Where Are Markets Today?

Through Thursday, Oct. 2, 2025, E.U. and U.S. stock futures show mixed messages as investors keep a sense of caution amid ongoing political unrest as well as impending releases of economic statistics. Dow Jones Industrial Average futures fall by 30 points, or 0.06%, as S&P 500 futures fall by 0.04%, with Nasdaq 100 futures unchanged. E.U. indices such as the DAX and FTSE also show small losses as investors across both sides of the Atlantic show a sense of caution. The mixed futures show uncertainty on the part of the market as investors digest the implications of the U.S. government shut-down as they monitor significant economic releases that could signal further softening of the economy.

One of the main factors responsible for this tentative market mood is the ongoing U.S. government shutdown that started following a breakdown in a spending agreement between Congress members. Even though Fitch Ratings has confirmed that the shutdown will not have a direct effect on the U.S. sovereign credit rating this time around, doubts over how long the shutdown will continue keep investors on edge. Indications are that the shutdown will continue for up to almost two weeks, further contributing to the panic in the market. The political impasse has held up some major economic indicators such as the impending employment report and created an air of uncertainty that is taking a toll on both the European and American markets. Alongside the shutdown, economic statistics are also serving as determinants for the market sentiment. The market has been waiting for the release of U.S. unemployment claims data that will provide some insight into the condition of the job market. In the event that claims rise more than anticipated, this will provide an indication that the economy might be weak and could then lead to lower spending by consumers as well as slower growth rates. This will potentially reinforce fears that the shutdown could undermine the soundness of the economy further. Conversely, a lower than projected number for unemployment claims will prove some comfort however this can potentially do no more than mitigate the overall fears that surround the event of a shutdown as well as its implications on the economy.

Overall mixed action in both U.S. and European futures can be attributed to a mix of political tension around the U.S. government shutdown as well as expectations around the release of economic data. Investors closely monitor the situation that is developing in Washington since the duration as well as effects of the shutdown will establish the trend in the near term for the market. In addition to the coming report on unemployment claims as well as ongoing fiscal policy concerns, sentiment on the market thus remains guarded with volatility anticipated as these trends evolve.

Key Index Performance up until Thursday, October 2, 2025

- S&P 500: Trading at 6,711.20, up 0.3% on the day.

- Nasdaq Composite: Up 0.4% to 22,755.16 amid accelerating gains on tech stocks.

- Dow Jones Industrial Average: Up 0.1% to 46,441.10 on advances in financials and industrials.

- Russell 2000: Up 0.2% to 2,442.35, exhibiting moderate outperformance as small.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—remain weak this week in response to the wider change in market sentiment. Significant reopening in shares such as Tesla and Meta saw investors rebalancing their portfolios as they divest overvalued tech shares in favour of more defensive positions. Feeling the sting of this reversal are the tech-dominated Nasdaq and S&P 500 as sectoral pullbacks continue to stall overall progress.

Drivers Behind the Market Move – Thursday, October 2, 2025

Today, U.S. and European markets exhibit mixed behavior due to a cross-section of political news, releases that contain economic data, as well as sentiment by investors. The primary movers for market behavior are as follows:

1. U.S. Government Shutdown and Political Instability

The current U.S. government shutdown that occurred after Congress could not agree on a spending bill continues to worry investors. Although Fitch Ratings indicated that the shutdown has no near-term implications on the U.S. sovereign rating, the lack of clarity on its sustainability is perturbing investors. Prediction markets indicate that the shutdown may persist close to two weeks, further fueling the concern across the markets. Political stalemate has held up important economic releases such as the next week’s job report as well as created a sense of instability that is being reflected in both the European and the U.S. markets.

2. Economic Data Releases and Market Expectations

Economic releases are greatly contributing towards shaping market expectations. Investors eagerly wait for the release of U.S. unemployment claims data soon. A larger than anticipated number of such claims may indicate softening of the labour market that could lead to diminished consumer spending as well as slower economic growth. A lower than anticipated number of such claims might temper some fears but could do little in clearing up doubts created by the government shut down. In a similar manner, European markets are reacting towards economic indicators where investors heed the releases of such data for clues on the strength or weakness of the economy.

3. Geopolitical Tensions and Market Volatility

Geopolitical tensions also create market volatility. President Trump’s recent Executive Order on Qatar, where he declared a recent attack on Qatar a direct national security threat on the U.S., raised further concerns over international relationships and possible conflict. This political discourse on global tension could create volatility in markets, particularly in energy segments such as oil and gas that underpin the geopolitical market structure. Since the United States is a significant participant in the energy marketplace, any perturbation or change in United States foreign policy may provide direction on market movements, particularly in prices for crude oil as well as natural gas, as fears over supply disruption in the Middle East grow.

Overall, mixed action in U.S. as well as in European futures is being fueled by a mix of political apprehension over the U.S. government shutdown, impending releases of economics statistics, as well as geopolitical uncertainty. Investors are taking close notice as these could prove major determinants of market direction in the near future.

Digesting Economic Data

The TRUMP Tweets and Its Implications

In recent remarks, President Trump made important statements that could have far-ranging effects on the U.S. economy as a whole as well as on foreign markets. One such important statement was that on his Executive Order on Qatar where he declared an attack on Qatar recently a direct threat against U.S. national security. This escalated rhetoric on international tension could inject uncertainty in the market, perhaps more so in energy segments such as oil and gas that are central to the geopolitical scenario. Being a significant player in the energy market, any kind of disruption or change in U.S. foreign policy may cause market reaction, more so on the price of crude oil as well as natural gas due to supply disruption fears in the oil-dominated Middle East region.

Trump’s statements regarding drug pricing stand out as well, particularly as they continue to fuel the discourse around U.S. healthcare policy. He made known that the U.S. will pay the lowest prices for drugs, taking an aggressive approach toward drug companies that will not agree with his pricing structure. That could have big implications for the drug industry, potentially reducing profit margins for large drug companies and changing marketplace trends within health-care shares. He also threatened that if drug companies will not make a deal, the U.S. will put tariffs of 5-8% on these corporations. Those types of statements could raise an eyebrow among investors in health-care and drug-related fields since tariff action usually means more regulatory uncertainty that can impact corporate earnings as well as stock prices. Adding to market volatility was a commentary by Trump on the recent U.S. government shut down. Even as Fitch noted that the shut down will not cause near-term impacts on the U.S. sovereign credit outlook, a renewed emphasis by Trump on job cuts as he looks for a shrinking scope of government could further increase concern over U.S. fiscal policy. Continued market response could materialize due to concerns over slow downs in major economic releases such as the next jobs report, potentially running a domino effect across segments that rely on spending by the government as well as regulation. This, on top of aggressive commentary by Trump on drug prices as well as foreign trade, may further establish an air of uncertainty over the economy that affects sentiment as well as prices on assets across a number of segments.

The series of these tweets and actions create a scenario where tension in both home- and foreign-policy areas is on the rise. Although his approach on drug prices and tariffs might bring more volatility to the pharmaceutical space, the geopolitical risks tied to his statements towards Qatar as well as the U.S. shutdown might hamper overall market sentiment. Investors will have to approach these moving dynamics cautiously as they might bring shifts in appetite for risk, especially in areas that are most susceptible to regulator action as well as geopolitical movements. Amid the full-fledged U.S. shutdown, the uncertainty tied to the functioning of the government will continue to fuel short-term volatility across a range of markets, bringing further nuance towards the investment space.

Competing Indicators from Manufacturing Sector

The September 2025 ISM Manufacturing PMI edged up to 49.1 from August’s 48.7, slightly surpassing expectations, but still signaling contraction in the sector for the seventh consecutive month. Despite the slight improvement, the subindex for new orders dropped significantly to 48.9, reflecting ongoing demand weakness, while employment rose marginally to 45.3, offering some positive insight into labor conditions. The prices paid subindex also decreased to 61.9, indicating a reduction in inflationary pressures. These mixed signals highlight persistent challenges in manufacturing, with tariff pressures still a significant drag on the sector’s growth prospects.

With these numbers, the prospects of cyclical stocks remain pessimistic. Failure by the manufacturing sector to breach the 50 mark indicates persistent headwinds, particularly among companies that depend significantly on industrial demand. Stocks of industrially oriented companies like General Electric and Caterpillar might come under heavy strain with weaker demand and cost-driven issues. Analysts should keep close attention on these companies’ capacity to transfer increased costs to consumers, and this will define their future growth of their earnings.

The softening of inflation pressures, reflected by relaxation of prices paid, can provide Federal Reserve policymakers with latitude to fine-tune rate hike action against weaker economic momentum. Against the outlook of possible slowdown, the Fed’s message on rate easing or holds will be crucial to investor sentiment. Investors should keep a close eye during the upcoming fortnight on U.S. non-farm payrolls and any future guidance by the Federal Reserve that will further define the economic direction and possible sector rotations within equities.

Labor Market Evinces Softening as Private Payrolls Fall

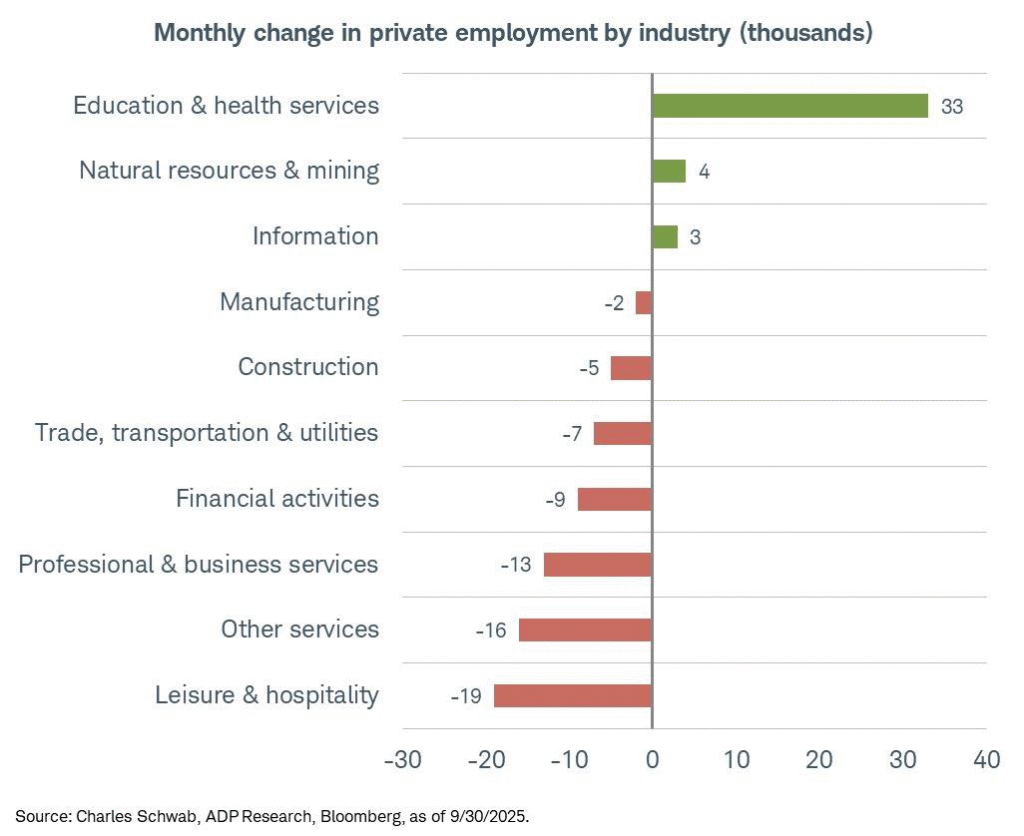

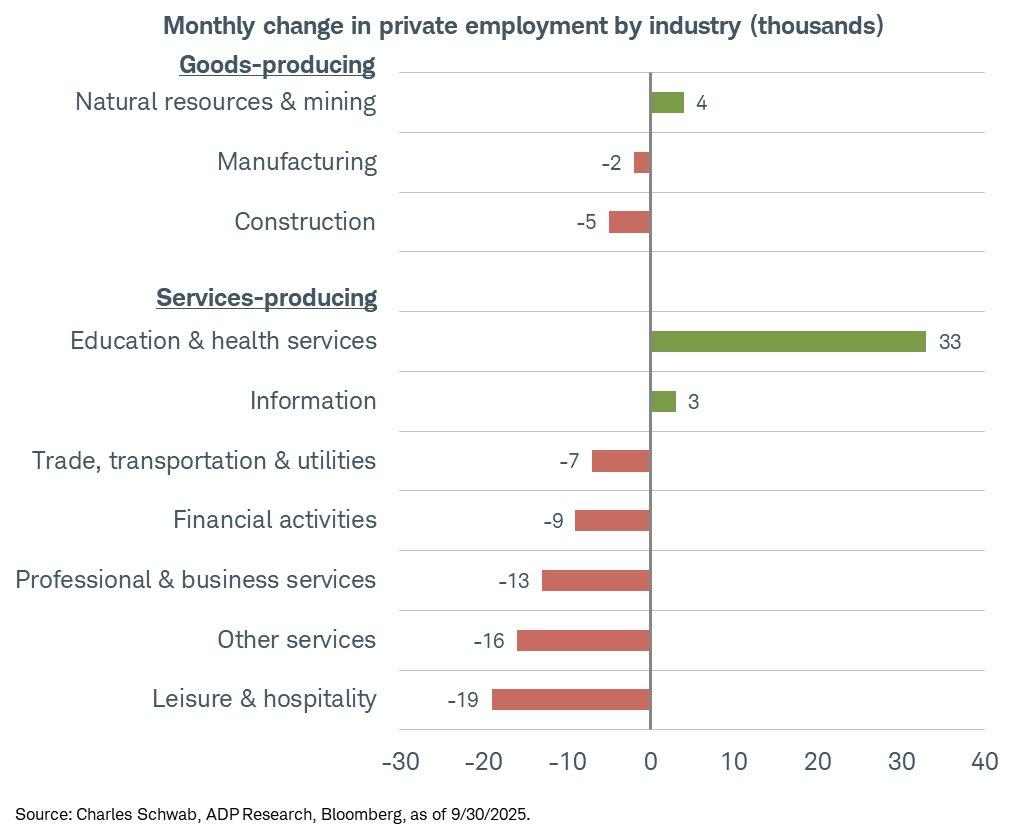

The ADP September 2025 report reveals a discouraging net private payroll loss of 32,000 jobs, a dramatic correction of August’s revised -3,000 (previously +54,000), a reflection of another softening of the labor market through ongoing economic uncertainty. Small businesses employing between 1-49 workers lost a massive 40,000 jobs, and mid-range businesses of 50-499 workers lost 20,000 jobs. Large businesses (500+ workers) gained 33,000 jobs, a reflection of the difficulty of small firms currently within the economic landscape.

Sector detail reveals gains were concentrated in education and health (+33,000), while losses were recorded in leisure/hospitality (-19,000), professional services (-13,000), and building (-5,000). The losses indicate setbacks in areas that are very economically and consumer-spending-cycle sensitive. The overall weakness of the labor market serves to underscore potential risks against the overall economy coming particularly out of industries that depend on discretionary consumption.

The Federal Reserve will likely consider this report while making future rate decisions. A weaker labor market, combined with a slowdown across key industries, might cause the Fed to reassess its hard-hitting tightening position. If these patterns continue, analysts will be eager to see possible policy shifts that can aid stability within the economy. Comparatively, relative to BLS payroll data, the difference between ADP’s losses and BLS’s gains of jobs within previous months might indicate divergence within underlying job formation patterns, necessitating further investigation within future reports.

Sector Vulnerability and the Lost Jobs of September

The September 2025 ADP report shows a net loss of 32,000 private sector jobs, the first net loss since March of 2023. The losses were across the board and were largest in leisure and hospitality (-19,000) and professional/business services (-13,000), a reflection of the ongoing economic pressures. The only sector to show large gains was education and health services, adding 33,000 jobs. Manufacturing and construction took losses too, down 2,000 and 5,000 respectively, partially driven by fears of upcoming tariffs and general economic uncertainty. This information indicates vulnerability of globally and dispositionally sensitive sectors.

An important note of the report is that large companies (500+ workers) increased jobs, while small companies (1-499 workers) made significant job losses. The trend of this dynamic is that smaller companies remain challenged economically. Wage growth came in flat at 4.5% year-over-year, but with net job losses, this could potentially be a theme shift within the labor sector that wage pressures will now ease, particularly should broader economic softness persist. The data release occurs against the background of increased concern regarding the impending U.S. government shutdown that can hold up other important economic data, including this month’s Bureau of Labor Statistics (BLS) nonfarm payrolls. The extension of the shutdown will rattle markets further, with data disruption having effects on investor sentiment and Fed policy direction. Comparing ADP’s report and BLS data, analysts should keep into perspective the difference between the trend of job formation, with BLS data recording better data over past months. The difference emphasizes the importance of keenly following the two reports to establish the actual conditions of the labor market.

Consumer Confidence Declines Under Inflation Projections

The Conference Board’s September 2025 Consumer Confidence Index shows a positive shift in consumers’ inflation outlook, with their 12-month inflation expectations decreasing to 5.8% from 6.1% in August. This decline could indicate that price pressures are easing, a potential sign that inflationary forces may be moderating. Despite this improvement in inflation expectations, the overall Consumer Confidence Index dropped to 94.5, its lowest level since April, suggesting that consumer sentiment remains fragile. Concerns about job availability and business conditions have overshadowed the decline in inflation expectations, raising doubts about future spending capacity.

The mixed consumer sentiment, with optimism about inflation easing but overall sentiment decreasing, may itself suggest that while consumers perceive inflation to be coming down, other issues within the economy—such as increased unemployment or slow-downs within the economy—cause their outlook to remain pessimistic. That could trigger a pull-back of discretionary consumption and have an impact on segments that rely correspondingly more heavily on consumer consumption, such as retails and leisure.

Inflation forecasts, though still considerably higher than the Federal Reserve’s 2% target, seem to be moderating, but remain stubborn compared to pre-pandemic standards. Analysts should not only keep close attention on these stubborn perceptions of inflation but how they affect consumer patterns and, by extension, the overall economic rebound. The Fed’s ongoing journey of rate increases will be made potentially problematic by the mixture of a tightening labor market and dampened consumer sentiment.

Schedule of Layoffs and Hiring by US Remains Healthy Despite Weaker Demand

The August 2025 U.S. JOLTS reported that layoffs fell to 1.7 million after being adjusted to 1.8 million in July and stayed near historically low levels ever since the measurement began in the year 2000. The Bureau of Labor Statistics data reveals the stability of the labor market with the layoff rate staying firm at 1.1%. Despite that, job vacancies stayed flat at 7.2 million, showing an ongoing labor demand and supply discrepancy, but with some clues of softening activity of hiring with a 3.2% hiring rate.

The data points to a healthy labor market, with personnel primarily retaining their positions amid continuing economic turbulence. However, the stagnating job vacancies and decreasing recruitment figures seem to indicate that labor demand could be softening. That aligns with the Federal Reserve’s aims of bringing about a soft landing of the economy, but runs contrary to sector-focused reports of redundancies, particularly by those industries hard hit by higher costs or negative economic turns. The analysts will be closely monitoring ongoing shifts within recruitment patterns and vacancies to determine the general direction of the economy and the success of the Fed to stabilize.

Even while the JOLTS report hints at relatively low dismissals, the hiring and vacancies freeze could be a harbinger of structural vulnerabilities in the labor market, specifically if softening demand persists. The dynamics will have implications within the Fed’s rate settings, with markets assuming that any suggestions of labor market downturn could trigger tighter monetary policy down the line.

Softening Labor Market Bodes Badly for Economic Growth

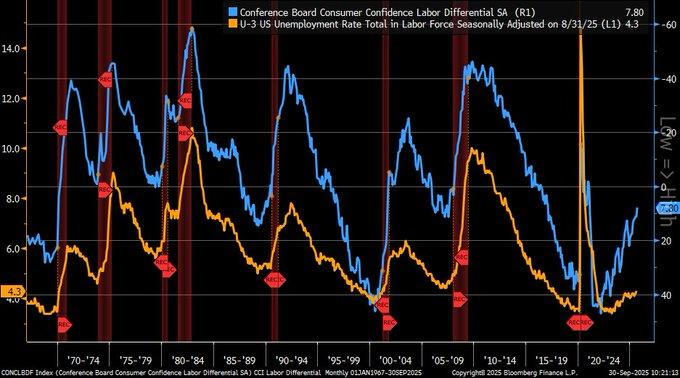

The Conference Board’s September 2025 Labor Differential took a sharp drop to 7.8 from August’s reading of 11.1, a reflection of a shift in sentiment about the labor markets. Calculated by subtracting the percentage of individuals that report jobs to be hard to get (19.1%) from those reporting that jobs are plentiful (26.9%), this indicator points to a softening labor market. The softening of the job availability typically revealed by the differential reversing (which, now, it has) tends to foreshadow unemployment gains by 3-6 months, a pattern evident before gains in joblessness spikes of 2001, of 2008, and of 2020.

This decline within the Labor Differential fits with overall economic anxiety, with the Consumer Confidence Index of the Conference Board slipping to 94.2, its lowest reading since April of 2025. The pessimistic consumer outlook is a reflection of growing concern about unemployment and general economic health. If October’s jobs report reveals an surge in unemployment rates to above 4.2%, the Fed will increasingly be compelled to make a shift to its monetary policy and possibly trigger rate reductions to aid economic stability.

With the Labor Differential and consumer sentiment turning south, slowdown risks increasingly emerge. That could make the Fed cautious, considering that softening of labor conditions can set off another batch of monetary policy tweaks. The jobless claims and the subsequent jobs report will need to be keenly followed by analysts, as they will ultimately dictate the degree of shifts and will be instrumental to future Fed actions.

Texas Services Sector Outlook Highlights Resilient Capital Expenditures

The Dallas Fed’s Texas Services Sector Outlook Survey for September 2025 shows an important shift in capital expenditure (capex) projections, with the index reaching 20.5—its highest mark since May. This returns the index to expansionary territory after falling close to zero earlier this year and indicates optimism among companies about future investment. Although overall, the business activity index of this survey falls to -5.6 to mark contraction with higher economic uncertainty, this improvement of capex is of significance. Approximately 29% of companies project higher capital spending over the next six months, while only 8% project reductions. This gap between capex trends and general business activity hints at a bright spot of the Texas economy despite general softening of conditions within the services sector.

The rise in capex is of specific concern to analysts that specialize in cyclical sector stocks. The data reveals that expansion and capital expenditures on infrastructure persist center stage with numerous companies despite general economic woes, and that technology and consumer service stocks have witnessed the highest increase in capex. The trend might be good news to companies within these industries, which might benefit from continued capital outlays and then fortify their equity outlooks across the near term.

Comparing regional capex patterns across the United States, we note that Texas is outpacing many regions while companies across other regions are more cyclical with their capex outlooks. Such regional variance highlights the relevance of monitoring sector and capex investment patterns as potential keys to future economic results. Under conditions of ongoing economic uncertainty, capex resilience within Texas could hold valuable insights to broader economic conditions, particularly within technology and consumer-based industries.

Upcoming Economic Events

Unemployment Claims

Enter another significant week of economic data, and investor attention will be solely on jobs data and manufacturing activity, key indicators that will determine markets direction. Key among keenly followed reports will be weekly unemployment claims data that gives a contemporaneous picture of the labor market. A close examination of this report and its impact on markets follows:

Unemployment Claims

- Claims unemployment remains one of the most timely and effective data points to assess labor market health. If actual claims come in below expectations, that will confirm continuing strength within the job market, supporting optimism about consumer spending and economic fortitude. That might strengthen sentiment within risk-on assets, notably cyclical stocks, and might induce the U.S. dollar to firm as investors bet on further economic stability. But below-expectation claims might crucially spark fears of enduring inflationary pressures, nudging the Federal Reserve to a firmer stance on higher interest rates.

- Conversely, stronger-than-anticipated claims would indicate a cooler labor market, which might temper consumer sentiment and foment fears about economic growth. Such a miss might induce risk-off sentiment, and bond and defensive stocks (e.g., consumer staples, utilities) might attract investors. A stronger-than-projected reading might boost speculation that the Fed will ease its tightening spree to boost the economy, putting bond yields and equities down.

Monitor over the course of the week how this data intersects with other manufacturing and inflation reports, and the interplay of this with these other pieces will significantly determine the Fed’s next move.

Earnings

Earnings Recap: October 1, 2025

- RPM International Inc. (NYSE: RPM)

RPM International reported a record first-quarter revenue of $2.11 billion, surpassing estimates of $2.06 billion, and adjusted earnings per share (EPS) of $1.88, meeting expectations. Despite these strong results, the stock declined by 3% in pre-market trading, reflecting broader market concerns. The company’s solid revenue growth was driven by strong demand for its coatings and sealants products, but the market’s response highlights concerns over the broader economic environment, particularly regarding inflationary pressures and ongoing cost challenges.

- Acuity Brands Inc. (NYSE: AYI)

Acuity Brands achieved a 17% year-over-year increase in net sales, reaching $1.21 billion. However, the company reported a diluted EPS of $3.61, a 4.2% decrease compared to the prior year. The sales increase reflected strong demand for lighting and controls, but the decline in earnings was due to higher raw material costs and logistics challenges. Investors will be closely monitoring how the company plans to manage these cost pressures going forward and whether it can sustain growth in its core markets.

- Conagra Brands Inc. (NYSE: CAG)

Conagra Brands reported first-quarter revenue of $2.63 billion, slightly above the estimated $2.62 billion, driven by strong demand for pantry staples like Slim Jim and Act II popcorn. Adjusted EPS was $0.39, beating expectations of $0.33. The company’s ability to outperform expectations was attributed to continued strength in its consumer brands, despite the broader economic uncertainty. However, investors will be keen to see if Conagra can maintain this momentum amid potential headwinds from rising inflation and changing consumer behavior.

- Cal-Maine Foods Inc. (NASDAQ: CALM)

Cal-Maine Foods reported its strongest first-quarter revenue in company history at $922.6 million, up 17.4% year-over-year. However, net income was $199.3 million, and EPS was $4.12, missing analyst expectations of $5.01. The company benefited from strong demand for eggs, but increased costs and supply chain disruptions dampened profitability. Despite the record revenue, the market reacted cautiously to the earnings miss, as investors remain focused on the company’s ability to manage costs and sustain profitability in a challenging environment.

Upcoming Earnings: October 2, 2025

- VinFast Auto Ltd. (NASDAQ: VFS)

VinFast is scheduled to report its third-quarter earnings today. The company is expected to report a loss per share of $0.25. Investors should focus on updates regarding EV deliveries and any developments in the company’s global expansion plans. As a newcomer to the electric vehicle market, VinFast’s ability to scale production and meet delivery targets will be key to its long-term success. Additionally, investors will be looking for commentary on the company’s plans to strengthen its position in the competitive EV market.

- AngioDynamics Inc. (NASDAQ: ANGO)

AngioDynamics is anticipated to report a loss per share of $0.13. Analysts expect a 7.8% increase in revenue to $72.73 million. The company has faced headwinds in its core medical device business, and investors will be focused on any updates regarding product development, particularly in the oncology and vascular sectors. Strategic initiatives to drive growth in these areas will be closely watched, as will the company’s ability to maintain margins in a highly competitive environment.

- Park Aerospace Corp. (NYSE: PKE)

Park Aerospace is scheduled to release its fourth-quarter and fiscal year earnings today. Investors should look for insights into the company’s performance in the aerospace sector, particularly with regards to defense contracts and any updates on its financial outlook. The company’s ability to navigate supply chain challenges and its positioning within the aerospace industry will be key factors in evaluating its long-term growth potential. Any guidance on future revenue growth or capital allocation plans will also be closely scrutinized by analysts.

- Lifecore Biomedical Inc. (NASDAQ: LFCR)

Lifecore Biomedical is expected to report a loss per share of $0.31. Analysts anticipate quarterly revenue of approximately $26.3 million. Lifecore’s focus on the biopharmaceutical sector, especially in contract manufacturing, is likely to be a focal point in today’s earnings call. Investors will be looking for updates on the company’s pipeline, regulatory approvals, and any new partnerships that could help drive future growth. The company’s ability to execute on its strategic initiatives will be crucial for maintaining investor confidence.

Stock Market Update – Thursday, October 2, 2025

The U.S. equities closed a strong session on Wednesday, October 1, 2025 as investors reacted to weak job growth as well as the partial shutdown of the U.S. government. Despite these challenges, big indexes kept their positive momentum due to gains by top tech shares as well as positive outlooks on earnings.

Stock Prices

Economic Indicators in Addition to Geopolitical

Sentiment was further driven by the softer than anticipated ADP payroll report that revealed a disappointing loss of 32,000 September jobs, bolstering hopes that the Federal Reserve will cut rates later this month. The partial government shut down, although a source of uncertainty, will ultimately prove to have a negligible long-term effect on the market, making investors more concerned with the overall economic statistics as well as earnings coming out this week.

Latest Stock News

- $EOSE: Just broken over $12 in a big breakout as the stock gains further momentum in its group. The upsurge is piquing the interest of traders seeking speculative bets.

- $NVDA: Nvidia’s market capitalization surpassed Amazon as well as Meta combined, a testament once again that it’s one of the tech sector’s greatest giants. It highlights the company’s continuous dominance over the realm of artificial intelligence as much as in the semiconductor domain.

- $TSLA: Tesla CEO Elon Musk just became the first-ever individual to reach a $500 billion wealth milestone. That’s a pretty big personal achievement for Musk as he oversees Tesla as its expands its leadership in the auto EV sector.

- $ASML: ASML reclaimed the $1,000 handle as investors continue to be positive on the company’s commanding leadership position in the manufacturing aspect of the semiconductor industry. ASML continues as a dominant player in the global supply chain for chips, aided by persistent strength in sales for its flagship leading edge lithography equipment.

- $INTC: Intel has been in initial talks to begin manufacturing chips for AMD in its own plants, according to reports. The prospective partnership can prove a sea change for the semiconductor business as a whole since Intel hopes to broaden its manufacturing base as well as diversify its customers.

- $GOOGL: Waymo, Alphabet’s autonomous drive unit, was granted renewed permission to operate in New York City until the end of the year, a testament to enduring governmental approval and momentum in the autonomous drive space.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—remain weak this week in response to the wider change in market sentiment. Significant reopenings in shares such as Tesla and Meta saw investors rebalancing their portfolios as they divest overvalued tech shares in favour of more defensive positions. Feeling the sting of this reversal are the tech-dominated Nasdaq and S&P 500 as sectoral pullbacks continue to stall overall progress.

Key Index Performance up until Thursday, October 2, 2025

- S&P 500: Trading at 6,711.20, up 0.3% on the day.

- Nasdaq Composite: Up 0.4% to 22,755.16 amid accelerating gains on tech stocks.

- Dow Jones Industrial Average: Up 0.1% to 46,441.10 on advances in financials and industrials.

- Russell 2000: Up 0.2% to 2,442.35, exhibiting moderate outperformance as small.

We still maintain that we are in a “risk-on but cautionary” phase. The strength of mega-caps in tech remains paramount for a prolonged rally on the upside. That being said, as valuations resync in the tech space, the better long-term stability can be found in less over-inflated areas, such as in industrials as well as energy.

Gold Price – Thursday, October 2, 2025

As of October 1, 2025, gold prices surged to new heights, reaching $3,866.10 per ounce and briefly touching $3,895.09 earlier in the day. This remarkable rally is primarily driven by a combination of factors, including heightened geopolitical tensions, notably following recent executive orders from President Trump regarding security and trade policies with Qatar, and the ongoing U.S. government shutdown. Investors are flocking to gold as a safe-haven asset amid concerns over potential delays in economic data, particularly the upcoming U.S. unemployment claims report. The market is also anticipating a potential rate cut from the Federal Reserve, as soft economic data continues to signal a slowdown. With the dollar weakening against other currencies, international buyers are increasingly turning to gold, boosting its demand further and supporting its price. Trump’s comments on drug pricing and tariffs on pharmaceutical companies are also contributing to the uncertainty, as any potential trade disruptions could exacerbate inflationary pressures, further underpinning gold’s role as a hedge. In the coming week, the release of the unemployment claims figures will be integral to determining market sentiment towards gold. A surprise increase in the number of claims will reinforce doubts over labour market softening that could raise the spectre of an economic slowdown, thereby increasing demand for gold as an inflation as well as an economic uncertainty hedge. A lower than anticipated number of claims could ease some immediate concerns over the economy, yet the integral safe-haven appeal that underpins gold will keep its price afloat. The overall environment for gold continues to be shaped by persistent geopolitical risk factors, lack of confidence in the economy, as well as the risk shift towards monetary policy that underpins the value of gold as investors find refuge in an uncertain global environment.

Oil Prices – Thursday, October 2, 2025

As of October 1, 2025, oil prices showed some fluctuations with Brent crude futures reaching $66.31 a barrel and U.S. West Texas Intermediate climbing to $62.63. The initial decline during the week was triggered by news that OPEC+ might increase its production by as much as 500,000 barrels a day in November as a bid by Saudi Arabia, in particular, to recover market share. OPEC later debunked this, relieving some downward pressure on prices. Despite prices stabilizing somewhat, fears over a global slow down in the economy continue to hang over the market, especially amid soft manufacturing figures coming out of leading oil-consuming areas such as Asia. U.S. oil stockpiles also provided mixed sentiment by reporting a decline of 3.67 million barrels in stockpiles of crude but coincidentally an increase in gasoline and a rise in inventories in the area of distillates. It means that although that demand for crude stands relatively solid, gasoline as well as refined product consumption is not as strong, further taking a hit on market expectations. The ongoing U.S. government shut down that has introduced a lot of uncertainty as well as postponed some important releases in the area of economic data also persists in impacting sentiment more so in the energy area. Oil’s price trajectory will heavily rely on a balance that these factors will reach over the next few days. The recent economic figures, particularly the U.S. labor market data, will likely dictate oil prices in the future. In case the unemployment claims report publishes a larger-than-anticipated number of jobless claims on Friday, then this might be an indicator that the U.S. economy happens to be weak; this could lower oil demand as well as exert downward pressure on prices. Alternatively, a lower-than-anticipated figure might temper some economic fears, providing a boost to oil prices. The executive orders by Trump as well as the recent conflict involving Qatar, coupled with his statements on tariffs as well as drug prices, might also indirectly influence oil prices in the future. Political risks as well as prospective supply interruptions might give rise to further oil market volatility, further increasing uncertainty. Furthermore, OPEC as well as the International Energy Agency will also continue playing a dominant role in shaping oil price direction as OPEC’s agreement on cuts in oil productions as well as the IEA’s outlook on oil demand across the entire planet will continue being central. The attention by traders on these bodies’ actions as well as prospective economic figures will be vital in dictating oil prices in the immediate future.

BITCOIN RATES SHOW POSITIVE BULLISH TRENDS DESPITE ECONOMIC INSTABILITY

As of October 1, 2025, Bitcoin (BTC) has been experiencing notable upward momentum, trading around $118,761 per coin, reflecting a 3.79% increase from the previous close. Throughout the day, the price fluctuated between $114,166 and $119,400, driven by several key factors. The primary catalysts for this rally include a weakening U.S. dollar, which typically boosts demand for alternative assets like Bitcoin, especially as a store of value in times of uncertainty.

The recent U.S. government shutdown also created fears over a stable economy, causing many investors to flock towards safe-haven securities further fueling the attractiveness of Bitcoin. The digital currency market has also been encouraged by favorable outlooks for the month of October with Bitcoin broadly set to keep its momentum as a result of wider investors’ positive outlook towards the digital currency space. Technical outlook projects that Bitcoin is on its way towards a significant resistance region around the price level of $120,000 with a symmetrical triangle developing on the daily chart. This portends the breakout event with a break above this level allowing for further appreciation in prices potentially reaching new highs in the immediate term. In the near term, the day’s economic statistics, more so the release of U.S. unemployment claims, will be instrumental in determining Bitcoin’s price action. In the event the report on claims prints larger than anticipated figures, the trend for a deteriorating economy will gain further impetus for investors to hedge against currency risk as well as inflation by taking positions in Bitcoin. This could create further bullish pressure on the digital currency, entrenching its status as a hedge asset. In the event that claims print lower than anticipated figures, reducing fears over the economy, the reaction on Bitcoin’s development could be far less pronounced.

In spite of these fluctuations, the very nature of Bitcoin as a decentralized, cross-border currency will continue to provide underpinning for solid demand, even in more settled macroeconomic conditions. Against a backdrop of continuing global geopolitical tension—the perpetual trade-security commentary by Donald Trump—the use of Bitcoin as a hedge against such risk becomes more clarified. With the alignment of the macroeconomic trends, Bitcoin’s positive technical configuration, and increasing institutional interest, the outlook for the digital currency over the coming few weeks retains a bullish tone.

At FP Markets, we keep a close eye on Bitcoin’s trajectory as increasingly it carves out a unique place as a core asset against a growing uncertain geopolitical and economic landscape.

ETH Prices – Thursday, October 2, 2025

As on October 1, 2025, Ethereum (ETH) trades around $4,385.57 after recording a minor gain of 0.0525% compared to the previous close. The day’s trading range has been between $4,127.10 and $4,386.17, a reflection of the prevailing market action triggered by macroeconomic factors as well as sentiment on the part of investors. Ethereum, like other digital currencies, records gains given a weakening U.S. dollar that usually makes digital currencies more appealing options as against traditional fiat currency alternatives. Ongoing uncertainty in terms of a U.S. government shutdown has served to further increase investors’ appetite for digital currencies such as Ethereum as an insurance policy against prospective currency devaluation as well as prospects of creeping inflation. A technical outlook on Ethereum reveals that it approaches an important resistance level around $4,400 with a symmetrical triangle developing on the day’s chart. Should the resistance level give way, then a further surge in bullish action on the part of Ethereum might be anticipated with a new set of day’s highs a prospective outcome in the immediate term. Aside from macroeconomic trends, news surrounding Ethereum’s market activity is dictating the price action. In recent times, big investors, or “whales,” have been buying up Ethereum as a sign of increasing sentiment toward the asset. Ethereum ETFs have also been gaining popularity as institutions seek exposure to Ethereum without direct holdings of the tokens themselves. The increase in whale activity and institutional interest points toward a continuation of the price action in an upward motion as more investors come on board. The decentralized nature of Ethereum as well as its central role in decentralized finance use cases as well as the execution of smart contracts continue to underpin its long-term value proposition. Ahead of the immediate horizon, the release of unemployment claims will help dictate the overall economic tone. A larger-than-expected claims print will bolster demand for Ethereum as a safe-haven asset, with a lower-than-expected print serving to stabilize sentiment on the broader market level. In any event, the strong technical as well as fundamental drivers underpinning Ethereum indicate a trend toward a bullish outlook on a near-term horizon.