Where Are Markets Today?

U.S. and European futures are trending lower this morning as investors brace for the potential fallout from a looming U.S. government shutdown. Dow Jones futures were last seen down 68 points (–0.15%), while S&P 500 and Nasdaq 100 futures fell more than 0.2%, reflecting growing concern that political gridlock in Washington could disrupt fiscal operations and delay key economic data releases. Across the Atlantic, European markets are also on the back foot, with Euro Stoxx 50 futures sliding modestly, following the global sentiment reset. The weakness comes as Congress continues to spar over a stopgap funding measure, with two failed Senate attempts on Tuesday deepening fears that the government could partially shut down by midnight. President Trump weighed in Tuesday night, calling a shutdown “probably likely,” and blamed Democrats for refusing to “bend even a little bit.” With SEC staff already told to prepare for a potential funding lapse and roughly 750,000 federal employees at risk of furlough (per CBO estimates), market participants are reassessing short-term macro clarity.

The futures drift lower today can be attributed to two core concerns. First, the possibility of a shutdown could significantly delay or cancel the release of critical economic reports—including the September Nonfarm Payrolls report, ISM services data, and CPI—which are essential inputs for the Federal Reserve’s rate path decision. Without those data points, monetary policy visibility declines sharply, increasing uncertainty for investors and policy-dependent sectors. Second, political instability and Trump’s aggressive rhetoric—including promises to lay off federal workers, threats to tariff drugmakers, and military warnings about Venezuela and Hamas—are raising fears of unpredictable policy shocks that could undermine investor confidence. The shutdown scenario is unlike previous episodes, where markets largely looked through the noise. This time, the risk is compounded by already elevated valuations, a fragile labor market outlook, and key central bank decision windows approaching.

In Europe, futures are echoing U.S. sentiment, dragged lower by concerns over both external macro headwinds and internal supply shocks, particularly in energy and resources. A potential disruption in U.S. data flow directly impacts European investors who rely on synchronized policy cues and transatlantic demand indicators. Additionally, OPEC+ supply plans and weakening industrial demand are weighing on cyclical sentiment in the region. The combination of U.S. political drama, data flow uncertainty, and commodity instability is fostering a defensive stance across European equity markets. Investors in both regions are gravitating toward safe havens like bonds and gold, while trimming positions in sectors that depend on government contracts, policy clarity, or high earnings visibility. With no resolution in sight as of this morning, futures remain weak, and market tone cautious.

At Zaye Capital Markets, we interpret this downbeat open as a function of tactical de-risking rather than outright panic. However, the inability of Congress to pass even a temporary spending bill sends a message of dysfunction that markets cannot ignore—especially with inflation, earnings season, and monetary policy decisions converging in October. For now, we expect trading to remain volatile and reactive to headlines, particularly around Capitol Hill developments and any signal of a last-minute deal. Should the shutdown become a reality, expect further deterioration in risk appetite and growing pressure on sectors like healthcare, defense, and federal contractors. On the upside, any last-minute compromise or clarity from the Fed regarding how they would handle data lags could stabilize sentiment. Until then, markets are operating with a high degree of policy fog—and futures are pricing that in accordingly.

Major Index Performance as of Wednesday, 1st of Oct., 2025

- S&P 500: Trading at 6,688.44, up 0.41% on the day.

- Nasdaq Composite: Currently at 22,660.01, up 0.30%, with modest gains despite tech headwinds.

- Dow Jones Industrial Average: Up 0.18% to 46,397.83, lifted by strength in financials and industrials.

- Russell 2000: Last trading flat near 2,432, showing signs of stabilization as small caps digest recent moves.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—remain central to market structure but continue to exhibit signs of valuation fatigue. With sector-wide pullbacks averaging over 18% from recent highs, this group has weighed heavily on both the Nasdaq and S&P 500. Meta and Tesla in particular have suffered from investor rotation out of AI and high-multiple names. The result: a narrow market advance that lacks broad participation. Without renewed strength from these top-weighted names, index-level resilience remains fragile, and attention has shifted toward sectors like energy, financials, and industrials as sources of relative strength.

Drivers Behind the Market Move – Wednesday, October 1, 2025

Global markets are navigating a tense and uncertain landscape today, driven by a mix of fiscal brinkmanship in the U.S., political volatility, and critical macroeconomic data releases. As traders in both the U.S. and Europe react to recent developments, futures are edging lower and volatility remains elevated. Key factors shaping today’s market trajectory include:

- U.S. Government Shutdown Concerns

The threat of a U.S. government shutdown looms large over today’s session. With Congress failing to agree on a funding resolution by the Wednesday deadline, federal agencies have begun preparing for a lapse in operations. The SEC has already advised staff to expect a funding halt, and the Congressional Budget Office estimates that around 750,000 federal workers could face furloughs. President Trump declared the shutdown “probably likely” and blamed Democrats for refusing to compromise, while also threatening mass layoffs of federal employees. The risk of a prolonged shutdown is unsettling markets not only because of potential service disruptions but also due to the expected delay of critical economic data—including the Nonfarm Payrolls report, ISM services data, and CPI—which markets rely on for rate and earnings clarity.

- Trump’s Tariffs and Political Volatility

President Trump’s recent remarks are injecting significant uncertainty into markets. His threats to impose 5%–8% tariffs on pharmaceutical companies that don’t agree to pricing terms, combined with a newly announced deal to slash drug prices via the “TrumpRx” platform, are hitting the healthcare and biotech sectors. Meanwhile, his fiery rhetoric—including promises to fire federal officials on the spot, comments on military aggression toward Venezuela, and declarations of being “very close to a deal on Gaza”—have broadened geopolitical and policy risk premiums. Markets are increasingly pricing in unpredictable executive actions, weighing on sectors tied to regulation, trade, and defense spending.

- Upcoming Economic Data and Policy Signals

Investors are also closely watching today’s slate of high-impact economic releases, including the U.S. ADP Non-Farm Employment Change, ISM Manufacturing PMI, and ISM Manufacturing Prices, alongside the Eurozone’s Core CPI Flash Estimate. These data points are vital in gauging inflation pressures and labor market strength—two central concerns for both the Federal Reserve and the ECB. Yesterday’s JOLTS data showed strong job openings but a weakening quits rate, suggesting labor market fragility under the surface. A weaker-than-expected ADP or ISM reading today could fuel expectations for earlier Fed rate cuts, while hotter prints could spark fears of delayed monetary easing.

In summary, today’s market movements are being shaped by a confluence of fiscal dysfunction, political escalation, and sensitive economic data flow. With the risk of a shutdown becoming more real and Trump’s policy tone turning sharply aggressive, investors are trimming risk and adopting a defensive posture. The next 24–48 hours will be pivotal in determining whether markets stabilize—or face renewed volatility driven by headline risk and data shocks.

Digesting Economic Data

The TRUMP Tweets and Their Implications

President Trump’s recent barrage of statements—ranging from sweeping economic threats to military posturing—has sent ripples across financial markets and policy circles alike. His remark that “we may do a lot of laying off federal workers” introduces a strong signal of administrative shake-up, raising questions about government continuity and the delivery of public services in the short term. Simultaneously, his promise to fire officials “on the spot” if disliked and to penalize pharma companies with tariffs if they don’t make a deal, paints an aggressive executive tone that could reshape investor expectations around regulatory risk, labor stability, and corporate profitability. These statements reinforce the perception of a policy environment driven by unilateral executive action, which tends to elevate volatility in equity markets, especially in sectors exposed to federal contracts and healthcare regulation.

Of notable impact is the administration’s upcoming launch of the “TrumpRx” platform, coupled with a sweeping agreement with Pfizer to slash drug prices by up to 100% in some cases. This populist push toward direct-to-consumer pricing, framed under “most favored nation” pricing logic, could fundamentally disrupt pharma sector revenue models, especially for companies like $PFE, $LLY, and $UNH. Markets will have to weigh whether this is a political play aimed at midterm votes or the foundation of a broader pricing regime overhaul. Trump’s declaration that drug pricing will have a “huge impact” on elections further supports the view that healthcare stocks could be facing heightened headline and legislative risk well into 2026.

Meanwhile, Trump’s foreign policy stance, especially his claim of being “very close to a deal on Gaza” and warning there’s “not much room to negotiate with Hamas,” suggests heightened geopolitical involvement, while his call to pursue cartels in Venezuela “by land” elevates concerns over military entanglement. Such rhetoric—amplified by Hegseth’s hawkish commentary about preparing for war—underscores a strategic shift toward a hard power doctrine, likely to benefit defense contractors and energy firms, while placing pressure on diplomatic institutions and oil supply routes. The reference to grading combat readiness “according to the highest male standard” also reflects a deepening emphasis on military performance and traditionalism, reinforcing the administration’s alignment with hardline defense narratives.

Altogether, these comments reveal a broader thematic convergence: an assertive, interventionist approach to both domestic policy and international strategy. For markets, this translates into higher sector-specific risk in healthcare, biotech, and pharmaceuticals, increased demand for defense and energy equities, and greater macro volatility as economic actors attempt to price in policy shifts with minimal legislative filtering. At Zaye Capital Markets, we see these comments as more than political theater—they represent directional cues for portfolio construction in a market where executive unpredictability may soon become the primary macro risk factor.

Texas Services Stumble, But Optimism Builds

The Dallas Fed Services Index, released September 30, plummeted to -5.6 during September following August’s +6.8, affirming a rapid service sector contraction within Texas. The move brings to a close a short-lived run of expansionary streaks and raises new doubts about forthcoming demand softness to follow within Q4. Subindices of revenue, employment, and general attitudes toward business all dropped into negative readings—as an aggregate whole, suggesting a weaker regional economy. Notably, the services sector accounts for nearly 80% of Texas output, and the data can be an early lead indicator of national soft services softness, specifically because Texas leads cyclical turns with its economically diverse foundation.

Yet the report was not universally pessimistic. Despite activity decline now, the six-month business outlook index recovered into positive ground and planned capital spending intentions rose. That’s a sign that many companies judge the weakness now to be temporary, perhaps triggered by near-term demand or cost pressures and not structural softening. Improved sentiment to come may correspondingly be triggered by rising expectations that the Federal Reserve may ease policy over coming quarters, particularly should broader service activity continue to ease down with soft labor markets and cooling wage growth. Against this context, our sense is that some mid-cap income office REITs or healthcare tenancy-focused REITs with professional services exposure within the Sun Belt are cheap. By virtue of valuations pinched by earlier rate gyrations and prices continuing to lag potential policy shifts, these stocks stand to gain on both sides of rate reprieve and a service sector rebound. Ahead of this turn, analysts should monitor services PMIs, NFIB small business hiring intentions and forthcoming FOMC wording to see confirmation of this about face. The interplay between short- and long-term horizons of business surveys will be particularly revealing of how long this contractionary stage can endure—and wherein true value resides.

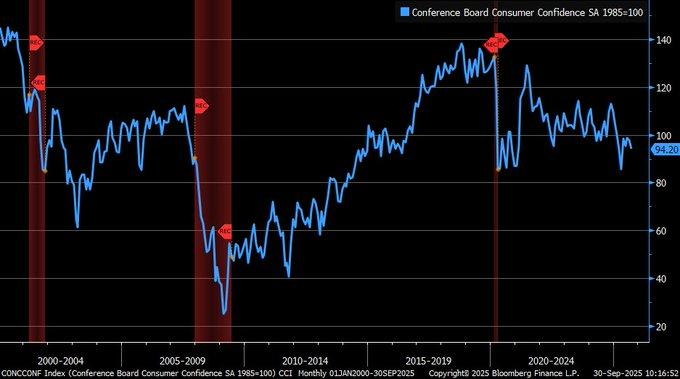

Consumer Confidence Breaks Lower, Future Outlook Dims

The Conference Board Consumer Confidence Index declined to 94.2 during September, below the expectations of 96 and marking the lowest print since April of 2025. The abrupt decline here following August’s revised 97.8 reaffirms a worsening consumer story against building macro risks. The Present Situation Index, registering feelings about conditions now, declined sharply to 125.4 from 132.4, and the Expectations Index declined to 73.4 and stayed firmly below the key 80-point recession peril signal threshold. By precedent, readings this close have been associated with onset-of-recession conditions, specifically with softening labor markets and fiscal uncertainty.

Being a forward-looking indicator, declining consumer sentiment is of keen interest to equity and credit markets alike. As expectations drop and the background shrouded by strain within the job markets and federal budget impasse, this decline potentially translates into increased equity volatililty, with consumer discretionary and retail-related areas being particularly sensitive. The fact that this indicator appears consistently across several independent reporting agents only serves to enhance its significance, as this represents a measure of objective sentiment and of subjective anxiety within households. Notably, the Expectations Index reliably leads spending patterns by several months and thus serves to foreshadow consumption momentum within Q4 and investor risk appetite. With this dynamic, we identify promise in a high-margin consumer staples stock that’s trading off its five-year average P/E multiple. Though discretionary units will endure through confidence-related pressures, staples with strong pricing power and reliable cash flow generation hold ground through demand downturns. Investors should monitor upcoming weekly jobless claims, initial October Michigan Sentiment data, and higher-frequency retail foot traffic to assess whether this softening consumer indicator is short-lived or part of a broader-based trend. The divergence between consumer outlook and equity valuation multiples through sentiment-driven industries could offer asymmetric setup to re-pricing.

Job Openings Level Off, But Employer Sentiment Weakens

August’s JOLTS report offered a nuanced snapshot of the U.S. labor market, with job openings inching up to 7.227 million—slightly above the 7.2 million consensus and revised 7.208 million in July. This marginal increase suggests underlying employer demand remains intact, even as broader macro uncertainties weigh on hiring sentiment. Employers are still posting positions, but filling them is becoming more measured, reflecting a labor market that remains tight but no longer overheating—a key distinction for rate path expectations and economic momentum going into Q4.

But beneath the headline strength, the quits rate fell to 1.9%, down from cyclical peaks above 2.3%, recording declining worker optimism and mobility. That’s important—past quit rates this low have corresponded to weaker wage gains, lowering inflation pressures and allowing room for the Federal Reserve to consider a rate cut should broader disinflationary patterns persist. The message: companies stay cautious but busy recruiting while workers increasingly take risks—I attribute this to higher living costs, diminished prospects elsewhere, and growing uncertain fiscal horizon.

We identify value developing within a national manpower and workforce solutions company with its shares below historic EV/Sales multiples. The stock is normally associated with labour churn and recruitment volumes, but could come into its own with companies relying on flexible staff while permanent recruitment is hesitant. Analysts will want to monitor upcoming Nonfarm Payrolls, average hourly wages and temporary recruitment data—these will be crucial in establishing whether JOLTS resilience presently experienced is a flattened peak or the commencement of a new labour cycle, and whether monetary policy accommodation is fast forwarded.

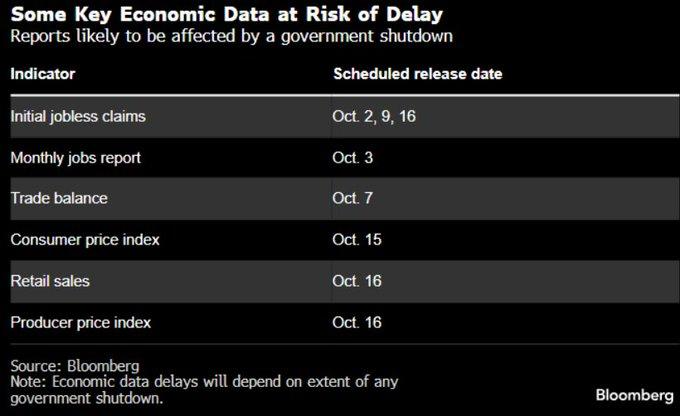

Threat Of Shutdown Can Cripple Prime Data Flow

As Congress cannot pass a funding bill before September 30, markets now run the risk of a government shutdown starting October 1—something that might temporarily freeze the publication of key U.S. economic indicators. A list of potential-risk releases compiled by Bloomberg and distributed among market strategists mentions initial jobless claims (Oct 2) and the report of September Nonfarm Payrolls (Oct 3) among vulnerable releases—instrumental to judge the conditions of the labor markets and to set the direction of monetary policy expectations. The risk of the shutdown boosts the vulnerability of traders and economists that get guidance about the economy’s strength through real-time information and position themselves accordingly.

From past experience, the 2018–2019 shutdown created an estimated 0.1% to 0.2% weekly GDP slowdown and injected palpable disruption into Treasury markets and equities. Aside from headline risk, the crux of the issue is that a shutdown creates a data void—leaving policymakers and investors to sense by touch. That boosts probabilities of reactionary policies and widens confidence intervals surrounding Fed decision-making. Lacking new labor and inflation data, the Federal Reserve’s next moves become ever more speculative and susceptible to policy misalignment and surprise re-pricing of markets. Here, we uncover potential mispricing of a large-cap data analytics and financial infrastructure stock with extensive government contract exposure and intrinsic shutdown strength. Such stocks, over the past, have benefited from rising volatility and heightened demand for alternate data flows during times of government data gaps. Analysts will want to track Fed’s regional bank statements, real-time private payroll indicators, and select federal agencies’ operating status after October 1 to gain a thorough understanding of the damage. The bigger risk here isn’t the shutdown itself—but the policy tilt and market vulnerability that results when visibility disappears.

Manufacturing Uncertainty Eases In Texas, Outlook Stabilizes

The Dallas Fed Texas Manufacturing Outlook Uncertainty Index declined to 13.9 during September and represents a sharp moderation following earlier this-year readings above 50. The decline indicates decreased dispersion of future production and shipment conditions evaluated by companies—i.e., manufacturers better align their short-term outlooks. Although overall sector activity is weak overall and soft in output and employment, the uncertainty decline represents a move to stabilisation rather than continuing reactive caution that is particularly significant for a heavily cyclally-exposed State.

The uncertainty spike in 2025 came courtesy of a mixture of volatility in the prices of oil, global demand projections, and mixed policy indications surrounding trade and infrastructure. The inputs having normalized, sentiment dispersion having narrowed, companies seem to be getting increasingly comfortable with their planning scenarios—even though the scenarios remain of slower growth. Though overall Texas Manufacturing Outlook Survey registers soft demand and slight workforce adjustments, new clarity of expectations may be the springboard to steadier capital allocation, particularly into machinery, fabricated metals, and industrial materials. From an investment perspective, we identify relative potential in a local industrial supplier with higher operating leverage and traditionally close correlation to Texas PMI cycles. As uncertainty abates and sentiment solidifies to lower but stable output levels, this kind of names can gain ground with visibility being restored and restocking of inventories resuming. Analysts should monitor the Kansas City Fed Manufacturing Survey, energy capex forecasts, and world export orders, each of which can confirm the broader thesis of stabilization within American manufacturing centers. As uncertainty diminishes, even small gains in demand can yield oversized equity reactions within operationally geared cyclical stocks.

Midwest Spike Suggests Demand Rebound Despite Affordability Gap

The National Association of Realtors announced a dramatic 8.7% month-to-month increase in Midwest pending home sales during August of 2025—the strongest reading within the area since mid-2023 and over twice the national gain of 4%. The surge snaps a streak of mostly flat action during the last two years and emphasizes the area’s emerging popularity as a relatively cheap area to live with median home costs of close to $280,000, significantly below the national median of $400,000. The visual data that follows underscores just how anomalous this shift is within a wider context of tempered housing momentum.

What’s driving the surge? Several converging factors: stabilizing mortgage rates, regional job stability, and a widening affordability gap between coastal and interior housing markets. Buyers appear to be recalibrating toward price-accessible metros, especially as high rates limit borrowing power in higher-cost areas. While middle-class wage growth remains tepid, the Midwest’s lower entry points and slower pace of price inflation may be unlocking sidelined demand from first-time buyers and relocating households—especially those priced out of markets like the West and Northeast. With the macro backdrop, we think a Midwestern-centric homebuilder stock that’s trading below book value offers relative upside. With land already banked at lower cost bases and healthy absorption levels across key metro cores, the stock is poised to enjoy volume-driven operating leverage as local demand rebounds. The analysts should monitor volumes of mortgage applications, builder sentiment indices, and local wage growth metrics to confirm if this sales surge is durable or a seasonally driven rate-driven bump. If resilience holds up in the Midwest, expectations of housing-related equities might need to reorder to account for local tailwinds instead of national averages.

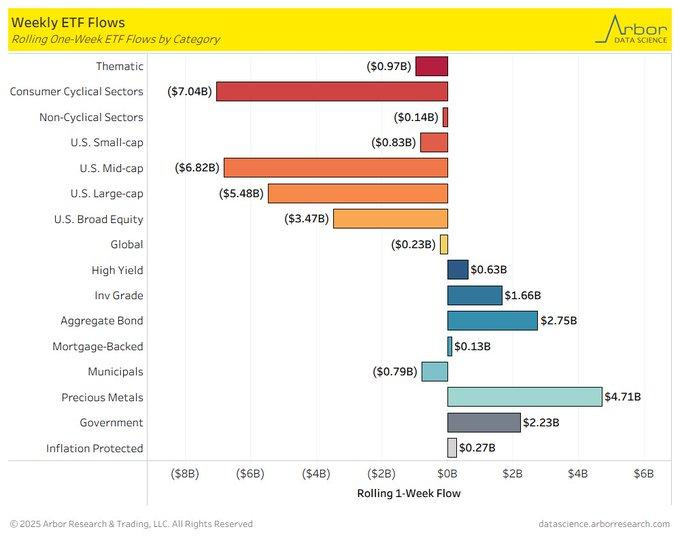

Equity ETF Outflows Surge As Bond And Gold Demand Spike

During the last week, equity ETFs experienced over $20 billion of outflows, marking a pronounced turn of investor sentiment to risk-off positioning. Consumer cyclical stocks (-$7B) and mid-caps (-$6.8B) were the leaders of the exodus, with selling hard by recent tech sector weakness having pulled broader sentiment and rebalancing flows off growth-sensitive areas. The scope and concentration of the outflows indicate something beyond short-term rotation—it indicates increased caution as markets process the commencement of a Federal Reserve rate-cutting cycle and position for weaker earnings momentum to come.

At the same time, fixed income ETFs took in more than $12 billion, clear evidence that rate-sensitive assets are coming into favor again with policy rates reaching their peak. Aggregate bond funds took in $5.75B and government securities took in $2.23B, aided by declining yields and fresh buying interest in duration. The sector shift is consistent with early-cycle flows when rate reductions tilt preference to income-generating assets with stability of capital, particularly with front-end compression of yields. The flows also mirror investor perception that the Fed’s about-face is not an isolated move but the beginning of a prolonged easing trend that gives a buoyancy to the medium-term total return picture of high-grade debt. Precious metals ETFs—headlined by gold—saw $4.71B inflows, the largest of any category. Investors are looking to buy portfolio hedges against geopolitical uncertainty, dollar weakness, and real rate compression with the yellow metal posting its largest September gains in nearly 14 years. Even through some final-week profit-taking off multi-year highs, assets keep flowing into safe-havens, supporting the continuing relevance of this asset class during a regime shift. We find appeal here to a large-core silver ETF, trading below its NAV and lagging the golden rally despite firmer industrial tailwind. Analysts will want to watch real yields, ETF velocity of flows, and COMEX positioning report data to gain further insight into how sustainable this defensive lean will be during the fourth quarter.

Upcoming Economic Events

EUR Core CPI Flash Estimate y/y, EUR CPI Flash Estimate y/y, USA ADP Non-Farm Employment Change, USA ISM Manufacturing PMI, USA ISM Manufacturing Prices

As we enter the opening days of October, a slate of high-impact economic releases across both the U.S. and Eurozone is poised to shape investor positioning and policy expectations. From inflation gauges in Europe to U.S. labor and manufacturing data, each release has the potential to recalibrate market sentiment and either validate or challenge current pricing around central bank easing cycles. Here’s a breakdown of what to watch this week—and how markets are likely to respond depending on the outcome of each data point:

EUR Core CPI Flash Estimate y/y & EUR CPI Flash Estimate y/y

The Eurozone inflation snapshot will be crucial for gauging whether the European Central Bank’s pause is temporary or could evolve into an easing cycle in the coming quarters.

- If either the Core CPI or headline CPI comes in above forecast, it would suggest that underlying price pressures remain sticky—particularly in services—and could prompt the ECB to retain a more hawkish bias longer than markets currently anticipate. This would likely trigger a rally in European bond yields, euro strength, and downside pressure on rate-sensitive equities like real estate and utilities.

- However, a weaker-than-expected inflation print would validate recent disinflationary trends, bolstering dovish policy expectations. In that scenario, the euro could weaken, while European equity markets—particularly export-heavy and growth-oriented sectors—could benefit from easing rate assumptions.

USA ADP Non-Farm Employment Change

Serving as a precursor to the more closely watched Nonfarm Payrolls report, the ADP figure will offer the first labor market pulse of the month.

- Should the actual number exceed expectations, it would reinforce the resilience narrative around the U.S. labor market, likely boosting cyclical equities, financials, and small caps while nudging yields and the U.S. dollar higher on the view that Fed rate cuts may be delayed.

- However, a miss on the ADP print would support the argument that job creation is losing momentum, especially in the private sector. This would likely ignite safe-haven demand for Treasuries, support longer-duration assets, and shift market sentiment toward a quicker Fed pivot, with upside potential for utilities, staples, and dividend-paying stocks that typically outperform in late-cycle environments.

USA ISM Manufacturing PMI & ISM Manufacturing Prices

The ISM Manufacturing data will offer a critical update on the health of the U.S. industrial base.

- A higher-than-forecast PMI reading would imply expanding factory activity, supporting the view that supply chains and business spending are stabilizing. This could fuel a relief rally in industrials, logistics, and raw materials stocks. However, the spotlight may fall even more sharply on the ISM Manufacturing Prices Index—a surprise increase there would signal that input cost inflation is re-emerging, potentially complicating the Fed’s dovish shift. Markets may respond with bear steepening in the yield curve, downward pressure on tech and growth stocks, and renewed volatility in rate-sensitive sectors.

- On the other hand, a cooler-than-expected PMI or Prices print would reinforce economic slowing and disinflation themes, driving bond yields lower and supporting a Fed-friendly environment that favors duration and growth.

Stock Market Performance

Indexes Bounce Back from April Bottoms, But Breadth Remains Weak

We observe at Zaye Capital Markets that U.S. stocks keep recording stellar headline advances off their April 8 lows but that data below the line demonstrates a market that struggles with uneven breadth and significant pullbacks. Year-to-date performances turn out to be positive across all of the four main indices but average member pullbacks indicate that below the index level, dispersion and volatility prove to be stalwarts.

These are our observations of the recent trend on key indexes with the latest data:

S&P 500: Solid Rebound, Limited Leadership

YTD: +13% | +34% off April 8th low | -19% from YTD high | Avg. member: -14% from April low / -25% from YTD high

The S&P 500 headline numbers are holding up well with a 13% YTD gain and a 34% rebound off of the April low. The 19% correction off of its all-time high and average member declines of 14% off of April (and 25% off of the YTD highs) demonstrate the rally to be heavy on large-cap leaders and light across broader markets.

NASDAQ: Tech Strength with Deep Underlying Losses

YTD: +17% | +48% off April 8th low | -24% from YTD high | Avg. member: -33% from April low / -48% from YTD high

The NASDAQ leads at the index level, higher by 17% this year and by a whopping 48% off the April low. But the sharp 24% correction off YTD highs and harsh average member draws—33% off the April low and 48% off the top—highlight how precarious the rally is below the mega-cap tech leaders.

Russell 2000: Small-Caps Lag Despite Rebound

YTD: +9% | +38% off April 8th low | -24% from YTD high | Avg. member: -23% from April low / -38% from YTD high The Russell 2000 rebounded 38% off April lows and is up 9% YTD, but small-cap strength remains impaired by poor liquidity and economic sensitivity. Declines of 24% off YTD highs and abysmal member drawdowns signify continuing doubts about a sustainable small-cap rebound.

Dow Jones: Defensive Tilt Gives Shelter

YTD: +9% | +23% off April 8th low | -16% from YTD high | Avg. member: -12% from April low / -23% from YTD high The Dow Jones is continuing to benefit from its defensive composition, registering a 9% YTD gain and a 23% rebound off of the April low. Perhaps with a less significant 16% correction to its high and average constituent losses of 12% from Apr and 23% off highs, the index is taking on more stability compared to its growth-oriented counterparts—but not entirely free of underlying stress.

We’re valuation-driven and selective here at Zaye Capital Markets and favor quality balance sheets and proven income streams. We’re closely observing breadth indicators to get confirmation of whether this rally can widen to a sustainable gain in the market.

Strongest Sector in All These Indices

Communications Services Assumes Leadership of 2025 Growth with Room to Spare

Up to September 29, 2025, Communication Services is the best sector performer of the S&P 500 both on a month- and year-to-date basis, establishing itself as the strongest overall sector. Here, we at Zaye Capital Markets see that as a very strong indicator of sector leadership based on resilient earnings, rebounding digital advertising, and media platform monetization strategies continuing to surprise to the upside.

YTD Performance: +24.3%

Communication Services has surged 24.3% year-to-date, well ahead of all other sectors, including Information Technology (+20.7%) and Industrials (+16.1%). This outsized gain reflects sustained demand for digital content, streaming platforms, AI-driven services, and a recovery in global advertising budgets.

MTD Performance: +6.0%

The month to date best performer is Communication Services by a gain of 6.0%, outperforming Information Technology (+6.3%) by breadth and depth of relative strength among its holdings. The rally gains traction with healthy capital flows into megacap media and interactive entertainment stocks that continue to show healthy revenue growth and expanding margins. We remain attentive to valuation spreads, momentum off of second-quarter’s strong earnings and subscriber growth metrics within the Communication Services space. Given the sector’s ability to provide both strength and relative stability, Communication Services represents a key overweight within our short-term equity positioning facing into Q4 2025.

Earnings

Earnings Recap — 30 September 2025

NIKE, Inc. (NKE)

NIKE surprised to the upside, reporting $0.49 EPS, significantly above consensus expectations (≈ $0.27). Revenue rose ~1% to $11.7B, driven by a wholesale rebound (≈ +7%) that offset a ~4% decline in Nike Direct (driven by a ~12% drop in digital). Tariff pressures—especially out of Vietnam—were highlighted, with the company now anticipating ~$1.5B in tariff-related cost headwinds. Inventory reduction efforts and better-than-feared margin compression also drew attention. The market reacted favorably, but management’s tone remained measured, reminding investors the turnaround is uneven and many geographies remain weak.

Paychex, Inc. (PAYX)

For Paychex, expectations were around $1.20–$1.21 EPS, with revenue growth ~16–17% YoY in services and management solutions segments. Key metrics to watch include client retention, fee revenue growth, and payroll processing volume as indicators of ongoing demand and pricing power. Investors are also attentive to guidance revisions given the macro backdrop of moderating employment growth.

Lamb Weston Holdings, Inc. (LW)

Lamb Weston was expected to report $0.54 EPS (↓ ≈ 26% YoY) with revenue pressures in its food‑ingredients business. Analysts are focused on commodity input costs, margin resilience, and guidance on agriculture cycles, especially as frozen potato and food-service demand normalizes post‑pandemic levels. Margin commentary is particularly critical as input prices remain volatile.

United Natural Foods, Inc. (UNFI)

UNFI was forecast to post a loss (≈ –$0.18 to –$0.22 EPS) on ~ $7.6B in revenues. For UNFI, key metrics include gross margin trends, supply chain efficiency, and working capital moves. With its scale in natural and organic distribution, the company’s commentary on consumer spending habits and inventory adjustments will be vital for gauging demand trends.

Earnings to Watch — 1 October 2025

- RPM International Inc. (RPM)

RPM is expected to post EPS of around $1.88. Important items for investors include margin trends in its coatings and specialty chemicals segments, raw materials inflation, and any forward guidance changes for industrial end markets, as these metrics will help assess the company’s resilience to input cost pressures.

- Acuity Inc. (AYI)

Acuity is projected to deliver EPS of approximately $4.79. Key metrics to monitor include order backlogs, commercial lighting demand, and export demand exposure, which serve as leading indicators of revenue stability in an environment of shifting capital spending.

- Conagra Brands, Inc. (CAG)

Conagra Brands is expected to report EPS of around $0.33. Watch for margins under cost pressures, input cost pass-through, and consumer demand resilience in its food segment. Pricing power and private-label competition are two areas that could drive investor reaction post-earnings.

- Cal‑Maine Foods, Inc. (CALM)

Cal‑Maine Foods is forecast to post EPS of about $4.61. Key variables include egg supply/demand dynamics, feed cost inflation, seasonal cycles, and any inventory adjustments. With food inflation moderating, commentary on pricing discipline and market share gains will be closely scrutinized.

At Zaye Capital Markets, we will be dissecting margins, segment breakdowns, and management tone for signals about sector demand trends and resilience amid macro pressures as these results and outlooks roll in.

Stock Market Overview – Wednesday, October 1, 2025

U.S. equity markets began the new quarter with a measured tone, as investor sentiment continues to hover in wait-and-see mode amid political and macroeconomic crosscurrents. The ongoing threat of a federal government shutdown is injecting fresh uncertainty, particularly around the timeliness of critical economic data releases. While the S&P 500 and Nasdaq are struggling to regain leadership due to continued pressure on mega-cap tech, the Dow Jones and Russell 2000 are showing relative stability, bolstered by rotation into value, defensives, and yield-sensitive sectors.

Stock Prices

Economic Indicators and Geopolitical Developments

The market’s cautious positioning is driven in part by concerns that the failure to pass a U.S. funding bill could disrupt upcoming data releases, including labor market reports and inflation metrics—key inputs for both the Federal Reserve and institutional positioning. The lack of fiscal resolution raises the risk of reduced government operations, delaying not just data, but also procurement decisions and federal spending guidance. In parallel, investor attention is fixed on Fed speak and global trade updates, particularly surrounding U.S.–China tensions, which have re-entered the narrative as manufacturing prints and logistics flow soften. The combination of delayed visibility and fiscal noise is creating conditions ripe for risk-off rotation, with increased flows into bonds and gold noted across trading desks.

Latest Stock News

- $NKE | Nike surged after posting better-than-expected earnings and margins, even as digital and direct channels softened. Investors welcomed its inventory reduction and controlled expense strategy, sending shares modestly higher on volume.

- $META | Meta shares remain under pressure as the company faces continued scrutiny over content monetization, coupled with signs of ad spend normalization.

- $TSLA | Tesla was among the session’s underperformers, with shares declining amid reports of margin compression in overseas markets and broader skepticism on near-term EV demand.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—remain central to market structure but continue to exhibit signs of valuation fatigue. With sector-wide pullbacks averaging over 18% from recent highs, this group has weighed heavily on both the Nasdaq and S&P 500. Meta and Tesla in particular have suffered from investor rotation out of AI and high-multiple names. The result: a narrow market advance that lacks broad participation. Without renewed strength from these top-weighted names, index-level resilience remains fragile, and attention has shifted toward sectors like energy, financials, and industrials as sources of relative strength.

Major Index Performance as of Wednesday, 1st of Oct., 2025

- S&P 500: Trading at 6,688.44, up 0.41% on the day.

- Nasdaq Composite: Currently at 22,660.01, up 0.30%, with modest gains despite tech headwinds.

- Dow Jones Industrial Average: Up 0.18% to 46,397.83, lifted by strength in financials and industrials.

- Russell 2000: Last trading flat near 2,432, showing signs of stabilization as small caps digest recent moves.

At Zaye Capital Markets, we maintain that this remains a “risk-aware but rotation-friendly” market. While mega-cap weakness poses a headwind for headline indices, under-the-surface rotation into quality, income-generating sectors is gaining traction. Until macro clarity improves—particularly around fiscal policy and data continuity—we expect continued chop and selective opportunity rather than index-wide upside.

Gold Price

Gold is currently trading at $3,778.53 per ounce, continuing its upward momentum as a wave of political, economic, and policy-driven uncertainty boosts demand for safe-haven assets. The latest surge is strongly influenced by a combination of aggressive political rhetoric and anticipated disruptions in economic data flow. President Trump’s remarks—ranging from threats of mass federal worker layoffs, tariffs on pharmaceutical companies, and military action against cartels in Venezuela, to negotiation standoffs with Hamas and calls for wartime readiness—have injected a notable risk premium into global markets. These comments paint a picture of potential domestic policy instability and rising geopolitical tension, both of which are historically bullish for gold. Furthermore, Trump’s deal with Pfizer to slash drug prices by as much as 100%, and the announcement of a new government-backed drug pricing platform (TrumpRx), introduce major policy shifts that could weigh on equity sentiment and encourage portfolio hedging. With threats to global stability, rising defense rhetoric, and increasing fiscal strain, investors are reallocating into gold as a buffer against both market dislocation and real yield erosion.

Compounding these political catalysts is today’s dense schedule of key economic data: the EUR Core CPI Flash, CPI Flash Estimate, U.S. ADP Non-Farm Employment, ISM Manufacturing PMI, and Manufacturing Prices Index. These releases will offer insight into inflation persistence and labor strength—two critical levers for monetary policy direction. A hotter-than-expected inflation print or stronger jobs data could briefly weigh on gold via higher yields, but would likely be offset by growing expectations for Fed caution given tightening credit conditions and policy fatigue. Meanwhile, yesterday’s JOLTS data revealed stubbornly high job openings but a declining quits rate, hinting at worker hesitation and wage disinflation—factors that further increase the likelihood of a dovish Fed tilt. In the broader context of possible shutdown-driven data blackouts, reduced institutional clarity, and Trump-fueled policy volatility, gold remains on solid footing as a hedge against both systemic risk and deteriorating visibility. The market’s tone suggests that unless political and economic clarity is swiftly restored, gold may continue to attract inflows throughout October.

Oil Prices

Oil is currently trading at $62.70 per barrel (WTI), stabilizing after a volatile stretch driven by conflicting supply and demand signals. Price action remains under pressure following news that OPEC+ will proceed with a measured production increase in October, with discussions reportedly underway for another output hike in November. This proactive stance from OPEC, aimed at managing global energy prices as inflation pressures subside, has dampened near-term bullish sentiment in the market. However, the downside is being cushioned by U.S. crude inventory drawdowns—with stockpiles falling by 3.67 million barrels last week—and Russia’s ongoing fuel export restrictions, which are tightening product availability in global markets. Additionally, geopolitical flashpoints—particularly renewed instability in Venezuela and broader Middle East uncertainties—continue to factor into the risk premium, even if not immediately reflected in prices. Traders remain cautious as the market balances fears of oversupply with physical tightness in refined products and logistical constraints in global energy trade.

President Trump’s recent comments have added another layer of volatility, especially his hardline stance on tariffing pharmaceutical and foreign goods, calls for military escalation, and direct intervention in Venezuela’s internal conflict, which signal a return to aggressive foreign and economic policy frameworks. This unpredictability adds to oil’s hedge appeal, as market participants begin pricing in policy-driven disruptions to global trade and energy security. Meanwhile, yesterday’s JOLTS data, which showed strong job openings but a declining quits rate, highlighted labor market fragility—fueling concerns over weakening fuel demand and growth. Looking ahead, today’s slate of economic data, including ADP Non-Farm Employment, ISM Manufacturing PMI, and Prices Paid, will play a pivotal role. Strong prints could revive expectations for industrial activity and transportation fuel usage, putting upward pressure on oil. But if these releases disappoint, markets may interpret it as confirmation that demand is slipping beneath already elevated supply levels—creating potential for further price softening. At Zaye Capital Markets, we continue to monitor both policy noise and demand signals closely, as oil trades at the intersection of geopolitical tension and economic recalibration.

Bitcoin Prices

Bitcoin is currently trading near $114,421, recovering from earlier losses linked to rising U.S. political tensions and a looming government shutdown. This modest rebound comes as crypto markets absorb a wave of fresh institutional support—over $1 billion in inflows into crypto ETFs this week alone—indicating a resurgence of confidence from large asset managers and hedge funds. Market commentary highlights that Bitcoin has now entered its historically strongest quarter, with many analysts projecting upside targets between $160,000 and $200,000 by year-end, driven by both seasonal strength and macro tailwinds. Supporting this momentum is growing regulatory clarity: an SEC commissioner’s recent speech outlined steps to enhance crypto custody protections, reinforcing institutional frameworks and unlocking sidelined capital. At the same time, infrastructure developments such as clean-energy-powered mining deals in Brazil point to a strengthening of Bitcoin’s ecosystem from an operational perspective. Despite technical signals flashing caution—due to recent large liquidations around the September 26 options expiry—market resilience has surprised many, with BTC dominance climbing while other segments like AI/DeFi remain under pressure.

President Trump’s recent wave of comments—from promising mass layoffs of federal workers, threatening tariffs on pharma firms, to suggesting military action in Venezuela and Gaza—have injected renewed geopolitical anxiety into markets. Bitcoin, often touted as a hedge against systemic dysfunction and centralized policy volatility, is benefiting from that uncertainty. As traditional markets wobble under the weight of unpredictable fiscal rhetoric and declining institutional trust, digital assets offer an alternative narrative. Yesterday’s economic data (particularly the JOLTS report showing stubborn job openings but lower quits) added to the cautious tone, reinforcing the view that the labor market may be deteriorating below the surface. Today’s economic prints—ADP Non-Farm Employment, ISM Manufacturing PMI, and Prices Paid—are also crucial. A dovish surprise could further support Bitcoin by fueling liquidity expectations, while a hawkish beat may trigger short-term volatility but reinforce the asset’s hedge utility. At Zaye Capital Markets, we continue to see BTC’s ecosystem maturing in tandem with broader institutional re-engagement, setting a foundation for long-term revaluation in an era of policy uncertainty.

Eth Prices

Ethereum (ETH) is currently trading at $4,153.98, retreating slightly from its recent highs as broader crypto markets consolidate following a week of macro and political uncertainty. Despite the mild dip, sentiment around ETH remains largely constructive, supported by a significant wave of institutional inflows. Over the past week, spot ETH ETFs brought in over $547 million, led by major players like Fidelity’s FETH and BlackRock’s ETHA, underscoring renewed interest from traditional finance in Ethereum-based exposure. This surge in ETF demand coincides with notable whale accumulation—wallets holding large ETH balances reportedly acquired over 431,000 ETH (~$1.73 billion) during the recent dip, suggesting long-term conviction at current price levels. These inflows are happening even as on-chain activity shows temporary weakness, with lower transaction volumes and declining gas fees, a common pattern during consolidation phases. Nonetheless, these structural inflows signal that key market participants are positioning ahead of potential Q4 momentum, especially as Ethereum’s roadmap toward scalability and institutional adoption continues to mature.

Meanwhile, the current macroeconomic and political backdrop is adding new layers to Ethereum’s pricing dynamics. Trump’s aggressive comments on federal layoffs, new tariffs, and military posturing have injected fresh geopolitical risk into markets, elevating crypto’s role as an alternative asset and hedge against centralized instability. ETH in particular may benefit from this narrative, especially as yesterday’s economic data (JOLTS showing high job openings but falling quits) reflects uncertainty in labor market momentum, reinforcing cautious investor behavior. Today’s high-impact data—ADP Non-Farm Employment, ISM Manufacturing PMI, and Prices Paid—could be pivotal. A hotter-than-expected reading could pressure crypto assets by supporting higher yields, while a soft set of prints may trigger renewed demand for ETH as a growth proxy. For now, ETH must break and hold above the $4,200–$4,275 resistance range to confirm upward momentum, and with institutional accumulation and whale activity picking up, Zaye Capital Markets views Ethereum as a key name to watch as macro and market narratives evolve into the final quarter of 2025.