Where Are Markets Today?

U.S. stock futures were on course for a higher trajectory Monday morning, forecasting a cautiously optimistic beginning for the week at large. Dow futures were up around 0.21%, S&P 500 futures were up 0.32%, and Nasdaq-100 futures were up 0.46%, forecasting a modest turnaround for sentiment after a volatile several days—especially for techs, as well for growth stocks. The early green for futures happens despite continued shutdown threats back home, with investor sentiment seemingly going risk-on, perhaps wagering on eventual resolution and stabilization some day down the road. There is also growing sentiment that despite a lack of quick political resolution, large-cap American tech names have been over-sold enough for a technical correction.

Across the Atlantic, European stock futures opened quieter—mostly unchanged to mildly mixed—due to less domestic catalysts and greater reactiveness towards broader international macro and political events. European markets are considering the spillover effects from American fiscal risk, yet also looking forward to the scheduled speeches from ECB President Christine Lagarde and BOE Governor Andrew Bailey today. With region-wise economics already priced in and inflation pace slowing down, the next directional signal for the market is awaited from the language of central banks and US-centric volatility. European markets react secondarily towards American events, and presently, it’s that uncertainty—around fiscal expenditure, economics data releases, and diplomatic moves—that is fuelling the caution. Two central drivers are defining the world futures landscape this morning. The first is political uncertainty. The specter of the U.S. government shutdown and last-minute sparring between political leaders, such as hardline budget threats and global geopolitics from leaders such as Donald Trump, are driving cross-asset position shifts. Interestingly, safety assets such as gold have risen and Bitcoin is trading near highs, indicating investor hedging. The second is a broader correction under way across tech and AI-related segments, which had been pressured over the past couple of weeks. Investors now seem to be looking towards this sector for rebound life—the more so, given that rate expectations ease modestly with weaker economic indicators.

Zaye Capital Markets sees this as a market trapped between risk repricing and hunting for opportunities. The rise in futures reflects a desire to selectively rotate capital while hedging macro uncertainty. If central banks’ comments today shed clarity on inflation or rate direction, and if shutdown talks demonstrate some movement, then momentum might extend further. A hawkish tone or rising political impasse, on the other hand, might turn early gains on their head. European markets, like their American counterparts, are holding their collective breath—but the positioning reflects a faint tilt towards optimism, with a close eye towards Washington and Frankfurt both.

Major Stock Market Performance on Monday, October 6, 2025

- S&P 500: 6,715.79, up 0.2% on the day after hitting new highs last week.

- Nasdaq Composite: At 22,844.05, trading flat as tech leadership fades.

- Dow Jones Industrial Average: Up 0.3% at 46,519.72, powered by energy stocks, industrials.

- Russell 2000: At 2,458.49, slightly higher, with small caps favored on rotation shifts.

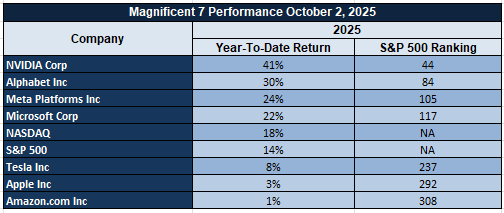

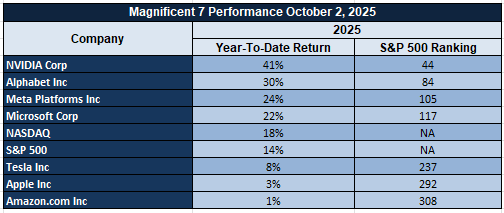

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are starting to look tired despite the S&P 500 floating at all-time highs, with tech giants suffering valuation squeeze, regulatory challenges, and AI fervor starting to wane. Tesla and Meta especially are on the back foot, both easing 15–20% from their highs for 2025. Without new leadership from this group, the overall market might struggle for upward impetus. Sector rotation out of tech into industrials, energy, and defensives is growing obvious as a search for alternatives for high-growth exposures picks up pace.

Drivers Behind the Market Movement – Monday, October 6, 2025

Global markets began the week on a cautiously hopeful but extremely reactive note, for investors remain balancing escalating political events, macroeconomic data stream, and policy cues from main central banks’ leaders. U.S. and European futures are indicating upward moves, but beneath the surface, vulnerability persists, led by a couple of overriding factors dictating sentiment for the day.

1. Rising Geopolitical Tensions Amid Trump’s Gaza Ultimatum

President Trump’s aggressive stance against Hamas and broader Middle East instability has caused market concern. As Trump demanded a Hamas deal by Sunday evening or threaten “unprecedented hell” otherwise, the risk premium for geopolitics has gone up across industries, particularly commodities and defense stocks. His statement asking for Palestinians to depart and saying Gulf allies may go it alone “with or without Hamas” has created a new level of risk asset volatility worldwide. As a result, gold has touched new highs as risk-avoiding capital shifts towards safety, while energy markets remain on high alert for any Gulf oil supply disruption risk. The rhetoric has also boosted defense stocks and created further hedging interest across FX and bond markets.

2. Economic Data Sensitivity and Central Bank Signals

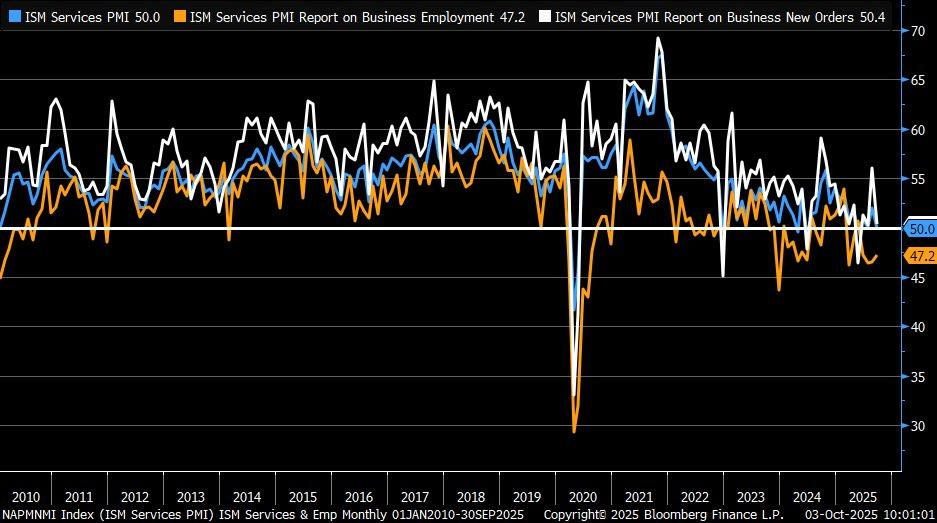

Market participants are eagerly awaiting today’s scheduled speeches of ECB President Christine Lagarde and Bank of England Governor Andrew Bailey for guidance on monetary policy for a world of persisting inflation and decelerating demand indicators. Last week’s soft US services print of the ISM, which marked stagnant new orders and slowing pace of hiring, solidified expectations that a weaker demand-side numbers-induced policy shift for the Fed, not to mention other central banks, might be needed. In Europe, sentiment remains soft with weaker PMI prints and mixed inflation signals, so markets are particularly attuned to any policy commentary on future rate paths or QT easings. As data dependence grows, asset prices respond more aggressively to each new macro input.

3. Shutdown Drama & Fiscal Disruption

Back home, Trump’s announcement to freeze $2.1 billion in infrastructure projects in Chicago, alongside his shutdown blame game with Democrats, has only added to fiscal market dislocation. While markets are still digesting what the freeze means for broader federal infrastructure spending, the symbolic move reflects the intensifying divide in Washington over government funding. Traders are now building in scenarios of extended shutdown risks, potentially delaying economic data releases and suppressing public-sector-driven economic momentum. All eyes are now on the upcoming unemployment claims and Friday’s NFP (should it be released on schedule), which could reshape expectations for Q4 growth.

At Zaye Capital Markets, we believe today’s price action reflects a fragile balancing act—where political flashpoints, uncertain macro data, and central bank communication all collide. For now, elevated volatility remains the baseline, and while futures are leaning risk-on, conviction remains shallow. Investors are advised to stay tactical and maintain positioning that can weather both inflation and geopolitical tailwinds.

Digesting Economic Data

The TRUMP Tweets and Their Implications

President Donald Trump’s weekend burst of pronouncements has caused ripples in geopolitical and financial communities, sparking a new bout of Middle East tensions and investor nervousness. His biting ultimatum against Hamas—to accept a ceasefire plan by Sunday at 6 p.m. ET or risk punishment “like no one has ever seen before”—threatens imminent escalations around Gaza. Trump’s call on innocent Palestinians to leave high-risk areas and threats of “potentially great future death” should the deal fall through betray a toughened position, likely enough to cause a market rout and safety flight. This should help support such assets as gold and the U.S. dollar while applying downside pressure on equities, especially those exposed to geopolitical riskiness.

Stoking the flames is Trump’s declaration that the U.S. will follow through on the proposed Gaza arrangement “with or without Hamas,” backed by Gulf allies. This type of rhetoric places both military and diplomatic channels on high notice. Should instability break out throughout the region—particularly around energy chokepoints like the Strait of Hormuz—oil markets could experience sudden upside churn. Trump’s labeling of this truce attempt as Hamas’ “last chance” also pins diplomatic leeway, which makes the next 48 hours crucial for world risk sentiment. Equities and bond yields could remain hyper-sensitive towards happenings on the ground and Washington, Tel Aviv, and Doha announcements. Domestically, Trump’s hold on $2.1 billion of Chicago infrastructure funding injects a further degree of uncertainty into fiscal policy, implying greater centralization of budgetary discretion. While potentially upbeat for federal deficit sheets on a short-term basis, such actions could hinder economic activity at the state and local level—affecting transport, construction, and indeed, utilities sectors. Muddying the waters, Trump doubled down on Democratic culpability for the current American government shutdown, although he did go on to say, “we’re ready to go back,” which could have some ground for negotiation involved. Markets might see this as a note of softness, yet until there is actual agreement, the shutdown risk remains a prime overhang.

Lastly, a possible geopolitical and macroeconomic wildcard has come from China. Trump is said to be lobbied quietly but fervently by Beijing, with China holding out a gargantuan U.S. investment deal—allegedly touted around $1 trillion this year—on the condition of relaxed trade barriers and regulatory clampdowns. If negotiations go further, this might spur a risk-on sprint across industrials, semiconductors, and materials stocks. That said, a failure to compromise could spark new volatility for the China-U.S. relationship, spoiling sentiment especially for tech stocks and export-sensitive industries. At Zaye Capital Markets, our attention remains on sorting signal from noise—Trump’s rhetoric matters, and the next several days might decisively dictate investor action across asset classes.

ISM Services PMI Touches Neutral, Indicates Susceptible Services Economy

We also witnessed a drastic slowdown in the services economy in the U.S. in September, with the ISM Services PMI dipping to 50.0—circling the dividing line between growth and contraction. This reading is evidence of a striking slowdown from 52.0 in August and supports stagnation in the engine of more than two-thirds of U.S. GDP. Of particular concern is the precipitous fall in new orders all the way to 50.4 from 56.0, which is signaling waning forward demand and calling into question the sustainability of consumer and corporate service spending through Q4.

Inflationary pressure remains elevated, and prices paid increased to 69.4, indicating sustained input cost concerns despite broader disinflationary indicators elsewhere. While upswing in prices along with weak demand may reflect stagflation-lite situation, employment sub-index continued in contraction at 47.2—and again confirming sustained weakness in services jobs. This contradiction makes it difficult for Federal Reserve, with inflation sticky despite declining economic momentum.

We think the discounting in consumer staples and certain utility stocks—which historically perform strongly in times of economic plateau—warrants analysts’ attention, specifically companies possessing robust pricing power and consistent dividend policies. Analysts should keep close scrutiny on services PMI in the upcoming month along with the labor market to see if that plateau turns towards contraction. Keeping tabs on wages in the service sector will also remain essential in tracking pressure on margins and potential inflation persistence in the downstream.

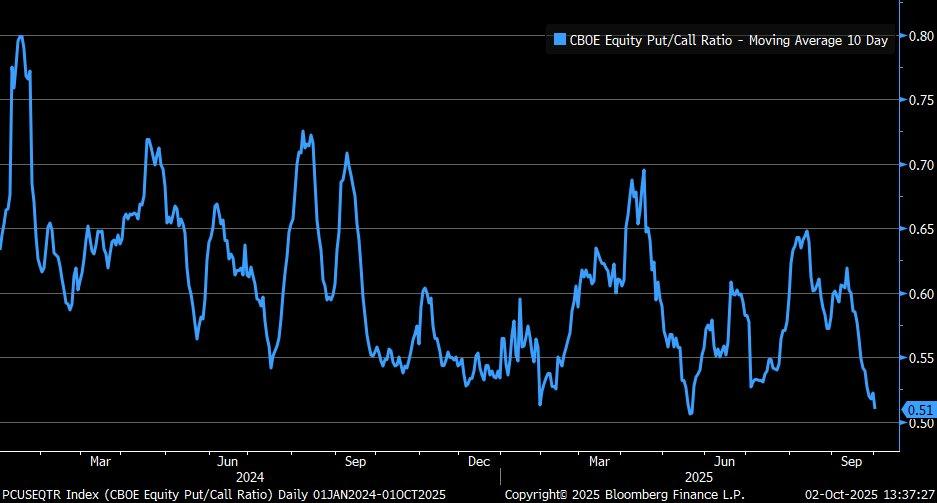

Decoding Put/Call Ratio: Market Froth Hiding Under the Rallying Continuation

The CBOE equity put/call ratio’s 10-day moving average has dropped sharply to approximately 0.51 as of early October 2025, nearing levels last seen in May when it touched 0.55. This steady decline from mid-2024 highs above 0.75 reflects a pronounced tilt toward call option activity—indicating heightened bullish sentiment and positioning in the equity market. Investors appear increasingly confident in continued gains following recent rallies in major indices, a setup that often breeds complacency and diminished hedging behavior.

This trend has historical significance too. Spreads below the 0.55 mark have been common leading up to market pullbacks, and low put volume versus calls is usually characteristic of investor optimism that’s too high. Social sentiment—especially on market-centered discussion boards—has escalated this narrative, and it implies building speculative euphoria. Though that doesn’t necessarily mean that it will turn, it does mean that present positioning is getting more and more lopsided, and equity markets may remain vulnerable to a volatility spike that’s prompted by macro surprises or earnings disappointment.

Given these dynamics, our thesis is that select defensive big-cap tech stocks with below-market volatility numbers appear attractive in this regard. They offer stable income, low beta, and room for upside if risk appetite falters. Analysts must remain attentive to shifts in options flow signaling, namely any sudden bounce back in put activity or rises in implied volatility indexes, both signals that would see the market re-setting in terms of sentiment. Close attention to these technical crossovers will prove critical in an equity market that is more positioning and less fundamental-driven.

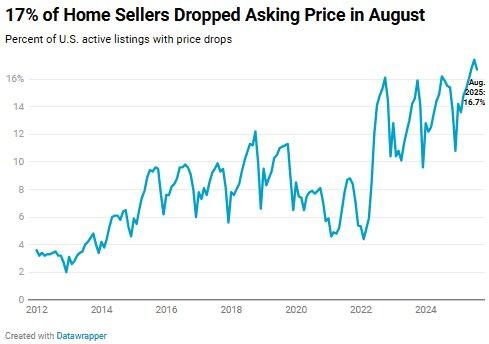

Shifting Housing Sentiment: Price Cuts Signal Buyer’s Leverage in Real Estate

New data indicates a significant slowdown in the U.S. residential market, with 16.7% of home marketers cutting asking prices in August 2025—the highest level in August since 2012. This increase, measured in accordance with nationwide list trends, constituted a distinct year-over-year rise from 15.9% and was yet another indication of the building pressure from high mortgage rates staying above 6.5%. As median household prices continued to remain at historic levels at $439,000, the number of price cuts is an indication of rising resistance from consumers, particularly in suburban and second-tier metro markets.

The relevant trend data shows an increasing rate of price declines since 2020, now close to the 17% level. This is in stark comparison to the post-2008 recovery, when limiting supply and ultralow interest rates favored stable pricing. Summer 2025 marked record-level 35% excess seller demand versus buyer demand, in itself a huge offset that moderates optimism for price gains now forecast at 1.5% annually. This landscape summarizes gradual backtracking from pandemic-era housing market dynamics toward more typical demand-supply dynamics.

With the structural shift, publicly traded real estate investment trusts (REITs) with residential exposure, specifically REITs that are trading below their net asset value (NAV), appear undervalued to us. Analysts would want to look for more deceleration in volume in mortgage origination and builders’ surveys on sentiment. Regional indexes of affordability, vacancy rates of rentals, and household formation would also be important in measuring the downside risk or stabilization in the real estate market.

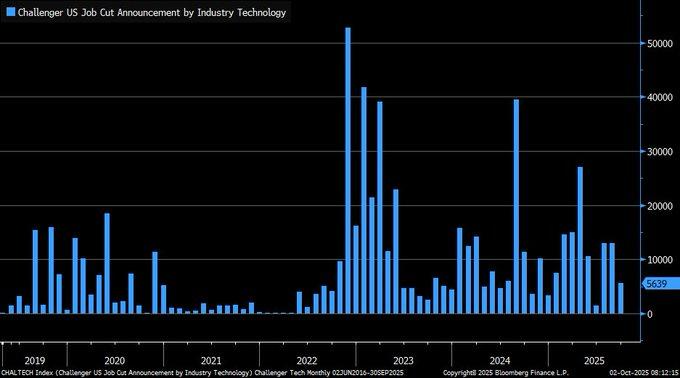

Tech Layoffs Cool But Remain Structurally Elevated Amid AI-Driven Realignments

Latest statistics show that American tech sector job cuts have slowed considerably in recent times, with monthly layoff announcements coming down from the 2022–2023 levels of more than 80,000 to a much tighter 500–5,000 in 2025. Though that is a substantial decrease, cumulative cuts year to date for the private trackers still remain in the 90,000–158,000 range, far higher than the pre-2022 average. This is an indication the sector continues in an epoch of structural readjustment, predominantly dictated by cost rationalization, digital revamp, and staffing realignments due to automaton.

The post-peak downturn doesn’t translate to complete labor market recovery. Unlike cyclical recoveries experienced in other industries like manufacturing or logistics, tech jobs continues to be hemmed in by continued AI implementation and productivity-driven streamlining. Organizations keep reorganizing jobs, and in operations, support, and legacy developmental roles, in particular, with their resulting use of AI automating tasks that used to require larger groups of workers. Contrast this with healthcare, learning, and construction, which are experiencing talent deficiencies and higher wages due to continuing demand versus supply mismatches.

We see undervalued potential in enterprise software and cybersecurity firms with lean cost structures and improving hiring trends, specifically firms that are in the process of implementing AI without making core talent redundant. Analysts should closely observe tech hiring trends in job descriptions within spaces of AI, cloud infrastructure, and function areas of compliance. Hiring stabilization in these niches could serve as a leading indicator of margin resilience and upcoming earnings visibility in the group.

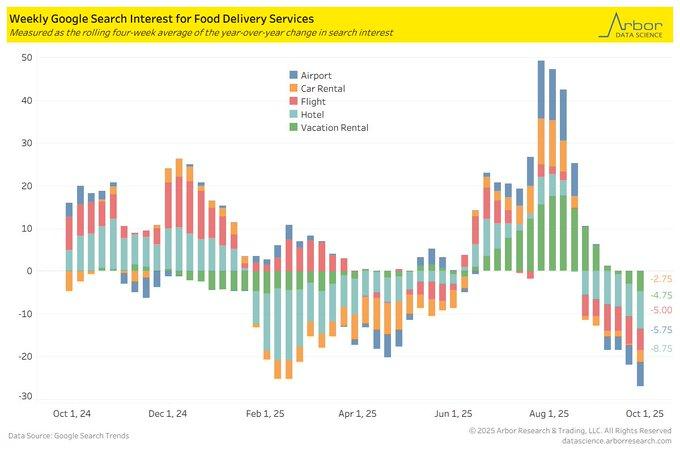

Significant declines in U.S. Google search behavior for travel-related services mark ebbing discretionary demand. Search for “hotel” declined -5.75% year-over-year in early October 2025, the lowest annual rate in more than one year, says recent trend data. Wider segments such as flights and holiday rentals have also gone negative following their mid-2025 highs of more than +40%. Typically, these digital intent indicators precede actual booking trends, and the indicators do suggest the possibility of cooling in spending on travel as we approach the end quarter of the year.

This behavioral change is in direct contrast to robust Q3 2025 GDP prints, supporting the narrative that consumer resilience is gaining selectivity. Real-time evidence suggests consumers are steadily retreating from non-essential purchases amidst higher inflation and persistent high borrowing rates. IATA global air traffic data is in support of this trend, exhibiting slower global international seat bookings and premium leisure segment yield compression—consistent household budget rebalancing toward core goods and services.

With these cues, we think undervalued bets lie in core consumer goods and value hospitality chains, specifically those with local exposure and pricing power. Forward-looking metrics like TSA traffic levels, credit card travel segments, and price sensitivity in mid-tier hotels should be tracked by analysts to gauge if the downshift is seasonal in nature or the beginning of a larger reallocation in the preference of consumers in spending.

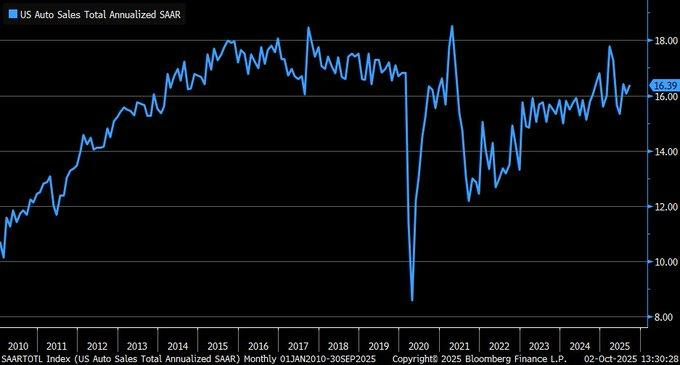

Auto Sales Pick-Up in Q3, but EV Push Runs Into Policy Hurdles

U.S. auto sales reached a seasonally adjusted annual rate (SAAR) of 16.39 million units in September 2025, up from 16.07 million in August, reflecting strong momentum in consumer demand. According to industry data, Q3 posted a 5.2% year-over-year increase, aided by competitive financing, stable inventories, and pre-policy deadline buying activity. This cyclical strength, rising off 2024 lows, suggests a supportive contribution to Q3 GDP and reflects broader post-pandemic normalization in durable goods consumption.

Unit volume—around 1.23 to 1.25 million—was driven by core segments and end-of-period EV demand spikes just prior to a significant policy shift. Expired federal EV tax credits, due for various models after September, drove a mini buying spree. EV penetration remains low, and Q3 data show Tesla and GM’s collective EV market penetration at just 6.8% of all-unit sales combined. This underscores that, while stimuli impact short-period behavior, the universal EV transition remains stuck with demand structure problems.

In this dynamic setup, dealership and auto supplier stocks with low EV exposure and diversified revenue streams look undervalued, and such stocks with high inventory turns and flexible pricing models stand out in particular. October sales data should be closely watched for analysts for gauging post-subsidy EV elasticity. Further attention should also be given to automaker margin commentary and consumer credit metrics, particularly given that interest rate hikes could put ceilings on affordability despite robust headline volumes.

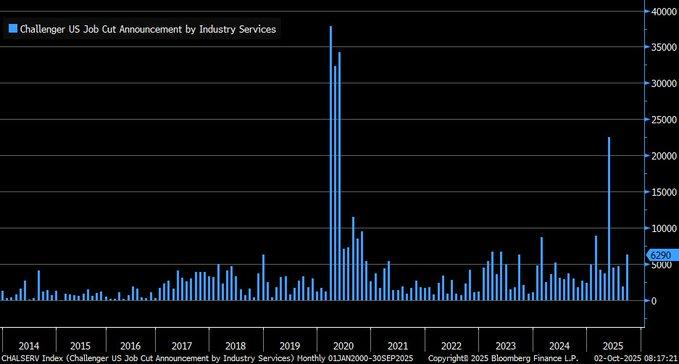

Services Sector Layoffs Spike in September as Labor Market Shows Uneven Cooling

September 2025’s announced U.S. services sector job cuts surged to 23,000—the highest month-to-month reading since March 2023—in revised workforce statistics released on Wednesday. They represented roughly 43% of the total 54,064 jobs cuts in the month, despite the total number being 37% less during August. With cuts through this year now at 946,426, the reading is the highest year-to-date level since 2020, signaling a strategically restructuring, not universally shrinking, workforce market.

The services economy, responsible for close to 80% of U.S. jobs, has in the past demonstrated volatility in layoff announcements without necessarily buckling larger labor market recovery. There were similar spikes in 2023 in rate-hike cycles but was taken in stride by subsequent hiring in sub-sectors such as healthcare and hospitality. This current spike could indicate selective cost control during margin pressure and not necessarily a systemic slowdown, but sustained increase in these numbers would indicate labor hoarding unwinding, an essential dynamic likely being monitored by the Federal Reserve.

We look for subtle potential in staffing and outsourcing companies with broad sector exposure and placement pipelines that remain robust, namely companies that have healthcare, logistics, and government services deals. Analysts should keep an eye on subsequent jobless claims, JOLTS, and services ISM employment components for more evidence of continued softness. Any continued increase in services layoffs would have the potential to spill over and impact the Fed’s tone on labor-market slack, giving more credence to arguments for holding or cutting rates in subsequent meetings.

Retail Investor Sentiment Edges Up but Remain in Neutral Territory

The AAII Investor Sentiment Survey’s bull-bear spread rose modestly to +3.7% for the week ending October 1, 2025, marking a slight uptick in retail investor optimism. While not excessive, this mild positive reading suggests that individual investors are cautiously constructive on the six-month equity outlook, without tipping into euphoric territory. The AAII survey has long served as a contrarian tool, with historical extremes above +30% or below -30% often preceding trend reversals in broad equity benchmarks.

The current mood is considerably less polarized than in past turning points, which puts markets in territory that is normally marked by firmness or modest gains. Bull-bear spreads within the neutral territory have been followed by median 12-month advances in the S&P 500 in the range of 10%, dating back to 1987, in favor of continued gradual gains, particularly with stabilization in the economy, moderation in inflation, and earnings in place for the end of 2025.

In this sentiment-driven world, undervalued quality mid-caps with consistent earnings and low macro exposure look appealing. They do well in balanced market conditions when sentiment is not running valuation up nor causing rotation. Analysts should monitor changes in weekly dispersion of sentiment and overlay on fund flow data to gauge conviction strength, especially in the approach to earnings season and macro policy meetings.

Upcoming Economic Events

President Lagarde of ECB, Bailey of BOE Speak

With world financial markets navigating entrenched inflation and diverging growth perspectives, this week features two prominent monetary spokemen: ECB President Christine Lagarde and Bank of England Governor Andrew Bailey. As monetary policy enters a more data-dependent regime and risk from geopolitics persists, investor sentiment will hinge on the tone and direction such policymakers send out. Here are things to watch for—and market reactions based on what is uttered:

ECB President Lagarde Says

The speech from Lagarde follows increasing nervousness about the Eurozone’s economic path. Inflation has eased modestly in the last prints, yet underlying pay pressures and services-sector rigidity persist.

- If President Lagarde adopts a hawkish position—mentioning lingering inflation or reaffirming a higher-for-longer rates path—the euro might rise, European bond yields could increase, and rate-sensitive industries such as utilities and property might underperform. Risk assets could experience a short-term squeeze as markets factor in prolonged monetary tightening.

- But a dovish shift—perhaps due to slowing growth, soft PMIs, or weak consumer appetite—should buoy stocks, narrow peripheral bond spreads, and depreciate the euro. A warning on risks to inflation outlook or policy flexibility should respond with a cyclical-sector bounce, additional belief in a soft-landing, and investor sentiment towards emerging-market debt and euro-cross FX trades.

BOE Governor Bailey Talks

With the British economy on the tightrope between repeated wage gains and disinflation, Bailey’s communications are going to carry some prominent policy significance.

- A hawkish signal, which centers on healthy labor market or high services inflation, might buoy the pound towards the top and maintain short-end gilt yield support. That, once again, should put a squeeze on rate-sensitive UK stocks, especially homebuilders and consumer-sensitive stocks, but buoy UK banks via steeper curves.

- Or, if Bailey puts out a signal for caution—pointing towards tempering inflation, soft retail activity, or credit stress—a dovish signal might appear. Anticipate sterling softness, high-dividend UK stock outperformance, and a bond rally that is confined to the 2- to 5-year tenor. A story on a policy pause might get credibility, reinforcing already-existing market guesses on terminal rate vicinity, presenting tactical opportunities on UK-centric ETFs.

Central bank communication this week could influence cross-asset volatility and FX market leadership. For analysts and investors, tone matters as much as substance—especially with rates nearing their cyclical peaks and markets rotating toward growth-quality hybrids. Watch the real-time reaction in currency markets, front-end yields, and global financials to assess how much credibility markets assign to each message.

Stock Market Performance

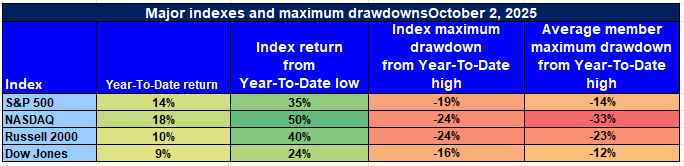

Indexes Bounce Back from April Lows, yet Member Drawdowns Show Cautious Optimism

U.S. equity indexes have provided stout returns since the Apr 8, 2025 low, but a closer examination finds that average member drawdowns are stil large—hinting at thin leadership and residual volatility beneath the surface. While headline performance depicts a portrait of resiliency, breadth and internal strength remain spotty across large-cap indexes.

Below, our in-depth analysis of the current performance update:

S&P 500: Large-Cap Strength, But Hidden Weakness Persists

YTD: +14% | +35% off April low | -19% from YTD high

Avg. member: -14% off Apr low | -26% from YTD high

The S&P 500 remains at the top with a 14% YTD increase with a 35% jump off the April lows. Nevertheless, the index-averaging stock remains 26% below its YTD high, showing uneven participation. Though a relatively modest -14% average dip off of the April trough, such dichotomization heightens concentration risk, where a select mega-cap stock or stocks are driving index-level returns.

NASDAQ: Strong Rebound Overshadowed by Member Pain

YTD: +18% | +50% off April low | -24% from YTD high

Avg.member: -33% off Apr low |=48% off YTD high

The NASDAQ boasts the top YTD performance and strongest rebound off the trough for April, yet its internals are a portrait of vulnerability. Member averages’ drawdowns remain steep—33% below April bottoms and close to 48% off YTD highs—to reflect persistent pressure on mid- and small-cap growth names, particularly in the areas of software, fintech, and AI-related stocks.

Russell 2000: Recovery Lags Behind Bounce Back in Small Caps

YTD: +10% | +40% off April low | -24% from YTD high

Avg. member: -23% off Apr low | -38% from YTD high

Small caps have recovered 40% off the lows of April, but the 10% YTD increase for the Russell 2000 continues to be evidence investor sentiment is uncertain. A 38% correction off YTD highs and a 23% decline from the trough of April remain evidence concern exists on the profitability, interest-rate, and credit fronts for small, less-capitalized issuers.

Dow Jones: Defensive Tilt Helps Limit Downside

YTD: +9% | +24% off April low | -16% from YTD high Avg. member: -12% off Apr low | -23% off YTD high The relative defensiveness of the Dow’s sector exposure has provided some stability. Lagging behind other indexes on cumulative return, its correspondingly modest drawdowns are a measure of relative strength, especially for dividend payers and industrials. The collective member down 12% from the YTD low and 23% decline from the high on the year reflect less dispersion than growth-weighted indexes.

We remain selectively bullish at Zaye Capital Markets. Although index-level action exhibits hopeful recovery, breadth remains shallow on that recovery. We remain bullish on high-quality names exhibiting good earnings visibility, healthy balance sheets, relative strength relative to their peer groups, especially on areas of valuation remaining out of alignment with fundamentals. As volatility continues to compress, monitoring intra-index dispersion continues to be essential for discerning true leadership from temporary beta rallies.

Strongest Performing Sector in All These Indices

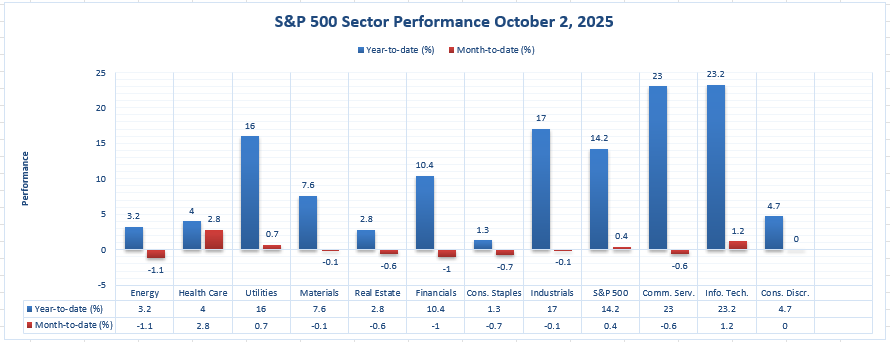

Tech and Communication Lead YTD, but Utilities and Industrials Possess Good Depth

The year-to-date performance of the S&P 500 up to October 2, 2025, is one of general strength, yet there have been two clear outperforming sectors: Communication Services and Information Technology. As some defense industries have picked up pace, leadership is still centralized at the upper echelons of the market, areas related to AI, cloud infrastructure, and online platforms.

Information Technology:

YTD: +23.2% | MTD: +1.2%

The tech sector remains at the helm of the index performance, notching the year’s biggest year-to-date return within all sectors. With a healthy 1.2% MTD rise, tech maintains pace heading into the Q4 season.

This reflects a persistence of demand for cloud, chip, and AI-enabled infrastructure despite pockets of recent valuation nervousness.

Communication Services:

YTD: +23.0% | MTD: -0.6%

Next behind tech, the comm services sector has delivered a robust 23.0% YTD, facilitated by ad recoveries, streaming profit margin improvements, and trends online towards engagement. A modest -0.6% correction occurred in October so far, but this sector is a bedrock of leadership within the equity market.

Utilities

YTD: +16.0% | MTD: +0.7% Not the highest earner, utilities remain the strongest-performing defense sector, returning 16.0% YTD, with a consistent 0.7% increase month-to-date. This return reflects rotation into inflation-sensitive and yield-generating assets as rate volatility returns to stability.

Industrials:

YTD: +17.0% | MTD: -0.1% The Industrials have also performed well, registering a 17.0% YTD increase, which has experienced strength in infrastructure, aerospace, and manufacturing orders. Although holding steady in October, the industry full-year performance suggests underlying economic strength. We’re positive on Information Technology for alpha exposure and on Utilities for defensiveness—both areas demonstrating absolute strength and relative stability. Our team urges close attention to sector moves and earning guidance, particularly considering our setup for a potentially volatile year-end macro backdrop.

Earnings

Earnings Recap — October 3, 2025

- Golden Matrix Group, Inc.

Golden Matrix Group did not issue a fresh earnings report on October 3. Its most recent published results remain Q2 FY 2025, where it recorded a net loss of –$3.6 million (≈ –$0.03 per share), missing consensus. The company continues to project full-year revenue in the range of $185 million to $188 million. Key issues analysts will watch include margin pressure amid low-margin iGaming operations, user growth trends across regulated markets, and whether management can better control operating costs given competitive and regulatory pressures.

Earnings Preview— October 6, 2025

- Constellation Brands, Inc.

Constellation Brands is scheduled to report its Q2 fiscal 2026 earnings today after postponing its release in observance of Yom Kippur. Consensus expectations are centered around EPS of approximately $3.42. Investors should focus on segment-level performance in beer, wine, and spirits, as well as margin impacts from input costs. Commentary around U.S. consumer demand, trade inventory levels, and price-mix dynamics will be especially important given recent softness in the beer category.

- Aehr Test Systems

Aehr Test Systems will report its Q1 fiscal 2026 results after the market close today. Analysts expect revenue to decline by roughly 17.9% to $10.78 million, with a near break-even EPS of –$0.01. Investors should track new order activity in wafer-level burn-in systems, backlog momentum, and how the company is positioning amid the broader AI and semiconductor equipment cycle. Commentary on gross margins and R&D investments will also be critical.

- LifeCore Biomedical, Inc.

There is no credible confirmation that LifeCore Biomedical will report today. If earnings are released, investors should look closely at product pipeline updates, regulatory developments, and any guidance revisions. Key areas include revenue growth across contract development and manufacturing segments, and how the company is managing costs within its biotech-heavy operational model.

Stock Market Summary – Monday, October 6, 2025

The US equity markets started the week cautiously strong on the back of hopes for a dovish Federal Reserve, despite lingering uncertainty over government funding and macro data disappointments. Although the S&P 500 and Nasdaq are at or around all-time highs, the gains look wanting on shifts towards quality earnings, clearer central guidance, and changes in sector leadership. The Dow and Russell 2000 are registering firmer support on a rotation into industrials and defensives.

Stock Prices

Economic Forces and Geopolitical Events

Market sentiment is on a thin tightrope between dovish Fed hopes and macroeconomic uncertainty. The mixed jobs report on Friday relieved some pressure on yields, supporting stocks into the new week. Government shutdown risk, however, looms large, potentially putting on hold pivotal data releases such as CPI and PPI, impairing short-term clarity around monetary policy decisions. At the same time, Middle East instability and hints of a revival of trade tension out of Asia are giving a note of prudence to the risk story globally. Market participants are highly attuned to shifts in rate policy, fiscal uncertainty, and sector-specific surprises on the earnings side.

Stock News Today

- $TSLA | Tesla is creating a stir with a tease video of a plane resembling a drone, previewing a scheduled October 7 unveiling. A potential partnership with $ACHR | Archer Aviation is generating excitement, with Tesla looking at a extension of its ground-based AI ecosystem to air mobility. Archer’s certified eVTOL aircraft and FAA tailwinds make the partnership highly likely—and perhaps transformative.

- $AMZN | Amazon is said to consider solar-powered AI data centers in orbit. After brash pronouncements from Chamath Palihapitiya about ground-based power constraints for large-scale GPU growth, Jeff Bezos might be setting up AWS to profit from zero-cooling and unlimited solar capabilities.

- $RKLB & $ASTS | Rocket Lab and AST SpaceMobile are being watched as top infrastructure enablers should space-based compute come to fruition. RKLB can deploy the hardware, with ASTS being able to handle data movement, which makes for a potential AI infrastructure backbone in orbit.

- $EOSE | Eos Energy Systems was selected as a battery provider for a proposed $100-billion mega data center project for Greene County, which is the one associated with $GOOGL and $AMZN. This, if true, would be a large hyper-scaler deal for the battery company—bullish on long-duration adoption of the storage for AI workloads.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are starting to look tired despite the S&P 500 floating at all-time highs, with tech giants suffering valuation squeeze, regulatory challenges, and AI fervor starting to wane. Tesla and Meta especially are on the back foot, both easing 15–20% from their highs for 2025. Without new leadership from this group, the overall market might struggle for upward impetus. Sector rotation out of tech into industrials, energy, and defensives is growing obvious as a search for alternatives for high-growth exposures picks up pace.

Major Stock Market Performance on Monday, October 6, 2025

- S&P 500: 6,715.79, up 0.2% on the day after hitting new highs last week.

- Nasdaq Composite: At 22,844.05, trading flat as tech leadership fades.

- Dow Jones Industrial Average: Up 0.3% at 46,519.72, powered by energy stocks, industrials.

- Russell 2000: At 2,458.49, slightly higher, with small caps favored on rotation shifts.

We remain selectively risk-on on this market at Zaye Capital Markets. Mega-cap tech isn’t holding up, yet thematic themes such as satellite-based AI infrastructure are picking up steam, so investors need to turn on a dime here. Earnings strength, financial clarity, and disruption driven by innovation will be the main drivers of risk-reward for the fourth quarter.

Gold Prices

Gold jumped above the $3,900 level today, trading at $3,910.09 and touching highs at $3,924.39, as a combination of geopolitical nervousness and macroeconomic crosswinds pushed the demand for safe havens upward. The trigger was a wide-ranging series of pronouncements from President Trump, who delivered a strong ultimatum to Hamas, warning of a coming, large-scale offensive unless a deal is brokered by Sunday evening. President Trump’s declaration that “all hell” may break loose plus a call for innocent Palestinians to leave the region has conjured the specter of expanded fighting in the Middle East—a region already sensitive to reaction within commodity markets. As a further source of uncertainty, President Trump also issued a hold on $2.1 billion worth of Chicago infrastructure projects and adopted a tough position on the current government shutdown, further stoking domestic gridlock fears. Meanwhile, China’s overture of potentially investing several hundred billions within the U.S. during a series of on-going talks adds another dimension of uncertainty, given that it links into broader trade and currency talks that commonly go inversely with the strength of gold. In this context, the precious metal is reaffirming the time-honored position of a risk hedge against geopolitics and buffer against inflation, while market participants gear up for central bank commentary due out shortly. Today’s speeches from ECB President Christine Lagarde and BOE Governor Andrew Bailey are also drawing attention, as their tone could influence interest rate expectations and real yield projections across developed markets. If either adopts a hawkish tilt, citing lingering inflation risks, it could strengthen local currencies and weigh on gold’s upside. However, any dovish hints—particularly amid Europe’s weak services data—may push real yields lower, widening the runway for further gold strength. Adding to this bullish case, yesterday’s economic signals reinforced market concern that growth is slowing. U.S. services data fell to the neutral 50 mark, job creation remained weak, and leading indicators like new orders slipped—all pointing to rising stagflationary risks. The combination of weaker macro prints, geopolitical volatility, and energy-driven inflation fears is creating a fertile ecosystem for gold, not only as a tactical trade but potentially as a structural allocation. At Zaye Capital Markets, we continue to monitor rate differentials, ETF flows, and physical gold demand in Asia as leading indicators for the next leg higher.

Oil Prices

As of Monday, October 6, 2025, Brent crude sits at $65.44, with the WTI at about $61.77. This modest recovery of crude prices follows a modest OPEC+ output increase of just 137,000 barrels per day for November—a modest step that calmed markets anticipating a more robust increase. The increase was seen by investors as a signal that the cartel is cautious given weaker-than-expected demand globally, firmer inventories, and decelerating developed and emerging market macroeconomic momentum. Still, the delicate rally betokens a nervous balancing act between soft macro data and lingering geopolitical threats, with increasing doubts that world energy markets remain susceptible to shocks. Yesterday’s subpar U.S. services sector report deepened worries about eroding world demand, which might blunt oil consumption heading into Q4. Further, the recent lurch out of Chinese stimulus momentum, combined with weak factory orders for Europe, shadow the outlook for demand. Geopolitical events are also raising market concern. Escalating rhetoric from President Donald Trump about Gaza and his ultimatum for a Hamas deal by Sunday is stoking risk premiums across the oil complex. After Trump said “all hell” might break out should a deal not be agreed—and urged innocent civilians to leave the region—the threat of further Middle East destabilization has traders spooked. At the same time, China is said to be putting pressure on Trump to reverse investment restrictions, even threatening a trillion-dollar investment program—a geopolitical intrigue with the potential to impact the direction of U.S. energy policy. Looking out, today’s commentary from ECB President Lagarde and BOE Governor Bailey should have a bearing on currency and rate assumptions, therefore impacting indirect forecasts of oil demand prospects. If such tone reflects slowing growth or prolonged tightening, then oil faces fresh selling pressure. In addition, commentary from the IEA and OPEC ministers continues on high alert for new guidance, given the world energy order navigates a tightrope of macroeconomic vulnerability, growing risk of conflict, and structural shifts in supply.

Bitcoin Price

Bitcoin currently sits at $123,358, staying close to its two-month high after hitting a lifetime high of $125,245 temporarily during the weekend. The rise is a part of a general trend toward decentralized currencies due to global political instability and increasing skepticism toward the soundness of fiat currency. Trump’s increasing rhetoric on the Gaza war, which includes a threat of a catastrophic military response should a ceasefire not be agreed, has provided world markets with a new aspect of geopolitical risk. His administration freezing $2.1B of Chicago infrastructure funds, a growing confrontation with Hamas, and China approaches toward planned $1 trillion investments throughout the U.S., cumulatively, are creating uncertainty throughout the traditional asset basket. For Bitcoin, uncertainty is bullish. The market sees BTC as a virtual hedge, similar to gold, when confidence wanes from governments and centralized infrastructure. The anti-establishment, pro-cryptocurrency lean Trump has signaled toward in earlier terms and what seems certain to be a return to power provides speculative impetus, which suggests a potentially less hostile regulatory outlook toward digital currencies throughout the U.S. Meanwhile, institutional demand is reinforcing the bullish case for Bitcoin. According to multiple sources, spot Bitcoin ETFs are seeing large inflows as traditional asset managers increase crypto allocations amid uncertainty in equities and bonds. The U.S. government shutdown, now in its third day, is another tailwind. It creates risk aversion toward dollar-based and policy-dependent assets, pushing flows into BTC, which is increasingly viewed as a macro hedge. Yesterday’s soft U.S. services data and declining new orders readings pointed to decelerating growth, supporting the thesis that the Federal Reserve may be nearing the end of its hiking cycle. This macro backdrop—slower growth, political friction, a weaker dollar, and strong crypto flows—is a cocktail that favors continued upside in Bitcoin. Investors will be watching today’s central bank speeches from the ECB and BOE closely, as any dovish tilt could further lower real yields globally, making non-yielding alternatives like BTC more attractive in the coming sessions.

Eth Prices

Ethereum currently trades at $4,600, having maintained above $4,600 in recent trading sessions despite adversity and a small (~1,000 ETH) insider sell-off. Among the strongest support dynamics is revived institutional confidence—Spot ETH ETFs recorded $1.3 billion inflows last week, a reversal of earlier outflows, a sign of growing demand from large allocators. Whale activity is also notable: a number of large addresses are withdrawing ETH from exchanges and into self custody, a time honoured accumulation trend. Combined flows are supporting prices at current levels and underscoring belief amongst long-term interested parties.

The overall macro and geopolitical environment is boosting Ethereum’s appeal. Trump’s increasingly aggressive talk about Gaza, infrastructure freezes, and China-U.S. escalations is adding market risk to the established markets—the kinds of environments that tend to make interest in digital currencies, such as alternative stores of value, more likely. Yesterday’s soft business activity and services data have injected fresh doubts about growth, which tends to favor less cyclical assets. Down the road, the central speeches at the ECB and BOE today have the potential for changing real rates and currency moves—if they turn dovish, it should further lower the opportunity cost of being long non-yielding assets like ETH, likely driving further upside.