Where Are Markets Today?

The global equity markets are set for a positive start today, with U.S. equity futures leading the way, while European markets follow suit. The S&P 500 equity futures are up by around +0.7 percent, while the Nasdaq 100 equity futures are up by around +0.9 percent, signaling widespread buying activity prior to the market opening. The European equity market indices are also trading higher, up by around +0.5 percent, albeit to a lower extent, given regional market concerns. This positive start is triggered by increasing hopes of a truce in the ongoing trade tensions between the United States and China, with both parties reporting near breakthroughs prior to a critical meeting scheduled between President Trump and President Xi Jinping later this week. Moreover, according to United States Treasury officials, the talks in Malaysia were “very constructive,” thereby signaling that the tensions could ease—at least for the time being.

The bullish tone in US futures is also supported by the recent ease in inflation expectations. The comments by senior advisor Kevin Hassett that “inflation is decelerating,” and that “there will be no inflation data next month,” have served to further ignite market speculation that the Fed will keep interest rates stable, or perhaps turn dovish if the economy continues to weaken. This has served to drive tech and growth-sensitive names sharply higher in pre-market action, especially in Nasdaq stocks. But market participants remain wary. The government shutdown is approaching its fourth week, and, according to Hassett, is serving to subtract “a tenth of a percent each week from US GDP growth.”

The European market, too, is receiving support from the same trends in the US-China relationship, although gains are limited by regional structural concerns. With slower growth, higher and sticky inflation, and limited flexibility for monetary policy, European investor sentiment has been dented. Trade optimism, although providing support in the near term, remains closely attuned to today’s German Ifo Business Climate Index, a clear pointer for European investors in understanding the collective mindset for the European Union’s biggest economy. Disappointment in that metric can readily destroy today’s optimism. The energy-sensitive sectors, too, remain delicate in the European market, where prices continue to swing on geo-headlines, particularly in Canada and Venezuela, both identified by Trump in recent comments. “Relief rally,” that’s how we view the strong futures market advance at Zaye Capital Markets. While it’s positive that tensions are de-escalating, it’s clear that the market has not yet fully priced a resolution. “Risk-on trade positioning is highly attuned to policy communication, macro data feeds, and geopolitical trends,” we note, and we continue to recommend that clients monitor central bank communication, particularly from the ECB and Fed, as well as U.S.-China trade talks in the days that follow. The market mood is currently tilted positive, but the big picture is still mixed, “with yesterday’s advance driven by hopes, not convictions.”

Major Indexes’ Performance through Monday, 27th October 2025

- S&P 500: ~6,791.69

- Nasdaq Composite: ~23,204.87

- Dow Jones Industrial Average: ~47,207.12

- Russell 2000: ~2,513.47

The Magnificent Seven and the S&P 500

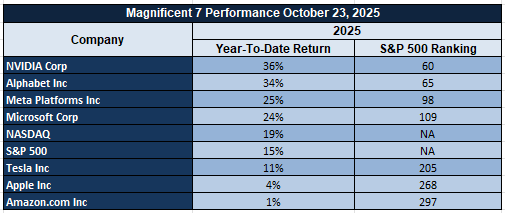

The “Magnificent Seven,” consisting of Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla, are again carrying an outsized burden in index gains and are also under intense scrutiny. The group has corrected hard from its recent highs, hurt by concerns of margins, regulatory tensions, and also muted growth outlooks. The weakness in the index leaders is pulling down the S&P 500 and Nasdaq Composite indexes, and it seems that without a rotation in market leaders, it will become difficult for the market to maintain its trends.

Drivers Behind the Market Move – Monday, October 27, 2025

With U.S. and European markets facing a cautiously positive open, factors such as trade signal activity, fiscal concerns, and upcoming economic releases are contributing to market perspectives in both regions. Despite markets being positive, positioning has remained sensitive, given the tensions between optimism and structural market issues.

- Renewed U.S.-China Trade Optimism with Mixed Messaging

Markets are reacting positively to any indication that there is forward movement for the upcoming meeting that is expected to take place between President Trump and President Xi, and comments from the Treasury that the recent trade talks in Malaysia were “very constructive” are certainly reassuring that a framework agreement can become a reality. However, the setting is still quite tumultuous, given the recent 10% tariff hike by President Trump on Canadian imports that added another twist to the trade story, along with the start of the Section 301 probe by the USTR related to China’s Phase One Agreement.

- Recent German IFO Business Climate Figures in Focus

European markets are expected to see small gains, with market participants waiting for the publication of Germany’s IFO Business Climate Index figures. The index is expected to provide market participants with important information on Germany’s economy, which is the biggest economy in the European region. Any figure that comes in lower than market expectations could result in market concerns escalating, particularly in light of ongoing inflation and reduced flexibility in monetary policies.

- U.S. Fiscal and Growth Concerns Mount

Comments from former White House economist Kevin Hassett that the ongoing government shutdown could shave off a tenth of a percent from GDP each week have injected fresh concerns about fiscal drag. Meanwhile, the lack of clarity on whether inflation data will be released next month adds to macro uncertainty. Combined with weaker U.S. regional manufacturing data reported last Friday, these developments are prompting investors to brace for potential downside revisions in Q4 growth forecasts. As a result, traders are positioning cautiously, rotating into quality and waiting on central bank guidance for further clarity.

In summary, today’s market movement is being shaped by a hopeful—but far from resolved—shift in U.S.–China trade diplomacy, Europe’s looming business confidence data, and rising concern over fiscal dysfunction at home. While futures point higher, the undercurrent remains one of selective optimism rather than broad-based conviction.

Digesting Economic Data

The TRUMP Tweets and Their Implications

Recent statements from President Trump and top-level officials in his administration have brought a unpredictable combination of factors for economists, geopoliticians, and trade experts to sift through. Perhaps the biggest shock, however, comes from the administration’s claim that it is “likely that no inflation data will be released next month,” injecting a whole new level of opacity into the larger economic backdrop when markets are thirsting for clarity. This, plus statements from Hassett that “inflation is decelerating,” will likely signal that the administration is trying to lower the pressure for more aggressive monetary policies, forcing the Fed to hold rates steady instead. However, without hard data from the administration, it’s likely that markets will start to factor in uncertainly, leading to unpredictable market swings for assets sensitive to inflation, such as bonds, gold, and cryptocurrencies.

With regard to trade, the tone emanating from the Trump administration has both contradictory and mixed messages. The administration speaks about hoping for “a complete and comprehensive agreement” with China, talking about “great friendship” with President Xi Jinping, and recognizing the “thawing” of relations. This is juxtaposed, however, by launching “a Section 301 investigation on China’s commitment to the Phase One Agreement,” and “frustrations,” making it clear that China has not adhered to the agreed trade policies. This mixed signal affects corporate planning, investment, and trade projection forecasts for global corporations that stretch from North America through Asia. The mixed messages are also witnessed when it comes to Canada, since the administration has announced an “expected talk” with the Canadian government by the “end of its term,” simultaneously increasing tariffs by 10% for Canadian imports, hardening trade barriers for corporations.

The energy and environment sector was not left untouched either. Trump has made it clear that the “temporary halt” on offshore wind energy plants in New Jersey will instead become “permanent,” implying that regulatory difficulties could become more severe for the energy sector. On the other hand, in relation to global security, it was made clear that Trump will no longer hold talks with Putin without having a “peace deal” in hand, yet also hinting at possible future attacks in Venezuela, along with a warning directed at Hamas for the return of hostages. The net result is that it has become extremely difficult to identify risk in the market through traditional channels, such as economic data releases and company results, when it comes to market shifts caused by the utterances of the new administration’s executives. With a macro lens, such comments are made while increasing fiscal distress, since the government shutdown has only “just begun to eat into the muscle” of the US economy, according to Bessent, a economist for the White House. With added drag from Hassett’s concerns that GDP could decline “a tenth of a percent each week” during the government shutdown, it’s clear that such mixed messages demonstrate a lack of clarity in the signals given from a tone that’s offered by the administration’s outlook, making for a reactive market environment in which we trade, from a hedging perspective, at Zaye Capital Markets by strongly advising our clientele to act prudently.

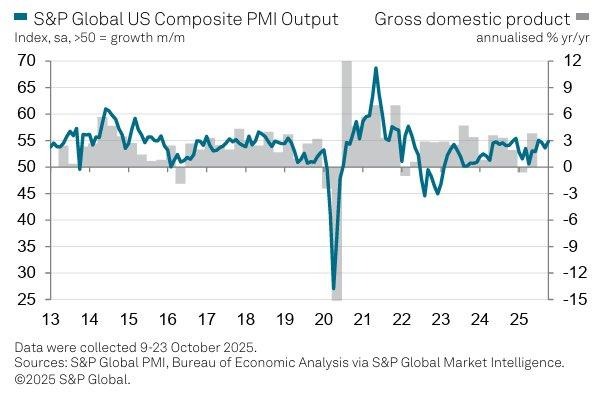

Expansion Persists Amid Policy Gridlock

Preliminary October figures for the U.S. Composite PMI indicate a strong recovery, growing to 54.8, significantly better than last September’s 53.9 reading, denoting faster growth for the private sector at an annual rate of approximately 2.5%. The sector breakdown for the October PMI, at 52.2 for Manufacturing and 55.2 for Services, completely vindicates the resilience in the economy, defying the country’s four weeks without a functioning federal government. While reality has proven that something can indeed happen every four years, the ongoing governmental stalemate does, however, include increasing elements of unpredictability when it comes to medium-term strategic outlooks.

Overlaying PMI trends with GDP performance, it can be seen that growth continues through the start of Q4, although confidence trends indicate that underlying conditions are eroding. Business confidence has dropped to its weakest level in three years, driven by concerns for costs related to tariffs and lack of clear policy vision. The contrast presented by both rising costs and weakening selling prices signals a shift in corporate profitability, wherein despite positive trends for demand, the pressure to maintain profitability through lower pricing for market share suggests that profitability trends may face a turning point.

Market-wise, it seems that the industrial and materials stocks are undervalued, since they are sensitive to production trends, pricing, and themes related to normalization of the supply side. Although the PMIs continue to support the growth story, it would be important for strategists to monitor leading indicators related to orders, delivery times, and employment. If the gap that has emerged between cost and production continues, it could dramatically change the way sectors perform through the end of the year. Our team at Zaye Capital Markets sees it as a phase for selective accumulation, offset by defensive income through the period until clarity emerges.

The Inflation Picture Reveals Contradictory Trends Amid Rekindled Energy Prices

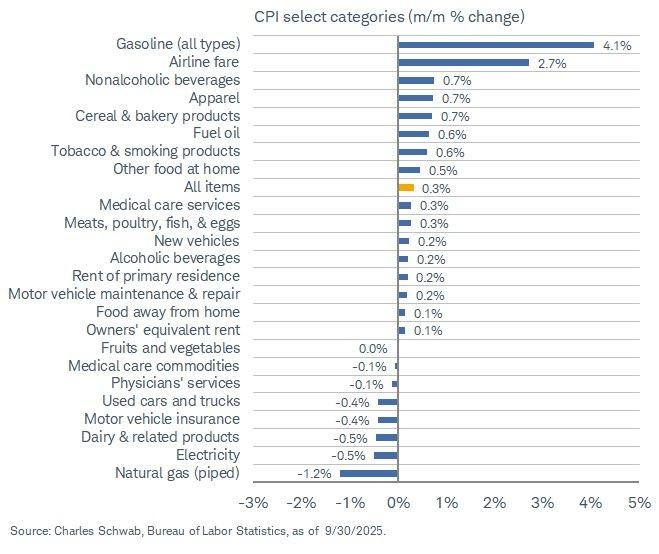

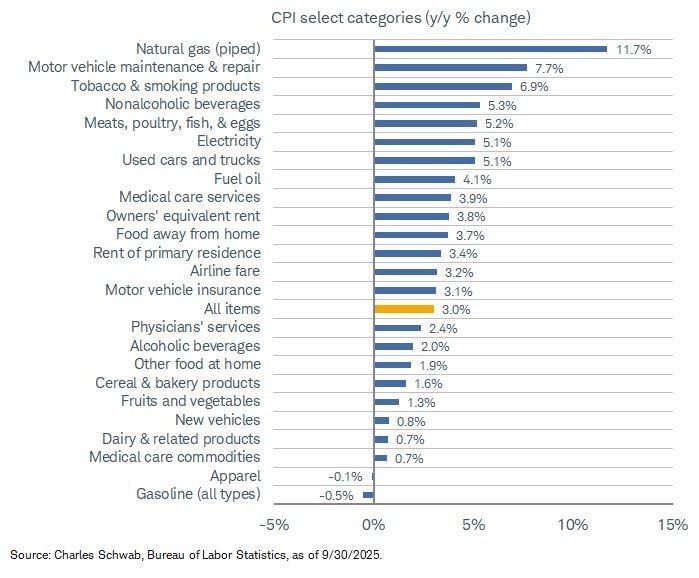

The most recent Consumer Price Index number for September portrays a rather mixed picture on the inflation front, with the headline index increasing by 0.3% on a monthly basis and by 3.0% on a year-over-year basis, exactly as expected, albeit again pointing to turmoil in energy prices. The break-down classification illustrates that gasoline prices are up by 4.1% and airline fares are up by 2.7% from the previous month, thereby again confirming that pass-through pressures from increases in crude prices continue to hold strong. However, when it comes to annual growth, natural gas is up by 11.7% and motor vehicle maintenance by 9.7%, thereby again confirming that services-based inflation continues to remain sticky, despite the downturn in goods, such as clothing and used cars.

The deeper lesson from the trends in the data is therefore one of controlled and fragile stability, whereby while trends in total inflation are relaxing, periodic energy shocks remain poised to disrupt the process of achieving normalized prices. The type of CPI growth also keeps evolving to include ever-higher growth in essential and energy-intensive commodities, whereby there is sensitivity to costs that can readily shape consumer behavior. Even so, the lack of confidence in data collection methods and imputations also adds its rationale, whereby the issue of path-inflation discrepancies between the economy and reality remains central to shaping market perspectives on monetary flexibility.

On a fundamental basis, consumer staples and utilities look undervalued in our view. The defensive nature of their earnings and their ability to generate cash flows beneficially in an invariant, higher inflation environment fit well with stable, higher growth rates for their prices. Analysts will note activity in core services inflation, wage growth patterns, and real income figures in upcoming releases for insight into whether the recent ease in goods prices can follow through to the rest of the economy. Our view at Zaye Capital Markets is that energy normalization and productivity, important determinants that could shape sector leadership trends, will drive further movement toward equilibrium for prices.

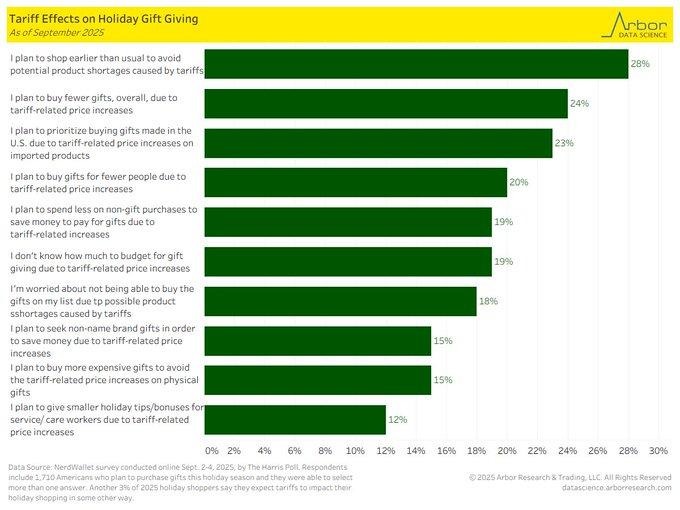

Shifts in Consumer Behavior Preceding Tariff Season

The latest available survey results also signal a significant shift in behavior in how American consumers are reacting to the tariff uncertainties that will impact holiday spending decisions. About 28% will start making their purchases well prior to the holiday season to prevent any possibility of future item shortages related to tariff policies, while 24% expect to purchase fewer items for the holidays, citing rising costs, and 23% will look to purchase domestic items. Here, it can also be noticed that tariff expectations, and not tariffs themselves, seem to affect the consumer mindset.

The data illustrate a layered macro backdrop: confidence readings remain moderately positive, yet sentiment surveys point to growing consumer fatigue from pricing instability and trade-related uncertainty. While aggregate spending may hold firm in nominal terms, composition shifts suggest a tilt toward essentials and domestic goods, reflecting cautious adaptation rather than outright retrenchment. The public discourse around tariffs—amplified by diverging opinions on necessity and impact—further underscores the fragile equilibrium between economic resilience and policy-induced risk perception. This evolving consumer narrative is a vital gauge for Q4 retail and logistics dynamics, particularly given how sentiment-driven demand often leads broader market trends.

With regards to equity analysis, it seems that consumer discretionary stocks that source domestically well could be undervalued, poised to capitalize on initial spending trends and minimize risk related to imports. Analysts will look for trends related to consumer purchases, indices related to the costs of imports, and surveys related to sentiment for validation related to shifts in behavior. This clarity related to prices and patterns related to goods could revitalize confidence related to the holiday spending period, or noise related to tariffs will continue patterns that favor domestic production. Our company, Zaye Capital Markets, finds it a market that is ripe for flexibility and value-driven strategies related to operations.

Regional Manufacturing Increases, But Demand Signals Weaken

The recent Kansas City Fed Manufacturing Survey for October illustrates that growth is moderate regionally, albeit seeing signs of weakness in demand, since the index rose to 6 from a previous measurement of 5, although the new orders index dropped to 1 from 2. Interestingly, this signal contrasts with an ongoing recovery for the industrial sector, which has become mixed in nature within the Tenth District, since its producers continue to see challenges related to the reduction in exports, credit, and inventory. Despite the improved level for output, it is clear that production has been driven by backlogged orders.

The historical perspective offered by the survey draws attention to the fact that the present new orders are currently poised around a decade-low, although the outlook for the next half-year has edged higher to 10 from 9, hinting at a glimmer of hope for the start of 2026. The manufacturing sect is adjusting to a life beyond the period of contraction, during which it has experienced stabilizing costs and initial hiring, although the weakness in the number of hours worked and exports casts a cloudy outlook on the recovery path. The outlook offered by the survey for the manufacturing sect draws parallels for investors observing the national scenario, in that growth is happening, although its basis still remains weak.

On a valuation basis, it appears that the stocks related to industrial and machinery equipment are undervalued, specifically for names that balance domestic representation and demonstrate strategic inventory management. Analysts ought to observe capacity use rates, inventory lead times, and new export orders in the coming regional and national releases for insight related to the sustainability of the recent turnabout. This is a transition period that we, at Zaye Capital Markets, believe strongly will support sound accumulation in superior industrials that can translate stabilization in demand through strengthened margins, thereby offsetting the still-weakening cycle.

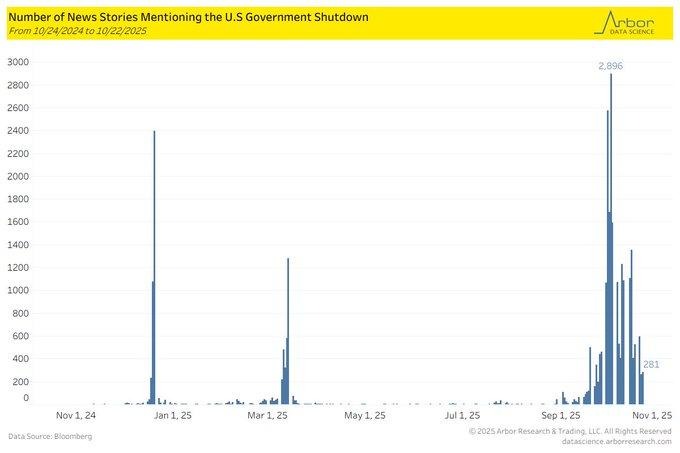

Fading Headlines, Lingering Fiscal Risk

The level of media coverage related to the ongoing U.S. government shutdown has significantly decreased, and the number of mentions in the news has fallen from 2,896 in early October to merely 281 by the end of the month, although it has been four weeks since the government shutdown. The significant downturn in media coverage reflects a shift in market narrative, where market participants are becoming numb to the implications of the ongoing issue. However, it is important to note that economic implications related to delayed grants, procurement, and wages for civil servants continue to affect short-term economic activity. Such past government shutdowns have impacted economic output, thereby reducing GDP.

However, the muted media cycle could end up concealing the actual extent of the ripple effects that happen. The actual past trends seem to indicate that each week that the government stays closed leads to an average deduction in productivity amounting to $1.5 billion, thereby pointing towards the inherent inefficiencies that end up arising when the budget discussions drag on. The financial market may well have absorbed the noise without too much volatility, but the underlying costs still continue to manifest, especially for small contractors and local communities that happen to revolve around government activity.

On a sector basis, defensive and infrastructure-tied stocks look undervalued, driven by temporary disruptions in market flow rather than underlying lack of demand. Analysts will note that T-security Flow, Contractor payments, and revisions to 4th-qtr government spending forecasts will drive liquidity Dynamics and budget normalization timelines once the crisis is overcome. Additionally, at Zaye Capital Markets, we believe that although market stability could improve once the headlines pass, fiscal inefficiencies pose an underlying risk that could manifest abruptly in the event that budget talks don’t lead to solid stabilization efforts.

Housing Market Gathers Pace Despite Persisting Affordability Pressures

The resilience of the recovery in the US real estate market has been reaffirmed by recent home sales figures, with median single-family home prices growing 2.26% from a year ago in September 2025, marking the 27th consecutive months since mid-2023 that home prices recorded gains. The market trend has reflected similar resilience, with existing home prices increasing to $415,200, growing 2.1% from a year ago, and total home sales rising 1.5% from last year, increasing to 4.06 million. Despite the continuous government shutdown, the market has continued to operate as a silent stabilizer for home wealth and economic activity.

Despite that, the gains in house prices are accompanied by interest in structural affordability issues. The inventory level remains remarkably low at 4.6 months, well below the level that reflects balance, at 6 months. Even as interest rates, down from 6.8% in September, become more favorable for entry, the ratio of house prices to income is still 40% higher than its average, posing clear affordability problems, especially for first buyers. Such a mismatch between house prices and purchasing power may hold growth in transaction volumes through the start of 2026, despite a constructive market setting.

On a valuation basis, residential construction and building materials stocks look undervalued, driven by strong pricing power, backlog trends, and underlying growth in the demand for residential modernization. Analysts are advised to monitor housing start, mortgage application, and regional-supply trends for affirmation that the recovery trajectory has strengthened and is on track. Our perspective at Zaye Capital Markets is that the resilience in the housing market, albeit buffeted by affordability challenges, is arguably the strongest support foundation for today’s ongoing U.S. cycle. This tactical philosophy of favoring well-positioned developers, thereby driving leverage through land inventory, continues to provide the soundest procedural course for a residential market rebalancing toward growth normalization.

Retail Sentiment Firms, Signaling Potential Market Upside

The latest AAII weekly survey, for the week ending October 23, does indicate that the bull-bear spread has improved to -5.8%, registering a slight decline in pessimistic outlook by retail participants, particularly after last week’s strongly bearish outlook. While still negative, such market readings have traditionally acted as contrarian market indicators, prior to equity market rallies. Peer-reviewed literature on studies related to human behavior in financial markets has identified that when the AAII bull-bear spread moves below -5 percent, average returns for the subsequent four weeks tend to range around 1.2 percent, thereby demonstrating that market recovery logically tends to happen when market jitters reach their peak.

The context in which this market sentiment information exists, therefore, is characterized by volatility, albeit tempered by pockets of optimism. Retail investors, despite the strong equity market performance in the year so far, continue to demonstrate defensive portfolios by reallocating to cash equivalent and income instruments, rather than becoming more market-friendly. However, contrarian analysis would indicate that when strong fundamentals coexist with ambiguity, the path for fresh growth can often become clearer when liquidity improves and the resilience in corporate profitability emerges from the haze.

On a fundamental basis, financial and technology stocks look undervalued, given the lack of widespread participation by individual investors and increasing estimates. Analysts should monitor equity ETF investment, margin debt, and participation rates to see if the process of normalizing market sentiment has translated into actual market participation. At Zaye Capital Markets, we view the market conditions that exist currently as conditions characterized by constructive skepticism, a market environment that has virtually always proven to be constructive for accumulation in quality growth and value stocks.

Upcoming Economic Events

German IFO Business Climate Index

With the upcoming release of the German IFO Business Climate Index, market participants are particularly interested in the largest economy in Europe for any indication related to its industrial sectors and growth trends. The IFO index, consisting of responses from thousands of German firms in industries such as manufacturing, services, trade, and construction, is widely regarded as one of the leading forward-looking indicators for the entire Eurozone. This important index is also used frequently as a first indication for Eurozone growth trends, investment, and future workforce trends.

German IFO Business Climate Index

- If the actual outcome overshoots expectations, it would indicate that businessmen are becoming gradually more optimistic about the outlook for the economy. This positive shock will conceivably boost the euro, regional stock market indices–especially the DAX, and bond yields, since financial markets will discount more optimistic growth prospects. Market participants will see it as having a positive impact on manufacturing, along with improved outlooks for exports. The implications for global financial markets could lead to greater risk appetite driven by improvements in Germany, causing commodities related to manufacturing to rise.

- On the other hand, a scenario where the actual number trails market forecasts would indicate that there is still a hint of pessimism in the corporate world, hinting that global slack, the energy bill, or trade tensions continue to affect corporate estimates. This would lead to pressure on the Euro, slight corrections in equity markets, and an influx of safe investment in government bonds. Analysts will also see it as a sign that could indicate lower Q4 industrial production in Europe, and thus speculation for additional European Central Bank policies will start once again. This announcement will also remain important for us at Zaye Capital Markets, since it will act as a crucial market risk appetite indicator, affecting European market trends for the coming period.

Stock Market Performance

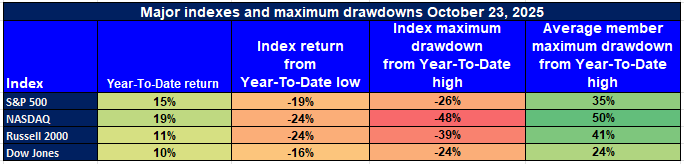

Indexes Rebound Sharply Since April, But Breadth Is Still Uneven

The market recovery since the troughs on April 8, 2025, has been strong for U.S. stocks, but corrections for underlying drawdowns indicate that the market still reflects imperfect participation and leadership. The market leaders are reporting double-digit gains for the year, although the difference separating index performance from average stock participation in the recovery has caught my attention for its emphasis on concentration risk. The resilience in the recovery has clearly been impressive, but beneath the surface, lack of market participation has become apparent.

S&P 500: Steady Recovery, Narrow Leadership

YTD: +15% | +35% from low on Apr. 8 | -19% from YTD peak | Average member: -26%

The S&P 500 is still the benchmark for equity market strength in the United States, having rallied 15% so far this year and 35% from its trough in April. However, the 19% fall from its annual highs and average sector participation of 26% indicate that recovery is still led by a few big index leaders.

NASDAQ: Tech Outperforms, but Member Weakness Persists

YTD: +19% | +50% from Apr. 8 low | -24% from YTD high | Average member: -48%

The NASDAQ is still leading the way with the highest market performance, jumping 19% so far in the year. The 50% rebound from its low in April clearly reflects risk appetite for growth stocks, although average losses for its constituent stocks at 48% clearly indicate volatility still inherent in the sort of market.

Russell 2000: Small Caps Recover, Sentiment Still Fragile

YTD: +11% | +41% from low on Apr. 8 | -24% from YTD high| Average member: -39%

The Russell 2000 Index appears to be alive, having rallied 11% so far in 2025 and 41% from its spring low. Notwithstanding, it is important to note that the level of maximum peak pull-back at 24% and the departure of numerous index members warn that prudence still prevails for economically sensitive and rate-sensitive small caps.

Dow Jones: Stability Outshines Momentum

YTD: +10% | +24% from low reached on April 8th | -16% from YTD peak | Average member: -24% The Dow is holding well, having made a 10% start to the year, albeit with decent volatility. This reflects its lower level of volatility, registering only a 16% drawdown, and average losses for its constituent companies of 24%.

Our outlook at Zaye Capital Markets is well rounded, preferring quality, cash-flow-strong names to directional trades in regard to breadth gauges still lagging completion. The current level of equity drawdown analysis implies that there is merit in lagging areas, although market health will depend on increasing participation beyond index leaders.

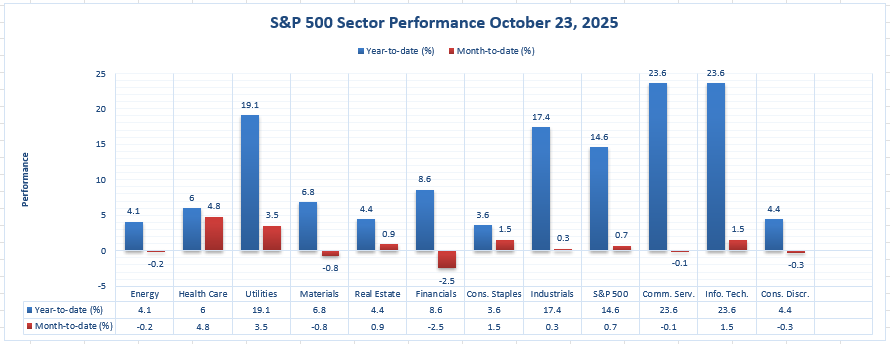

The Strongest Sector in All These Indices

Leaders Focused on Communications Services and Information Technology

With the latest sector scorecard (as of 10/23/2025), we notice that the leadership has remained in a tight group. Year to date, the leaders include Communication Services and Information Technology, tied for first place at 23.6%, leading the S&P 500 at 14.6%. The others in the second tier include Industrials at 17.4% and Utilities at 19.1%, leading the S&P 500. Mid-tier performers include Financials at 8.6%, Materials at 6.8%, Health Care at 6.0%, Consumer Discretionary at 4.4%, Real Estate at 4.4%, Consumer Staples at 3.6%,

Month-to-date, the leaders include Health Care, leading at 4.8%, followed by Utilities at 3.5% and a tie for third place by Information Technology and Consumer Staples at 1.5%. The S&P 500 index has recorded a 0.7% gain, with both Industrials and Real Estate notching small gains of 0.3% and 0.9%, respectively. The sectors that recorded the weakest performance include Materials at -0.8%, Communications Services at -0.1%, Energy at -0.2%, Consumer Discretionary

Our read: The crown for “strongest sector” YTD is split between Communication Services and Information Technology (both 23.6%), while Health Care (4.8% MTD) is the near-term pace setter. At Zaye Capital Markets, we frame positioning around these leaders while benchmarking to the S&P 500’s 14.6% YTD and 0.7% MTD prints, with attention to defensives like Utilities (19.1% YTD; 3.5% MTD) that are participating in both time frames.

Earnings

Earnings Recap – Yesterday (October 24, 2025)

- Procter & Gamble Company (The)

The Procter & Gamble Company (PG) reported Q1 FY2026 sales of $22.39 billion, up approximately 3% year-over-year, with non-GAAP EPS of $1.99, surpassing consensus estimates of around $1.90. The company reaffirmed its full-year earnings guidance of $6.83–$7.09 per share and cited a notable reduction in tariff-related after-tax costs (approximately $400 million) compared to previous levels. These results highlight the resilience of its core consumer categories amid ongoing cost pressures. For us at Zaye Capital Markets, the key watchpoints remain P&G’s ability to sustain pricing power across product lines, manage input cost volatility, and mitigate trade exposure risks under shifting tariff regimes.

- HCA Healthcare, Inc.

HCA Healthcare, Inc. (HCA) delivered a strong quarterly beat, posting adjusted EPS of $6.96 against expectations of roughly $5.72, alongside revenue near $18.5–$18.6 billion. The company also raised its full-year outlook to about $27 EPS and $75–$76.5 billion in revenue. Growth was driven by robust elective procedure volumes, steady patient utilization, and an improving payer mix. We note that this performance underscores the healthcare sector’s continued post-pandemic normalization. The focal points for analysts remain volume sustainability, cost control amid staffing pressures, and any margin sensitivity to potential policy or reimbursement changes.

- General Dynamics Corporation

General Dynamics Corporation (GD) reported Q3 revenue of $12.91 billion, reflecting 10.6% year-over-year growth, and adjusted EPS of $3.88, outperforming estimates near $3.70. The upside was primarily attributed to strong Gulfstream business-jet deliveries and continued expansion of its defense backlog. The results highlight steady momentum across both aerospace and defense segments. At Zaye Capital Markets, we remain focused on the aerospace supply-chain recovery trajectory, order-book visibility, and the potential implications of defense budget realignments amid evolving geopolitical conditions.

- Illinois Tool Works Inc.

Illinois Tool Works Inc. (ITW) announced Q3 EPS of $2.81, exceeding expectations of roughly $2.69, with revenue up about 2.3% year-over-year. Despite modest top-line growth, the earnings beat reflects effective operational discipline and strong pricing execution. Key areas of interest include end-market demand trends across industrial segments, stability in operating margins, and the company’s adaptability to shifting global manufacturing and trade conditions. We view ITW’s consistent margin control and diversified exposure as indicators of enduring industrial resilience.

Earnings Preview – Today (October 27, 2025)

- Welltower Inc. (REIT)

Welltower Inc. (WELL) is set to release its Q3 results after market close, with analysts forecasting FFO of around $1.30 per share and revenue of approximately $2.70 billion. The company previously raised its 2025 FFO guidance to roughly $5.10 per share, reflecting improving operating fundamentals. Key metrics to monitor include occupancy rates across senior housing and healthcare facilities, net operating income growth, leverage ratios, and forward commentary on funding costs. For investors, these data points will indicate how WELL is balancing rate pressures with operational expansion.

- Cadence Design Systems, Inc.

Cadence Design Systems (CDNS) is expected to post Q3 earnings after the close, with consensus targeting EPS of about $1.79 and revenue near $1.323 billion. The focus for investors will be on software demand tied to AI and semiconductor design activity, as well as forward guidance regarding export and tariff exposures. At Zaye Capital Markets, we believe the company’s ability to sustain growth through cyclical chip fluctuations and regulatory headwinds will be key to maintaining premium valuation levels.

- Waste Management, Inc.

Waste Management (WM) is also scheduled to report after market close, with consensus estimates pointing to EPS of approximately $2.02 and revenue around $6.51 billion. Investors should pay close attention to trends in pricing power, recycling profitability, and cost management amid labour and fuel inflation. Guidance on capital expenditures and cash-flow strength will be essential to gauge balance sheet flexibility and dividend sustainability.

- NXP Semiconductors N.V.

NXP Semiconductors (NXPI) will announce Q3 results after the bell, with consensus expectations of EPS at $3.12 (down around 9.6% year-over-year) and revenue at $3.16 billion (down 2–3% year-over-year). The company’s outlook on automotive and industrial chip demand, inventory normalization, and trade-related commentary will be critical. Zaye Capital Markets views NXP as a key bellwether for semiconductor supply-chain dynamics entering 2026.

- Universal Health Services, Inc.

Universal Health Services (UHS) will release its Q3 results post-close. The company continues to see strength in its behavioral health segment, supported by stable patient volumes and improving payer diversification. Analysts will watch for inpatient and outpatient utilization trends, margin control, and Medicaid reimbursement commentary. These indicators remain central to assessing profitability visibility and risk resilience within the broader healthcare landscape.

At Zaye Capital Markets, our outlook remains anchored on guidance strength, margin discipline, and capital allocation clarity as key determinants of post-earnings market reaction.

Stock Market Overview – Monday, 27th October 2025

The United States equity market began the week on a tentative basis, as market sentiment is still delicate, given the dominance, valuations, and macro policies. Despite the pressure on the S&P 500 and Nasdaq, the Dow Jones Industrial Average and Russell 2000 display slight resilience, given the rotation of funds towards defensive and value stocks. Our market outlook at ZAYE CAPITAL MARKETS is still risk on, awaiting market participation.

Stock Prices

Economic Indicators and Geopolitical Developments

The market mood currently is characterized by a level of concern related to concentration and leadership. Market headlines include that the “Magnificent Seven” mega-caps (Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla) are again under pressure, pulling down the entire S&P 500 and Nasdaq Composite index, in a debate related to whether euphoria in the AI world is dissipating. Bond yields remain higher, and trade tensions also continue to pressure markets, leading some market participants to tilt towards lower-beta names.

Latest Stock News

Current trends that are affecting the tech leaders’ narrative include:

- $AAPL pondering Starlink for iPhone – If Apple decides to use Starlink satellite communication, it proves that satellite communication will become the norm for every smartphone user. However, ASTS has already started making efforts for end-to-end communication (voice, internet, video) on every device without any modifications and is also in talks with $T, $VZ, Vodafone, and Rakuten. Although the collaboration between Starlink and iPhone could temporarily cause confusion for ASTS, it will neither alter nor remove the need for global internet connectivity for cell towers that become unavailable.

- $AMZN introducing “Blue Jay” robotics in logistics – The company is launching a new type of robot that is able to perform multiple picks, inside its massive logistics machine, increasing fulfillment density without the need for new buildings. This is pure margin growth inside the moat.

- TSLA’s autonomy stack and “AI5”: Perhaps “AI5,” if it lives up to Elon Musk’s recommendations, will enable TSLA to become less reliant on third-party compute resources, such as Nvidia, and could bring its autonomy stack more fully under its domain. This could, in turn, shape the trajectory and cost for FSD enhancements during autonomous scaling.

- $GOOGL quantum positioning – Google is gearing up for the quantum computer future. Quantum processing does not compete with GPUs, but it’s an additional layer, a type of solution that regular chips can’t provide, and Google wants it for themselves.

- The new frontier for power is in AI centres, where the CEO for Nvidia, Jensen Huang, stated that AI data centres use gigawatts of power. The battle for scale for utility-grade connectivity, not chips, is becoming the value proposition. Those that can provide construction and use the power for AI could prove to be strategic leaders.

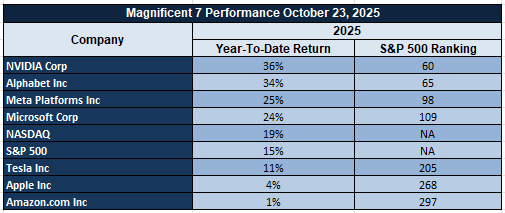

The Magnificent Seven and the S&P 500

The “Magnificent Seven,” consisting of Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla, are again carrying an outsized burden in index gains and are also under intense scrutiny. The group has corrected hard from its recent highs, hurt by concerns of margins, regulatory tensions, and also muted growth outlooks. The weakness in the index leaders is pulling down the S&P 500 and Nasdaq Composite indexes, and it seems that without a rotation in market leaders, it will become difficult for the market to maintain its trends.

Major Indexes’ Performance through Monday, 27th October 2025

- S&P 500: ~6,791.69

- Nasdaq Composite: ~23,204.87

- Dow Jones Industrial Average: ~47,207.12

- Russell 2000: ~2,513.47

The thought process at Zaye Capital Markets has remained that we are in a selective risk-on environment. With mega cap tech showing cracks, spec names resetting, and rate sensitivity rising, the trade has remained to focus on quality names that generate strong free cash flow, demonstrate moats, and benefit from a sector tilt.

Gold Price – Monday, 27th October 2025

The market for spot gold is currently trading around $4,112 per ounce, albeit down from recent peaks exceeding $4,140. The recent pull-back, however, does little to change the fundamental outlook, still well supported by ongoing macro-risk factors and rising levels of geopolitical tension. The monetary policy environment has become clouded by the recent series of market-sensitive comments from the administration. Comments such as “likely no release of inflation data next month” and “inflation is decelerating” have added confusion to Fed policy, suppressing near-term expectations for any bold rate moves. However, the recent monetary backdrop has also seen increasing fiscal uncertainty, from the ongoing shutdown, through the new 10% tariff hike in Canadian products, through to trade tensions in China, ensuring that there is a solid foundation beneath the gold market, through concerned market participants. Although it has also been stated that “constructive trade talks were held in Malaysia,” along with “tensions between the US and China are thawing,” simultaneous statements casting doubt upon urgency for sufficient speed, through a recent probe into China’s Phase One Agreement enforcement, indicate that there’s little clarity in sight. With tariff escalations also in various scenarios, along with escalated tension in Venezuela and along Israel’s borders through Hamas, it’s clear that the delicate market foundation also will continue to support safe-haven investment activity in the gold market. However, simultaneously, yesterday’s economy, as well as low new orders from the regional manufacturing survey from the Kansas Fed, has strengthened concerns for weakening industrial appetite and growth difficulties. This, in turn, has caused allocations to shift away from risk assets, especially since equity markets are still largely driven by a small number of strong performers. The upcoming German IFO Business Climate also contributes to a level of anticipation for the global outlook. If market sentiment in the European region grows weaker, it will only cause the attractiveness for gold, acting as a hedge for global growth slowdowns, to gain strength. Additionally, since there seems to be uncertain conditions concerning inflationary pressures, along with a probability for delayed releases for US economic figures, gold finds itself in a rare narrative support window, sandwiched between weakening disinflation trends and global geopolitics.

Zaye Capital Markets is still convinced that, despite any near-term limited potential for growth for gold without a rate pivot or an inflation shock, there is still a basis for strategic allocations for a hedge for both policy and global growth uncertainties.

Oil Prices – Monday, 27 Oct 2025

Current oil prices are trading in the low $60s per barrel for Brent, indicative of increasing anxiety about the fundamental mismatch between global supplies and demand. The International Energy Agency (IEA) has adjusted its forecast, estimating that global oil supplies will rise by around 3 million barrels per day in 2025 and by a further 2.4 million barrels per day in 2026, while demand growth will only average 700,000 barrels per day each year. This increasing difference has exerted considerable pressure on prices, even amidst periodic geopolitical tensions or efforts by the Organization Petroleum Exporters Countries (OPEC) to cut supplies. Although OPEC is comparatively more optimistic, estimating that global oil demand will grow by 1.3 million barrels per day in 2025, growing discrepancies in forecasts highlight increasing ambiguities in energy use, especially in the developed world. Additionally, the latest information from ZeroHedge and major oil desks accents that rising inventory trends, combined with reduced refining margins, continue to contribute to sullied market sentiments, stuck to fundamental rebalancing instead of temporary shocks. Geopolitics, courtesy of President Trump, is also creating a new dimension for market volatility. The announcement of a 10% tariff hike for Canadian imports, coupled with his murky strike warnings for Venezuela, pose possible supply-side factors, albeit tempered by his quotes on a “thawing relationship” and hopes for a comprehensive China trade pact, downplaying the note-worthy implications for energy markets. The mixed signals are making it difficult to forecast any “precarious” outlook for energy demand, notably if global trade tensions start to take greater tolls on manufacturing production. The economic releases from the U.S. yesterday, pointing to lower new orders for manufacturing, only made it clear that global growth anxieties continue, casting doubt on any forecast for global oil consumption. Additionally, market interest for energy trends in Europe could depend on the German Business Climate Index, expected for release today. If it comes in low, it will only confirm that global growth anxieties and weaker global oil demand can cause lower oil prices, while the reverse can provide a boost.

Bitcoin Prices – Monday, 27 Oct 2025

Bitcoin currently finds itself trading around $111,000 to $112,000, ranging near its recent highs as the market hopes for a new macro or regulatory trigger. The recent BTC rally has also found support from increasing hopes for a positive outcome from the upcoming U.S.-China presidential summit, given headlines featuring “constructive trade talks in Malaysia and hopes for a comprehensive outcome.” This has led to increasing risk appetite in global markets, and Bitcoin has not lagged behind, once again breaking through $113,000. Institutional investment through Bitcoin ETFs, along with institution-buyers, has also added to the positive vibes. Bitcoin, from a technical perspective, does seem to find support around the mid-$110,000 level, wherein chart patterns indicate a possible test for the $115,000 level once again. However, it’s also important to remain alert. The recent words from the White House, including the probability that there will be no inflation data next month, along with assurances from Hassett that “inflation is slowing,” has added to the complexities in the market. This could lower support for Bitcoin, traditionally used for its “inflation hedge,” although it simultaneously lowers any chances for a “hawkish Fed,” making “risk-assets,” once again, look more appealing for the time being. Additionally, tensions related to tariffs, Canada, and Venezuela, also mixed trade talks related to China, continue to lead to a scenario that has traditionally benefitted Bitcoin’s “non-sovereign utility,” thereby making its adoption look appealing once again. Sentiment-wise, the regional manufacturing figures for the U.S. yesterday, especially the fall in new orders, has caused market participants to tread cautiously in equity and commodities markets once again. This will emphasize Bitcoin’s importance as a safe-haven instrument for traditional economic weakness, especially when it comes to confidence in central bank policies. The announcement for the IFO Business Climate Index for Germany will also prove crucial, and any negative figures will confirm market participants’ concerns for a global synchronized slowdown, leading them to continue flowing money into Bitcoin, which can act as a versatile investment option once again. Conversely, strong figures will reduce their enthusiasm for alternative assets, causing Bitcoin prices to remain rangebound. The altcoin market, on the other hand, has remained muted, and its absence has indicated that the ongoing rally is driven by institutional interest.

Eth Prices – Monday, 27 Oct 2025

The present range for Ethereum (ETH) remains around $3,900 to $4,000, although the latest figures indicate it is around $3,933. This is happening after a significant jump in the first week of the month and is currently in a crucial phase where institutional activity is driving the market significantly. This week, analysis on the blockchain has reflected that the “whales,” or the Ethereum accounts that hold 100 to 10,000ETH, accumulated around 218,000ETH, thereby halting several weeks’ net outflows. This is an important indication that the confidence level amongst the “whales,” also believed to drive the market, is increasing. However, the spot ETF for ETH has displayed mixed trends. One aspect is that it has recorded net inflows, thereby demonstrating interest from institutional investors for investing in Ethereum’s ecosystem for the long term. However, it also reflects that a couple of funds recorded net outflows for the past two weeks, thereby demonstrating that, despite confidence, market tension stays temporarily uncertain. The present market scenario, thereby, reflects that although the fundamental scenario for Ethereum continues to remain strong on account of staking income, Layer-2 growth, and usage, it still remains extremely sensitive to market sentiments. Also, it’s important to understand that mixed flows, such as both institutional and ETF inflows, are important for gauging the existing structure for ETH. Institutional flows tend to precede strong bullish action in the cryptos, especially when whale accumulation patterns, such as what we are observing in the market currently, are also in play. The recent ETF outflows, however, indicate that not everyone is convinced, perhaps taking profits from recent strength in ETH or rebalancing for larger-scale macroeconomic releases, such as yesterday’s soft economic indicators in manufacturing and today’s expected release for IFO sentiments in Germany, both of which contribute to the risk premia for cryptos. Were economic sentiments to continue weakening, we could see additional interest in decentralized, fiat, and policy risk hedges like ETH. Were signs of stabilization to appear, the urgency for cryptos could diminish for the near term. To us at Zaye Capital Markets, it seems that the existing conditions for ETH are that it’s in an accumulation and stabilization phase, in that whales are accumulated for strong bullish action, institutions are divided, and it currently holds a tactically important level. If that accumulation pattern continues, along with strong macroeconomic volatilities, we could see Ethereum overcome $4,000 strongly and target $4,250-$4,400 again.