Where Are Markets Today?

Global markets will turn slightly higher on Tuesday, August 5, 2025, as U.S. and European futures trade slightly higher. Dow Jones futures rose by 48 points, or around 0.14%, while S&P 500 and Nasdaq 100 futures rose 0.14% in initial market action. On the European side, DAX futures rose 0.30%, Euro Stoxx 50futures rose 0.13%, and FTSE 100futures rose 0.13%. The rises come after Wall Street’s reversal on Monday, when markets rebounded from last week’s selloff on the back of tariffs and last week’s disappointing jobs data. The session sees stabilising investor sentiments, wherein investor attention remains centred around earning strength and potential policy easing.

Source of optimism tempered by caution is fresh policy shift by the Federal Reserve. Poor jobs print last July, and President Trump’s direct disdain against head of the BLS, coupled by hints at manipulated labour statistics, has amplified speculations around monetary easing. The market pricing now reflects 94% probability of rate cuts by September, significant shift from previous week. Trump’s direct call rate cuts now, coupled by widespread unease around integrity in economic data, is catalyzing risk-asset friendly market mood, including equities and commodities. In corporate reality, earnings season continues to be a source of relief. Palantir’s stock jumped more than 4% in after-hours trading after more than $1 billion in revenues from the company reinforced confidence in enterprise software. Hims & Hers Health, though, dropped more than 13% after a top-line miss—but overall, earnings mood remains positive. European mood takes further support from resilient industrials and bank-sector performances, and Asian and European service-sector PMIs increasing mark areas of demand strength increasingly countering macro headwinds.

In our opinion, today’s rebound in futures represents market pricing – balancing monetary optimism against geopolitical risk – and we have a Fed governor and BLS head to fill at the White House, institutional credibility remains at the forefront of attention. Traders will be looking closely at today’s ISM Services PMI and forthcoming earning announcements to feel reassured this rebound should be sustained. Futures indicate, for now, a market tentatively looking to relief, but not wishing to be caught out by politically manufactured shocks or policy mistakes, which can quickly unwind optimism.

Major Index Performance to Tuesday, August 5, 2025

- S&P 500: At 5,841.52, down 0.4% on the day.

- Nasdaq Composite: Fell 0.6% to 18,220.78, lower led by technology and semiconductor group decline.

- Dow Jones Industrial Average: Up 0.2% to 41,182.34, led by advances in energy and industrials.

- Russell 2000: Remains flat at 2,147.63, disappointing as it’s still rate sensitive in small caps.

The Magnificent Seven and the S&P 500

The so-called “Magnificent Seven” stocks—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are under increasing pressure, with each down over 18% from recent highs. This broad retreat highlights growing investor skepticism around inflated AI-driven valuations and earnings momentum that may not hold under tightening conditions. Tesla and Meta have led the downside, while Nvidia is seeing position unwinding from institutional desks. The S&P 500 remains under pressure, now highly sensitive to the performance of these mega-cap names. Without renewed leadership from this group, broader index recovery will be difficult to sustain, particularly as energy and industrials can only offer limited offset.

Drivers Behind the Market Move

U.S. and European markets began positively on Tuesday due to a combination of dovish policy, solid earnings, and picking-up service-sector growth. Futures open slightly firmer as market players respond to recent policy news, data, and solid announcements. Weakened U.S. jobs data from last week and President Trump’s heated firing of the head of the BLS have done much to sustain doubts concerning data integrity and to promote rumors of an earlier-than-expected intervention by the Federal Reserve to spark policy. The sensational resignation of a Fed governor only served to fuel further belief that monetary policy has veered away from its previous course.

- Hope for Fed Rate Reduction Acceleration

Sentiment remains influenced by quickly evolving rate forecast interest rate directions. After poor July payroll figures and President Trump’s suspected data falsification claims, marketplaces now think there’s now a 94% chance of a rate reduction by September. Internal conflict within the Fed—two members voted to reduce it—creates more movement to advocate policy loosening. The move has prompted an equities and gold bounce back and Treasury yields and the U.S dollar down, as market professionals set themselves up for gentle times ahead.

- Tariff Risks and Trade Instability

Trump’s whole policy of tariff remains a source of volatility in global markets. Trump’s application of 41% maximum tariffs to India, Canada, and other allies has created maximum uncertainty within global supply chains. While most nations were in haste to sign trade agreements by deadline, there remain good chances of escalation and Retaliation which remain to be gauged in numbers yet. Most vulnerable remain hi-tech sectors and manufacturing-based industries, and market players now prepare themselves up to more volatility if negotiations deteriorate or White House slaps second round sanctions upon nations facing Russia.

- Sentiment Moderation towards Earnings Stability

In the face of political headwinds, corporate earnings are a stabilizer. Palantir’s announcement of more than $1 billion in revenue lent a shot of optimism to enterprise tech, and other healthy earnings in industrials and finance are a bulwark to the broader market. Hims & Hers, whose stock dropped more than 13% after disappointing revenue guidance, is the exception. Overall earnings season is continuing to surprise to the upside, which is soothing investor concerns over macro risk factors as well as central banks’ legitimacy.

To us, what we see here is crosswinds—a meeting of institutional volatility and trade issues versus good earnings and optimism about monetary stimulus. The week’s large benchmark event will be today’s reading of the ISM Service PMI and any additional appointments or releases from within the Trump Administration, which has the ability to shift sentiment either direction in an instant.

Digesting Economic Data

The TRUMP Tweets and Their Implications

President Trump’s recent string of public comments has injected a new wave of volatility into market conditions, with spillovers extending well beyond political theater. His criticism of Bureau of Labor Statistics (BLS) director, calling recent jobs report “rigged” and attributing it to past pre-electoral data manipulations, has intensified generic suspicions regarding accuracy of U.S. economic data. That erodes market confidence in government-produced indicators such as unemployment and inflation—a critical Fed policy input and investor psyche driver—beyond creating concerns regarding Washington’s capacity to accurately gather and report data, potentially slowing future policy implementations. Trump’s promises to appoint an “exceptional” replacement and revalue labour data raises questions, with investors pitting future report politicized data revision risk against bullish domestic growth prospects and solid global growth underpinnings.

Meanwhile, Trump’s stepped-up trade language—especially his threat to aim at India, Canada, and other US trading countries sweeping tariffs of up to 41%—has reused global trade apprehension. Public allegation by Trump against India of not only purchasing but now marketing Russian oil for profit further contributes to geopolitical tensions, adding pressure to energy markets and bilateral ties. Threat of secondary sanctions and passing on of tariff receipts to poorer Americans spells re-prioritizing of trade flow and domestic budgetary dynamics. For equities, it implies increased duress to import-sensitive industry such as manufacturing and technology, and exporters can prepare to be targeted by retaliatory handling and cost push. The wider implication here is undermining institutional autonomy, and specifically Trump’s assault on Fed monetary policy. Fed independence blame, rate cuts now demands, and interference in future appointments, including the new Federal Reserve governor, imply a move towards politically-motivated monetary policy. There can be market interpretation of losing central bank credibility, which can produce risk-off behavior, flight to safe-haven assets such as gold, and reprice of rate expectations in bond markets.

In the long term, Trump’s remarks portend a shifting macro setting in which traditional economic levers no longer seem as safe from political intervention. While some of his policies—such as supporting domestic energy infrastructure or pushing back against foreign interference—have some backing from particular investor constituencies, execution risk and international blowback represent extreme danger. We at Zaye Capital Markets continue to watch closely for these developments, subtleties amid data transparency, central bank power, and cross-border capital flows as election season approaches.

Easy Financial Conditions Reemerge—Are Markets Ignoring Signs?

Dramatic change we see as the Chicago Fed’s National Financial Conditions Index (NFCI) records a very loose August 2025 reading, its level not seen since the late 2021 timeframe. Such a low-interest-rate, liquidity-rich climate has predecessors in previous recessions’ recoveries, as well as risk-taking excesses. As credit and asset price growth rises when financial conditions become easier, we wonder how stable this cycle shall be.

The analogies with 2021 are pointed. Back then, accommodative conditions fueled a high-yield issuance boom, planting the seeds of instability. Without policy’s timely restraint, such liquidity can fuel asset bubbles, especially for equities and corporate credit. Banks might be exhibiting robust capital provisions now, but based on earlier regulative reports, it is a fact that such financial resilience existed before the 2022 inflationary downturn. The prevailing situation can cause investors to overlook the risk of tightening until it is too late.

Here, Citizens Financial Group seems to be underpriced, with strong domestic diversification and capital strength, but it is discounted on the back of broader banking sector issues. Investors should remain vigilant on Fed forward guidance, dynamics in bond market spreads, and liquidity coverage ratios to already be able to identify mispricing in the credit markets. Inability to make pre-emptive risk balance tweaks would leave the economy vulnerable to a more-than-expected reversal.

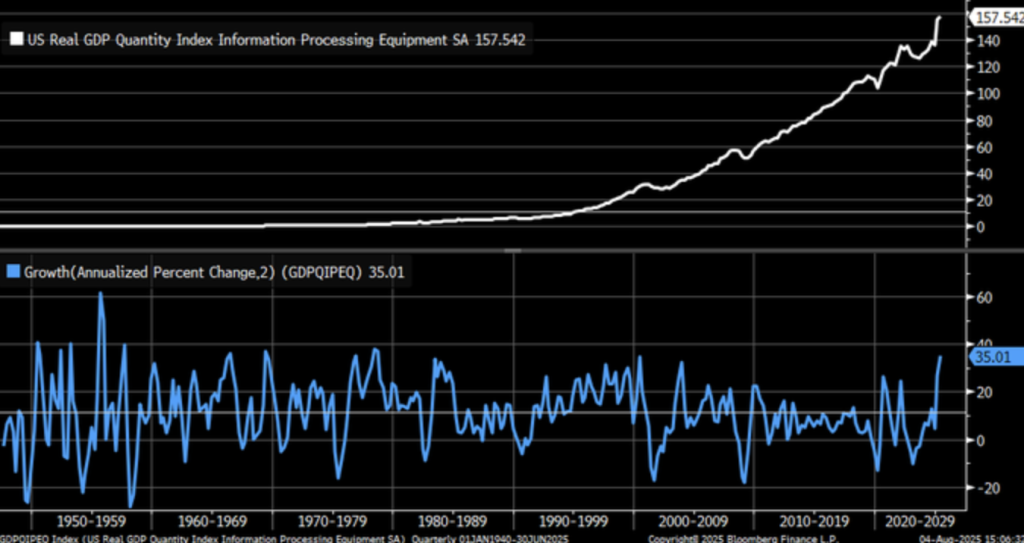

Business Technology Expenditure Skyrockets—Is Productivity Ready To Enter A New Era?

A 35%-yoy U.S. business investment in data processing gear in Q2 2025 represents its largest gain since 1978, by when personal computing’s conception is. Though GDP growth does not change at 3%, this differential indicates speeding up decoupling of current economic production and digital transformation wave driven by AI- and cloud infrastructure buildout. In our opinion, this surge indicates a structural cycle of business investment as opposed to a short-term bounce-back.

Earlier, as high tech spending waves–monitored by the Bureau of Economic Analysis–have arrived with strong productivity growth, so too in the late ’90s. While previous waves saw volume expansions, integration efficiency now becomes a concern. Cloud-native SaaS software and AI platforms demand software, labor, and operational cohesion. Without integration, capital investment risks failing to live up to expectations.

Our view is that NetApp Inc. remains underappreciated compared to its strategic position in cloud data administration and hybrid storage solutions. Its position at the enterprise level aligns with changing infrastructure requirements but continues to quote below sectoral multiples. Analysts need to track the lags in deployment in tech capex and productivity measures in non-tech industries to make judgments on true economy spillover. Misdiscord between investment optimism and realized returns has the potential to reshape equity valuations aggressively.

Market Breadth Narrows As NYSE A-D Line Signals Potential Turbulence

Further divergence in equity internals arrives as NYSE cumulative A-D line bottoms out lowest since late June 2025. That translates into weakening market breadth as S&P 500 rose to 6,251.01 last week. The underlying message, though, cannot be avoided: whereas headliner indices are showing enthusiasm, the participation continues to be thin, a sign of weakness behind the grandeur. Dislocations of this sort have a tendency to portend narrow group of large-cap issues behind the spectacle.

This is a pattern which has a vintage warning sign feel to it. Traditional research has consistently linked falling A-D lines to pre-correction environments, especially when dividend-paying indices decline against advancers. The 2007 pre-crises scenario was the example du jour—where similar conditions concealed intrinsic system frailties. Should history rhyme, our present rally remains more speculative positioning than a broader rebound, all at least when liquidity tilts mega-cap tech vis-a-vis cyclicals.

Against this context, we have Invesco S&P 500 Equal Weight ETF (RSP) undervalued against its diversification, currently trailing index-weighted counterparts. Its relative decline has room to rebound if breadth reverts to mean levels. Brokers should be responsive to inversions in NYSE and Nasdaq breadth indicators as a precursor to measure early index leadership exhaustion signals. Forgetting internal decline makes the portfolio exposed to risk concentrations to the negative.

Flat Manufacturing Orders Reveal Industrial Sector Stall

In our recent survey of U.S. manufacturing data, it is worth observing that new orders, excluding transport, have been flat year to date to June 2025, in line with a flat industrial outlook. While recent growth has been sharp in some measures, overall the picture remains muted. Lead order expansion has also been flat since 2020, in line with a structural absence of momentum in the manufacturing sector—a trend concealed by aggregate economic enthusiasm.

Historical precedent comes to the fore: sharp 2008 and 2020 order downturns have been accompanied and succeeded by solid bounce back. But bounce back is tight this time. Ongoing bottlenecks in supply chains, high input prices, and labour availability maladies still restrict production. While macro narrative is story of industrial renaissance following pandemic, this data is proof that industry remains restricted by logistical inefficiency and demand-side riskiness.

Here, we believe Lincoln Electric Holdings (LECO) is fairly valued. Though it has good global exposure and automation tilt, its price subjects its long-term fundamentals to cyclical paths. Freight prices, supplier lead times to ship, and ISM new orders sub-indices should be monitored by analysts to capture moments of real-time turnings. Without labour and input reprieve, its group’s room to move up remains narrow, and bullish industrial bets not easiest to place.

Utilities Index Hits Record High As Ai Demand Redefines Defensive Growth

The S&P 500 Utilities Sector Index peaked at 453.58 back on August 1, 2025, and continues its multi-decade ascent since 2018. The action reflects the transformation of the group from a traditional defensive play into an AI age growth anchor strategy. What were once previously previously formerly 2020 rebounding external shocks now seem base-supported by global changes in energy demand. What were once previously previously formerly utilities’ lagger sectors now become infrastructure supports to the digital world.

Energy usage has been redefined by AI with AI data centers requiring near-continuous uptime, calling forth long-duration electricity demand to all-time highs outside the bounds of the old grid paradigms. With business deploying capacity to meet digital loads, utilities themselves are an integral supporting strut, enabled by capital spending and government expenditures. The $90 billion PA power grid buildout by the U.S. government can be interpreted as policy guidance in that regard. Geopolitical trade risk, likewise, has investors favoring domestically based, dividend-generating assets.

Here, Vistra Corp. (VST) falls short, although fundamentals do have some strength and it does have some experience in legacy and renewables-based infrastructure. Although growth catches surging AI-based demand, its valuation falls behind sector leadership. Prioritizing region infrastructure growth, future electricity prices, and AI infrastructure buildout will let long-term sector positioning be evaluated. Exclusion of utility-tech convergence can generate structural allocation error.

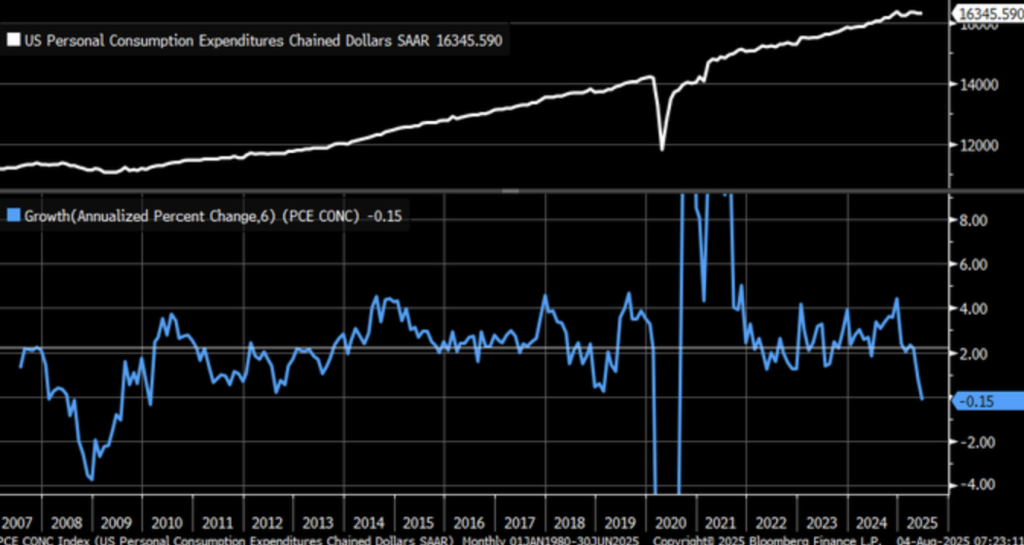

PCE Contractions Indicate Consumer Weariness Amid Tariff Stress

Closely following a U.S. personal consumption expenditures (PCE) decline recording a growth rate of -0.15% in the first six months of 2025—lowest decline since 2020—the indicator, when measured by chained 2017 dollars to gauge inflation, reflects an important decline in real family spending, a top U.S. growth driver. Serving as a long-term indicator of probable recessions, the indicator should be more closely monitored by market professionals.

A compilation of this decline is a steep decline in consumer confidence. Internal surveys and wider augurs of a 32% drop in mood this year, primarily because of additional tariffs and ongoing inflation, are making families cut discretionary spending and turn to cheaper alternatives even in necessities—a path that showed in 2008 after-slowdown decline. Disabled demand has yet to be properly valued by growth prospects or retail profit expectations.

Here, Target Corporation (TGT) appears to be cheap, given its stock price reflects overall retail negativity. Nevertheless, its averagely profiled positioning and store brand products provide a cushion against consumer trade-downs. One should be keeping an eye on future profits to observe how inventory turn, real wage growth, and price discounting are doing. If it doesn’t normalize PCE, it can observe all consumption-sensitive sectors witness downward revisions.

Upcoming Economic Events

ISM Service PMI

Punctuating what might be a combustible moment awaiting global financial markets, all eyes are on today’s ISM Services PMI report, a leading indicator of U.S. economic health. Following hints of deterioration by consumer outlays and manufacturing growth slowing, the services sector has been nothing short of the lifeblood of the American economic system. That report is not just another indicator; it’s a road map to Fed policy, investor risk appetite, and sector rotation in equities. Here’s what market action would be influenced by varying outcomes:

If Actual ISM Services PMI is greater than Forecast:

- A bigger-than-expected number would be good for the case that services are still robust, offsetting weakness in industrial production and demand. That will enhance risk appetite, fueling equities flows into cyclicals such as finance and transport. But it’s all a breeze—a strong services reading can drive wage inflation and push rate cuts out of the picture, making the bond market hawkard. Be prepared for yields to go up, tech to get pushed on valuation grounds, and the dollar to appreciate on interest rate differentials.

If Actual ISM Services PMI falls short of projected:

- Negative shock would further raise fears of a synchronized economic downturn. Manufacturing has softened already, PCE growth has turned negative, a disappointing services report would raise further fears of a synchronized downturn. Stocks would shift to defensive sectors—utilities, staples, and treasuries—while preparing the market for policy easing or recessions cover. Rate-cut probabilities would increase, and the yield curve would continue to steepen as growth outlook declines another step.

Zaye Capital Markets believes analysts should be looking for follow-through in service-hiring and prices paid inputs within the next couple of weeks, not least as markets await the next inflation print and Fed comments.

Earnings

Yesterday’s Earnings – August 4, 2025

- Palantir Technologies Inc.

Palantir reported a strong second quarter, with adjusted EPS climbing to $0.16—marking a 78% year-on-year increase—and revenue surging 48% to surpass $1 billion. This impressive performance was driven by robust growth in both commercial and government segments, particularly with U.S. commercial revenue up 93% and U.S. government revenue rising 53%. Palantir raised its full-year guidance to $4.14–$4.15 billion, and the stock rallied approximately 4% after hours in response.

- MercadoLibre, Inc.

MercadoLibre delivered results that met expectations, with revenue and earnings per share broadly in line with forecasts. However, investors are awaiting further guidance from management, particularly around margin trends and e-commerce growth in high-inflation regions. The market’s response remained cautious, pending additional forward-looking commentary.

- Vertex Pharmaceuticals Incorporated

Vertex disappointed investors after revealing setbacks in its experimental pain therapy program. Despite delivering respectable earnings, the failure to progress a key drug candidate into later-stage trials triggered a sharp selloff, with the stock tumbling around 14%. The results raised concerns about pipeline durability and near-term growth drivers.

- Williams Companies, Inc.

Williams posted solid second-quarter earnings, supported by strong demand across its natural gas infrastructure business. The company reported an adjusted EPS of $0.46, with stable revenue driven by regulated assets and long-term contracts. The results reinforced Williams’ positioning as a defensive utility amid rising energy demands and geopolitical volatility.

- Hims & Hers Health, Inc.

Hims & Hers reported Q2 revenue of $544.8 million, representing a 73% year-on-year increase, alongside an adjusted EPS of $0.19, which beat expectations. However, softer-than-expected revenue guidance for Q3 and recent legal uncertainties weighed heavily on sentiment, sending the stock down roughly 12% after the close.

Today’s Earnings – August 5, 2025

- Advanced Micro Devices Inc.

AMD is set to report after market close, with analysts expecting strong revenue and earnings growth fuelled by AI, PC, and data centre demand. Investors will pay close attention to updates around EPYC server chip adoption, AI GPU shipments, and forward guidance. Any signs of sustained pricing power could boost sentiment across the semiconductor sector.

- Caterpillar, Inc.

Caterpillar’s results will be closely watched for signals on global construction and mining activity. With recent commodity price volatility, markets will assess machinery backlog, regional sales breakdown, and cost inflation pass-through. A strong showing here could provide insight into industrial demand resilience, especially across emerging markets.

- Amgen Inc.

Amgen’s Q2 print will focus on pipeline momentum and pricing outlook, particularly as biosimilar competition and policy headwinds continue. Analysts will also look for updates on key oncology and inflammation treatments, with R&D costs and regulatory developments in Europe and the U.S. under the microscope.

- Arista Networks, Inc.

Arista’s earnings will be a barometer for enterprise cloud infrastructure demand. Expectations centre on data centre switch sales, especially from hyperscale clients. Investors will be keen to see if the firm sustains its momentum in AI-driven networking solutions and margin performance in a high-capex environment.

- Eaton Corporation, PLC

Eaton reports today with focus on electrical systems growth and industrial automation resilience. As a key player in the global electrification shift, Eaton’s outlook on AI-powered infrastructure and utility demand could shape market sentiment in both industrials and green energy.

- Fidelity National Information Services, Inc.

FIS will draw attention to trends in digital payments and financial software services. Investor focus will be on core merchant volumes, organic revenue growth, and commentary on client demand amid shifting interest rate environments. Performance in its banking and fintech segments may reveal how well it’s navigating the evolving payments landscape.

We at Zaye Capital Markets are tracking each release closely and will provide follow-up analysis on earnings surprises, sector reactions, and investment opportunities.

Stock Market – Tuesday, August 5, 2025

U.S. equities began the session mixed as market players continue to grapple with divergent macro cues. Following recent data showing diminished consumer spending and a weakened jobs market, elevated yields and obstinate inflation continue to be adding blemishes to the broader recovery narrative. President Trump has increased warnings of tariffs in recent months, and geopolitical hot spots have erupted in Asia, leading markets to go defensive. Techs and growth names suffer, while energy, utilities, and financials represent short-term havens.

Stock prices

Economic Indicators and Geopolitical Trends

markets were rattled by President Trump’s recent threat to impose 41% tariffs on some Asian imports, vowing to disrupt supply chains. ISM Services PMI printed to a better-than-anticipated number, adding to sticky inflation concerns and postponing rate cut timing. Yields rose on the news, igniting a rate-sensitive names dump. Policy hawkishness dominance versus strength in earnings into Q3 remains what investors can’t agree on.

The Magnificent Seven and the S&P 500

The so-called “Magnificent Seven” stocks—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are under increasing pressure, with each down over 18% from recent highs. This broad retreat highlights growing investor skepticism around inflated AI-driven valuations and earnings momentum that may not hold under tightening conditions. Tesla and Meta have led the downside, while Nvidia is seeing position unwinding from institutional desks. The S&P 500 remains under pressure, now highly sensitive to the performance of these mega-cap names. Without renewed leadership from this group, broader index recovery will be difficult to sustain, particularly as energy and industrials can only offer limited offset.

Latest Stock Updates

- Amazon (AMZN) stock declined after last month’s report of sluggish warehouse traffic, which may be an early indicator of e-commerce volume weakening. Prime Day was solid, but following concerns around weaker back to school and holiday season demand in Q4, investors have turned away from high multiple retail tech.

- Tesla (TSLA) dropped over 3% during the day after reports emerged that Chinese electric vehicle makers are escalating price wars in key European markets. Analysts are concerned that Tesla’s margins will keep on decreasing without a plan to respond, especially with raw material prices beginning to increase again.

- Alphabet (GOOGL) made slight declines as EU regulatory powers continue to gather steam prior to forthcoming future AI legislations which will have significant impacts on underlying ad business models. Investors have been tentative looking to future growth market monetisation as policy evolution changes course.

- Microsoft (MSFT) stock remains unchanged after contrasting analyst comments. Despite cloud growth merely holding its own, some early checks in Q3 have indicated enterprise spending drop-off starting to impact near-term pipeline at Azure.

Major Index Performance to Tuesday, August 5, 2025

- S&P 500: At 5,841.52, down 0.4% on the day.

- Nasdaq Composite: Fell 0.6% to 18,220.78, lower led by technology and semiconductor group decline.

- Dow Jones Industrial Average: Up 0.2% to 41,182.34, led by advances in energy and industrials.

- Russell 2000: Remains flat at 2,147.63, disappointing as it’s still rate sensitive in small caps.

We remain at Zaye Capital Markets focusing closely on thin line between inflationary pressures, geopolitical tensions, and corporate earning delivery. Sector rotation and earning integrity, as valuations in tech have been redrafted, will be what defines performance in the coming weeks.

Gold Price

Spot gold, Tuesday, August 5, 2025, is $3,381.40 an ounce and slightly higher by 0.3% and riding gains as investors react to spikes in geopolitical risk, ebbing economic optimism, and ratcheting trade tensions. President Trump’s sweepingly critical remarks—slamming last week’s jobs report as “rigged” when going after BLS head, and pledging to be replaced by a politically acceptable one—reawakened fresh doubts over U.S. data credibility. With Trump also pledging up to 41% tariffs versus India, Canada, and others, gold’s previous safe-haven flows have risen further still. Additional strains include Fed Governor Kugler’s resignation and Trump’s prodding to initiate rate easing now, stoking fears over possible monetary policy manipulation. These, along with threats similar to that of Fitch by officials like Hassett, are creating a case around gold as a hedge against inflation and institutional risk both.

The day’s ISM Services PMI reading, however, adds another variable to the equation. If it comes in better than expected, it will be taken by markets as a bullish indicator of economic strength, gently deflating gold’s recent price momentum. But any disappointment on the miss side will embolden rate-cut expectations further and incur further dollar weakness, and gold will gain further support to the bullish side. Underlying backdrop—a politicized Fed call, tariff-imposed supply-chain dislocation, and integrity questions over macro credit data—remains bullish to gold. As sentiment continues to worsen across equities and sovereign credibility is questioned, gold remains one of the few of available hedging tools to investors to navigate an increasingly more volatile economic and political environment. At Zaye Capital Markets, we are still bullish on gold as a strategic bet against a backdrop of rising volatility and structural skepticism.

Oil prices

Brent trades at $68.75 per barrel on Tuesday, Aug. 5, 2025, and WTI around $66.25, both down following OPEC+’s September 547,000 bpd supply increase, which has again stoked oversupply fears. Moderate demand growth this year has been predicted by the International Energy Agency (IEA) despite U.S. shale production picking up and global fuel demand falling, led by the U.S., continuing to remain a mood dampener. Poor U.S. jobs report yesterday has also kept the bear bias going, further stoking recession fears and pricing in hopes of monetary easing out. Treasury yields have edged up and appetite for risk has diminished, and oil has turned range-bound as more definite cues of future demand come in.

President Trump’s comments on criticizing India for re-exporting Russian oil and threatening US action to impose 41% punishing tariffs added a geopolitical risk factor to oil markets. Such comments risk re-shaping global trade patterns and obfuscating energy policy intentions, particularly if India diversifies crude origin. Trump’s denouncement of labour data and demands for instant Fed rate cuts also add to economic policy risk, injecting volatility. Attention now turns to today’s ISM Services PMI—a strong reading can confirm economic resilience, hardening yields and tempering oil demand prospects. A weak reading, on the other hand, can trigger recession fears, driving oil lower. In the face of supply growth, dismal macro data, and trade tensions, oil is under bearish pressure, as weakness in demand overshadows geopolitical tailwinds.

Bitcoin Price

On 5 August 2025, Tuesday, Bitcoin hits $114,708, rock-solid as markets absorb divergent macro data and institutions’ relentless purchases. Last week’s purchase by MicroStrategy of 21,021 BTC, adding its combined storehold to 628,791 coins valued at more than $72.5 billion, remains a testament to Bitcoin’s strategic treasury asset status. As another reason to be bullish, U.S. President Trump last week announced creation of U.S. National Crypto Reserve, Bitcoin to be its notable holding—a historical digital asset policy move adding to BTC’s sovereign-level status. Following last week’s redemptions of $223 million of crypto funds, altcoin strength and risk appetite back remain to display underlying strength, retail sentiment, by contrast, rallying into dip-buying levels, notably below $100K, as highlighted by influential names such as Robert Kiyosaki.

Trump’s remark brushing aside the integrity of labor statistics, alongside his prescriptive Fed rate cut demands and hawkish tariff taunts, has shaken long-standing policy norms and stoked Bitcoin’s hedge demand. The confluence of decreased U.S. institution trust and politicized economic rhetoric is bolstering a movement towards trustless, decentralized assets. Yesterday’s dismal jobs report fostered speculation that the Fed will keep rates unchanged or cut it sooner, bullish for Bitcoin, an asset that yields nothing. ISM Services PMI data this morning will be a near-term catalyst: a weak reading would stoke Bitcoin’s flight to $118K+, and a surprising positive risk would reverse momentum without changing structural bullishness. Overall, Bitcoin remains supported by institutional demand, monetary policy risk, and rising geopolitical tensions—a solidifier of its status as macro hedge and strategic asset.

ETH Prices

Ethereum has risen to $3,678.58, posting a healthy 3.1% increase over the past 24 hours as institutional and whale buying fuels the rally. A whale-OTC mega trade of over $300 million of ETH, rolling positions to over 79,000 tokens, ignites bullish emotions in the market. ETF inflows keep gaining strength as well, with BlackRock’s ETHA and iShares Ethereum Trust fetching over $1.7 billion of new capital in 10 consecutive trading sessions, 40% institutional demand over the past month. These headwinds have gained legitimacy in ETH’s price rallies, none more so as it bounces from lows below $3,400 and holds firm above critical resistance levels.

At a macro scale, Ethereum is being met with a more favorable policy climate. Down-drafted U.S. jobs data yesterday and increasing doubt surrounding its veracity have rekindled laten Fed tightening expectations, creating bullish liquidity around risk assets such as ETH. ISM Services PMI, due out today, will be watched carefully: a soft reading can create more buying, while a surprise larger-print can create near-term risk-on flow suspension. Either case, ongoing ETF demand and whale conviction continue to ignite a structural support level, set to propel ETH to a near-term move to the $4,000–4,200 region against its current trend. We at Zaye Capital Markets observe these inflows and wallet action closely as canaries surrounding deeper institutional conviction.