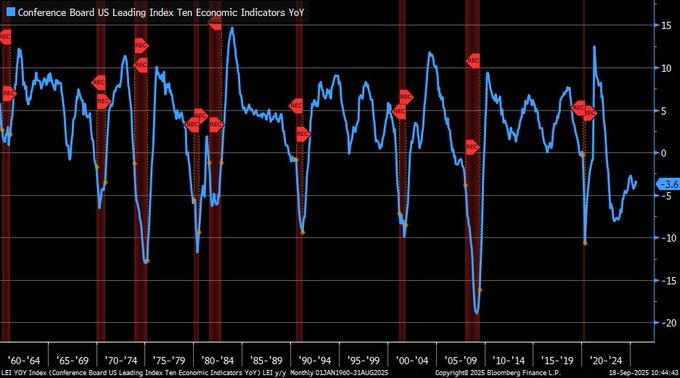

LEI Diffusion Underscores Fragile Growth Outlook

We at Zaye Capital Markets observe that the Conference Board’s Leading Economic Index (LEI) 6-month diffusion index fell to 25% in August 2025, historically incompatible reading for continuing expansions. Diffusion at below 50% and negative growth of over -4.1% as per the Board’s “3Ds rule” generally indicate high risk of recession. This precipitous decline points to fraying strength throughout forward-looking indicators—employment, housing, credit, and industrial production—indicating weakening momentum under headline GDP stability.

Our reading is for the U.S. cycle to remain stuck between services-led resilience and manufacturing-induced weakness. While inward capital flows to production centers overseas, as seen in Vietnam’s $320.7 billion in foreign capital inflows in processing and manufacturing, as indicators of global re-allocation of supply chains, they also underscore vulnerabilities: single-sector over-reliance, currency risk, and shifting trade balances. At home, stagnating LEI suggests domestic consumption fatigue, slowing recruitment, and stricter lending criteria could be undermining faith. Research on diffusion dynamics highlights that often these changes occur prior to weakness in top-line output, cautioning policy euphoria surrounding a “self-sustaining” recovery to be tested. From an equity perspective, narrowing diffusion necessitates selectivity. Undervalued stock: USB—a sizeable regional bank with conservative credit risk and cross-fee diversification, set to gain from eventual normalization of rates while enduring loan-loss cycles. Valuations already imply larger recession probabilities than our base case. What analysts need to monitor: near-term consumer confidence and credit availability surveys, ISM new orders slope, commercial loan delinquency, and revisions to payroll and household employment figures. Failure for breadth to stabilize may steer consensus to further easing and enlarge spreads between defensives and cyclicals in performance.

Manufacturers See Prices Paid Staying Elevated

We at Zaye Capital Markets observe an obvious disconnect in one of the largest regional manufacturing surveys: prices pressures have lessened in the near term, but prices paid in six months remain elevated. That gap indicates sticky input prices—energy, freight, and customized inputs—remain ingrained in supply chains despite weakening near-term activity. The same sequence through previous cycles historically seemed to signal tighter policy in coming periods instead of swift easing, suggesting the trajectory to easing rates could be gradual and contingent upon proof positive cost-push pressures indeed cease.

Global context rhymes: August indicators reported reacceleration in UK consumer inflation to 3.8% year-over-year, reminding us commodity and energy volatility can re-resurrect price impulses even as goods disinflation ages. For the United States, ongoing “prices paid” expectations imply margin risk for manufacturers who have poor pricing power and to a moderate inflation breakeven upside bias if input prices remain steadfast. Our base case remains slower, bumpier glide to target inflation, and policy recalibration more likely in later 2025 if forward indicators do not ease. On an equity basis, we prefer pass-through contracts and durable cash flows as long as input-cost volatility persists. Undervalued stock: KMI—volume-anchored midstream exposure with inflation-linked tariffs can protect EBITDA and underpin distribution growth as long as energy curves remain volatile. What analysts must watch: PMI “prices paid” vs. “prices received” spread in regional and national PMIs; intermediate-demand PPI; curves innatural-gas and diesel; industrials and logistics wage trackers; used-equipment trends; and long-end term-premium movements. We would take persistent narrowing in prices-paid indicators in combination with softer PPI as confirmation of multiple expansion for rate-sensitivities; otherwise, to remain overweight in cash-flow defensives.

Federal UCFE Claims Increase As Public-Sector Labor Stress Grows

We at Zaye Capital Markets note that weekly initial unemployment claims for federal employees jumped to roughly 1,200 in mid-2025—the highest since 2020—and, while off the peak, remain elevated versus 2022–2023 norms. The persistence suggests more than seasonal noise: hiring freezes, program consolidations, and procurement delays are likely tightening headcount just as broader labor momentum cools. With the share of long-term unemployment hovering near the mid-20s percent, skill mismatches and slower reabsorption risk extending durations and dampening household demand.

Our take: increasing UCFE notices serve as an early-cycle strain indicator for the public sector ecosystem. As agencies hold back hiring, jobs often migrate to projects, grants, and contract work; this migration, though, happens unevenly and can strain near-term production in case appropriations remain tight. Public-sector furloughs in the past have tended to spill over in local services and certain industrial end-markets before appearing in wider payroll changes. The policy signal is in favor of gradual relaxation, yet relief will still percolate slowly to rehiring, and the labor balance remains precarious until late 2025.

On an equity basis, we favor companies set to win outsourced federal workloads with robust backlog and cash conversion. Undervalued stock: LDOS—defense/civil sector exposure, mission-critical services, and long bid pipeline can make up for hiring delays within agencies; we believe budget and timing risk is over-discounted in relation to multi-year visibility. What analysts need to watch: weekly UCFE prints and continuing claims, federal quits and job openings, appropriations/CR deadlines, contractor book-to-bill and fully funded backlog, locality pay trends, and the temp-help index. A reversal in UCFE in combination with stickier awards and decreasing duration would confirm multiple expansion for federally levered names.

LEI Slide Flags Broader Cycle Fragility

We at Zaye Capital Markets observe the U.S. Leading Economic Index drop to around -3.6% y/y in August 2025—a decline historically clustering near slowdowns. Unlike during the post-2008 expansion period, in which LEI scarcely declined by more than -2%, today’s drawdown suggests weakening breadth in forward drivers. Manufacturing and housing—big weights in the LEI—have declined since mid-2024 as increased financing rates, slower new orders, and stricter credit criteria filtered through. The long-view trend (1960–2025) reveals downswings in LEI often accompanying outside-price shocks and financial tightening; today’s combination also features global supply frictions capable of spurring through import prices, freight, and stock piles.

Our read: the message is less about an imminent contraction and more about narrowing momentum. Goods demand is stabilizing at a lower run rate, capex selectivity is rising, and labor rebalancing is gradually lifting duration risk. If diffusion breadth fails to improve, policy may lean more accommodative, but the hurdle for aggressive easing remains evidence that cost-push pressures are truly receding. A base-case soft-landing still requires firmer order books, cleaner inventories, and steadier housing permits; absent that, growth expectations risk repeated downward nudges. On an equity basis, our preferences include long-duration cash flows with pricing strength and negative LEI. Undervalued stock: LIN—mission-critical industrial gases with multi-year contracts, high switching rates, and structural exposures to semis, health care, and energy transition; defensive growth and durable margins under-appreciated if industrial volumes only base-build. What to watch, analysts: LEI component breadth and 3-month momentum, ISM new orders vs. inventories, building permits and mortgage applications, NFIB plans to hire, credit terms and delinquencies, term premium and 2s/10s slope, and freight/energy cost trends. A sharp inflection in these would warrant multiple expansion beyond defensives.

Retail Sentiment Reversal Near Neutral

We at Zaye Capital Markets observe that one commonly followed retail-investor sentiment poll indicates the bull–bear spread springing back to around zero, and bullish replies leaping to around 42%, just shy of, but still modestly above, long-run average near 38%. The reversal would indicate investors have been easing back into risk, helped by sentiment that policy support and softening nominal earnings can belie growth scares. In the past, sharp sentiment recoveries from negative ground have often been an omen for attempts at late-phase rallies, not beginnings to sustainable advances.

Macro environment moderates the optimism. Mid-year 2025 tariffs and persistent input-cost volatility keep an inflation premium built into prices, and breadth and earnings reversion remain patchy. History suggests sharp sentiment recoveries can be followed by corrections in the subsequent 6–12 months in case fundamentals fail to affirm—particularly as financial conditions re-tighten or profit margins shrink. Base case: rougher ride for risk assets short of order books, pricing control, and forward-guidance trend establishing themselves decisively.

From an equity perspective, we favor exposures to win if volatility re-prices while continuing to compound through cycles. Undervalued stock: CBOE—justifiable market-structure assets, diversified mix of derivatives, and operating leverage to durable volume/volatility; we believe markets undervalue strategic optionality and cash generation. What to watch: advance/decline and 52-week highs breadth, put/call and skew in equities, credit spreads vs. implied vol, earnings-revision breadth, buyback velocity, and high-frequency pressure gauges of prices. Confirmation across these would support sentiment turn; failure supports fade-the-rally positioning.

Capex Intentions Slide Despite Headline Bounce

We at Zaye Capital Markets also observe a marked decline in a leading six-month factory capex index in September, as the same gauge’s headline activity momentarily recovered. The diffusion index—monitoring companies increasing vs. reducing investment—has edged down to neutral, traditionally an omen for factory payrolls and machinery purchases. Recent manufacturing job losses also confirm the signal of producers delaying large-ticket purchases in view of weakening new orders, restrictive credit, and persistent input-cost fluctuations.

Our view: this isn’t quite as broad-based withdrawal as it is mix shift. Businesses are turning to software, sensors, and process automation rather than greenfield expansion—hoping to boost throughput and reduce unit labor cost without boosting capacity in any way. It supports medium-term productivity but can hurt near-term recruitment and traditional equipment demands. Should backlogs fade and pricing power return to normal and financing remain restrictive, this pause in investment may endure through until orders, margins, and credit availabilities return to equilibrium.

For an equity view, we keep our money on cash-generating automation platforms with recurring revenue and balance sheet flexibility. Undervalued stock: EMR—broader process-automation exposure, growing software mix, and strong free-cash-flow position the stock to win as digital projects outpace heavy capex. What to watch from analysts: core cap-goods orders/shipments (ex-air), manufacturing hours and OT, regional “capex intentions” vs. backlogs, C&I lending standards and utilization, and “prices paid” vs. “prices received” spread. A move higher across orders, backlogs, and credit would affirm re-acceleration; without it, prefer efficiency winners over capacity stories.

Upcoming Economic Events

Heading into a critical period for monetary indicators, at Zaye Capital Markets, we’re paying attention to two podium risks capable of swinging rates, FX, and equity factor dominance in live time. Against one senior U.S. official and the chief of the Bank of England speaking, markets will dissect tone, direction, and any balance-sheet or labor-risk judgment inklings. What to watch—and how “stronger vs. softer than projected” results could have ripples throughout assets.

U.S. Federal Speaker (FOMC Member

- In the event that the tone comes in more hawkish than expected (hawkish surprise):markets would mark less/further-dated cuts. Front-end rates higher, long-end term premium higher, curve flattening bias; USD stronger; cyclicals and high-duration growth pressured while cash-flow defensives and short-duration value hold strong. Credit spreads could widen moderately as a consequence of higher real yields.

- In event of softer-than-anticipated tone (dovish surprise): Chances of premature/larger easing rise. Front-end yields decline with bull-steepening direction; USD declines; duration and rate-sensitives (quality growth, regulated utilities, REITs) benefit; credit tone improves as refinancing rates decline.

What to pay attention to: labor-market downside risk terms, core/services inflation mentions, balance-sheet runoff frequency, and policy repositioning trigger points.

Bank of England Speaker (Governor)

- In case of guidance being stronger than expectations (hawkish surprise): Gilts sell-off at front end; GBP strengthens; UK-sensitive risk assets move defensively; overseas rates see sympathy bid lift higher. Imported-inflation vigilance and wage dynamics discourse would support “higher-for-longer” in Britain and be mildly hawkish for international curves as well.

- In case of dovish surprise (guidance softer than anticipated): Gilts rally; GBP weakens; UK domestics and rate-sensitives receive a bid; global duration gains. Any stress on slowing activity, easing labor pressures, or patience for below-trend growth would favor an earlier easing trajectory.

What we’ll be hearing: inflation persistence vs. services disinflation, wage/settlement debate, trajectory of QT, and patience for slower growth to reestablish price stability.

Positioning lens: We prefer maintaining optionality through event-risk hedges through front-end rates and FX, and a barbell in equities (good quality cash flows + selective cyclicals). Confirmation of dovish skew would affirm increment in duration; a hawkish skew would support narrower risk budget and strong preference for short duration and durable free-cash-flow drivers.

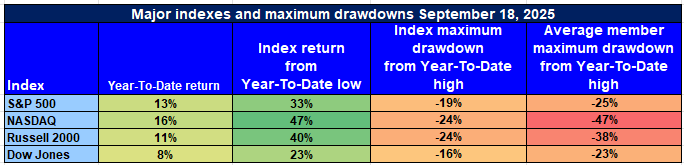

Stock Market Performance

Indexes Recover Off April Bottoms, but Damage under the Surface Seen Deep

We at Zaye Capital Markets observe an economy characterized by two truths simultaneously: strong reversals from the April 8 low and dramatic constituent-level destruction still limiting optimism. Indexes appear healthy; average members continue to bear heavy drawdowns. That dichotomy maintains volatility in factors, limits leadership, and insists upon time and quality selection.

S&P 500 — Strong Headline, Thin Underpinning

YTD: +13% | +33% off April low | -19% from YTD high | Avg. member: -25%

The S&P 500’s year-to-date gain and outsized rally from the April low argue for durable earnings and liquidity support. Yet the average member’s -25% slide from its own YTD high pairs with a -19% index drawdown, telling us breadth is still incomplete. This is a classic “top few carry, middle struggles” setup—fine for momentum while liquidity is friendly, unforgiving when macro surprises reprice duration or risk premia.

NASDAQ — Leadership Shines, Internals Suffer

YTD: +16% | +47% below April low | -24% from YTD high peak | Average member: -47%

A dramatic +47% surge off the April trough reinforces growth leadership, but the average component’s -47% drawdown from its YTD high is a stark reminder of fragility beneath the megacaps. With the index itself -24% from peak, rallies can run, but they rest on narrow pillars. When real yields or policy tone shift, dispersion widens, crowding risk climbs, and factor reversals can be abrupt.

Russell 2000 — Small-Cap Rebound, Confidence Still Rationed

YTD: +11% | +40% below April low | -24% below YTD high | Avg. member: -38%

Small-caps have erased +40% from their April low, yet the index trails its YTD high by -24% and the average constituent -38%. That combination breeds financing sensitivity, uneven pricing power, and scant balance-sheet buffers. The way forward likely hinges on clearer order-stability indicators, easing credit frictions, and further margin insulation.

Dow Jones — Shallower Index Injury, Member Stress Persists

YTD: +8% | -23% lower than April low | -16% lower than YTD high | Avg. member: -23%

The Dow’s more defensive mix shows: a smaller -16% index drawdown and steady +23% rebound from April. Even so, the average member’s -23% drop from its high reveals that classic value cohorts aren’t immune to earnings revision risk or factor whipsaws when macro signals blur. Our Positioning Lens

We prefer selective discipline: overweight in durable free-cash-flow compounders with pricing power and having pristine balance sheets; pair with select cyclicals in which operating leverage can reassert itself. Use volatility tactically—own optionality at policy and data inflections. End confirmations we’re monitoring: breadth thrusts, earnings-revision breadth, credit spreads vs. implied vol, and factor concentration. Until average-member drawdown indicators recover, we consider strength as conditional and seek evidence of participation broadening before upgrading risk.

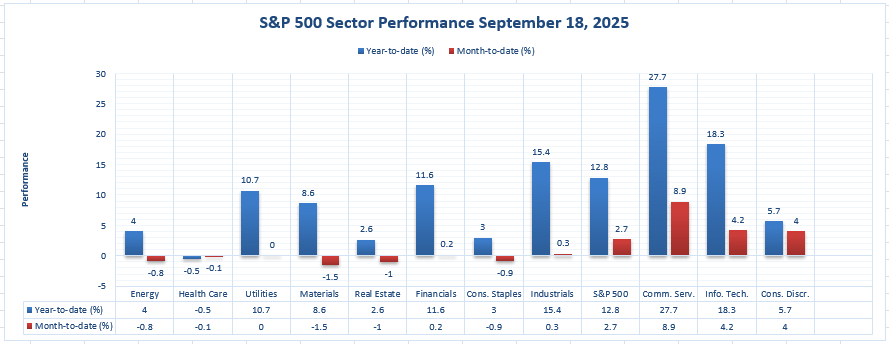

Strongest Sector in All These Indices

Communication Services Remains at YTD and MTD Leader; Tech and Industrials Follow

We at Zaye Capital Markets take this latest sector tape as an unambiguous leadership indicium: Communication Services leads both horizons – +27.7% YTD and +8.9% MTD – bettering the S&P 500 at +12.8% YTD and +2.7% MTD. Strength across the board compared to peers and validates where momentum and earnings durability are being rewarded.

Next level of leadership:

- Information Technology: +18.3% YTD, +4.2% MTD—firmly positive on both frames.

- Industrials: +15.4% YTD, +0.3% MTD—solid annual gain with a flatter monthly print.

- Financials: +11.6% YTD, +0.2% MTD—steady, modestly green in the month.

- Utilities: +10.7% YTD, 0.0% MTD—double-digit YTD, flat near-term.

Middle of the pack:

- Materials: +8.6% YTD, -1.5% MTD

- Consumer Discretionary: +5.7% YTD, +4.0% MTD

- Energy: +4.0% YTD, -0.8% MTD

- Consumer Staples: +3.0% YTD, -0.9% MTD

- Real Estate: +2.6% YTD, -1.0% MTD

Lag

- Health Care: -0.5% YTD, -0.1% MTD

Our view: The Communication Services sector (+27.7% YTD / +8.9% MTD) leads on all fronts, and Information Technology (+18.3% / +4.2%) and Industrials (+15.4% / +0.3%) support leadership dominance. We will pay attention to whether monthly breadth extends beyond these leaders or if defensively strong in YTD—such as in Utilities (+10.7%/0%)—segments join in alongside the index (+12.8%/2.7%).

Earnings

Earnings Recap — Yesterday (19-Sep-2025)

- MoneyHero Limited (MNY)

- We at Zaye Capital Markets reviewed the tickers you flagged. Of the four, only one posted results on 19-Sep-2025. MoneyHero Limited released Q2’25 before the open. Headline takeaways: turned profitable for the quarter (net income positive) with continued top-line traction. Focus items: paid-marketing efficiency, take-rate by product, and cash runway relative to growth investments. Watch any commentary on regulatory data-sharing and cross-sell into insurance.

- Golden Matrix Group (GMGI)

No earnings released on 19-Sep. The most recent quarterly print was 6-Aug-2025; next company-guided event is in November, per investor materials. Treat any 19-Sep stock moves as positioning/newsflow-driven rather than results-driven.

- Anebulo Pharmaceuticals (ANEB)

No earnings on 19-Sep. Company communications point to a late-September results timing; monitor corporate channels for the official release and filing. Key factors when it reports: cash balance/quarterly burn, trial timelines, and partnering updates.

- Incannex Healthcare (IXHL)

No earnings on 19-Sep. Third-party calendars show an expected results date in the week of 29-Sep. For the coming print, focus on R&D cadence, financing plans, and milestone catalysts.

Earnings Preview — Today (22-Sep-2025)

- Firefly Aerospace (FLY)

Q2’25 results after the close with a conference call slated for 5:00 p.m. ET. What to watch: launch cadence vs. backlog conversion, gross margin trajectory by program (launch, lunar, space services), cash usage vs. pre-funded milestones, and any updates on FAA/mission timelines. Balance sheet/liquidity and FY backlog color will drive the stock’s after-hours skew.

- Marti Technologies (MRT)

H1’25 results at 8:30 a.m. ET. Focus on unit economics (rides, utilization, take rate), adjusted EBITDA path, liquidity runway, and commentary on regulatory/tariff impacts in core markets. Pay attention to guidance on ride-hailing vs. micromobility mix and capital needs into seasonally slower quarters.

Stock Market – Monday, September 22, 2025

U.S. equities began the week cautiously. We at Zaye Capital Markets continue to watch rate-path uncertainty, headline tariffs, and positioning in megacap tech to keep factor volatility tense. Thin leadership continues despite last week’s closes at records, and any inflation-adjacent upside surprise in data or hawkish-biased commentary can strain long-duration equities; and softer impulse in data would otherwise lift rate-sensitivities and ease the dollar.

Stock Prices

Geopolitical Motion and Economic Indicators

Today’s sentiment incorporates three near-term swing factors: (1) how soon another batch of rate cuts come following last quarter’s quarter-point move; (2) overhanging tariffs and export control impacting supply chains and prices; and (3) new inflation data later this week providing stress to the “sticky services” narrative. We also have budget dynamics in D.C., whereby any budget frictions can create headline sensitivities.

Top Stock Headlines

We’re leaning into PEG ratio (price/earnings-to-growth) dispersion as a tell for where leadership could rotate next. Quick lens:

PEG < 1 = potential mispriced growth;

PEG > 2 = danger zone if rates back up or estimates cool. ORCL — ~3.4x

- NOW — ~2.5x

- MSFT — ~2.4x

- PLTR — ~1.9x

- CRM — ~1.8x

- AMD — ~1.7x

- AMZN — ~1.7x

- AAPL — ~1.5x

- META — ~1.5x

- ASML — ~1.4x

- NFLX — ~1.3x

- GOOGL — ~1.1x

- AVGO — ~1.1x

- TSM — ~0.7x

- NVDA — ~0.6x

Our take: cut exposure where PEGs congregate above ~2x into rate/backdrop risk; add selectively where expansion is valued more cautiously and cash-flow strength is strong.

The Magnificent Seven and the S&P 500

We’re witnessing increased attention on the mega-cap group driving the index. Many members are navigating double-digit down swaths from recent highs as (i) elevated real yields test long-duration cash flows, (ii) tariff/export restrictions muddy demand and supply chains, (iii) AI capex comes to earth vs. steeper comps, and (iv) regulatory chatter diminishes optionality in advertising, app stores, and data platforms. Until breadth recovers, the S&P 500 is vulnerable to multi-compression on macro surprises.

Major Index Performance — Today (Mon, Sept 22, 2025)

- Nasdaq Composite: previous close 22,631.48; initial response relatively softer.

- S&P 500: previous day’s closing 6,664.36; preliminary indications near unchanged to slightly down.

- Russell 2000: last close 2,471.96.

- Dow Jones Industrial Average: last close 46,315.27.

We’re still barbelled at Zaye Capital Markets: stable free-cash-flow compounders in pricing power and, on the flip side, selective cyclicals where operating leverage can come back into play on clearer order books. We’re monitoring earnings-revision breadth, front-end rate expectations, and participation breadth before jumping in and boosting risk.

Gold Price — Monday, September 22, 2025

We at Zaye Capital Markets note spot gold at $3,689/oz this morning and near U.S. futures at $3,724/oz both just below record territory following last week’s jump. The near-term catalyst mix is biased to risk-premium support: President Donald Trump’s series of security and legal-state communications (Bagram air base, maritime attacks, prosecutorial actions), and a high-profile diplomatic thread (calls with Chinese leadership and White House meeting with Turkish president), provides headline volatility that in most cases supports haven demand and volatility hedging sentiment. Into today’s podium risk, a hawkish FOMC Member Miran or BOE Governor Bailey would increase real-rate and dollar headwinds and could put bullion tactically to an end; a dovish tone—leaning to labor-market weakness or policy patience—would lower real yields, reduce dollar impulse, and keep gold anchored near highs.

Stepping back, yesterday’s data pulse and last quarter-point U.S. easing still support the easing narrative, which—alongside central-bank accumulation and ongoing supply-chain/energy doubt—lies at this rally’s structural foundation. Practically, this means the gold ecosystem (miners’ margins, ETF flows, and physical premiums) remains positive as long as real yields do not spike higher. Our near-term map: if speakers re-price direction more hawkish, expect a knee-jerk fade down to support areas as positioning diminishes; if guidance supports further easing and growth nerves remain, the market can re-challenge highs as hedging needs and reserve-diversification flows persist. Netting it out today: high geopolitical noise + easing bias > tactical blips in yields, maintaining our bias positive, tight risk management around the speaker headlines.

OIL PRICES — Monday, September 22, 2025

We at Zaye Capital Markets confirm crude is firmer but range-bound: Brent ~$66.9–67.1/bbl and WTI ~$62.7–63.0/bbl as of this session. The tape is being tugged higher by geopolitics—Russian military activity near NATO airspace and ongoing strikes on Russian energy assets, plus fresh Middle East frictions—while supply growth (Iraq lifting exports and OPEC+ set to add ~137 kb/d from October) and refinery-maintenance season lean the other way. Net effect: shallow rallies fade as the market fades risk spikes back into an oversupplied shoulder season. The IEA’s September OMR kept demand growth steady (~+700 kb/d for 2025/26) and flagged a typical ~1 mb/d demand step-down from summer peaks, consistent with flat-to-soft balances into Q4; OPEC’s own updates and Iraq’s SOMO guidance reinforce the supply-side looseness. Yesterday’s (Friday’s) data pulse—weekly declines despite the Fed’s quarter-point cut, distillate builds, and softer U.S. macro—kept a lid on crude by amplifying demand doubts even as a weaker dollar impulse didn’t deliver a bid. Today, the podium risk from FOMC’s Miran and BoE’s Bailey matters chiefly via USD/real-rate channels: a hawkish skew would pressure crude (stronger dollar, tighter financial conditions), while a dovish tilt would ease the dollar and help the bid—but likely within this capped range absent a larger supply disruption. On the political tape, the latest Washington rhetoric you flagged intersects directly with oil through Russia/Europe flows and tariffs. Statements pressuring Europe to curb Russian oil purchases elevate headline risk and, at the margin, support Brent via seaborne flow uncertainty; simultaneous talk of broader tariffs and tighter tech/export controls tempers the demand outlook for fuels and petchems, damping sustained upside. Market-moving snippets from real-time wires (e.g., Walter Bloomberg) stressing Europe’s reliance on Russian barrels underscore how quickly risk premium can rise on policy signal alone; similarly, weekend wires have the U.S. urging the EU to further curb Russian energy imports. Looking across ZeroHedge and other flow-watchers, the narrative is consistent: incremental OPEC+ supply restoration, scattered inventory builds, and Ukraine-Russia infrastructure risk keep volatility elevated but trend-capped into autumn. Bottom line for today: without a decisive supply shock or an outright dovish pivot from speakers, we expect crude to chop near $67 Brent / $63 WTI, with geopolitics providing intraday pops and the supply/macro stack selling those pops.

BITCOIN PRICE — Monday, September 22, 2025

We at Zaye Capital Markets verify Bitcoin trades at $114,475, following an intraday range of approximately $114,264–$115,861 thus far today. The policy and politics combination is carrying the heavy lift on tone. The combination set of comments you highlighted—from elevated security stance and legal brinksmanship to short-term diplomacy with key counterparts—injects headline and policy doubt, which tends to increase option value in liquid, internationally transferable assets such as BTC, but only if USD liquidity and real rates aren’t constricting in tandem. On the cryptocurrency-native side, constructive news persists: continuing institutional take-up, clearer rule-books, and post-cut strength keep dip-buyers interested, and talk of an imminent breakout still in circulation. Yesterday’s macro pulse—sluggish growth tell-tale indicators and recent policy reduction—anchored the easing narrative, absorbing risk appetite even while foci of classical risk sold down. Today’s podium risk matters for the next leg: FOMC Member Miran and BOE Governor Bailey can sway real-rate expectations and the dollar path in a way crypto is acutely sensitive to. A hawkish tilt (emphasis on sticky services inflation, restraint on additional easing) would typically pressure BTC via higher real yields and a firmer USD; a dovish lean (labor-risk emphasis, patience on inflation) would loosen financial conditions and support crypto beta. Meanwhile, the policy headlines around China engagement and tech platforms intersect with the “institutional rails” story: smoother cross-border flows and stable market structure tend to lower friction costs for large allocators—supportive for depth and liquidity—even as periodic Washington rhetoric can spark volatility. Netting it out: constructive adoption + easing bias keep the medium-term skew positive, but near-term tape direction hinges on today’s speakers and the dollar impulse.

ETH PRICES — Monday, September 22, 2025

We at Zaye Capital Markets verify ETH at ~$4,302, this day’s intraday range ~$4,288–$4,499 as liquidity focuses on round-number strikes. Recent flow developments remain bias positive: spot ETH ETFs have booked net inflows in recent weeks after an early-September stumble—CoinDesk counted ~$171.5M weekly inflows to ETH products as cryptocurrency ETFs generally recovered, and broader fund-flow trackers also highlighted new buying in crypto ETPs. Moreover, this September 18 SEC rule adjustment allowing core U.S. exchanges to utilize generic listing criteria for spot cryptocurrency ETFs reduces frictions to future products and thematic baskets in which ETH participates—an incremental support to structure-driven demand. Strategists remain divided on upside acceleration (e.g., Citi’s base case to year-end), but policy shift and improving fund flows continue to support downswings as long as real yields and the USD do not jump significantly higher.

On the whale tape, large holders offloaded ~90,000 ETH over 48 hours last week, creating short-term supply that coincided with a pullback from recent highs; such bloc sales tend to pressure price temporarily but can be absorbed when ETF and institutional demand are rising. Net effect for the near term: ETF inflow/outflow cadence and on-chain whale behavior will set the tone around $4.3–$4.5k; continued inflows and calmer macro would argue for re-tests higher, while renewed outflows or a hawkish rates impulse could extend consolidation. We’re watching (i) daily ETF creations/redemptions, (ii) exchange balances and large-transfer alerts, and (iii) real-rate/dollar moves for confirmation of the next leg.