Where Are Markets Today?

European and U.S. stock futures are positioned for a mixed open today, Thursday, former policy expectations. Futures tied to the S&P 500 are trading near flat, while Nasdaq 100 futures have risen by 0.1%, and Dow Jones Industrial Average futures have gained 35 points, or 0.08%. This cautious optimism follows a second consecutive day of record highs for the S&P 500, fueled by Oracle’s strong earnings report, which saw its stock surge approximately 36%, adding $244 billion to its market capitalization. Investors are now focusing on the August Consumer Price Index (CPI) data, scheduled for release at 8:30 a.m. ET, with expectations of a 0.3% monthly increase and a 2.9% annual gain, which could provide insights into future Federal Reserve actions.

One significant factor influencing the market’s direction is the recent unexpected decline in the Producer Price Index (PPI), which fell 0.1% on the month. This has led to speculation that inflationary pressures may be easing, potentially prompting the Federal Reserve to reconsider its current monetary policy stance. Additionally, Oracle’s impressive earnings have bolstered investor confidence, particularly in AI-related stocks such as Broadcom, AMD, and Micron, which have also seen gains. However, the upcoming CPI data remains a critical determinant, as higher-than-expected inflation could dampen expectations for rate cuts, while a weaker-than-expected report might reinforce the case for more accommodative monetary policy.

In Europe, stock futures edged higher early Thursday, with investors awaiting the European Central Bank’s (ECB) interest rate decision. While no major trading updates are expected, the ECB’s stance on monetary policy will be closely scrutinized, especially in light of recent economic data and inflation trends. The ECB’s actions could have significant implications for the eurozone’s economic outlook and investor sentiment across European markets. ECB officials have previously indicated that inflation pressures, while slowing, are still a concern, meaning any hawkish rhetoric could impact market dynamics, particularly in sectors sensitive to interest rates.

Overall, market participants are adopting a wait-and-see approach, closely monitoring economic indicators and central bank communications to gauge the future trajectory of monetary policy and its impact on market dynamics. As investors await further clarity on inflation trends, future rate cuts, and central bank guidance, today’s CPI data will play a pivotal role in shaping market sentiment across both the U.S. and European markets. With earnings reports continuing to drive stock-specific movements, broader indices will look for direction from these key macroeconomic data points.

Major Index Performance Through Thursday, 11th of Sept., 2025

- S&P 500: Trading at 5,841.52, down 0.4% on the day.

- Nasdaq Composite: stood at 18,220.78, down 0.6%, pulled down.

- Dow Jones Industrial Average: Up by 0.2% to 41,182.34, led higher by the energy and banking shares.

- Russell 2000: Underperforming even at 2,147.63 due to small-cap reactivity to.

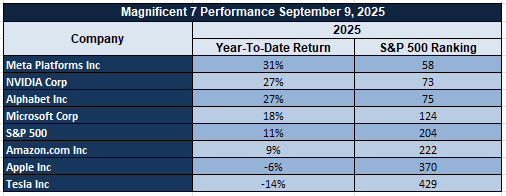

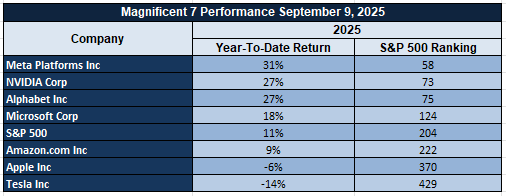

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are showing signs of fatigue. A recent sector breakdown shows the group averaging a drawdown of over 18% from their recent highs, with Tesla and Meta leading the decline. This signals a valuation recalibration, especially in AI-driven growth stories that have run ahead of fundamentals. The S&P 500 remains under pressure as tech leadership wavers. While energy and industrials are offering some support, the index is unlikely to rally sustainably without renewed participation from its core mega-cap drivers.

Drivers Behind The Market Move – Thursday, September 11, 2025

As markets get underway today, there are some key factors driving the sentiment of investors within both the United States and European markets. They consist of the releases of economic information, developments surrounding geopolitics, and policy intentions, and they all determine the positive but cautious market sentiment.

1. Inflation Figures and Hopes for Rate Cut by Federal Reserve

The awaited publication of the August Consumer Price Index (CPI) is a center of focus for investors. Forecasters expect a 0.3% monthly and a 2.9% yearly increase, with core CPI advancing by 0.2% month-to-month and 3.2% year-to-year. These readings are crucial for formulating Federal Reserve policy expectations. Coming off the back of a weaker-than-projected Producer Price Index (PPI) report for August revealing a 0.1% drop, markets are currently pricing a 90% chance of a 25 basis point cut for the Federal Reserve at its next policy meeting. This dovish sentiment is helping underpin sentiment among investors, especially across the growth sectors such as the tech and related AI equities sectors.

2. Geopolitical Risks Affecting Market Sent

Geopolitical events are also contributing their share to market action. President Trump’s criticism of the Israel airstrike over Qatar brought unpredictability into Middle Eastern politics, and it indirectly impacted energy markets and risk appetite of investors. Also, the recent shot down of Russian drones by Poland increased tension over Eastern Europe and volatility within regional markets. These geopolitical threats are forcing investors toward the purchase of safe-haven currencies and commodities, and these markets are affected accordingly.

3. Corporate Earnings and Consumer Behavior Insights

Corporate quarterly earnings reports are providing a window into the behavior of consumers and the health of the economy. Today, company earnings such as Restoration Hardware and Kroger will reveal spending by consumers on necessity items and luxury items. Earnings of Kroger will reflect increased consumption of value-driven items, and earnings of Restoration Hardware will give an indication into the sustainability of the home goods segment despite macroeconomic concerns. These quarterly earnings announcements are critically important for an analysis of the health of the consumer sector and its implications for overall macroeconomic growth.

In short, the day’s movements are determined by a combination of variables such as the performance of inflation, geopolitics, and company results. The investors are paying great attention to the factors as they try and adapt their portfolios amidst the changing economic scenario.

Digesting Economic Data

The TRUMP Tweets and Their Implications

The latest string of comments and tweets by ex-President Donald Trump showcases a combination of political, economic, and global issues, each with consequences for both market sentiment and global geopolitical stability. Trump’s comments relating to the Federal Reserve have been especially significant. His repeated exhortations for Chair Jerome Powell to make large cuts in the interest rates, including his latest assertion that the Fed needs “lower the rate, big, right now,” demonstrate his ongoing anxiety regarding the state of the United States economy. As the latest economic data such as the Producer Price Index (PPI) reflect softer-than-projected figures, Trump’s comments reflect concerns that he thinks hard-hitting cuts in the interest rates can push up growth and alleviate pressure upon the economy. Should the Federal Reserve respond positively to the call, there can be an injection of increased liquidity into the markets favoring risk assets such as equities and cryptocurrencies such as Bitcoin and Ethereum, which do their best where the interest rates are low. Nevertheless, such exhortations can also sow the seeds for inflation fear where the interest cuts are perceived as too harsh and can lead to increased prices for commodities such as gold and oil.

On the geopolitical front, Trump’s remarks regarding international relations have created a new wave of uncertainty, especially related to the airstrike by Israel near Qatar and the Poland situation, where Russian drones were brought down. Trump himself criticized the Israeli strike on Qatar, labeling it a “bad situation” and a danger for U.S.-Qatar relations, and indicated the possibility of increased Middle Eastern diplomatic tensions. That uncertainty could push the safe-haven currencies such as gold and Bitcoin upward as investors retreat from the risk associated with geopolitics. Secondly, the Trump call on the European Union for imposing 100% tariffs on China and India as a tool for pressuring Putin regarding the ongoing Ukrainian conflict could worsen global trade tensions and impact prices of commodities and trigger volatility in the markets. The economic consequences of the same would be experienced across sectors with energy and tech sectors on the receiving end for the increased input cost and overall market sentiment impacted by the higher probability for the disruption of trade. In addition, Trump’s speeches on political violence and his calls for stiffer penalties, including the death penalty for the offenders involved in high-profile cases, can have social impacts, furthering political polarization both within the U.S. and globally. These remarks, along with his video message responding to Charlie Kirk’s assassination, can evoke public opinion and affect social stability and hence market sentiment. An increasingly polarized political environment could increase market volatility, with investors reacting to perceived volatility. Trump’s remarks also serve to signal his intentions to exert significant influence within the politics of the U.S., positioning himself as an authority where economics and foreign policy are concerned. This ongoing influence, along with his policy advice, will continually affect market expectations, particularly up to any potential 2026 presidential campaign.

Trump’s overall geopolitical agenda, in particular, the United States’ relationship with Russia, China, and Israel, will spillover into the global markets. The oil markets, for example, can directly be affected by Trump’s call for EU tariffs for China and India, and could widen the prevailing trade friction and disorder the supply chains. Energy prices, such as oil prices, could surge if the tensions translate into any sanctions or disruptions in supplies, and equity markets could react to the volatility with uncertainty. Investors will want to follow these events very keenly because Trump’s impact continues to determine the economic and geopolitical environment.

U.S. PPI Data Suggests Cooling Inflationary Pressures—Market Implications

The United States (U.S.) Producer Price Index (PPI) Final Demand, ex-food and energy, decreased notably down to 2.6% year-over-year for the month of August 2025, below analysts’ estimated 3.3% and the prior 3.3%. The downward movement is an indication of a potential cooling of wholesale inflation and brought cheer to market participants. The PPI decline fits into broader expectations of weakened inflationary pressures and is supported by a Federal Reserve analysis released back in 2023, where it was analyzed that lowered PPI readings were related to relaxed consumer pricing pressures. As an indicator for investors, it seems where inflation is concerned, it could be going down, and such would be positive for interest-sensitive sectors going forward over the next few months.

The Core PPI, minus the more variable items of food and energy, also experienced a material decline, falling to 2.8% from 3.7% the previous month. This pattern suggests a more stable inflation climate throughout the economy, although it’s worth keeping the existing uncertainties in mind. A 2024 analysis from the Bureau of Labor Statistics voiced concerns over the quality of PPI data, and considering recent revisions to employment estimates that indicated a loss of 818,000 jobs. That puts into question the quality of existing economic indicators and really calls for caution when reading these data sets. For analysts, the point is that despite the PPI drop implying cooling inflation, the gap between producer and consumer inflation should be tracked. Wholesale movements historically translate slowly into the consumer prices because of the distribution and retail markups, and the process lags. Therefore, although PPI could reflect a cooling phase, retail consumers could experience inflationary pressure for a little longer yet. Forecasters should therefore look at sectors such as consumer staples, more immune to the inflationary movements, and technology and industrials, where pricing stability can accelerate consumption for core goods. Stocks such as Nvidia (NVDA) and Tesla (TSLA) are top contenders for taking advantage of the trend, considering their interest for industries of high demand such as AI and energy infrastructure.

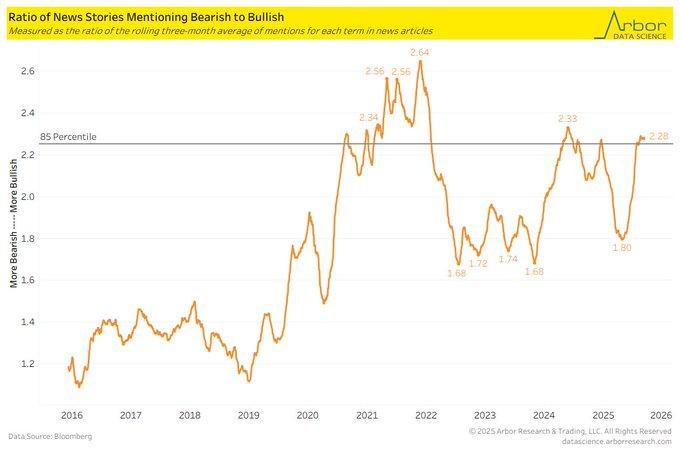

Spike Up in Bullish Sentiment Drives Market Correction Possibilities

Bloomberg News Trends’ latest data, processed by DataArbor, shows a significant surge in bullish news items, up to a bullish-to-bearish ratio of 2.6, and indicative of a change in market sentiment. This is an inverse reaction compared with the usual post-crash prudence following the drop the S&P 500 experienced in April 2025. In the past, such spikes for bullish sentiment quite frequently were followed by market corrections. In a National Bureau of Economic Research study done back in 2019, it was emphasized that a bull-to-bear ratio of more than 2.0 was associated with a 65% probability within a six-month time frame of an approaching downturn because investors’ overoptimism normally creates a pullback within the market.

The consequences associated with such sentiment change are significant for analysts and investors. Although the positive market sentiment at the beginning could initially secure positive momentum, overoptimism can lead to a market reversal, particularly when it diverges too much from the fundamental economic realities. This calls for the investors to be cautious and attentive to changes occurring in the market fundamentals. As we notice the recent surge in the number of bullish sentiments, analysts are ought to anticipate volatility within the upcoming months.

For analysts, monitoring market correction indicators like the VIX (Volatility Index), signs of economic slowdown, and sudden reversals in leading indices will be essential. Stocks in the technology and consumer discretionary sectors that gained from the bullish scenario could suffer if sentiment moves into cautious territory. Stocks with defensive qualities and healthy balance sheets will stand a better chance if there is a correction. Nvidia (NVDA) and Tesla (TSLA) were although leading players that could be at risk for price corrections considering their stretched valuations in a potential sentiment shift scenario.

Slowing Borrowing Costs Provide Relief for Small Businesses

Small businesses’ short-term loan interest rates, on average, were at 8.1% in August of 2025, a significant decline from the recent peaks. The drop is an indication of a loosening of the cost of borrowings, and it could be the outcome of shifts in global economics and monetary policy. OECD data affirms the trend, showing that short-term rates follow the movement of the central bank base interest rate, such as the Bank of England base interest rate. Lower rates of borrowing are a good omen for small businesses, one that could be an indication of better financial health, though global markets reposition themselves.

This change is reinforced by the NFIB’s most recent Small Business Optimism Index, which reported a decline in financing uncertainty, indicating that small businesses are starting to reap the benefits of a soft labor market and reduced borrowing requirements. In particular, only 23% of small business owners borrowed routinely in the month of August, the lowest since the month of November 2021. This is an indication of decreased dependence on borrowing, probably because of decreased expenditure on capital and a more cautious marketplace. The history shows that it is the lowest proportion since the month of May 2023, when aggressive interest hikes were used for the purpose of battling inflation. Since small businesses normally suffer from a lag when benefiting from interest cuts, the early drop is an unexpected but comforting sign of steady economy. For analysts, the issue is that such development can be seen as an early sign of the overall economy easing and could be favorable for industries relying on credit. Small-cap stocks, particularly from industries such as retail and services, which tend to be more sensitive to the financing scenario, could benefit from such lowered cost of borrowing. However, analysts should be cautious because small businesses typically get delayed impact from the shift of interest rates. Companies with stronger financial strength would be better equipped to handle volatility within the broader economy. Stocks like Square (SQ) and Shopify (SHOP), catering to small businesses, could get positive traction as the cost of borrowing lowers.

Seasonal Travel Decline Signals Economic Sensitivity in 2025

Latest data reflect a mid-2025 high for TSA passenger volume followed by the seasonal decline for the month of September. That pattern mirrors the same patterns as the 2021 TSA seasonal travel trends report where September declines for travel were customarily linked with back-to-school spending and end-of-summer lethargy. Despite the decline, however, TSA volume remains higher than it was pre-pandemically and yet suggests continuing resilience for travel demand though spending remains tempered by economics.

According to a 2023 Federal Reserve report, consumer spending on travel typically drops by 15% in September due to the financial strain of back-to-school expenses and the post-summer lull. This seasonal dip, despite high demand, challenges the narrative that the travel sector is experiencing a post-2020 slump. Global passenger numbers for 2025, as reported by the International Air Transport Association (IATA), are projected to exceed 2019 levels by 8%, indicating robust long-term resilience in the travel industry. This resilience suggests that, despite typical seasonal fluctuations, the demand for travel has remained strong, contributing to the sector’s recovery and growth post-pandemic. For analysts, the seasonal drop off in travel must be considered within the context of broader economics. Though short-term decreases in travel activity are inevitable, the overall landscape is bullish, and airlines, hospitality, and travel stocks are poised for the eventual recovery over the longer term. Investors must look to firms with dominant market positions and the capacity to absorb off-peak seasonal downturns, especially those firms diversifying their revenue streams. Air carriers such as Delta (DAL) and booking websites such as Expedia (EXPE) are poised to reap the ongoing strength of the recoveries within the travel sector even as short-term volumes within the travel sector suffer small decreases within the month of September.

Retail Recovery for the U.S. Continues Firm Growth Despite Prolonged Inflation

The Johnson Redbook Index reported a strong +6.6% same-store SAAR year-over-year same-store sales growth for the year 2025, a considerable bounce back from earlier drops. This comeback is evidence of the resilience of the retail industry after a rough stretchduring the pandemic of 2020 when retail sales dipped by as much as 15% through extensive lockdowns. Though the comeback is impressive, it is worthwhile to comprehend the drivers behind the growth. A PwC UK retail forecast report for the year 2025 highlights the strong performance through the grocery and leisure channels through reduced inflation and strong holiday sales. Nevertheless, despite the encouraging signs, the sustained inflation ranging from 2-3% for the year 2025 estimated by the ONS remains a limiting factor for broader consumption and thus the potential growth for most retail businesses.

In comparing U.S. and U.K. retail trends, it’s clear that regional factors influence the pace and scope of recovery. The Johnson Redbook Index, which has tracked retail performance in the U.S. for over 40 years, suggests steady recovery in key sectors, despite inflationary pressures. On the other hand, the U.K. faced a dramatic number of retail closures in 2024, with 7,537 store closures recorded, according to the Centre for Retail Research. This stark contrast highlights the ongoing struggles in U.K. retail, driven by factors such as higher operating costs, consumer behavior shifts, and post-pandemic economic adjustments. The U.K.’s retail sector is grappling with more closures and subdued growth, while the U.S. retail market shows signs of recovery, particularly in specific categories like groceries and leisure goods. For analysts, the overall conclusion is that although the U.S. retailing sector continues apace, driven by sector-specific demand and consumer recovery, the United Kingdom market is more challenged, with a higher store-closure rate. Analysts need to zero in on the supermarket and entertainment industries within the United States, where retail growth seems to be emanating from. Broader growth within the sector might, however, remain restrained owing to ongoing inflation pressures. Investors need to consider firms that possess sound bases among consumers within such industries where growth is evident, such as within Walmart (WMT) and Target (TGT), both of which are poised for ongoing retail recovery irrespective of headwinds within the economy.

Upcoming Economic Events

Main Refinancing Rate, Monetary Policy Statement, Core CPI m/m, CPI m/m, CPI y/y, Unemployment Claims, ECB Press Conference

As we head into another crucial week, market participants are bracing for a series of important economic events that could influence both short-term and long-term market sentiment. With inflation data, unemployment figures, and central bank decisions all coming into play, investors will be keeping a close watch on these indicators. The European Central Bank (ECB) monetary policy statement and inflation reports, in particular, will be key drivers in shaping investor expectations. Here’s a comprehensive breakdown of what to watch for, how each data point could impact market behavior, and what the market might expect if the actual results come in higher or lower than forecasts:

Main Refinancing Rate & Monetary Policy Statement (ECB)

The Main Refinancing Rate and the accompanying Monetary Policy Statement from the European Central Bank (ECB) are set to dominate the focus today. This event is a significant barometer for gauging the ECB’s stance on inflation and economic growth in the Eurozone.

- If the ECB raises the Main Refinancing Rate beyond expectations, this could signal that the central bank is becoming more aggressive in its efforts to tame inflation. In such a scenario, the euro would likely strengthen, driven by expectations of higher yields on euro-denominated assets. Meanwhile, equities might face pressure, particularly in interest-sensitive sectors such as real estate, utilities, and consumer staples, as higher rates increase borrowing costs and dampen economic growth.

- Conversely, if the ECB decides to lower rates or signals a dovish tone, the euro could weaken significantly as investors adjust their expectations for a prolonged period of low interest rates. Such a dovish outlook could also stimulate a relief rally in risk assets like equities, as lower borrowing costs would support economic activity and corporate profitability. Bond yields could also decline, further easing financial conditions in the Eurozone. Analysts will be focused on any forward guidance provided by the ECB in its Monetary Policy Statement; comments suggesting more accommodative policy measures could be supportive for stocks and risk assets in general.

Core CPI m/m, CPI m/m, CPI y/y (U.S.)

The release of U.S. Core CPI m/m, CPI m/m, and CPI y/y data will be closely scrutinized as the market continues to navigate inflationary pressures.

- A higher-than-forecast CPI reading could reignite concerns about persistent inflation and prompt the Federal Reserve to maintain or even accelerate its tightening stance. In such a scenario, the U.S. dollar would likely strengthen due to expectations of higher interest rates, while equity markets might face a pullback, especially in sectors sensitive to inflationary pressures, such as consumer discretionary and tech. Higher inflation would further bolster market speculation that the Fed may continue to raise rates to combat price pressures, which would also push bond yields higher as investors price in more aggressive monetary policy.

- On the other hand, if the CPI readings come in lower than expected, it could signal that inflationary pressures are easing, offering some relief to investors. A soft CPI print would likely increase expectations for a dovish Federal Reserve, prompting a rally in risk assets, especially equities. Lower inflation would support expectations for rate cuts or pauses in the Fed’s tightening cycle, which could fuel further gains in growth and technology stocks. The U.S. bond market could also see a rally, with yields dropping as expectations for higher rates wane. Investors would likely interpret a softer-than-expected inflation print as a positive signal for both the economy and corporate earnings, encouraging a shift back into cyclical and growth-oriented stocks.

Unemployment Claims

The release of Unemployment Claims will offer a critical snapshot of labor market health.

- A lower-than-forecast unemployment claims figure would suggest that the labor market remains resilient, with fewer people relying on unemployment benefits. This could indicate that consumers are still spending robustly and that the broader economy is holding up well despite inflationary pressures. A strong labor market would likely boost confidence in cyclical sectors such as consumer discretionary, financials, and industrials, while also supporting a generally positive sentiment across equity markets. However, a lower-than-expected claims number could also trigger concerns about wage inflation, which would put further pressure on the Fed to maintain a hawkish stance to curb inflation, particularly in sectors like labor-intensive industries.

- If unemployment claims rise above expectations, it would signal a softening labor market, which could reinforce the view that the economy is cooling. In such a scenario, safe-haven flows would likely increase, with investors shifting towards defensive sectors such as healthcare, utilities, and consumer staples. Bonds would likely benefit from this shift, with yields coming under pressure as the market re-prices expectations for economic slowdown. A sharp increase in claims could also dampen sentiment towards risk assets, triggering a flight to safety in the U.S. Treasury market.

ECB Press Conference

The ECB Press Conference will follow the monetary policy decision and provide valuable context for interpreting the ECB’s stance on inflation and economic growth.

- If President Christine Lagarde adopts a hawkish tone, signaling that the ECB is committed to tightening monetary policy further, the euro is likely to appreciate, and bond yields in the Eurozone could rise as investors adjust to the prospect of tighter financial conditions. A hawkish press conference would likely pressure equities, particularly in interest-sensitive sectors, as higher rates would weigh on economic growth.

- On the other hand, if Lagarde adopts a dovish tone, indicating concerns over economic growth and the potential need for more accommodative measures, equities could experience a relief rally, especially in risk-sensitive sectors. A more dovish stance could also weaken the euro as markets price in expectations of prolonged low rates. In either case, the ECB press conference will provide important color on the central bank’s outlook for the Eurozone economy, which will be crucial for shaping both currency and equity market movements.

As we prepare for today’s key events, the market’s reaction will largely depend on whether actual results deviate from forecasts. Higher-than-expected inflation or employment data could fuel fears of persistent price pressures, leading to a more hawkish stance from central banks and a shift towards risk-off sentiment. On the other hand, weaker-than-expected data could prompt a rally in risk assets as expectations for policy easing rise. Keep a close watch on these data points, as they are likely to set the tone for market movements in the coming days.

Stock Market Performance

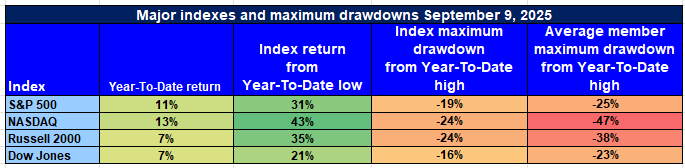

Indexes Recover from April Bottoms, But Sensitive Breadth Continues Cautionary Indication

Domestic equity markets have managed a significant recovery off the April 8th lows but for the foreseeable future, there are persistent signs of fragility lurking beneath the surface. Even though leading indexes reported positive performance year-to-date, the related underlying individual constituent drawdowns signal a lack of universal market participation and therefore prudence continues to be the better part of valor.

Here is our summary of the latest performance through the main indexes:

S&P 500: Decent Recovery, But Breadth Still Relatively Narrow

YTD: +11% | +31% off April low | -19% off YTD high | Avg. member: -25%

The S&P 500 experienced robust performance through the year 2025, rising by 11% year-to-date and a significant 31% since their April lows. But with an 19% decline from the YTD high and an average member decline of 25%, the index is heavily reliant on the performance of some giant-cap stocks. The advances show strength at the index level but the overall market taking part is minimal and with many members disappointing.

NASDAQ: Strengthened Recovery, Yet Cautious Expansion

YTD: +13% | +43% below April low | -24% off YTD high | Avg. member: -47%

The NASDAQ has been the clear victor, rising 13% year-to-date and recovering 43% from the April low point. Even with the remarkable reversal, the 24% retreat from its YTD high and alarming-looking 47% avg member loss are a sign that tech-heavy index growth continues to be sporadic. The gulf between the index itself and individual stocks also suggests continuing weaknesses and vulnerabilities within the overall tech sector itself.

Russell 2000: Small-cap Recovery Comes into View

YTD: +7% | +35% below April low | -24% below YTD high | Avg. member: -38% The Russell 2000 has enjoyed a respectable 7% year-to-date performance and recovered emphatically by 35% from April lows. Yet its 24% drop from the YTD top and an average member loss of 38% are signs of lasting strain on small-cap shares. That implies that small-cap shares experienced some kind of comeback but investors’ hopes are still thin, especially where more economically sensitive shares are concerned.

Dow Jones: Defensive Bias Offers Stability

YTD: +7% | +21% below April low | -16% below YTD high | Average member: -23% Dow Jones continues to derive advantage from defensive make-up, rising 7% year-to-date and climbing 21% off its April trough. Registering only a relatively decent 16% pullback from the YTD top, the index held up fairly well. Nevertheless, the average member’s 23% pullback still reflects tension within individual issues even within normally stable, value-weight sectors.

At Zaye Capital Markets, we continue to favor quality names with strong balance sheets and resilient earnings streams. The broader market remains fragile, and we are monitoring the breadth of the rally closely, looking for confirmation that more stocks are participating in the upward movement before becoming more aggressive in our positioning.

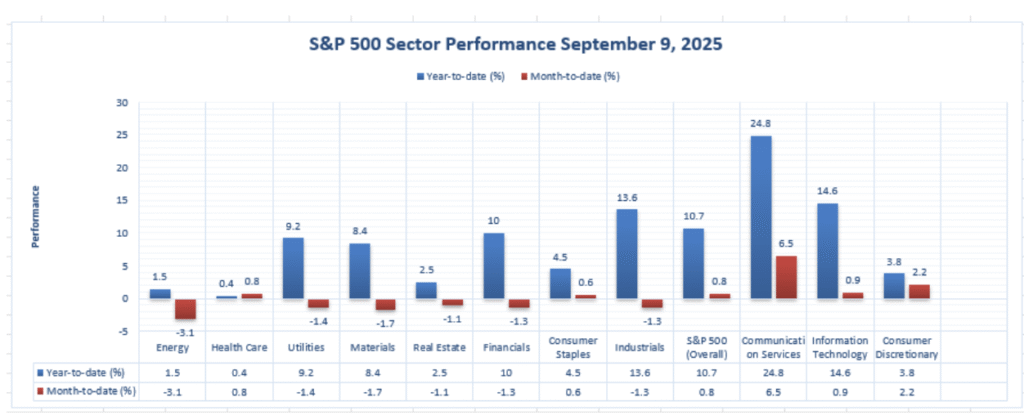

THE STRONGEST SECTOR IN ALL THESE INDICES

Sector Leadership Makes Sense, But Breadth and Drawdowns Require Discipline

In Zaye Capital Markets, we see an unequivocal lead emerging among significant benchmarks, and sector performance offers clear leading indicators where risk-adjusted momentum proves strongest. Although the broader indexes staged significant rallies since early April, the best-performing sector shines not only through the year-to-date performance, April 8 rebound off the low, and comparative drawdown map, but also through the depth and risk exposure within the sector. The combination suggests selective positioning over broad market exposure.

Top Sector Summary (from your chart data):

- Year to Date performance: +24.8%

- Rebound from the 4/8/25 low: +43

- Maximum drop since YTD high: -24% (Communication Services)

- Average member worst month drop: -47% (Communication Services)

Communication Services tops the chart with an impressive 24.8% YTD showing, and a 43% recovery from the April 8th low, demonstrating leadership resilience. Nevertheless, the sector’s 24% highest drawdown from the YTD highs and the 47% median member pullback mark the dangers of slender participation where the sector’s headlining performance isn’t consistently replicated by its members individually. Although such an outperformance by the sector is a sign of lasting leadership, the significant pullbacks are indicative of the volatility and thus the call for prudence.

We believe Communications Services are priced too low relative to their earnings durability and cash-flow clarity, and particularly relative to broader indexes where median member losses remain elevated. Sector analysts should monitor sector breadth (advancers and decliners), revision trends within earnings, and the fundamental underpinnings for such leadership. Allocation should focus on quality within the sector where there is focus on the well-capitalized, earnings-certain businesses versus pursuing broader market beta or growth via speculation. The strategy will allow the investors to participate in sectoral leadership and stay disciplined against volatility.

Earnings

Earnings Report: September 10, 2025

- Chewy, Inc. (NYSE: CHWY)

On September 10, 2025, Chewy, Inc. reported its Q2 2025 results, revealing a year-over-year sales growth of 8.6%, reaching $3.10 billion. However, net income declined to $62.0 million, with diluted earnings per share (EPS) at $0.14, compared to $0.68 in the previous year. The drop in earnings was primarily due to increased share-based compensation expenses. Despite the earnings miss, Chewy raised its full-year revenue forecast to $12.5–$12.6 billion. The stock saw a 15% decline following the announcement, possibly driven by high investor expectations despite a strong revenue increase.

- National Beverage Corp. (NASDAQ: FIZZ)

National Beverage Corp.’s Q1 2026 earnings report is scheduled for release before the market opens on September 11, 2025. The company is expected to report revenue of approximately $354.18 million. Investors are looking to see how the company’s flagship brand, LaCroix, performs amidst ongoing challenges. The market will also be closely watching any updates on the competitive dynamics in the beverage sector, as National Beverage faces stiff competition in the sparkling water and flavored beverage space.

- Daktronics, Inc. (NASDAQ: DAKT)

Daktronics, Inc. posted strong Q1 2026 results, with net sales of $219 million, exceeding the FactSet estimate of $196.9 million. The company reported net income of $16.5 million, compared to a net loss of $4.9 million in the same period last year. Orders rose 35% year-over-year, and operating cash flow surged 34% to $26 million. The company’s performance reflects strong demand in the electronic display sector, with improved financial stability, as Daktronics closed the quarter with a cash balance of $137 million.

- Tsakos Energy Navigation Ltd. (NYSE: TNP)

Tsakos Energy Navigation reported its Q2 2025 net income of $26.8 million, or $0.67 per share, with revenue of $193.3 million. The adjusted revenue stood at $161.4 million. The company also declared a dividend of $0.60 per share in July 2025. Despite ongoing challenges within the shipping industry, the company has maintained a strong financial position, benefiting from high demand for tankers and robust fleet utilization.

- Oxford Industries, Inc. (NYSE: OXM)

Oxford Industries’ Q2 2025 earnings revealed a 4% decline in net sales, with total revenue at $403 million. However, the company posted adjusted earnings per share of $1.26, which exceeded the company’s previous guidance. The Lilly Pulitzer brand showed strong performance, while the Tommy Bahama line faced difficulties due to less favorable spring and summer collections. Despite these challenges, Oxford maintained its full-year sales and profit guidance, signaling confidence in its ability to manage market pressures.

Earnings Due Today: September 11, 2025

- Adobe Inc. (NASDAQ: ADBE)

Adobe Inc. will release its Q3 FY2025 earnings after market close on September 11, 2025. Analysts expect Adobe to report total revenues between $5.87 billion and $5.92 billion, with adjusted earnings per share ranging from $3.00 to $3.05. Investors will focus on the performance of Adobe’s digital media segment, especially its Creative Cloud and Document Cloud services. Additionally, Adobe’s efforts in integrating AI technologies into its software products will be key factors that analysts will look for, particularly how this impacts customer growth and engagement.

- Kroger Co. (NYSE: KR)

Kroger is scheduled to report its Q2 2025 earnings at 10:00 a.m. ET on September 11, 2025. Analysts expect the company to report revenue of approximately $34.6 billion. Key metrics to watch include same-store sales growth, digital sales performance, and how inflation impacts consumer behavior. As one of the largest grocery chains in the U.S., Kroger’s performance will provide valuable insights into the state of consumer spending, particularly in the retail and food sectors, as well as the ongoing trends in the grocery business.

- National Beverage Corp. (NASDAQ: FIZZ)

As mentioned earlier, National Beverage is expected to report its Q1 2026 earnings today, with revenue expected to be around $354.18 million. Investors will look for updates on the performance of LaCroix, as well as any new strategies or products that could help the company navigate the competitive beverage market. The company’s ability to innovate and maintain strong consumer demand will be crucial for its ongoing performance, especially as competition in the sparkling water segment intensifies.

- Kestra Medical Technologies, Ltd. (NASDAQ: KMTI)

Kestra Medical Technologies is also set to report its earnings today, September 11, 2025. Investors will focus on the company’s progress with its medical device pipeline, especially the launch of any new products, regulatory approvals, and partnerships that could boost future growth. Any insights into the company’s financial health, particularly related to capital expenditure and R&D investments, will be key to understanding its position within the medical technologies sector moving forward.

At Zaye Capital Markets, we continue to monitor these earnings reports closely, as they offer valuable insights into company performance and broader market trends. Investors should pay close attention to earnings results, forward guidance, and key factors driving performance in these industries.

Stock Market Update – Thursday, September 11th, 2025

The US stock markets started the day on the defensive since there were concerns amongst investors regarding the newest economic indicators and global developments. The Nasdaq Composite and S&P 500 gave up some grounds, and the Dow Jones Industrial Average remained steady. The Russell 2000 remained on the backfoot amidst the uncertainty cloud over the economy.

Stock Prices

Geopolitical Events and Economic Indicators

The market’s cautious tone is attributed to a combination of factors. The U.S. economy added only 73,000 jobs in July, significantly below expectations, raising concerns about labor market strength. Additionally, President Trump’s recent imposition of tariffs on imports from several countries has heightened trade tensions, contributing to market volatility. These developments have led to increased risk aversion among investors, impacting market performance.

Latest Stock News

There were notable movements observed from some companies throughout the day, with information and moves that are driving sentiment within the market today:

- $UBER: Uber is taking a mega step forward as it integrates Joby Blade Helicopter flights within the app, diversifying its transport offerings and seizing the emerging market for aerial mobility for urban populations. This Joby Aviation deal further diversifies the Uber portfolio and moves the company toward being a more diversified transport and logistics platform.

- $CRWD: Crowdstrike has teamed up with Amazon Business Prime to offer Falcon Go, which will be available free for Amazon Prime Business tiers. Normally priced at $59.99 per device, this collaboration is strategically aimed at seeding small-to-medium-sized businesses with cybersecurity tools as AI-powered solutions gain ground. With 89% of businesses still ransomware-exposed, this move could drive adoption among SMBs.

- $NBIS: NeuroBo Pharmaceuticals announced a $3 billion financing consisting of a $2 billion private convertible notes offering and a $1 billion Class A offering. The stock shot up, crossing over $100 for the first time, which suggests investors were optimistic. Zaye Capital Markets views the scenario as an opportunity to buy on any significant drop and that is precisely the situation considering the growth potential within neurodegenerative disease treatments.

- $AMZN: Amazon is said to be working on AR glasses under the project code-name “Jayhawk” for a head-to-head with Meta and Apple. The transportable glasses would get Alexa off the kitchen counter and into an AR-powered, more transportable system, and it could dramatically change the user interaction within Amazon’s platform.

- $HIMS: Hims is growing its men’s health product line with the addition of oral testosterone. Product comes off the back of a success with other health products such as balding and ED treatments, and the goal is to keep customers locked into the platform through a recurring, high-demand pipeline.

- $OPEN: OpenAI brought in Shopify COO Kaz Nejatian as its new CEO, and founders Keith Rabois and Eric Wu returned to the board. The move could usher a growth phase for the company as it builds up its ability and innovation pipeline for AI.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are showing signs of fatigue. A recent sector breakdown shows the group averaging a drawdown of over 18% from their recent highs, with Tesla and Meta leading the decline. This signals a valuation recalibration, especially in AI-driven growth stories that have run ahead of fundamentals. The S&P 500 remains under pressure as tech leadership wavers. While energy and industrials are offering some support, the index is unlikely to rally sustainably without renewed participation from its core mega-cap drivers.

Major Index Performance Through Thursday, 11th of Sept., 2025

- S&P 500: Trading at 5,841.52, down 0.4% on the day.

- Nasdaq Composite: stood at 18,220.78, down 0.6%, pulled down.

- Dow Jones Industrial Average: Up by 0.2% to 41,182.34, led higher by the energy and banking shares.

- Russell 2000: Underperforming even at 2,147.63 due to small-cap reactivity to.

At Zaye Capital Markets, we are monitoring sector rotation and positioning strategies very closely as the earnings season continues. Whether or not top companies are able to sustain earnings growth through tightening policy will shape the direction for broader equity markets through Q3.

Gold Price – Thursday, September 11, 2025

Up to the present day, September 11, 2025, gold continues close to its recent peaks, currently trading at around $3,636.59 an ounce, slightly lower from the day’s high of $3,673.95 earlier this week. The December gold futures price is also firm at $3,676.40 an ounce, showing some volatility but still showing high investor appetite for the yellow metal. The lift for gold is mainly attributed to investors’ hopes that the Federal Reserve will more than probably cut interest rates following weaker-than-projected economic data, especially the disappointing Producer Price Index (PPI) and jobs growth estimates that were lower than anticipated. Lower interest rates cut the opportunity cost of holding unproductive assets such as gold, and investors seeking cover for a potential economic slowdown now find it more worthwhile investing in gold. The prospective cut in the interest rate is likely to be reaffirmed at the upcoming Federal Reserve monetary policy meeting scheduled for September 17, and such hopes normally trigger a rush for gold purchases. In addition, the weaker dollar coupled with the higher purchases coming from central banks, especially China and India, has been another upward boost for gold’s prices, belying its position as the first-choice diversification and hedging asset. Aiding gold’s attractiveness, geopolitical risk is contributing notably to its recent rally. President Trump’s latest remarks, wherein he criticized Israel’s Qatar airstrike as “counterproductive” to American-led peace initiatives, have brought volatility into the already sensitive geopolitical arena. Any escalation of tension, especially in the Middle East, increases purchases of safe-haven goods such as gold. That is because investors want cover amidst the uncertainty of global relations. Furthermore, concerns toward the United States CPI and unemployment claims reports scheduled for the week ahead will be pivotal for future sentiment toward the Federal Reserve’s monetary policy. A stronger-than-projected CPI reading can calm hopes for a cut in interest rates, thus placing downward pressure on gold. In the alternative, if the reading disappoints for the second month running, the argument for an interest rate cut can gain traction again, stoking further upside for the metal. Economic indicators and the political situation will for the foreseeable future lead gold’s direction, and investors will heed these indicators for further direction for the precious metal.

Oil Prices – Thursday, September 11, 2025

As of September 11, 2025, the prices of oil are going through volatility influenced by the combination of geopolitical risk and economic data. Brent crude currently sells at around $67.50 a barrel and West Texas Intermediate (WTI) at $63.69 a barrel. These are conditioned by a number of factors. Geopolitics like the airstrike by Israel on Qatar brought into the market an element of uncertainty, and there are the fears of disruption of oil supplies. Also, President Trump’s recent remarks calling for the European Union to apply 100% tariffs on China and India for their purchases of Russian oil have created an element of complexity for the world trade and could impact the prices of oil. On the economics front, the recent data that producer prices decreased and employment grew raised hopes for an interest rate cut by the Federal Reserve, which could impact oil demand and prices. Going forward, the day’s economic data, such as the Consumer Price Index (CPI) and unemployment claims, will be instrumental in forming market sentiment. Higher-than-expected CPI could temper hopes for a cut in interest rates, and thus could put downward pressure on oil prices. Nevertheless, weaker-than-expected CPI and jobs claims could support the argument for an interest rate cut and add tailwinds for oil prices. The International Energy Agency (IEA) too has also raised concerns over the possibility of an oversupply situation emerging for oil, and it expects a hefty build-up of inventories over the coming months amidst weaker-than-expected demand and a pick-up in supplies. The forecast, therefore, is for oil prices to experience downward pressure if the expected supply surplus comes through. Market players and investors will be watching these economics and geopolitical situations very keenly and assessing their impact on oil prices over the short term.

Bitcoin Rates – Thursday, September 11, 2025

Today, Bitcoin (BTC) is hovering around $114,115, up by 2.33% compared to the previous day’s close. This Bitcoin price jump comes after a bumpy market day, where the cryptocurrency touched an intraday high of $114,427 and a low of $111,399. The upward push is primarily driven by rising hopes for a cut in the Federal Reserve interest rates. In the PPI data released, where the number depicted a minor drop of 0.1%, the concerns of inflation were quelled and the possibility of the Fed cutting monetary policy in the upcoming meetings was sparked. Lower interest rates generally lower the opportunity cost for holding non-interest-bearing assets like Bitcoin, and thus the cryptocurrency appears more attractive for both retail and institutional buyers. Besides, global geopolitics, including President Trump’s latest criticism of the Israel airstrike upon Qatar and increased tension regarding Russia’s moves in Europe, have created uncertainty within the financial markets. When the situation is unstable geographically and economically, investors flock into the shelter of currencies like Bitcoin perceived as a store of value away from mainstream financial channels. Together, all these factors—economic data, speculation regarding the Fed, and geopolitical turbulence—are all contributing significantly toward Bitcoin’s price movement and sentiment within the market over the past few days. Next up is attention for upcoming economic data, specifically the Consumer Price Index (CPI) and unemployment claims data, both of which will shed more light on the inflationary trends and labor market fundamentals. A higher-than-expected CPI reading would most likely temper hopes of a large cut by the Fed and could place downward pressure on Bitcoin prices as the narrative moves toward tighter monetary policy. Alternatively, if the CPI and unemployment jobs data arrive weaker than expected, the argument for a cut by the Fed would firm up and lend support toward additional bullish movement in Bitcoin prices. Also acting on sentiment will be ongoing geopolitical developments, specifically any and all that revolves around trade policy or renewed tension among the global powers, which could push investors toward the safer havens such as Bitcoin. As the market digests today’s economic data and moves forward toward Fed meetings, the direction of Bitcoin prices continues tied up with the broader macroeconomic and geopolitical considerations and offers both opportunity and risk for investors alike.

ETH prices – Thursday, September 11, 2025

As of today, Ethereum (ETH) is at $4,412.15 and registered a gain of 2.37% compared to the previous close. This was after Ethereum reached an intraday high of $4,448.54 and a low of $4,298.67. The positive pricing is mainly attributed to rising investment sentiment related to the Federal Reserve’s monetary policy following the easing of inflation concerns signaled by the drop of 0.1%, as indicated by the released PPI data. Since the reduced interest cost of holding non-income paying assets like Ethereum outweigh the benefits of holding cash and bonds, and especially with the Federal Reserve scheduled for a meeting where it could cut interest rates, the reduced interest rate prospects would attract institutional and retail investors alike, causing the asset’s price to increase. Ethereum is also riding the wave of general market sentiment since the rising global market uncertainty, such as the latest criticism of Israel’s airstrike on Qatar by President Trump, creates increased risk appetite among investors seeking alternative storehouses like ETH for their investments. In light of all these, the conducive state for Ethereum is leading to the increase in its price. Ahead, the day’s economic releases, such as the Consumer Price Index (CPI) and the unemployment claims, will be an essential determinant of market sentiment going forward. Should the CPI data turn up higher than forecasted, it would curb the prospects of a large interest rate cut by the Federal Reserve and could lead Ethereum prices to pull back. However, should the CPI and the jobless claims reading turn up weaker than expected, it will make the argument for the cutting of interest rates more compelling and could support Ethereum’s upswing further. Moreover, whales and big-ticket institutional investors also remain the dominant factor behind Ethereum’s pricing, with more purchases by large buyers on an aggregate scale working as a prime motivator for the ongoing upswing. As Ethereum continues to attract renewed interest among retail buyers and institutional investors alike, any emerging news regarding the monetary policy front or global conflicts could serve as an additional motivator for the direction of prices. Investors and traders alike will be forced to scrutinize the aforementioned economic releases and market dynamics because they will very probably serve as the determinants for Ethereum’s short-term direction amidst an increasingly turbulent climate.