Where Are Markets Today?

U.S. equity futures are modestly higher today, with S&P 500 futures up a bit more than 0.2%, Nasdaq 100 futures up 0.1%, and Dow Jones futures down 0.2%. Across Europe, major indexes also are poised for a higher open, with Euro Stoxx 600 futures up modestly on the heels of universal advances in the industry and mining sectors. Investors are plotting a mixed landscape—celebrating earnings stamina from Oracle and M&A momentum, but bracing for key inflation data and high political noise. Here at Zaye Capital Markets, we view today as a classic “relief open” scenario: markets are tilted toward risk-on, but ultimately utterly reactive to macro and politial triggers not yet resolved.

Overnight’s big catalyst was Oracle’s post-earnings rally. Shares of the technology giant rose over 26% in after-hours trading, after the company posted a whopping 1,529% gain in multicloud database sales, driven by Amazon, Microsoft, and Google’s demand for AI-exclusive infrastructure. Oracle’s chief highlighted four multi-billion-dollar contracts in the first quarter alone—fuelling confidence throughout the AI ecosystem. Associated technology names including Nvidia and Palantir were seen getting favorable spillover benefits, boosting Nasdaq futures. It strengthens the hypothesis that the market remains very responsive to enterprise-scale investment themes in AI and vindicates stories of profitability in the clouds as solid market catalysts. European futures are ahead on M&A optimism as sentiment increases, despite a tightening bond market and French jitters over politics, where headlines surrounding an Anglo American–Teck Resources $50 billion merger awoke bullish sentiment in resource-intensive parts of the FTSE 100 and DAX, countering nerves related to the eurozone’s inflation trajectory and French bond market gyrations of late. Investors are weighing macro prudence against sector rotation on an opportunistic basis ahead of European Central Bank policy direction and commodity-related earnings releases. European bourses, as of this morning, are trying to build on earlier week’s gains on the back of favorable corporate transaction flow and robust earnings.

Nevertheless, the picture remains precariously poised. Geopolitical risk is back in the market story after Trump’s criticism of the Israeli bombing in Qatar, renewed talk of tariffs against China and India, and military threats against Venezuela. These pronouncements are stoking volatility in oil, defense, and emerging market assets. On the macro front, today’s Producer Price Index (PPI) and tomorrow’s Consumer Price Index (CPI) are set to provide definitive guidance on the Federal Reserve’s future course. A cooler-than-anticipated PPI release can continue to underpin rate-cut expectations up to September, maintaining equity traction. A hawkish surprise, on the other hand, can unravel futures euphoria and aggressively repeal risk assets. We at Zaye Capital Markets remain tactically bullish but continue to observe bond yields, option skew, and cross-asset volatility for early signs of market shift.

Major Index Performance – Wednesday, September 10, 2025

- S&P 500: At 6,502.12, up 0.22%, on the back of the energy and.

- Nasdaq Composite: 18,661.31 up 0.28%, on the heels of a major upsurge.

- Dow Jones Industrial Average: Higher 0.4% to 45,711.34, on healthcare and financials.

- Russell 2000: Edged back to 2,381.82, -0.5%, a reflection of ongoing stress on small-cap liquidity and sensitivity to.

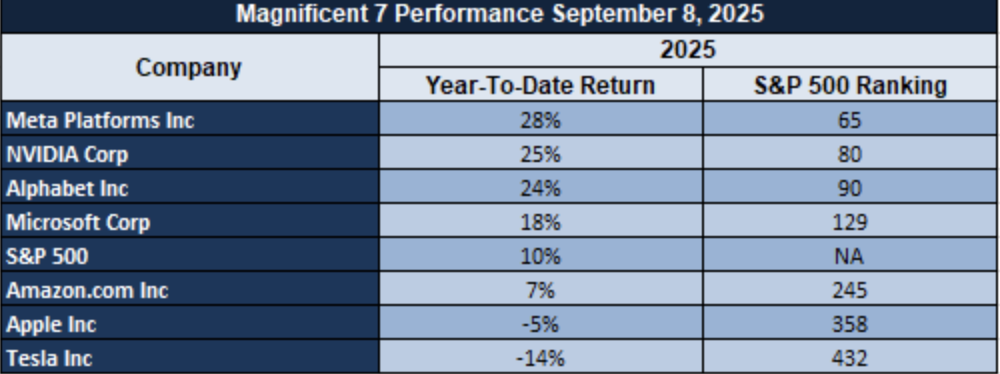

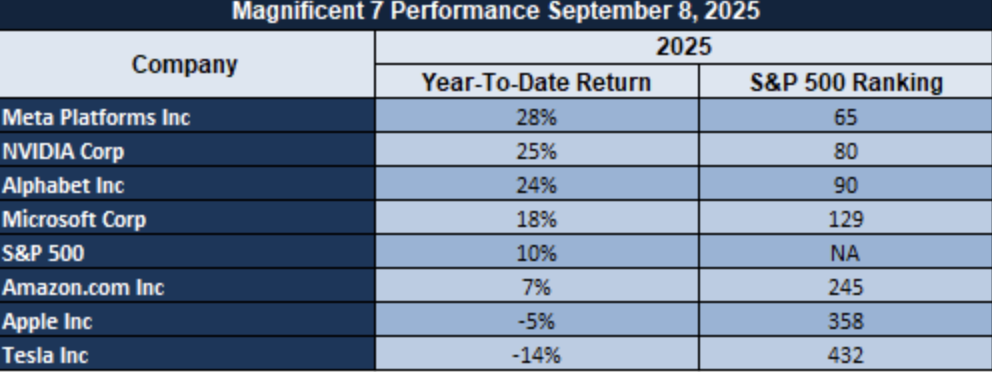

The Magnificent Seven and the S&P 500

The “Magnificent Seven” continue to display signs of exhaustion. Apple’s decline, coupled with compressed multiples across other mega-cap names, has pulled on S&P 500 breadth. While the index has been supported by defensives and selective cyclicals, its reliance on a narrow set of tech leaders makes it vulnerable. Investors are now demanding not just revenue growth, but disciplined execution, clear monetization of AI initiatives, and margin stability to sustain elevated valuations.

Drivers Behind the Market Move

Below are the three key drivers typical of U.S. and European markets today:

1. Inflation Signals and the Fed Rate Outlook

Markets are focusing intently on today’s release of the Producer Price Index (PPI), coming on the back of a surprise 3.3% year-on-year rise in U.S. wholesale prices for July—the biggest such gain in five months and a sign producer inflation is gathering pace. Albeit, inflation is still close to 3%, higher than the Fed’s 2% target, but still rate cuts are anticipated, in light of remarks implying the Fed could reduce rates even in a higher inflationary scenario. Such a delicate balance—resurgent inflation and dovish policy leaning—is spooking equity and bond investors, although for the time being, risk assets remain propped up.

2. Geopolitical Climate and Trade Rhetoric

Geopolitical hotspots continue to cast a shadow over sentiment in markets. President Trump’s labeling of Israel’s strike in Qatar as “counterproductive,” alongside his demand for steep (100%) EU tariffs on China and India, have increased geopolitical and trade-related uncertainty. These are stoking safe-haven flows and increased volatility in energy, defense, and commodity markets. At the same time, markets are absorbing these political cues while waiting for resolution, generating a tenuous balance on risk appetite versus defensive strategy.

3. Labor Market Weakness Amplifying Monetary Easing Expectations

Investors are also reacting to a sharp slowdown in U.S. job growth—just 22,000 new positions added in August—confirming labor market softening and increasing pressure on the Fed to act. This dovish sentiment supports equity markets, especially for rate-sensitive sectors, although it also raises concerns about broader demand strength, particularly in consumer-oriented and cyclical industries. The tension between weaker macro data and policy flexibility remains a central theme driving asset allocation decisions.

We interpret today’s market positioning as fundamentally “watch-and-wait”, with risk appetite tethered to improving inflation clarity, geopolitical de-escalation, and incoming labor data trends. Confirmation in any direction—either through softer PPI figures or easing rhetoric—could catalyze renewed momentum. Until then, we remain selectively tilted toward high-quality, rate-sensitive assets, while monitoring volatility channels and internal breadth for signs of sustainable recovery.

Digesting Economic Data

The TRUMP Tweets and Their Implications

President Trump’s latest publicly released comments have caused geopolitical stirrings through diplomatic, economic, and market corridors. His series of explanations on the Israeli strike in Doha, labeling it as “unfortunate” and “counterproductive,” amounts to a clear attempt to disown the move, blaming only Israeli leadership. Trump’s vocal discontent, especially in referring to the event as a threat to the U.S.–Qatar relationship, reflects deeper strategic prudence in a region already volatile in the Middle East calculus. These remarks are also set to push up risk premiums in oil markets and safe-haven instruments, particularly as Qatar remains a major participant in world LNG supply and U.S. base facilities. His disavowal is set to be taken in markets as a prelude to a bid to contain diplomatic fallout in the run-up to upcoming multilateral energy and defense summits.

Trump’s EU push for 100% tariffs on China and India represents a re-escalation of international trade friction, linking directly the strategy on tariffs to exertions on Russian influence and international commodity routes. Though no explicit policy measure has taken place as yet, such pronouncements can stoke pre-emptive volatility in equity and FX markets, notably for globally exposed industrials, semiconductors, and farm exporters. His remarks on current talks with India, however, presented a more moderate tone—presaging space for bilateral de-escalation even in the midst of aggressive multilateral grandstanding. At Zaye Capital Markets, we are of the opinion that markets might start discounting increased policy risk surrounding tariffs and retaliatory trade, specifically in the event the EU takes a diplomatic or legislative response. Domestically, a call for a supplementary $1 billion in appropriations to avert a potential government shutdown, in conjunction with a 42% approval rating, mark increased fiscal anxiety and political acrimony. Such issues might weaken consumer sentiment, defense industry sentiment, and overall macro risk evaluation—particularly should debates over appropriations continue to unfold in the guise of a completed shutdown scenario. Additionally, the White House’s announcement that it is in favor of a forensic investigation of the suspected Trump handwriting on a letter related to Jeffrey Epstein produces yet another political diversion, and might help to further attenuate an already low measure of policy certainty and legislative functionality in a contentious fiscal period.

Adding to the volatility are Trump’s remarks on Venezuela, where he threatened to shoot down any Venezuelan aircraft posing a threat to U.S. ships. Such statements bring military risk to a previously tenuous geopolitical environment, especially in the aftermath of U.S. naval deployments in the Caribbean region. With his much-publicized appearance at Yankee Stadium and open-statement pronouncements that again dominate both headlines and algorithmic sentiment triggers, Trump’s media footprint continues real-time leverage over intraday volatility, particularly in defense, energy, and emerging market assets. At Zaye Capital Markets, we continue focus on the second-order consequences of such policy cues—from pricing in the commodity space to defense stock outperformance—while monitoring closely a shift in the flow of foreign capital in response to hardening rhetoric.

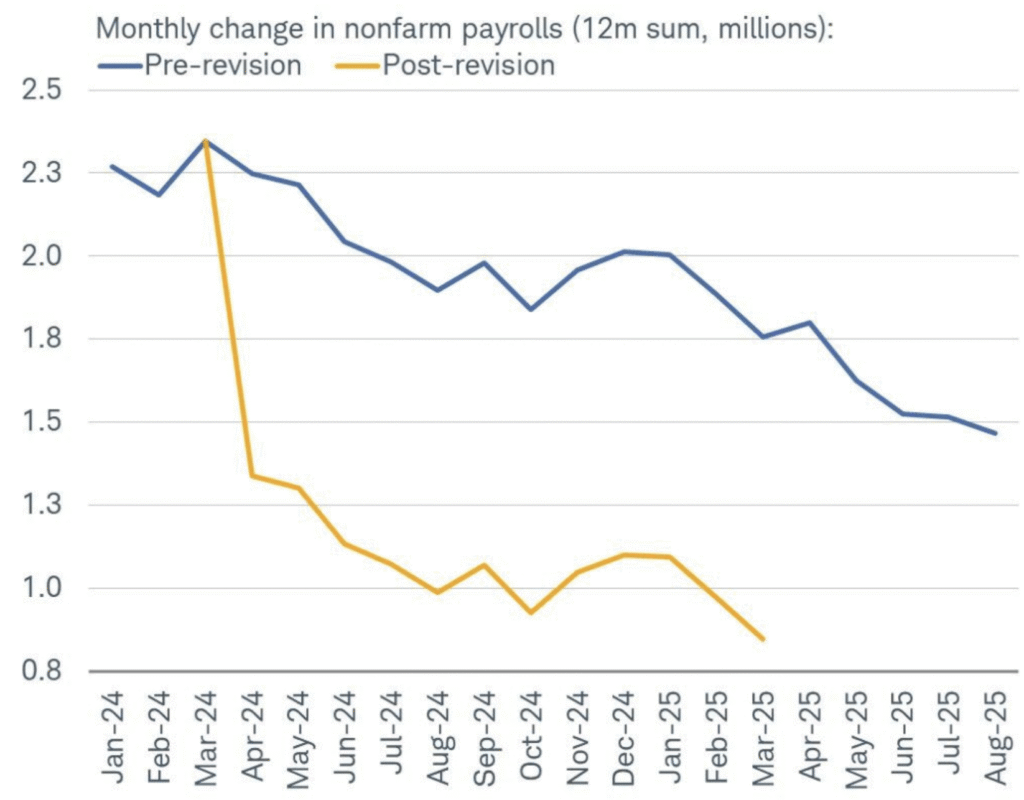

Payroll Revisions Expose Fragile Labor Market Momentum

Preliminary benchmark revisions to U.S. nonfarm payroll data revealed a sharp downward adjustment, with monthly job gains over the past year reduced from an average of 186,000 to just 71,000. This marks one of the steepest revisions in decades and raises questions about the durability of the labor market’s momentum. The recalibration signals that employment strength may have been overstated in earlier reports, suggesting slower hiring trends are emerging beneath the surface of headline growth figures.

This weaker pattern was reaffirmed in the September 2025 report, where employment growth stalled at a paltry 22,000. Combined with regional Federal Reserve officials’ warnings on tariff-related pressures, these events suggest trade policy brought a further friction on business investment and employment growth. BLS revisions in the past are normally within a ±0.1% margin, so this lopsided revision is an exceptional occurrence highlighting structural ambiguities, from survey nonresponse to forecasting errors. Such a magnitude places the labor market in a more exposed position toward policy errors and external shocks than previously thought.

For investors, the implications are multifaceted. While broad equity sentiment may soften on fears of weakening growth, opportunities remain in undervalued sectors poised to benefit from policy shifts. Financials and consumer discretionary stocks appear attractively priced as the weaker labor narrative increases the likelihood of rate relief, supporting credit and household demand. Analysts should monitor upcoming wage data, capital expenditure intentions, and sector-specific earnings revisions to gauge resilience. Selective positioning remains key, and labor-sensitive sectors may offer re-rating potential as the market digests these new economic realities.

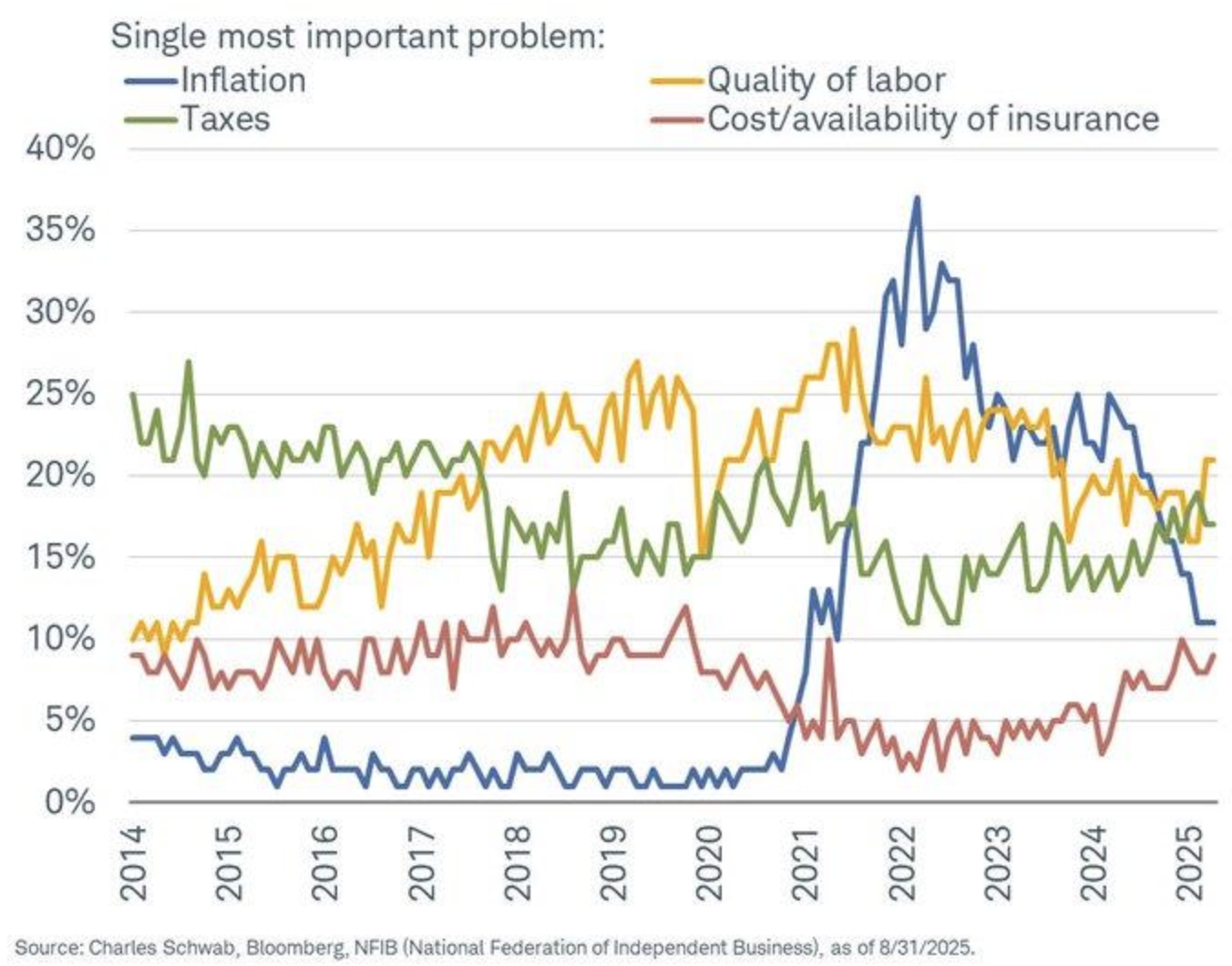

Labor Quality Problem Faced by Small Firms

We observe a widening gap in recent data between the longstanding economic worries—inflation and taxes—versus a newer, pressing problem brought to prominence only in recent years: labor quality. Through late August of 2025, 21% of small business owners specifically cited labor quality as their biggest challenge, up 5 points from June and a steady leader in their worries. Across the same period, inflation and taxes dropped back in relative severity, cited as a problem in a 11% and a 17% of owners respectively.

Such a movement reflects more than a short-term trend—it reflects a structural shift in the small business landscape. Labor issues continue to persist, with 32% of owners currently having openings they could not fill, a measure far higher than in past years. It’s particularly common in sectors where we might least want to see it, such as in construction, manufacturing, and transportation, where nearly half the businesses reporting describe having persistent voids. Erosion in talent in the workforce could be inhibiting small business growth far more than at a macro level such as expense or rule.

From our analyst perspective, select sectors appear particularly undervalued in light of these dynamics. Industrial services and productivity-enhancing technologies are poised for upside as businesses seek solutions to bridge staffing gaps. Meanwhile, training and workforce development initiatives—both public and private—warrant close monitoring. Investors should watch for policy signals or corporate strategies aimed at upgrading labor quality, as these could catalyze sector re-rating and drive outperformance in industries aligned with small business operations.

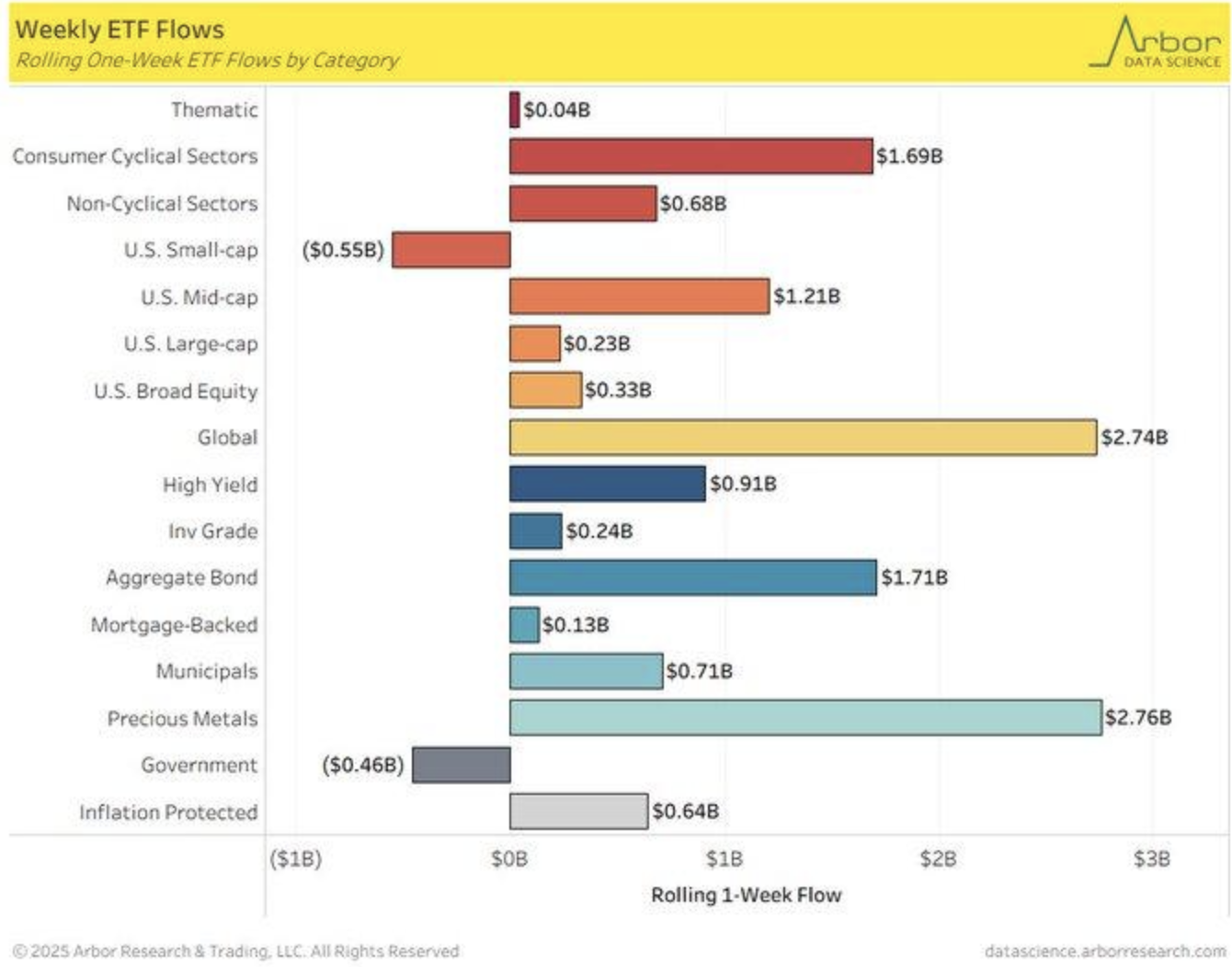

ETF Flows Indicate Hedges Against Inflation and Fading Confidence

Last week’s data on ETF flows indicates a rapid change in investor sentiment. Global high-yield debt gathered $2.74B in flows, and precious metals gathered $2.78B, in a rotation towards assets thought to provide inflation hedges or stores of value as uncertainty grows. It was as U.S. small-cap ETFs had $0.68B in outflows, with a $0.48B withdrawal from government bonds, implying investors are taking a measure of the appetite for risk and confidence in familiar safe havens.

From an inflation perspective, such flows highlight a market increasingly doubtful of the efficacy of policy in restraining price pressures. Trends in inflation have demonstrated persistency in service and energy-related segments, muddying disinflation stories. The shift towards high-yield bonds reflects a desire on the part of investors to take credit risk for yield in a wager that inflation-adjusted earnings remain positive in the event central banks soften their tightening approach. Such a position reflects not only high inflation expectations but also spurring tactical asset allocation out of low-return government paper.

Gold, in our opinion, requires close attention. Precisely, the $2.78B precious metal inflow follows classic patterns in which dollar depreciation risk and inflationary concern expectations build up bullion demand. Current parameters suggest gold prices might reach new peaks as institutional and retail flows build up pace. For investors, this further bolsters the opinion that precious metals and certain high-yield assets are undervalued in comparison with defensive profiles. Analysts must monitor gold ETF flows, central bank purchases for reserves, and real interest rate swings as the key predictors for future precious metals space upside momentum.

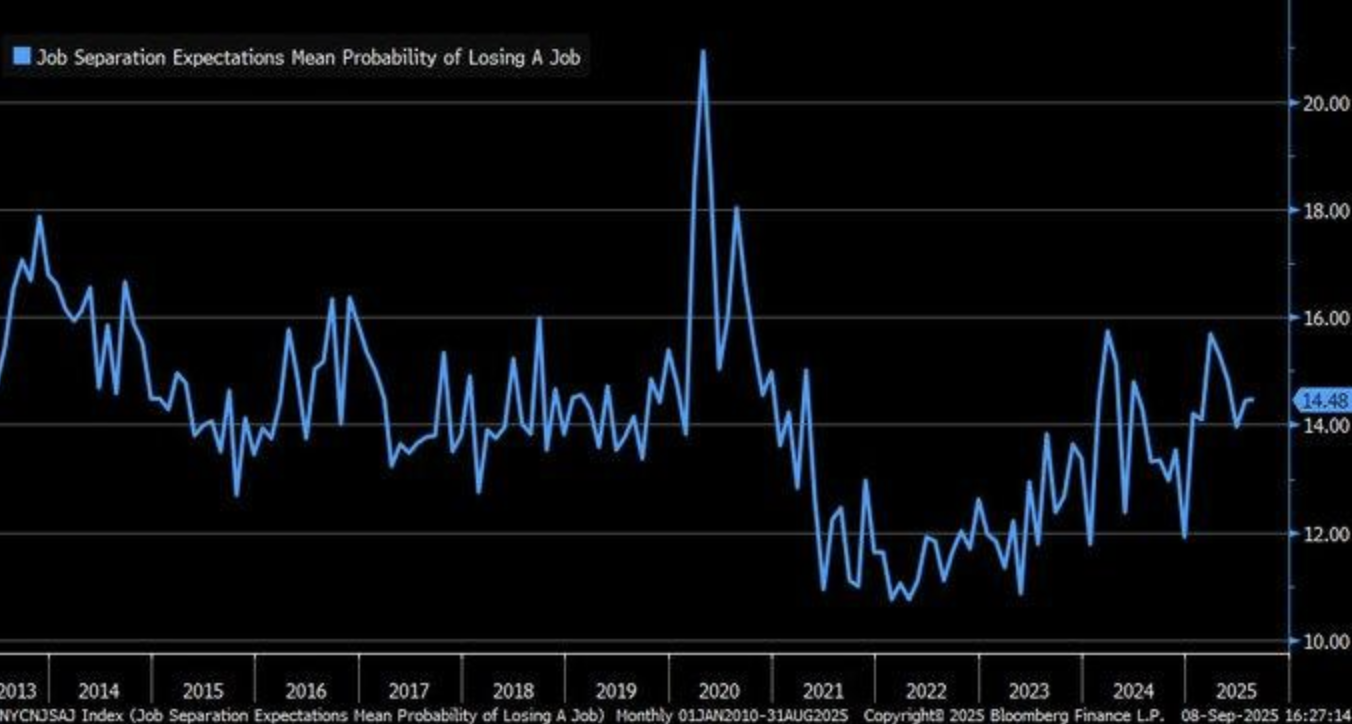

Soaring Fears of Job Loss Test Labor Market Stability

New data shows a sharp divergence between official statistics and consumer sentiment. Bloomberg estimates put the mean probability of job loss at 14.48% in August 2025, a level far above historical norms and inconsistent with the Bureau of Labor Statistics’ reported 62.3% labor force participation rate. This disconnect suggests that headline indicators may not be fully capturing underlying weakness, particularly as industries like manufacturing shed 78,000 jobs over the past year and transportation equipment employment fell by 15,000 in August due to strike activity.

For investors, both these data points are important to consider as they indicate a need to go beyond usual metrics in assessing labor market health. Higher job insecurity was consistent with University of Michigan sentiment surveys registering increased labor pessimism, echoing consumer recession fears in spite of a “stable” jobs environment. Studies in academia elaborate on this phenomenon: worries over job losses often precede actual unemployment increases by 6–12 months, so a spike in perceived insecurity currently could turn out to be an early indicator. Analysts must beware drawing conclusions on official stability as a reflection of resilience where forward-looking sentiment is something different.

This setting recalibrates market sentiment. Those areas most sensitive to consumer confidence, retail and discretionary equities for example, are exposed and potentially overheated against near-term threats. Consumer staples and defensive healthcare are appearing undervalued, for they benefit disproportionately in the event of retrenchment of spending plans in households. It will be important to monitor sentiment indicators in conjunction with revisions in payrolls and strike data.

Soaring Card Dependence Stirs Economic Heat-Up Risks

Revolving consumer credit jumped 9.7% annualized in July 2025, registering a clear shift towards increased use of credit cards for maintaining spending in the face of inflationary demands. A marked contrast to the dip in credit demand back in 2020, when expenditure dropped steeply and revolving use dropped in double digits. It is a reflection of both durable consumption and a nascent strain on household budgets with borrowing remaining high at 7–8% on weighted credit card rates.

This trend goes against usual expectations in monetary tightening. Rather than reducing borrowing, higher rates are ostensibly producing higher credit dependency as families turn towards short-term credit to fill income-expense gaps. Scholarship suggests such dependency is often a prelude to consumer economy stress points, where unsecured debt is at once a lifeline and a future destabilizer. Revolving credit growth is presently ahead of non-revolving segments such as autos and students, akin to 2008-style patterns not seen since before the last big banking crisis.

From an investor’s perspective, they represent areas of risk and opportunity. Consumer discretionary stocks are vulnerable to downside in the event higher credit burdens are converted later in the year to decreased spending power, while banks with high credit card exposure may initially benefit from higher earnings from higher yields but are vulnerable to higher delinquency risk in the event of continued stress in the household sector. Analysts need to monitor delinquency patterns, credit spreads, and retail earnings guidance in determining whether the borrowing spree is evidence of short-term strength—or early warnings of economic overheating capable of toppling broader market stability.

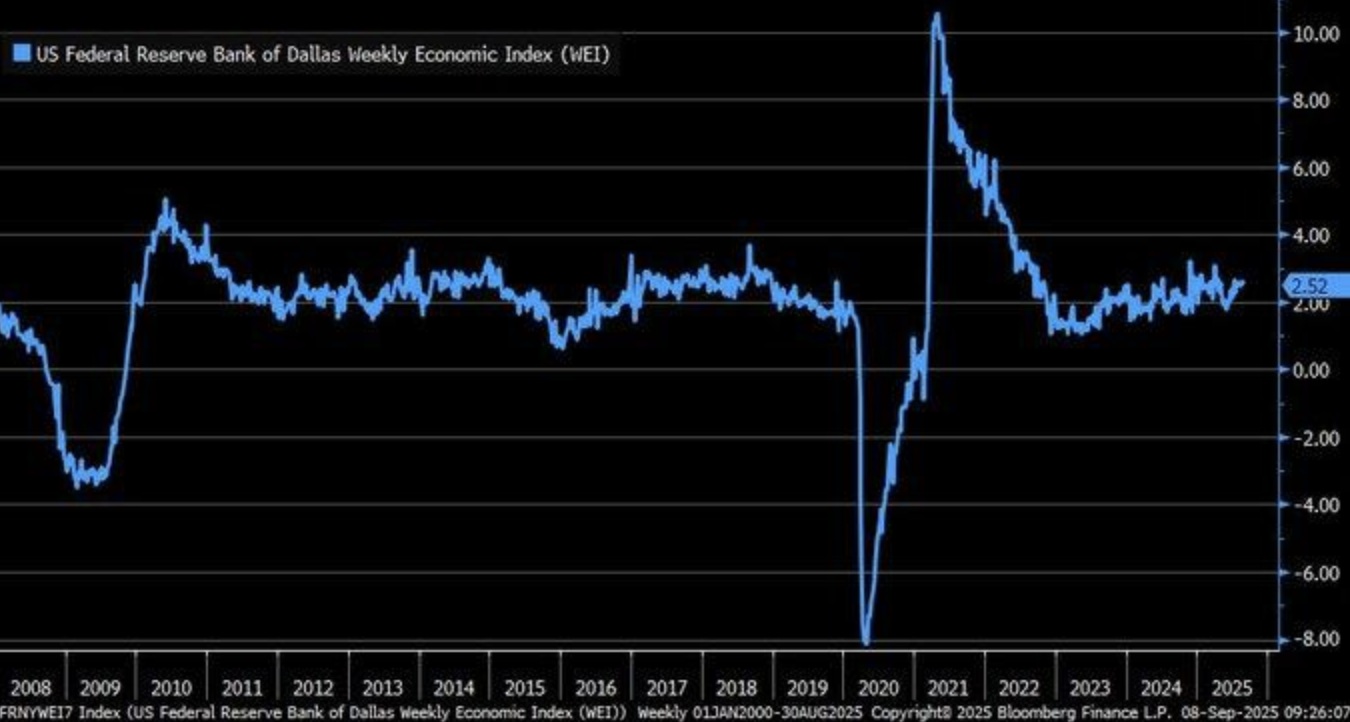

WEI Stability Masks Primary Weaknesses

The Weekly Economic Index (WEI), compiled by the Federal Reserve Bank of Dallas, has remained broadly stable throughout 2025, aggregating signals from labor, consumption, and production data. At face value, this paints a picture of resilience in the U.S. economy, particularly when contrasted with the sharp collapse in 2020. Yet this steadiness now stands in tension with the Bureau of Labor Statistics’ recent benchmark revision, which removed 900,000 jobs from the record between 2024 and 2025, the largest adjustment in modern history. Such a correction calls into question the real-time accuracy of indices like the WEI.

Comparing economic indices reveals such divergence. As the WEI implies stability, payroll changes indicate a far more subdued employment background more in line with a decelerating economy rather than stability. It reflects concerns from throughout financial leadership that growth is overestimated by the coincident indicators. A 2023 study from the National Bureau of Economic Research lends credence to such a perspective, in turn commenting that real-time indices are prone to lag in the midst of structural change, obscuring movement in labor force participation, productivity, or business start-ups. The danger then is optimism from composite measures proves deceptive.

For investors, the lesson is to view headline indices with a healthy skepticism and focus more on cross-comparisons. Labor market-sensitive sectors like consumer discretionary and regional banks are put on vulnerable footing if latent weakness turns out deeper than aggregate data indicate. Defensive stocks and high-quality dividend payers are cheap on relative merit against such dangers and offer protection against volatility. Market sentiment and sector leadership are foreshadowed in most instances by inconsistencies between high-frequency indices like the WEI and later revisions from official agencies. Analysts have to heed such divergences.

Upcoming Economic Events

Core PPI m/m, PPI m/m

For Zaye Capital Markets, today’s later release of producer price data is viewed as a primary market sentiment gauge. Both the headline PPI and core PPI (excluding food and energy) are forecast to give a major input into the durability of underlying patterns of inflation. As investors continue to become increasingly responsive to surprises in inflation, those numbers are forecast to have a primary determining impact on future directional expectations for Federal Reserve policy and sectoral performance.

Core PPI m/m

- Above-consensus Core PPI would emphasize continued input price pressures in manufacturing and the services sector. From our perspective, such a result would revisit higher rate expectations, with yields likely propelling up as markets price in lower probabilities of near-term easing. Equity investors need to gear up for rotation out of growth-dependent sectors, as higher discount rates squeeze valuations.

- On the other hand, below-consensus Core PPI would provide support to the disinflation narrative we’ve been tracking since mid-summer. Such a situation would provide a relief for the Fed, renewing risk appetite and boosting technology, real estate, and consumer discretionary shares still undervalued in a soft-inflation world.

PPI m/m

The headline PPI carries equal importance, though food and energy inputs may emphasize volatility.

- If the print comes in stronger than expected, then defensive positioning would gain traction, and precious metal, commodity, and dividend-oriented equity flows would act as hedges against the risk of inflation. U.S. Treasury paper could see shorting revived, taking yields up and putting further strain on rate-sensitive assets.

- A below-expectation headline PPI, however, would reinforce the view of easing supply-side cost pressures, particularly in energy-sensitive areas. Such a development is expected to boost equity momentum, push bond yields lower, and prolong the case for a more dovish Fed approach through end-of-year.

As a firm, we emphasize analysts need to track not only the headline versus core gap but also sector-level market reactions in real time. Higher volatility in the period surrounding these releases offers both risk and opportunity, especially among investors who are long cyclical and inflation-sensitive stocks. We see next week’s PPI data as a watershed indicator, determining whether inflation risk is still deep-seated or disinflationary forces are coming to dominate the economy more widely.

Stock Market Performance

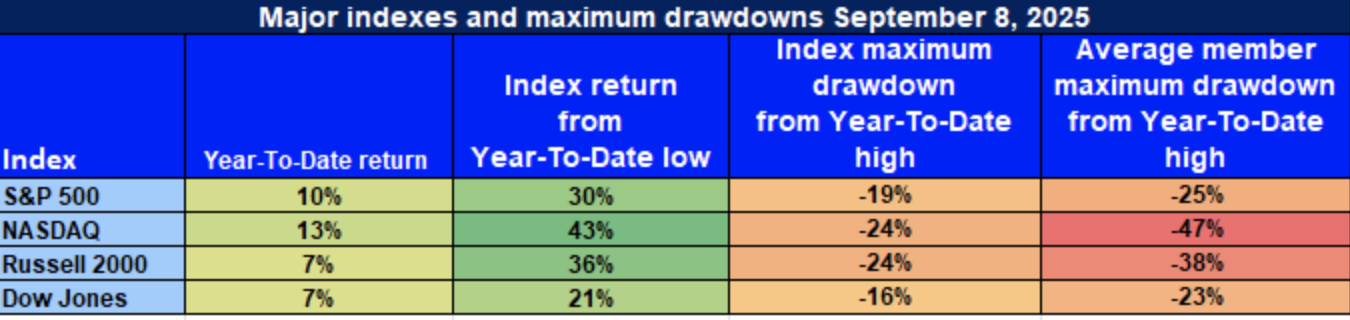

Indexes Recover from April Lows, But Weak Breadth Indicates Caution Remains

U.S. equity markets have substantially recovered from the low on April 8, but the strength is haphazard. Year-to-date performance remains shallow, and peak drawdowns highlight most constituents remaining submerged beneath the surface. While headline indices show strength, median member performance sheds light on narrow breadth and continued volatility.

We have here our summary of last week’s performance on major indexes:

S&P 500: Gains Tempered by Underlying Weakness

YTD: +10% | -30% below April low | -19% from YTD peak | Avg. member: -25%

The S&P 500 indicates good 2025 progress with a 10% advance and a 30% recovery from April. However, a 19% retracement from YTD tops and average member retracements of 25% indicate leadership continues to be narrowly centered in a few big-cap stocks while broader participation remains soft.

NASDAQ: Outperformance Hides Drastic Member Erosions

YTD: +13% | -43% below April low | -24% from YTD high | Avg. member: -47%

NASDAQ was the clear leader, up 13% for the year and up 43% from April lows. A steep 24% decline from tops and an average member loss of 47% suggest technology-heavy index weakness testing growth leadership sustainability.

Russell 2000: Small-Caps Struggle Despite Rebound

YTD: +7% | -36% below April low | -24% below YTD high | Avg. member: -38% Small caps rose 36% from the low in April, yet the Russell 2000 is only up 7% on a year-to-date basis. Further 24% drawdowns from the high and a 38% typical member decline demonstrate ongoing stress on more economically sensitive and lower liquidity stocks.

Dow Jones: Defensive Bias for Relative Stability

YTD: +7% | -21% below April low | -16% from YTD high | Avg. member: -23% The Dow Jones continues in its defensive leaning, having gained 7% in the year so far and 21% from the low in April. Its modest 16% drawdown on a low reached in April is a sign of strength, but 23% average member declines highlight the stress even in traditional value sectors.

For Zaye Capital Markets, we are cautious. Market breadth is still vulnerable, and although headline gains are cheerful, fundamental data cements the argument for selective exposure. Quality businesses with healthy balance sheets and defensive earnings streams remain preferred, while we continue to observe index breadth as a necessary prelude to a more durable rally.

Earnings

Earnings Recap— Yesterday (09-Sep-2025)

- Oracle (ORCL)

Oracle posted strong Q1 FY26 results with revenue of $14.9B (+12% y/y) and cloud revenue rising to $7.2B (+28%). Remaining performance obligations reached $455B (+359% y/y), reflecting robust demand for multicloud and AI-related services. The critical factors to watch are Oracle’s OCI growth trajectory, its ability to scale AI workloads, and whether the elevated capex pace delivers the expected returns.

- Rubrik (RBRK)

Rubrik’s Q2 FY26 revenue came in at $309.9M (+51% y/y), supported by subscription ARR of $1.25B (+36%). Non-GAAP gross margin held at a healthy 81.6%, with free cash flow rising to $57.5M. Investors should focus on subscription durability, margin progression, and how well Rubrik integrates GenAI initiatives—particularly following its Predibase acquisition.

- Core & Main (CNM)

Core & Main reported Q2 net sales of $2.093B (+6.6%), with GAAP EPS of $0.70 and adjusted EPS of $0.87. However, management lowered FY25 guidance to $7.6–$7.7B in net sales and $920–$940M in adjusted EBITDA. The outlook highlights near-term caution, and we are watching whether municipal demand remains strong enough to counter residential softness and margin pressure from pricing adjustments.

- GameStop (GME)

GameStop delivered Q2 revenue of $972.2M (+22% y/y), with collectibles up 63% and hardware/accessories up 31%. The after-hours stock reaction was positive, reflecting improved momentum. Still, analysts should closely monitor the company’s software mix, inventory discipline, and how its sizeable cash position will be deployed to stabilize long-term operations.

Earnings Preview— Today (10-Sep-2025)

- Chewy (CHWY)

Chewy is set to report before market open, with its earnings call scheduled for 8:00 a.m. ET. Key areas to monitor include Autoship penetration, active customer trends, and margin dynamics—particularly the mix between private-label products and freight costs. Advertising monetization also remains a critical lever for profitability.

- Daktronics (DAKT)

Daktronics will also report before the market opens. Our focus is on backlog conversion, margin recovery following prior supply-chain challenges, and cash flow against working capital needs. These metrics will indicate whether operational improvements are translating into sustainable earnings strength.

- Tsakos Energy Navigation (TNP)

Tsakos is expected to release Q2 results this morning. The core drivers to watch are fleet utilization, spot versus time-charter exposure, and leverage management in the face of volatile tanker rates. Performance here will shape investor sentiment toward tanker-linked equities.

- Oxford Industries (OXM)

Oxford Industries reports after the close today. Analysts should track direct-to-consumer momentum across Tommy Bahama and Lilly Pulitzer, alongside wholesale order trends. Inventory turnover and markdown activity will be important signals for margin protection in a more cautious retail backdrop.

- National Beverage (FIZZ)

Although initially flagged for today, National Beverage earnings are expected tomorrow, September 11, 2025. When reported, investor focus will be on case-volume growth, channel mix, and pricing elasticity in its sparkling water portfolio, which remain critical for brand competitiveness.

Stock Market Overview – Wednesday, September 10, 2025

U.S. equities continued ahead and were spurred on by growing optimism for loosening Federal Reserve policy after last week’s historic revision of labor market data. As mixed economic data were in evidence, investor sentiment was bullish, with major indexes hitting or staying near historic highs. Trends were driven by a combination of dovetailing labor data, selective earnings surprises, and pre-inflation-report optimism.

Stock Prices

Economic Indicators and Geopolitical Changes

Last week’s revision lower of 911,000 jobs from March payrolls cemented the sentiment that the labor market is decelerating, bringing forward expectations for a rate cut. Markets now widely expect at least a single 25-basis-point rate reduction by year-end. Against this background, optimism in rate-sensitive corners was boosted, though higher oil prices and geopolitical risk, especially surrounding renewed hostilities in the Middle East region, complicate the macro picture. Hesion in investors over inflation data remains, especially ahead of PPI releases later in the week.

Live Stock Update

UnitedHealth increased 8.6% on favorable Medicare Advantage projections, and Nebius surged near 50% after taking a $17.4 billion Microsoft contract for AI infrastructure. Apple dropped 1.5% after it unveiled iPhone 17 with lukewarm investor responses. Oracle surged up over 20% in after-hours on back of robust cloud backlog growth. Palantir, TSMC, and Netflix had breakout days too—but valuation concerns remain a thorn for the overall sector technology.

The Magnificent Seven and the S&P 500

The “Magnificent Seven” continue to display signs of exhaustion. Apple’s decline, coupled with compressed multiples across other mega-cap names, has pulled on S&P 500 breadth. While the index has been supported by defensives and selective cyclicals, its reliance on a narrow set of tech leaders makes it vulnerable. Investors are now demanding not just revenue growth, but disciplined execution, clear monetization of AI initiatives, and margin stability to sustain elevated valuations.

Major Index Performance – Wednesday, September 10, 2025

- S&P 500: At 6,502.12, up 0.22%, on the back of the energy and.

- Nasdaq Composite: 18,661.31 up 0.28%, on the heels of a major upsurge.

- Dow Jones Industrial Average: Higher 0.4% to 45,711.34, on healthcare and financials.

- Russell 2000: Edged back to 2,381.82, -0.5%, a reflection of ongoing stress on small-cap liquidity and sensitivity to.

For Zaye Capital Markets, we are still watching to see if such a rally constitutes durable participation or a mere reaction to dovish monetary indications. Ahead of data on inflation and sector rotations underway, we prefer selective exposure to those businesses for whom clear earnings visibility exists, deft free cash flow, and defensible valuations.

Gold Price

Gold jumped to a new record high of $3,673.95 per ounce today on a perfect storm of macro catalysts: renewed geopolitical tension, softening labor market indications, and building expectations of Federal Reserve interest rate cuts. A key institutional vehicle, the SPDR Gold Shares ETF (GLD), is trading in the region of $334.06, in reflection of the move. Yesterday’s shocking Bureau of Labor Statistics payroll revision—revealing 911,000 fewer jobs added than initially estimated—has hastened the shift in market sentiment towards a looser monetary stance. This dovish shift, in sync with a weakening dollar and rising anxiety surrounding systemic risk, has boosted gold’s barometer-hedging properties against both inflation and political risk. As such, today’s releases of Core PPI and headline PPI figures will act as a key validation point. A softer-than-projected inflation print will bolster the argument in favour of easing, delivering additional upside for bullion. However, a hotter print might temporarily stall the rally, but the overall trajectory remains upward unless the Fed takes on a renewed hawkish stance—which currently appears improbable in light of recent economic data.

From a geopolitical standpoint, gold is in focus again as a world risk barometer. President Trump’s explicit criticism of Israel’s unilateral air strike against Qatar—an affair described by him as both “counterproductive” and “unfortunate”—has added to diplomatic friction in the region. His additional threat to the EU to impose 100% tariffs on China and India, in the midst of a broader campaign of economic coercion against Russia, added a whole new dimension to international trade nervousness. As a rule in the past, when diplomatic understandings concerning oil-exporting regions and world centers go bad, gold tends to benefit from a safe-haven flow bonanza. Market participants are also watching the Fed’s reaction to soft labor markets and today’s inflation data for a shift in policy. At Zaye Capital Markets, our opinion is that a mixture of geopolitical friction, disappearing real yields, and structural dollar vulnerability puts gold on a sweet spot in the near term. As long as core macro data and diplomatic certainty remain out of reach for us, we see physical gold and gold-backed ETF demand remaining healthy, with institutional flows continuing to drive price strength.

Oil Prices

Crude oil prices are pushing higher, with NYMEX WTI crude at $63.12 a barrel and Brent at $66.87, both notching modest gains of around 0.7% for the session. This upward push comes against a difficult set of geopolitical risk, macro economical instability, and cautious OPEC+ supply signals. Markets reacted forcefully to the Israeli strike on Doha, reviving Middle East risk premiums, even as the White House made a bid to play down further escalation prospects. OPEC+’s recent output agreement did nothing to dampen the bullish spirit—increasing output by a meager 137,000 barrels a day for the month of October, far short of expectations. Non-OPEC production growth, the IEA says, is flatlining, even as non-investment in upstream supply persists. Yet softness on the demand side—led by Asia and Europe—is capping advances, in combination with U.S. inventory build and a possibility of an oil supply glut back in the picture in the approach to Q4.

President Trump’s remarks have added a further layer of complexity to oil market sentiment. His explicit dissatisfaction with Israel’s missile strike on Qatar and biting criticism of unilateral military aggression have increased diplomatic friction, while his demand for the EU to put 100% tariffs on China and India fans the flames of a global trade standoff. Such inflammatory language threatens to dampen global trade volumes and cramp up energy demand, particularly if retaliatory policies emerge. Yesterday’s sharply-downgraded revision in payrolls revived the prospect of a looser Fed, providing a tailwind for commodities via a softening dollar storyline. While traders remain laser-focused on today’s Core PPI and headline PPI reports, such a softer-than-anticipated inflation print would likely underpin crude, reinforcing demand expectations to buoy energy equities. Conversely, a Sri Lanka-style inflation shock could resurrect growth fears and reignite demand anxiety. At Zaye Capital Markets, we hold the view oil’s near-term direction lies at the crossroads of geopolitical chess, monetary recalibration, and whether macro data solidifies a disinflationary glide path or a nascent wave of stagflation risk.

Bitcoin Prices

Bitcoin currently trades at $111,469, steady after a topsy-turvy 24-hour period in which it hit intraday highs of $113,237 and lows of $110,812. The digital currency continues to consolidate above the key $110K psychological level, a reflection of resilience in the face of growing worldwide and economic instability. At Zaye Capital Markets, we believe Bitcoin’s newfound stability is the result of both increased liquidity expectations and geopolitical hedging behavior. US President Trump’s denunciation of Israel’s Qatar strike and his renewed demands for 100% EU tariffs on China and India have increased world tension and reignited worries surrounding energy security, trade bifurcation, and widespread political instability. In such atmospheres, Bitcoin repeatedly establishes its value as a non-sovereign, decentralized asset, especially when confidence in international coordination falters. Meanwhile, institutional corridors remain enthusiastic: Microstrategy’s acquisition of 3,200 coins in September, Gemini’s valuation lift through their IPO, and Nigeria’s Senate bid for regulation corridors continue to indicate increased world integration. Couple those with El Salvador’s renewed declaration of BTC as a legal tender and a record high world hashrate, and we are seeing a rare simultaneous build-out of both top-down and grassroots momentum behind the asset. The macro story is no less favorable.

Yesterday’s historic BLS job revision—downing over 900,000 payrolls from earlier reports—created a watershed event which tilted the rate path narrative sharply dovish. Bitcoin reacted appropriately, sustaining levels well above $110K as markets factored in the possibility of earlier Federal Reserve rate reductions and renewed dollar softness. Bitcoin’s market increasingly follows classical economic triggers, and today’s release of Core PPI and headline PPI figures shall remain the next major volatility spark point. A softening inflation print shall continue to support Bitcoin’s short-term bull trajectory, as decreasing real yields and decreasing opportunity costs of owning non-yielding assets start to kick in. Technically, a break higher toward $120K remains a possibility, says analysts, if present support stands the test, although option data does indicate some dealers are pricing in downside via increased put buying—particularly if inflation data surprises higher. As liquidity returns and the world’s central banks move toward accommodation, Bitcoin remains well placed to benefit from both system hedging demand and structural adoption tailwinds. Zaye Capital Markets remains cautiously bullish, yet continues to monitor key world responses from regulators and shifts in capital flows, both capable of boosting or dampening Bitcoin’s rally in the run-up toward Q4.

ETH Prices

Ethereum (ETH) trades at $4,320.52 currently, having seen a low-key day’s appreciation of +0.52% intraday, in a session range of $4,279 to $4,379. As Ethereum also trails Bitcoin in headline leadership, present market activity reflects a deeper, more strategic rotation of funds into ETH—primarily from institutional investors. Since the beginning of the week, spot Ethereum ETFs have seen $1.4 billion in aggregate inflows in the past week alone, almost doubling flows into Bitcoin-related vehicles, with major contributor units coming from BlackRock’s ETHA and Fidelity’s FETH products. It reflects renewed institutional confidence in Ethereum’s multipurpose use case, including leadership in DeFi, Layer 2 scaling, and tokenization infrastructure. Analysts now point out ETH is quietly taking in the benefit from the broader trend towards asset tokenization and “crypto yield” themes, while taking advantage of the network’s prolonged protocol-level fee burn and upcoming Layer 2 gas compression upgrades.

On the whale activity side, the accumulation trend is steadily positive. During the last seven days, three newly minted wallets acquired a total of $148.8 million in ETH, while a major legacy whale switched $435 million in BTC for around 96,800 ETH in one of the largest cross-asset on-chain reallocations for 2025. Said reallocation looks to originate from increased confidence in ETH’s medium-term bull prospects—particularly ahead of forthcoming network efficiency upgrades. Data from DeFi platforms indicates in the meantime a single party transfers $7.6 million in ETH from Binance directly into decentralized platforms—most likely for staking or yield farming, a positive indicator of HODLing intentions. But not everything is perfectly constructive: data from ETFs indicates while inflows remain robust, Ethereum-related products also notched $787.6 million in outflows across a four-day period, suggesting some tactical rotation or profit-taking in the midst of volatility. Zaye Capital Markets views the present ecosystem then as one in transition—where short-term swings in ETF-driven price are balanced against deep institutional belief, the foundation for a price breakout to the $4,800-$5,000 range in the event macro circumstances remain favorable.