Where Are Markets Today?

US and European stock futures are little changed today, as worldwide markets process a combination of defensive corporate news and political unease. Dow Jones Industrial Average futures are up just 7 points, or a meager 0.02%, as S&P 500 futures are up by just 0.04%, and Nasdaq 100 futures by 0.07%, as a lack of conviction ensues following the S&P 500 breaking a seven-day winning streak. The momentum break followed the release of a story that showed Oracle’s cloud business margins falling short of analysts’ expectations, and that the firm is losing money on certain Nvidia chip-rental contracts. The story spurred the shares of Oracle falling by 2.5%, shaking up broader sentiment among AI-biased names and causing fresh comparisons with the days of the dot-com bubble. In the European market, the futures are little changed to slightly positive, following Wall Street’s defensive note and as the mixed cues from China and softer eurozone inflation reads led the market across the continent.

The subdued open comes as the market reassesses the sustainability of the artificial intelligence boom. Weakness in the margin at Oracle is causing skepticism about how scalable and lucrative the current AI buildout is, particularly as the capital-intense infrastructure starts to squeeze the return. It has led to a broader-based sector-wide rethinking, as investors question valuations across the chip, the software, and the cloud-computing ecosystem. The parallel with the late 1990s internet bubble is gaining credibility, as market veterans are calling for portfolio rebalancing and increased discipline in allocation. But bulls contend that the fundamentals around data-center growth, AI model demand, and compute capacity remain solid—you’re just getting a potential reset, as opposed to a collapse. Another key overhang is the US government shutdown, which is into the second week with limited apparent progress toward resolution. Political standoff—described by President Trump as a kamikaze attack by the Democrats—has already delayed some key economic releases and risks blunting consumer sentiment, federal government spending, and operational clarity among contractors and public-sector-related industries. Market participants are presently implying the risk of a prolonged standoff, and analysts note that prolonged breakdown could spill into the debt ceiling negotiation as well as Q4 earnings sentiment. In European markets, risk from US policy uncertainty as well as US rate cues continues to be high, and any sign of breakdown on the European side of the Atlantic still impacts sentiment globally.

At Zaye Capital Markets, today’s market tone is seen as one of uncertainty versus reversal. The AI trade—although overstretched in certain corners—still warrants institutional inflows, and market breadth should pick up if macro signals solidify. Two near-term catalysts will, for the time being, dictate direction: the tone of the FOMC meeting minutes later today, as well as any shift in fiscal negotiations surrounding the shutdown. A dovish tone at the Fed could re-inspire risk appetite and counter AI fatigue, although a sustained political standoff could divert capital towards defensive equities and commodities. For the time being, futures indicate investors are holding back, not running back.

Major Index Performance as of Wednesday, 8th of Oct., 2025

- S&P 500: Trading at 6,710.42, down 0.4% on the day.

- Nasdaq Composite: Currently at 22,700.61, down 0.7%, as mega-cap tech continues to unwind.

- Dow Jones Industrial Average: Down 0.2% to 46,600.88, with modest strength in industrials offering support.

- Russell 2000: Down 1.1% at 2,430.17, underperforming as small caps face rate headwinds.

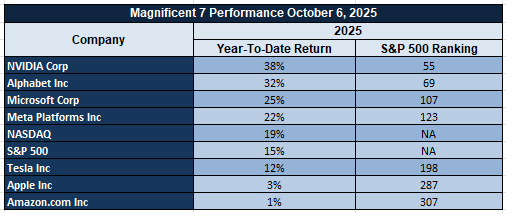

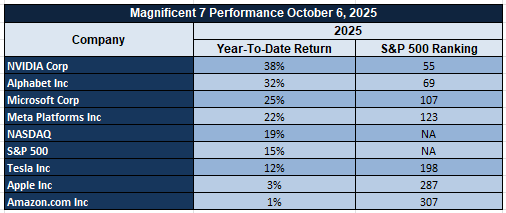

The Magnificent Seven and the S&P 500

The “Magnificent Seven”–Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla–are still under sellers this week. With sectoral drawdowns exceeding over 18% from recent tops, these stocks have become the biggest drag on major indexes. Tesla and Meta are experiencing steeper re-alignments as excitement around AI cools and valuations tighten. Absent renewed leadership from these megacaps, the S&P 500’s ability to maintain a sustained rally seems limited, causing investors to look towards diversification in energy, industrials, and select real assets.

Drivers Behind the Market Move – Wednesday, October 8, 2025

US and European markets open the day on mixed terms, as a trio of AI market adjustment, rising political tension, and forthcoming policy direction from the Federal Reserve combine to frame market sentiment. Although futures are little changed, beneath the surface increasing strain—especially in the technology and infrastructure spaces—is being fueled by precipitous responses to commentary on earnings, geopolitical statements from President Trump, and delayed economic data owing to the current US government shutdown.

- AI Margin Shock and Tech Sentiment Reset

The precipitous drop in Oracle—provoked by disclosures that its AI cloud unit is producing way weaker-than-anticipated margins—brought back into focus broader overvaluation concerns across the artificial intelligence space. The firm’s gross margin on AI-based services totaling just 14%, combined with unprofitable Nvidia chip lease arrangements, provoked a 2.5% drop in its shares and ended the S&P 500’s previous seven-day winning streak. This has had a trickle-down effect across high-multiple tech names as well as AI-associated infrastructure provision names, causing investors to question anew if the prevailing levels of valuation across the “AI trade” are properly supported. With comparisons being likened back to the late-90s dot-com boom, the Nasdaq —with a high concentration on tech stocks—now comes under added pressure to maintain forward momentum given profit deceleration fears.

- Government Shutdown and Political Divisions

The United States government shutdown—now past its second week—is further rattling investor sentiment. President Trump’s rising rhetoric, labeling the standoff as a “kamikaze attack from Democrats,” and warning that government programs would be targeted for “elimination” has further entrenched the impression of Washington paralysis. His remarks on the uncertainty surrounding backpay for furloughed workers, layoffs in days, and Democratic leader-lessness further the poisonous political atmosphere that is holding back critical data releases and damping fiscal policy clarity. Those factors are having a bearing on risk appetite, particularly among government contract-dependent sectors and consumer sentiment. European markets are also not immune, as policy-sensitive stocks are responsive to possible transatlantic economic spillovers.

- Next FOMC Minutes and Rate Policy Expectations

The release today of the FOMC Meeting Minutes is the next key market pivot point. Traders seek the clarification that the Fed will be dovish in response to slowing consumer credit growth and political uncertainty, or that inflation stickiness will continue to concern policymakers. Warnings from Fed officials such as Kashkari and Bostic indicate caution, reporting that we’re too early in the cycle on knowing if the tariffs and political deadlock will have lasting inflationary effects. A dovish tone would revive demand for rate-sensitive sectors and high-beta stocks, whereas a hawkish outlook could solidify the existing rotation into defensives and value. With the core inflation data still outstanding due to the shutdown, the market is flying half-blind—leaving the central bank language the clearest directional indicator on the table for the time being.

Overall, the market remains narrowly balanced between the tech-fundamental re-calibrations, policy risk on the basis of headlines, and the Fed’s short-term positioning. In our view at Zaye Capital Markets, the climate is one that requires selective exposure along with disciplined positioning, especially as sentiment swings between risk and opportunity with every new twist on the shores of the Atlantic.

Digesting Economic Data

The TRUMP Tweets and Their Implications

President Trump’s latest parade of statements, communicated through public addresses and social networks, yield significant insight into the dynamic changes in the American economic, geopolitical, and domestic policy landscape. At the very top of his list is the release of imminent trade negotiations with Canada’s Mark Carney, involving potential Canadian sectors liberalization on tariffs and deeper strategic convergence on the Golden Dome project. At the same time, he doubled down on protectionist rhetoric when he declared, “We’re the king of being screwed by tariffs,” and that Canada “will have tariffs.” This contradictory message—oscillating between reassuring gestures and protectionist leanings—injects uncertainty into bilateral economic interactions. For markets, such dual tones can make the price models for the North American industrials, material, and energy exports vulnerable, and engender volatility in FX and commodities relating to the sectors subject to tariffs.

Globally, Trump’s comments on the possibility of a Middle Eastern peace deal and his meeting with President Xi later this week in South Korea bring into play key geopolitical factors. Should a Middle Eastern diplomatic success occur, risk premiums could decline globally, reducing energy market stresses and shifting investor flows out of gold-based defensive sectors. On the other hand, the China meeting—following the shadow of revived Chinese tariff threats—can reopen hostilities or provide market-disruptive breakthroughs on the basis of tone and content. Follow-through will be key, and markets will be monitoring, particularly in trade-sensitive sectors like autos, heavy manufacturing, and semiconductors. Even the suggestion of strategic engagement on the part of the United States with both adversaries and allies speaks towards an intentional bid on the part of the United States towards re-establishment of American global leadership in regions in which uncertainty has recently prevailed.

Domestically, attention was directed toward the growing federal government shutdown that Trump characterized as a “kamikaze attack from Democrats” without any leader at the helm. His jobs-“eliminated in four or five days” statements, combined with open-ended comments on backpay to the furloughed workers, sent chill messages both to federal workers as well as market participants. An extended shutdown not just threatens key economic data and agency operations, also prolongs uncertainty over fiscal soundness, credit ratings, and consumer attitudes. Trump’s talk on removing programs and shutting off communication with Democratic leaders further diminishes the prospects for near-term resolution, casting a cloud on industries reliant on federal contracts or services—e.g., defense, infrastructures, and healthcare administration.

We would consider this week’s rhetoric as a high-volatility mix of strategic communication and political brinksmanship. Risks are high: investors must be prepared for trade policy reversals, shock risk from geopolitics, and domestic business disruption in the event the shutdown elongates or intensifies. While some of the President’s statements lean towards de-escalating and continuation of diplomatic efforts, others reflect increasing fraying across policy streams. In the near term, markets will likely remain reactive, prone to short-term moves directly correlated with the tone from the President as well as the actual achievement—or non-achievement—of the agendas hinted at in this latest salvo of rhetoric.

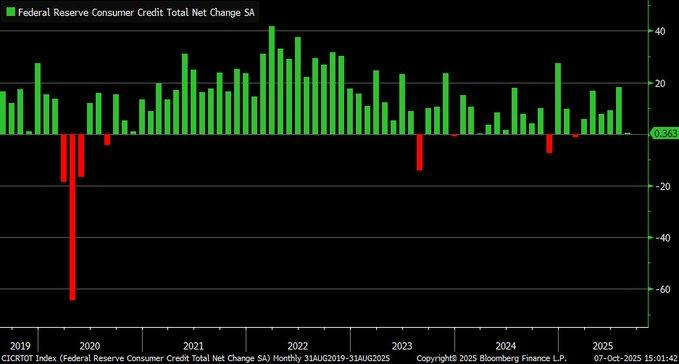

Consumer Credit Stalls As Households Shift To Deleveraging

US consumer credit rose by a paltry $0.36 billion in August 2025, far below market expectations of $14 billion and much lower than the previous July’s surge of $18.05 billion. Data is evidence of a definite cooling of household borrowing enthusiasm and indicates a broader phase of fiscal caution among households. Revolving credit, spearheaded by credit cards, fell at an annualised 5.5%, one of the steepest declines recorded since 2012, whilst non-revolving credit, comprising auto and students’ loans, rose moderately, restrained by tighter financing environments and high borrowing charges. Intersegment differential suggests that households are turning towards servicing debts and critical spending instead of discretionary growth, evidence of a consumption shift towards the late cycle.

This credit creation softness is not unique; it coincides with indicators of distress in personal savings and growing credit delinquencies. With consumers constraining leverage, retail and services sectors experience tailwinds from softer transactional activity and diminished demand for high-ticket items. Auto incentives and selective education financing cushion non-revolving segments, which are otherwise displaying resilience, though credit flow as a whole is lacking enough support to maintain retails’ fourth-quarter momentum. It also makes forecasting aggregate demand challenging, as household credit declines often foreshadows one-to-two-month slower retails sales growth, potentially testing inventories and margins in mid-tier consumer sectors. From a valuation perspective, consumer staples, auto part suppliers, and discount retails equities look underpriced, marking defensive opportunities amidst a climate of restraint in spending. Revolving credit usage ratios, retails foot-traffic indicators, and household balance sheets should be monitored as leading indicators of sentiment recovery by analysts. Lasting deleveraging will mean a more discriminate base of consumers—rewarding companies with price flexibility, low leverage, and predictable cash flows. As seen by Zaye Capital Markets, market stability in the near term will be determined by the speed with which credit dynamics stabilize before the season on holiday spending.

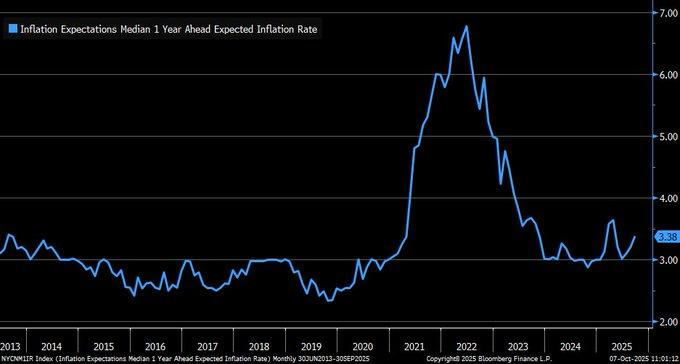

Consumer Inflation Expectations Turn Higher Despite Policy Easing

The latest New York Fed consumer survey for September 2025 shows inflation expectations edging higher, signaling that households are regaining concern over persistent price pressures despite recent policy easing. One-year inflation expectations climbed to 3.38% from 3.2%, reversing a gradual cooling trend seen since early 2025, while five-year expectations rose to 3.0%. The data highlights an inflection point in sentiment—consumers are recalibrating their inflation outlook as tariffs on imported goods and elevated service costs offset the dampening effects of recent rate cuts. This shift reveals that monetary adjustments have yet to meaningfully reshape inflation psychology, keeping long-term expectations anchored above the Federal Reserve’s preferred range.

The survey’s worsening outlook on financial conditions further suggests softening consumer confidence, as fewer homes project income growth or better affordability prospects in the coming months. Price premia attributable to tariffs in consumer electronics, autos, and metals have started influencing household cost forecasts, further fueling concerns regarding sustained erosions in purchasing power. Although short-term relief through falling financing charges is favorable, the intersection of high price stiffness and policy uncertainty maintains downward pressure on sentiment. On a historical basis, inflation expectations of this persistent nature will be constrictive on discretionary spending and delay core goods purchases, presenting challenges among retailers and service-based industries as the season moves toward the final quarter. On this backdrop, certain industrial exporters, utilities, and consumer staples stocks look underpriced, enjoying price control and stable margins in the midst of persistent inflation and defensive consumer attitudes. Month-to-month inflation expectation, core service prices, and import-sensitive industries should be watched by analysts as a check on the re-acceleration or stabilization of price pressures. At Zaye Capital Markets, we interpret the continuation of high expectations as evidence that the normalisation of inflation is still incomplete—pointing towards prudent portfolio positioning towards quality earnings and defensive cash-flow durability.

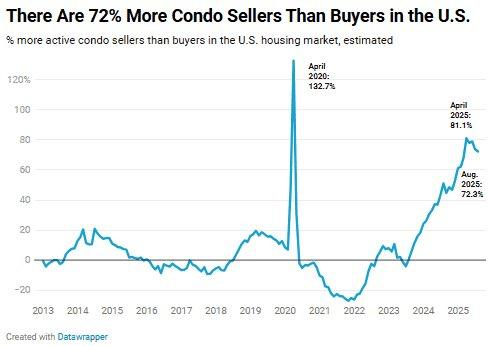

Condo Market Tips Sharply In Favor Of Buyers As Supply Outpaces Demand

The American condominium market is in its strongest buyer’s season in more than a decade, with sellers outweighed by buyers by 72.3% through August 2025. For the fifth consecutive month, the level exceeded the 70% barrier, marking a persistent structural shortage across key metropolitan areas. At the national level, just over 260,000 active condominium sellers are vying for just 150,000 purchasers, echoing growing inventory in high-construction areas like Florida and the Sun Belt regions. Even with this overwhelming excess, average condominium prices have kept creeping upwards—up 1.5% year-over-year to $385,000—implying demand is still selectively robust in high-demand urban and beach areas where inventory turn is holding up.

The divergence between market leverage and price stability underscores a deeper fragmentation in U.S. housing dynamics. Elevated mortgage rates have deterred new buyers while encouraging existing owners to list non-primary assets, particularly investment condos, to capture remaining equity value before further rate normalization. Meanwhile, single-family housing shortages continue to constrain substitution effects, sustaining modest pricing support even as transaction volumes weaken. The 15.1% cancellation rate for pending home purchases in August reflects affordability fatigue, suggesting that the current market equilibrium may shift further toward discounting unless financing conditions improve in the coming quarter. From a valuation perspective, construction material suppliers, select REITs with multifamily exposure, and regional mortgage service firms look undervalued, with the potential for upside as the housing market rebalances. Market participants should keep new permit issuances, condo absorption, and regional construction backlogs in focus as a way to evaluate if supply is peaking or plateauing. In our opinion, at Zaye Capital Markets, this is a transitional opportunity: although near-term pressure works in the favor of the buyer, the eventual stabilization of the rate has the potential to unleash dormant demand, paving the way towards the recovery in well-located, income-generating residential properties.

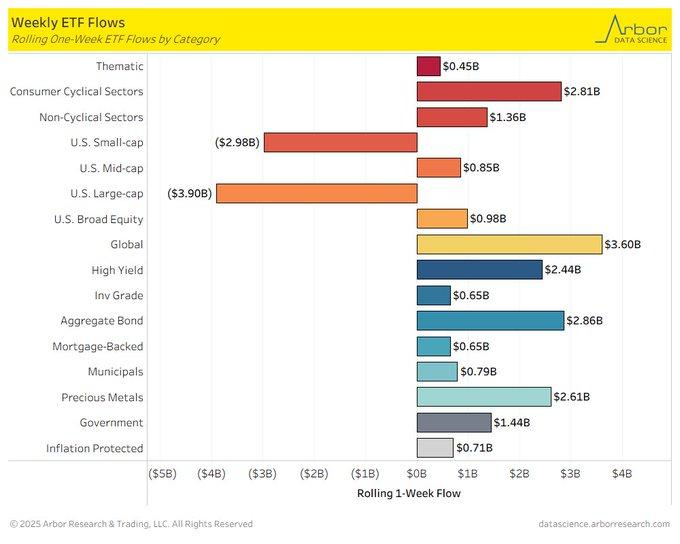

Investors Rotate Toward Defensive Assets Amid U.S. Equity Outflows

ETF flow data for the week ending October 4, 2025, underscores a decisive investor shift toward fixed-income and global diversification as capital rotates away from U.S. equities. Global equity ETFs absorbed $3.6 billion in inflows—the strongest among all categories—while U.S. large-cap and small-cap ETFs registered sharp outflows of $3.9 billion and $3.0 billion, respectively. This divergence highlights growing concern over stretched U.S. equity valuations and tariff-related policy uncertainty weighing on corporate margins. In contrast, bond markets drew robust demand, with aggregate bond ETFs gaining $2.9 billion, high-yield $2.4 billion, and precious metals $2.6 billion, reflecting a clear tilt toward income generation and capital preservation.

Versus the previous week, when allocations were evenly balanced between credit and equities, the new rotation points towards a growing risk-off tone as investors react to macro weakness and decelerating liquidity. Increased geopolitical uncertainty and new import tariffs have again motivated reallocations into assets that are least vulnerable to local policy risk. Strength in precious metals as well as ex-U.S. developed equity ETFs indicates market participants are positioning on the defensive hand while still keeping exposures open to diversified growth sources beyond the United States. Such a realignment is in sync with the third quarter’s all-time high withdrawals from equity funds, despite benchmark indexes still holding near all-time highs—a harbinger that sentiment, rather than price, is driving the decision on cap flows. Here, high-quality bond fund managers, gold miners, and a subset of internationals look cheap, underpinned by new flows and expanding yield premiums. Strategists will be monitoring further developments on tariffs, PMIs globally, and credit spread dynamics in the next days in deciding if the defensive stance is a tactical correction or the start of a broader structural rotation. At Zaye Capital Markets, we interpret the persistent bifurcation in ETF flows as evidence of readjustment among investors—preferring real asset and income approaches as risks in valuation overrule growth momentum.

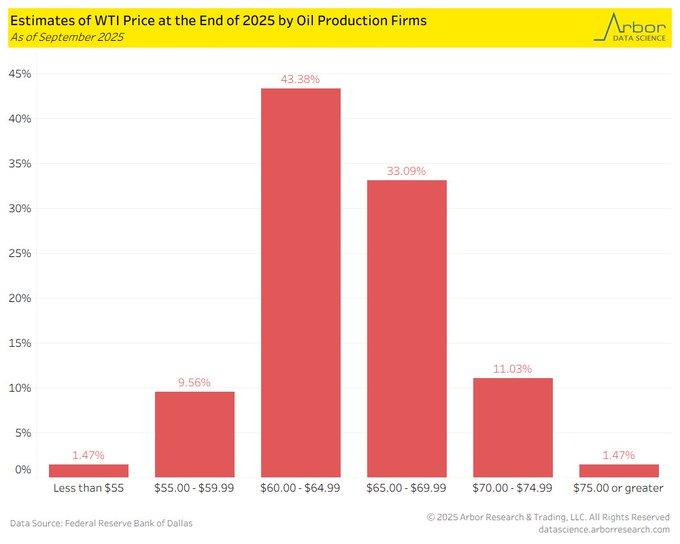

Energy Outlook Shows Price Restraint And Investment Caution

The Dallas Fed’s September 2025 Energy Survey indicates a significant shift towards conservative price views among American oil producers. About 76% of companies predict WTI crude will end the year in the band between $60 and $70 a barrel, with the average outlook at $63—slightly above current price levels around $62. Only 12.5% anticipate prices above $70, showing restrained euphoria compared with previous cycles when such geopolitical and supply impediments spurred rosier outlooks. The survey points towards a market adjustment in which producers favor capital discipline and shareholder remittances over fast-paced output growth, especially as cost inflation and financing constraints test small-scale players.

This prudent outlook is supported by breakevens in the Permian Basin, where production levels average around $60 per barrel. Persistently high prices around this level offer little room for reinvestment, particularly among independent drillers who need external capital support. OPEC’s persistent production control further reinforces the supply situation, as worldwide collaboration toward stabilizing prices restricts American manufacturers from benefiting from short-term upticks. The end is a situation in which growth in shale production can be tempered, making American response flexibility toward worldwide demand shocks limited and increasing the impact that foreign supply decisions have on the stability of the energy situation in the country. From a valuation standpoint, integrated energy majors, oilfield service companies with leaner balance sheets, and midstream infrastructure businesses look undervalued, underpinned by stable cash flow visibility and limited price risk one way at these levels. Drilling activity data, OPEC production changes, and United States producer capex guidance should be watched as key leading indicators of supply flexibility into the 2026 timeframe. At Zaye Capital Markets, we view the current energy sentiment as one of strategic caution—where volume-oriented growth is suppressed in favor of disciplined spending and operational excellence, insulating the sector in a timeframe of moderation on the price front and tempered enthusiasm.

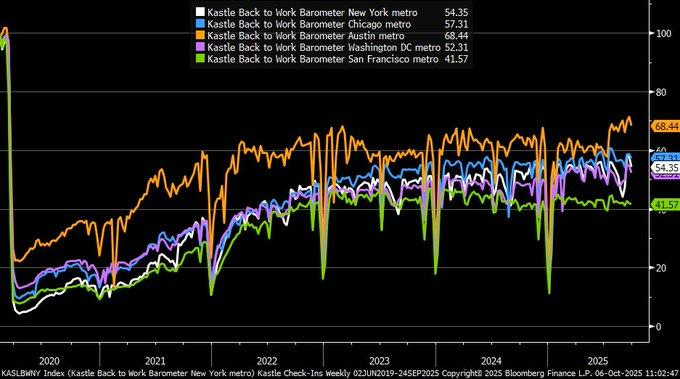

Austin Tops The National Return-To-Work Trend As Coasts Lag Behind

Kastle Systems’ Back to Work Barometer finds American office usage expanding further apart, with Austin achieving 68% of the levels seen before 2020 in early October 2025, the highest among the major metros that have been tracked. National office attendance was at 54%, highlighting the patchy nature of workplace recovery. Conversely, San Francisco is still muted at 41.6%, depressed by persistent hybrid modes and corporate flexibility that is widespread among large technology firms. Austin’s persistent advantage in talent inflows, business relocations, and commercial property stabilization is underscored by this spatial inequality, underscoring the city as a leader in physical office demand growth following the pandemic.

In other innovation hubs—such as New York, Boston, and Seattle—return-to-work is between 50% and 60%, still below structural equilibrium occupancy, indicating slow normalcy. Austin is resilient because the economic base is diversified across tech, energy, and professional services, allowing landlords the benefit of price leverage and competitive new leases. In the meantime, the coasts continue with sublease oversupply, compressed valuations, and subdued new construction, meaning the fuller recovery is further down the road. At the national level, the trend is that geography and cost competitiveness remain determining factors driving bifurcation of the office market through 2026. From an investment perspective, Sun Belt commercial REITs, local construction distributors, and property tech companies promoting hybrid workspace adoption look underappreciated, enjoying favorable leasing traction and capital flows from high-cost coastal properties. Expect analysts to track metro-level leasing velocity, vacancy absorption, and corporate relocation submissions as leading indicators of structural migration on-going. At Zaye Capital Markets, we interpret Austin’s outperformance as symbolic of a new cycle in commercial real estate—where affordability, accessibility, and local diversification spearhead the office market recovery over traditional coastal stalwarts.

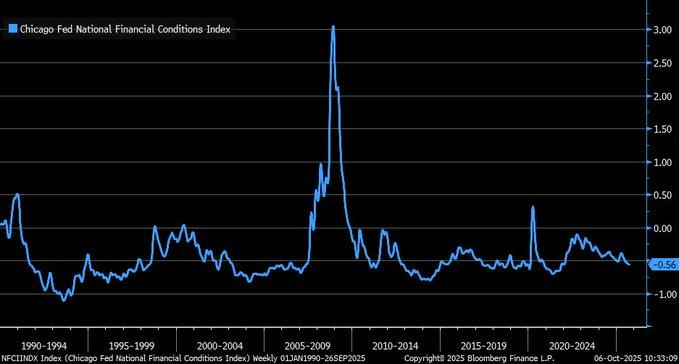

Financial Conditions Ease Further, Signaling Supportive Backdrop For Growth

The Chicago Fed’s National Financial Conditions Index (NFCI) fell to -0.56 in September 2025, a further easing trend that would indicate loose credit access, squeezed risk premiums, and better market liquidity. The index, comprised of 105 indicators in money, debt, and equity markets, is still well in the negative, a reading that corresponds with conditions more accommodative than long-term historical norms. Readings like these generally foreshadow real GDP expansion one to two quarters later, and as such, the current easing cycle would cushion economic momentum into the first half of 2026, despite the policy and inflation uncertainty that prevails. It is a sign, too, of the robustness of the American financial infrastructure, with credit transmission channels still active despite cyclical downturns in consumer borrowing and spending on business inventories.

Historically, periods of sustained negative NFCI readings have coincided with market tranquility and normal corporate issuance, though the level of easing is policy-cycle dependent. Conditions today are very different from times of tighter conditions seen in past recessions when risk spreads and borrowing costs explosively rose. Conversely, recent weakness in volatility indexes and stable interbank conditions reflect a risk environment that, although prudent, is still broadly constructive, though lingering inflation risks and lagged responses of previous rate cuts mandate further caution, as too-easy conditions again will fuel speculative activity and asset inflation before demand fundamentals rebalance. From a valuation standpoint, regional banks, investment-grade credit funds, and diversified financial service providers appear undervalued, poised to benefit from sustained liquidity and stable funding margins. Analysts should monitor NFCI’s subcomponents—particularly leverage and credit sub-indexes—for early signs of directional shifts that could foreshadow policy recalibration. At Zaye Capital Markets, we interpret the latest NFCI downturn as evidence of underlying financial health and accommodative market mechanics—an environment favorable for selective equity re-entry and duration exposure, provided inflation expectations remain anchored through year-end.

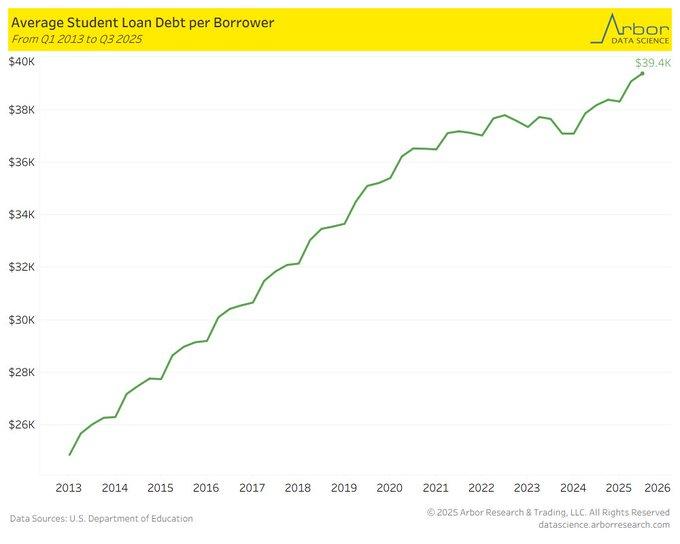

Student Debt Climb Outpaces Inflation, Weighing On Youth Economic Mobility

Data from the U.S. Department of Education, as charted by Arbor Research, indicates average borrower student loan debt rose from below $24,000 in early 2013 to above $39,000 in the third quarter of 2025—a 62% increase that substantially exceeds cumulative inflation of approximately 45% over the same interval. Acceleration is due to chronic inflation in tuitions, averaging between 3–4% per year, surpassing wage growth and increasing the financial strain on younger households. This prolonged spread has made education financing a structural macroeconomic phenomenon, more commonly associated with delayed asset formation and reduced first-time homebuyer penetration, especially among individuals under the age of 35. Total American student borrowing is now over $1.7 trillion, and the consumption disincentive through the reduction in discretionary income is becoming more prominent.

Tuition increases continue to be driven by institutional operating budgets, administrative growth, and plant investment, spurred on by shrinking state support towards public institutions. Result has been excessive federal and private borrowing, driving a self-perpetuating cycle between growing expense and borrowing by students. Relief efforts on the part of repayment offer temporizing relief, but the overall fiscal implication of chronic accumulation falls beyond the individual, impacting formation of housing, start-up of small business, and aggregate demographic consumption habits. Data, then, suggests not merely issue of individual finances, but growing structural impediment towards economic mobility and aggregate demand. Regional banks with education loan exposures, diversified consumer lenders, and construction companies connected with multifamily demand housing seem undervalued, with potential gains arising from both ordinary servicing activity and delayed homebuying trends. We recommend monitoring delinquency levels, income-driven repayment take-ups, and enrollment data as leading indicators of fiscal distress and credit risk dispersion. At Zaye Capital Markets, we consider the ongoing increase in student loan obligations as a policy and market inflection point—a one that will define the lifetime spending habits of generations and redefine the household leverage dynamics over the next decade.

Used Vehicle Prices Stabilize As Auto Market Normalizes

The Manheim Used Vehicle Value Index stood at 207.0 in September 2025, posting a 2% year-over-year gain but a 0.2% monthly decline, signaling that the post-pandemic surge in used vehicle prices is giving way to a more balanced market environment. The index, which tracks wholesale vehicle auction prices, has now returned to a range consistent with pre-2020 norms of 0–3% annual growth, reflecting easing supply chain constraints and improved dealer inventory levels. This moderation carries meaningful implications for inflation dynamics, as used car prices—once a primary driver of headline inflation—now contribute less upward pressure to consumer price indices. The trend reinforces a broader cooling in durable goods inflation that could offer the Federal Reserve additional policy flexibility in late 2025.

From a structural perspective, normalisation of second-hand car prices coincides with economic recovery in new car output and better supply chains. Stock replacement across the new and second-hand markets is aiding stabilisation after price distortions on the back of shortage conditions over the past few years. Soft demand conditions continue, though, in the low-income mass market consumer base, as financing charges and tighter credit have eased replacement demand. As wholesale prices stabilise, manufacturers and dealerships risk margin squeeze, especially on non-premium segments where market power is weak. This dynamic equilibrium between affordability, financing, and production competitiveness will define the performance of the auto industry through 2026. From a valuation perspective, auto part suppliers, logistic providers, and diversified dealership groups look undervalued, due for a gain from normalized prices and stable unit traffic. It will be useful for analysts to track the dealer inventory ratios, retail velocity of autos, and auto delinquency patterns in order to assess the durability of this price equilibrium. In our view, the current stabilization in the values of previously owned autos is a bullish inflection point both for consumers as well as investors—meaning the cessation of abnormal volatility and the resumption of predictable, fundamentals-based price dynamics across the American auto marketplace.

Upcoming Economic Events

As markets approach a critical juncture, the spotlight among investors is on the Federal Open Market Committee (FOMC) Meeting Minutes, one major release that can rebalance bets on monetary policy through the year end. This readout, comprising internal discussion from the recent policy meeting at the Fed, tells the market about policymakers’ views on inflation dynamics, the health of the labor market, and the desired trajectory for interest rates. Following eased liquidity conditions and weakened credit markets, the tone and content of these minutes will be uppermost in determining risk appetite as well as rate-sensitive trades.

FOMC Meeting Transcript

The minutes of the FOMC are, in effect, a contemporaneous leading indicator of policy belief and economic optimism.

- Should the data in the minutes—be it inflation attitude, growth outlook, or bias among voting members—be more hawkish than anticipated (implying greater worry about inflation or diminished appetite for rate reductions), markets would swiftly repriced tighter conditions. In that event, Treasury yields would be likely to rise, equity valuations—especially high-growth and technology—would potentially soften, and the U.S. currency could firm on renewed hopes of delayed monetary easing. Energy and banking stocks would have limited room on the up-side as the cost-of-capital issue comes back into play, and defensive shares such as utilities and consumer staples would be the beneficiaries of inflows.

- On the other hand, should the minutes’ tone turn out dovish more than anticipated—expressing more favor towards easing or belief that inflation is still under control—markets will take this as a go signal for risk appetite. This would probably further accelerate equity advances, squeeze yields, and hammer the buck downwards, as market participants look forward to a more accommodative policy ahead of the next policy window. Rate-sensitive areas like property, consumer discretionary, and tech would be best-placed to gain under this scenario.

We highlight at Zaye Capital Markets that this FOMC release is more than just a policy transcript, as it is a forward-looking signal on just how decisively the Fed plans on balancing the control of inflation with the preservation of growth. This week’s minutes could define the liquidity environment in the final quarter and decide if market bulls hold on to the current cheer or prepare for fresh volatility.

Stock Market Performance

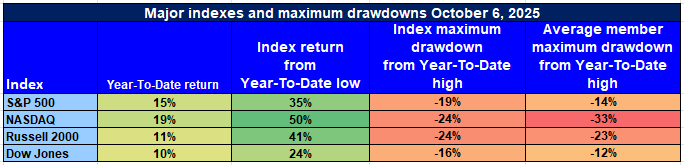

Indexes Extend Gains from April Lows, but Participation Remains Uneven

U.S. equity benchmarks have maintained upward momentum since the April 8th trough, yet structural volatility and uneven participation persist beneath the surface. Despite strong year-to-date advances, the depth of drawdowns across individual constituents reveals that the broader market recovery remains fragile and concentrated in select leaders. At Zaye Capital Markets, we interpret these dynamics as signaling optimism tempered by caution—a market still balancing growth enthusiasm with valuation fatigue.

S&P 500: Stable Leadership, Narrow Breadth

YTD: +15% | +35% off April low | -19% from YTD high | Avg. member: -14% (from April low) / -26% (from high)

The S&P 500 continues to reflect headline strength, advancing 15% year-to-date and climbing 35% since its April low. However, a 19% drawdown from the year’s high and the average member’s 26% decline from peak levels underscore that leadership remains narrowly concentrated among megacaps. Broader participation is still lacking, suggesting the rally is driven by balance sheet quality and large-cap defensives rather than widespread sector recovery.

NASDAQ: Growth Momentum Faces Deep Underlying Strain

YTD: +19% | +50% off April low | -24% from YTD high | Avg. member: -33% (from April low) / -48% (from high)

The NASDAQ has outpaced peers with a 19% YTD gain and a 50% rebound from April levels, highlighting resilience in the tech-growth complex. Yet a severe 24% drawdown from highs and steep average member losses emphasize internal fragility. Market leadership remains confined to a handful of high-multiple names, while much of the index still trades deep below prior peaks.

Russell 2000: Small-Cap Recovery Struggles for Traction

YTD: +11% | +41% off April low | -24% from YTD high | Avg. member: -23% (from April low) / -38% (from high)

The Russell 2000 shows modest year-to-date improvement at +11%, aided by a strong 41% rebound from April lows. However, persistent 24% drawdowns and wide member losses highlight ongoing pressure in small-cap and regional segments. Weak liquidity, higher debt costs, and inconsistent earnings visibility continue to restrain sustained small-cap participation.

Dow Jones: Defensive Tilt Shields Against Deeper Drawdowns

YTD: +10% | +24% off April low | -16% from YTD high | Avg. member: -12% (from April low) / -23% (from high)

The Dow Jones’ value and industrial composition has offered relative stability, posting a 10% YTD gain and limited 16% drawdown from highs. Average member losses remain contained compared to growth indices, reaffirming the index’s defensive profile amid cyclical uncertainty.

At Zaye Capital Markets, we continue to favor high-quality, cash-generative equities with durable earnings momentum and prudent leverage. Broader participation across mid- and small-cap segments will be essential to validate this rally’s durability and confirm that market strength extends beyond index-level resilience.

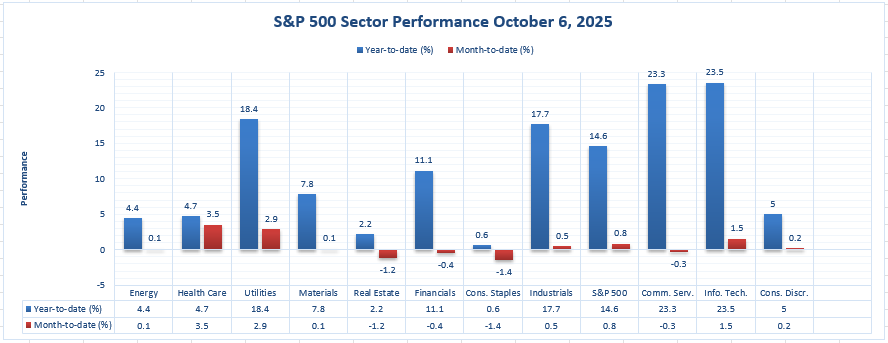

The Strongest Sector in All These Indices

Information Technology and Communication Services Sector Year-to-Date Sector Momentum

Up to October 6, 2025, sector-level activity through the S&P 500 showcases a clear profile of leadership, with the Information Technology and the Communication Services sectors as the leading sectors across the industries covered. With these two growth-laden sectors combined, these segments have outperformed the broader index’s 14.6% year-to-date increase, demonstrating unrelenting demand among investors in high-margin, scale-driven business models despite shifting macro environments.

Information Technology is the leader with a +23.5% year-to-date performance, underpinned by a +1.5% month-to-date return, highlighting further resilience in enterprise software, cloud infrastructure, and semiconductor stocks. The sector has retained its pace despite earlier-in-year tighter policy conditions, echoing resilient earnings strength and persistent capital spending across the digital domains. This showing reinforces investor demand for asset-light growth companies with resilient pricing power and robust balance sheets.

Communication Services is the second best-performing sector with a +23.3% year-to-date return, though the sector dropped marginally -0.3% this month, suggesting recent correction after a multi-quarter run-up. Led by digitization-based advertising, content streaming, and telecom infrastructure, the sector has benefited from recurring revenue streams and affordable methods, despite softening broader consumer sentiment.

While Utilities also had a brilliant +18.4% year-to-date and +2.9% month-to-date performance, the historically defensive nature keeps the sector into another positioning category—one that is more about focus on yield and stability versus acceleration in growth.

Zaye Capital Markets considers Information Technology the structurally best positioned sector into year-end 2025, and certain Communication Services names provide second-tier momentum opportunities. analysts should consider monitoring revisions, cap spending guides, and forward-looking free cash flow metrics as a way to capture sustainable outperformers across these groups of leaders.

EARNINGS

Earnings Recap– 07 October 2025 (Yesterday)

- McCormick & Company (MKC)

Yesterday, McCormick & Company (MKC) delivered its third-quarter results for the period ending August 31, 2025, surpassing consensus expectations. Reported net sales rose 3% year-over-year, driven by volume-led growth of 2% organically and a 1% favorable currency impact. Adjusted diluted EPS came in at $0.85, topping the ~$0.81 estimate, while gross profit margins contracted by 130 basis points, pressured by rising commodity and tariff costs. Key drivers and risks in McCormick’s report include cost pressure and margin compression—despite solid top-line growth, input inflation and tariff exposure eroded gross margins, requiring tight control over SG&A and continued cost-saving initiatives. The company lowered its full-year adjusted EPS guidance to $3.00–$3.05 (from prior $3.03–$3.08), citing additional tariff and currency headwinds. Meanwhile, resilience in consumer demand remains a bright spot, as volume-led growth reflects strong pantry behavior with consumers emphasizing home cooking—benefiting McCormick’s core seasoning and flavor portfolio. However, foreign currency and trade exposure remain areas of concern, with international operations, particularly in Mexico, facing vulnerability to tariff policy shifts and currency depreciation. Overall, this set of results underscores McCormick’s balanced execution: solid demand offset by cost instability and cautious forward guidance.

Earnings Preview– 08 October 2025 (Today, Expected)

- AZZ Inc. (AZZ)

Today, AZZ Inc. (AZZ) is scheduled to report its quarterly earnings after market close, with consensus estimates pointing to EPS of approximately $1.57. Investors and analysts should closely watch several factors in AZZ’s release, including whether the company beats or misses expectations around this figure. A result above $1.57 could lift sentiment materially, while a miss would likely highlight margin or demand pressure.

AZZ’s forward guidance—covering revenues, capital spending, and margin expectations—will also be critical for assessing demand trends in its galvanizing and coatings segments. In addition, order backlog and book-to-bill metrics will be closely observed, as they serve as leading indicators of sustainability in demand pipelines for infrastructure and industrial activity. Input costs, energy expenses, and operational efficiencies will play a key role in determining whether AZZ can preserve or expand its profit margins amid cyclical headwinds. At Zaye Capital Markets, we will be watching whether AZZ delivers upside and resets investor confidence, or opts for a cautious tone reflecting macroeconomic uncertainty.

Stock Market Analysis – Wednesday, October 8, 2025

US equity markets began the day on the back foot as technology-fueled volatility remains a damper on investor morale. In spite of strength in certain value and industrial stalwarts, the larger indices continue to weaken as a result of disappointing progress among key AI-related megacaps. The Nasdaq and S&P 500 trade lower, headed by softness among the “Magnificent Seven” names, as the Dow Jones and Russell 2000 hold up marginally on sector rotation into less rate-sensitive sectors.

Stock Prices

Economic Insights and Geopolitical Developments

Risk-averse feelings today are driven by a combination of disappointing quarterly results and general AI-driven equity fatigue. Market responses track softer sentiment in Tesla and Oracle—Tesla dipped after the release of new lower-priced Model 3 and Model Y versions that underwhelmed market participants, and the cloud margins of Oracle came into question as spending on infrastructures increased. Conversely, bullish Chinese economic data along with a small retracement in the United States Treasury yields have had little success in balancing risk-off flows. Investor attitudes remain responsive towards any policy-tightening signal or geopolitical risk, and focus is growing in the runup towards this week’s minutes on the FOMC meeting.

Latest Stock Stories

- $OKLO | Oklo has doubled over the last three months as investors accept micro-reactors as a strategic margin play in the AI data-center build-out. Oklo’s 15-megawatt reactors can be a significant winner in next-generation computing hubs—evading multi-year grid interconnect delay lines and making Oklo a critical enabler in AI infrastructure. Every new data-center deal announcement basically is a potential customer if Oklo is able to execute on deployment.

- $RKLB | Rocket Lab secured a new three-launch agreement with Japan’s iQPS through 2026, covering a total of seven missions reserved. Agreement supports the track record for reliability and control over launch tempo that Rocket Lab enjoys among small satellite constellation providers and solidifies market share.

- $IREN | Iris Energy is issuing $875 million in convertible notes, positioning itself for the next phase of AI data-center construction. It is a sign of aggressive balance-sheet positioning to grab infrastructure demand as well as strengthen liquidity before the next spending boom.

- $TSLA | Tesla finally launched the Model Y Standard, which is priced at $39,900 with a more-than-320-mile capability. It is the most unambiguous entry into the mass-market crossover segment by Tesla, aimed at growing accessibility and retaining market share as the competition intensifies in the EV space.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”–Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla–are still under sellers this week. With sectoral drawdowns exceeding over 18% from recent tops, these stocks have become the biggest drag on major indexes. Tesla and Meta are experiencing steeper re-alignments as excitement around AI cools and valuations tighten. Absent renewed leadership from these megacaps, the S&P 500’s ability to maintain a sustained rally seems limited, causing investors to look towards diversification in energy, industrials, and select real assets.

Major Index Performance as of Wednesday, 8th of Oct., 2025

- S&P 500: Trading at 6,710.42, down 0.4% on the day.

- Nasdaq Composite: Currently at 22,700.61, down 0.7%, as mega-cap tech continues to unwind.

- Dow Jones Industrial Average: Down 0.2% to 46,600.88, with modest strength in industrials offering support.

- Russell 2000: Down 1.1% at 2,430.17, underperforming as small caps face rate headwinds.

We view the current setup as a “rotation-led pause” wherein profit-taking on growth securities is giving way to selective strength on the part of value and defensives. Sustainable recovery in the overall market will depend on a reacceleration in leadership by the mega cap tech sector—broader sector take-up driven by positive macro data and resilient policy setup.

Gold Price

Through October 8, 2025, gold remains solid as a key hedge asset amid increased geopolitical and fiscal uncertainty, with SPDR Gold Shares ETF (GLD) at $366.26, and spot gold recently passing the $4,000 per ounce level on the market for the very first time. The swift leg higher is being fueled by a trio of safe-haven flows, expectations for monetary easing, and rising worldwide tensions. President Trump’s recent words have introduced a new level of complexity, including multiple references towards trade negotiations via Canada, changes in tariffs, and a possible Middle East peace breakthrough. His commentary on tariff negotiations, favorability toward Canadian industries, as well as a rebuke toward Democratic leadership amidst the current government shutdown, indicates high levels of uncertainty surrounding the economic stability in the United States. Also, Trump’s statement that he would meet Chinese President Xi in the next few weeks in South Korea introduces one possible flashpoint toward trade readjustment, something that historically has acted as a bullish catalyst toward gold. Markets are also processing words from Fed officials such as Kashkari and Bostic, who are cautioning about inflation’s direction and economic turbulence—views that continue to enhance the attractiveness toward gold as a repository for value amidst fluctuating macro fundamentals. Meanwhile, the focus is on the release today of the FOMC Meeting Minutes, which should offer cues on the Fed’s policy perspective through the end of the year. If the minutes are dovish or show rising concern over growth, gold will continue to receive inflows as hopes on real yields fall. But if the minutes become hawkish, they will momentarily curb gold’s advances, though the fundamental conditions remain favorable. In additional evidence, soft consumer credit yesterday showed that households are becoming more aggressively leveraged down, a harbinger that discretionary spending is slowing with potential strain on growth. As the shutdown enters the second week and federal furloughs rise, fiscal confidence is deteriorating—propelling investors into hard assets. In our view at Zaye Capital Markets, the geopolitical maneuvering, uncertainty over the central banks, and rising risks that consumption in the United States is slowing make the bull case on gold structurally bullish through the fourth quarter.

Oil Prices

As of October 8, 2025, the price of WTI crude oil is at $62.17 per barrel, with that of Brent at approximately $65.85, representing a slight rebound as markets absorb cues from the supply-side as well as macroeconomics. One major catalyst has been OPEC+’s release of a subdued production increase of a mere 137,000 barrels per day in November, which arrived lower than market forecasts and eased the near-term panic over the specter of oversupply. The move betrays the cartel’s delicate balancing act between underpinning the price, on the one hand, and recognizing softening demand globally, on the other hand. In the meantime, the International Energy Agency (IEA) has indicated that the inventories are increasing slowly across OECD countries, exerting some strain on the medium-term price. But the Energy Information Administration (EIA) this week increased the estimate of Q4 2025 American oil production, anticipating increased shale production that will partially counter the support efforts of OPEC. This back-and-forth between prudent supply management and rising production comes as fuel into intraday price moves. In addition, recent tanker flow data issued this week by ZeroHedge indicates Middle Eastern shipment levels remain high, and fresh doubts have been raised about future storage capacities if demand continues weak into Q1 2026. On the geopolitical side, President Trump’s statements have brought near-term uncertainty back into the energy markets. His allusions to possible changes in tariffs with Canada, forthcoming negotiations with Chinese President Xi, as well as an “imminent” Middle Eastern peace accord, are fueling a risk-sensitive volatility backdrop. Energy traders are scrutinizing any trade flare-up or retreating that could have effects on flows of crude in North America or general commodity sentiment. His statements on Canada’s Golden Dome project and American supremacy in trade also underscore the geopolitical risk that oil markets must price in. In the interim, yesterday’s soft American consumer credit data have raised fresh demand concerns at home, particularly on the part of gasoline and transportation fuels. If today’s FOMC meeting minutes reflect a dovish message or solidify slower economic pace, we can anticipate bullish pressure on oil via a softer greenback and diminished pace toward the high side. Conversely, a hawkish lean could effortlessly bring down prices if risk appetite declines further. At Zaye Capital Markets, we maintain the expectation that crude will remain firmly range-bound, with geopolitical cues, central banking tone, and the production strategy by OPEC still dictating directional conviction toward the end of Q4.

Bitcoin Price

The price of bitcoin is at $121,691, retreating slightly from the recent all-time high above $125,000. This correction, as a about a 2% intra-day loss, is viewed as fleeting short-term profit-taking, rather than structural shift in sentiment. Even with the retrenchment, institutional flows are still heavily bullish. In recent reports, combined global crypto ETFs recorded a new all-time high of $5.95 billion inflows last week, with bitcoin alone contributing over $3.5 billion. Spot bitcoin ETFs located in the United States also recorded a one-day net inflow of $1.2 billion, almost entirely from the product issued by BlackRock, IBIT. Such level of engagement is a testimony of increasing conviction on the part of institutional allocators who are no longer viewing bitcoin as a speculative asset, but as a macro hedge as fiscal and political instability continue to pile up. Strong inflows into the ETFs also go hand in hand with the broader-based “digital gold” story, as investors, in times of volatility in the dollar and uncertainty among the central banks, look towards scarce, non-sovereign safe havens. President Trump’s recent statements—spanning from trade negotiations with Canada to possible Middle Eastern peace deals—are fueling broader geopolitical uncertainty and trade rebalancing angst, all further boosting the attractiveness of Bitcoin as a decentralized hedge. Shutdown rhetoric is escalating and internal fiscal instability is driving investors toward stores of value unconnected with government or credit cycles. Yesterday’s soft consumer credit data stoked such fears, highlighting soft US consumption and increasing caution among consumers—conditions that generally erodes faith in fiat-based financial products. Today’s FOMC meeting minutes will play a key hand in crypto sentiment, too—dozens reading dovish could solidify risk appetite and increase BTC, while hawkish cues might, temporarily, depress prices. At Zaye Capital Markets, our view is that Bitcoin is still fundamentally supported on structural macro tailwinds—least notably increasing institutional demand, ETF accessibility, and evolving status as a liquidity hedge in a policy-fractured world.

ETH Price

Ethereum (ETH) is valued at $4,448.49, down approximately 5% intraday, as the overall crypto market corrects sharply after rapid rallies over the past fortnight. Despite the correction, on-chain and institutional data still reflect bullish demand and accumulation. In the past week, Ethereum-specific ETF products have seen more than $1.48 billion in net inflows, making ETH the second-most popular crypto asset after Bitcoin in institutional portfolios. This explosion in capital flow into ETH-linked ETFs is a bellwether of growing investor faith in Ethereum’s long-term relevance and its linchpin status in the Web3 and decentralized finance (DeFi) economy. At the same time, on-chain whale activity has been busy: one prominent wallet address, irrespective of intent, transferred $188 million in ETH out of exchanges, a telltale sign of bullish, longer-term holding intent. Meanwhile, another high-profile whale—earlier bulking up with 86,001 ETH at an average price tag of $3,023—recently transferred 6,010 ETH (~$27.25 million) into Binance, indicating strategic profit-takeout or portfolio rebalancing. The coexistence of simultaneous large-scale purchases and selective selling presents a balanced scenario. While rotating capital whales or locking in profits after the surge in Ethereum’s 2025 is possible, new addresses are entering aggressively. An example saw one such wallet purchase 5,297 ETH (~$24.7 million) recently, demonstrating persistent high-conviction entry on current price levels. Such reciprocal flows cause near-term volatility, but the net effect is bullish when combined with ETF momentum and exchange flows. Diminishing liquid supply on the exchange level usually results in increased price responsiveness when purchasing pressure is back on track. On the macro backdrop, Ethereum is still very responsive when it comes to Federal Reserve tone, general crypto sentiment, and network upgrade. Should today’s FOMC minutes reflect a dovish bias, and should Bitcoin maintain its institutional inflows, ETH is well on track for another leg higher—especially given as it continues to solidify itself as the base layer protocol for decentralized apps. At Zaye Capital Markets, we remain of the opinion that Ethereum’s medium-term trajectory is constructive, with ETF adoption, scalability into smart contracts, and DeFi resilience acting as key price supporters—despite short-term volatility that continues to remain fueled by strategic whale activity and liquidity flows.