Where Are Markets Today?

Indices are headed for a subdued open as U.S. and European stock futures trade close to the flat line, reflecting the nervous sentiment going into the release of the Core PCE Price Index—the Federal Reserve’s favorite inflation measure. In U.S. pre-market action, Dow futures rose by 0.04%, S&P futures increased by 0.06%, and Nasdaq 100 futures increased by 0.05%. On the other side of the Atlantic, the outlook was also for a subdued open across major European markets as investors await inflation surprises and central bank cues for a clearer directional impetus. This flat character follows a spotty week of price action with the S&P 500 lower by close to 0.9%, the Nasdaq off by 1.1%, and the Dow lower by 0.8%, a reflection of investors’ discomfort with stretched valuation multiples as Treasury yields continue to creep higher.

The cautious positioning reflects the market’s delicate balance between optimism for easing and concerns about economic resilience. Yesterday’s stronger-than-expected labor data and the sharp upward revision of U.S. Q2 GDP to 3.8% reinforced the narrative that the economy is on firmer footing than previously thought. While positive from a growth standpoint, these signals reduce the urgency for the Fed to deliver aggressive rate cuts, tempering bullish sentiment. In Europe, worries about fiscal strain in key economies, alongside weaker business activity data, are keeping investors on edge. Together, these factors explain why futures are not signaling a decisive move—market participants are unwilling to commit until inflation data and subsequent central bank responses set the tone. Two factors outstand in the development of this flat futures landscape. First, the market remains ultra-sensitive to the signals of central banks, and the Core PCE report could revise outlooks. Futures continue to price two quarter-point cuts across coming Fed meetings, with a 92% probability of a move in October. However, if inflation is stickier than expected, yields could continue higher, prompting traders to revisit the rate path and invoking risk-off flows. Second, political and geopolitical news of the past week adds another element of uncertainty. Trump’s comments regarding tariffs, national security enforcement, and possible government shutdown scenarios injected volatility into the macro environment. Trade risks and worldwide political instability continue to press export-sensitive areas of Europe, which cements the caution against aggressively committing to either side prior to new data.

At Zaye Capital Markets, we consider today’s flat futures a sign of market balance under tension, with bulls and bears refusing to take charge until the inflation release sheds light. Bulls await assurance of easing inflation pressures by a magnitude that will create room for easing by the Fed, while bears await any indication that sticky price growth may freeze the easing cycle. With already-stretching valuation levels coupled with ongoing global uncertainty, the Core PCE print—and the policy sentiment that results from it—will be crucial given that risk appetite will rise again or defensive strategies become more pronounced deeper into Q4.

Major Index Performance up to Friday, 26th of September, 2025

- S&P 500: Current price at 6,600.12. Down by 0.

- Nasdaq Composite: Currently at 22,300.44, down by 0.8%, with selling concentrated on.

- Dow Jones Industrial Average: Lower by 0.2% at 46,050.21, aided by selective strength across defense.

- Russell 2000: Flat at 2,420.18, responding mildly following small caps pullback.

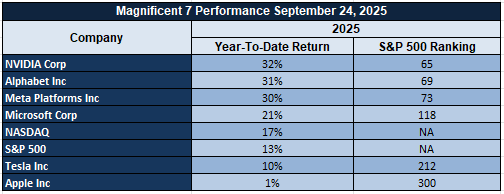

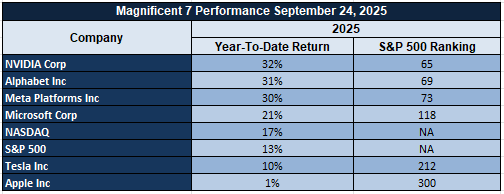

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—continue to feel the squeeze this week, with average pullbacks of over 18% from recent tops. Tesla and Meta are at the forefront of the losses, while Nvidia’s pullback has fanned worries about AI-fueled frenzy. The softness of those leaders is holding back the S&P 500, calling its sustained rally potential into question. Meanwhile, investors are shifting into energy and industrials, which have fared relatively well despite worries over tariffs and international uncertainty. Without renewed strength from its largest components, the broader index finds it hard to pick up speed.

Drivers of the Market Movement

The three biggest catalysts of today’s pre-market market actions out of the U.S. and Europe are the following — from the latest news, Trump’s remarks, and coming economic data:

1. Policy Uncertainty and Geopolitical Rhetoric.

Trump’s latest actions and comments are literally feeding market nervousness. His government’s announcement of sharp new tariffs—up to 100% on medicines and large percentages on trucks, furniture, and other imports from October 1—has increased fears of trade frictions and inflationary costs. Combined with forceful national security rhetoric, political violence of an organized kind, and threats of mass firings related to government shutdowns, investors are putting a new political risk premium on U.S. assets. This is spilling over too into Europe, where export-dependent and globally oriented companies are trading tentatively for fear of increased trade barriers and policy uncertainty.

2. Resilient Economic Data Dampening Rate-Cut Optimism.

Cyclical economic data out of the U.S. in recent days has featured a stronger economy than expected by markets. Jobless initial claims surprised on the downside and Q2 GDP was reassessed sharply higher at 3.8%, suggesting stronger labor and growth conditions. Though favorable for economic momentum, the pair diminishes the Federal Reserve’s need to provide short-term rate cuts. The takeaway is that tighter financial conditions could be sustained across the board, at least for rate-sensitive areas such as tech and real estate. Already struggling with weaker business sentiment and fiscal stress, European bourses are following suit with the cautious sentiment as investors scale back central bank elasticity outlook across the Atlantic.

3. Macro Overhang from Key Data Releases of the day.

All eyes are then on the U.S. Core PCE Price Index and the Adjusted University of Michigan Consumer Sentiment report today. PCE is the Federal Reserve’s preferred inflation measure, and a hotter-than-expected print will force markets to recast their easing sentiment, firming yields and the greenback while threatening equities. Otherwise, a softer reading with weaker sentiment will confirm rate-cutting prospects and may spark a risk asset recovery. Until those data are known, U.S. as well as European futures remain capped around the flatline as investors hold off on huge allocations.

It’s a collection of political shocks, resilient but complicating economic data, and the threat of tomorrow’s inflation data. Conviction remains shallow at the market level, and today’s clarity will be pivotal in helping decide if sentiment strengthens or falters as the week approaches its close.

Digesting Economic Data

The TRUMP Tweets and Their Implications

Trump’s latest series of pronouncements highlights the scope of political and economic turbulence that is informing investor sentiment. His assurance that the Justice Department will make any indictments of Comey, coupled with an expanded crackdown on political violence of an “organized” sort, betrays an increased focus on law-and-order issues that injects unpredictability into civil and institutional order. The White House directive that its agencies develop plans for widescale firings if there’s a shutdown of the government adds fiscal and labor market risk to the mix, threatening disruption of public services and consumer confidence. Investors’ attention is drawn by these events to an increasing thickness of political risk premium that could prop up safe-haven flows while putting increased strain on risk assets that are sensitive to policy shocks.

On the economic side, Trump cited Q2 GDP growth of 3.8% as evidence of a continuing boom, pitting the administration’s buoyancy against market doubts over sustainability. The political message is effective but market prudence prevails, recalling that headline strength in the GDP may obscure patchy sectoral performance. Orders affecting TikTok—ranging from pricing a forced sale at $14 billion while at the same time proclaiming it “saved” subject to national security terms—signal the willingness of an administration to aggressively intervene in private market transactions. These cast doubt over policy coherence, regulatory overreach, and potential countermeasures from international trade partners that impede technology valuation and wider equity market performance. Globally, Trump made commitments that Israel wouldn’t annex the West Bank while simultaneously inviting Turkey’s President Erdogan to the White House. While indicative of diplomatic outreach, such moves also demonstrate a fine balancing act that may redefine Middle Eastern alliances. In energy markets, Middle Eastern stability is of crucial importance, and any uncertainty over U.S. foreign policy spreads fast into oil pricing as well as investor sentiment across the commodity space. In addition to orders over implementing the death penalty within the District of Columbia, such steps reinforce a governing approach that combines hardline domestic policy with high-profile foreign interventions—both of which raise geopolitical uncertainty.

For financial markets, the aggregate impact of these announcements is evident: increased volatility and decreased clarity for investor and corporate planning. The potential of layoffs by a shutdown impasse, compounded by hints of regulatory scrutiny of layoff strategies, injects another dose of uncertainty into corporate strategy. Some of Trump’s announcements are symbolic while others have direct market effects—most notably those related to assertions of economic growth, interventions in the labor market, and foreign trade maneuvering. At Zaye Capital Markets, we believe that the combination of domestic and foreign actions serves as a reminder that political risk is a leading market sentiment driver that will shift capital flows rapidly from risk-off assets to risk-on assets.

Kansas City Fed Manufacturing Index Indicates Bumpy Recovery

The Kansas City Fed Manufacturing Index climbed to +4 in September 2025, providing a humble but welcome indication of strength in an industrial sector that has experienced chronic problems over the past two years. Gains across employment (+7) and shipments (+7) imply companies are tentatively building capacity, both a necessity for steady demand levels and continuing resolution of structural issues with automation technologies against chronic manpower gaps. Although an estimated 2.1 million industrial jobs continue to go unfilled, companies are spending aggressively on productivity upgrades, and that is coming to bring stability to select subsectors despite increased financing and energy expenses. The data thus indicates a balancing act: a sector getting its footing while still adjusting to structural issues.

However, the underlying image is anything but strong. New orders only registered a slim +2 advance while the workweek also remained steady at +3, fueling skepticism that the recovery will be sustained. This adds weight to worries expressed by earlier Federal Reserve studies that industrial comebacks threaten unevenness despite structural currents such as surging input prices as well as international supply chain reorganizations. Volatility of energy prices specifically remains hard on the margins of manufacturers while suppressing their capacity to convert incremental growth at the margin towards wider industry growth. The disconnect of headline gain against softer internals implies that the market could be overreading the vigor of the recovery while local weaknesses could pull down national momentum. For equity markets, this dynamic requires careful discrimination between sectors. Traditional industrials look increasingly stretched, as valuations already embed expectations of a more decisive rebound than current data supports. By contrast, undervalued opportunities are emerging in automation and advanced manufacturing stocks, where investments in technology directly address both labor shortages and efficiency pressures. Analysts should closely track the trajectory of new orders and monitor cost-push risks, particularly in energy-intensive segments. At Zaye Capital Markets, we believe positioning defensively within industrial equities, while tilting toward undervalued automation leaders, provides the most resilient exposure as the sector navigates a fragile and uneven path forward.

Housing Market Sends Mixed Signals Amid Changing Rate Dynamics

U.S. existing-home sales declined by just 0.2% in August 2025, significantly better than the forecast slid of 1.5%, reflecting the market’s strength despite continued affordability issues. Median prices rose by 2% year-over-year to $422,600, again reflecting persistent demand despite high borrowing costs. This resilience is a reflection of structural supply deficits continuing to support valuations despite consumers facing tighter purse strings. The data implies that the home market is stronger than expected rather than being extremely frail but its stability is spotty by regions as well as by income groups.

Meanwhile, leading indicators are providing brighter outlooks. Sales of new homes rose by over 20% in the latest report, helped by flattening mortgage rates, which have dropped to 6.26%. Federal Reserve cuts of rates later in the year forecast by economists provide another potential tailwind, providing relief for buyers who are pinned back by costs of borrowing. However, care is needed here: sale of existing homes usually falls behind agreement activity by one to two months, so the August report will probably reflect agreements contracted earlier in the summer, prior to the latest easing of financing terms. As such, although the new home data indicates building strength of momentum, there may be a while before such a shift translates fully into resale activity. For equity investors, this dual narrative presents both risk and opportunity. Traditional homebuilders appear fairly priced after the strong new home sales rebound, but undervaluation exists in real estate investment trusts tied to rental markets, which stand to benefit if affordability pressures push more households away from ownership. Analysts should also monitor mortgage lenders and housing-related consumer discretionary names, as their performance will serve as a barometer of whether lower rates are truly unlocking pent-up demand. At Zaye Capital Markets, we see this as a pivotal moment for housing equities, where selective positioning will determine whether investors capture the upside of a rate-driven rebound without overexposure to lingering affordability headwinds.

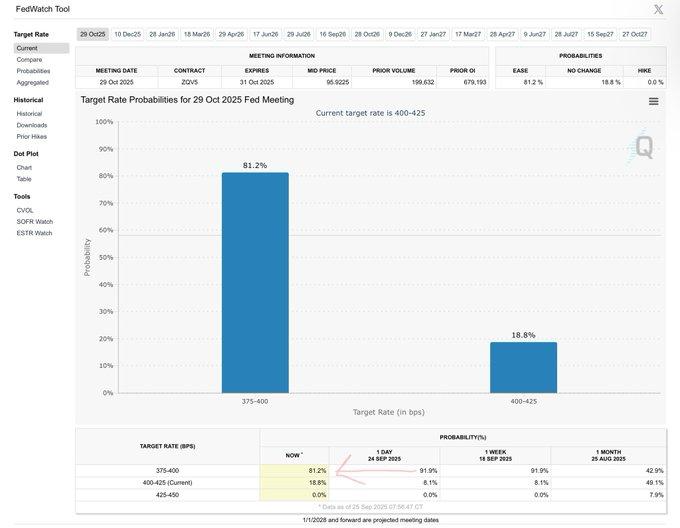

Labor Market Strength Reshapes Fed Rate Cut Expectations

Hope for a Federal Reserve rate reduction at the October 29, 2025, meeting dropped sharply, with CME FedWatch probabilities decreasing from 81.2% to only 18.5%. The catalyst was stronger-than-expected jobless claims data that indicated initial filings at 218,000 for the week ended September 20, from 232,000. The decline strengthens the persistence of the labor market such that conditions continue resilient enough to diminish the need for another near-term easing of monetary policy. The reversal highlights the sensitivity of market sentiment to incremental labor commentary, especially against an existing backdrop of an economy already responding to earlier rate steps.

This information puts at risk the prevailing market view of stimulus around the corner. While the Fed did mark an earlier 2025 reduction of 0.25%, lowering the benchmark rate to 4–4.25%, resilient employment coupled with higher GDP growth has reset the policy outlook. The central bank itself seems more willing to focus on inflation moderation consistent with its dual mandate of maximum employment and price stability. With inflation remaining above target and wages experiencing local pockets of rigidity, markets are being compelled to revise downward the probability of a swift easing cycle. For investors, the rate expectation pivot has definite sector implications. Rate-sensitive stocks like utilities and real estate could slow down in the short term given that the odds of lower borrowing costs fade. Undervaluation could be brewing in a few selected financial stocks, specifically banking stocks, given stable rates as well as a robust labor market favorable for profitability driven by net interest income. Analysts need to focus on labor indicators as well as inflation data as immediate catalysts of Fed repricing. At Zaye Capital Markets, we highlight vigilance: the seesaw of inflation control and growth support will continue to fuel rate expectation volatility with direct implications for the performance of equity sectors.

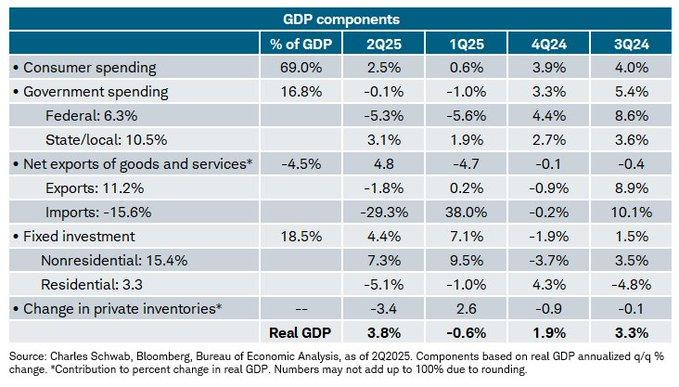

Upward GDP Revision Masks Uneven Recovery

U.S. real GDP growth for Q2 of 2025 was also upgraded from 3.3% to 3.8%, a firmer expansion than previously estimated. The upgrade was led by healthy consumer spending and lower imports that delivered a favorable contribution to net trade. Residential investment contracted by 5.1% over the same interval, highlighting the patchy character of the recovery. Although headline growth indicates strength at the broad economic level, imbalances at the sectoral horizon continue to persist, most notably in housing and other rate-sensitive areas.

The robust GDP reading has elicited skepticism, as analysts wonder if the surge indicates sustainable productivity gains or temporary distortions. Despite widespread spending on artificial intelligence, latest company disclosures show that companies are not yet churning such technologies into hard earnings growth. The disconnect provides food for thought that strength in the GDP could be exaggerated by speculative money flows instead of sustained gains in efficiency. Past analogies with the dot-com era, when GDP statistics overestimated underlying fundamentals by way of inventory accumulation and tech frenzy, offer a timely but cautionary example of headline growth obfuscating vulnerabilities.

For investors, the takeaway is clear: while consumer-driven growth offers a good backdrop, caution is warranted in areas that appear overvalued by sentiment over substance. Stocks linked with speculative rises in productivity appear overvalued while those which may be subject to inefficient valuation are defensive sectors like utilities and healthcare that continue to be supported by robust demand fundamentals. Our opinion at Zaye Capital Markets is that analysts need to observe corporate earnings quality and consumer spending sustainability while deciding whether the good GDP trajectory will be sustained or we will encounter another cycle of overblown optimism.

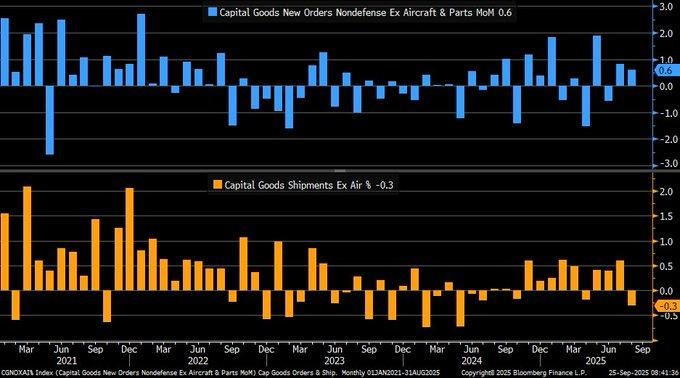

Capital Goods Orders Improve but Shipments Decrease

August data for 2025 recorded a rise of 0.6% of core capital goods orders (excluding aircraft and defense) that outstripped market predictions of stable growth and indicated continued demand for business equipment. Shipments fell by 0.3% versus predictions of a moderate pick-up, however, as an indication of delays towards ordering that is converted into realized investment. That gap indicates businesses are committing towards spending over the longer term but that its fulfillment is slow, perhaps an indication of logistical strains as well as financing limitations.

The wider picture was also muddled by a 2.9% surge in total durable goods orders, powered by a strong 7.9% gain by transport equipment. Although this seems heartening, underlying motivations are more ambiguous given that prices driven by tariffs could be pushing nominal order values upwards with no matching volume expansion. Inconsistencies between increasing orders and softer shipments consequently prompt queries as to whether demand is genuinely strengthening or if firms are front-running spending to offset price pressures. Such processes prompt attention towards probing deeper than order headline growth and examining sustainability of actual output.

For equity markets, this split dynamic has direct sector implications. Traditional industrials appear vulnerable if shipment delays persist, particularly for firms exposed to supply chain bottlenecks and higher input costs. Undervaluation may instead be found in logistics and supply chain management companies, where efficiencies could benefit from ongoing investment trends, and in technology-driven capital goods producers better positioned to navigate execution lags. At Zaye Capital Markets, we advise analysts to monitor shipment activity as the leading indicator of whether elevated orders will translate into real economic expansion or remain stuck in the pipeline.

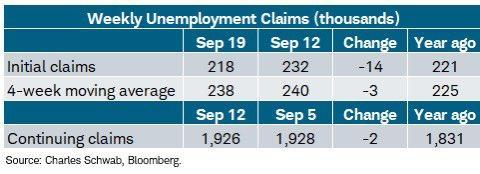

Jobless Claims Reiterate Labour Market Strength

U.S. initial jobless claims fell to 218,000 for the week of September 19, 2025, below the forecast of 233,000 and from the previous week’s 232,000, while the four-week moving average declined to 238,000 from 240,000. This consistent downtrend is evidence of a labor market that persists despite wider macroeconomic headwinds. Although growth has slowed in selected areas, companies continue not to reduce their manpower bases despite the challenge of rehiring when business picks up again plus recurring needs for manpower-intensive services. These factors confirm that the employment environment remains the largest stabilizer of the economy, absorbing the shock of household spending power despite continued high borrowing costs.

Continuing claims came in at 1.926 million, modestly below the 1.932 million forecast, but regional divergences reveal important undercurrents. California saw an uptick of 1,700 claims, pointing to stress in specific industries such as technology and entertainment, while Texas reported a sizable 6,900 decrease, supported by resilience in energy and construction. These regional splits highlight the uneven impact of policy frameworks, industrial composition, and local economic cycles, which national averages often mask. Historical research shows that while initial claims remain one of the strongest leading indicators of economic health, their predictive power diminishes during periods of regional policy shifts or sector-specific disruptions—conditions that could be developing now, particularly in public services and government-linked employment. For markets, there are multiple implications. This tight labor market tests the necessity of near-term monetary easing, making the story more complicated for rate-sensitive stocks such as utilities and real estate investment trusts that rely significantly on lower-cost financing. In contrast, undervaluation opportunities emerge in financials, where stable employment markets underlie credit quality and activity in lending, as well as consumer discretionary names that enjoy household spending strength. At Zaye Capital Markets, we note that although aggregate labor data still supports a constructive view, analysts need to monitor regional claims, employment adjustment at the industry level, and fiscal policy threats as key leading indicators of whether such resilience will continue or whether hotspots of weakness will spill over into the national picture.

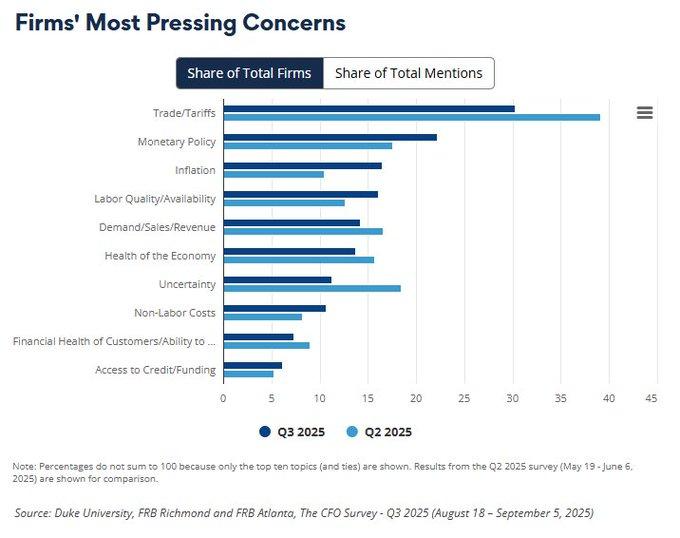

Firms Switch Attention from Trade to Inflation and Political Risks

The Q2 2025 CFO Survey, commissioned by Duke University, the Richmond Fed, and the Atlanta Fed together, identifies a significant shift in corporate priorities. Uncertainty related to tariffs that was prominent across headlines in earlier years dropped from 40% of references to 30%, marking increased focus on something other than trade policy as tensions dissipated. In its stead, uncertainty and monetary policy worries increased sharply, echoing the strains from a reported September 25, 2025 GDP growth rate of 3.8% and an acknowledgment that higher prices are chipping away at confidence in forecast-based planning. The shift highlights just how companies are adjusting their risk footing at a time when trade tensions are no longer the only impetus for volatility—price stability and rate policy are stepping into the spotlight.

The shift is not merely perception-driven. Academic evidence from a 2023 Journal of Monetary Economics study suggests prolonged inflation uncertainty can reduce firm investment by up to 15%, a finding directly aligned with the survey’s results. The persistence of pricing instability threatens capital spending, even in a period of above-trend GDP growth, highlighting the fragility of this expansion. Global metrics from multilateral institutions reinforce the point: elevated economic volatility continues to cloud business visibility, complicating strategic planning for firms balancing domestic growth momentum with unpredictable global dynamics. This stands in contrast to earlier market narratives that portrayed tariffs as the primary systemic risk, when in reality the inflation-policy nexus may prove far more destabilizing. For investors, there are key sector ramifications from the survey results. Industrials and consumer discretionary stocks, which depend greatly on leading investment cycles and consumer demand, appear stretched in an environment of policy and inflation uncertainty. Undervaluation could instead lie within defensive groups like utilities and healthcare, wherein stable demand balances out monetary swings. Analysts will need to pay close attention to decisions from the Federal Reserve docket at year-start because the survey is an indication that companies are already readjusting to a higher hurdle on rate cuts amid the lingering inflationary impulse still built into costs. At Zaye Capital Markets, we stress that sentiment at the corporate level is also indicative of a deeper structural threat: monetary policy uncertainty rather than tariffs could prove the key determinator of buy-side trends and S&P equity performance through year-end.

Looser Monetary Conditions Supportive of Market Tone but Risks Remain

The Chicago Fed National Financial Conditions Index (NFCI) relaxed to -0.54 in late September 2025, its loosest reading since early 2022. The dramatic decrease, backed by recent cuts by the Federal Reserve, is indicative of a significant shift towards market liquidity and credit conditions. Negative values of the NFCI over history have pointed towards accommodative financial conditions, often aligned with stronger equity market performances and easy borrowing. Positive values on the other hand often precede stress-tightening signals that were present around the crisis of 2008. The present shift thus indicates an interesting deviation from recession risk indicators, consistent with market sentiment of strength despite global uncertainty.

However, the environment is more subtle. Although relaxed conditions favor short-term market buoyancy, the unexpected easing follows a mid-2025 spike of the index that indicated tightening forces were coming on. Volatility of this sort highlights the delicate nature of the recovery, with threats related to lingering international tension—comprising trade disputes and changing monetary policy sentiment. Scholarly analysis echoes such circumspection: a study published by the Journal of Financial Economics in 2023 proved that positive readings of the NFCI are good forecasters of downturns but that impromptu shifts of the index—negative even—may presage instability of underlying credit and funding markets. This draws attention to the potential that favorable conditions prevailing today may obscure fragility rather than betoken fully robust expansion. For investors, the gap between easing financial conditions and ongoing macro risks provides opportunities as well as hazards. Growth- and high-beta stocks will gain from enhanced liquidity, but their valuation already may incorporate ongoing easing. Undervaluation, on the other hand, could be present in certain financials, where stable conditions favor lending yields, and defensive stocks that provide stability if conditions turn. We at Zaye Capital Markets emphasize that analysts need not regard the NFCI as an independent barometer of safety but use it as part of an integrated framework: easing financial conditions will tempt risk-taking but volatility within the index itself cautions that optimism about market direction needs to be tempered.

Elevated Mortgage Rates Challenge Housing Affordability

U.S. 30-year mortgage rates that peaked above 6.34% around the end of 2023 have relaxed a little over the past few weeks but continue to be significantly higher than the pre-2022 historic low. The spike was first led by the Federal Reserve’s rapid tight cycle that was initiated to contain inflation that peaked at 9.1% in June of 2022. Though there was moderate relief, mortgage rates continue to stay significantly higher than the long-run mean, a sign of structural shift of financing costs that has redefined affordability as well as demand across the landscape of housing. This higher backdrop provides evidence of lingering policy tightness despite inflation moving towards normal.

Notably, the mortgage rate is not solely a function of the Fed funds rate but is greatly influenced by longer-dated yields. The yield on the 10-year Treasury has climbed from 1.5% in 2020 to over 4% in 2025, basing mortgage rates at higher levels despite recent central bank rate cuts. This reality challenges the conventional narrative that easing short-term policy will soon unlock affordable housing finance. Instead, the persistence of higher longer-dated yields means that structural issues—fiscal imbalances, inflation expectations, and foreign capital flows—will play an disproportionate role in determining mortgage affordability. As such, the outlook for housing is less about headline policy easing and more about underlying currents from the bond market. For stock investors focused on equities, the picture is equally straightforward. Ongoing high mortgage rates continue to depress homebuilders and residential demand-related real estate investment trusts, where valuation could stay fully priced if affordability does not recover. Undervaluation could be brewing, by contrast, in renter-oriented REITs as well as select consumer discretionary stocks that serve households priced out of home ownership, wherein demand could prove more stable. At Zaye Capital Markets, we advise that analysts need to pay attention only to the interaction between Treasury yields and the costs of mortgage financing because that interaction will determine both the performance of the housing market as well as larger consumption trends related to household wealth effects.

Upcoming Economic Events

Throughout the week, market participants will be intently focused on two key economic data releases: the Core PCE Price Index m/m—the inflation preference of the Federal Reserve—and the Revised University of Michigan (UoM) Consumer Sentiment measure. Both have significance for markets balancing the tightrope of inflation control, consumer sentiment, and the shifting policy approach of the Fed. Here’s what to expect, and how the figures will influence market sentiment:

Core PCE Price Index m/m

The Core PCE is broadly regarded as the Fed’s best barometer of inflation, providing a cleaner read than headline CPI by removing food and energy.

- If the actual reading is above forecast, markets could view it as a bet that inflationary pressures are sticky enough that the Fed will hold off from easing further. That could be negative for rate-sensitive assets such as real estate and utilities while strengthening the U.S. dollar and pushing up bond yields. Equities linked to consumer spending could also weaken as hopes for tighter conditions gain traction.

- If the Core PCE reading is softer than anticipated, that will reinforce the case for the Fed doing rate cuts, leading to risk-on flows into growth areas such as tech and consumer discretionary while relieving pressure on longer-duration debt.

Revised UoM Consumer Sentiment

Consumer sentiment gives a real-time insight of households’ perceptions of spending, inflation, and income.

- If the new reading comes out stronger than forecasted, that will be a sign of surging household confidence that will reinforce the strength of consumption as well as add strength to cycle-related equities that are attached to retail, autos, and leisure. But higher sentiment will also fuel concern about sustained demand-pull inflation that will push investors to price in a more dovish US Fed.

- If sentiment reading comes out lower than forecasted, that will create red flags of fading consumer psychology that could feed through to softer spending. That will likely push flows towards defensive equity areas like healthcare and utilities while Treasuries will receive safe-haven demand.

STOCK MARKET PERFORMANCE

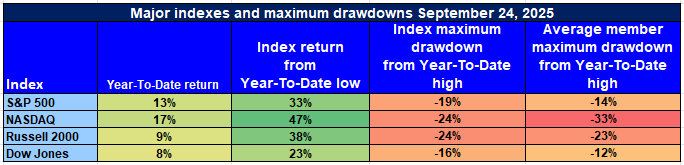

Indexes Rebound from Apr Bottoms but Broadness is Weak

U.S. stocks have made a robust recovery from the April 8, 2025 bottom, but the data highlights a patchy rally below the surface. Although headline indexes reflect double-digit rises in a number of instances, participation depth is softer, with mean member Drawdowns continuing to reflect that volatility and selective leadership continue to characterize market structure.

Here’s our roundup of the latest performance across leading indexes:

S&P 500: Solid Headline Gains, Limited Depth

YTD: +13% | +33% below April low | -19% below YTD high | Avg. member: -14% (from the low of April), -25% (from the high of YTD

The S&P 500 surged strongly by advancing 13% year-to-date and jumping 33% from the April low. But a 19% off its high and average member declines of up to 25% also show that the advance is still very narrow strength focused on large-cap leaders with poor breadth elsewhere.

NASDAQ: Growth Leadership With Underlying Stress

YTD: +17% | +47% lower than April low | -24% lower than YTD high | Avg. member: -33% (lower than April low), -47% (lower than YTD high

The NASDAQ is leading with a 17% YTD gain and a sharp 47% surge from April lows, but the picture is less stable beneath the surface. A 24% retreat from highs and steep average member drawdowns nearing 47% reflect fragility in growth and technology-heavy components, raising questions over sustainability.

Russell 2000: SmallCaps Bounce but Lack Conviction

YTD: +9% | +38% off Apr low | -24% from YTD high | Avg. member: -23% (off Apr low), -38% (off YTD high) Russell 2000 mounted a remarkable 38% comeback from its year’s low of April and is up by 9% year-to-date but enthusiasm is still muted. The 24% pullback from peak highs and large member losses—average of close to 38% from tops—highlight the stress on smaller economically sensitive issues.

Dow Jones: Defenive Profile Suggests Relative Stability

YTD: +8% | +23% lower than April low | -16% lower than YTD high | Avg. member: -12% (lower than April low), -23% (lower than YTD high The Dow Jones has increased by 8% year-to-date and by 23% from its April high with a comparitively tepid 16% pullback evidencing the robustness of its defensive bias. However-average declines of 23% from highs by its typical members suggest areas of weakness even of mature value groups.

At Zaye Capital Markets, we are still selective on position but prefer good-quality companies with stable earnings and balance sheets. Breadth remains a key measurement to monitor—without higher participation within the average stock, sustainability of the rally is doubted.

THE STRONGEST SECTOR IN ALL THESE INDICES

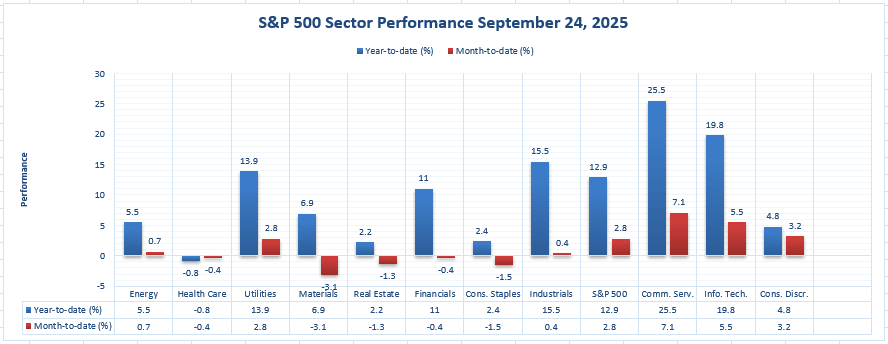

Leaders Focusing on Communication Services and Technology

From the latest sector prints we could obtain, we see that leadership is completely focused. The S&P 500 sits at +12.9% YTD and +2.8% MTD, a good baseline. Relative to that, Communication Services is the best-performing sector at both horizons at +25.5% YTD and +7.1% MTD, followed by Information Tech at +19.8% YTD and +5.5% MTD. Industrials rounds out the YTD top three at +15.5% (MTD +0.4%).

Best performers (by MTD and YTD):

- Communication Services: +25.5% YTD | +7.1% MTD

- Information Technology: +19.8% YTD | +5.

- Industrials: +15.5% YTD | +0.4% MTD

- Utilities: +13.9% YTD | +2.8% MTD

- Financials: +11.0% YTD | -0.4% MTD

Middle & laggards (numbers exactly as printed):

- Energy: +5.5% YTD | +0.7% MTD

- Consumer Discretionary: +4.8% YTD | +3.2% MTD

- Materials: +6.9% YTD | -3.1% MTD

- Real Estate: +2.2% YTD | -1.3% MTD

- Consumer Staples: +2.4% YTD | -1.5% MTD

- Health Care (weakest YTD): -0.8% YTD | -0.4% MTD

We at Zaye Capital Markets notice that Communication Services is strongest on both metrics followed by Technology which also outperforms index by +19.8% YTD / +5.5% MTD—though Health Care is the only negative sector YTD at -0.8%.

Earnings

Earnings Recap– 25-Sept-2025

- Accenture (ACN)

Accenture beat consensus on adjusted EPS of $3.03 (vs ~ $2.98) and revenue growth of 7% to $17.6B, bolstered by acquisition contributions and continued AI & technology bookings. However, management issued cautious guidance for FY 2026 growth (1–5%), citing macro uncertainties and softness in U.S. federal spending. Key factors include backlog exposure, visa cost pressures (H-1B fee discussions), and margin sensitivity to discretionary spending.

- Jabil (JBL)

Jabil delivered a strong quarter with adjusted EPS of $3.29 (versus consensus ~$2.92) and revenue of $8.3B vs $7.6B expected. Its forward outlook targets ~5% revenue growth and slight margin expansion, leaning heavily on AI / data center demand to offset weakness in auto and renewables. The stock fell intraday ~9%, indicating that markets required more than just beats—investor expectations were elevated.

- TD SYNNEX (SNX)

TD SYNNEX also reported, per pre-market expectations an adjusted EPS of ~$2.98 on revenue ~$15.12B. Analysts will look at its performance within IT distribution and hyperscaler channels, margin compression, and supply chain costs.

- Costco (COST)

Costco was slated to report its Q4 results after the close, with consensus EPS ~$5.81 and revenue ~$86.11B. Investors will scrutinize membership trends, same-store sales, margin pressures from freight, and inventory levels.

Earnings Preview– 26-Sept-2025

- Apogee Enterprises (APOG)

Apogee Enterprises has previously reported quarterly results (e.g. Q1 2026 EPS $0.56 beat vs $0.45) and revenue ~ $346.6M. While a new release today has not been fully confirmed, investors should watch for updates to its outlook, segment performance (glass, architectural), and cost pressures in materials and freight.

- Golden Matrix Group (GMGI)

Golden Matrix Group is expected to report today with limited consensus data available. Investors should monitor revenue growth from its gaming platforms, margins within licensing, and guidance on international expansion, where volatility has been a theme.

- Taylor Devices (TAYD)

Taylor Devices has limited coverage ahead of today’s results, but focus should remain on aerospace and defense segment performance, backlog health, and margin resilience in the face of material and supply chain costs.

- Anebulo Pharmaceuticals (ANEB)

Anebulo Pharmaceuticals also has results due today, with little market consensus. The key will be updates on clinical trial progress, R&D spending, and cash burn rates, as these factors will drive investor sentiment more than top-line numbers at this stage.

Market Wrap – Friday, September 26, 2025

U.S. stock markets started the day on tense ground, with sentiment getting progressively weakened by the stress of renewed threats of tariffs, sticky inflation signals, and uncertainty over the next moves of the Federal Reserve. While the S&P 500 and Nasdaq are once again being dragged down by frailness out of mega-cap techs, the Dow Jones and Russell 2000 are holding up a bit as the market shifts towards defensives and industrials.

Stock prices

Economic Indicators and Geopolitical Developments

The market’s nervous tone today is being spurred almost entirely by new tariffs, with 25% to 100% duties landing on groups like industrial companies and pharma. This escalation of trade is fueling inflation fears at precisely the moment that stronger-than-anticipated jobless claims alleviated hopes of immediate easing by the Fed. As a whole, these factors are providing a confusing backdrop—sensitive-to-growth equities continue to weaken while defensive areas are experiencing flows. Meanwhile, geopolitical nervousness over U.S.–China tension is fueling risk-off sentiment and impacting tech valuation heavily.

Latest Stock News

- $NVDA | Nvidia stock slips back under stress after declining below a crucial technical level, an indication that market fervor over AI is fading. That’s spilling over into the wider semis space.

- $TSLA | Tesla is perhaps most severely affected of the mega-cap stocks as high-flying multiples are revalued by investors against evidence of softening demand alongside rising competitive forces within the electric vehicle market.

- $META | Meta falls again as markets recalibrate its ad revenue trajectory amid high spending on AI initiatives that cast clouds over near-term profitability.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—continue to feel the squeeze this week, with average pullbacks of over 18% from recent tops. Tesla and Meta are at the forefront of the losses, while Nvidia’s pullback has fanned worries about AI-fueled frenzy. The softness of those leaders is holding back the S&P 500, calling its sustained rally potential into question. Meanwhile, investors are shifting into energy and industrials, which have fared relatively well despite worries over tariffs and international uncertainty. Without renewed strength from its largest components, the broader index finds it hard to pick up speed.

Major Index Performance up to Friday, 26th of September, 2025

- S&P 500: Current price at 6,600.12. Down by 0.

- Nasdaq Composite: Currently at 22,300.44, down by 0.8%, with selling concentrated on.

- Dow Jones Industrial Average: Lower by 0.2% at 46,050.21, aided by selective strength across defence.

- Russell 2000: Flat at 2,420.18, responding mildly following small caps pullback.

At Zaye Capital Markets, we closely follow rotation trends, macro drivers, and flows of capitals. While markets price inflation uncertainty, shifts in tariff policy, and the next steps of the Fed, leading companies’ capacity to hold earnings momentum will prove pivotal to determining direction of equities into Q4.

Gold Price – Friday, September 26, 2025

Gold is at $3,748.98 an ounce today, drifting narrowly lower as markets digest a confusing batch of political headlines, macro data, and anticipated releases. Trump’s broad basket of comments—from threatening firings if there’s a government shutdown, to orders on political violence, forced sale of TikTok, and threats over Israel’s status—have injected an element of geopolitics tension across markets. Typically, such uncertainty would provoke safe-haven flows into bullion, but the price action of the metal itself indicates resistance against stronger economic currents. Ahead of the Core PCE Price Index and Revised University of Michigan Consumer Sentiment data later, investors decide if sticky inflation or robust consumer confidence will push U.S. yields higher, consequently suppressing bullion’s appeal. If the data surprises on the high side, yields and the greenback are set to harden, creating downward pressure on bullion; if softer, bullion could regain momentum as demand for defensive assets grows against an uncertain political and economic backdrop. Yesterday’s economic data also rewrote sentiment. The decrease in weekly jobless claims coupled with a GDP growth update to 3.8% reinforced the narrative of a still-robust U.S. economy, hardening the case for the Federal Reserve holding off on near-term easing. This equation puts the opportunity cost of holding bullion higher as greater real yields and a stronger dollar circumscribe upside follow-through against the continued ferment of political risk. We thus see analysts divided: while policy unpredictability and geopolitics favor medium-term safe-haven status for gold, the very short term remains governed by the Fed’s approach and inflation indicators. At Zaye Capital Markets, we underline that bullion is at a crossroads—the scales of balance between robust macro data on the one hand and building geopolitical risk on the other will determine whether $3,750 forms a consolidation floor ahead of another leg up or beginning of a deeper corrective phase.

Oil Prices – Friday, September 26, 2025

Oil is at $65.29 per barrel for WTI after recovering from recent lows as the market processes a blend of supply disruptions, geopolitics, and shifting demand forecasts. Russia’s move to reduce fuel exports after renewed Ukraine strikes has strengthened the diesel market, pushing crude higher, while OPEC+ production adjustment speculation and a possible resumption of Iraqi Kurdistan exports have injected volatility. Profit-taking by traders after the surge also echoes doubts over whether supply-side shocks will be able to sustain higher levels unless there is a corresponding rise in demand. From the policy angle, Trump’s ramping up of rhetoric—on tariffs, national security orders, and geopolitical positions—adds an element of uncertainty. His position on trade and enforcement actions could complicate cross-border energy flows, particularly if sanctions or retaliation become an outcome that strengthens crude’s status as a geopolitics hedge. On the flip side, investors continue to factor that stronger U.S. production growth, if spurred politically, could cool upside momentum, creating a fine balance between supply bull-positive risks and bearish oversupply scenarios. Yesterday’s economic figures have also fed directly into oil’s sentiment profile. Bigger-than-expected jobless claims and GDP only reinforced a robust U.S. economy, paradoxically putting a squeeze on crude by reaffirming hopes that the Federal Reserve will hold off on rate cuts, maintaining tighter financial conditions and elevating the expense of holding commodities. Next week’s Core PCE Price Index and Revised UoM Consumer Sentiment are crucial: a hotter PCE read will spur yields and the dollar higher, suppressing oil demand and putting downward pressure on prices, while a softer inflation reading coupled with weaker sentiment will rekindle demand hopes and facilitate another leg higher in crude. Both OPEC and the IEA continue at the center of such an ecosystem—future remarks by OPEC on quotas, spare capacity, and by the IEA on demand forecasts could swing sentiment either way. At Zaye Capital Markets, we recognize that oil exists within a region of increased sensitivity wherein supply shocks, Trump policy cues, and macroeconomic data intersect to determine the immediate course of direction with investors forced to chart a market governed equally by politics as fundamentals.

Bitcoin Prices – Friday, September 26, 2025

Bitcoin is rangebound around $109,000-$111,000 after crashing sharply from earlier highs and dipping below $110,000 yesterday. The move indicates both a larger crypto market decline—wherein over $160 billion of value was erased—and macroeconomic headwinds continuing their_pressure upon digital currencies. Soaring Treasury yields and a stronger U.S. unit have contributed to additional downward pressure from traders reassessing prospects of near-term easing by the Federal Reserve. These dynamics underline Bitcoin’s delicate position: although exhibiting technical strength in previous selloffs, its status as a high-beta risk asset entails remaining extremely responsive to liquidity condition shifts. Market observers believe that the present consolidation could precede a comeback only if macro forces are alleviated or safe-haven buying reasserts itself more strongly. Trump’s series of policy pronouncements and political maneuvers—from threatening mass government firings in the event of a shutdown, to ordering national security directives and reinforcing U.S. positions abroad—introduce fresh political volatility that normally supports Bitcoin’s appeal as a hedge against institutional instability. However, this tailwind is being overshadowed by stronger U.S. data: yesterday’s dip in jobless claims and GDP growth revision to 3.8% reinforced confidence in economic resilience, reducing the urgency for Fed rate cuts and tightening financial conditions further. This has dampened speculative appetite in the crypto market, pulling Bitcoin lower despite geopolitical and political uncertainty. Looking ahead, today’s Core PCE Price Index and Revised UoM Consumer Sentiment will be pivotal: hotter inflation data could push yields higher and pressure Bitcoin further, while softer prints may open space for a rebound. At Zaye Capital Markets, we see Bitcoin caught between its narrative as a hedge against political turbulence and the reality of macro forces that continue to dictate short-term price action.

ETH Prices – Friday, September 26, 2025

Ethereum hovers at $3,872.11, dipping below the $4,000 handle as the crypto market digests changing capital flows and macroeconomic headwinds. Spot ETH ETFs have seen outflows of $79.4 million over the last three consecutive days, highlighting institutional indecision and profit-taking following the earlier surge. Those outflows are indicative of short-term risk aversion as higher bond yields and a stronger greenback reduce demand for zero-yielding assets. But underlying that surface-level weakness, whale wallets holding between 1,000 and 100,000 ETH have been building aggressively, adding almost 3.8 billion ETH worth around $1.49 billion over recent sessions. That dichotomy spots widening separation of positioning: institutional vehicles withdrawing capital while deep-pocket investors flash conviction that Ethereum is priced too low at present levels.

This tug-of-war is creating ETH’s ecosystem. On one hand, continued ETF outflows may accelerate downside pressure if wider macro data, such as today’s Core PCE, spurs a stronger dollar and higher yields, sapping demand for crypto exposure. On the other hand, whale accumulation provides a stabilizing influence, soaking up selling pressure while building medium-term support around the $3,800 mark. If whale buying persists, that could provide the foundation for a medium-term recovery, but any rise in ETF outflows or further crypto-market liquidations could test that support more aggressively. At Zaye Capital Markets, we believe ETH’s ongoing consolidation is a delicate balance between bearish macro forces and bullish on-chain accumulation. The institutional outflow vs. whale conviction battle will decide if Ethereum’s price stabilizes here or drifts into a deeper corrective mode.