Where Are Markets Today?

Up until Wednesday morning, US and European stock futures are projecting a flat/slightly bullish opening. Futures connected to the Dow Jones Industrial Average went up by 18 points or 0.04%, the S&P 500 futures rose 0.06%, while Nasdaq 100 futures appreciated 0.09%. This comes with a retreat of the S&P 500 from a record high, breaking a three-day rally. Despite the retreat, investors remain optimistic yet cautious, and the market has stayed fairly stable. The flat movement of the futures has mostly been due to the expected Federal Reserve Chair Jerome Powell speech, where investors are expecting clues as to the direction of the Fed regarding interest rates and the state of the economy. Markets are trying to get any indicators of future changes in policy and are making traders cautious and contributing to flat market sentiment during the morning.

The defensive mood in the futures market is also driven by profit-taking following the recent all-time highs in the S&P 500. Investors, after experiencing a good rally in stocks, are opting to book gains, leading to a minor pullback. It is a typical reaction following prolonged rallies, particularly when the stock market hits a new high. Also, recent economic indicators were mixed with some of them registering robust growth while others indicating possible slowdowns and leading to general indecision in the market. With the inflationary pressures, worries regarding the slowdown of the global economy and doubts regarding the profitability of the AI industry sectors, investors are unwilling to make major changes until more direction comes from Powell’s remarks. In European markets, stock futures are also showing a flat to mildly upbeat open. The Stoxx Europe 600 index of pan-European large and mid-cap companies was unchanged during morning trading as major national markets posted minor gains as well as declines. European investors are paying close attention to coming economic data releases and possible repercussions of central bank actions as the European Central Bank (ECB), still struggles with keeping inflation and growth under control. European futures’ cautious mood follows that of their US counterpart as both sides wait and see further indicators of policy directions as they could hugely shape the economic picture throughout the region. geopolitical events and fluctuations of energy markets also fuel the subdued market mood.

Overall, both US and European futures are pointing towards a flat opening as markets look to major economic indicators and central bank guidance. The mixed economic reports and promise of a speech from Powell has left investors optimistic yet cautious. Profit-taking off of the recent rally and skepticism of the trajectory of economic recovery has created a less optimistic tone towards trading for the day. Ongoing speculation of policy shifts from central banks both in the US and Europe will likely guide stock market direction as traders seek a lead from the recent high ground and global economic pressures.

Major Index Performance as of Wednesday, September 24, 2025

- S&P 500: Trading at 6,656.92, down 0.55% on the day.

- Nasdaq Composite: Down at 22,573.47 from a fall of 0.95%,.

- Dow Jones Industrial Average: Up 0.19% at 46,292.78 with advances from energy and financials.

- Russell 2000: Flat at 2,457.51, underperforming due to rate sensitivity in small caps.

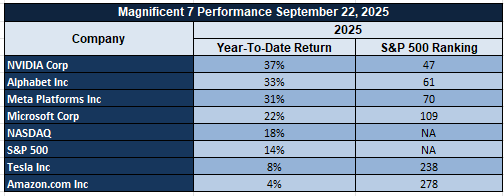

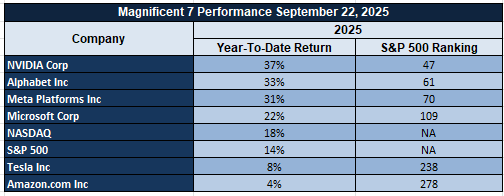

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are showing signs of fatigue. A recent sector breakdown shows the group averaging a drawdown of over 18% from their recent highs, with Tesla and Meta leading the decline. This signals a valuation recalibration, especially in AI-driven growth stories that have run ahead of fundamentals. The S&P 500 remains under pressure as tech leadership wavers. While energy and industrials are offering some support, the index is unlikely to rally sustainably without renewed participation from its core mega-cap drivers.

DRIVERS BEHIND THE MARKET MOVE

As markets arrive at their opens this morning, a volatile environment driven by recent economic indicators, geopolitical issues, and statements from policy makers greets investors. US and European futures are trading with a careful attitude and mirror the interplay of said influences.

1. Federal Reserve’s Cautious Policy towards Inflation and Employment

Federal Reserve Chairman Jerome Powell’s recent comments injected a degree of doubt into market optimism. He highlighted the problem of striking a balance between worries about inflation and a softening jobs market and implied that the central bank has a “no risk-free path” in making policy calls. His dovish commentary has precipitated a retreat of US stocks with the S&P 500 giving up record levels. Traders are watching closely leading indicators and Chairman Powell’s next speech next week as a further guide as to how the Federal Reserve will handle interest rates and economic stability.

2. President Trump’s Trade Policy and Its Impact Around the World

President Trump’s recent trade measures since coming into office, like setting tariffs, also raised concern about their impact on the world economy. Even the Organization for Economic Cooperation and Development (OECD) has warned that the measures may hurt global economic growth. Additionally, the Bank of Canada has also insinuated that the safe-haven status of the U.S. dollar could be threatened with such policies. These are all contributing to volatility in the markets as investors consider the impact of the trade stance of the U.S. on global relations and economic stability.

3. Economic Data and Market Sentiment

Recent economic indicators have shown a mixed picture, and investor sentiment has been influenced. In the United States, less-than-anticipated business activity data created fears of sluggish economic growth and prompted minimal gains in stock futures. European markets are still optimistic, with stocks closing mostly higher due to advances on Wall Street and European region activity indicators. However, geopolitical hotspots and fears of future economic policies are still inhibiting horizons.

Generally speaking, the day’s activity has been motivated partly through dovish central bank moves, shifting trade flows, and spotty economic indicators. Traders are countering those stimuli as they seek further action that may provide more direction for the markets.

Digesting Economic Data

The TRUMP Tweets and Its Implications

President Trump’s recent remarks created a major stir, particularly regarding his speech at the United Nations General Assembly. His major point of discussion was his stiff resistance to climate change policies, which he dubbed as a “green scam.” He threatened nations embracing aggressive climate action with severe economic repercussions. His rhetoric will likely create lasting effects on global energy markets, especially on fossil fuel sectors such as oil and natural gas. Trump’s stand may create more conducive regulatory settings for the sectors with traditional energy policies receiving an upsurge and the renewable energy segment likely encountering greater regulatory challenges. His statements also indicate that energy security and not only environmental interests will control future global energy debates with a possible creation of further investment in fossil fuels as opposed to renewable energy.

Alongside his remarks on energy, President Trump’s remarks about tariffs as a defense strategy and his encouragement of the United States to exert dominance of energy policy may provoke substantial shifts in the marketplace. Trump’s unwillingness to negotiate with Democratic leaders regarding the government shutdown also indicates his larger economic approach of giving priority to United States marketplace interests. His hardline approach regarding tariffs may bring further trade restrictions affecting energy imports and exports and may specifically impact the oil marketplace. Volatility may result from this and especially if sanctions are reimposed on major oil-exporting nations. Trump’s statements regarding continuing declines in the price of gasoline throughout the next year may also have an impact on energy trading and oil futures anticipation as traders adapt possible changes in the United States policy regarding energy production and usage.

Trump also referenced his global oil markets issue and strongly criticized China and India for continuing to purchase oil from Russia while there are ongoing sanctions. What this announcement does beyond raising geopolitical risk is call into question fragmentation of the global energy market. His remarks about energy independence are almost certain to put a bullish interpretation on US oil and natural gas production as they are positioned as less subject to global geopolitical risk. His repeated rhetoric of energy nationalism also suggests that any global disruptions of a nature such as military action or trade embargo may push oil markets’ price volatility further and subject them further to disruptions of the supply chain. His remarks about NATO and Russian airspace are also likely to further destabilize the geopolitical system and introduce an extra risk factor into global energy markets. President Trump’s recent statements indicate a continuing energy policy direction of nationalism and a greater geopolitical interest. These are likely drivers of price volatility in oil markets as trading patterns continue to remain driven by supply chain and geopolitical factors. With international energy prices continuing to remain volatile, President Trump’s influence in energy policy will continue to keep oil prices responsive both to international global events and domestic U.S. initiatives.

Labor and Manufacturing Developments

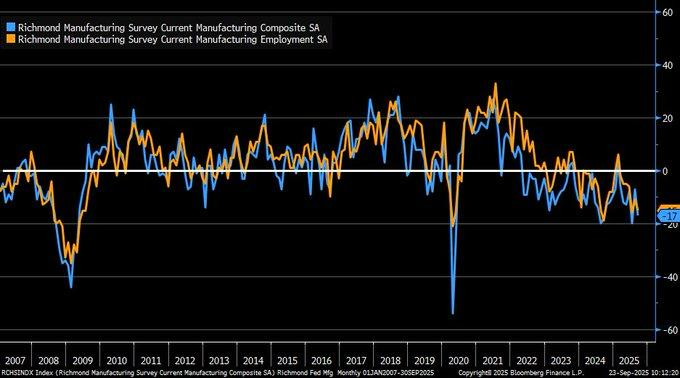

September 2025 Richmond Fed Manufacturing Index drop to -17 reflects a steeper contraction than expected, worsening from setbacks in shipments, new orders, and employment. Yet a significant footnote exists for the continued durability of wage growth, rising by +13. This implies the industrial economy lags with soft output but labor market pressures continue driving wages upward. This contradiction points up the interplay between softening manufacturing growth and strong labor market forces and one which analysts need to treat with caution for the time ahead, as such wage growth may continue supporting inflationary pressures.

When this is put side by side against the broader US manufacturing health as indicated by the ISM Manufacturing Index, a corresponding contraction pattern becomes evident as the ISM index falls below the critical level of 50 indicating a contractionary situation. While the two indices report spot vulnerabilities within the sector, the fall of the Richmond Fed by -17 and simultaneous declining rates of employment indicate deeper local trouble spots which are not reflected in the national data from the ISM. This divergence points out potential regional trends or structural issues with the US manufacturing base which analysts must take into account when making future economic predictions.

Notwithstanding the decline in manufacturing, the trend of wage growth came into the focus of intense analysis. Although indices of employment usually lag during industrial downturns, data from the past indicates robust wage growth cannot prove sustainable if manufacturing trouble persists. The increasing wages, particularly amid stagnant industrial output, provide an inflationary danger posing difficulty for the decision-making process of the Fed, compelling analysts to remain attuned both to manufacturing indicators as well as the trend of wages. This may trigger the larger-market responses, particularly from the interest-rate sensitive sectors.

Service Sector Divergence

The recent rise in the September Philly Fed Services Index to -12.3 from -17.5 signals a slight improvement in regional business activity, though it remains firmly in contraction territory, reflecting a persistent weakness in the service sector. This index, which surveys firms in eastern Pennsylvania, southern New Jersey, and Delaware, provides a vital snapshot of regional economic trends. Despite the modest improvement, the index has been in negative territory for nearly a year, underscoring the ongoing challenges for service industries. Analysts should pay attention to how these figures evolve, especially as the service sector’s lagging recovery could pose risks to broader economic stability.

This uptick in the services index contrasts with the Philly Fed Manufacturing Index, which traditionally tracks factory activity and has been above zero when signaling growth. The divergence between services and manufacturing performance is notable, as it reflects a broader economic trend seen post-recession. According to a 2023 Federal Reserve study, service sector recovery typically lags behind industrial rebounds, a pattern that is evident as manufacturing shows signs of stabilization while services continue to struggle. This shift highlights potential structural issues within the service economy, which analysts should monitor closely to assess any long-term risks.

The broader economic context, including global supply chain disruptions and inflationary pressures, has further complicated service sector recovery. The sharp decline in the index since 2022 aligns with these challenges, with a 2024 IMF report linking reduced consumer demand to continued struggles in service-related industries. Analysts should be particularly attentive to the pace of service sector improvement and the risk that delayed recovery may weigh on overall economic growth, especially as inflationary pressures persist. This suggests that the service sector may face further challenges, possibly weighing on investor sentiment if trends continue.

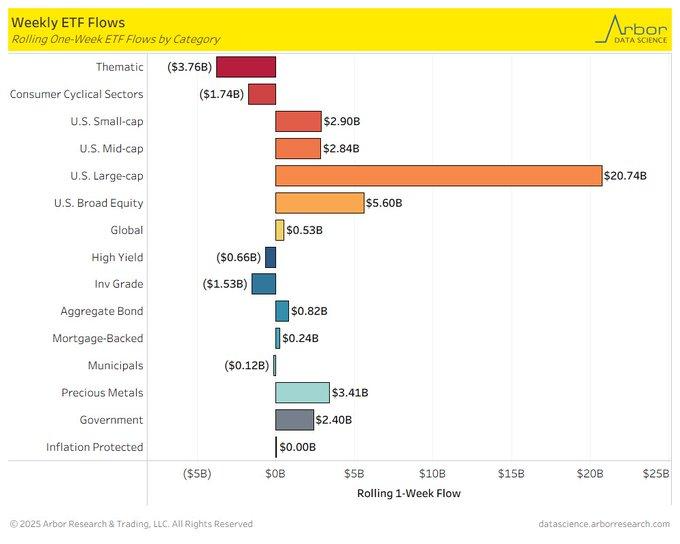

Investor Sentiments and ETF Flows

The recent inflows into U.S. large-cap ETFs, totaling $20.4 billion over the past week, indicate a shift towards stable, established companies, possibly driven by investor confidence amidst growing market uncertainty. This trend is notable in light of recent volatility tied to speculation surrounding Federal Reserve rate cuts in September 2025. The large-cap preference stands in stark contrast to historical market patterns, where small-cap and thematic funds typically dominated during recovery phases. This divergence suggests that investors are taking a more cautious approach, preferring lower-risk, large-cap stocks to navigate potential economic turbulence.

On the other hand, redemptions from consumer cyclical sectors ($3.7 billion) and theme funds ($6.3 billion) indicate a general movement away from trend-driven, high-growth investments. These sectors have struggled, especially as global interest rates rises since the beginning of 2022 for a negative impact on growth stocks. This aligns with Morningstar data, which noted the same trend during the prior-year period, and underscores the increased responsiveness of investors to interest rates. This trend could accelerate during 2025 as the market adapts further to a tightening of monetary policy, increasing the capital cost for high-growth sectors. This large-cap focus over thematic and cyclical funds supports the results of a study published in the Journal of Financial Economics in 2023, which associated macroeconomic uncertainty with increased demand for low vol. As analysts peer into the future, observing the large-cap ETF performance will be key, as further inflows suggest a more risk-averse market approach. Investors need to remain aware of the risk of further volatility, not least as the Federal Reserve proceeds with a strategy of reducing rates, which may continue to impact the behavior of investors as well as the structure of their asset allocation.

Indicators of Economic Growth and External Forces

The current fall of the Chicago Fed National Activity Index (CFNAI) three-month moving average below zero implies below-average economic growth, which bears close attention from analysts. As recent data from the Federal Reserve Bank of Chicago (September 21, 2025) suggest, a value for the CFNAI below -0.70 used to commonly prelude recessions. Even though this negative movement implies economic decline, it offers little assurances for a rapid recession. This trend follows historical practice whereby a continued negative drift precedes recessions becoming a reality as shown by proven indicators of recession.

Despite this, international trade tensions, including persistent US-China negotiations over issues like the sale of semiconductors and the ban (as of the date of this writing, September 23, 2025) of the TikTok app, could further impact US economic cooling. These external factors could compound the slowdowns forecast by the CFNAI, which would suggest the possibilities of domestic economic setbacks getting larger due to the international trade disagreements. This introduces another element of complexity into the broader recovery narrative, which had been predicted by many analysts as self-perpetuating post-pandemically.

The responsiveness of the CFNAI to external shocks like geopolitical tensions and trade tensions reveals U.S. growth vulnerability to external events. Against the current global backdrop, the current surge of interest rates and rising inflationary pressures makes the chances of another set of disruptions deepen the slowdown. Analysts need to pay close attention not only to the domestic economic indicators like the CFNAI but also international trade flows, as these would determine the trajectory for future U.S. economic performance.

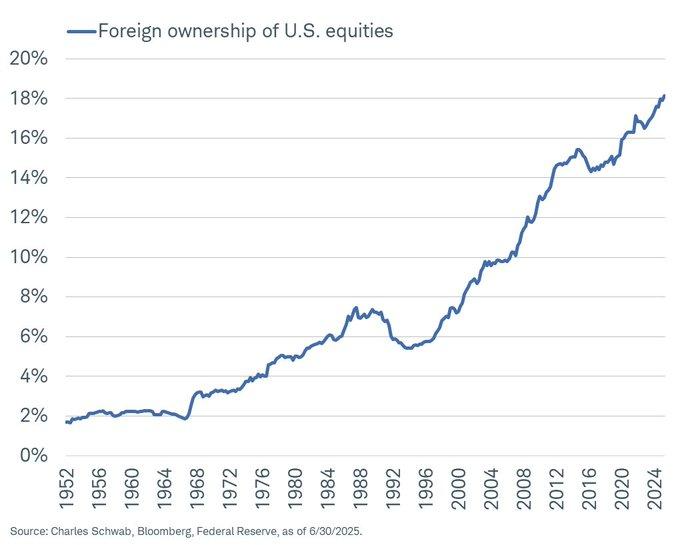

Foreign Owner Occupancy Trends and Security Risks

The consistent growth of foreign ownership of U.S. equities, from less than 5% during the 1950s to more than 18% up until mid-2025, demonstrates a notable change in global investment trends, mainly prompted by deficits in trade. Foreign investors continue to reinvest their dollars into the United States, as noted by a 2025 analysis from the Apollo Academy. This development contradicts the theory of foreign interest diminishing for the United States’ equities, especially during increased trade tensions. Worrying over tariffs, a report published by BlackRock in 2025 contends the United States equities continue to attract the international community due to their excellent 10-year yields when compared with the indices of other European markets, such as the FTSE, especially when the value of the dollar weakens further and makes them highly attractive internationally.

While this increasing foreign ownership comes as a contrast to the previously raised national security concerns, foreign investors now have greater access to highly classified U.S. information. The GAO produced a study in 2023 which sounded alarms regarding potential risk for foreign entities taking control of core industries, prompting CFIUS reviews for some foreign investments. The lack of peer-review research which conclusively measures these risks means a gap exists for empirical research, leaving policy-makers without the information necessary for them to appropriately balance economic gain against national security. For comparison, foreign ownership of European markets continues significantly lower, as economies such as Germany and the United Kingdom historically had less foreign investment into their equity markets compared with the United States. This may be a result of varying economic structures, regulatory climates, or less globalization of their equity markets. Analysts need to keep observing the long-run consequences of increased foreign investment into United States equities as the trend may accelerate amidst changing global market trends and economic policies.

Shifting the Focus from the Product Market

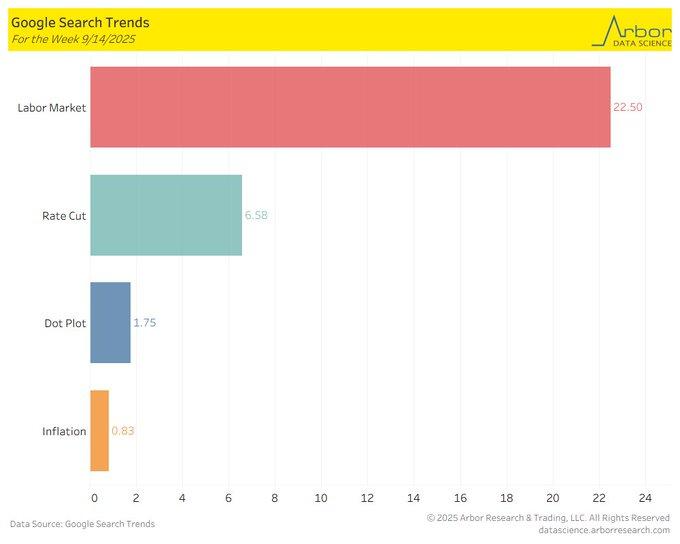

Recent Google Trends data illustrates a notable shift in public opinion, as searches for “Labor Market” have surpassed other topics concerned with the Fed, such as “Rate Cut” and “Dot Plot,” by a margin of 3-4 times. The spike in search interest, by a 22.50 compared to 6.58 and 1.75 interest index, indicates rising anxiety over job security. In line with the result of a study from the 2023 Federal Reserve study, which indicated a result wherein Americans preferred job security over concerns of inflation by a margin of 68%, this change illustrates the rising value of employment stability for the general public. Analysts need to pay close attention as this trend signifies future Fed policy choices as well as general economic sentiment.

This increased emphasis upon the labor market also comes at a time of turbulent U.S. labor markets, as a July 2025 UK Office for National Statistics report indicated a 5.0% pay growth, as concerns over AI-based job displacement continue to rise. A 2024 MIT study confirms this, as it suggests 20% of work would be automated by the year 2030, a potential further upset for job security for the majority of workers. The trends are also potentially affecting the actions of the public, as increasing numbers seek the help of search engines to learn more about the changing environment for work. Automation’s effects upon job displacement represent a key for analysts to consider when developing long-run labor market forecasts. The emphasis on the labor market goes against the current consensus that inflation continues as the central issue prompting Federal Reserve policy debates. The statistics indicate a change in public sentiment, as the need for reliable jobs and economic stability gains pace. The trend could further gain from global economic woes stemming from the 2024 United States general election, which affected trade policies and general market trends. The analysts need to keep a close eye on any policy change by the Fed, as the issue of employment stability may begin affecting future policies and change the course of the United States economic recovery.

Earnings Changes during Economic Recovery

The latest surge in the Citi U.S. Earnings Revision Index, which measures the optimism of analysts by the net share of upward vs. downward revisions of earnings-per-share, points towards a positive forecast for the S&P 500. The positive result reveals increasing optimism towards corporate earnings, which finds support from a 2018 research study by the Journal of Financial Economics, which associated positive revision indices of earnings with subsequent stock market advances. The development signals robust sentiment among investors, as analysts remain optimistic for continued profitability amid larger economic apprehensions. Investors would do well to monitor significant movement into this index, as this frequently corresponds with upward movement for the equity markets.

This positive earnings revision trend contrasts with historical volatility since 2006, but it aligns with a resilient U.S. economy in 2025. Mid-year data from Charles Schwab (6/6/2025) shows steady capital expenditures (capex) growth and a labor market with declining job openings but no significant layoffs, suggesting that the labor market remains relatively stable despite concerns of a recession. This trend challenges narratives of an impending economic downturn, as corporate investment and employment stability indicate a healthier economy than anticipated. Analysts should continue monitoring corporate earnings growth and labor market dynamics as signals of economic strength. September 23, 2025 release of the Citi U.S. Earnings Revision Index aligns with a hectic economic week, including the speech by Fed Chairman Powell and the release of the GDP. This may magnify market responses since investors readjust growth projections against the backdrop of the unexpectedly robust revisions of the earnings. Since economic data may alter the expectations of investors, it is imperative for analysts to consider how this robustness of earnings and economic data may shape subsequent trends of the market especially for those sectors highly correlated with economic growth.

Housing Market Dynamics and Additional Implications

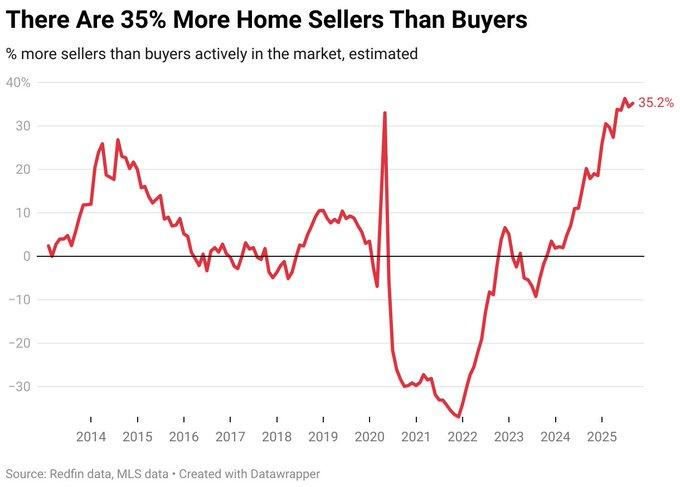

The August 2025 real estate market statistics, according to Redfin reports, shows a huge 35.2% gap between home sellers and buyers, the strongest buyer’s market on record. This gap, caused by elevated interest rates (6.6% average for a 30-year fixed mortgage), signals a tough environment for potential buyers, lowering affordability and changing market sentiment since 2022. The ongoing trend of a gap between homes for sale implies many sellers refuse to drop their prices amid a market downturn, a sign of a larger supply-demand gap. As the market unfolds, the need for analysts to identify how long this gap may continue and what it may indicate for general housing market trends comes into focus.

Some of this imbalance comes from the growth of short-term rental platforms such as Airbnb, which have driven a 10-15% decline in long-term housing stock for the key cities of the US, as one study from Forbes published in 2024 revealed. This decline in stock of property for long-term rent calls into question the current theme of a shortage of housing, which implies the market may instead suffer a dynamic shift in supply. Furthermore, these trends for short-term renting may also impact the home prices and supply of popular cities, as owners decide instead of selling or renting long-term to take the higher yields for renting shorter term. The wider economic spillover from this movement of the housing market could involve falling house prices in some hot markets and a possible diversion of capital into other liquid investments such as bonds or equities. High interest rates were associated with a 5-7% decline in real estate liquidity, the study by the 2023 Federal Reserve indicated, a sign of wider macroeconomic repricing. As housing markets decline, this may prompt investors to diversify into other classes of assets, redrafting investment strategy as well as the general movement of capital within the economy. Analysts need to monitor further movement in house prices, which may prove profound for spending by consumers and investment behaviour.

Upcoming Economic Events

With a key week for economic indicators, the markets will respond to big events this week which could clarify more on the condition of the world economy. Since the docket consists of speeches, sentiment reports from the business community, as well as housing figures, the moods of investors may significantly alter depending on those announcements. The following is a recap of what could happen and how each could impact the markets:

President Trump Speech.

President Trump’s speech is always a market focal point, and this time won’t be an exception. Investors would be searching for any clues on trade policy, especially regarding tariffs for critical economies such as China and Europe, as well as any hints on fiscal policy or the stance of the Federal Reserve.

- Any hint from his speech towards more robust tariffs or stricter economic policies may trigger a risk-off mood for the market, with equities falling and the dollar rallying as investors reach for safe havens.

- Conversely, any cues of looser trade policies or a dovish tilt towards interest rates may trigger a risk relief rally into risk assets, driving equities up and taking bond yields down as economic strains concerns unwind.

German Ifo Business Climate

German Ifo Business Climate is one of the key sentiment indicators for companies operating from the region’s biggest economy.

- A better-than-expected read would indicate rising German business confidence and potentially robust economic times ahead for the Eurozone. This would ensue with a positive market response, as Eurozone equities advance and the euro rises relative to other currencies.

- Conversely, if the actual print comes in less than expected, it would indicate a possible softening for Germany’s economy, which would serve as a damper for regional broader growth. Markets would respond with risk-off posture, taking European equities down and the euro lower as sentiment deteriorates.

New House Sales

The New Home Sales figures will give a snapshot of the health of the US housing market, a main stimulant for economic growth.

- If the figures come out higher than predicted, this would suggest robustness in the housing market, with increasing demand for new property as a sign of an economic pickup. This may cause stock market bullishness, especially for the real estate and construction sectors, as well as potentially boost bond yields as investors see reduced economic risk.

- A lower-than-expected reading would suggest potential softness in the housing market, potentially due to elevated interest rates or concerns over affordability. This may cause a risk-off move for equities, especially the cyclical ones, as investors seek safe havens such as bonds and gold.

Stock Market Performance

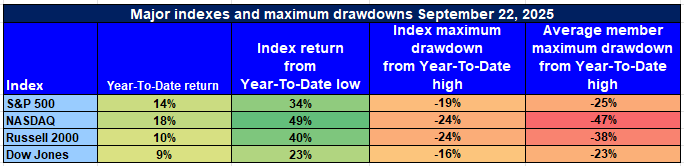

Indexes Keep Climbing from April Lows, Inner Weakness Endures

U.S. stock indices has continued the upward push since the lows of April 8th, yet a closer examination of index-level declines and component action finds continuing sensitivity beneath the surface. Even with positive returns through major indexes, the gap between index advances and individual stock action betrays slender leadership as well as ongoing volatility.

Below is the current week’s snapshot of Zaye Capital Markets’ analysis:

S&P 500 Records Robust Recovery Despite Light Volume

YTD: +14% | +34% lower from April low | -19% from YTD high | Avg. member: -25%

The S&P 500 still registers healthy gains, advancing 14% year-to-date and rebounding from the April low by 34%. Yet a 19% correction off of recent highs and an average member decline of 25% indicates much of the advance still rests with a few of the largest-cap leaders.

NASDAQ: Tech-Led Surge Masks Broader Weakness

YTD: +18% | off April low +49% | off YTD high -24% | Ave. member: -47%

NASDAQ’s 18% YTD gain and 49% April breakout are healthy headline action, but the 24% index sell off and dramatic -47% average member declines are a clear indication of grave underlying distress for a disproportionate number of its members—beyond mega-cap tech.

Russell 2000: Small-Cap Recovery Still Under Pressure

YTD: +10% | +40% from April low | -24% from YTD high | Ave. member: -38% Although the Russell 2000 has risen 40% from the low of April, the 10% YTD gain reflects investor reluctance towards the small economically sensitive names. Average member drops of 38% indicate that the majority of the names remaining in the index are still considerably off their peaks.

Dow Jones: Defensive Orientation Minimizes Drawdowns

YTD: +9% | +23% less than April low | -16% from YTD high | Average member: -23% The Dow’s mild 9% rally this year and 23% rebound off the lows suggest resilience from the defensive direction tilt. A relatively lower 16% drawdown and 23% average member decline suggest it’s withstanding volatility less than others and still susceptible to general market currents.

At Zaye Capital Markets, we continue to favor quality at the expense of momentum and favor fundamental-driven names and stable streams of income. While index gains are optimistic, continued breadth and improved participation are needed to confirm a solid bull market.

The Strongest Sector in All These Indices

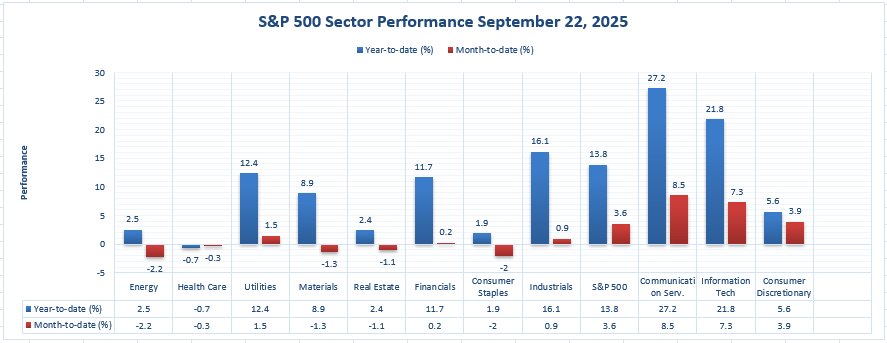

Communication Services Leads as Sector Momentum Highlights Areas of Growth

At Zaye Capital Markets, we are always keen on sector leadership as a measure of underlying health of the marketplace and patterns of rotation. Communication Services has been the clear leader of S&P 500 sectors both month-to-date and year-to-date during the period of 2025 to date.

Communication Services: The Clear Winner

YTD Performance: 27.2% | MTD Performance: 8.5% Driven by strong demand for mega-cap tech and media platforms, Communication Services has surged 27.2% year-to-date, the highest among all sectors in the S&P 500. Even in the short term, the sector continues to lead with an impressive 8.5% month-to-date performance. This dual strength underscores the ongoing investor appetite for growth in digital advertising, content streaming, and platform dominance, making it a focal point for growth strategies.

Other good YTD performers are:

- Information Technology: 21.8%

- Industrials: 16.1%

- Utilities: 11.0%

None of them are near rivaling the consistent performance of Communication Services both in near- and long-term frames.

As sector leadership often drives index-level success, we also see a possible Communication Services gain offering vital assistance at a broader marketplace level—perhaps particularly if breadth gains traction beyond a handful of mega-cap names.

Zaye Capital Markets has an overweight exposure to this segment and closely tracks valuation and earnings sustainability as the macros are evolving.

Earnings

Earnings Recap: September 23, 2025

- Micron Technology, Inc. (MU)

Micron Technology reported a record fiscal Q4, with revenue reaching $11.3 billion, a 46% year-over-year increase. Adjusted EPS of $3.03 surpassed estimates of $2.86. The company highlighted that AI-driven data center demand now accounts for 40% of sales, up from 19% last year. Looking ahead, Micron forecasts $1.2 billion in sequential revenue growth, with gross margins exceeding 50%, indicating strong growth momentum driven by the expanding AI market.

- AutoZone, Inc. (AZO)

AutoZone’s Q4 adjusted EPS of $48.71 fell short of the $50.57 consensus. Revenue came in at $6.24 billion, slightly below expectations. However, same-store sales increased by 5.1%, reflecting ongoing consumer demand for auto parts. Despite the earnings miss, AutoZone announced a $1.5 billion share buyback program, which could provide support for the stock in the near term, signaling management’s confidence in its future prospects.

- Worthington Enterprises, Inc. (WOR)

Worthington Enterprises reported Q1 FY2026 net sales of $303.7 million, an 18% increase. Net earnings rose 45% to $34.8 million, with adjusted EPS improving from $0.50 to $0.74. The company also declared a quarterly dividend of $0.19 per share, payable on December 29, 2025, reinforcing its strong financial position. These results suggest solid performance and an optimistic outlook for the company’s future earnings.

- AAR Corp. (AIR)

AAR Corp. delivered strong Q1 FY2026 results, with adjusted EPS of $1.08, exceeding the $0.98 estimate. Revenue reached $739.6 million, surpassing expectations. The company reported strong growth in new parts distribution and secured new business wins with partners like Trax. This solid performance signals a positive outlook for AAR’s future growth, especially in the aerospace and defense sectors.

Upcoming Earnings: September 24, 2025

- Cintas Corporation (CTAS)

Cintas is set to report Q1 FY2026 earnings before market open. Analysts expect EPS of $1.20 and revenue of $2.7 billion. Investors should focus on the company’s performance in its uniform rental and facility services segments, along with any updates on pricing strategies and customer retention. Cintas’ ability to navigate challenges in labor markets and inflation will likely be a key theme in its earnings call.

- Uranium Energy Corp. (UEC)

Uranium Energy is scheduled to release Q4 FY2025 earnings before market open. Analysts project an EPS loss of $0.04 and revenues of $17 million. Investors should keep an eye on updates regarding uranium production levels, pricing trends, and any strategic initiatives related to resource expansion. The company’s ability to capitalize on rising uranium demand could be a focal point for investors looking to assess future growth prospects.

- Thor Industries, Inc. (THO)

Thor Industries will announce Q4 FY2025 earnings before market open. The consensus estimate is an EPS of $1.20 on revenue of $2.33 billion. Key factors to watch include RV demand trends, margin resilience amid macroeconomic headwinds, and any commentary on inventory levels and dealer orders. Thor’s ability to manage supply chain pressures while maintaining strong demand for RVs will be crucial for sustaining its growth trajectory.

- KB Home (KBH)

KB Home is set to report Q3 FY2025 earnings after market close. Analysts expect EPS of $1.50. Investors should focus on the company’s new home deliveries, average selling prices, and any guidance on future orders. With the housing market facing challenges from higher interest rates, any insight into KB Home’s ability to navigate these conditions will be important for assessing the future outlook for the company.

Stock Market Outlook – Wednesday, September 24th, 2025

U.S. stock exchanges opened trading today under selling pressure due to investor fears of recent economic indicators and geopolitical pressures. Both Nasdaq Composite and S&P 500 slid while Dow Jones Industrial Average held steady. Russell 2000 continued struggling due to doubts of the economy.

Stock Prices

Economic Indices and Geopolitical Evolution

Cautionary tone of the markets can be attributed to a mix of factors. Current economic indicators have reflected sluggish growth as a cause of worry regarding the vigor of the recovery. Moreover, geopolitical tensions have mounted and are adding volatility to the markets. These are resulting in a higher risk aversion among investors and affecting market behavior.

Newest Stock Updates

- $ORCL and OpenAI to Make Datacenter Expansion Announcement in Texas

Oracle and OpenAI, funded by SoftBank, are increasing US datacenter capacity with Project Stargate. During the $400 billion build-out of this initiative, five US cities are coming online and planned capacity reached ~7GW, one of the biggest utility buildouts of all time, while AI demand continues to grow.

- Micron (MU) Receives Robust Data Center Growth

Micron generated $2 billion of HBM revenue last quarter as AI demand continued. With a 56% revenue share of the segment and a 52% gross revenue from data centers, it solidifies a leadership position in the AI ecosystem.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are showing signs of fatigue. A recent sector breakdown shows the group averaging a drawdown of over 18% from their recent highs, with Tesla and Meta leading the decline. This signals a valuation recalibration, especially in AI-driven growth stories that have run ahead of fundamentals. The S&P 500 remains under pressure as tech leadership wavers. While energy and industrials are offering some support, the index is unlikely to rally sustainably without renewed participation from its core mega-cap drivers.

Major Index Performance as of Wednesday, September 24, 2025

- S&P 500: Trading at 6,656.92, down 0.55% on the day.

- Nasdaq Composite: Down at 22,573.47 from a fall of 0.95%,.

- Dow Jones Industrial Average: Up 0.19% at 46,292.78 with advances from energy and financials.

- Russell 2000: Flat at 2,457.51, underperforming due to rate sensitivity in small caps.

We are closely watching active sector positioning and sector rotation at Zaye Capital Markets as the earnings season progresses. Success of leading business houses in maintaining earnings growth during accelerating policy will determine the trajectory of broader equity markets during Q3.

Gold Price – Wednesday, September 24, 2025

As of today gold is trading at $3,746 per ounce after a slight retreat from the all-time high of $3,790.82 reached during the week. The retreat has mainly been due to profit-taking after gold’s spectacular rally as geopolitical fears escalated and Federal Reserve interest rate reductions became more expected. Nevertheless, the medium-term prospects of gold remain upbeat with the aid of a plethora of fundamental drivers such as a weakening of the U.S. dollar, dropping Treasury yields, and ongoing inflation fears. Ongoing market nervousness and risk appetite continue to push investors towards safe havens such as gold that traditionally shines during economic uncertain times. Apart from the fact that gold becomes a more attractive proposition with the possibility of rate reductions since low interest rates further reduce the opportunity cost of possessing non-yielding assets such as gold coins or gold bars or gold exchange-traded funds, doubt regarding U.S. fiscal policy and ongoing geopolitical instability and fears of conflict areas such as Eastern Europe and the Middle East continue to push gold further into favour with risk-averse investors. Latest economic news, such as the Federal Reserve’s dovish commentary on the economy, has further strengthened gold’s appeal. Chair Jerome Powell’s comments highlighted balancing sticky inflation with evidence of a weakening jobs marketplace, and this has prompted investors to anticipate possible rate reductions in the coming months. Traditionally, as interest rates are lowered, gold gains as the payoff of carrying gold becomes less. What has further supported this mood has been global economic uncertainties—both economic and political—that continue to push investors towards safe-haven assets such as gold. Moreover, yesterday’s economic figures of slower job growth and indicators of an economic slowdown only further buttress the argument for further rate reductions, sending gold higher. In a nutshell, although gold dipped a tad due to profit-taking, the broader economic and geopolitical situation still offers substantial support towards gold’s price direction. With central banks likely turning dovish and reducing policy as a response towards inflation and economic slowdowns, gold should remain an attractive investment prospect for the short and medium term.

Oil Prices – Wednesday, September 24, 2025

As of today, oil prices have been experiencing upward momentum, with Brent crude trading at $67.90 per barrel and West Texas Intermediate (WTI) at $63.69 per barrel. The price increase can be attributed to a combination of supply disruptions and inventory draws. A significant factor driving this upward movement is the supply uncertainty surrounding Iraq’s Kurdistan region, where a deal to restart oil exports has stalled. This disruption continues to contribute to a tighter global oil supply, supporting higher prices. Additionally, the American Petroleum Institute’s report, which showed a 3.82 million barrel drop in U.S. crude inventories, signals a tightening of supply and suggests that demand may still be outpacing production, further pushing prices higher. Despite concerns about potential economic slowdowns, this tight supply backdrop is keeping upward pressure on oil prices, which is reflected in the current trading prices. On the flip side, global demand for oil remains uncertain as geopolitical factors and slowing growth concerns continue to cloud the broader outlook for the commodity. With continued tensions in Eastern Europe and the Middle East, particularly around Russian oil purchases, traders are closely monitoring how geopolitical developments could impact supply chains. President Trump’s statements at the United Nations General Assembly criticizing European countries for buying Russian energy have infused a degree of geopolitical unpredictability into the oil marketplace. These statements and the already existent sanctions and possible trade restrictions intensify the risks of an extension of disruptions with oil supply. Such rhetoric amplifies fears of a deterioration of the supply situation and especially if further steps are undertaken to halt Russia’s oil exportations and further tighten global markets. From an economic perspective, the Federal Reserve’s dovish approach towards interest rates—coupled with indicators of a weakening jobs market—indicates a possible cooldown of the economy of the United States and may temper oil demand prospects. Nevertheless, the decline of U.S. crude stock and bottlenecks in major oil-producing areas are likely to negate a number of those demand fears and preserve bullish attitudes and sentiment in the near term. Today’s economic indicators continue to reflect tight oil supplies with stock reports and supplier disruptions enforcing a bullish price direction of oil. Despite possible demand erosion from a less robust economy, the current issues with oil stock and supplies from a state of geopolitical tensions and stock reductions favor higher oil prices at least in the near term. How these influences pan out during the coming weeks and beyond will ultimately determine oil price direction with ongoing doubts regarding OPEC & IEA action likely exerting much of an influence upon marketplace action.

Bitcoin Prices – Wednesday, September 24th, 2025

Trading at $111,564 and experiencing a slight decline of 0.6%, Bitcoin has mostly withstood a sell off of the entire cryptocurrency space that wiped out a total of a record $162 billion. Bitcoin has held steady with support at $112,000 and $113,000 and has continued dominance of the space with a 57.7% dominance. Its solid performance has been a result of continued institutional inflows that indicate persistent optimism about Bitcoin’s long-term future irrespective of short-term price movement. Movements throughout the space also reflected some of the overarching influences such as Federal Reserve interest rate cuts and institutional flows shifts. Bitcoin has remained one of the foundational assets of the cryptocurrency space, although yesterday’s sell off reflects marketplace sentiment with regard to persistent economic and regulatory challenges. President Trump’s recent remarks about crypto regulations, especially the US-UK cooperation regarding crypto regulations, complicated Bitcoin’s outlook. While on one side clearer regulations and greater access to capital markets may encourage further institutional investment and push Bitcoin’s price higher, Trump’s general economic policies like his statements regarding tariffs, foreign trade, and global regulations may bring out the uncertainty factor and cause investors to become defensive. Though it may cause some near-term pullbacks of Bitcoin’s price, its decentralized nature helps it stay less vulnerable to geopolitical risks vis-a-vis traditional assets. Moreover, yesterday’s economic indicators like the cooling of job growth as well as the Federal Reserve’s dovish approach towards interest rate hikes further strengthen Bitcoin’s safe-haven appeal during economic uncertain times. With the US economy cooling off further investors may become bullish and flock to Bitcoin as a store of value like gold during inflationary times, yet constant regulatory changes may continue and remain at the forefront of determining its price direction.

ETH Prices – Wednesday, September 24, 2025

As of today, Ethereum (ETH) is trading at $4,137.33, marking a slight decline of 0.67% from the previous day’s close. Over the past 24 hours, ETH has seen fluctuations between a low of $4,100.16 and a high of $4,224.33, showing its usual volatility in the current market environment. The price drop follows a broader market sell-off, with ETH experiencing a 7% decline over the past week, a result of profit-taking activities and some caution ahead of upcoming economic data. Despite these pullbacks, Ethereum has demonstrated a strong level of support between $4,100 and $4,200, indicating that investors are still holding onto their positions. Ethereum’s resistance levels are currently pegged at $4,360 and $4,550, and should the market show bullish signs in the coming days, we may see ETH testing those boundaries. As the overall market sentiment fluctuates, Ethereum’s performance continues to reflect its strong position as the second-largest cryptocurrency by market capitalization, though it remains highly sensitive to both institutional actions and broader market trends.

Ethereum’s market movements are significantly influenced by both institutional investments and whale activities, which have created a dynamic market environment. One of the key drivers of recent price stability has been substantial institutional inflows. For example, BitMine Immersion, a firm led by Tom Lee, recently purchased over $1.1 billion worth of ETH, increasing its holdings to more than $10 billion. This reflects a growing institutional interest in Ethereum, especially amid regulatory shifts in the crypto space. Alongside institutional interest, Grayscale’s approval of the Digital Large Cap Fund (GLDC), which includes Ethereum, has further legitimized the asset and provided a regulated platform for exposure to ETH. However, whale activity is showing signs of fluctuation, with large Ethereum holders—those holding between 1,000 and 10,000 ETH—reducing their holdings by over 200% in the past week. This indicates a more cautious sentiment among some of the larger players in the market, which may create downward pressure on the price in the short term. The interplay between institutional support and whale movements remains critical in shaping Ethereum’s price trajectory, with institutional purchases potentially absorbing the selling pressure from whale movements, allowing ETH to maintain a relatively strong position despite the volatility in the broader cryptocurrency market.