Where Are Markets Today?

U.S. and European stock futures decline as markets enter the week struggling to keep pace with an influx of new economic and political uncertainty. As of early Monday, S&P 500 futures are down 0.4%, Nasdaq 100 futures are down 0.5%, and Dow Jones futures are down 183 points. European futures are down as well, as are STOXX 50 and DAX contracts, falling in the range of 0.6–0.7%. The root weakness is coming largely in reaction to President Trump’s Saturday announcement that the U.S. would impose 30% tariffs on European Union and Mexican imports, effective August 1. With no economic releases on today’s agenda, sentiment is being set nigh on entirely on political news and threatened tariffs.

One of the most compelling explanations for the sell-off is the intensification of US protectionist trade policy, which revived global supply chain jitters. Trump’s recent remarks not just reiterate the imposition of tariffs but also escalate the rhetoric, calling boycotts on consumers of European cars as well as chastising Democrats for aligning with foreigners. The European Commission responded to the threat and announced that negotiations would be resumed until July. But investors are factoring in greater cost of doing business, potential retaliation in trade, and an unfavorable earnings season for multinational companies—specifically, industrial and automobile ones.

Another cause for concern is the lead-in to significant U.S. inflation releases. Later in the week, scheduled CPI and PPI releases will inform us whether prior rounds of tariffs have become price pressures. The risk today is twofold: inflation prints hot, and the Federal Reserve would be compelled to maintain or even solidify policy in the face of political tumult, but in doing so, in-earnings corporate margins in synchronized harmony will be squeezed on both higher input costs as well as stagnant consumer demand. The macro-policy squeeze is both spooking U.S. as well as European markets on a tenuous tightrope.

As second-quarter earnings season begins, investors are not so sure about pricing in positive upside. European futures are more active since they are directly attributed U.S. tariffs, while U.S. indexes seem to be waiting in anticipation of earnings relief or mitigation in CPI. Futures markets, on the other hand, will continue to be pressured until such a time, since tariff risk is serving as a limit to risk appetite. At Zaye Capital Markets, we continue to anticipate near-term volatility to remain high as investors wait in anticipation of additional details on inflation dynamics, continuity of corporate earnings, and whether de-escalation is possible for the latest bout of trade talks.

Major Index Performance – Monday, July 14, 2025

- S&P 500 (through SPY ETF): 623.62, slightly lower due to tariff fears

- Nasdaq (through QQQ ETF): 554.20, gentle correction in line with tech

- Dow Jones Industrial Average: Down moderately–reflecting futures pressure

- Russell 2000: Underperforming, in line with widespread weakness in small-cap stocks.

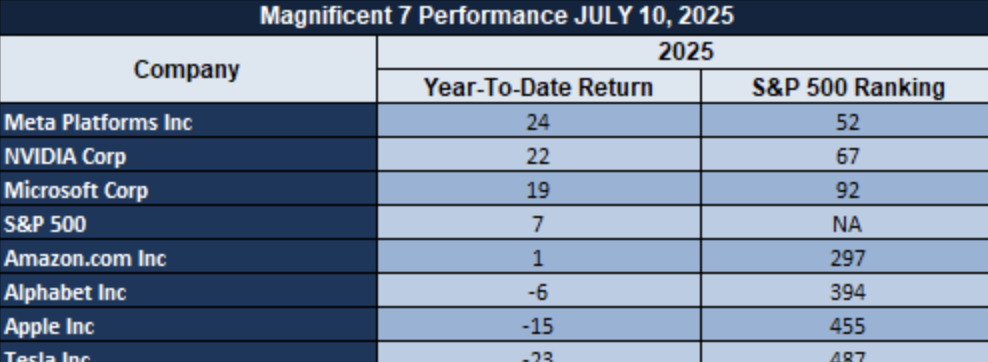

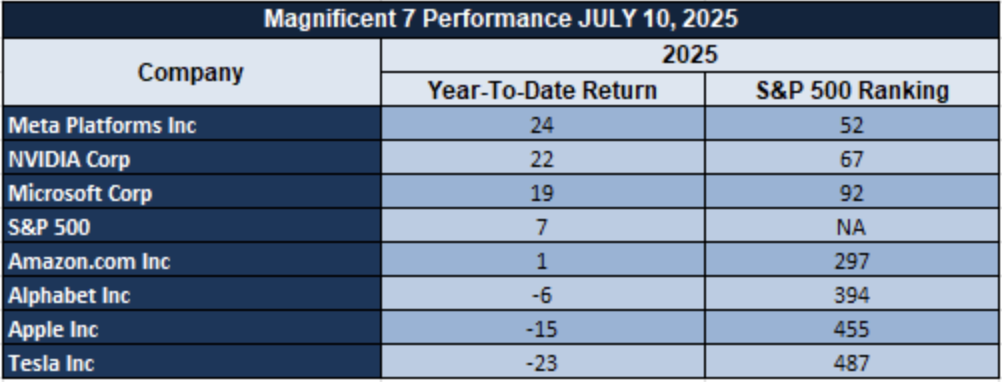

The Magnificent Seven and S&P 500 Leadership

Core mega-caps—the so-called “Magnificent Seven” (Alphabet, Amazon, Apple, Broadcom, Meta, Microsoft, NVIDIA)—remains the anchor supporting strength in the S&P 500. Market breadth is, nevertheless, poor on a broader front as the gains are relatively narrowly confined in such mega-cap stocks. The gap between such headline index levels and intrinsic problems in participation is a cause for concern: such stocks can suffer sharp corrections in case sentiment changes.

Drivers Behind the Market Move

Zaye Capital Markets pointed out three main U.S. and European market drivers for today as:

- Escalating Tariff Tensions

President Trump’s threat to place 30% tariffs on EU and Mexican import products, as well as prior threats on Canadian and Brazilian import products, increased political and trade tension. Although European leaders indicated a willingness to negotiate in July, markets are acting defensively, most notably in areas most susceptible to trade, such as industrials, automobiles, and materials. Fears about retaliatory moves and ongoing supply chain disruption are building hedging demand in both U.S. and European futures.

- Upcoming Inflation Readings

Market players are preparing for major U.S. inflation prints next week, with releases of the Consumer Price Index (CPI) and Producer Price Index (PPI) on Tuesday. Since pass-throughs to input prices will take place for tariffs, investors will worry about inflation printing higher than anticipated. The inflation print can cause renewed fear on a policy shift to a higher, more hawkish rate for the Fed and will put upward pressure on yields, weighing down valuations in growth-sensitive stocks.

- Q2 Income in Focus

The second-quarter reporting season begins this week, with the large banks and the technology sector moving first. Already, hopes have been lowered, from a rate of perhaps 10% to below 6%, so the burden of proof falls on companies to beat expectations. Failures would unleash fresh volatility on an already fragile market under siege from geopolitical risks and macroeconomic headwinds.

Global equities are beginning the week on the wrong foot in general. Since tariffs, inflation risk, and defensive earnings sentiment have been the subject, investors continue to keep their guard up. Here at Zaye Capital Markets, we are keeping our eye open for indicators in inflation numbers and earnings guidance which can switch this risk-off mindset.

DIGESTING ECONOMIC DATA

The TRUMP Tweets and its Implications

At Zaye Capital Markets, we are following closely market-wide responses to ex-President Trump’s latest barrage of comments, which again generated political and economic commentary. Trump released a barrage of high-impact comments over the weekend ranging from aggressive trade policy commentary to inflammatory personal attacks extending even to risk sentiment across all asset classes. Most significantly, he reaffirmed 30% EU and Mexican import tariffs from August 1, fueling global trade backlash sentiments and affirming protectionist policy shift. The markets followed their cue cautiously, and risk-off flows to defense markets, gold, and cryptocurrencies like Bitcoin are viewed as indicators of hedging.

Aside from the tariffs, Trump’s rhetoric also grew sharpened. Acts such as allowing ICE officials to “use all force necessary,” an implied cabinet reshuffle prior to August, and referring to Rosie O’Donnell as “a threat to humanity” injects further unpredictability in an already volatile concoction. Trump’s rhetoric against Democrats for “bucking foreign governments” and car-boo threats against European vehicles injects polarisation in consumer and trading realms—the latter possibly derailing automobile equities, cross-border supply chains, and retail sentiment. Investors must factor in tariffs, not retaliations, and consumer upco reactions to politicized brand stories.

Meanwhile, his visit to flood-affected Kerrville, Texas, emphasized both his praising of FEMA as well as fierce confrontations with the media, consistent with a leadership that oscillates between populist reassurance as well as institutional confrontation. The remarks can be important for sectors like insurance, utilities, as well as infrastructure, where risk pricing is based on the credibility for government response. His public annoyance at central banking leadership—the less defined nature of which dominated in the week ahead—the shadow also falls on upcoming monetary policy expectations.

Usually, Trump’s rhetoric is introducing political risk premium in the markets. Threats on the tariffs spill over to industirials, autos, and commodities; enforcement comments on immigration-related industries offer commentary on sentiment in the US; and social volatility introduces noise in regular economic indicators. At Zaye Capital Markets, we anticipate asset correlations to change as rhetoric-driven geopolitics takes center stage over policymaking driven by data–warranting a tactically favored flight in policy-strong areas and safe-havens in the weeks ahead.

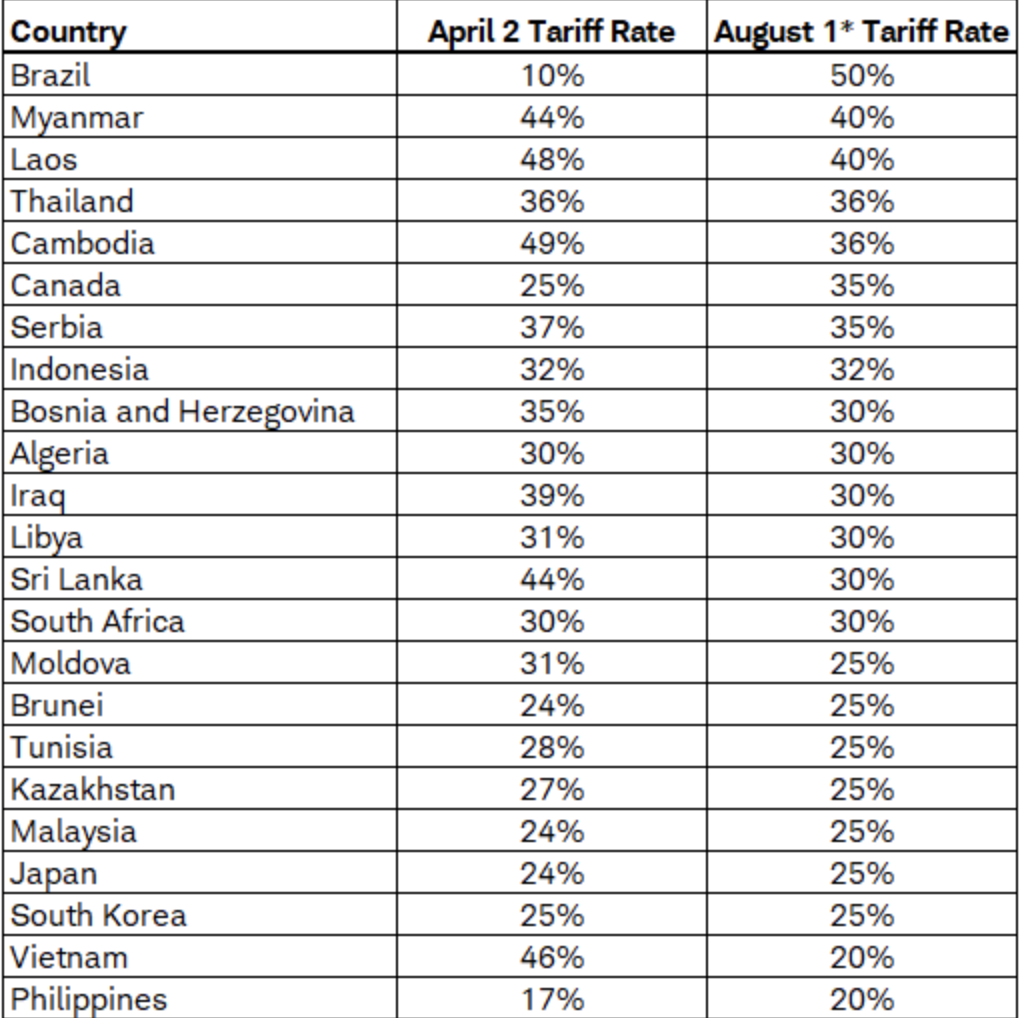

Tariff Increase And Global Trade Risk

We at Zaye Capital Markets are tracking the sudden surge in U.S. tariff rates with several trading partners—most significantly Brazil and Myanmar, where the tariffs have been increased from 10% to 50% during April-August 2025. This is a sudden U-turn towards protectionism in the midst of escalating trade tensions. This 90-day tariff holiday in the first half of the year appears to have been a temporary measure, and the U.S. is now reverting to aggressive trade protection once again. This sudden policy shift envisions repeating the trends of the past witnessed during past tariff wars, with the surge in the number of tariffs triggering retaliatory actions at the global level and impairing trade flows.

The economic expense already stings. Mid-point American tariffs are now over 30% and most supply chains, especially in technology, autos, and machinery, already have inflationary costs. Not merely are the margins narrowed, it discourages offshoring production or reducing output. America, for example, reported a $7.4 billion trade surplus with Brazil in 2024; that balance is being tested now that Brazilian partners strike back. Spillover is likely to extend outward beyond two-way trade, perhaps to world price behavior and investor demand in export-centric business.

Subject to tensions, Intel Corporation (INTC) is undervalued in the existing environment. Despite short volatility, its home-country biased manufacturing capability and recent investment in chip foundries with bases in North America provide insulation from world frictions. Inventory rebuilds and trade balance reversals are owed special consideration from analysts—the former key to deciding if companies front-loaded shipments before tariff dates, and the latter deciding if companies introduce permanent adjustments to the paradigm of sourcing.

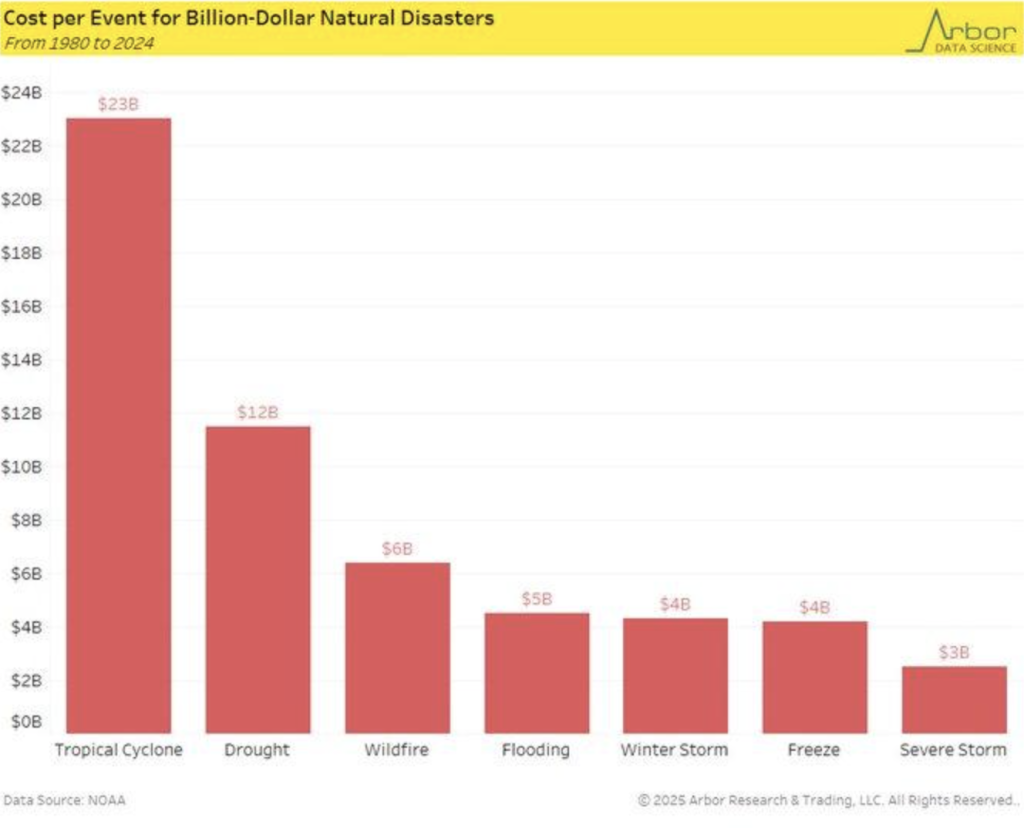

Escalating Cyclone Costs And Regional Risk Reassessment

We at Zaye Capital Markets pay particular attention to the growing economic loss from tropical cyclones, the most financially damaging natural disasters within the U.S. By long-term historical measurements, the events have averaged $23 billion an event from 1980 to 2024 and become the leading cause surpassing droughts and wildfires. Increased intensity, due to larger-scale shifts in the climate, is reconstructing the way investors and underwriters assess risk, particular, as the frequency and severity rise.

Not surprisingly, regions historically designated as low-risk—most notably the Northeast—now face greater exposure. FEMA’s National Risk Index uncovers underlying vulnerabilities, discrediting long-held assumptions that must be reassessed. Hurricane Sandy’s $70 billion cost and the 2017 trio’s $339.2 loss—Harvey, Irma, and Maria—are representative of the systemic damage such storms inflict on infrastructure, insurance, and demand at the consumer level. These disruptions have far-reaching consequences across the home-construction, energy, and regional banking industries, which may not have the balance sheet resiliency to absorb building losses.

Our view is that NextEra Energy (NEE) is underappreciated currently in this environmentally conscience world. By way of its expanding renewable investing portfolio and proactive approach of grid resiliency, the company is poised to gain from infrastructure adjustment plays. Capital investment trends to protection from disasters and energy infrastructure building, primarily in historically under-invested areas, will drive future earnings predictability and investment attractiveness.

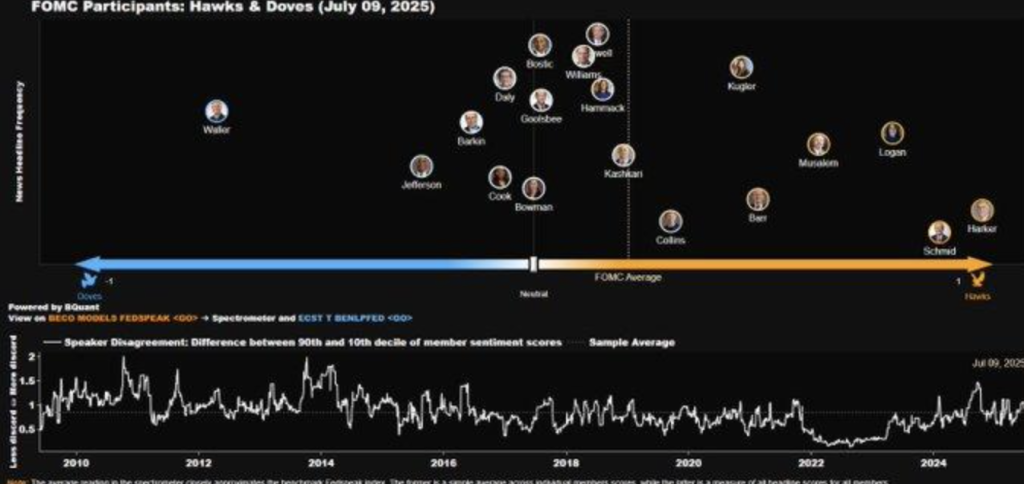

Fomc Divide Signals Policy Uncertainty

We at Zaye Capital Markets are tracking the newly emerging internal disagreement at the Federal Open Market Committee (FOMC) keenly, as can be seen from the latest sentiment models. The figures out in June 2025 show a strong dovish-hawkish difference among FOMC members, a reflection of the economy-wide indecision. The difference is strong, with the earlier dispersion of opinion having been a portent of policy direction reversals. With the tighteners emphasizing the importance of inflation management and the doves cautioning about stopping weak growth, the interest rate outlook is now more uncertain than it has ever been.

It is in accord with rising macroeconomic uncertainty. Asymmetrical growth signals and trade tensions are triggering uncertainty, which is testing the Fed’s mandate. History is that such polarisation can be deterring doing something, especially if public policy is opposite to market stress. Fragmentation now is in accord with previous monetary indecision episodes, which have typically taken the form of unstable market expectations and short-rate volatility. Investors need to be prepared for possible dislocations in risk assets and shape of the yield curve as the committee tries to get around this internal standoff.

Against this backdrop, JPMorgan Chase & Co. (JPM) is seen as undervalued. Due to its healthy balance sheet and diversification of revenue sources, it will benefit from heightened volatility in rate spreads and still enjoy credit discipline. Investors need to remain responsive to future FOMC minutes and take special notice of any change of language that might indicate movement towards the mainstream or heightened polarization, as it will be invaluable in terms of impacting interest rate futures and the profitability of banks.

Continuing Welfare Claims And Work

At Zaye Capital Markets, we notice the most recent numbers reporting 5.87% year-earlier growth in ongoing claims in July 2025. Seeing payroll growth news that is good—i.e., the 147,000 increase in June—continuing higher claims is a warning sign that something more complex is brewing in the employment situation. The labor market is heading toward the “low-hire, low-fire” stage, with firms neither hiring aggressively off the payroll nor cutting it, maybe looking ahead to future demand and frugal costs instead of getting euphoric about economic growth momentum pickup.

This resiliency masks underlying vulnerabilities. Structural rigidity—i.e., freezes on hiring and falling worker mobility—suggests that employers, hard hit in the recruitment crises of recent years, are opting to hold on to their labour rather than run the risk of being tight in the future. But this sort of rigidity could turn into a vulnerability. If growth in top-line revenues slows, companies could be left with cashflow deficits with inflated cost bases established. This apparent labour market resiliency could be flawed and uncover the downside risk in regions based on discretionary consumption and skimpy margins.

Here, Automatic Data Processing (ADP) is considered to be inexpensive. By its long history of inclusion in employment patterns and business labor pool systems, Automatic Data Processing offers immediate exposure to employment activity and payrolls. Its ability to forecast and diversification of clientele is a healthy hedge in the downturn portion of the labor cycle. We need to be tracking the shifts to the productivity information and forward-looking employment surveys, which will prove invaluable to determine if the present stability will be maintained or is in fact hiding rising labor market tensions.

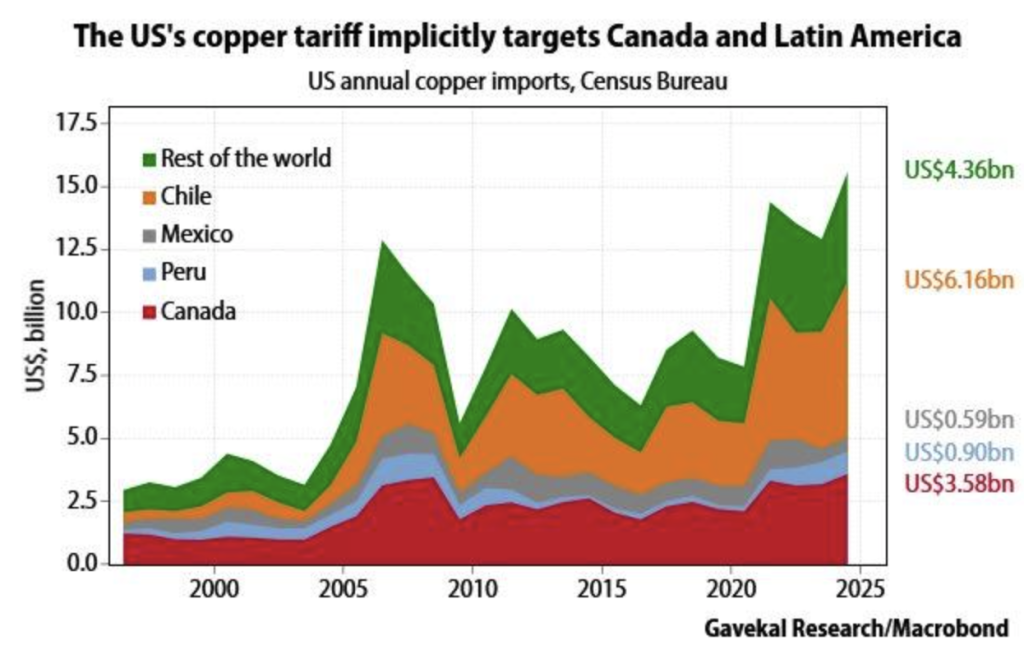

Copper Tariffs And Industrial Supply Pressure

We are monitoring the economic risk being imposed as a result of the rise of the U.S. import tariff on copper, with the 50% tariff set to be imposed in August 2025. Imports already did triple from 2000 to the current year, to over $15 billion, 75% of the supply coming from Mexico, Peru, Canada, and Chile. The looming future new tariff will heavily tax trade streams under the USMCA, with special pains being imposed as a result of Mexico and Canada already having absorbed the 25% hit. At the center of the disruption is Chile—providing 64% of refined copper—and price volatility is bound to increase.

It is being sold as a step to increase domestic mining output, but history has something else lined up. Metal protectionism efforts in the past did not pan out in reversing domestic production, but did trigger cost hikes among producers. Industries that consume fixed-priced copper—most significantly renewable energy, construction, and electric vehicles—can now see their margins undermined, the outcome being delayed project schedules and higher burdens of capital costs that could put the brakes on larger energy transition plans.

These trends, thus, lead us to the thesis that First Solar (FSLR) is undervalued. Although in a raw material-sensitive industry, its vertical integration and cover contract over the long term provide it with protection from input shocks. Its domestic presence is also well placed to benefit from policy support recovering tariff expenses. Analysts must, thus, be following the curve move and level of the industrial production, as the direction here will reveal whether substitutive policies or margin squeezes are the prominent quarters to come.

Apparel Tariffs And Consumer Price Risks

We at Zaye Capital Markets are considering the impact of impending U.S. apparel and shoe tariffs, which will raise another $24.2 billion in taxes, weighted average 22%. A step to redefine trade patterns is being brought at the economy’s wrong time. Given 97% of the apparel and footwear are imported from foreign countries, mostly Vietnam and China, the impending tariff regime with 54% and above on Chinese imports is light years away from the past regimes when supply chains bore the brunt.

What makes the current path different is the pass-through to consumers. In contrast to previous trade cycles, retailers receive lower margins, lower labour slack, and lower price authority. Pass-through rates vary extensively depending on sectoral competition, but with apparels increasingly sourced from Vietnam—almost one-quarter of the U.S. imports—options for cost absorption are in retreat. If the full cost is passed on, inflation in this one sector alone will increase 4–5%, adding to below- and middle-income households already sensitive to prices.

Compared to that benchmark, Walmart Inc. (WMT) is inexpensive. Its size, supply base diversification, and cost leadership emphasis offer category level price increase insulation. The company is also in a position to take market share away from more constrained-merchandising competitors that are not able to sustain tariff-plugged cost hikes. Investors need to keep an eye on retail import volumes, core PCE inflation that’s correlated with apparel, and discounters’ commentary on earnings in order to observe the in-real-time inflationary footprint of the policy actions.

Climate Risk And Insurance Market Pressure

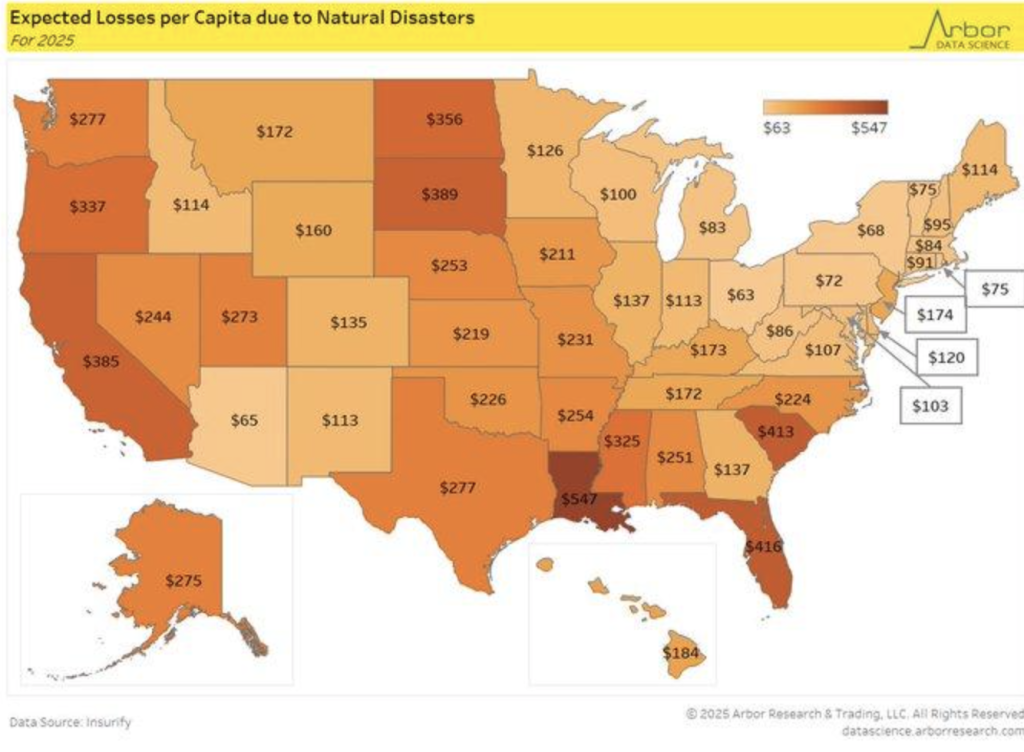

We at Zaye Capital Markets are assessing the increasing economic expense of climate-shareable natural disasters, such as in the extremely exposed U.S. states of Louisiana, which is set to suffer a $547 loss per capita in 2025. The state, which has had eight hurricanes since 2020 and an average economic loss of $2.5 billion, has an exposure that reflects an acute macroeconomic problem. This is the scenario repeated in Florida and South Carolina, with losses of over $400 in per-capita loss, borne by increased frequency and severity of storms—trends that increase the level of risk for the insurer, the municipality, and the investor equally.

These losses are transforming the insurance marketplace. The average U.S. State of Louisiana home insurance premium has hit $10,964, displacing home-owning families and driving large insurers out of business. Peered and peer-reviewed modeling anchors that the increases are structurally, and cyclically, connected with climate risk. This is jeopardizing the long-term viability of property markets within exposure areas and could ignite devaluation or repricing of area-sensitive asset-backed securities based on actual catastrophe loss. The Texas flood is an example of the policy failure aspect, with an inadequately implemented pre-event mitigation that resulted in heightened losses.

The Travelers Companies, Inc. (TRV) appear undervalued under such dynamics. Though its industry faces challenges, its conservative underwriting approach and strong reinsurance cover positions it favorably compared with its peers that are more vulnerable. Investors must be alert to shifts in the pricing of the reinsurance, regional policy redefine, and investment trends in climate adapt—triggers of how the industry is in the process of rebalancing its risk modeling and capital application strategies under rising environmental exposures.

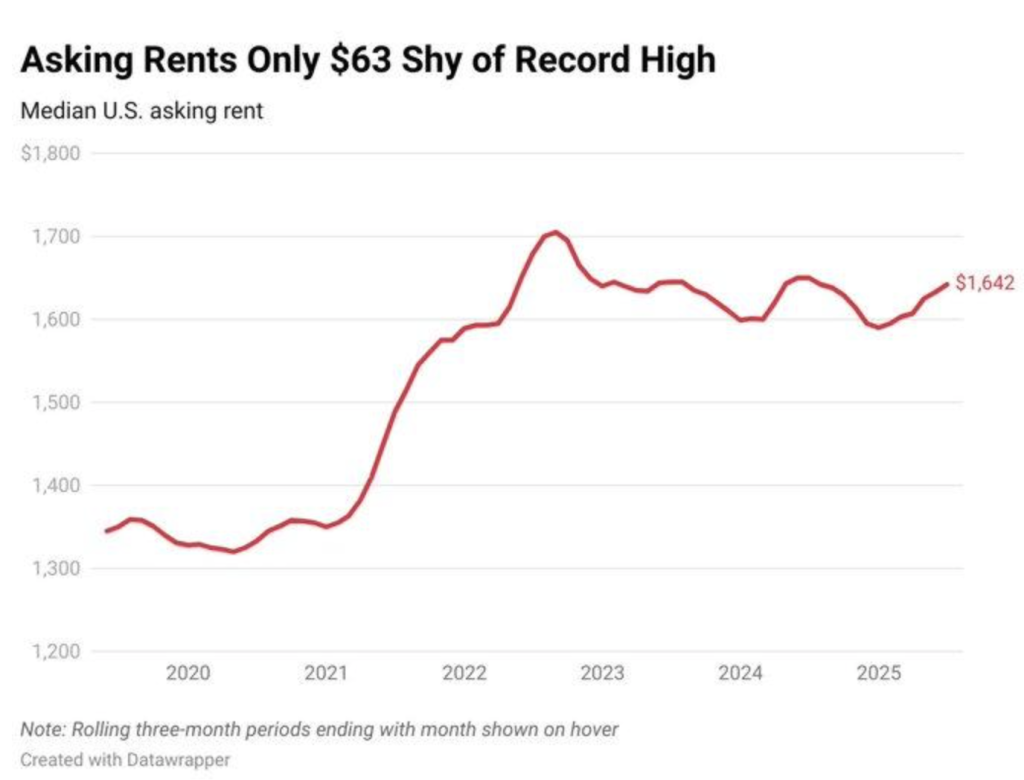

Rental Market Frition And CPI Distortions

We are also observing closely the trend in the dynamics of the U.S. rental market, with the median asking rent having hit $1,642—just $63 shy of its all-time high level. This is after the deceleration in rent growth and the surge in the level of rental vacancies, which hit 7.1 percent in mid-2025—its quickest since 2017. The disconnect is suggestive of segmentation in the market: renewals of old leases could be in the form of flat or down renewals, but newly listed homes are hitting the market aggressively, sending the wrong inflationary message to the headline figures in the house market.

It is especially relevant to the measurement of the Consumer Price Index (CPI). Shelter components account for 7-8% of the CPI measure, but new series capture deflation in year-earlier rent. The gap is an alarm bell that numbers in the CPI may lag behind recent market patterns or mismeasure trends due to outdated surveys or over-projecting owner’s equivalent rent series. This will impart dollar policy based on such numbers with too-tight policies during the very periods that there is genuine relaxation of cost-of-living constaints, primarily among core large-area renters.

Realty Income Corporation (O) is undervalued here. It has a diversified long-term leased base and is highly occupied and generates consistent income regardless of further bifurcation of rent markets. Multifamily over-development exposure is decreasing with exposure to defensive retail and essential service real estate. One has to pay attention to shelter inflation components movement to CPI and watch rental index revision, which will provide essential signals whether or not the Federal Reserve’s inflation indicator is indeed reflecting the market’s reality.

Student Debt Tensions And Aging Borrower Burden

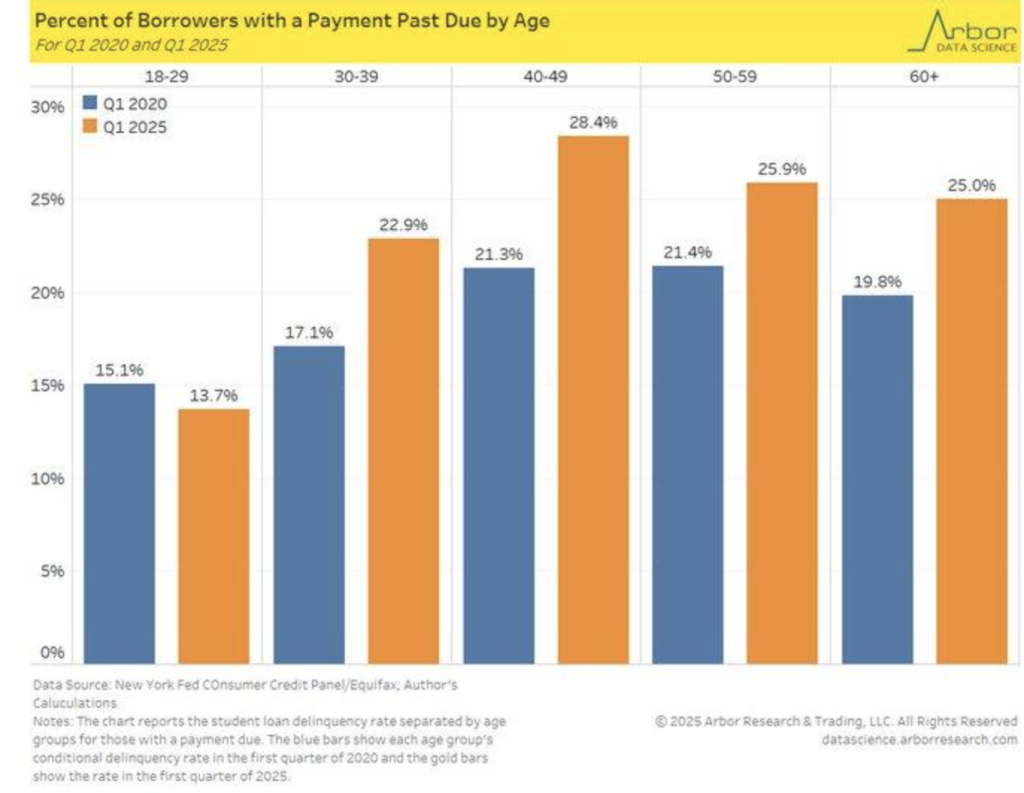

We at Zaye Capital Markets are monitoring the increase of distress in the U.S. student loan market, and the New York Fed’s Q1 2025 numbers logged 28.4% past-due rate among 40–49 year-old borrowers, all greater than any of the other age groups and the long-term outcome of the 1990s’ and early 2000s’ college expenses increasing 141% and positioning the Gen X generation front and center in the structural debt overhang. This is the opposite of the prevailing assumption that student loan concern is the domain of the young borrower and portends more widespread financial weakness.

The cost strain is also augmented with legacy policy impacts, i.e., the CARES Act, and underutilization of income-driven repayment plans. Borrowers are predominantly in deferments or in grace periods, which is distorting true delinquency rates. This is providing credit markets and consumer expenditure projections erroneous risk analysis, with the middle-aged cohort having peak mortgage and healthcare expenditure as well. The confluence of aging debt and deteriorating repayment capacity is concerning in retail lending, residential mobility, and credit card performance in this age group.

SoFi Technologies Inc. (SOFI) appears undervalued here. Its focus on financially oriented service delivery to high-debt households and its refinancing product is an indirect hedge here. As borrower groups become more splintered, adjustable, digitally focused lending products have the most to gain from policy readjustment and demand for tailored repayment terms. Investors are to watch cohort-level delinquency shifts, regulation-level activity regarding the servicing of the loans, and trends in the volume of the refinancings in an effort to gauge the factors impacting the revenues of the fintech credit lending and consumer credit stability.

Investor_Sentiment And Market Inflection Signals

We at Zaye Capital Markets see extreme shifts in investor attitudes, as evidenced from the latest AAII Investor Sentiment Survey. The bull-bear spread, in decline now, is warning, but the S&P 500 is hanging on despite geopolitical setbacks such as the Middle East war between Iran and Israel. The 38% mean since 1987 has been an adequate norm, but divergence from it quite frequently generates market turning points. The current pullback can be an intermediate phase and not necessarily bearish.

Space between price action and sentiment is a cause for concern. Markets are staying tight, but erosion of investor optimism is a sign of growing concern for future earnings, liquidity, or geopolitical spill over. Sentiment is an early warning sign which typically precedes, before the reaction of the markets. Since, in the behavioural finance literature, it is observed on an average, 1–2 month lag between sentiment change and market movement, the world now needs special warning, with the macro data busy schedule and corporate quarterly numbers looming close.

In this regard, Charles Schwab Corporation (SCHW) is a contender to consider as an undervalued prospect. As a sentiment-sensitive product with broad exposure to individual investors, its behavior will help reflect retail positioning and cash deployment shifts. Its diversified business, spanning trading, wealth management, and banking, makes it buffered against sentiment-driven equity repositioning. Fund flow gauges, retail activity levels, and earnings estimates should be monitored by analysts in an effort to discern whether this erosion of sentiment is merely an interim hesitation or the start of a more profound realignment.

Upcoming Economic Events

Attention Turns to Data Releases Next Week

With no major economic players scheduled today, the markets are experiencing a break from directionals catalysts. This is providing the investors with the consolidation break after volatility driven during the week due to trade tensions, central guidance, and macro opinion changes. Prior to the big events tomorrow, the trade today could simply be positioning moves to the events tomorrow.

Lacking top-level product, price action becomes more technical, volume subdued as investors seek to maintain capital and take on little exposure. Quiet-muted, however, won’t endure long. Tomorrow, with the release of the most recent batch of economic figures, expectation becomes that the direction of future monetary policy and the overall growth picture will determine sentiment and that it will determine investor sentiment. Surprise areas of policy and data—where technology and the financials meet—are due for pre-emptive trades as investors seek imminent direction in sentiment shifts.

We at Zaye Capital Markets watch the volatility gauges and cross-asset flows closely. Even though today may appear to offer respite in the very short run, the figures that tomorrow could yield could alter the narrative very quickly, and we are ready to detail such events in real-time to clients and stakeholders.

Stock Market Performance

Markets Bounce Off the Low, Top-Down Damage Continues

Zaye Capital Markets observes that U.S. stocks see large recovery from the April lows through July, yet large indexes still cannot get through or reach resistance at or near year-highs. Despite the positive news headlines, second-look finds that the weakness is underlying and that is translated into the disconnect between the level of the index advance and the average member, which is leadership that is narrow and sector particiation that is defensive.

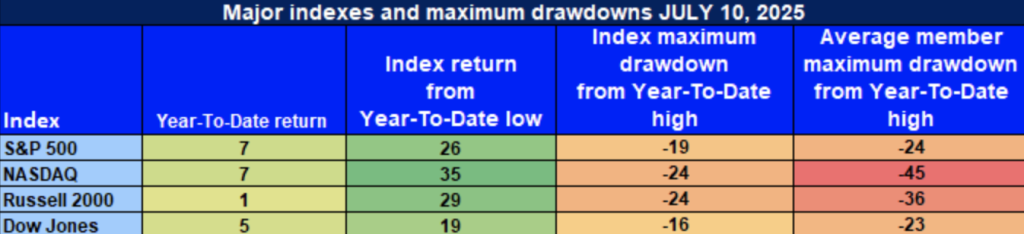

Following is our summary of the key indexes on 7/10/2025:

S&P 500: Momentum Ongoing, Divergence Continues

S&P 500: +7% YTD | +26% off 4/8/25 low | -19% from YTD high | Avg. member: -24%

The S&P 500 is 7% ahead year-to-date, pushed and made possible by the +26% reversal of the April bottom. However, the -19% correction from the YTD high and the -24% average member gain indicate that broad-based strength is still a faraway dream. Bias in the returns is seen within the close circle of heavyweight members, with the overall index structure still unbalanced.

NASDAQ: Technology Keeps Rising, But Exposes Vulnerability

NASDAQ: Up 7% YTD | Up 35% from 4/8/25 low | Down 24% from YTD peak | Avg. member: Down 45%

NASDAQ also formed the bottoms with a commanding +35% reversal and +7% YTD gain. But the average NASDAQ member lags -45% off the high, indicating the weakness of technology and growth stocks. Under the surface, investor sentiment remains cautious and concentrated in the highly select leadership names.

Russell 2000: Small Caps Lag Behind in Recovery

Russell 2000: +1% YTD | +29% off 4/8/25 low | -24% from YTD high | Avg. member: -36% The small-cap shares lag, with the Russell 2000 as low as +1% better this year. Even while the reading’s position is +29% below the April low, unwanted down-draws of -24% below recent record highs and -36% for run-of-the-mill members foretell ongoing investor skepticism regarding smaller, less liquid shares with thin balance sheets.

Dow Jones: Stabilized Overall, But Still Under Stress

Dow Jones: +5% YTD | +19% since 4/8/25 low | -16% since YTD peak | Avg. member: -23 The Dow has marked a decent +5% YTD rise thanks to exposure to the industrials and the defensives. The +19% comeback from the April bottoms is an example of underlying resiliency but the -16% slide back from peaks and the -23% average member loss is an indication that blue-chip stocks too are down on losses thanks to the overall macro uncertainties.

We at Zaye Capital Markets continue to track internal breadth indicators and sector-level dispersion this week in order to view the sustainability of the recovery.

The Strongest Sector In All These Indices

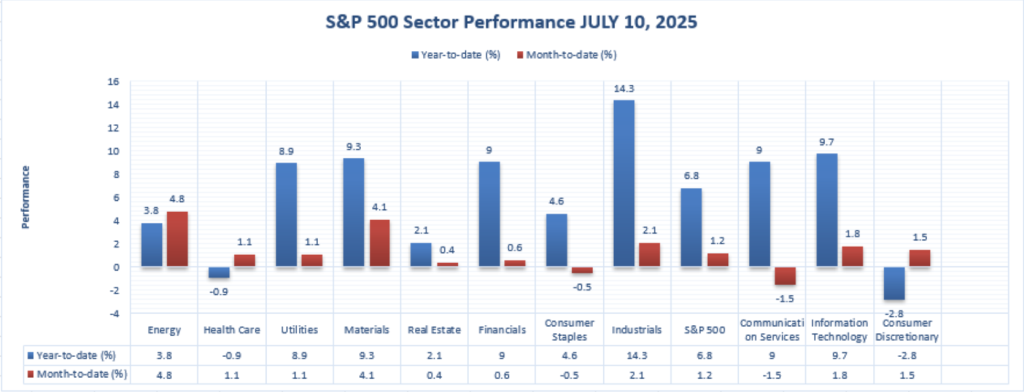

Industrials Leads The Sector Chart In 2025

From sector rotation to cost reduction, Industrials comfortably emerged as the crown jewel as the top-performing sector in 2025. At Zaye Capital Markets, we’ve seen tails of strong winds lift the leadership in manufacturing, logistics, aerospace, as well as infrastructure. With normalized global supply chains and capex growth poised to pick up further, growth and stout resistance against policy-driven demand saw Industrials putting in a good performance.

Industrials: +14.3% Ytd | +2.1% Mtd

Through mid-July, Industrials recorded a top-performing +14.3% year-to-date return, the best of the S&P 500’s eleven sectors. July leadership to date also is present, as the sector recorded a +2.1% month-to-date return, spurred on the heels of positive earnings, increasing factory orders, as well as positive sentiment in logistics and transport stocks. The sector was alsosupported through smooth fund flows, underpinned by heightened infrastructure spending and confidence in local production capacity. Such stability positions Industrials in an extended market still processing macro shocks.

Though Information Technology (+9.7% YTD) and Communication Services (+9.0% YTD) were running second in line, they could not match Industrials in terms of consistency or depth of improvement, nor could they keep up. Consumer Discretionary (-3.7% YTD) and Health Care (-1.5% YTD) were way behind, reaffirming leadership in rotation-hugging year for Industrials. Analysts are recommended to look at sub-industries like machinery, engineering, and defence, where profit momentum and fiscal tailwinds are positive. Though cap flows remain in a runaway mode to cyclic growth with stability, Industrials is a good story in 2025 of structural strength.

Earnings

Yesterday’s Earning Update, Friday 11 July 2025

- Delta Air Lines, Inc.

Delta announced a robust Q2, revenues of $15.5 billion, and EPS of $2.10, a record quarter. Premium travel demand is still the growth engine, high-margin travel increased 5% which made up for weakness in economy. The airline increased full-year EPS guidance, and the dividend was restored, which reflects positive views on future cash flows. The investors would be interested in transatlantic capacity as well as fuel hedging policy as Delta aims to continue the momentum in Q3.

- Conagra Brands, Inc.

Conagra underperformed the quarter, as margin compression was further reduced by an estimated 140 basis points, and organic sales declined moderately. The quarter’s adjusted EPS was in line at $0.70, but investor concern remains due to ongoing cost inflation and weak volumes. With price falling and promoter activity building, Conagra potentially can be facing margin compression in future quarters. See how well the company is able to compensate for product mix and cost control on payables in an attempt to insulate earnings.

- Levi Strauss & Co.

Beating forecasts, Levi earned net income of $67 million and historic gross margin of 62.6%. Revenue was 9% higher and EPS 37% higher as an indication of good execution, but much in direct-to-consumer businesses that contribute significantly to half of all sales. With global demand for jeans still strong, diversified supply chain as well as inventory management will be crucial in accelerating growth in the latter period.

- The Simply Good Foods Company

Solid brand-level growth was experienced at Simply Good Foods, as Quest increased 11% and OWYN increased 24%. Litte commentary on margin in the top line is not good for profitability. The ideas they provide on promotional activity and retail-channel performance would be areas to watch for investors, as the consumer trends in the healthy-snack category continue to shift.

- PriceSmart, Inc

PriceSmart registered a 7.1% peak-peak net sales growth to $1.32 billion and an 8% net profit growth. Solid operating income and further membership growth improvement in Latin America remain underpinning the expansion drive. With most core marketplaces’ macroeconomic environments still in transition, investor attention is centered on regional retailing’s exposure to currency changes and regional competitiveness.

- WD-40 Company

WD-40 topped earnings expectations in reporting $1.54 EPS on $156.9 million revenue. Margin growth to 56.2% and EBITDA growth helped dampen small revenue shortfall. Results did include one-time tax benefit but steady core performance is reassuring. Investors are keen on international sales and pricing strategy construction after tax tailwind.

Earnings Preview: July 14, 2025

- Fastenal Company

Fastenal will be focused on an anticipated EPS of $0.28 on revenues of $2.07 billion. The non-res building construction and industrial supply markets will be under the microscope. With a premium payout ratio and margin squeeze throughout the industry, today’s results will be watched closely for price strength and free cash flow consistency in an attempt to prove dividend sustainability.

- FB Financial Corporation

FB Financial reports after the market and would need to make $0.88 EPS on revenues of $136 million. The loan growth, net interest margin stability, and indication of further credit quality decline would be watched. Given regional banking’s continued transition mode for deposit flows as well as cost of funds, deposit mix as well as fee income strength will be areas of focus.

- WAFD, Inc.

WAFD’s earnings will give additional clarity on commercial lending trends and deposit competition in the west U.S. market. As long as the interest levels are high, pressure in the net interest margin is anticipated. The analysts need to be careful on the credit provisioning as well as loan growth targets revisions.

- Equity Bancshares, Inc

EQBK’s earnings will provide insight to middle-market banking asset quality. With market focus on small business exposure, analysts will be listening for discussion on asset quality, charge-offs, and liquidity on the balance sheet, all against the backdrop of larger regional stress.

- Farmers & Merchants Bank of Long Beach (CA)

This keenly followed community bank will provide insight on domestic credit and deposit flows. With few analyst estimates, our paper today can provide insight on risk appetite, lending discipline, and capital buffers in small banks.

Yesterday’s leaders were price, demand, and margin management in Levi and Delta, while Conagra was hurt under cost headwinds. Call for the next few days will be stock-specific on DTC strength and premium trip trends. Today’s reports on Fastenal and regional banks will be industrial demand and regional credit quality driven. The investors would be looking for demand signals, Fastenal’s margin and payout sustainability, asset quality, and deposit behavior in the financials—the factors important in monitoring economic resilience as well as cap deployment trends.

Stock Market Report for Monday, July 14, 2025

U.S. markets began the week under renewed cautiousness as investors process the latest news on trade policy as well as wait for new economic figures. President Trump’s most recent threats involving mass 30% tariffs on EU as well as Mexican goods as well as its previous threats against Canada as well as Brazil triggered protectionist concerns. Markets, though, registered muted reactions, which could be seen as investors’ resistance or indifference in the face of prolonged political uncertainty.

Stock Prices

Trade Policy and Market Tone

President Trump’s ongoing commentary on trade, in such as future tariffs and renewed demands for the dismissal of Federal Reserve Chair Powell, brings market sentiment risk. Equities are spooked, and futures are even further extended lower after announcements on tariffs even as market watchers seriously wonder whether the latter is risk-off pricing or normal headline-driven volatility.

The Magnificent Seven and S&P 500 Leadership

Core mega-caps—the so-called “Magnificent Seven” (Alphabet, Amazon, Apple, Broadcom, Meta, Microsoft, NVIDIA)—remains the anchor supporting strength in the S&P 500. Market breadth is, nevertheless, poor on a broader front as the gains are relatively narrowly confined in such mega-cap stocks. The gap between such headline index levels and intrinsic problems in participation is a cause for concern: such stocks can suffer sharp corrections in case sentiment changes.

Top Growth Players for 2025

Whilst selective strength is evident in broader indices, each stock on the list made material gains in the year to date. The top 15 growth stocks in 2025 to date are: $MP (+189%), $OKLO (+164%), $HOOD (+164%), $PGY (+148%), $ASTS (+116%), $SYM (+98%), $HIMS (+98%), $STNE (+94%), $PLTR (+88%), $RBLX (+83%), $TMDX (+80%), $QS (+78%), $QBTS (+76%), $CELH (+71%), and $TEM (+68%). The gains are a testament to ongoing demand for innovation, high growth, and speculative activity—the latter particularly

Major Index Performance – Monday, July 14, 2025

- S&P 500 (through SPY ETF): 623.62, slightly lower due to tariff fears

- Nasdaq (through QQQ ETF): 554.20, gentle correction in line with tech

- Dow Jones Industrial Average: Down moderately–reflecting futures pressure

- Russell 2000: Underperforming, in line with widespread weakness in small-cap stocks.

Throughout the day, markets will be watching for policy tone changes, subsequent week’s economic updates, specifically inflation and trade figures, and whether heightened investor interest takes hold or volatility sets in. The interplay between mega-cap tech stability and protectionist tension will be the deciding factor in market action for the week. ease dynamic.

Gold Price

At Zaye Capital Markets, we can verify that gold is trading at about $3,315 an oz on Monday, July 14, 2025. The metal is well supported, with rising policy uncertainty and risk emanating from geopolitics. President Trump’s ongoing string of comments, ranging from threats of 30% EU and Mexican import tariff threats, cabinet reshuffle demands, to strong political rhetoric, is causing global market uncertainty. With no major economic data releases scheduled for today, the policy vacuum is filled by rising political noise, which is further solidifying gold’s position as a strategic hedge. Since no new macro metrics are scheduled to distract markets, investors are buying safe-haven assets to position for policy volatility and escalation in tariffs.

Yesterday’s tone of risk-off flows and equities breadth loss carried over today’s session. The absence of economics news maintains sentiment flat to be easily reactive to headline risk indicators, mostly those involving trade, immigration enforcement, and presidential decision-making. Trump remarks ranging from sanctioning trade to supporting ICE to attacking foreign leaders are keeping defense investor mentality. Therefore, gold is maintaining base near session highs, basking in ongoing uncertainty. Unless bond yields skyrocket or the greenback severely retraces, we expect gold to keep back weaknesses in the week in the $3,300–$3,350 area, with added momentum higher in the event political uncertainty remains well ahead of clarity on the economics side.

Oil Prices

We at Zaye Capital Markets ensure that Brent crude is trading at approximately $70.44 a barrel and U.S. WTI is trading at approximately $68.50 a barrel as of July 14, 2025, Monday. Prices become slightly firmer due to near-term prospects for tauter supply conditions, supported by robust summer refining demand as well as ongoing U.S. threats against Russian oil flows. The plus side is, however, countered against initial OPEC+ production growth signals along with dovish demand outlooks from the IEA. The market remains sensitively poised between summer demand strength as well as structural supply surplus building signals.

President Trump’s most recent comments, like his new threat on tariffs, aggressive posture against European and Mexican trading partners, and bellicose geopolitical rhetoric, introduced further volatilities in oil sentiment. Buying is due to the apprehension that rising trade tension could hit world energy flows indirectly, i.e., in the event when retaliatory actions are against oil products or regions. As no macroeconomic data is due today, lack of new macro cues makes oil markets highly subject to political updates. Yesterday’s broader market sentiment, which was characterized by geopolitical concern and selective rebound in equities, is supporting oil’s rally, but without actual validation in the economy, gains could be held below the resistance band between $72–75.

Bitcoin Prices

At Zaye Capital Markets, we are looking at Bitcoin at about $119,127, supported by solid institutional buying and policy-positive news flow. There was a series of news headlines over the weekend—it included Trump’s incendiary rhetoric on tariffs and “we’re the hottest country” boasts, as well as his calls for bo頼cotts of European goods—to remind markets of continued political risk. The news, combined with increased attention for legislation-around Bitcoin ETFs under the GENIUS Act, played fuel for the appeal for Bitcoin as policy risk hedging. With economic data releases on Wednesday revealing no weakness, the risk-off tilt that benefits digital assets, especially in the context of a thawing equity environment, is serving Bitcoin well.

Crypto-specific news cements the trend: Bitcoin was just at a record all-time high well above $118,000 on record ETF inflows, whale demand, and on-chain indicators suggesting bullish sentiment. Trump’s protectionist trade agenda adds to dollar uncertainty–supporting Bitcoin’s safe-haven story. Friday’s risk-off risk sentiment for equities, for the second week running, driven by escalating tariffs and contradictory economic data, supports crypto demand again. With alternative stores of value in the mix for investors, Bitcoin is once again center stage. With no substantial macro releases today, politics and regulatory metrics will be in driver’s seat for sentiment, bolstering Bitcoin near current highs with potential for further gains in the event of ETF flows and political risk persisting.

ETH Prices

In Zaye Capital Markets, we find Ethereum at $2,971, remaining in the psychologically significant $3,000 zone even as institutions are continuing to buy. U.S. spot Ethereum ETFs last week saw an estimated $907 million of net inflows, an all-time weekly high, which marked a ninth consecutive week of buying. On their peak days, ETF buying surpassed Ethereum’s day’s issuance by 34, creating for the time being a supply squeeze which maintains price steady and gains on the higher side. Such buying on the ETF side is an indication of ongoing institutional conviction in ETH as a long-term hold unit and smart contract foundation.

Whale activity further cements such bullish sentiment. One well-established whale recently transferred 1,900 ETH from Binance and staked 1,888 ETH, demonstrating long-term conviction in Ethereum’s value and in the staking system of Ethereum 2.0. Additionally, seven giant-sized wallets purchased over 127,971 ETH, worth about $358 million, in a span of 24 hours. Such concentrated buying by big-pocketed investors, accompanied by wholesale demand on the structural side, indicates rising conviction in ETH’s fundamentals, dominance in the DeFi space, and future staking gains. As such, these narratives indicate Ethereum’s price is supported on both structural demand as well as concentrated buying initiated by deep-pocketed investors.