Where Are Markets Today?

U.S. stock futures began trading on Tuesday on a moderately positive note, lifted by advances of AI-associated sectors and expectation of interest-rate eases giving way to date. On the latest session, approximately 0.17% higher were Dow E-minis, whereas S&P 500 E-minis gained 0.38%, and Nasdaq-100 E-minis headed a 0.59% jump. Tech-heavy leading gain better reflectors current appetite for growth tales associated with semiconductor build-outs of infrastructures and artificial intelligence. Regardless of how deep into its second week U.S. government shutdown holds on and how it delays major releases of data, market focus remains on forward policy bias and gauges of liquidity. Traders are perceiving shutdown-caused data blackout as yet one more pretext for dovish course of policy by the Federal Reserve for further tightening, maintaining risk sentiment on overall stable terrain.

Regionally across the Atlantic, stock futures are mixed, a subdued to slightly positive bias being dampened by local threats. Even if some of the indicators are trying a bounce off last week’s sell-off, faith is tenuous amidst politically driven volatility running its course, notably regarding France. France’s premier’s resignation has been a major drag on French stocks and bonds, opening broader spreads and injecting volatility into hopes for interest-rate shifts by the eurozone. Interest traders are also whetting their interest ahead of coming euro-area reads of inflation and shape of yielded curves as possible ignites, notably as a cripplingly divided core moves against flagging growth indicators for its watchful eye, the ECB. Regional futures can’t maintain upside, as political static and structural divergence between members rob holders of risk of faith. The U.S.-Europe divergence mirrors two primary drivers: growth concentration and political cohesion. U.S. equities continue to be cushioned by a centralized group of forward mega-cap leaders of tech and AI infrastructure, affording a cushion against broader macro uncertainty. Europe has no similar growth driver and is more exposed to decentralized policy reactions and fiscal risk. French political strains and generic EU leadership doubts are now market-worthy drivers, having repercussions on equity and bond risk premiums. On such a scenario, U.S. equities are seen better cushioned, short term at least, by their intrinsic exposure to innovation-led sectors and healthier corporate earning, respectively.

In the short term, both sides are sensitive to forthcoming data and central banking sentiment. Investors await President of ECB’s speech later today for a sense of policy direction of the eurozone—especially a change of language about cutting rates or inflation guidance. On the American side, further shutdown-related lagging of data will make market dependent on sentiment and positioning flows, not hard data. Zaye Capital Markets view is short term tactically positive for American risk assets, but weak breadth and external shocks, including tariff tensions, fiscal uncertainty, and geo-spoll over, are one-sided risks both sides of Atlantic.

Major Index Performance Through Tuesday, October 7, 2025

- S&P 500: 6,740.28, up 0.4%

- Nasdaq Composite: 22,941.67, up 0.7%

- Dow Jones Industrial Average: 46,694.97, down 0.1%

- Russell 2000: 2,486.35, up 0.4%

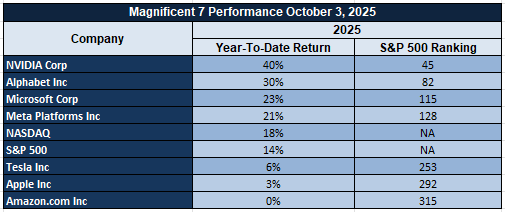

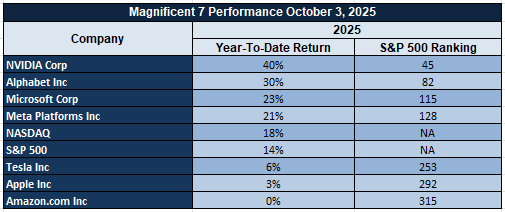

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla–remain at the center of the S&P 500’s direction. As a group, their names endure average drawdowns of over 18% off recent peaks, weighing on both the Nasdaq and the large-cap index. Tesla and Meta are sorely troubled, as excitement about AI and growth thaws. Without fresh life by its largest members, the S&P 500 faces pullbacks and rotation flows into industrials, energy, or consumer staples.

Drivers Behind the Market Move – Tuesday, October 7, 2025

U.S. and European markets are showing mixed to cautiously positive momentum today, shaped by a blend of political headlines, delayed economic visibility, and evolving investor positioning. Below are the key drivers influencing market behavior:

1. U.S. Government Shutdown and Delayed Economic Data

The U.S. government shutdown continues into its second week, creating friction across both domestic and global markets. With key data releases like jobless claims, trade balance, and retail figures delayed, investors are operating without the usual fundamental anchors. This uncertainty has prompted a risk-on tilt in tech and crypto, while more cyclical areas remain range-bound. The White House has placed blame squarely on Democrats, and President Trump has kept the pressure high through repeated commentary—underscoring political gridlock that traders fear could spill into debt ceiling negotiations if prolonged. Markets are now pricing in a higher probability of Fed inaction at the next FOMC meeting due to the lack of fresh labor market data.

2. Trump’s Policy Moves and Infrastructure Momentum

President Trump’s approval of the Ambler Mining Road and announcement of broader infrastructure and mining investment in Alaska has triggered speculation across commodities and energy markets. This is compounded by his declaration that a 25% tariff on medium and heavy-duty trucks will begin November 1—suggesting renewed protectionist stances that could impact inflation, trade flows, and industrial input prices. These developments are influencing capital rotation toward real assets and inflation hedges, including energy, metals, and even digital assets like Bitcoin and Ethereum. His administration is also preparing a farmers’ bailout plan, adding to the perception of significant fiscal stimulus ahead, which could reshape risk appetite and fuel commodity-led rallies.

3. European Political Risk and Market Sensitivity

European markets are holding steady but fragile, following the political shock of the French Prime Minister’s resignation. This development has widened bond spreads in France and added pressure on the euro, dragging on broader sentiment in the region. While European futures are slightly positive, investors remain hesitant as they await further guidance from the European Central Bank. ECB President Christine Lagarde is scheduled to speak later today, and markets will be closely parsing her language for any dovish tilt that could support rate-sensitive sectors and provide relief amid growing uncertainty. Currency moves and yield curves in the eurozone will be especially important in determining whether equity strength can extend further into the week.

In summary, today’s market narrative is driven by three interconnected forces: the extended U.S. shutdown and its ripple effect on data and Fed expectations, aggressive fiscal and industrial policy messaging from Trump, and political instability in Europe that continues to test investor confidence. As we await clarity from the ECB and the resumption of U.S. data, markets are likely to remain headline-driven with an elevated sensitivity to policy tone and geopolitical risk. At Zaye Capital Markets, we’re watching for confirmation signals across rates, commodities, and FX to gauge the next directional move.

Digesting Economic Data

The TRUMP Tweets and Their Implications

President Trump’s new set of policy-motivated announcements is rewriting market narratives across sectors. Chief among them is approval of Alaska’s Ambler Road mining project and administration’s reportedly taking a stake in Trilogy Metals—moves sending a clear message of renewed federal interest in domestic resource production and critical mineral infrastructure. By placing those moves as part of a larger Alaska infrastructure and mining spending surge, Trump is putting policy into tandem with commodity sector renaissance. Industrial metals, building, and energy inputs—industries historically linked to large government spending—are poised to gain. Investors may begin to reallocate portfolios to materials and industrial ETFs, as prospects build for more public-private partnerships and domestic supply incentives.

Trump’s statement of a 25% tariff on medium and heavy-duty trucks from November 1 is yet another market-mover event. It is reminiscent of his prior tariff measures but occurs in a different macro scenario—where inflation threats, supply chains, and cycles of capital spending are themselves squeezed. It might spark cost-push inflation dynamics across logistics and transport sectors, increasing input prices across several sectors. It might also spark trade tensions against foreign trading partners and increased volatility across global equities and FX space. For commodities, it usually bolsters near-term energy demand (as manufacturers build ahead of schedule) but might spawn longer-term frictions, weighing upon economic output. Geopolitically, Trump’s involvement of himself in the Gaza peace process—stating that phase one might be done by the end of the week—indicates a re-establishment of U.S. influence across Middle East policy. It’s paired, however, with a sharp statement about desires to know Ukraine’s intentions regarding its employment of Tomahawk missiles, which implies more oversight and potential realignment of U.S. defense policy. Both, though not yet priced by their respective markets, escalate stakes for defense firms as well as global security policy. Domestic tensions are also kept high: Illinois’ litigation effort aimed at a preemption of National Guard mobilization in Chicago shows mounting resistance to federal activism. Both of these litigious flashpoints bring a dimension of domestic volatility that could affect risk premiums, specifically across bond and municipal marketplaces.

Lastly, political tension regarding the current government shutdown grows by the day. Trump and the White House directly faulted Democrats for the standoff, while concurrent voices in Congress indicated an entrenched split. With releases of economic data frozen by shutdown, market participants are navigating partial darkness, growing dependent on sentiment and positioning cues. Meanwhile, Trump’s statement “stock markets continue to hit record heights” is bravado of more than just talk—it’s a battle cry poised to fuel further retail inflows and headline-speculation, notably on high-beta assets. Here at Zaye Capital Markets, we’re monitoring closely, for the combination of policy volatility and market exuberance generates both tactical opportunity and systemic risk for the foreseeable months ahead.

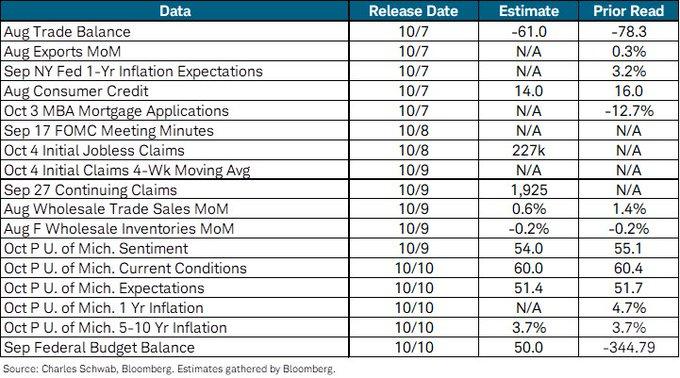

Understanding Jobless Claims Volatility Amid Shutdown Disruptions

Initial jobless claims, a principal weekly indicator of labor market health, are also possible to be held back this week by the current federal government shutdown. Otherwise, this release provides one of the earliest indicators of employment momentum, shaping hopes for wage growth, household consumption, and ultimately policy at the Federal Reserve. The week of October 7–10 was set to bring new information through claims data, trade balance, and consumer sentiment. With the shutdown now past its first week, however, markets are confronted by a short-term information vacuum, potentially accentuating short-term volatility.

Jobless claims releases are often a leading indicator of broader employment trends. A rising trend in claims tends normally to prefigure early labor softness, pushing inflation expectations lower and risking a dovish adjustment of interest rates. As a result, investors are left, short of this release, reliant on higher-lag indicators and labor proxies, amplifying uncertainty. Shutdown-forced data latency in the past hasn’t dramatically alter course of market but did force risk premiums upward before Fed meetings, when reliance on data is highest—as it is now.

For analysts, now is a moment for increased emphasis on high-frequency labor indicators like continuing claims and private employment trackers. From a positioning perspective, we think consumer staples stocks are quietly cheap for our current environment. Their defensive qualities and durable cash flows position them well as market information opacity and policy uncertainty are considered. We are attentive to sentiment gauges and revisions, as a perceived worsening of labor conditions or weakening consumer sentiments might reprice expectations on the way to the next FOMC decision.

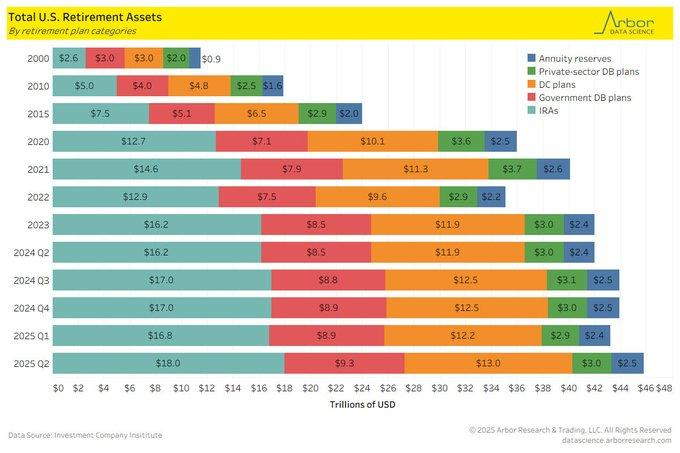

Tracking Retirement Asset Growth and Shifts in Wealth Allocation

U.S. retirement assets totalled nearly $46 trillion in Q2 2025, having risen by a quarter-over-quarter 6%. Driven largely by successful returns on equity markets and stable contributions flows, market-based retirement wealth accumulation solidifies its growing dominance. Remarkably, Individual Retirement Accounts (IRAs) now constitute by far the largest proportion—roughly $18 trillion—over defined contribution programs and government-directed defined benefit programs. The division of assets documents a continuing structural realignment of retirement solutions towards individually administered retirement solutions as a result of shifting labor dynamics and investment trends.

The longer-term picture is even more indicative: aggregate retirement assets have increased by more than a factor of four since 2000, demonstrating the power of gradual savings and market appreciation on a compound basis. IRAs, individually, have gained increased flexibility, inflows from roll-ins, and growing portfolio choices. Relative to other countries, aggregate U.S. retirement assets remain largest and most diverse, having been built on a solid foundation of institutional infrastructure and retail investor involvement. The figures correspond to overall economic optimism in early 2025, as families increasingly position themselves for long-term security even despite macro headwinds.

This bodes two major things to watch for analysts. Firstly, the continued rise of IRA contributions bolsters deeper penetration of passive funds, affirming flows into large-equity benchmarks. Secondly, diversified asset managers—through their direct exposure to asset growth and scale-based revenue models—are undervalued, and we are watching inflows of funds, rollover patterns, and retail trading closely to anticipate the retirement-driven capital allocation next phase across marketplaces.

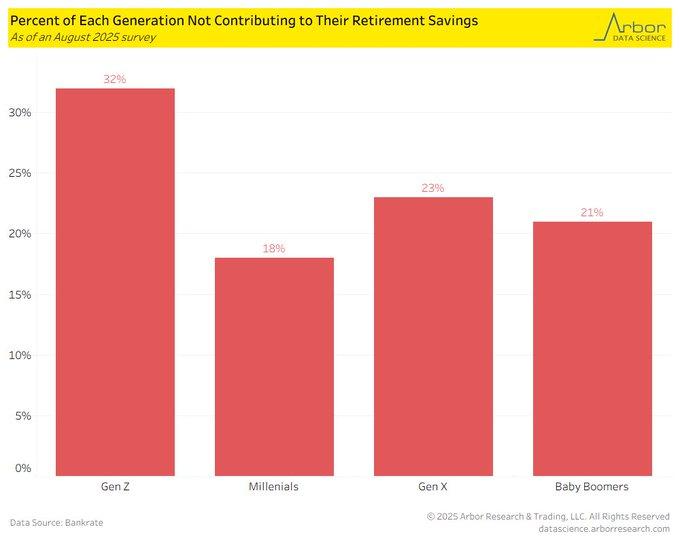

Gen Z’s Retirement Gap and Long-Term Market Impact

More current figures report that 32% of Gen Z workers are currently not planning for retirement, a figure nearly twice the Millennials’ rate. That difference, pertaining to higher living costs and college loan burdens, points to growing intergenerational fiscal divergence. Gen Z, despite its highest-ever percentage of optimism—over a majority expect someday to have enough saved—also shows widespread confusion, a third being uncertain about how much is actually enough. Such a gap between planning and optimism bespeaks systemic pre-adult vulnerabilities of finances and long-term wealth accrual.

Inadequate contributions induce a delay in the compounding necessary for long-horizon growth, potentially constraining aggregate individual asset accumulation and market inflows accruing long-term. In times of recession, young non-participants are hurt exceptionally, increased unemployment among them having consistently coincided historically with weak consumer spending and weak investment participation. As retirement holdings rise at the national level, these participation shortfalls create long-run headwinds to market capital breadth and financial inclusion.

This trend for analysts underscores the relevance of monitoring demographic-based asset flows and labor market participation data. We identify a relative opportunity for financially services firms dedicated to digital advisory platforms and employer-sponsored plan innovations, aimed at closing the Gen Z access gap. Those firms are today undervalued compared to expected growth of digital account openings and education-based engagement metrics. Student debt policy shifts, wage growth dispersion, and Gen Z employment patterns should be tracked by analysts, to predict future contributions behavior and market participation shifts.

Services Inflationary Pressures Continue Despite ISM Prices Sub-Index Rises

The September ISM Services report for 2025 provided a mixed picture for both the U.S. and world economies. Headline services activity flatlined at a PMI of 50, whereas a sub-index, Prices Paid, surged to a high of 69.4—its highest reading since early 2023. The change here shows ongoing inflationary momentum for the services component, a large and important sector of interest closely watched by the Fed. On a historical chart, there’s been a significant—far-from-excellent—correlation between ISM Services Prices Index and core CPI services inflation, for which it’s a leading directional indicator of policy thinking.

Core services inflation, also still high at 5.6% year-year in August, is yet one of the most enduring segments of total price growth. With the creeping rise of input prices for services—typically correlated to wages, insurance, and rent—comes speculation about a timeline for substantive disinflation. Therefore, even during a larger deceleration across manufacturing and goods-connected inflation, this stuck trend may cool hopes for near-term rate reduction, even if service-sector wage pressures hold steady. The route to the Federal Reserve’s target inflation seems all the more dependent on normalization of a single sector.

From a valuation perspective, we pinpoint regional banks and insurers as undervalued during the current rate environment. Their firms are better positioned to benefit from higher short-term rates through net interest margins, and markets might have written in too sharp of an easing cycle too soon. We are monitoring future PCE releases, wage trackers, and real-time procurement cost gauges for better insight into whether the services inflation impulse is topping—or planning a follow-up swell.

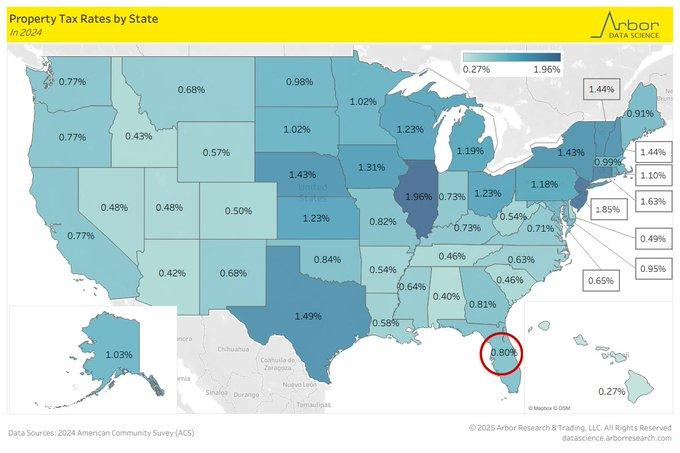

Property Tax Disparities Highlight Migration Shifts and Regional Housing Pressures

Recent 2024 property tax data reveals stark discrepancies between U.S. states, where high effective rates are observed for Illinois (1.96%), New Jersey (1.85%), and Connecticut (1.63%) and low for Hawaii (0.27%), Alabama (0.40%), and Arizona (0.42%). Such figures confirm a larger trend—the high-tax states, also those of the Northeast, continue outward migration as families and businesses require better tax environments for themselves. The allure of Sun Belt states is neither short-term nor purely economical, as lower property taxation is a real cost-of-living advantage for both renters and owners of houses.

These patterns of migration are becoming increasingly apparent in real estate markets and state fiscal planning. States experiencing growing inbound flows—like Texas, Florida, and Arizona—are winning tax base growth, whereas traditional high-tax states are experiencing declining populations and revenue challenges. Yet it’s important to examine property tax rates alongside income and sales tax structures, as it’s often the case that the overall tax burden reveals a more comprehensive picture. States with low property levies, for instance, might compensate with higher consumption taxes or income levies, conditioning tradeoffs for individuals and businesses by affecting decisions about where to relocate.

This is a positive for analysts by way of opportunity for Sun Belt homebuilders and REITs with a focus on high-growth, low-tax areas. They remain largely underappreciated compared to demographic growth and pricing ability, particularly for secondary metros picking up traction. We keep a keen eye on state net migration numbers, inventory of houses, and municipal bond issuance as a lead indicator of changing regional demand, fiscal health, and investor positioning across property-linked asset classes.

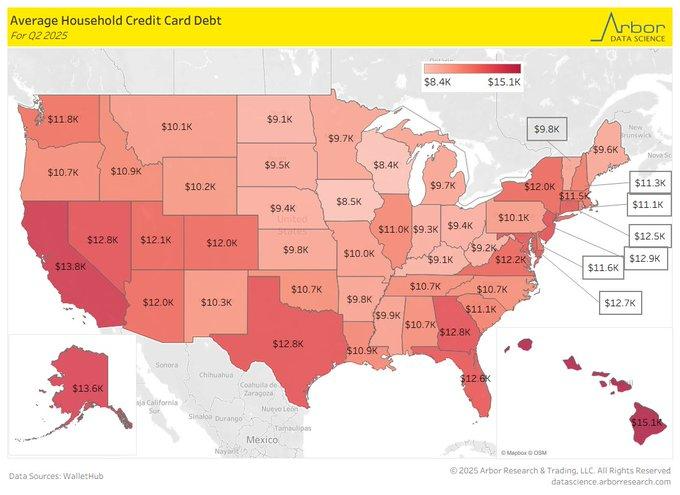

More Credit Card Debt Boosts Regional Stress and Leverage Risks

In Q2 2025, national average household credit card debt reached $10,668, with states such as Hawaii ($15,000), California ($13,800), and Alaska ($13,600) notably higher. Such numbers reflect more than spending patterns—they highlight the income pressures stemming from inherently high cost of living structures. In Hawaii, real estate prices are more than 150% higher than the U.S. median, and Alaska’s import-based economy pumps up basic prices. Even with paychecks in these states 20–30% higher than nationally, many families are relying more on credit to sustain mediocre consumption patterns.

Domestically, U.S. credit card debt reached a record $1.32 trillion during Q2 of 2025, increasing by 5% year-over-year. This is the fifth successive year-upon-year rise and underscores a larger theme of sustained consumer leverage despite nascent signs of ease in inflation. As opposed to previously seen debt cycles based on discretionary spending, current balances are linked more to necessities—utilities, shelter, and food—due to questions about long-term capacity to repay. With interest rates continuing to be high and delinquency rates increasing, consumer credit stress is becoming a key macro risk, particularly for jurisdictions exposed to excessive degrees of variable-rate commitments.

This creates an opportunity for analysts for non-bank financials by way of their conservative underwriting approach and stable interest income—a space we also view as underappreciated compared to peers who are exposed to riskier segments of lending. We are studying household savings rates, trend of credit utilization, and state income-to-debt ratios better to evaluate where spending strength is likely to give way first. Such parameters will better identify pressure points for retail, residential, and consumer credit-sensitive segments for quarters ahead.

Upcoming Economic Events

ECB President Lagarde Speaking

With global financial markets confronting enduring inflation as well as diverging growth indicators, market spotlight of the week is a possible statement by ECB President Christine Lagarde. As monetary policy becomes a more data-dependent regime and geopolitical tensions are a lingering risk, investor sentiment should remain reliant on policymakers’ tone and direction. Here’s what’s ahead—and how markets are likely to act based on what’s being said:

ECB President Lagarde Speech

Lagarde addresses markets at a moment of heightened uncertainty. While headline inflation in the Eurozone has shown signs of easing, underlying wage growth and services-sector pricing remain uncomfortably firm.

- Should Lagarde adopt a hawkish tone—emphasizing persistent inflationary risks or reiterating a higher-for-longer stance—the euro may strengthen, core European bond yields could rise, and sectors like real estate and utilities may come under renewed pressure. Broader risk assets might also pause or retrace, as investors reprice the probability of extended monetary restraint.

- Nonetheless, a dovish bias—potentially a nod to slowing growth, weak PMIs, or weakening consumer demand—should benefit equities, thin peripheral bond spreads, and depress the euro. A mention of downside risks to inflation prospects by Lagarde or policy flexibility signs should bring about a reversal in cyclical sectors and increased conviction about a soft landing. Investor positioning of both emerging-market debt and cross FX of the euro should also be affected by her tone.

Stock Market Performance

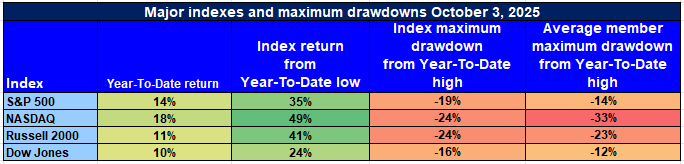

Indexes Rebound from April Low, but Drawbacks Reinforce Markets Vulnerability Again

Major U.S. equity indicators have recovered well off their April 8 lows, boosted by improved macro data and flows on momentum conviction. Headline numbers, however, continue to mask significant intra-index variation. Member average drawdowns remain deep, reflecting weak breadth and generalized stress lurking beneath the surface. Index-level rebounds are not yet mirroring investor confidence on a broad base.

This rundown of current performance for major indexes is below:

S&P 500 Index Resistance, Member Vulnerability Continue

YTD: +14% | +35% below April low | –19% below YTD high | Ave. member: –14% (from low), –26% (from high)

The S&P 500 shows healthy index-level strength, having gained 14% YTD and 35% from its April low. Member-level data, however, is a more cautious picture: the typical constituent remains down by 14% relative to its April low and by 26% compared to its YTD high—a sign of thin leadership and selective participation.

NASDAQ: Growth-Led Surge with Deeper Cracks Below

YTD: +18% | +49% lower than April low | -24% lower than YTD high | Average member: -33% (from low), -48% (from high)

NASDAQ activity has been market-centred, having recovered by a staggering 49% since April and yielding 18% YTD returns. However, the average constituent is down by 33% from its April low and by 48% compared to its high, reflecting extreme clustering of a few mega-cap names and vulnerability lurking beneath the surface.

Russell 2000: Small-Cap Rebound, but Hurt Runs Deep

YTD: +11% | +41% below April low | -24% below YTD high | Ave. member: -23% (from low), -38% (from high) The Russell 2000 is a harbinger of increased interest in small caps, having surged by 41% off its April low and being higher by 11% YTD. Average-member losses of 23% off the low and 38% off its high, however, reflect ongoing pressures on liquidity-sensitive holdings and more general doubts about early-cycle holdings.

Dow Jones: Modest Gains, Modest Damage

YTD: +10% | +24% below April low | -16% below YTD high | Ave. member: -12% (off low), -23% (off high) The Dow Jones still provides a more stable route, having risen 10% this year and 24% since April. Boasting its shallowest average drawdowns among its peers, its defensive and value-dominant profile has protected members to some extent, though potential for a slip downwards is still seen.

We at Zaye Capital Markets continue to focus on underlying market breadth, rather than index-level strength. With average member drawdowns still large across the board, we continue to prefer high-quality firms with durable earnings power, strong free cash flows, and defensible sector positioning as this market rally progresses.

The Strongest Sector in All These Indices

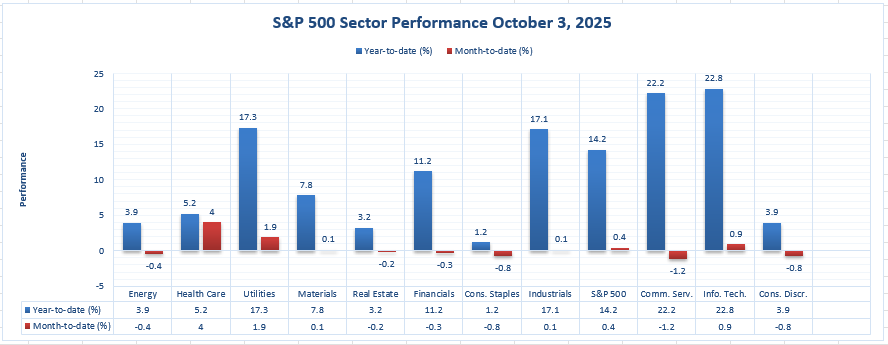

Tech and Communication Services Lead YTD Industry Leadership

Through Oct 3, 2025, sector-level activity for the S&P 500 shows a distinct pattern of leadership—Information Technology and Communication Services have been ahead of all other sectors year-to-date, which suggests investor interest in growth names and innovative names even during a macroenvironment of selectivity and resiliency.

Information Technology

YTD: +22.8% | MTD: +0.9%

With a commanding 22.8% year-to-date gain, Information Technology leads all sectors by a significant distance. Moderating positive returns for October for the month also reflect steady inflows despite macro headwinds. That kind of strength is a byproduct of a combination of resiliency in earnings, strong free cash flows, and investor convictions regarding secular themes like AI, cybersecurity, and cloud infrastructure.

Communication Services YTD: +22.2% | MTD: -1.2%

Close behind is Communication Services, up by 22.2% YTD. Despite month-to-date performance easing a bit (-1.2%), broader-strength has been powered by megacap media, internet ads, and streaming giants regaining profitability and operating leverage. This month’s sector decline may give selective points for re-entry, especially for longer-term positioning.

We at Zaye Capital Markets keep a close eye on rotation signals by sectors but for the moment, communication and technology sectors remain the structurally most favored for capital allocation, rerating of valuation, as well as thematic growth prospects. Active positioning here stays central, particularly as market leadership narrows further.

Earnings

Yesterday’s Earnings (06-Oct-2025)

- Constellation Brands, Inc. (STZ)

The company reported Q2 fiscal results with net sales down ~15% to $2.48 billion—just ahead of estimates—and delivered adjusted EPS of $3.63, beating forecasts of $3.38. Key drivers included relative resilience in its beer segment, though shipment declines and weaker volumes pressured margins. Management reaffirmed full-year guidance of organic sales down 4–6% and EPS between $11.30–$11.60. What to watch: margin trends (especially raw material and aluminum costs), volume recoveries in key markets, and consistency with its forward guidance amid macro pressures.

- Aehr Test Systems / LifeCore Biomedical, Inc.

We did not locate any verifiable public earnings reports on these firms dated 06 October 2025. It is possible they did not report or the reports were not captured in major financial media sources.

Today’s Earnings (07-Oct-2025)

- McCormick & Company, Inc. (MKC)

McCormick is scheduled to report Q3 2025 results. The consensus EPS estimate is ~$0.81, representing a slight year-over-year decline, while revenues are expected near $1.71 billion. Analysts will scrutinize margin pressure from ingredient costs, regional performance (especially EMEA), and guidance for FY 2026 continuation. What to watch: New volume growth or contraction in emerging markets, cost pass-through capability, and management tone on future pricing and supply chains.

Stock Market Overview – Tuesday, October 7, 2025

U.S. equity markets opened with a cautious tone, reflecting investor nervousness over macro uncertainty and headline concentration risk. The S&P 500 and Nasdaq are starting the session under pressure, led lower by fatigue in mega-cap tech names, while the Dow Jones and Russell 2000 are showing relative steadiness as flows rotate into defensive and industrial areas.

Stock Prices

Economic Indicators and Global Developments

Sentiment during the day is being influenced by the current federal government shutdown, increasing worries about delayed economic information and policy uncertainty. Meanwhile, speculative interest ahead of chipmakers was spurred by a large AI‑infrastructure deal announced yesterday, but fears of overvaluation of the space also increased. International sentiment is being influenced by weak PMI reports emanating from Europe and renewed geopolitical tensions across multiple regions, pushing investors cautiously.

Latest Stock News

- $OSCR | Oscar Health rose by 11% following President Trump’s statement under which a bipartisan ACA subsidy deal is “in reach,” a relief for health insurers exposed to exchange market.

- $APP | AppLovin is investigated by SEC on data-collecting policies, putting stock under strain and fueling broader worries about ad-tech business models and risk of non-compliance.

- $OPEN | Opendoor Technologies rose by 15% after announcing it is going to accept Bitcoins ($BTC), Ethereum ($ETH), and other virtual currencies for real estate payments, increasing its speculative potential and investor interest.

- $AMD / $NVDA | OpenAI’s aggressive build-out of infrastructure is continuing to reshape market sentiment. Sam Altman’s aggressive securing of $100B of NVIDIA GPUs, a 10% stake agreement for AMD, and the $500B Stargate build-out of compute is causing renewed debate about OpenAI’s valuation trajectory—potentially laying the groundwork for a $1 trillion footprint within the AI landscape.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla–remain at the center of the S&P 500’s direction. As a group, their names endure average drawdowns of over 18% off recent peaks, weighing on both the Nasdaq and the large-cap index. Tesla and Meta are sorely troubled, as excitement about AI and growth thaws. Without fresh life by its largest members, the S&P 500 faces pullbacks and rotation flows into industrials, energy, or consumer staples.

- Major Index Performance Through Tuesday, October 7, 2025

- S&P 500: 6,740.28, up 0.4%

- Nasdaq Composite: 22,941.67, up 0.7%

- Dow Jones Industrial Average: 46,694.97, down 0.1%

- Russell 2000: 2,486.35, up 0.4%

In Zaye Capital Markets, our perception of the current environment remains “selective caution.” The mega-cap tech dominance is being reaffirmed, but universal participation is yet to happen. We remain biased towards quality, strong balance sheets, and sectors with buoyant fundamentals as better places for positioning for this phase.

Gold Price

Gold is trading around $3,960 per ounce, remaining just below record highs as market sentiment remains tilted towards safe-haven assets. This move is a reflection of increasing investor demand for predictability amidst rising geopolitical and economic uncertainty. A key driver is President Trump’s comprehensive set of policy initiatives, including a 25% tariff on medium and heavy-duty trucks from November 1, coupled with a strong policy shift towards infrastructure and mining development—marked by giving a green flag to Alaska’s Ambler Mining Road and his administration’s interest in Trilogy Metals. Such moves are fueling inflationary expectations, also as industrial metals and raw material supply chains are a focus point again. Additionally, the U.S. government shutdown, now blamed by the White House for being a result of congressional gridlock, remains a dampener for key releases of economic data, none of which are easy to replace for investors relying on it for positioning cues. Here, gold becomes increasingly appealing as a hedge against policy uncertainty, noise around fiscal stimulus, and risk of data misinterpretation. Even central banking moves are under a spotlight, here awaited is ECB President Lagarde’s speech, which may dictate the course of the euro and cross-market rate flows. If Lagarde adopts a dovish pitch or stresses Eurozone growth risk, it might further enhance gold’s appeal through stress on global yields and cross-base currency rescalings. To the bullish case for gold, we add broader macro context fueled by recent data disruptions and ongoing political uncertainty. Shutdown-delayed jobless claims and trade figures give investors no new information about labor strength nor about inflationary trends, assuring additional flows of capital into storehouses of value that don’t pay a yielding income. The policy-led regime has converted gold’s role from passive hedge to a strategic allocation—particularly as Trump’s rhetoric portends a broader populism of interventionism in economies. With speculation about huge infrastructure spending, a forthcoming farmer bailout plan, and rising tensions internationally—especially about Gaza and Ukraine—gold’s attraction moves beyond a narrative of inflating hedge to one of risk insurance for global events. Meanwhile, OpenAI’s growing presence in a hardware arms race for AI is fueling speculative flows both into tech and into commodities, but investors are increasingly hedging both exposures against hard currencies like gold. Unless central banks shock investors with aggressive rate communication, geo-political risk subsides substantially, we at Zaye Capital Markets continue to see upward potential for prices for gold, eyeing $4,000+ as long as market dislocation and policy ambiguity continue to prevail.

Oil Prices

Oil prices are trading at about $61.69 per barrel for WTI and $65.48 for Brent, showing signs of stabilization following a tumultuous few weeks fueled by mixed supply and demand dynamics. The recent OPEC+ move to raise output modestly by only 137,000 barrels per day for November arrived below more hawkish predictions, placing a soft floor beneath prices, yet exuberance on the market remains muted by fears of weakening global demand, especially as inventory data starts to capture build-ups during the season and macroeconomic indicators point towards industrial activity deceleration. The International Energy Agency (IEA) has been maintaining a cautious tone, reflecting slower growth of demand by China and stricter credit market tightening by advanced economies. Meanwhile, markets are yet to absorb the shock of softer-than-expected economic releases emanating from Europe and Asia, and even as a lingering U.S. government shutdown stays for longer, delaying critical economic indicators, curtailing near-time insight into real-time domestic consumption trends. A dearth of new data is causing traders to turn more defensive, particularly as possible supply shocks remain in the picture amidst sustained geopolitical tensions and delicate shipping routes. Overlaying this macro context is a surge of headline volatility by the Trump administration, which is becoming an increasingly significant crude sentiment input. President Trump’s approval of the Ambler Road mining development and broader Alaska infrastructure initiative point to longer-term positive demand for fossil fuel-based building inputs, but his statement of a 25% tariff on medium and heavy-duty trucks complicates things. On one hand, tariffs of this type point to stepped-up domestic production and transport demand—potentially lifting fuel demand; on the other, they are likely to dampen global growth through trade retaliation pressure. Meanwhile, today’s statements by ECB President Christine Lagarde are also being watched by the market. If dovish-leaning, hopes for a weakly softer-dovish turn by the euro and looser-money conditions may rise, potentially weakening the dollar and lifting oil prices by extension. Still, given risk asset nervousness, genuine momentum by crude market forces may depend on a better sense of when U.S. macro numbers resume and whether demand-side indicators surprise to the upside by a meaningful amount. We at Zaye Capital Markets remain cautiously neutral, looking for oil to trade narrowly near-term, where directional bias depends on policy tone, data normalization, and geopolitical adjustment.

Bitcoin prices

Bitcoin is trading just above $125,000 now, having entered new all-time high territory during the week, flirting with $125,600 for a moment. That swift upside is being fueled by a combination of macro and sentiment-based drivers. The current U.S. government shutdown dramatically diminished market visibility, delaying key economic releases like jobless claims and trade figures, which, in turn, is inducing investors to hedge policy risk via decentralized stores of value like bitcoin. Bitcoin, aided by healthy ETF inflows and institutional acceptance, is now being perceived as a tactical risk-safe haven alternative, notably as traditional risk assets flirt with risk of their own amidst headline risk. Its function, having evolved from a speculative tool, is now a macro-reactive store of value, notably as fiat credibility weakens and central bank guidance becomes increasingly difficult to factor into prices. As potency builds across geopolitical and domestic noise—from stuck fiscal negotiations to labor market uncertainty—the surge of safe-haven demand that’s building amidst it is fueling capital flight into crypto even as traditional equities volatility stays elevated. Trump’s latest remarks are also fueling Bitcoin’s rise. His aggressive spending push—emphasized by greenlighting Alaska’s Ambler Mining Road and investing in Trilogy Metals—coupled with a potential 25% tariff on medium and heavy-duty trucks by November 1, are indicative of growing inflationary and fiscal impulses. Such policies portend increased deficit spending and supply-side shortages, both of which fortify the inflation hedge thesis around Bitcoin. Meanwhile, Trump’s mounting rhetoric across global and domestic flashpoints—from Ukraine and Gaza to National Guard patrols of Chicago streets—only enhances the sense of political and economic instability. It’s all funneled capital into decentralized, uncorrelated alternatives. Traders are now looking to ECB President Lagarde’s remarks for dovish reveals potentially weakening the euro and boosting BTC’s credentials vis-à-vis fiat further. Here at Zaye Capital Markets, we see Bitcoin’s breakout of late not merely as a technical breakout, but a structural realignment of capital flows into a world where faith in sovereign data, central bank timing, and political coordination is falling apart far faster than anyone’s yet acknowledging.

ETH prices

Ethereum is trading between $4,200 and $4,500, retaining around multi-month highs amidst a pickup in institutional interest and ongoing on-chain whale demand. During the last seven days, Ethereum-centered spot ETFs have seen inflows of $1.3 billion, reversing a prior trend of redemptions and indicating renewed demand from asset managers and institutional allocators. This rotation back into ETH is arguably linked to increasing enthusiasm about Ethereum’s long-term position in smart contract infrastructure, real-world asset tokenization, and decentralized finance (DeFi) applications. On-chain analysis affirms the positive tone—whale data reveals whales have been net accumulative for around 800,000 ETH during recent days, implying large funds and high-net-worth individuals are positioning for a further run higher. This whale accumulation tends to serve as a prices backstop, diminishing exchange available supply and supporting the positive thesis. Moreover, Ethereum’s position of prominence in a developing ETF space—particularly if approval momentum perseveres—renders it a leading beneficiary of a rotation towards digital asset diversification among regulated products for investment. From a macro and policy perspective, Ethereum also benefits from larger capital allocation shifts spurred by fiscal and political uncertainty. President Trump’s aggressive infrastructure initiative—illustrated by his Alaska Ambler Mining Road advocacy and resource-themed investment themes—bolsters inflationary tailwinds and commodity-linked growth stories, which tend to spill into crypto markets. The current U.S. government shutdown, delaying key economic indicators, adds a further veil of ambiguity to traditional financial markets, leading investors to expand exposure to decentralized holdings operating independent of national institutions. Meanwhile, today’s expected commentary by ECB President Lagarde may alter global liquidity expectations. A dovish message by Europe’s central authority may soften the euro and lift crypto sentiment as capital seeks to find yield and security. Zaye Capital Markets considers Ethereum’s near-term fortitude as backed by both structural accumulation and macro regime change, continuing flows by ETF and whale behavior remaining key indicators of sustainable upside stress on a weekly basis ahead.