Where Are Markets Today?

U.S. and European stock futures drew a mixed picture on Monday, with the U.S. market set to open higher while European markets beginning the week on the defensive. S&P 500 futures advanced 0.13%, Nasdaq 100 futures advanced by 0.18%, while Dow futures advanced by 0.09% in signaling cautiously optimistic sentiment in the days ahead with critical earnings. Meanwhile, Euro Stoxx 50 and Germany’s DAX declined by about 0.3% in signaling increased concern about near-hanging U.S. tariff deadlines and precarious trade negotiations. The divided opinions capture the dominant theme: optimism in homegrown growth versus anxiety about global trade risk.

Two drivers are powering the U.S. futures rally. One, the strong beginning to earnings season, where to date more than 86% of those companies which have reported in the S&P 500 have beat expectations, is bolstering investor confidence. With market-leader big-techs Microsoft, Amazon, and Apple in the earnings lineup this week, expectations of continued earnings strength are bolstering sentiment. Two, the strong retail control-group sales results last week of the strong U.S. retail sector further confirmed U.S. consumers are doing well, bolstering the overall economic environment and bolstering investor positions in risk assets.

To the contrary, the European sentiment remains guarded as markets absorb new U.S. Commerce Department pronouncements. The new tariff deadline of August 1 has been reconfirmed, yet pronouncements also indicated that negotiations remained in place. Nonetheless, European bourses—most directly impacted being those with high export exposure like industrials and autos—are factoring in the risk of flows in trade being disrupted and the rise in costs. It has that negative aspect taking the European equities market down as well as generating a defensive sentiment in investors in the hopes of increased policy direction. According to Zaye Capital Markets, the destiny of the shape of the future in the present day hinges upon diversified macro exposure. U.S. markets are receptive to earnings optimism, while Europe is faced with a higher risk environment related to external policy refinement. Next-version tech earnings and the next steps in the trade negotiations will be of key significance in confirming or limiting regional divergences. For the present, the market bifurcation spells opportunity—yet demands selectivity.

Major Index Performance as of July 21, 2025

- S&P 500: 627.58, down 0.07% on the day.

- Nasdaq Composite: Currently near 561.26, dipping 0.10% on the day.

- Dow Jones Industrial Average: Moved little to mildly higher, helped by defensive stocks.

- Russell 2000: Still modestly behind, however overall sentiment around the small-caps remains subdued.

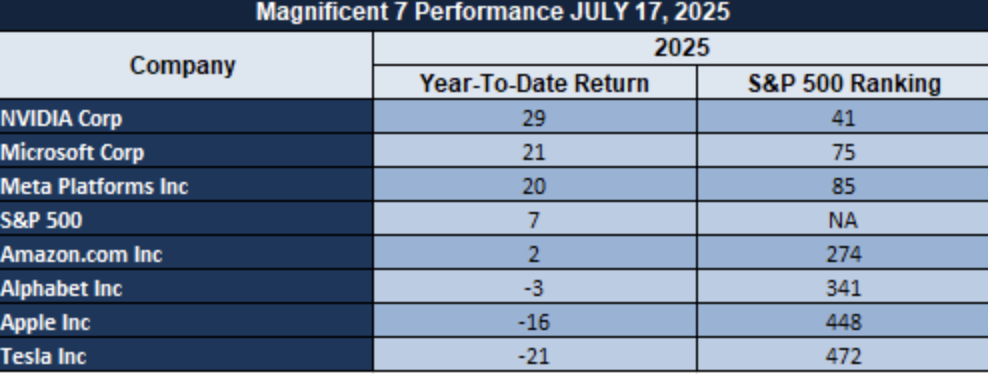

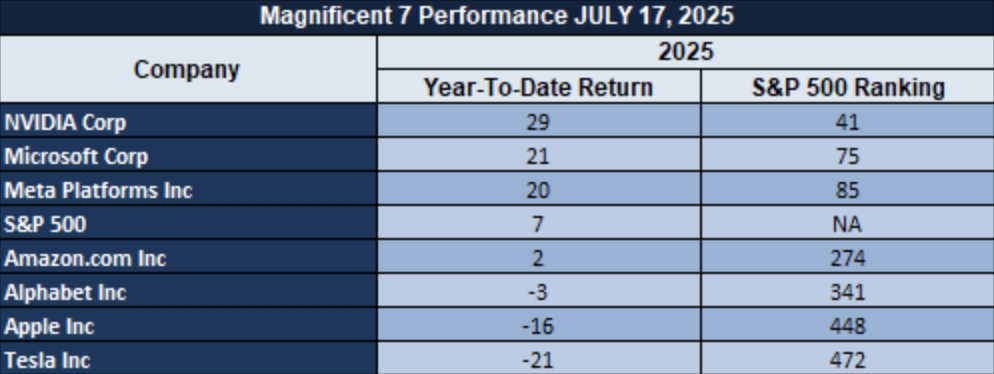

The Magnificent Seven and the S&P 500

S&P 500 still relies on the Magnificent Seven. Microsoft, Meta, and Nvidia leadership has in turn been supported by strong AI-driven earnings. Tactical errors and regulatory issues, however, await Apple, Alphabet, and Tesla. Tesla, in fact, has been hurt by weakening EV demand alongside leadership distractions. The gap further decreases the index’s breadth, with the growth being even more concentrated among the winners.

Drivers Behind the Market Move – Monday, July 21, 2025

Markets are being driven today by a mix of solid corporate earnings indications, shifting trade policy rhetoric, and reassuring economic data. Following are the three major influences directing both U.S. and European futures:

1. Tech‑driven Earnings Momentum

Over 86% of S&P 500 companies that have reported so far have beat expectations, fueling optimism in futures markets. U.S. futures are rallying in expectation of pending results from mega-cap tech giants—Apple, Microsoft, and Alphabet—anticipating continued outperformance. European futures are also imperceptibly spurred by a global sentiment but more subdued on regional concerns over trade risks.

2. Trade Tensions and Tariff Clarity

The White House has reaffirmed an August 1 “hard deadline” to impose tariffs, though talks remain open—conveying toughness and possible flexibility to investors. The stance alleviated some equity pressure, especially in autos and industrials, as the markets interpreted it as a less belligerent tone. European futures, however, continue to trade lower, amid worry over export‑reliant sectors and in anticipation of clarity on U.S.-EU tariff arrangements.

3. Macro Resilience and Risk Appetite

Conflicting economic data and geopolitical background noise signals are influencing sentiment subtly. The retail control-group sales upside surprise last week assisted in reinforcing underlying domestic economic strength, U.S. equities. Asian market commentary, including Japanese market stability despite political uncertainty, also supports global risk sentiment. Trump’s call for Federal Reserve rate cuts amidst tariff-driven inflation also supplies an implicit dovish bias, which supports risk assets but occasionally dampens dollar strength.

At Zaye Capital Markets, we interpret these drivers as U.S. futures capturing positive earnings expectations and benign economic fundamentals, while European futures are still pressured by external policy risks. The balance between macro data, tariff developments, and earnings momentum will determine market direction as the week progresses.

Digesting Economic Data

The TRUMP Tweets and Their Implications – Monday, July 21, 2025

At Zaye Capital Markets, we remain mindful of the excessive market influence of public comments—policy as well as culturally polarizing—of Trump, the President. Trump’s tweetstorm of the past 48 hours has added to volatility across a variety of different asset classes. Most urgently, his demands for historic Federal Reserve rate cuts facing tariff-induced inflation revived speculation regarding policy accommodation, driving dollar weakness and new gold, cryptocurrency, and high-beta stock buying. Trump’s commentary on the economy is a gauge of a populist shift toward stimulus-infused rhetoric ahead of the next APEC Summit, where Trump sits down with Xi Jinping—an event that could have a radical impact on world trade flows and commodity flows.

His support of the GENIUS Act—now law—has solidified a pro-crypto tone in the nation’s capital. With terms to regulate stablecoins and denominate Bitcoin as a national asset in a new strategic reserve, Trump’s agenda has catalyzed a wave of institutional investment in digital assets. Ether and Bitcoin shot to multi-month highs, powered by ETF flows and whale accumulation. Trump’s words have made him the most crypto-friendly political leader in U.S. history, turning regulatory tone from enforcement to adoption. The market reaction isn’t just relief at finality but conviction in eventual structural inclusion of crypto in national finance policy. Geopolitically, Trump’s rhetoric creates ripples of discomfort. His censure of Netanyahu’s belligerence in Syria and Gaza creates diplomatic tension at the time of strategic significance, his threat of aid to Afghan passengers trapped in the UAE has realignment of foreign aid narratives possibilities, and his increasing threat of prosecution—against media groups such as the Wall Street Journal and individuals in the Epstein probe—creating defensive hedging by reputation risk-sensitive investors. These flashpoints of the political variety are being read by markets as creating yet another source of uncertainty, further compelling the need to hedge in gold and take risk dispersion into decentralised stores of value such as crypto.

From a cultural angle, Trump demands the restoration of the country sport teams’ vintage/original names such as Redskins, Indians, etc., has triggered Polarized responses, and they’ve hit the country debate. Indirectly market-sensitive, the type of statements fall within the broader theme of Trump all-over the news radar—keeps policymaker, investor active, busy, but responsive, not proactive. At Zaye Capital Markets, we view Trump multi-pronged communication attack as noise-generator, risk premium inculator across the board. Without reassuring economic data, the type of statements will maintain risk sentiment, capital flows, as well as the political risk narrative, active through Q3.

Inflation Expectations Ease Amid Policy Shift Signals Stable Sentiment

Expectations of inflation moved sharply down, the University of Michigan survey of July suggesting a one-year horizon of 4.4% and five-to-ten-year of 3.6%. Decreases from previous readings of 5% and 4% respectively, therefore, indicate a softening of consumer concern, in our opinion associated with fading talk of tariffs and better sentiment. These readings despite persistent risk of policy are helpful in reinforcing that the consumer becomes increasingly accustomed to ambiguity at the macro level, including tightening tensions in the world of trade.

Higher leap in the Consumer Sentiment Index up to 61.8, the highest in five months, underscores tentative positive shift in consumer sentiment. Though Trump’s tariff plan had at one point drawn record-high inflation expectations (as high as 4.9% in March), headline data indicate a population desensitized to uncertainty about trade policy. By precedent, sentiment reassignment of this kind follows periods of monetary policy conviction, the kind we witnessed in previous cycles when inflation expectations had dropped below 4% and the Fed was steadfast.

We are still bullish on consumer discretionary stocks with this trend and Target Corp. the most underappreciated of the bunch by virtue of its sentiment-sensitive consumption base. Investors can monitor near-term validation of this theme in the form of next PCE and core inflation prints. Upcoming escalation of trade-related brinksmanship will also test these high hopes in the near term. Our general market outlook remains neutral, opting for selective exposure to sentiment-driven retail.

Sentiment Rises But Spending Caution Signals Complex Outlook

University of Michigan Consumer Sentiment Index rose to 61.8 in July 2025, from 60.7 in the prior month, and modestly above expectations. Upward improvement was supported by softening inflation expectations—4.4% for one-year ahead (down from 5.0%) and 3.6% for five years (down from 4.0%). Although evidence suggests consumer expectations leveling out, continued uncertainty about the eventual course of trade policy still acts as a brake on optimism, at least, after recent tariff policy that has eroded confidence in price stability.

History testifies that consumer inflation expectations, and even more significantly, those registered in the Michigan survey, tend to exceed actual inflation. Put another way, the present 4.4% view may be overstated, more the result of political spin than economic reality. To that, we can add the worsening historical correlation between consumer sentiment and consumer spending discussed in recent analysis articles that shows better sentiment improvements are not automatically going to result in better retail spending—especially in the face of increasing price pressures born of trade tariffs.

In this respect, we consider Costco Wholesale Corp. to be undervalued, given its defensive profile alongside price leadership in retail inflation-sensitive markets. Analysts will be keenly interested in Aug. PCE data, retail sales reports, in a bid to confirm the gap between sentiment, spending. Policy direction on tariffs will be crucial in adjusting investor expectations, as well as corporate margin expectations.

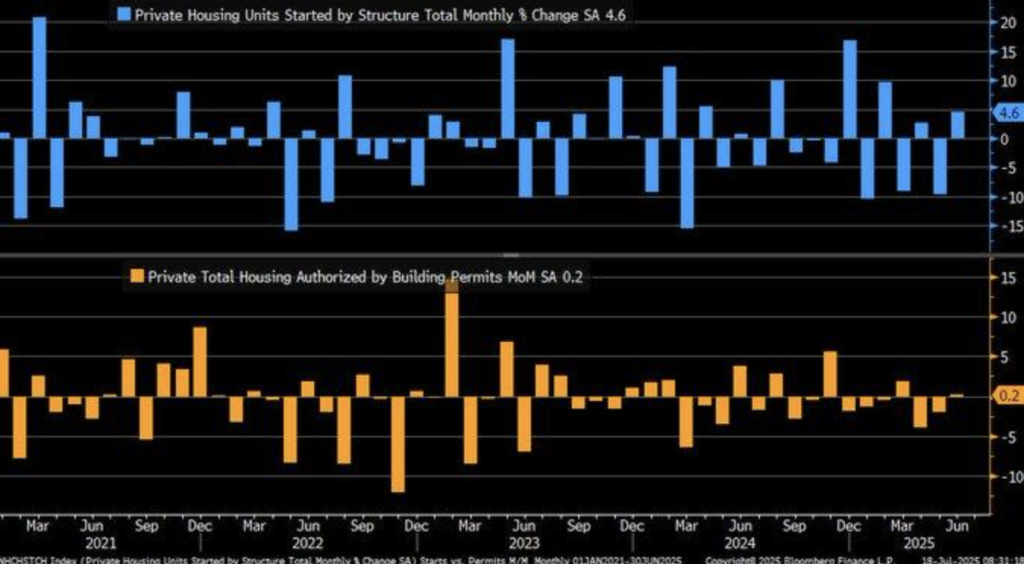

Multi-Family Surge Makes Up For Single-Family Housing

Residential building in June 2025 homebuilding data marks a radical change in U.S. residential construction fundamentals. Starts in homebuilding increased by 4.6% to 1.321 million units, better than forecast as a 30.6% rise in multi-family construction completely made up for a 4.6% decline in single-family starts to 883,000—low since July 2024—illustrative of how far mortgage rates and unaffordability are transforming residential demand. Permits also increased modestly in the total, however, with a 3.7% decline in single-family permits, to indicate potential near-term supply shortages.

It signals a shift in builder tactic. While affordability declines—clear in medians rising well into the $427,000s and mortgage eligibility up 60% from 2021—builders are focusing doubly on multi-family developments. It meets the increasing demand for renters by the millennial generation, the increasing population of renters now being denied home purchases. The 11% decline in 2025 single-family starts forecast puts the seal of approval on the structural market realignment.

We feel that AvalonBay Communities Inc. is under-priced here, with its proven multi-family platform and multi-year rent-generating history. Analysts will be looking at the next mortgage rate direction and area permitting flows, in that either funding cost weakness or zoning codes can add volatility to the forecast for the single-family supply. For now, multi-family remains the stable core of the U.S. residential universe.

Homebuilder Sentiment Increases, But Recovery Is Segmented

In Zaye Capital Markets, we find the NAHB July Housing Market Index bettered moderately, to 33, from the previous month on largely the better final sales expectations. Although that was a modest gain, the index has yet to recover much from the 50-neutral baseline, again supporting that home builders’ sentiment has remained soft despite the markets remaining at the over 6.5% mortgage rate, a position that has endured since 2022.

Persistent pressure from higher funding rates remains a demand drag, as the existing research of the Federal Reserve supports the direct negative correlation between purchase demand and mortgage rates. While sentiment has regained the positive tone in the barest of terms, the demand recovery remains sidetracked. Interestingly, regional patterns present a contrary scenario—Glasgow, e.g., witnessed the price of residences rise by 8.7% to £187,000 in the month of April 2025, most likely being the result of localised supply-side tightness rather than the general market upturn.

Here, we view Lennar Corp. as undervalued based upon its strong land locationing and market exposure to multi-market geographies that will benefit from regional divergences. Analysts need to keep a keen eye on mortgage rate activity and builder backlog levels in determining the merits of this guarded optimism. Sentiment remains modestly better, yet the larger market remains well short of full recovery.

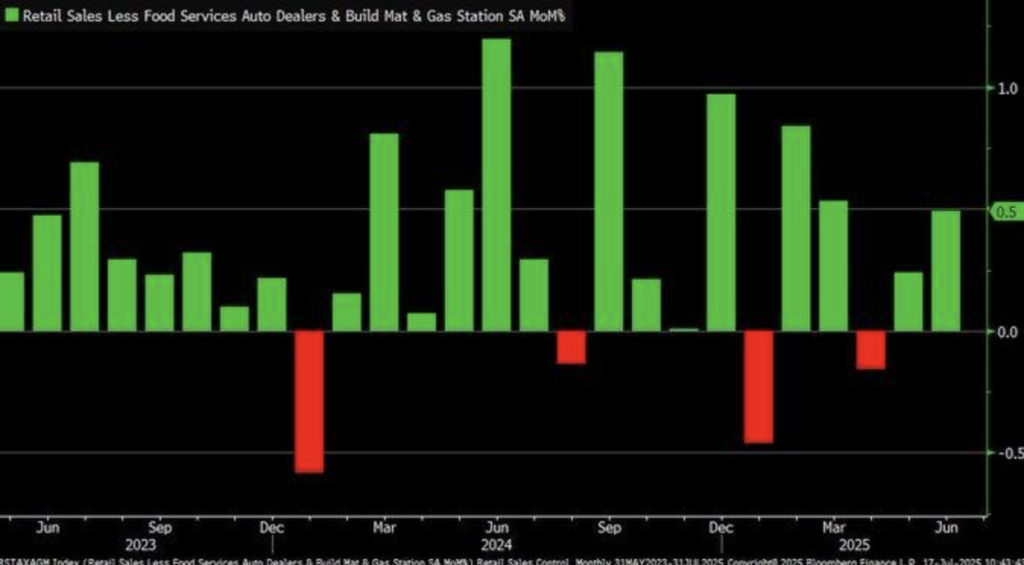

Retail Control Group Strengthens, Signaling Consumer Resilience

In Zaye Capital Markets, we observe here a 0.5% month-to-month increase in the control group of retail sales in June 2025, showing further strengthening of underlying consumer spending. It is the second consecutive increase in the refined measure, removing temporary products of car dealerships as well as gas stations, to have a more stable look at the consumption trend. The rise denotes that the consumer continues to be active even in the midst of the pressure of the tightening of finances alongside pressures of inflationary.

It follows the longer-term spending resilience trend, even despite periods of macro weakness. Control group resilience compared to the broader retail series of sales, typically subject to overstating weakness by sectoral distortions, supports our view that underlying consumer strength persists and can provide insulation against adverse industrial growth or softer labour leads. Sentiment readings continue to present conflicting signals, however, spending behaviour in real terms paints the better story of economic resilience.

We identify Walmart Inc. as being under-valued under such a circumstance, underpinned by ever-present availability of necessities in addition to constant foot traffic by price-sensitive families. Retailers’ next-term income reveals, combined with Q2 GDP statistics, will be of prime interest, consumer expenditure being the anchor stabilizing factor within the U.S. economic narrative. Leading momentum’s control group trend continues to be an important barometer.

Food Service Spending Slows, Flashing Early Signals Of Demand Fatigue

We are closely observing the recent consumer data, where the 3-month average of the monthly variation of sales of food services and drinking places slowed to 0.4% in June 2025. Following a very whipsawed interval including the -0.4% dip in mid-2024, the move presents the possibility of a turning of the page in discretionary consumer expenditures. With the sector’s high susceptibility to contemporaneous macro economic fluctuations, the trend is an early warning that is meriting attention.

This dip follows all-time full-year 2023 foodservice sales of $1.094 trillion. It would therefore now appear that inflation fatigue, as well as tightening financial conditions, are likely influencing the higher-frequency spending domains. Extended high price levels—especially of service—may thus be altering household-level spending patterns, diverting attention away from spending on discrete items. A slowing Baltic Dry Index can only fuel the skepticism of weaker demand in general, with spillover effects reaching even beyond domestic consumption.

We think that Darden Restaurants Inc. is undervalued on current levels of downside risks in the market. Color on Q3 earnings from leisure and hospitality segment, as well as forward traffic and average ticket guidance, would need to be watched by the analysts. Another decline in service sector spending would further add to fears of the cyclical downturn even before the typically responsive macro data.

Northeast Manufacturing Indices Stay At High Level

In the Zaye Capital Markets note, we see a powerful reversal in the July 2025 Empire State and Philly Fed Manufacturing Indexes, in the employment component, as indication of a breathtaking regional labour market about-face. The rise in the employment index shows better labour market recruitment prospects in the manufacturing corridor of the Northeast, after a multi-year flat spot, as a reflection of renewed resilience in the presence of overall macro nervousness.

As the broader business conditions gauge rises to 5.5—its highest reading since February—mimicking cautious optimism in regional manufacturing, the outcome thwarts national tale of labor momentum easing, with U.S. nonfarm payrolls falling to 147,000 in June. Nonetheless, the outcome works in favour of the argument that regional trends can leave headline trends in the dust. The difference here, in the context of measuring industrial America hotspots of resilience, comes into sharp focus.

We see Illinois Tool Works Inc. here as being underpriced, benefiting from diversified industrial coverage with access well into the Northeast supply chain. Reassurance in the ISM manufacturing and regional PMIs in August would be sought by analysts in order to establish whether this bounce continues through short-term replenishment of inventories. The Northeast labour fundamentals could be the template of sectoral resilience as the series at the national level unwind.

Investor Sentiment Turns Bullish, Raising Contrarian Signals

At Zaye Capital Markets, we are aware that the AAII Investor Sentiment Survey moved into a slightly bullish direction, with 39.3% of the membership now being positive—just above its long-term average of 37.5%. While not extreme, the move follows a recent high and points to similar to prior patterns we have seen at market highs. Research has indicated that such moves in sentiment are later followed by corrections within the 6-12 month realm, especially if optimism moved up without the macro pressures unwinding.

The latest turn in sentiment falls during a period of temporary global policy strain, with the U.S. Treasury quantifying tariff revenue gains over and above broader concerns about potential spillover. Investor sentiment perhaps is showing over-optimism in fiscal results, citing past examples of confidence being ahead of the fundamentals. While a positive spread in itself is not bad, the timing thereof—coupled with the ongoing economic risks—deserves caution, especially with GDP growth still at a modest 2.1% rate on an annualised basis.

We still view Procter & Gamble Co. as being undervalued in this atmosphere, offering defensive support in the event of sentiment being turned around. Sentiment gauges must be supported by macro data such as PMI momentum change and direction change of earnings in order to further determine market alignment. Bullish sentiment willmost likely provide short-term ramps, yet we are apprehensive of speculation and position unwinding that will probably cap upside the next quarter.

Input Costs Climb While Supply Chains Stabilise In Manufacturing

We are keenly monitoring Philadelphia Fed July 2025 Manufacturing Index figures, which disclose a strong increase in the “Prices Paid” gauge, signaling growing input cost pressures in U.S. manufacturing. It can be employed to alert inflationary pressures within the manufacturing pipe, as has happened all too often in the past, with the increase in inputs being the leading predictor of general inflation, aided by unrelenting demand.

Conversely, the concurrent decline in the “Supplier Deliveries” index indicates expeditious delivery, a reassuring development that portends the lessening of supply-side constraints. The gap here is significant—it would implicate that while the manufacturing sector incurs the higher input price, logistical refinement may check the intensification of the inflationary torque. Endemic supply-side refinement may contain the impact of cost pressures and allay the specter of stagflation, even as this has appeared in the aftermath of the recent threat of geopolitics, including U.S.-Iran tensions that impinge upon global trade flows.

Emerson Electric Co. to us looks cheap on the strength of its process optimization and automation operating leverage, where short supply cycles are a blessing. Anybody would want to monitor the August PPI to see if the trend holds. Whether the home producers succeed in passing through higher costs without sacrificing the margin will be the best indicator of industrial sector strength to the rest of H2 2025.

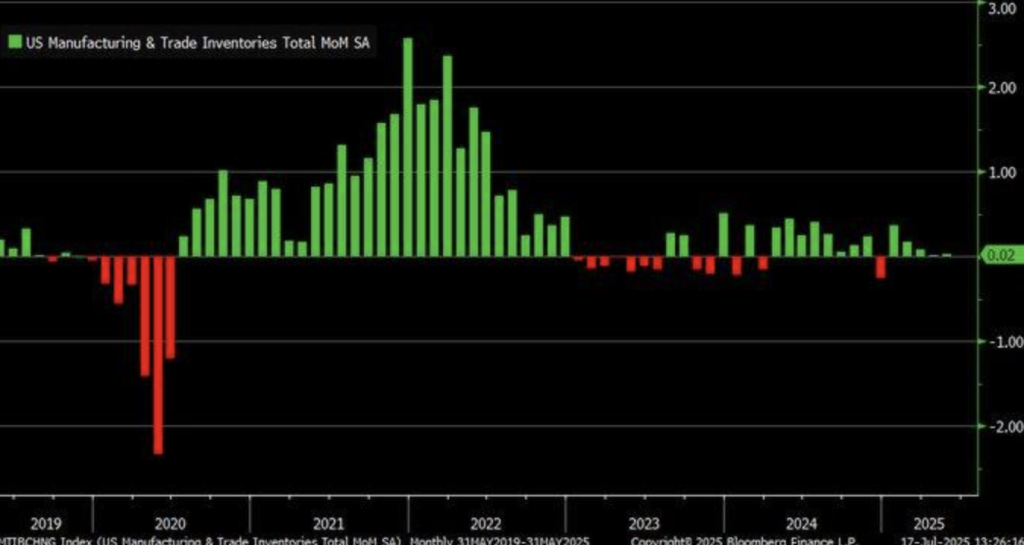

Flat Inventories Hint At Caution As Sales Momentum Fades

In Zaye Capital Markets, we see that US manufacturing and trade stocks in May 2025 stayed neither up nor down at $2,656.5 billion, the second month in a row. After uncertain accumulation of stocks since 2020, the stability signals change of agenda of business—more likely the indication of either less optimization of the supply system or fading growth of demand. Although the flatness falls short of the prior optimism of being overstocked, rather, indicates concern about broader economic momentum.

For this purpose, April’s 0.1% sales decline is consistent with fears of declining consumption. Historical precedents connect idle inventories in declining sales months with pre-recession months due to companies shying away from stocking in anticipation of decreasingly lackluster follow-through demand. Timing also coincides as the OBBB tax reform, in July 2025, comes into effect, realigning the bonus depreciation rules—most likely in a way intended to discourage speculative stocking investments by altering the capital rationing incentives of the firms.

We continue to regard Oracle Corporation as cheap in the setting, through the virtue of lower exposure to physical inventory risk and strong repeat revenues. Q3 inventory-to-sales ratios and the new tax environment capex trends will be closely of analyst interests. Fiscal incentives vs. inventory discipline will be a changing corporate behavior through the year-end, giving insight into cyclical resistance and demand expectations.

UPCOMING ECONOMIC EVENTS

Calm Before the Storm: Markets Look for Key Clues

There isn’t much new in the economic agenda for the day, so the market players are in wait-and-see mode. Without any important releases scheduled, the markets are simply floating on the heels—digesting new data and hedging positions in consideration of what will be a climactic series of new updates.

In Zaye Capital Markets, we interpret this silence as not of absence, but of introduction. The silence of the day a precursor of what lies down the road, that can offer much-needed direction on the consumer sentiment, as well as general economic direction. Volatility can be kept at bay now, yet direction of market-defining events can be around the corner.

We advise staying invested. Over this quiet time, there is a valuable chance to go over portfolios and position for possible high-leverage communications during the subsequent days. Tomorrow the true story develops.

STOCK MARKET PERFORMANC

Stocks Rally From April Bottoms, Internal weakness Extremely Pronounced

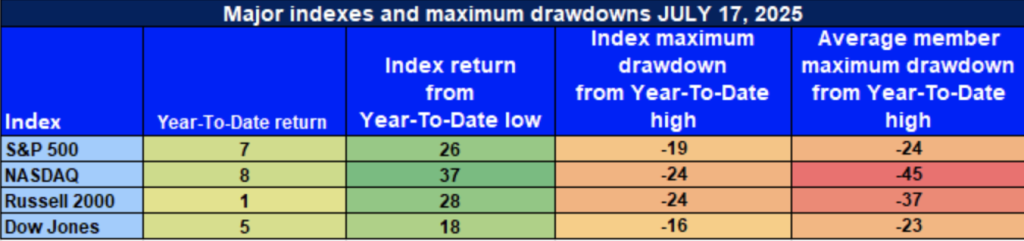

In Zaye Capital Markets, we can see that even though the key U.S. gauges are surging significantly after bottoms formed on the 8th of April, the breadth of the rally remains a concern. At the index level, the strength persists, yet the YTD high drawdowns and average member loss tell much about a market that remains troubled by valuation stress, sector distortions, and frags of participation.

S&P 500: Front-page Resilience, Behind the Scenes Stress

YTD: +7% | -26% lower than April low | -19% lower than YTD high | Average member: -24%

7% YTD return and healthy bounce from April low of S&P 500 are comforting, but 19% decline from highs and average member decline of 24% indicate that leadership is still concentrated at the top. We are witnessing evidence of the underlying deeper structural weakness in the index.

NASDAQ: Tech-Led Rally Confounds With

YTD: +8% | +37% from the April low | -24% from the YTD high | Avg. member: -45%

NASDAQ has led the way in the rebound, up 8% year-to-date and 37% above the April low. But with a 24% fall from the highs and a startling average member drawdown of 45%, risk exposure in the growth stocks is still high and disproportionately weighted.

Russell 2000: Small Caps Take Center Stage Amid the Rally

YTD: +1% | -28% lower than the April low | -24% lower than the YTD high |Avg. member: -37 While the Russell 2000 increased by 28% in the month of April, its 1% YTD gain and general drawdowns negated. Investor hesitancy persists within the small-cap spaces, while earnings visibility and liquidity still remain uncertain.

Dow Jones: Overall Stability, But Weakness Still Exists

YTD: +5% | -18% below April low | -16% below YTD high | Avg. member: -23% Its 5% YTD return and small 16% drawdown are a relative stability source due to its defensive character. Average member loss of 23% indicates, however, that the index is not exempt from typical market jitters. We continue at the firm level to maintain our focus on capital preservation and risk allocation. Divergence among indices also requires that we be selective to be long quality stocks. Recovery in breadth continues to be the most critical indicator in determining market resilience.

STRONGEST SECTOR OF ALL THESE INDICES

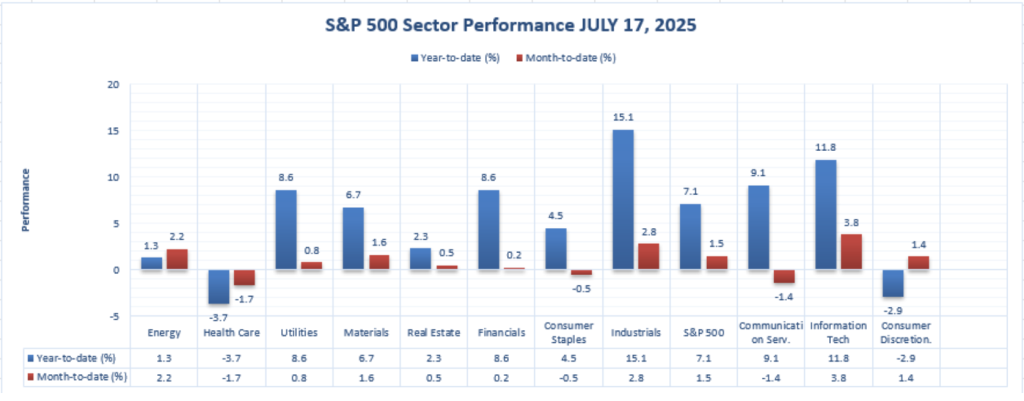

Industrials Lead the Sector with Across-The-Board Gains

In Zaye Capital Markets, we see that Industrials up to now steadfastly remain ahead of all other S&P 500 industries year-to-date, once again becoming the top performing sector within the ongoing cycle. Up to now, through mid-July 2025, the sector has risen 15.1% YTD, fueled by another 2.8% hike month-to-date, reflecting ongoing demand in the defence, aerospace, and industrial equipment niches.

It originates from structural resilience, in addition to investor demand for price-power sectors, multi-end markets, as well as supply-chain adaptability. With macro uncertainty remaining, in the face of capital spending staying on the mend, Industrials are in a good position to take advantage of US infrastructure spending, alongside reshoring. Line that up next to sectors like Health Care (-3.7% YTD) as well as Consumer Discretionary (-2.9% YTD), hurt badly by cost pressure, alongside margin squeeze.

We are positive in our view of the sector and view Honeywell International Inc. as being discounted based on its exposure to green technologies and automation. Analysts should be waiting to see the release of the next PMI data and US infrastructure plans, which are further sources of the sector’s potential outperformance. Rotation into the industrials looks valuation-driven as well as macro-helpful.

EARNINGS

July 18, 2025 – Earnings Summary

- American Express Company

American Express reported a good Q2 result with $17.9 billion of net revenue, 9% year-over-year growth, and earnings per share (EPS) of $4.08, beating estimates. The result was powered by high card spending growth and premium member stability, further demonstrating the firm’s leadership within the high-income consumer’s market. The shares decreased, however, after the release as markets struggled to come to terms with the management’s cautious outlook on competition pressures and macro headwinds that are likely to dampen the growth in the subsequent periods.

- Charles Schwab Corporation

Charles Schwab announced robust Q2 earnings, adjusted EPS of $1.14, and net income of $2.2 billion. Total client assets of the company increased 14% to $10.76 trillion, on the back of robust trading in market turbulence. The market welcomed the steady increase in fee income, and in the trading revenue of the Schwab, the shares achieving new record-highs. The figures confirm that the investor trust in the hybrid model of the company, and in the digital growth model, remains steady.

- 3M Company

3M surpassed expectations of adjusted EPS of $2.16 on revenues of $6.2 billion, based on a 290-basis-point expansion of the margins. Management upped its full-year EPS guidance to the range of $7.75–$8.00, citing successful reduction of the costs, in addition to cushioning of the tariff pressures. Even though the outlook bettered, concern was registered about the persistent softness in several industrial markets, about which the management made statements in the earnings call.

- Truist Financial Corporation

Q2 Truist Financial falls short of market expectations, non-interest segment, and the trading segment, missing the mark. Although the core loaning was flat, sub-par fee-driven revenue kept the EPS lethargic. Pressure on the margin, related to duller capital markets activity, reflected in the tone of the bank, kept the market in suspense despite the credit profile being reasonable.

July 21, 2025 – Stocks watchlist

- Verizon Communications Inc.

Pre-earnings for Verizon releases today, with the region of most attention being the trend of wireless service revenues, as well as subscriber additions. Levels of Capital Expenditures will also be of attention, the reason being the ongoing 5G rollout. Margin quality, as well as churn, would be the measure of operating resilience, the telecom space under price pressure.

- Roper Technologies, Inc.

Premarket, Roper will release earnings, highlighting its industrial software and technology segment. Durable growth in sources of recurring revenues, anticipated. Whether the revenues keep the double-digit growth, the margins as well, will be the focal points, at least in the aftermath of strong enterprise demand, acquisitions.

- NXP Semiconductors N.V.

NXP will report after the markets close with market expectations of $2.66 of EPS and $2.9 billion in revenue. Automotive and industrial demand within the end-markets will be of particular interest, along with guidance in the future in the context of continued global rebalancing of chips. Inventory levels, as well as prices, will be keenly watched.

- W.R. Berkley Corporation

We will be hearing from W.R. Berkley after the market closure, and looking at underwriting profit trends, reserving development, and investment earnings. Higher yields being in the mix, investment portfolio return-on might be maintaining earnings, loss ratio softening being of concern to general insurers.

- Steel Dynamics, Inc.

Steel Dynamics is to report before the bell, and investor focus will be on volumes delivered, price realisation, and margin squeeze. The company’s report will be a proxy for industrial demand as well as the cost inflation dynamics within application of the steel related to construction and motor vehicles.

- Domino’s Inc.

Before the market opens, Domino’s will also report earnings, with same-store sales growth in the domestic and international regions in focus. Analysts would want to see how the pressures in commodity prices and promotion prices are affecting the margins, against a softening consumer environment.

We are putting extra focus at Zaye Capital Markets on such consumer durability, industrial demand, and margin strength earnings forухs, all of which are key to navigating through the second half of 2025.

Stock Market Update – Monday, 21 Jul 2025

Markets began the week cautiously upbeat, with market participants citing next week’s earnings, expectations of monetary policy, as well as lingering trade tensions. Although thin economic data materialized during the day, there remains sentiment also too prone to geopolitics and forward guidance by the mega-caps. The equity atmosphere indicates a split scenario—large-cap techs are supporting the larger tape despite the lagging of the smalls as well as the cyclicals.

Stock Prices

Geopolitical Events and Economic Indicators

Attention is kept on direction of earnings and rate path completion. Optimism regarding persistent consumer spending and positive employment readings in firms is being tempered by risk of tariffs and international trade tensions. Participants will be seeking validation in the subsequent earnings round to support position, in the aftermath of the sustained dovish tone adopted by the Federal Reserve. At the same time, soft inflation prints are supporting the case for potential policy accommodation in the second half of the year.

The Magnificent Seven and the S&P 500

S&P 500 still relies on the Magnificent Seven. Microsoft, Meta, and Nvidia leadership has in turn been supported by strong AI-driven earnings. Tactical errors and regulatory issues, however, await Apple, Alphabet, and Tesla. Tesla, in fact, has been hurt by weakening EV demand alongside leadership distractions. The gap further decreases the index’s breadth, with the growth being even more concentrated among the winners.

Top 10 Construction Companies of the Future

We hold long on infrastructure growth stories—Stocks that we feel are designers of the future industrial and digital age. Some of our favorite long growth ideas are:

- $PLTR – the workhorse of real-time AI deployment

- $AMZN – the unrivaled giant of electronic commerce and cloud;

- $AXON – public safety’s digital command system

- $NET – protecting and optimizing the global internet infrastructure

- $CRWD – leading the charge in safeguarding cloud-native ecosystems

- $RKLB – space logistics and launch capability redefined;

- SNOW – delivering data liquidity for AI scaleability

- $MELI – powering the e-commerce and fintech stack of Latin America;

- TSLA – leading the vanguard of mobility, robotics, and AI integration;

- $RBRK – facilitating decentralized data protection solutions.

These businesses are not simply working in their industries—they are building the long-term economies in which they operate. These retreats are being acquired in the long-term accumulation positions in the stocks.

Major Index Performance as of July 21, 2025

- S&P 500: 627.58, down 0.07% on the day.

- Nasdaq Composite: Currently near 561.26, dipping 0.10% on the day.

- Dow Jones Industrial Average: Moved little to mildly higher, helped by defensive stocks.

- Russell 2000: Still modestly behind, however overall sentiment around the small-caps remains subdued.

Our outlook at Zaye Capital Markets remains cautiously optimistic. The short-term earnings, breadth confirmation remain in focus, with the next leg of stocks going to need broader participation, fundamental support.

Gold Price – Monday, 21 Jul 2025

Gold stays close to $3,353.80 an ounce, still in charge after investors balanced a series of politically charged remarks by President Trump with a lackluster economic agenda. Trump’s latest call for Federal Reserve cuts in the face of interest rates—thanks to tariff-induced inflation—and warning words on BRICS and the trade war fueled additional safe-haven demand. Meanwhile, tensions in the Middle East over Israel in Syria and Gaza military attacks and fresh unrest in immigration and legal accounts are keeping the hedging role of gold. With no heavy data due out today, sentiment remains extremely sensitive to anything in the realm of politics and speculation over monetary policy, thus placing pressure on the psyche of defensive markets such as gold.

In spite of improved-better-than-anticipated retail control-group numbers on Friday, improving on what normally supports the bond yield and strong dollar, but gold prices still holding firm. Consumer spending resilience suggested in the data could make life challenging for Fed loosening bets, but the precious metal continues to gain from ubiquitous uncertainty elsewhere. It is a story of two narratives that shape the gold universe: robust home fundamentals on the one hand, uncertain trade policy, Fed skepticism, and political noise on the other. From our view at Zaye Capital Markets, we believe the setup supportive of gold in the near term, with price action set to stay positive as long as clarity on the political and macro fronts remains uncertain.

Oil Prices – Monday, July 21, 2025

Crude now trades around $78.50 a barrel, flashing the continuation of volatility as markets struggle to process mixed signals between supply flows and macro stories. Although OPEC recently said a few producers would start voluntary cuts, support at the bottom, the IEA nonetheless cautions dwindling demand prospects in key importers, dampening sentiment. American shale has however remained resilient, with stock jumping, adding bearish pressure. Zero Hedge, among Bloomberg analysts, also blame softer refinery margins, lethargic risk appetite in commodities, among key headwinds, even as supply outlooks broadly hold steady around the world. With no relevant economic data up for release today, market participants are taking focus at the geopoliticial noise, among stocks expectations, into the week.

Trump’s latest comments calling for Fed rate reductions amid inflation-ignited by tariffs is fueling the commodity debate. Otherwise, softer dollars benefit commodities like oil, but the macro backdrop here isn’t making that trade so easy. Tariff tensions, combined with perceived U.S. foreign policy uncertainty—particularly by BRICS nations, Middle East countries—adds yet another geopolitcal risk premium to the mix. Mood in risk markets was boosted by positive U.S. consumer spending reports yesterday, indirectly supporting oil via expectations of rising consumption. With that caveat, light economics data this morning has oil in a technical standoff, contained by any OPEC news, or change in U.S. stockpile reports later this week. At Zaye Capital Markets, we are closely monitoring for drawdowns in the warehouse and any surprise policy adjustment that can tip the needle either way.

Bitcoin Prices – Monday, 21 July 2025

Bitcoins are trading around $117,978 levels, a modest decline from the recent all-time high of around $123,000 that it had touched in the vicinity of the “Crypto Week” booster. The booster was triggered primarily because President Trump signed into law the approval of the passage of the GENIUS Act, an unprecedented action that entrenched stablecoin regulation in law and made the Bitcoin holdings a national asset. The legislative change is a revolutionary shift in U.S. digital-assets policy. This tide of pro-regulatory sentiment might have fueled strong institutionally driven demand and encouraged market capitalisation to over $4 trillion, but Bitcoin has moved into a consolidation process with market players waiting for newer breakthroughs on how the rules of the treasury will be divided and implemented.

Recent commentary by Trump has added yet another layer of bullish tailwind to the Bitcoin ecosystem. Trump’s call for Federal Reserve rate decreases in the face of tariff-driven inflation has generally been interpreted to be positive for crypto markets, themselves preferring a lower-interest-rate environment. Trump’s repeated support of digital assets—ranging from his support of Bitcoin testimony in the House of Representatives to support of crypto-friendly appointees—has similarly raised the profile of Bitcoin as a legitimate alternative asset. While strong retail sales data yesterday has supported further economic strength, the data has also tempered much of the speculative fervor behind the recent Bitcoin price increase. Here at Zaye Capital Markets, we continue to believe that Bitcoin remains in a structurally bullish environment, however, short-term volatility will be the norm as market participants await the timing of regulatory developments alongside the macroeconomic policy responses.

ETH Prices – Monday, 21 July 2025

Ethereum traded at around $3,750 per token, in the frenzied spike that has shot the asset to six-month highs. Attributable to ratcheting institutional demand, the spike in the past couple of weeks—more than 40% month-to-date—was prompted by U.S. spot ETH ETFs reaching all-time buying volumes. One day registered flows of upwards of $727 million, with net flows of upwards of $2 billion since early July. Whale demand has also picked up, with one of the larger buyers said to have made a purchase of $50 million in ETH at the weekend, taking cumulative purchases of the token by wallet whales to upwards of $260 million in recent weeks. These have shot ETH to near the $3,800 resistance level, with rising expectations of spiking through to $4,000 if institutional demand fails to relent.

Tuesday’s upbeat retail control-group data supported market sentiment in risk assets, therefore backing the surge in Ethereum. Improved economic data obviously puts pressure on crypto due to the risk regarding interest rates, but Ethereum more and more looks less correlated as being caused by ETF momentum as well as whale accumulation instead. Without any of the major economic releases on the day, ETH can now be traded solely on crypto-specific information. At Zaye Capital Markets, we believe the near-term trend remains structurally bullish. However, we are keeping a close eye on ETF flow sustainability as well as on-chain whale accumulation as major pointers to whether ETH can maintain the surge or stabilize near the current levels.