Where Are Markets Today?

U.S. and European futures are edging quietly higher this morning, as a result of wary optimism following the close of the Nasdaq Composite at a new high. Dow Jones futures gained 0.13%, with S&P 500 and Nasdaq 100 futures gaining 0.12% and 0.11%, respectively. Euro Stoxx 50 and DAX futures are softer in Europe by around 0.15–0.2%, with the FTSE 100 little changed. Overall, the picture is building toward a quiet but judicious open across the world’s leading equity markets as investors position themselves ahead of essential inflation data this coming week.

First catalyst underlying this tone is the outlook that the Federal Reserve is about to loosen policy. The softer U.S. labor report last week reinvigorated rate-cut expectations, putting investors’ attention firmly on this week’s releases of the Producer Price Index and Consumer Price Index. Any indication of weaker inflation would provide affirmation of the dovish move, bolstering U.S. and Eurozone equities. Stronger-than-anticipated prints, however, may instantly reverse direction, bolstering caution in futures pricing.

The second factor lies in the backdrop of global politics and sector-specific developments. Leadership changes in Japan, France, and Argentina, coupled with policy shifts in Indonesia, have injected uncertainty into global markets. Yet this geopolitical turbulence is being overshadowed by the strong U.S. policy narrative, with futures also buoyed by momentum in high-profile stocks such as Nvidia and Robinhood—particularly after the latter’s inclusion in the S&P 500 index. Anticipation around Apple’s iPhone 17 launch is also lending support to sentiment in the tech-heavy Nasdaq. Lastly, supportive signals in futures and bonds are forging futures direction. The prices of oil are stable after the smaller-than-projected OPEC+ production hikes while the U.S. Treasury yields remain at five-month lows, loosening financial conditions. Combined, the two continue to support valuations in equities and offer another safeguard against risk appetite. At the Zaye Capital Markets, we see this futures formation as range-bound but stable with the rate outlook serving as the ultimate anchor. The next significant move will be determined based on inflation readings that either sustain or test the current dovish consensus.

Major Index Performance – Tuesday, September 9, 2025

- S&P 500: Moderately higher trading, up near 0.2.

- Nasdaq Composite: Outperforming, up roughly 0.4–0.5% and testing record levels.

- Dow Jones: Advanced by around 0.2%, with gains in energy and financial stocks.

- Russell 2000: Little changed to slightly better at +0.1%, as small caps are hamstrung by interest rate sensitivity.

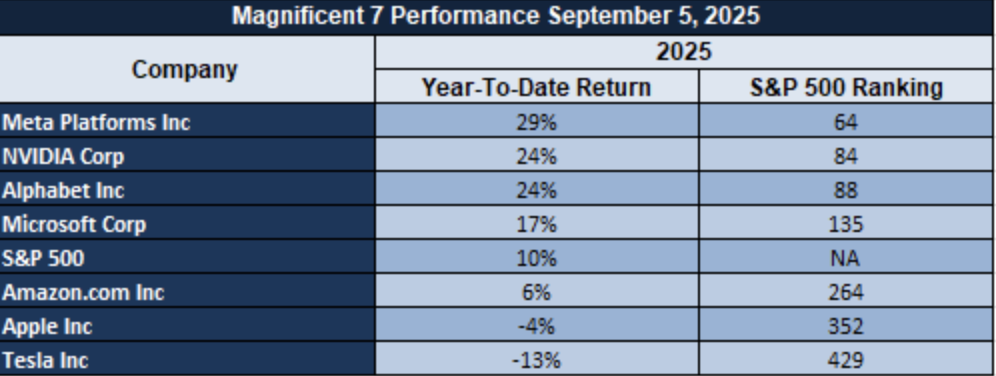

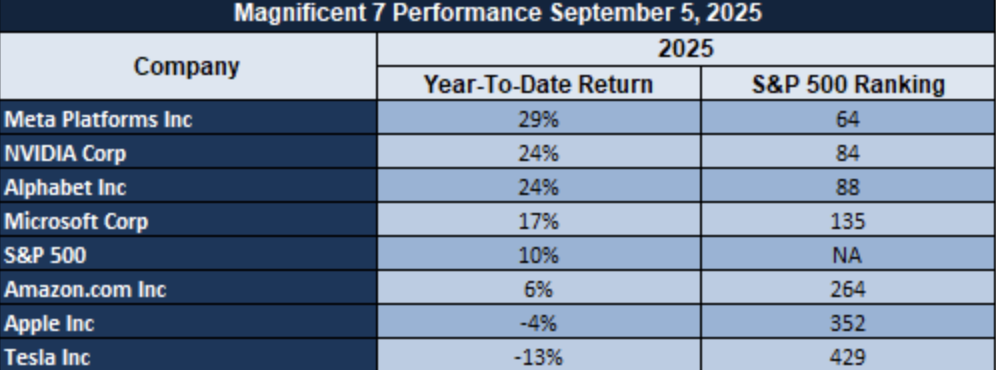

The Magnificent Seven and the S&P 500

The Magnificent Seven continue in the spotlight as rising data-center and silicon investment pressures release the near-term free cash flow. Compounded with valuations and regulation concerns, this sees weakness spread through swathes of the group. The S&P 500 finds difficulty breaking through the top in the absence of their full contribution. A weaker CPI tomorrow would see numerous pressures ease and leadership re-ignite, but a hotter print would extend the phase of de-risking in high-duration tech stocks.

Drivers Behind the Market Move

We at Zaye Capital Markets identified the three main drivers of the day’s U.S. and European market movements from the current events:

1. Hopes of Fed Easing as Labor Market Stabilizes

Markets are responding favorably to rising hopes that the Federal Reserve will launch rate cuts, triggered by last week’s weak-as-expected U.S. jobs report. Futures markets across the board are optimistic in the runup to crucial inflation data—in part the Producer Price Index and Consumer Price Index—to be published later this week. Investors are hedging defensively but hopefully, getting ready to switch gears toward growth-sensitive sectors if inflation readings justify further monetary relaxation.

2. Geopolitics and Policy Indications from Trump

Whereas recent remarks from the President have focused on religion, national unity, and education, their near-term market impact is moderated. Instead, markets keenly observe prevailing trade and tariff moves–most notably tariff reimbursements under discussion at the level of the courts of last resort, with the U.S. Treasury preparing action contingent on the courts. Such moves substantively impact trade-sensitive arenas within both U.S. and European equities.

3. Wider Market Trends and Sectoral Rotation

Global markets bask in universal vigor, with major indices outside the U.S. ‘Magnificent Seven’ close to new highs—a sign of growing investor confidence in foreign equities. Nevertheless, wariness remains surrounding the megacaps, as growing expenditure in AI-based capital starts gnawing at margins, hopefully marking the end of over-concentrated leadership in the tech sector.

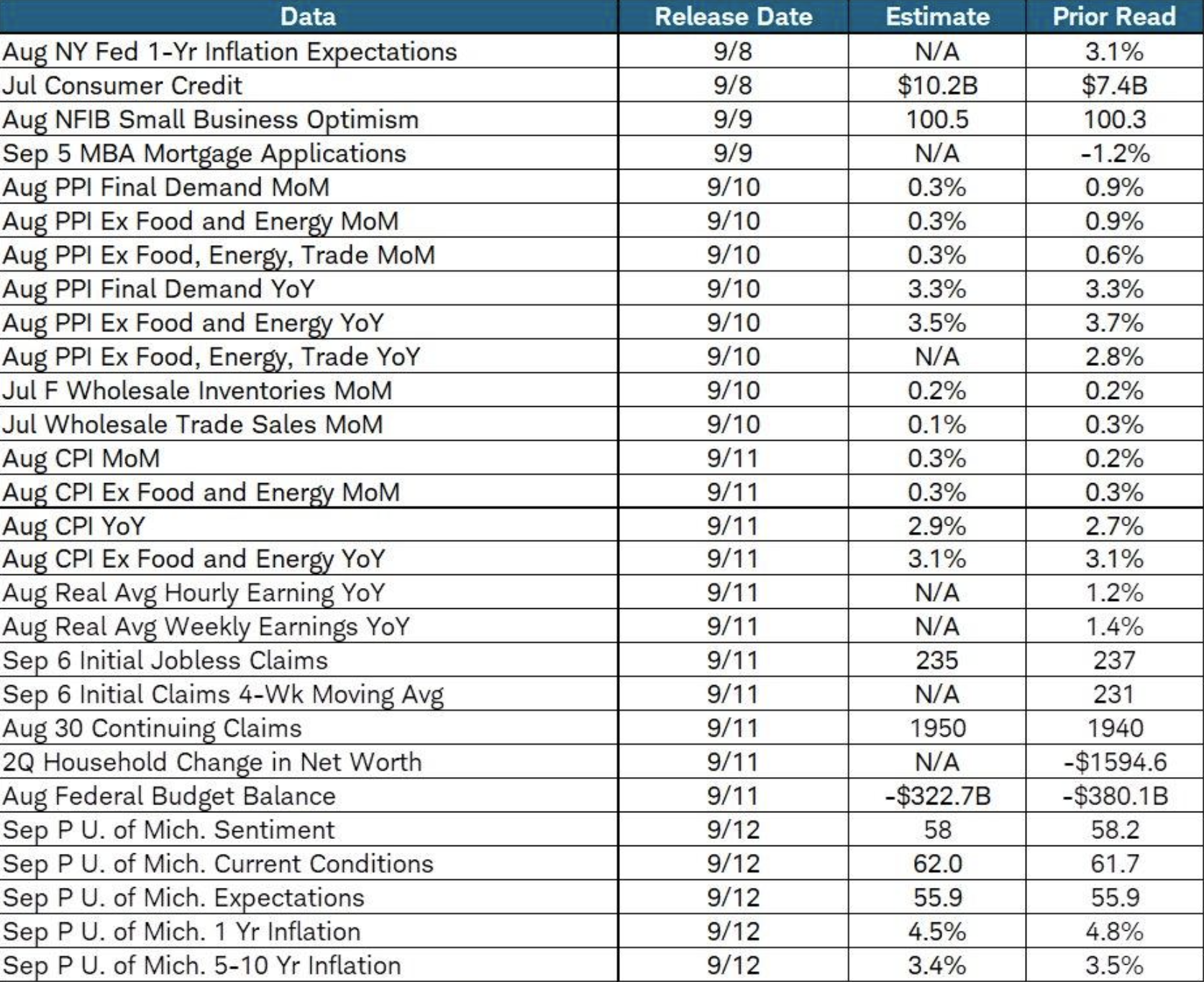

Digesting Economic Data

Trump’s tweets and what followed from them

Trump’s series of recent remarks reflects an apparent effort at re-framing the political narrative in terms of religion, domestic security, and immigration. By reducing domestic upheavals while basking in the decline of D.C. crime, the administration aims to signal stability and order in inner cities. The White House’s response in defense of allegations of underplaying domestic violence similarly reflects an attempt at public relations management and an assertively tough-on-crime message. For markets, the sort of political message that such rhetoric reinforces is the general law-and-order theme, often gaining support from defense, security, and defense-related infrastructure sectors.

Faith has become a prominent theme, with Trump unveiling the “America Prays” campaign in celebration of the nation’s 250th birthday. Enrolling more than 70 groups, his vow to protect prayer in school and his ceremonial gift of an family Bible to a museum solidifies a political campaign founded on cultural and religious convergence. Such acts may not directly affect market fundamentals but build the administration’s credibility with the core constituencies, influencing sentiment in consumer confidence and community activism. Analysts should take the indirect economic impacts of the policies into account, specifically in relation to education, nonprofit finance, and grass-roots mobilization. In security and enforcement, Trump’s approval of Operation “Midway Blitz” in Chicago and the attack on a Caribbean drug ship emphasize an aggressive response in law enforcement and border protection. Alongside demands that foreign firms honor U.S. immigration law, such policies may have an impact on sectors related to defense, energy logistics, and cross-border commerce. Enforcements with strong rhetorical tones are usually taken in the market as favorable to select sectors but as possible epitomes of geopolitical risk premiums, particularly in commodity markets like oil in which routes of supply are enforcement-sensitive.

Lastly, the political and personal scandals continue to be at the forefront. The refusal of the Supreme Court to overturn the E. Jean Carroll defamation case, along with the outrage over the Epstein birthday book, keep Trump in the headlines beyond policy. These issues will not swing markets directly but add an aspect of unpredictability around political stability and investor morale. The polarized reception at the U.S. Open similarly puts the spotlight on the division in public opinion. For investors, this division underlines the importance of maintaining political risk under close observation, as changes in public confidence can quickly bleed over into broader market narratives.

Inflation Expectations Steady but Risks of Sticky Prices Remain

The next week’s U.S. economic data releases commence with the CPI excluding food and energy and the New York Fed’s inflation expectations for one year ahead. Both should be at levels similar to the previous ones, emphasizing that although inflation cooled off from the tops, the latter is nevertheless stubbornly in excess of target. The one-year-forward medium-term expectation at 3.1% cements the perception that both households and businesses remain unconvinced of seeing swift disinflationary dynamics. Structural drivers like the readjustments in the supply chain and immigration-driven labour flows continue influencing attitude, forging an environment in which price stability is more than policymakers would like.

In the Federal Reserve’s book, this data is something of a tricky balancing act. The easing cycle that was launched in 2024 gave support to growth, but a flat spot in inflation expectations makes the case for further cuts more complicated. Markets are now pricing in something more subtle—a more nuanced result in which policymakers reduce the rate of accommodation even as there are signs of weakness in the labour market. The result is that both rates and the dollar remain at risk of volatility as investors debate the extent to which the Fed will prefer cushioning growth rather than bringing inflation further toward its 2% target. Expectations path is crucial: if the consumer surveys continue to reflect underlying price concerns, the Fed may take on more cautionary language regardless of the expectations that the markets have built up in terms of aggressive easing. Equities, in turn, signify this tension in the form of sector rotation. Stability in inflation expectations is favorable for valuations more widely, but rate-sensitive sectors—technology, housing, and utilities—are at this point most underpriced in our view. These areas would gain disproportionately if policy relaxation persists, specifically due to their exposure to financing costs and long-duration growth opportunities. Market participants should watch if this week’s inflation information shifts Fed messaging in the direction of firmer or looser guidance, as even marginal changes will shape positioning across growth-sensitive assets. Technology remains, at this time, our least objectionable region of undervaluation, with the combination of resilience in the earnings along with policy tailwinds.

Slowing Wage Rate Indicates Calming Labour Market

U.S. private wage growth in the three months leading up to September slowed to an annualised 3.35%, far weaker than the more exuberant period at the beginning of the year. The slowdown is consistent with other labour market indicators that suggest decreasing demand, in part due the ongoing trade tensions as well as stiffened credit markets. Whilst wage growth was stronger than the most recent U.K. CPI release at 3.8%, the close correlation is evidence that family purchasing power is being maintained but with far more weakness than in previous quarters.

Easing wage growth creates another complication in the rate outlook for policymakers. Wage inflation in the past was the primary gauge in determining the Federal Reserve’s policy stance, and the current decline can be considered as a step in the direction of bringing balance. However, research cautioning that current wage pressures may decelerate the disinflationary process cannot be readily overlooked. The same is indeed visible in the dovish outlook of the Fed, with officials reiterating that although cuts are imminent, the way ahead will be via gradual cuts so as to prevent fueling the fire of price instability again. The worry for investors is that even small wage stickiness may constrain the possibility of further deeper cuts in the near term. From an equities point of view, the wage moderation yields a mixed scenario. The weakening labour costs should reduce margin pressure on companies, specifically in the manufacturing and retail sectors. However, weaker wage growth would dampen consumption spend dynamics, limiting top-line growth in discretionary sectors. Technology and industrials continue in our view as undervalued names under this scenario, with the resilience in earnings and relative protection from wage movements being the positives. Traders should remain vigilant on revisions in the wage trend, as reaffirmation of the sustained slowdown would underpin the dovish inclination from the Fed and be beneficial to sector exposure with the greatest risk-free rate exposure.

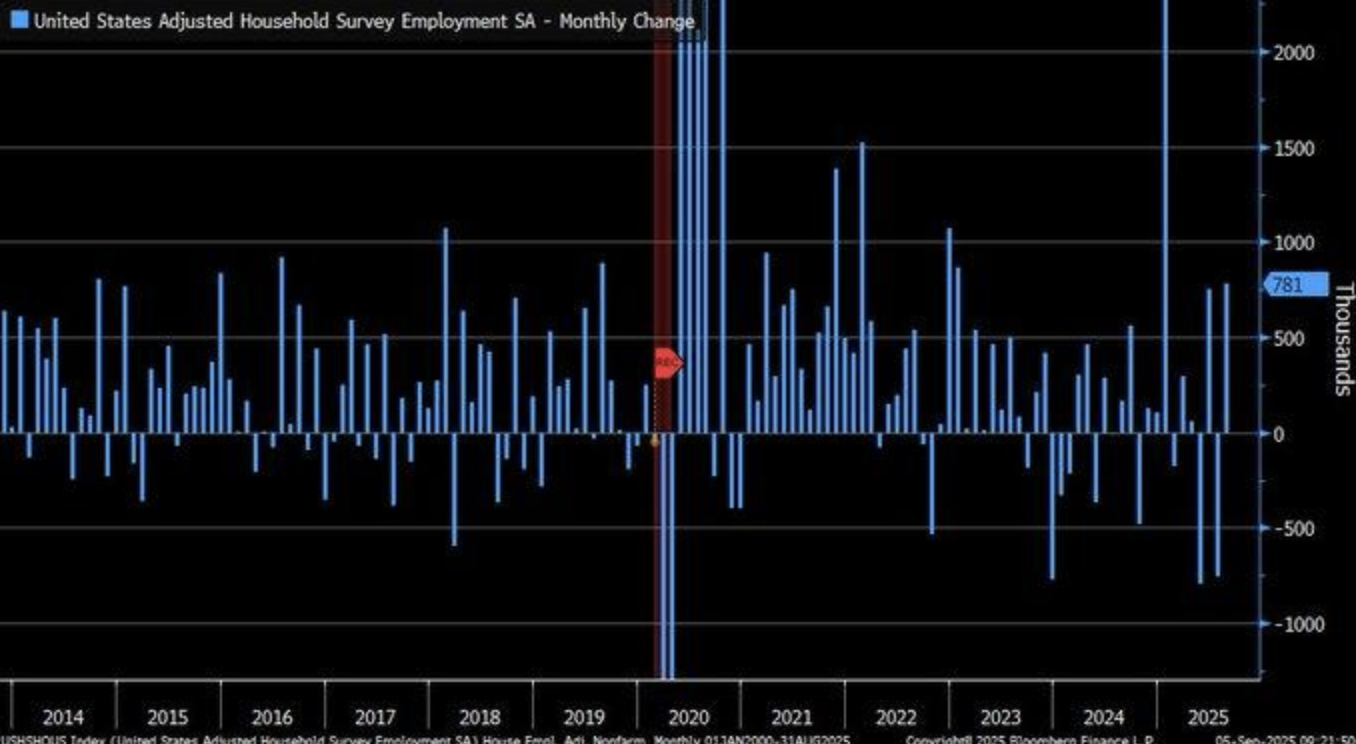

Payrolls Surge as Government Forecasts Diverge from Household Survey

U.S. payrolls in the nonfarm sector, reweighted using the household survey protocol, surged in August by 781,000—a big increase that is theexact opposite of the narrower payroll release from the Bureau of Labor Statistics. The protocol captures a broader employment base that includes the self-employed and multiple earners per family and in the past has flagged discrepancies of as much as 300,000 in the monthly number of jobs. The new number therefore would imply the outlook in jobs may be more durable than the headline payroll readings would themselves imply, but the potential overstatement is possible.

The increase in this period is especially remarkable against the back-drop of continued global economic instability. Recent disturbances, including an East Coast ports strike, have stretched supply lines and made the outlook for growth more complicated. Such a surge will inevitably command notice from the Federal Reserve, as favorable employment data dissuades the necessity of forceful policy relaxation. Still, there is doubt among economists concerning the legitimacy of household survey adjustements, especially during tumultuous times when transitory factors may overstate fluctuations in employment. For markets, the gap creates more at stake in forthcoming Fed messaging, as policymakers will be forced to reconcile strong adjusted readings with broader measures of deceleration elsewhere. For investors, the implications cut across asset classes. Equities tied to domestic demand, especially consumer discretionary and retail, could benefit in the near term if employment strength translates into steadier spending. At the same time, higher-than-expected labour resilience risks delaying deeper Fed cuts, creating headwinds for rate-sensitive sectors. We continue to see technology as undervalued in this environment, offering structural earnings growth less dependent on payroll volatility. Analysts should monitor whether subsequent revisions narrow the gap between household and payroll surveys, as clarity on employment strength will be critical in shaping both rate expectations and sector performance into year-end.

Investor Sentiment Stays Extremely Bearish, Contrarian Indicators Forming

The recent AAII Investor Sentiment Survey finds the bull-bear spread solidly negative, as is true with this signal since mid-2022. Traditionally, bullish sentiment has averaged close to 38%, but recent readings continue to indicate bears far outpacing bulls. Such disassociation is indicative of profound scepticism among private investors, in spite of stabilising macro environment. Academic papers have long pointed out that such negativity is often ahead of equity bottoms, which supports the belief that negative sentiment is a contrarian signal of undervaluation.

What makes the current backdrop particularly striking is the contrast between investor psychology and central bank positioning. Global policymakers, including the Federal Reserve, have signalled a willingness to ease policy in 2025, setting the stage for improved liquidity conditions. Historically, periods where sentiment was most depressed but monetary support increased have often coincided with market rallies. The persistence of bearish readings in the face of prospective rate cuts suggests investors may be underestimating the potential for a rebound in equities as financial conditions ease.

For sector exposure, this divergence breeds opportunity. Profoundly negative sentiment, in combination with dovish monetary indications, has historically favored growth-sensitive sectors like technology and industrials, both of which remain cheaper than long-term earning potential warrants. Pessimism should be perceived as entirely natural and no harbinger of doom when the underlying policy environment is poised to ease and inflation is stable. If policy easing becomes reality with stable inflation, current bearishness can serve as catalyst for broad-based rally, especially among under-priced tech names that will gain from liquidity boost as well as building demand drivers.

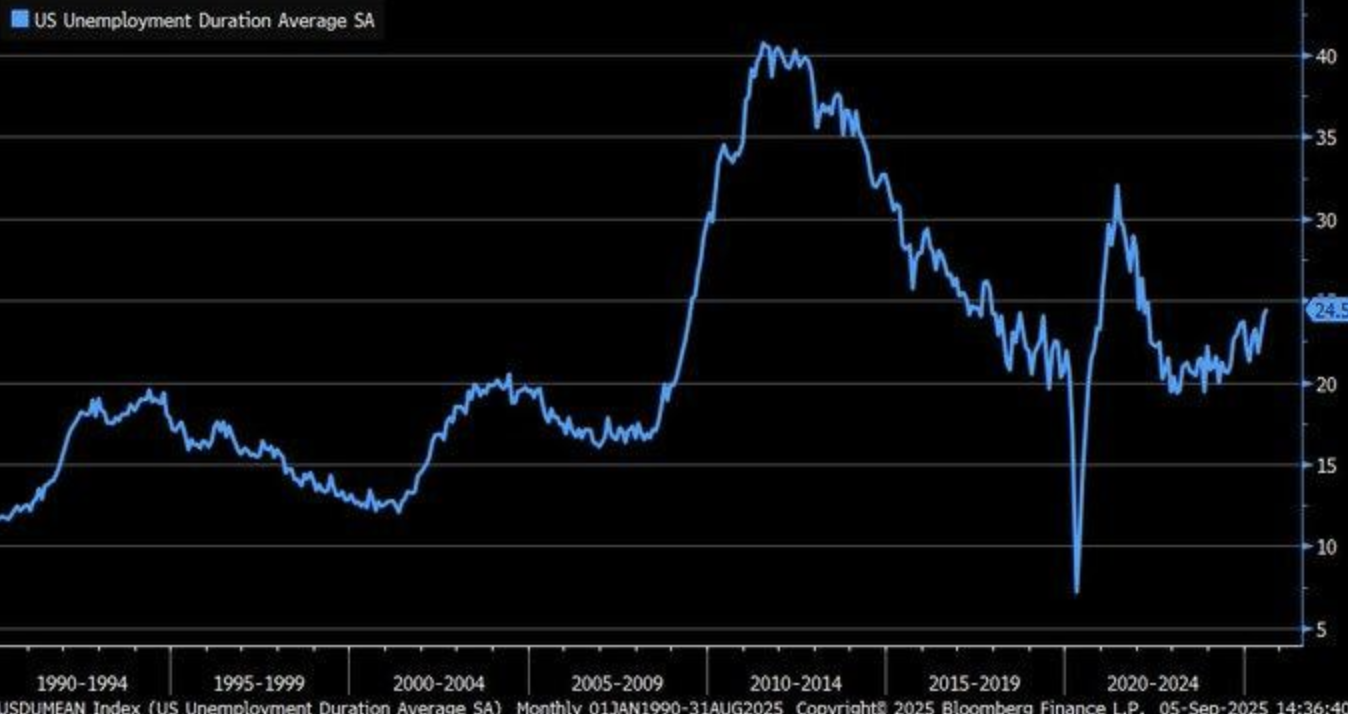

Unemployment Spells Increase, Unveiling Structural Labour Market Changes

The average American unemployment duration rose to 24.5 weeks during August of 2025, straying well beyond historic averages and indicating underlying issues under the surface of headlining jobs recovery metrics. Statistics from the Bureau of Labor Statistics reveal that long-term unemployment across the United States was high from the year 2020 onwards, with the percentage of people unemployed for over 27 weeks increasing during each successive downturn. Thefact that this was so consistent indicates labour marketstructural friction, as displaced employees find difficulty readjusting in the face of shifting sector dynamics.

A number of factors lie behind this trend. Technological advancements, driven by the transition to digital and remote working arrangements, have reconfigured working patterns, suppressing demand in some jobs while heightening the mismatch in required skills across industries. Meanwhile, sectors that depend on physical presence, such as services and tourism sectors, remain under continued stress, capping the possibility of fast rehiring. The tendencies reflect an intensifying gap between high-skill sectors that are benefiting from investment in technology and labour-based sectors that are still adapting to slow cycles of demand. For policymakers, the increase in the duration of unemployment reflects the challenge that the cyclical weakness is coinciding with the structural headwinds, which will render the Federal Reserve’s judgement concerning the resilience of the labour markets more complicated. The effects are dual for investors. Extended duration of unemployment is suppressingconsumer confidence, eliciting caution in the consumer discretionary names that are correlated with non-essential purchases. However, technology and industrials sectors, being less labour-intensive, remain relatively insulated, with the growth in earnings being supported by the gain in productivity instead of expansion in the workforce. These sectors continue appearing underpriced in our opinion, especially with the possibility of policy relaxation augmenting the capital invest flows. Analysts should keep the metrics of labour market duration in tandem with wage growth directions because both will dictate the demand strength expectations as well as the Fed’s threshold of continued policy relaxation.

Gender Mismatch in Labour Participation Causes Structural Issues

U.S. labour force participation levels showed an alarming gap in August 2025 as the participation among males surged to 68.6%, against that of females that dropped to its lowest levels since late 2022 at 56.9%. The gap is indicative of the structural mismatch being witnessed in the labour market as males are joining the jobs at a quicker clip compared to women exiting the jobs. The trend is raising alarm over the sustainability of the recovery as well as the economic losses due to uneven participation, especially in industries that are dependent on a broad-based labour pool.

Behind this decline are well-documented constraints on female participation. Studies from the Bureau of Labor Statistics have confirmed that care giving is the leading constraint, while university research suggests that significant proportions of women with young children quit the labour force after the pandemic. As childcare costs and accessibility continue to be issues, many women may be exiting the formal labour force in favour of informal or gig economies. The same period sees the general moderation in the creation of jobs, which cements the idea that official measures of participation underplay the reshuffle in the dynamics of labour. The effects on markets are two-sided. A smallering workforce, especially among women, may worsen skill shortages in core sectors, keeping wage pressure high even as overall payroll growth slows. Non-consumer-facing firms may also be hurt if incomes at the household level are strained due to falling female participation. Technologically driven sectors and health care sectors are undervalued in our view due to their exposure both to the efficiency drive and the structural demand that is independent of this participation volatility. Labour force structure should be closely watched, with analysts keeping in mind the possibility that chronic imbalances in the composition of the labour force may reflect underlying structural impediments that loom large over long-term growth prospects as well as future monetary policy.

Upcoming Economic Event

With little of significance on the current economic calendar, the spotlight therefore falls entirely on tomorrow’s publication of the U.S. Consumer Price Index (CPI). The latter will be the final sentiment-driving number as the former will directly reveal inflationary pressures and therefore the Federal Reserve’s next policy directive.

In the countdown phase, the release of CPI tomorrow will be the final critical test of inflation expectations and measure broader September market positioning. Investors will be well advised to be on high alert because the outcome will dictate sector rotation as well as the risk appetite in world markets.

STOCK MARKET PERFORMANCE

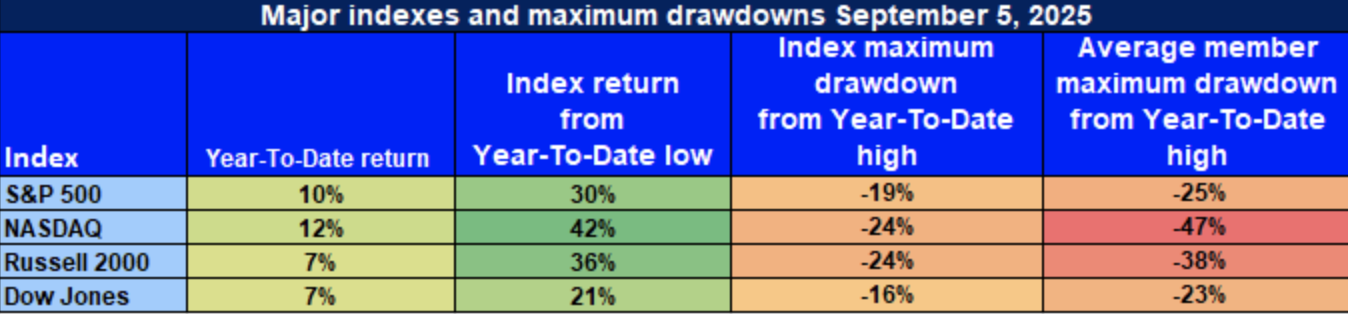

Indexes Repeat the April Bottoms, but Deep Losses Emphasize Fragile Breadth

U.S. equities have registered respectable bounces from the low on April 8th, but the YTD high is spotty and drawdowns betray underlying market weakness. Though indexes are up, average constituent weakness implies that breadth is weak and so the rally may be no more sustainable.

Following is our commentary on recent activity in core indexes:

S&P 500: Headline Gains Mask Underlying Weakness

YTD: +10% | +30% below April low | -19% from YTD high | Avg. member: -25%

The S&P 500 is up 10% this year and rebounded 30% from the April low. Still, the move from the YTD high in a decline of 19% and average member losses of 25% reflect that the paticipation remains narrow with big-cap names powering the majority of the performance.

NASDAQ: Tech Momentum Sees Deep Member Losses

YTD: +12% | -42% below April bottom | -24% from YTD top | Avg. member: -47%

The NASDAQ leads the charge with a 12% YTD gain and convincing 42% recovery from April. The index, though, lost 24% from highs and experienced dramatic -47% average member decline, reflecting weakness across the growth names and that volatility is once again a perennial theme in the tech-heavy index.

Russell 2000: Small-Cap Rally Lacks Conviction

YTD: +7% | +36% off April low | -24% from YTD high | Avg. member: -38% Small caps have rallied back from the April lows by 36%, but are only up just 7% in the year. The Russell 2000’s decline from highs of 24%, and average-member decline of 38%, reflect the weakness in the more-illiquid economically-sensitive stocks that continue to struggle find solid footing.

Dow Jones: Defensive Tilt Cushions Volatility

YTD: +7% | +21% from April low | -16% from YTD high | Avg. member: -23% The Dow is up 7% on the year and 21% from the April lows based on defensively weighted sector exposure. A relatively mild 16% correction implies more stability, but average member losses of 23% mean that even value-biased sectors aren’t immune from general stress. Zaye Capital Markets is selective, preferring companies with solid balance sheets and durable earnings strength. Ahead of improving market breadth, the best opportunities remain in high-quality technology and defensive value stocks that can endure the volatility while gaining from policy relaxation ahead.

THE STRONGEST SECTOR IN ALL THESE INDICES

Communication Services Leads the Pack as Market Breadth Remains Uneven

Among the S&P 500 sectors, Communication Services has solidly become the strongest performer year-to-date so far in 2025. The sector is up 23.2% year-to-date, well ahead of the broader S&P 500’s 10.2%. On the shorter timeframe as well, Communication Services impresses with resilience with month-to-date gain of 5.1%, both indicating signs of cyclical strength along with demand from investors that prefer companies with scalable business models as well as subscription-based revenue structures.

Other industries including Industrials (+14.1% YTD) and Information Technology (+13.8% YTD) have also posted strong form as demand remains strong for productivity solutions and digital infrastructure. Both, though, post month-to-date returns of -0.9% and +0.2% respectively highlight near-term consolidation and that the momentum in the period weakened relative to the consistent Communication Services’ form. Defensive sectors like Utilities (^+9.6% YTD) and Financials (^+9.5% YTD) remain positive on the year but in recent periods have weakened, with month-to-date losses of -1.1% and -1.7%, highlighting the impact of rate volatility.

In the Communication Services sector at Zaye Capital Markets, we observe that the YTD gain of 23.2% makes it the undisputed leader among sectors, underpinned by both resilience in earnings as well as in investor flows. The sector remains one that analysts should watch closely, as continued outperformance compared with the broader index is indicative of sustainable momentum. We believe select names in Communication Services remain undervalued, and this is particularly true in names that boast solid balance sheets as well as exposure in digital advertising, media, and telecom services, whereby the earnings power remains underestimates in current market levels.

Earnings

Yesterday’s Earnings (September 8, 2025)

- Casey’s General Stores, Inc.

Casey’s General Stores reported its fiscal first quarter 2026 results, posting an EPS of $5.77, comfortably ahead of market expectations of around $5.01. The upside surprise reflects continued strength in foodservice offerings, digital expansion, and solid fuel margins. With revenue also exceeding estimates, investors should track forward guidance closely, particularly around fuel costs and consumer demand trends. Retail plays within the convenience space remain appealing, with certain downstream names still trading at discounted valuations.

- National Beverage Corp.

National Beverage released its quarterly update, highlighting resilience in its beverage portfolio amid shifting consumer spending. While headline results were broadly in line with expectations, pressure on input costs remains a central theme. Investors should monitor pricing strategies and distribution growth, as these will dictate margin recovery. Stocks across the non-alcoholic beverage segment may present undervalued opportunities if cost-management gains materialise in coming quarters.

- Planet Labs PBC

Planet Labs reported results that showed steady progress in growing its data-as-a-service revenues. While revenue growth aligned with forecasts, the company remains challenged by profitability metrics, with analysts continuing to assess its long-term scalability. The expansion of commercial contracts provides upside potential, but investors should remain focused on cash burn and operating expense trends. The broader small-cap tech space could harbour undervalued firms with similar recurring-revenue models.

- Yext, Inc.

Yext delivered results showing modest revenue improvement but ongoing pressures on margins. Its focus on digital knowledge management continues to attract enterprise demand, though profitability remains a near-term challenge. Analysts should look for updates on cost-cutting and AI-driven product integration as drivers of potential upside. The undervaluation case is stronger among digital platforms that can demonstrate sustainable recurring revenue while moving toward operating leverage.

Today’s Earnings (September 9, 2025)

- Oracle Corporation

Oracle is scheduled to release its Q1 FY2026 earnings, with consensus expecting EPS of $1.47 on revenues of roughly $15.0 billion. Investors will closely watch its cloud and AI infrastructure performance, alongside commentary on margins and demand for GPU clusters. A positive surprise could reinforce confidence in its AI-driven growth strategy, while a miss may pressure sentiment around valuation premiums. AI infrastructure stocks remain positioned as undervalued beneficiaries of strong cloud momentum.

- Rubrik, Inc.

Rubrik is set to report results with forecasts pointing to a loss of around $0.50 per share. The focus will be on subscription growth, contract retention, and progress toward narrowing losses. As a cybersecurity-focused data protection firm, consistent momentum in recurring revenues could justify long-term value despite short-term losses. Select software security stocks in the sector remain undervalued given their growth runway.

- Core & Main, Inc.

Core & Main is expected to announce EPS of $0.78, with infrastructure demand and municipal projects likely to be the focal point. Pricing discipline and project backlog visibility will be critical in shaping investor sentiment. Should the company deliver above expectations, infrastructure-related equities may benefit, with several names in the sector still trading below fair value given long-term demand drivers.

- GameStop Corporation

GameStop is forecast to post EPS of around $0.155, with the market’s focus on liquidity preservation, inventory management, and monetisation strategies. While the firm continues to navigate structural headwinds, clarity on long-term strategy could shift sentiment. Certain consumer discretionary stocks in turnaround situations may be undervalued if management execution begins to stabilise fundamentals.

Stock Market Report – Tuesday, September 9, 2025

U.S. stocks are still biased to the upside heading into the inflation-centric week. The possibility of rate cuts is still high ahead of tomorrow’s CPI and that’s keeping risk appetite going despite ongoing policy rumors out of Washington. The least-resistant path is inflation printing high enough to offer near-term cause for ease. The rally in equities is spilling over from the mega-caps but leadership is weak before the data.

Stock Prices

Economic Indicators and Geopolitics Developments

Two swing factors are in play today. The policy tone comes first—a signal of tougher trade moves usually depresses risk assets while improving the dollar and Treasury yields, but a dovish shift usually causes relief rallies. The other is the inflation path—if CPI prints stronger than expected, markets will re-think the easing plans, with negative effects on equities; if in at the lows, the rally will continue. Softer jobs data in the prior week keeps rate cuts alive and supports market resilience through tomorrow’s release.

Latest Stock News

Markets are increasingly pricing a September rate cut, with CPI standing as the ultimate arbiter for both size and pace. A benign print would likely support tech and quality growth, while an upside surprise may push investors toward defensive and value sectors. Breadth has improved, but the AI-heavy complex faces margin pressures as capital expenditure accelerates. This is pushing investors to consider rotations into utilities, real estate, and select cyclicals with infrastructure exposure.

The Magnificent Seven and the S&P 500

The Magnificent Seven continue in the spotlight as rising data-center and silicon investment pressures release the near-term free cash flow. Compounded with valuations and regulation concerns, this sees weakness spread through swathes of the group. The S&P 500 finds difficulty breaking through the top in the absence of their full contribution. A weaker CPI tomorrow would see numerous pressures ease and leadership re-ignite, but a hotter print would extend the phase of de-risking in high-duration tech stocks.

Major Index Performance – Tuesday, September 9, 2025

- S&P 500: Moderately higher trading, up near 0.2.

- Nasdaq Composite: Outperforming, up roughly 0.4–0.5% and testing record levels.

- Dow Jones: Advanced by around 0.2%, with gains in energy and financial stocks.

- Russell 2000: Little changed to slightly better at +0.1%, as small caps are hamstrung by interest rate sensitivity.

At Zaye Capital Markets, we remain attentive to CPI risk as the main market driver. A soft take would affirm positioning into duration-sensitive growth, whereas a hotter result would prefer the defensives as well as selective cyclicals with better pricing power.

Gold Rate

Gold is at an all-time high of approximately $3,651 per ounce, with futures at just under $3,690, as softer labor statistics and growing unemployment have bolstered prospects of Federal Reserve rate reductions. Smaller Treasury yields and the weakening dollar have solidified the metal’s function as a hedge, propelling demand globally. Investors are demanding more stability in gold as belief in monetary policy stability erodes, with the yellow metal becoming a foundation safe-haven holding.

Although Trump’s recent remarks emphasized domestic cooperation and religion, the immediate impact on gold is small relative to the economic context. The catalyst is instead yesterday’s underwhelming labor data, which intensified dovish expectations of policy loosening. The latter has boosted flows into the yellow metal and powered its breakout move. Look out tomorrow as CPI is next on the menu, with the metal’s next destination depending on inflation: a weaker print would push prices higher, while an increase in inflation could bring short-term volatility. At Zaye Capital Markets, we believe gold will continue strong support as the environment points toward lesser interest rates and growing safe-haven demand.

OIL Prices

Crude benchmarks are slightly stronger today, with Brent at around $66–67/bbl and WTI at approximately $62–63/bbl. The market is in balance across supplies and macro dynamics: OPEC+ will initiate a small unwind of previous cuts in October, although small volumes and capacity constraints have dampened the bearish impact. U.S. shale drilling remains weak, helping prices by calming the risk of oversupply. Meanwhile, the weakening dollar and growing rate-cut expectations underpin the complex, despite the capping of rallies from demand concerns globally. Overall, the oil market is within a tight range based on supply discipline, small capacity openings, and positioning ahead of the inflation data.

Politically, Trump’s recent remarks have no direct impact on oil with no new sanctions or tariff moves so the sentiment remains relatively unchanged. Yesterday’s weak jobs data added fuel to the argument in favor of Fed easing, benefiting the latter indirectly with a weaker dollar but at the same time capping demand growth prospects, limiting gains. No significant economic releases are due today, so the market is preemptively focused on tomorrow’s CPI print and the forthcoming OPEC and IEA reports. A cooler CPI would be expected to push up energy prices with the re-enforcement of the easing theme while a hotter figure would threaten crude with the dollar’s gain and the tightening of financial conditions.

Bitcoin Prices

Bitcoin trades at $111,690 levels today while remaining close to the crucial $112K resistance area. Technical indications spot an inverse head-and-shoulders formation, with the move above $113K eyeing $120K while breakdowns may push prices south of $108K–$100K. Institutional flows continue as the favorable driver with the inflows in the ETFs nearing $250 million while bolstering market depth amidst trimming exposure from some large holders. Such symbolic acts as the purchase of 21 BTC by El Salvador on the day of the Bitcoin Law’s one-year anniversary and programs like the push into tokenized securities by Nasdaq continue solidifying adoption momentum through both sovereign as well as institutional corridors.

Macro-wise, Trump’s recent emphasis on domestic policy and faith-based unity engenders little direct crypto pricing influence as Bitcoin’s environment remains more sensitive to economic and regulatory cues. Yesterday’s weak US labor figures reinforced expectations of Fed loosening, and the dollar weakened as Bitcoin’s safe-haven and hedging demand surged. The next move in the near term will depend on inflation tomorrow, with the CPI data due out; as prices print softer, they will validate further the upside move, but as prices print strong, they will solidify resistance. As Bitcoin enters this critical phase of consolidation, as we see at Zaye Capital Markets, institutional demand in this environment and consensus expectations regarding monetary policy will be the determining factors of whether this move extends towards new highs or retests the downside supports.

Eth Prices

Ethereum is ranged at $4,305, consolidating in a narrow band as the market moves back and forth between support at $4,250 and resistance at approximately $4,370. The technicals provide no clear bias with the momentum neutral, not overbought or oversold. A move through the resistance would provide the catalyst for the rally through $4,500–$4,700, while a breakdown would risk sliding through the $4,100–$3,900 area. Institutional flows continue supportive in the face of this pause, with demand from the ETF and bullish forecasts supporting the outlook, keeping the longer-term targets above $5,000 in the picture with the continuing build-out of network adoption.

On-chain action accounts for conflicting but significant whale movement. Three new wallets just purchased $148.8 million in ETH, indicating institutional-type conviction, while an inactive ICO-period whale re-emerged through the act of staking 150,000 ETH (approximately $645 million), denoting long-horizon commitment and diffusing near-term selling pressure. A third whale moved 47,507 ETH (~$207 million) into new wallets, fueling rumors of possible redistribution. These activities account for a marketplace driven both by accumulation and repositioning, with the overall environment skewed in favor of resilience. At Zaye Capital Markets, in our opinion, the future in terms of prices in Ethereum rests on whether whale accumulation overrides redistributions, in addition to macro tailwinds from dovish monetary policy and rising institutional demand.