Where Are Markets Today?

As of Wednesday, September 17, 2025, futures for both U.S. and European markets are trading slightly higher, which is a reflection of a cautious optimism mood. U.S. S&P 500, Dow, and Nasdaq futures are up slightly, with Euro Stoxx 50, Germany’s DAX, and London’s FTSE futures also rising slightly within Europe. The slight increase is a prelude to a critical Federal Reserve policy meeting later in the day where a 25 basis-point reduction is expected to take the federal funds to a 4.00%–4.25% region. However, the real area where investors’ attention is centered is not where a reduction is being made but where Fed Chairman Jerome Powell speaks with his comments and revised dot-plot guidance. These will indicate if additional reductions are forthcoming prior to year-end. Thus, futures are being cautious but slightly optimistic.

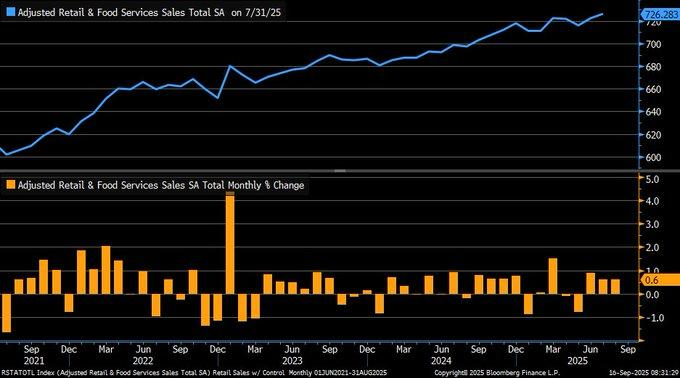

Yesterday’s economic data is dictating much of the sentiment. American retail sales gained a stronger-than-expected 0.6% in August as import and export price indices were higher than anticipated to signal ongoing inflationary pressures. Meanwhile, weakening labor market data continues to keep recession risks alive to complicate a messy backdrop. The outcome is a futures market having priced in the first cut but is still reluctant to commit to a wider rally until a clearer picture is painted by the Fed regarding inflation or growth risks dictating policy perspectives. Gold surging near historic tops and a weakening American dollar further highlight that investors anticipate dovish undertones but hedge for future volatility. The tone is also measured in Europe. Euro Stoxx 50 futures rise about 0.35%, the DAX up 0.4%, and the FTSE higher by 0.2%. Hopes that U.S. monetary easing will trickle down to help lift European shares, increasing region-wide liquidity and confidence among investors are behind optimism. Gains, however, stay contained as eurozone inflation again displays stickiness to keep the European Central Bank on guard. Traders recognize that any euro gain versus a weaker greenback might hammer export-facing European sectors to contain upside room for local bourses.

Adding to the cautious tone are geopolitical dynamics. Trump’s latest remarks—urging Europe to halt Russian oil purchases, highlighting trade tensions, and pressing for Fed independence—are reinforcing uncertainty across asset classes. Energy markets remain on alert after reports of disruptions at Russian refineries and ports, which could tighten supply. At the same time, ongoing concerns about tariffs and trade disruptions contribute to a higher geopolitical risk premium in both equity and commodity markets. Against this backdrop, futures are moving higher but only incrementally, reflecting investor preference for holding back until Powell provides clearer direction later today. At Zaye Capital Markets, we view this setup as one where measured optimism is prevailing, but the path forward will depend heavily on how central banks balance inflation control with growth risks.

Major Index Performance Through Wednesday, September 17, 2025

- S&P 500: 6,606.76, down 0.13%

- Nasdaq Composite: 22,333.96, down 0.07%

- Dow Jones Industrial Average: 45,757.90, down 0.27%

- Russell 2000: 2,403.03, down 0.10%

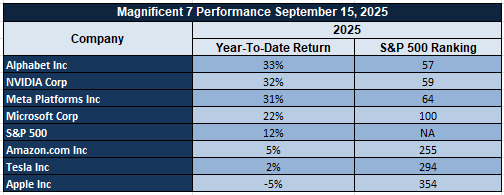

The Magnificent Seven & S&P 500

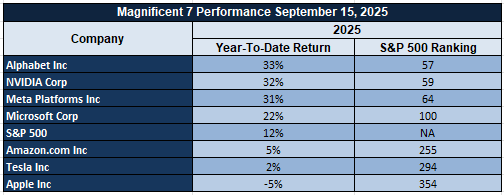

The “Magnificent Seven” continue to sell off, with a combined drawdown averaging over 18% off recent highs. Nvidia and Meta lead the down moves as pulled valuations intersect with profit-taking and rate angst. The S&P 500’s recent strength appears increasingly fragile, relying heavily on these mega-cap names and therefore calling into question sustainability. Energy and industrials are providing some offset, but with a lack of renewed leadership from the core tech leaders, the index is struggling to maintain upside momentum.

Drivers Behind the Market Move

1. Fed Expectations Based Upon Inflation & Consumer Statistics

Investors respond to stronger-than-expected U.S. consumer data —particularly August retail sales beating estimates and import/export price indices running hotter than anticipated. These inflation indicators are reaffirming our view that despite a widely anticipated 25 basis point rate reduction at next month’s Fed meeting, the central bank might be more reluctant to go much further than that absent stronger cooling signals. Accordingly, markets are positioning positively but discounting some easing with caution with Powell’s forward guidance and what the dot-plot might be saying about additional reductions later this year. The fall in treasury yields (short-term especially) and a weaker dollar indicate that inflation expectations remain an integral part of the equation.

2. Trump’s Trade, Tariff & Policy Rhetoric Rising Risk Premiums

Trump’s recent comments — calling on Europe to stop buying oil from Russia, insisting that the Fed must be non-politic but responsive, reinforcing that tariffs will be applied to reduce debt repayment, calling for closure to TikTok / China trade disputes — inject geopolitical risk into investors’ arithmetic. They add risks related to disruption of trade, supply chain tightening, even political stress to institutions like the Fed. Uncertainties like these have a tendency to boost risk premiums that beget caution among investors about broad equity exposure and a preference for sectors seen to be safer or better placed to take advantage of policy decisions (energy, defense, exporters).

3. Global & European Inflation Pressures Firm Up ECB Watch

Headline inflation in Europe has increased to ~2.1% yr-over-yr in August (slightly higher than expected), with core elements in select countries remaining high. Consumer sentiment also continues to highlight inflation as a leading concern. As recent ECB decisions left rates unmoved, its own communication indicates it is data-dependent and could revise course. Trading is currently offsetting U.S. easing expectations against spillover risks: a stronger euro or renewed pressures from energy or services would slow European exporters and forestall ECB easing. Accordingly, futures in Europe are slightly higher but is held back by these inflation dynamics.

At Zaye Capital Markets, our take is that these three drivers—consumer strength & sticky inflation, policy risk led by Trump, and differentiating central bank pressures—are today’s market movers’ principal levers. Investors tread a tightrope: leaning optimistic about policy loosening but sensitive to what will be necessary for central banks to provide it without fuelling inflation or yielding to political commentary.

Digesting Economic Data

The TRUMP Tweets and Their Implications

Trump’s recent batch of comments provides a broad glimpse into his economic and geopolitical agendas with ramifications throughout trade, monetary policy, and international relations. On the macroeconomic side, his repeated assertion that “tariffs will pay for the debt” clarifies his support for tariffs as a revenue generator and bargaining chip. In conjunction with comments that if inflation were a pressing issue “he’d be okay with having hikes,” the signal displays a willingness to alternate dovish and hawkish strategies based on perceived homegrown pressure. It generates increased market uncertainty because investors have to build into currencies, equities, and commodities more volatility whenever tariffs or Fed independence is called into question.

The TikTok saga is still at the heart of Trump’s agenda, with rhetoric ranging from “we have a deal on TikTok” to conceding China’s final approval over the agreement. He has insisted that various huge U.S. companies want to acquire TikTok’s U.S. business and has hinted that he is prepared to allow the platform “go dark” should conditions not be met. It is a harder line with respect to technology transfer and digital sovereignty, supporting U.S.–China rivalry across strategic sectors. Investors should be aware that such bluffing impacts valuations for tech directly but also contributes to wider trade tensions that might spill into supply chains, capital markets, and currencies. Geopolitically, Trump’s comments reveal a belligerent tone toward Russia and Europe. Trump’s persistent claim that “Europe must stop buying oil from Russia” fits with wider U.S. policy objectives but runs a risk of further volatility to energy markets. At the same time, his comments regarding NATO, auto duties, and tariffs reveal ongoing tension with allies. With his insistence that Ukraine’s President Zelenskiy “will have to make a deal” with Russia’s Putin despite their animosity towards one another—Trump is revealing a desire to shake up realignment in Europe that has the potential to redraw risk analysis to energy, defense sectors as well as overall global stability. Such commentary injects considerable geopolitical premium into foreign exchange and commodity markets.

Lastly, Trump’s dual insistence that “the Fed has to be independent” but also “listen to the people” manifests the perpetual tension between political pressure and central bank credibility. In signing documents to appoint Miran to the Fed, Trump is assuring his imprint reaches into the policy-setting framework, which would bias expectations toward looser or politically responsive monetary policy. For markets, that would imply more-frequent recalibration of rate and inflation expectations, with safe-haven currencies such as gold and Bitcoin set to benefit whenever concerns about credibility emerge. In our view at Zaye Capital Markets, these comments represent a reminder that volatility throughout currencies, commodities, and equities is here to stay, thereby necessitating diversification and selective positioning more than ever.

Consumer Strength vs. Structural Weakness

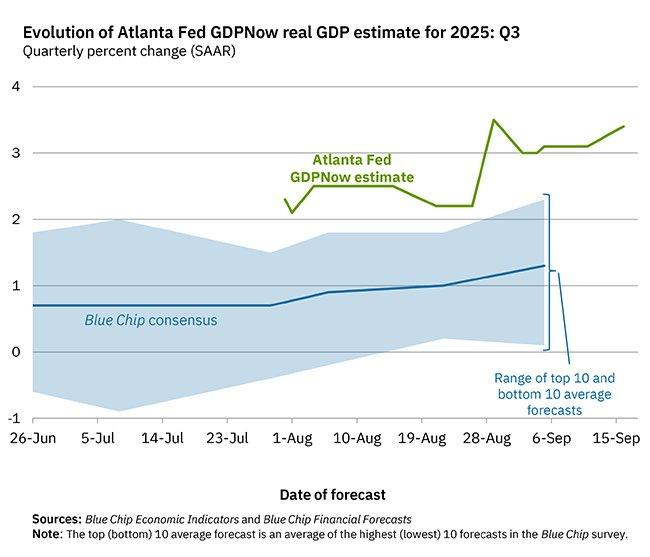

Atlanta Fed’s GDPNow tracker has upgraded its U.S. Q3 growth estimate to 3.4% year-on-year from 3.1%, stronger August retail sales driving an upside revision. In stark contrast to sub-2% market consensus from Wall Street, it suggests that consumers are stronger than anticipated despite prior concerns about a slowdown. It is a sign of surprising momentum among household demand that puts a more positive spin just days ahead of markets preparing for Federal Reserve’s policy meeting on Sept 17–18. For stock investors, undervaluation is strongest among some consumer discretionary names where pricing power as much as steady demand would warrant near-term upside.

Below that headline strength, residential remains a drag to growth. Supply shortages of nearly five million units are constraining labor mobility, limiting affordability, and generating risks to longer-term economic flexibility. For as long as demand for residential is structurally robust, affordability concerns keep a squeeze on homebuilder valuations. Such a disconnect between supply and demand is a signal, though, that homebuilder shares could be discounted relative to their longer-term growth trajectory, with analysts being prompted to watch policy incentives or supply-chain relief that could release value. This GDPNow update complicates the near-term picture for the Fed. A 25-basis-point reduction is near-unanimously anticipated, but the appearance of loosening policy into a 3.4% growth environment might be perceived as testing credibility, particularly with inflation risks lingering. But data for labor indicating 4.3% unemployment is cause enough to be cautious. Such a divergence—healthy consumer activity vs. labor soft—provides mixed signals. Look for simplification in Fed commentary because financials might face margin pressure with loosening, but growth-sensitive tech names look discounted should liquidity improve.

Housing Sentiment Signals Fragile Stability

NAHB Housing Market Index remained stagnant at 32 in September 2025 with no improvement from previous months and reflecting the fragile sentiment within the industry. Trending lower throughout history since the 2008 financial crisis, the index is an indicator of continuing influences by high borrowing costs on activity among buyers. Prospective traffic dipped to 21 reflecting pressures from a lack of affordability, with present sales staying even. The divergence indicates that residential is still a structural drag to overall growth despite consumer spending elsewhere remaining stronger. For investors, undervaluation is present within homebuilders where long-term demand is stronger than supply being restricted. Near-term volatility should be taken into consideration.

Leading indicators present a mixed scenario. Future sales expectations edged up to 45 from 43, reflecting prudent optimism amidst soft buyer traffic. It indicates the tug-of-war between rising financing costs and core demand resilience. Affordability trends and policy interventions to alter momentum deserve close attention from analysts as ongoing improvements to financing conditions could present upside to fair-valued real estate shares. Conversely, construction activity-related housing providers face vulnerability if higher rates persist to deter new starts. The seasonality to date for subdued housing sentiment has particular relevance going into November’s U.S. presidential election, where policy hopes can induce volatility among interest-rate sensitive sectors. There is historical precedent for housing indices to react to election periods’ fiscal and regulatory changes, so the next couple months represent an important compass point for establishing direction. From an equity positionning standpoint, undervalued plays continue to be found among housing-connected companies possessing good balance sheets and pricing strength, but overall market observers should be aware of political events that can redistribute sentiment throughout real estate and financial sectors.

Industrial Output Shatters Weakness Myth

U.S. industrial production rose by a seasonally adjusted 0.1% in August 2025 to a surprise to the upside from a tepid fall predicted. Factory output gained 0.2%, reversing some of last month’s downturn and reflecting strength in a sector commonly squeezed by high interest costs. As the overall economic story has been one of deceleration, a positive reassessment here indicates industrial activity is remaining stronger than hoped to temper concerns about a one-size-fits-all slowdown. In equity markets, undervaluation is seen in individual industrial names benefiting from trends toward automation and gains in productivity where structural trends facilitate a re-rating.

Outperformance/underperformance between industrial production and healthy consumer spending indicates a diversified economic landscape. Retail sales jumped 0.6% in August to $732 billion, suggesting healthy household demand despite lagging production trends. Such mismatches throughout history signal transition periods within the business cycle where some sectors transition quicker than others. Investors should monitor closely if momentum in manufacturing is maintained or if consumer strength peaks as discretionary retailers and durable producers would be most vulnerable to cross-currents. Undervalued sectors would be industrial companies whose businesses would be positively positioned to take advantage of capex-driven efficiency as a response to consumer-driven demand. The timing of this industrial rebound is critical, arriving just ahead of the Federal Reserve’s policy meeting. With GDP growth tracking higher and consumer demand strong, the case for immediate policy easing becomes less straightforward. However, mixed signals from labor markets and sectoral imbalances keep the door open for cautious adjustments. For investors, financials may face compression risks if easing persists, while industrials and select manufacturers remain undervalued as resilient demand trends counter cyclical headwinds. Analysts should monitor Fed communication for clarity on how structural shifts across sectors influence the central bank’s longer-term policy stance.

Services Vulnerability Exposes Risks of Recession

The New York Fed Services Index fell sharply to -19.4 in September 2025, marking one of the steepest declines in recent years. Historically, such deep contractions have preceded periods of economic recession, most notably during 2008–2009. This deterioration in business activity underscores mounting pressures in the services sector, a critical driver of U.S. economic output, and challenges the prevailing narrative of broad-based resilience. For investors, undervaluation is most apparent in defensive consumer staples, which tend to hold pricing power when cyclical sectors like services signal weakness.

The timing of this downturn is notable, as it contrasts with earlier consensus that a recession would not materialize until 2026. The sharp decline indicates that the slowdown may be accelerating faster than anticipated, raising questions over the durability of recent consumer-led growth. Analysts should focus on service-heavy equities, particularly in hospitality and transportation, where earnings expectations may prove overly optimistic. Within this setup, undervalued opportunities can be found in quality healthcare and utility names, offering stability as services activity contracts.

Ongoing services index softening is commonly associated with labor market stress because risk-averse business practices manifest as reduced hiring or even layoffs. Coming off a rise in unemployment already, a threat of overall labor softening cannot be discounted. For investors, that leaves a tactical landscape where cyclical-sensitive sectors such as discretionary retail could be vulnerable to the downside but undervalued industrial companies with good balance sheets better placed to withstand a protracted contraction. Investors should keep close watch on services sentiment versus job market data as a leading indicator for policy reactions as well as portfolio tilting.

Trade Prices Reflect New Inflation Pressures

The U.S. Export and Import Price Indices gained 0.3% m/o/m in August 2025, better than market expectations for gentler readings. Import costs were anticipated to decline on the heels of a strengthened greenback but instead indicate supply-chain bottlenecks and persistent demand remain a source of inflationary forces. Export costs also gained more than anticipated to signify robust interantional demand for American products. Taken together, these data refute optimism about fading trade-related price pressures, further muddling near-term disinflation expectations. Undervaluation is also evident within export-based industrials where stronger international demand is possibly not yet fully captured in profits.

Divergence from expectations signals a miscalculation concerning exchange rate impacts because so few U.S. transactions take place with a non-dollar currency. Limited pass-through thus dilutes the ability for the dollar to curb import costs, making U.S. buyers vulnerable to supply shocks from abroad. In our view, analysis should most intensively center on import-sensitive companies—retailers and manufacturers who depend heavily upon their foreign procurement components—because margin pressures remain higher here. Exporters with pricing discipline might gain instead because most undervalued names with our coverage lie among agriculture names as well as energy-related names with a strong external demand. Revised higher prior data for export prices strengthens arguments for resilience in U.S. trade flows to emerging markets. Such resilience makes it more difficult for Federal Reserve policy because higher trade prices indicate inflation threats just as markets expect a loosening by the Fed. In equity positioning, undervaluation is found among globally diversified companies with good pricing power, but rate-sensitive sectors might come off badly if inflation pressures defer or diminish the size of reductions. Traders should watch future trade reports as well as Fed guidance to allow cross-border demand to cushion effects from sectoral softening domestically.

Retail sales exceed expectations but credit risks remain near

U.S. retails sales jumped 0.6% month-to-month in August 2025 to $732 billion, tripling expectations for a 0.2% increase. Our control group that directly enters GDP computation increased by 0.7%, a signal that household demand is a strong growth engine. Year-on-year sales gained 5.0%, paced by sharp increases in e-commerce (+10.1%) and food services (+6.5%), emphasizing consumer-facing sectors. Investors most obviously see undervaluation in select consumer discretionary and e-commerce names where spending momentum has yet to be adequately priced into equity valuation.

Underneath the headline strength is a glimpse of vulnerability. At an inflation-adjusted measure, real demand is possibly flat instead, putting sustainability into question. Increasing credit usage indicates that households might be straining to support current expenditure. Retailers with exposure to low-income groups should be most concerned about increasing costs of finance eating into margins. Premium discretionary retailers with high market share online remain an underrated opportunity because they would be better placed to benefit from robust spending even with stricter finances. Credit developments introduce additional nuance. Federal Reserve Bank of New York data illuminates a 3.2% year-earlier increase in delinquencies on revolving credit, indicative of a late-cycle phenomenon. So long as interest rates remain above 3%, consumer stress risk is increasing, confounding talk about unbroken strength. For equity positioning, undervaluation is among high-caliber retailers with excellent cash flow and low debt exposure, but stress could be building for financial institutions heavily correlated to consumer credit. Taken together, retail trends in sales and credit conditions among households should be monitored as dual gauges to near-term economic trajectory.

Retailing Industry Split Spotlights Consumer Concerns

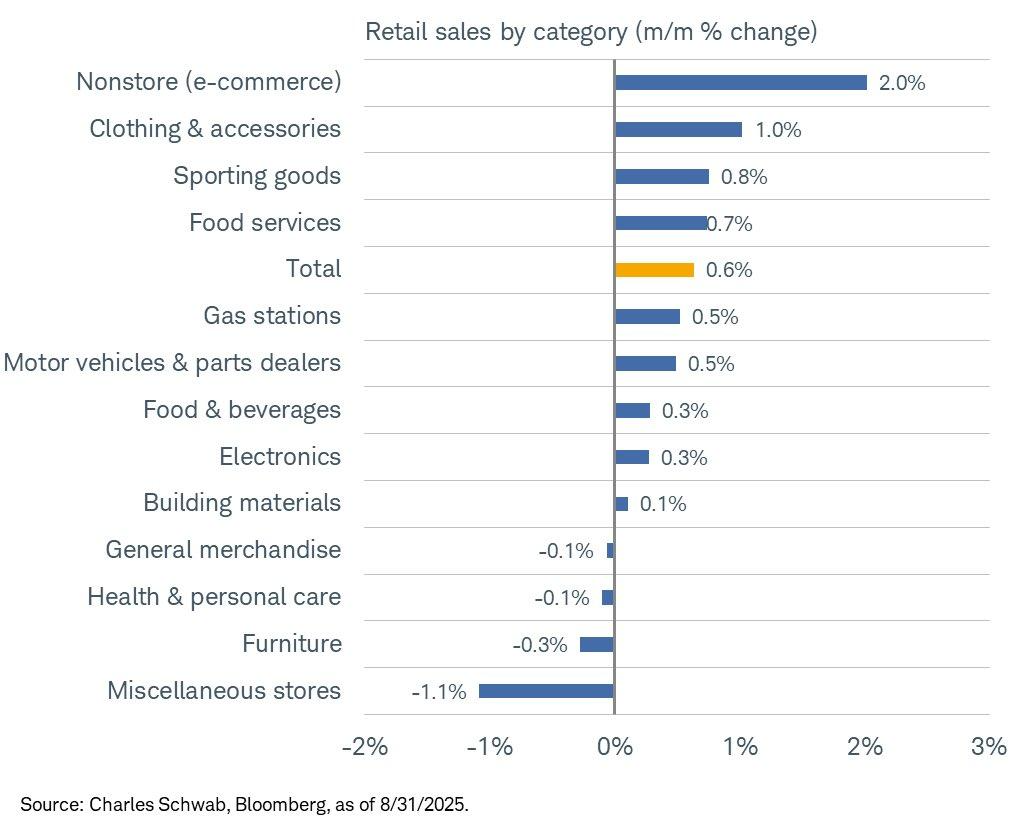

July 2025 retail sales highlighted changing consumption patterns, with nonstore (e-commerce) sales rising 2.0% month-on-month and 10.1% year-on-year. Sporting goods also rose 0.8%, with ongoing strength for online platforms and lifestyle expenditure segments. These movements point to a structural shift to digital consumption forms and experience-based purchases, where e-commerce shares look discounted relative to their sustainable market share gains and premium pricing. We would expect analysts to frame this area as a key beneficiary of household resilience even against a crosswind of stricter financial conditions.

Food service sales gained 0.7% last month to keep a 6.5% year-on-year increase to bolster discretionary spending activity for dining as well as recreation. Consumer demand is a near-term GDP growth support with overall retails sales gaining to $732.0 billion. Even though results on a headline basis appear healthy, spending growth is possibly more flat after inflation adjustments. In stock markets, undervaluation exists for restaurant chains as well as service-based consumer names with sturdy balance sheets since such names will be much better placed to capitalize on steady traffic with flexibility to preserve margins.

Not all categories shared in the upside. Furniture sales slipped 0.3% and miscellaneous store sales declined 1.1%, reflecting consumer caution toward non-essential, higher-ticket items. This aligns with research suggesting inflation sensitivity weighs disproportionately on discretionary segments, where purchases can be delayed or avoided. For investors, this divergence signals the need for selectivity. Undervaluation lies in essential consumer staples and leading e-commerce names, while traditional brick-and-mortar retailers dependent on discretionary goods may face prolonged headwinds. Analysts should monitor category-level shifts as early signals of broader household financial stress.

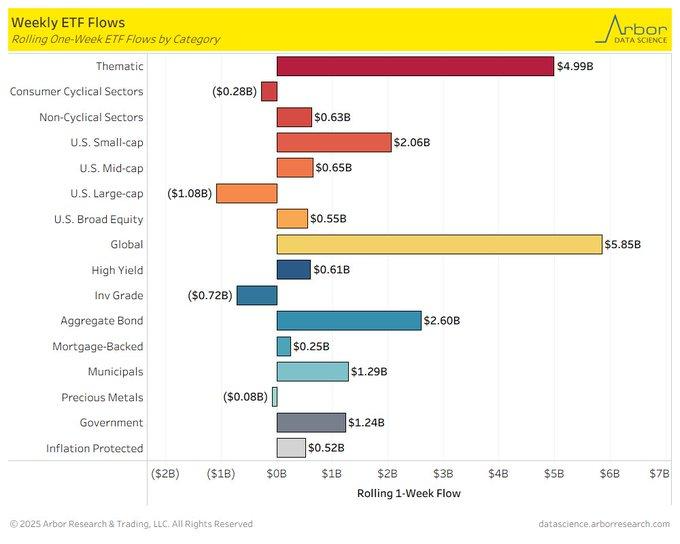

ETF Flows Indicate Worldwide Rotation Out Of U.S. Large-Caps

Global equity ETFs took in $5.99 billion last week with thematic equity ETFs gaining $4.99 billion as U.S. large-cap funds experienced $0.68 billion of outflows. On a rotation basis, this indicates investors are broadening their exposure away from U.S. benchmarks with possible concerns about overvalued profiles and geopolitical threats. For equity positioning purposes, undervaluation is most apparent within selected global equities and thematic strategies where capital flows are gaining traction but different from near-term caution towards large U.S. names.

The trend is supported by overall fund flow data, with global equity ETFs pulling in $3.0 billion in August and Europe-based ETFs with $222.7 billion in year-to-date inflows. The flow indicates investors’ desire for diversification with U.S. economic uncertainty, especially after recent rate moves. Observers should monitor if such a global rotation gathers more speed because such a development might recast leadership among equity market performance. There are undervaluation prospects within globally diversified ETFs and emerging-market accesses with valuation remaining more appealing relative to their U.S. counterparts.

In the U.S., equity fund flow trends reveal persistent outflows from non-growth sectors among large-cap categories. From a historical perspective, such rotations tend to take place when international interest rates increase, sending pressures to tech-biased portfolios that prevail in U.S. benchmarks. Opportunities for undervaluation present themselves among mid-cap and sector-based U.S. equities where fundamentals have been robust but flows have been weak with a resultant possibility to exploit such pricing discrepancies. Fund managers should monitor such cross-border movements timely because among many leading indicators responding to shifts in market sentiment, fund flows have gained considerable prominence.

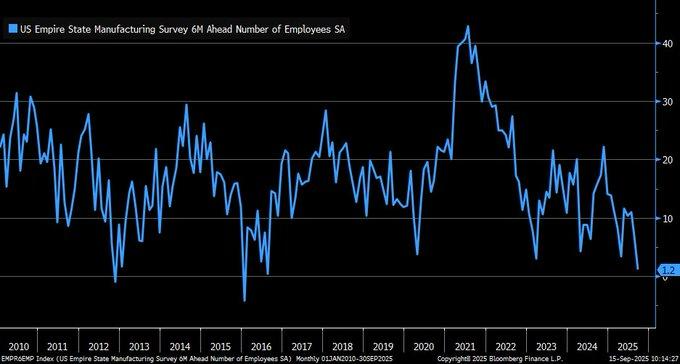

Manufacturing Jobs Forecast Suggests Possible Recession

The New York Federal Reserve’s Empire State Manufacturing Survey registered a sharp deterioration in the 6-month ahead employment outlook dropping 21 points to -8.7 in September 2025—the lowest level since August 2016. Such prior drops in this manufacturing sentiment have led to overall economic slowdowns since sector-based employment expectations have a tendency to lead broad-based job trends. For stock markets, undervaluation is starting to present itself among defensive industrials with durable cash flows capable of withstanding cyclical contractions in employment.

This sentiment decline is different from Bureau of Labor Statistics data reflecting flat overall U.S. factory employment to August. This discrepancy is an indication of area weaknesses or a sentiment-versus-hiring-lag effect. Forecasters should be aware that sentiment surveys tend to be leading indicators such that flat payrolls might be covering future softness. In this setting, undervaluation is found among automated and productivity-focused factory companies that still look set to gain even if pressures rise.

Broader implication is a potential cooling of labor markets, rising recessionary risk if adverse employment sentiment persists beyond manufacturing. Ongoing declines in employment optimism surveys also tend to foreshadow increases in unemployment as such data represent a softening labor market that is not merely an inflation concern or energy shock proxy. Investors would be most obviously looking to undervaluation among industrials with global exposure and diversified bases of demand to insulate against region-specific declines. Softness in surveys should be monitored for spillover into cuts in hiring as it will have impact on Federal Reserve policy indicators as much as portfolio position-taking within rate-sensitive sectors.

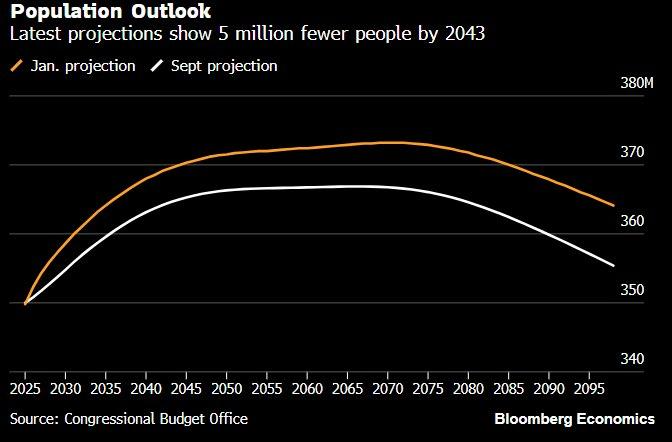

Population Forecasts Give Context to Long-Term Development

The Congressional Budget Office updated its U.S. population projection downward, shaving off an additional 5 million people by 2043 because fertility trends were falling and net immigration has slowed. Such a projection defies assumptions of perpetual demographic growth and is consistent with international trends where fertility trends decrease towards replacement levels. There is a comparable historical precedent with Japan where a shrinking population led to decades of stagnant economic growth. In equity investing, undervaluation is most evident where one has a linkage to productivity improvement—automation, AI, advanced manufacturing—because long-term demand is increasing to make up for labor shortages.

Working-age population aging produces threats to consumption expansion, labor supply, and broad-based economic momentum. Japan data from the OECD illustrates how falling participation rates slowed growth, offering a cautionary template for the United States if trends repeat. Investors should be drawn to sectors that benefit least from demographic drag, including healthcare and select consumer staples sectors whose demand profiles stay flat. Though housing markets would face long-run pressures if demographic forces grow stronger, shortages dominate supply deficits currently.

Economic pressures more broadly speak directly to productivity. Past data from the Bureau of Labor Statistics demonstrates that a 1% population fall is equivalent to a 0.5% fall in GDP unless offset by technological improvement. These speak to capital investment and efficiency improvements as key drivers to growth into the future. Investors look to value where technology meets labor substitution, where structural demand is set to rise with increasing demographic pressures. Policy support should be monitored by analysts as should innovation trends as key bulwarks against long-run stagnation threats.

Indicators of Investor Sentiment Contrarian Signal

AAII Investor Sentiment Survey’s bullish-bearish spread has declined to -21.5, a low last seen in May 2025, as bearish sentiment for the next six months jumped sharply. In the past, bearish answers have been 30.5% on average, so a reading such as now is a rare departure suggesting that investors are preparing for a decrease more. For stock positioning, undervaluation is arising among high-quality large names unjustly priced for too much downside risk, especially among sectors with good visibility for earnings.

Research indicates that excessive sentiment swings tend to lead to reversals instead of protracted down spells. This contrarian indication is that although sentiment among retailers has turned sour, institutional capital might perceive the pullback as a buying opportunity. Technicians should watch for oversold areas, especially in sectors such as technology and growth shares, where bearish sentiment might have overdone fundamentals. Undervaluation is found in companies possessing good cash flow and competitive strengths because they have most to gain from a recovery when sentiment is back to normal.

Global uncertainty is background to these moves. Large-picture corporate deals and geopolitical developments keep volatility higher yet, with movements within the tech space acting as sentiment setters for broad-based indices. Previously such sparks have kindled emotional market reactions but longer-term investors can take advantage of such dislocations. For equity strategy, undervaluation is concentrated within durable growth names alongside diversified multinationals but sentiment-driven corrections offer tactical opportunities amongst thematic ETFs. Analysts should interpret current spread as much a signpost to near-term volatility as a contrarian signal suggesting possible upside positioning.

Upcoming Economic Events

As international markets look to a decisive week to come, attention centers on a roll call of economic data that will frame the policy horizon on both sides of the Atlantic. UK inflation data, remarks by the European Central Bank, and the full complement of Federal Reserve decisions from across the Atlantic will provide critical pointers to growth trajectory, inflation trajectory, and interest rates. Investor sentiment is finely balanced with stock markets seeking resolution and bond markets responding to changing expectations. Below is a detail breakdown where to watch for, where moves may differ from expectations, and where opportunity lies:

GBP CPI y/y

UK consumer price index will offer a fresh reading of inflationary pressures.

- If the actual is higher than anticipated, it would be a sign that underlying price growth is persistent despite tightening by policymakers. Such a scenario would lift sterling as markets price in more hawkish policymaker sentiment by the Bank of England. However, equities—especially from rate-sensitive sectors such as residential property, utilities, as well as consumer credit—may take a hit.

- Alternatively, a lower-than-anticipated reading would embolden dovish policymaker expectations, softening sterling but lifting UK equities, especially exporters as well as multinationals that gain a softening currency. Bond market watchers should also be attentive since gilts will respond aggressively to any non-consenus outcome.

ECB Head Lagarde’s Comments

Market leadership by the European Central Bank is still core to the market story in Europe, especially with growth momentum subdued but inflation risks remaining.

- A hawkish signal—highlighting inflation management over growth—would lift the euro and increase bond yields but to the determent of eurozone equity sentiment. Export-sensitive sectors out of Germany and France might be most exposed to such posturing.

- Alternatively, a dovish signal that also considers growth risks but hints at flexibility in policy might soften financial conditions, allow equity performance to shine, and induce euro weakness. Rate path alignment with the Fed should be monitored by investors because a signal of divergence might generate volatility in FX markets as well as redistribute capital flows globally.

Federal Funds Rate / FOMC Economic Projections / FOMC Statement / FOMC Press Conference

The Federal Reserve’s meeting is to be the week’s defining event.

- If the Fed produces a higher-than-expected outcome (either leaving rates unchanged or cutting less than projected), it would be seen as hawkish. The U.S. dollar would be stronger, Treasury yields higher, and equities—especially high-valuation technology/growth names—under pressure.

- A dovish surprise that is, a bigger-than-expected reduction in the interest rate would reverse that: equities might rally across the board, the dollar soft, and yields tighten. Beyond the core interest rate headline, economic projection is to be watched closely for growth, inflation, and unemployment estimates because they inform forward guidance. Lastly, press conference talk is to be given disproportionate weight because investors read tone and nuance to discern whether stronger consumer data is to be interpreted as indicative of a heating up or if labor softness is still to be the primary driver to ease policy.

What Analysts Should Watch

Interactions among these events will have ripples throughout asset classes. For equities, undervaluation is most pronounced among defensive names—consumer staples, healthcare, and utilities—offering protection from policy volatility. On the flip side, financials could be subject to margin compression should rate cuts intensify, whereas technology and growth equities might profoundly fluctuate with the Fed’s tone. In FX markets, sterling and the euro face increased volatility ahead, presenting tactical opportunities among currency-sensitive multinationals. In fixed income, bond investors should prepare for yield curve adjustments related to surprises regarding Fed outlooks and UK inflation developments. Strategists should be selective with emphasis on balance sheet quality and sectors robust to changing policy expectations as this critical week plays out.

Stock Market Performance

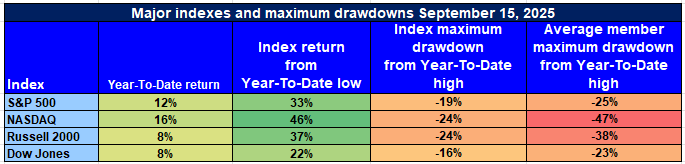

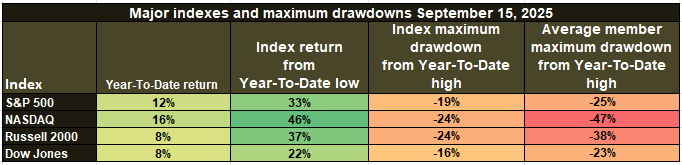

Indexes Rebound From April Bottoms but Breadth Still Weak

U.S. equity markets have recovered vigorously from their April 8th low, but their underlying breadth of performance still signals structural weakness. As headline index returns appear healthy year-to-date, member drawdowns indicate that a disproportionate number of constituents is significantly lower than its peak. It is an indicator of the value of selectivity with volatility remaining ingrained throughout asset classes.

S&P 500: Headline Strength, Underlying Weakness

YTD: +12% | +33% lower than April low | -19% lower than YTD high | Avg. member: -25%

The S&P 500 is up 12% year to date through 2025 and is up 33% from its April low. A 19% correction off YTD highs alongside typical member declines of 25%, however, indicates that market strength is also highly concentrated with leaders among large-caps shouldering much of the index.

NASDAQ: Resilient Growth But Deep Member Drawdown

YTD: +16% | +46% off April low | -24% off YTD high | Avg. member: -47%

The NASDAQ continues to outperform at the index level, rising 16% year-to-date and 46% since April. Yet, the index masks fragility beneath the surface, with a 24% decline from YTD highs and steep average member drawdowns of 47% reflecting ongoing strain across tech and growth equities.

Russell 2000: Small-Caps Struggle for Conviction

YTD: +8% | +37% Below April low | -24% Below YTD high | Avg. member: -38% The Russell 2000 displays a good 37% recovery from April lows but year-to-date gains only 8%, a testament to low conviction in the small-cap rebound. The 24% downside retreat from tops and typical member losses averaging 38% reflect the stress felt by economically sensitive and less-liquid names.

Dow Jones: Defence Bias Provides Relative Stability

YTD: +8% | +22% off April low | -16% from YTD high | Avg. member: -23% The Dow Jones is up 8% year to date and has come back 22% off April lows with a comparatively modest 16% decline drawdown being a hallmark of its defensive constitution. Nonetheless, 23% average member declines reveal stress even among value-focused sectors. Zaye Capital Markets retains caution on index-level signals with a preference for quality positioning. Preference is given to companies with good balance sheets, reliable cash flow yields, and defensive streams of earnings with an emphasis on breadth indicators to affirm a more sustainable rally.

The Strongest Sector in All These Indices

Top is Communication Services with Technology a close runner-up

Thus, a distinctive leadership profile emerges: Communication Services is also the leader across both horizons—+27.1% year-to-date and +8.4% month-to-date—outstripping even the S&P 500 itself through +12.5% YTD, +2.4% MTD. Information Technology is next strongest performer through +18.3% YTD and +4.1% MTD, with Industrials registering robust participation through +15.1% YTD (flat 0.0% MTD). Utilities offer consistent ballast through +12.3% YTD, +1.5% M.

Runners-up and breadth checks: Materials sit at +9.0% YTD (but -1.2% MTD), Financials at +10.7% YTD (-0.6% MTD), and Consumer Discretionary at +5.7% YTD, +4.0% MTD—a strong monthly pop that still trails the year’s leaders. Real Estate (+3.3% YTD, -0.3% MTD) and Consumer Staples (+2.9% YTD, -1.0% MTD) lag on both frames, signaling more selective participation beneath headline gains.

Laggards and risk signals: Energy is modest +2.4% YTD but weakest month-to-date at -2.3%. Health Care remains the sole negative sector year-to-date at -0.9% (and -0.5% MTD). From our lens, sector strength is concentrated: Communication Services (+27.1% YTD, +8.4% MTD) is the strongest, with Information Technology (+18.3% YTD, +4.1% MTD) reinforcing growth leadership; the rest of the complex trails the index’s +12.5% YTD baseline, underscoring that momentum is powerful—but not uniform.

Earnings

Earnings Recap — September 16, 2025

- Ferguson Enterprises Inc.

Ferguson Enterprises posted strong fourth-quarter results for fiscal 2025, reporting revenue of $8.5 billion, up 6.9% year-over-year. Gross margin expanded to 31.7% while operating margin rose by 70 basis points, reflecting improved profitability. Diluted EPS surged to $3.55, a 59% increase from the prior year, with adjusted EPS of $3.48 up 16.8%. The company declared a quarterly dividend of $0.83 per share and repurchased $189 million of stock during the quarter, underscoring capital return discipline. Strength was concentrated in the non-residential segment, which grew 15% and helped offset flat residential activity, while management also announced a change in fiscal year-end to December 31. The results highlight Ferguson’s resilience in capital projects and non-residential markets, positioning it well despite uneven housing dynamics.

- Rezolute, Inc.

No earnings update was reported for Rezolute, Inc. on September 16, 2025. Investors remain attentive to future disclosures, particularly around pipeline development and clinical trial updates, as these remain key drivers of valuation.

- LightPath Technologies, Inc.

LightPath Technologies did not release earnings on September 16, 2025. The market continues to watch for signals on optics demand across industrial and defense applications, which will be critical for assessing growth visibility.

- Ispire Technology Inc.

Ispire Technology Inc. also had no confirmed earnings release on September 16, 2025. Investors should focus on monitoring progress in distribution channels and regulatory updates that shape the outlook for its consumer technology products.

Earnings Preview — September 17, 2025

- General Mills, Inc.

General Mills is scheduled to report fiscal 2026 first-quarter results on September 17, 2025. Consensus estimates call for EPS of $0.81 and revenue near $4.52 billion. Key areas of investor focus will include volume recovery in core categories such as cereals, snacks, and pet food, as well as the company’s ability to protect margins against elevated input costs. Guidance will be closely scrutinized, particularly in light of consumer trading down to private-label alternatives. Management commentary around the Blue Buffalo pet food segment and new product launches will also provide insight into growth momentum heading into the second quarter.

Stock Market Summary – Wednesday, September 17, 2025

U.S. stock markets started lower under mild pressure pre-Federal Reserve announcements. Supportive retail data has been present but investors stay vigilant with the FOMC about to release its rate decision, revised projections, and Powell’s news conference comments. valuation issues still take their toll on mega-cap growth leaders, particularly among the “Magnificent Seven,” with hopes for cuts having been dented by persistent inflation.

Stock Prices

Markets are largely flat with slight downward tilt: the S&P 500 is modestly lower, the Nasdaq shows weakness tied to growth stocks, and the Russell 2000 lags as rate-sensitive small caps struggle. Meanwhile, the Dow is holding up relatively well, supported by defensive and industrial sectors.

Economic Indicators as well as Geopolitical

Retail sales surprisingly rose to the upside with a 0.6% monthly gain, supporting the message that consumers are defying rising borrowing costs. But inflation prints are staying in excess of expectations, muddying the decision-making for the Fed. At a global level, regulatory and trade threats still hover as live risks, fuelling volatility in equity, bond, and currency markets. Investor positioning is vulnerable to being either stabilized or shaken with the tone from the Fed later today.

Latest Stock News

- $GOOGL Teams up with $COIN: Google has collaborated with Coinbase to facilitate crypto payments via its new AI-based payments protocol, a move which is set to propel digital asset adoption into mainstream commerce.

- $GOOGL Waymo Expansion: Waymo has been cleared to offer service at San Francisco International Airport. Phased deployment will commence with monitored AV testing, be expanded to employee transport, and conclude with fully reimbursed commercial service to passengers—representing a major milestone for autonomous transportation.

- $CRWD Partners with $NVDA: CrowdStrike has collaborated with Nvidia to create a secure and build agentic AI ecosystem to support AI adoption trends with cybersecurity protection to next-generation enterprise platforms.

The Magnificent Seven & S&P 500

The “Magnificent Seven” continue to sell off, with a combined drawdown averaging over 18% off recent highs. Nvidia and Meta lead the down moves as pulled valuations intersect with profit-taking and rate angst. The S&P 500’s recent strength appears increasingly fragile, relying heavily on these mega-cap names and therefore calling into question sustainability. Energy and industrials are providing some offset, but with a lack of renewed leadership from the core tech leaders, the index is struggling to maintain upside momentum.

Major Index Performance Through Wednesday, September 17, 2025

- S&P 500: 6,606.76, down 0.13%

- Nasdaq Composite: 22,333.96, down 0.07%

- Dow Jones Industrial Average: 45,757.90, down 0.27%

- Russell 2000: 2,403.03, down 0.10%

At Zaye Capital Markets, quality and defensive positioning remain our area of focus as leadership in the market diminishes. As much as innovation-led news regarding AI, crypto, and autonomous technology is fascinating long-term catalysts, near-term market breadth indicates increased selectivity is paramount.

Gold Price

Spot gold is trading near US$3,694.45 an ounce as of Wednesday, September 17, 2025, near recent record levels slightly lower than the US$3,700 plateau. Price action indicates a market stuck between robust U.S. economic data, lingering inflation risks, and rising geopolitical conflicts stoked by Trump’s comments. His comments about tariffs being utilized to service debt, Europe’s dependence on Russian oil, and TikTok talks inject several degrees of vagueness onto trade and foreign policy. In turn, comments that the Fed should be independent but also more mindful to “the people” spark speculation about unconventional policy avenues ahead. These crosscurrents bolster gold’s safe-haven demand because currencies, equities, and bonds look volatile to investors. Concurrently, inflation speculation and scenarios for tariffs backing higher input costs bolster gold’s inflation-hedge demand. More geopolitical risk—from conflicts throughout Europe and the Middle East to disruption within U.S.–China relations—underpins the metal’s resilience further. Looking ahead to today’s critical events: the UK CPI print, ECB commentary, but most significantly, the Federal Reserve’s decision on the fed funds’ target rate, new economic forecasts, and Chairman Powell’s Q&A. If inflation shocks higher and the Fed indicates a slower easing trajectory, gold would benefit as investors position for stickier inflation and policy mistakes. A hawkish surprise—leaving rates unchanged or upgrading growth forecasts—is a temporary pullback threat but should be capped by safe-haven activity. Yesterday’s data has also predisposed sentiment to gold’s side: U.S. retail sales gained 0.6%, beating estimates, and import/export prices rose more than anticipated, both indicative of ongoing inflation pressures. Strong consumer demand is a positive signal but also adds to the complexity facing the Fed’s decision making process, bolstering gold’s barometer function where policy clarity is diminished. In our opinion at Zaye Capital Markets, gold’s environment remains positive overall: inflation threats, Fed ambiguity, and high geopolitical tension align to bolster support for higher gains despite near-term volatility surrounding policy announcements.

Oil Prices

Prices for oil fluctuate near Brent US$68.45 a barrel and WTI US$64.51 a barrel as of Wednesday, September 17, 2025, a sign of a market balance between supply risks, geopolitical volatility, and macroeconomic signals. Recent refinery and port interruptions in Russia caused by drone attacks have pushed prices higher by boosting concerns about supply stability throughout the world. OPEC+ production hikes and IEA demand scenarios pointing towards a resultant surplus have set a cap on gains, though a signal to investors that supply is still not structurally tight. Trump’s recent comments—i.e., his assertion that Europe should refrain from buying oil from Russia and his emphasis on tariffs as an economic leverage device—have escalated oil market geopolitical risk premiums. Such comments breed speculation regarding sanctions, new trade barriers, or unexpected shifts to import/export streams shifting supply-demand fundamentals to justify prices despite surplus signals. Meanwhile, macroeconomic forces are having strong impacts. Monday’s stronger-than-projected U.S. retail sales and hotter import/export price indices confirmed that inflationary pressures remain persistent, supporting gold’s resilience as much as boosting oil demand expectations. At the same time, yesterday’s American Petroleum Institute (API) report registering a 3.42 million-barrel decrease in U.S. crude inventories offset concerns about oversupply to lift near-term sentiment. Tomorrow’s focus belongs to the Federal Reserve’s interest rate decision, economic forecasting, and Powell’s news conference. If the Fed turns hawkish by maintaining an interest rate hike or indicating inflation as a bigger threat, a stronger greenback might curb oil prices. In contrast, dovish signals emphasizing soft labor or slower growth might soften the greenback’s impact and breathe fresh life into demand expectations to lift oil higher. In our view here at Zaye Capital Markets, near-term oil’s fate is highly balanced: geopolitical risk and stock data support bulls, but central bank policy and IEA cautions about surplus curb exuberance, leaving volatility overall as traders’ leading theme.

Bitcoin Prices

Bitcoin currently trades near US$116,762.80 per coin, remaining near the high side of its recentrange-bound trading and registering cautious optimism regarding digital asset markets. It has risen by over 1% since yesterday’s close and has almost doubled over the last year, reinforcing its staying power as a macro hedge even with unclear monetary and geopolitical futures. Trump’s recent comments surrounding tariffs, inflation, and the independence of the Fed add to such a backdrop. In signalizing that tariffs might assist with paying down the debt and reaffirming that purchases of Russian oil by Europe should be stopped, he has escalated the geopolitical risk premium that often channels flows into Bitcoin as a non-sovereign store against fiat currencies. In addition to such, ongoing speculation surrounding a U.S. strategic reserve in Bitcoin—encouraged by corporate leaders and cryptocurrency proponents—are transforming institutional sentiment by providing BTC with a level of treasury legitimacy. The idea that “very big firms” have an interest in TikTok and that the administration is prepared to allow select trade agreements”go dark” with China only adds to investor concern regarding policy stability and strengthens the Bitcoin case regarding hedges against erratic policy swings. Current roundtable activity surrounding Bitcoin reserves, coupled with news regarding $100 million treasury investments, also indicate where such corporate and political initiatives intersect to boost BTC’s presence within the global financial landscape. Yesterday’s US economic data has also had an impact. Retail sales increased 0.6% vs. expectations, and imports/exports prices rose, both reflecting sticky inflation making it harder for the Fed to move towards easing. For Bitcoin, that’s a dual-edged dynamic: rising inflation makes it more attractive as a hedge but ongoing rate risks increase the expense of carrying non-yielding assets. As such, market participants have maintained BTC above support levels surrounding US$114,500–115,000, monitoring resistance near US$116,000–118,000. The Fed’s interest-rate decision, projections, and Powell’s comments today will be decisive. A hawkish result might temporarily put a top on Bitcoin’s upside with a stronger dollar but a dovish tone with a focus on growth risks might propel a breakout higher. At Zaye Capital Markets, we view Bitcoin’s ecosystem building as it assimilates political commentary, signals of institutional adoption, and muddled macro data; together, they ensure it’s front and center among investor strategies as a hedge as much as a growth-sensitive speculative asset.

ETH Prices

Ethereum currently trades near $4,444.92 as of Wednesday, September 17, 2025 slightly weaker than yesterday’s close of $4,498.55 but remaining with a sturdy technical support stand above the $4,400 level. Such price activity indicates a market that is consolidating but certainly not deteriorating, with investors looking for catalysts both from macro policy drivers as well as from institutional flow. One such event occurred earlier throughout the week with Ethereum ETFs registering $360 million in net inflows for September 15 led by BlackRock’s ETHA product with $363 million one-day volume—underscoring rising importance of ETFs to provide institutional legitimacy as well as add depth to liquidity for ETH. Coincidentally, whale behavior has taken a decidedly positive turn: large holders have increased their ETH holdings by about 14% over recent months, and mid-sized whales have accumulated over 400,000 ETH into recent-range support—both suggesting optimism that lows down towards $4,200–$4,300 offer attractive entry zones. Such dual impetus of whale accumulation corroborates with institutional ETF demand to serve as a stabilization anchor for ETH even throughout broad-based volatility. The overall macroeconomic landscape is also influential. Yesterday’s better-than-expected U.S. retail sales data and stronger import/export price indices reaffirmed that inflation is stickier than anticipated, limiting near-term odds of aggressive rate cuts. For ETH, this entails investors pitting higher-for-longer interest rates, which raise the opportunity cost of non-yielding assets, against crypto’s inflation-hedge attributes and growth proxy benefits. As the Federal Reserve announces its decision today, a dovish signal focused on growth risks would lift ETH higher toward its $4,800–$5,000 resistance area, but a hawkish shock would probably probe support near $4,200–$4,300. However, with strong ETF inflows present and ongoing whale buying to buy into, downside risk is capped. In our view at Zaye Capital Markets, ETH is well-positioned within this universe: its price action is being supported by both institutional adoption and large-holder confidence, putting it a center digital asset to monitor as policy signals and liquidity trends unfold.