Where Are Markets Today?

US and European stock futures Wednesday morning open in defensive mode with a mix of corporate profitability and further concern about economic momentum taking its toll on sentiment. Thus far this morning, S&P 500 futures down by less than 0.1%, Nasdaq 100 futures down 0.2%, Dow Jones Industrial Average futures about even. In Europe, Euro Stoxx 50 futures up 0.3%, FTSE 100 futures modestly lower down 0.2%. The divergence in performance is indicative of divergent investor expectations with Wall Street working through corporate earnings and Europe grappling with weak economic data.

U.S. futures were hurt by a series of high-profile misses in after-hours earnings. Advanced Micro Devices (AMD) fell near 5% after an EPS miss in an adjusted measure which tempered enthusiasm within the chip community. Snap Inc fell 15% following a below-average revenue catchup report but Arista Networks provided a lone plus 14% higher on solid numbers. Those individual gains weren’t enough to reverse recent market softness—the fifth loss day in six for the S&P 500 and sixth in seven for the Dow—a sign of increasing investor fatigue and caution towards risk. Mood was equally delicate elsewhere in Europe. The 50.2 reading for the July Eurozone Services PMI was slightly better than levels of growth but below forecasts, fanning concern about stagnation. Industrial orders dropped sharply in Germany, meanwhile, fanning existing fragility in Europe’s factory sector. Investors are also dealing with lackluster EU’s industrial giants’ earnings, fanning concern about the region’s economy losing steam. Poor advance in futures can do little more than signal overall indecision with markets not wanting to set themselves up too aggressively going into more company earnings and policy course.

To our mind at Zaye Capital Markets, this muted futures action is cross-market weakness. As long as geopolitical risk is high in Trump’s belligerent approach to trade policy and macroeconomic data still refusing to provide reassurance, U.S. and European stocks cannot be shaken out of a stalemate. Further consolidation cannot be excluded until earnings momentum comes back or surprise economics turns the script around. Investors now eye sector rotation and money signals with greater anxiety with respect to near-term direction for Fed leadership and European growth prospects.

Major Index Performance on Wednesday, August 6th 2025

- S&P 500: 5,829.41, down 0.3%, dragged lower by technology weakness.

- Nasdaq Composite: 18,106.55, -0.5%, as losses in semiconductors deepen.

- Dow Jones Industrial Average: Remains steady at 41,185.77, supported by industrial stocks and energy stocks.

- Russell 2000: Down 0.2% at 2,143.08, as small-caps react negatively to rate sensitivity and weak

The Magnificent Seven Plus S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet and Tesla—are exerting a large weight on the S&P 500 with AI-fueled growth sentiment deflating. 18%-plus retracements on averages off highs, the aggregation sellback in this select group—led by Nvidia—has had a large weight on the index. Index-level advances won’t resume durably without a stabilizing action in leadership.

Drivers Behind the Market Move

At Zaye Capital Markets, we have three key drivers of the U.S. and European markets today, based simply on the news reported in the last 24 hours alone:

- Mounting Trade & Tariff Threats

US President Trump’s recent tariff threats—on semiconductors, on pharma, on India, on the EU—are creating fresh uncertainty across the world’s markets. These aggressive policy moves are prompting firms to reexamine supply chain economics and price power with inflationary pressure consequences. US industrials have already begun signaling tariff-related headwinds through earnings calls with European exporters preparing for tit-for-tat counterattacks. This new sense of geopolitical jitters is prompting investors towards more defensive but less cyclical places, a large-scale move towards defensive positioning.

- Economic Stress Indicators from Service Sector Data

U.S. ISM Services PMI recent outcome captured worsening employment and rising input prices—a harbinger for stagflation. Meanwhile, the European Services PMI for Europe registered a little better than the level for contraction, but German industrial orders fell more sharply than expected with a similar impact of a tightening of conditions of demand with manufactures production. Ease of growth with firming costs has caused eyebrows over the efficacy of conventional monetary instruments and dents investor confidence over a sustained pick-up in growth.

- Weak Profits And Policy Uncertainty

Differing earnings reports—i.e., tech stocks like AMD—have been a cause for conservative mood with weak guidance depressing sentiment. Trump rejection of BLS chief, hints at manipulated jobs reports, and a call for a reformed Fed contribute to a sounding of alarms over political meddling in monetary policy. Volatility source also comes with a governor’s departure at the Fed. Investors pre-warn expectations prior to a potential cut in rates but little is understood about institutional credibility, a delicate set of conditions for risk assets.

We think these factors—policy uncertainty, macro softness, and earnings pressure—are the main causative drivers of current market sentiment. Defensive stocks, hard assets, and selective positioning are what we like currently until more clarity prevails.

Digesting Economic Data

The TRUMP Tweets and Their Implications

President Trump’s recent wave of public statements, interviews, and social media posts has unleashed a fresh layer of volatility across global markets. From abruptly firing the Bureau of Labor Statistics chief to accusing the labour data of being “rigged,” Trump has aggressively questioned the credibility of institutional reporting. These remarks have stirred deep concern on Wall Street, where data transparency and reliability are critical to market functioning. Investors now face growing uncertainty around the integrity of upcoming macroeconomic releases, leading to increased demand for assets that exist outside the realm of government manipulation—such as gold and cryptocurrencies.

To add to domestic volatility, Trump’s overseas oration also has become more menacing. Threats at imposing heavy tariffs on India—categorically blaming the nation for buying Russian oil and reselling for a profit—along with fresh threats of a 35% tariff for the European Union and a new batch of tariffs for semiconductors and pharmaceuticals has once more sparked global trade anxiety. This tariff platform has the capability for unwinding highly fragile supply chains for businesses at a delicate point for world growth recovery. Although Trump mentioned progress with China and hinted at a meeting between the two heads over the course of the year, the global trade discussion as a whole still appears belligerent and mercurial. Market reaction has been circumspect with cycle stocks lagging behind and safe-haven flows gaining ground. In his living room, Trump’s allegations of the “highly political” Federal Reserve, in addition to hints at some “very good” sorts in queue for taking over Chair Powell, predict a possible reorganization of U.S. monetary oversight. Following the resignation of Fed Governor Kugler and Trump’s promise of a near-proximal appointment for the Fed Chair, there is a discernible move towards politicized monetary policy. Investors now wager on sharper rate cuts and aggressive easing trajectory already impacting bond markets and catalysing non-yielding assets such as bitcoin and gold.

We at Zaye Capital Markets view these developments as triggers towards higher market sensitivity and adjustment of investor sentiment. As confidence in government Stats falls and policy uncertainty rises, capital will continue flowing towards defensive and decentralized segments. Volatility will be sustained, and markets will remain more sensitive towards political rather than economic fundamentals, at least until institutional clarity returns.

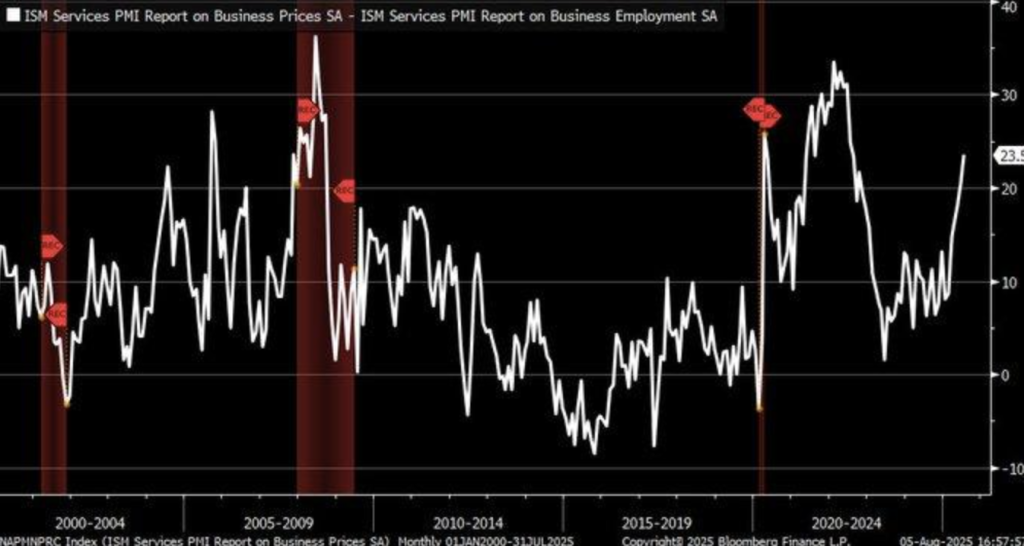

Stagflation Signals Resurface As Service Sector Spread Widens

We closely monitor deviation between lag behind/employment prices on the ISM Services PMI because the deviation rekindled stagflation concern—a period with inflation on the roll but flatlining/slowing economy activity. It fell for the Services PMI for July 2025 all the way down to 50.80 from 50.10 registering a fair growth but prices paid accelerated at their fastest rate since October 2022. This dislocation which in the earlier times clustered together in 1970s oil shock has a historical association with diminished purchasing power and dislocation in markets.

Our evidence indicates that this is more than a transient anomaly. For labour market indicators, they are softening but inflation pressures continue to be firm, a pattern characteristically observed outside recession or supply-shock settings. These inflation pressures are apparently being supported in recent Trump administration tariff actions, as suggested by historical precedents that associate tariffs with elevated consumer prices in slowdown economies. Policy environment—specifically with respect to trade and monetary policy—is perhaps if anything introducing rather than removing economic friction.

Here, our view is for Procter & Gamble (PG) to be currently undervalued in the context of its defensive price power and past strength in inflationary settings. August services/factory data will be closely examined by analysts and in particular new orders/new input prices spread for signs whether the divergence at face value is temporary or more of a wider structural shift towards stagflation settings.

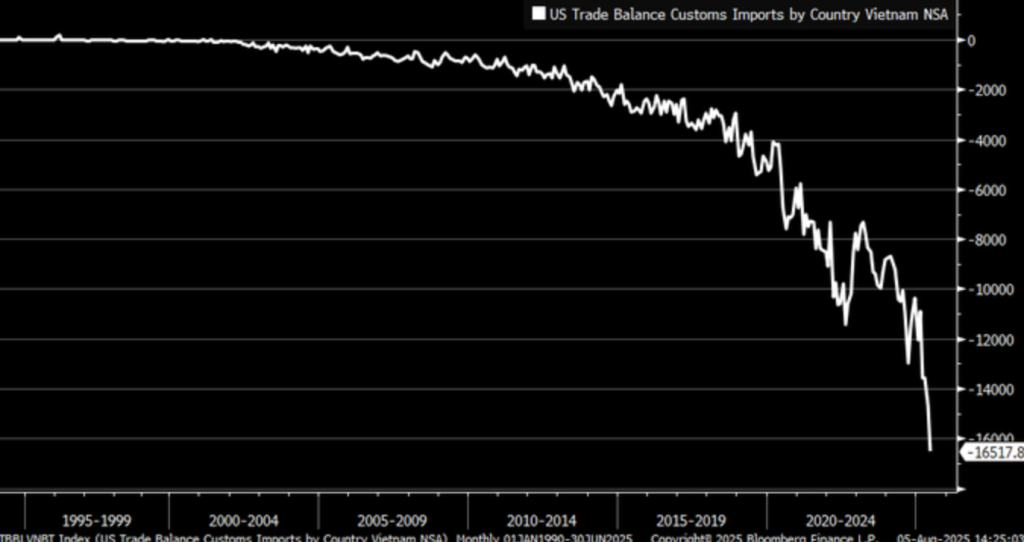

Vietnam Trade Gap Surges As Supply Chains Dodge Tariff Walls

We are observing a structual deficit of relevance with the U.S./Vietnam trade deficit increasing by the largest amount on record, to -$12 billion for the June 2025 period. This decrease is a part of a broader supply chain redirection where Vietnam plays a major transshipment point for reoriented Chinese export flows. Vietnamese imports have increased with 2024 levels at $136.6 billion, therefore the deficit in trade is a consequence of geopolitical engineering rather than Vietnamese organic growth in manufacturing.

Our assessment is not inconsistent with the argument that the U.S.-Vietnam corridor has been taking in bypassed trade flows, possibly in a pattern at odds with China-facing regimes of tariffs. Up to 16% of Vietnam’s U.S.-bound exports can be Chinese-origin goods, evidence shows. The new agreement between the U.S.-Vietnam subjects a 20% base rate with high 40% penalty transshipments in an effort at crushing circumvention. But whether the effort will be effective is doubtful asstructural trade deficits continue to grow—something which could suggest these policies amount to window dressing rather than corrective.

Here, FedEx (FDX) seems cheap precisely where intercontinental shipping lanes realign in meeting changing trade agreements. Its Southeast Asian logistics segment sets it up for taking advantage of expanding volume and enforcement-driven rerouting. Container traffic data, Vietnamese import composition, and customs enforcement data should be kept in focus for indications of whether U.S.-enforced trade is winning—or rerouting procedures become standard with more complex trade terms.

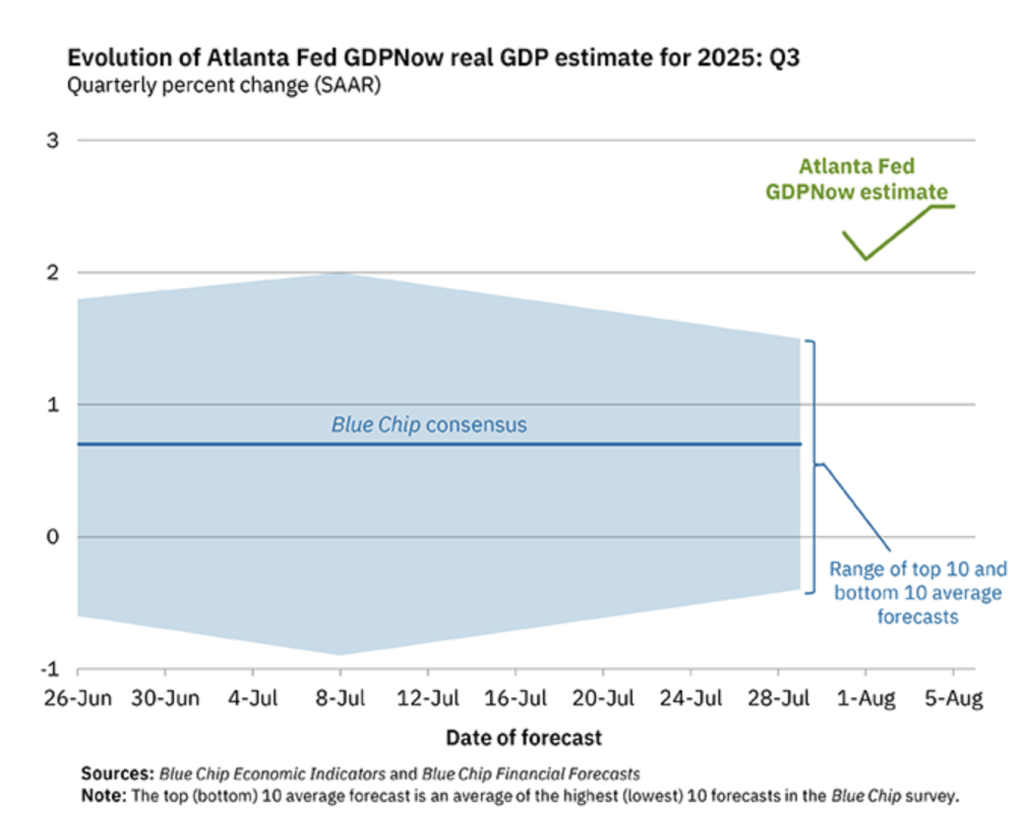

Growth Surprise: Atlanta Fed Model Defies Soft Landing Expectations

We are observing great divergence for the economic predictions with Atlanta Fed’s GDPNow gauge forecasting 2.5% Q3 2025 U.S. GDP growth—a very large increase over the Blue Chip median of about 1%. This current-time estimate with 13 subcategories like consumer spending, spending on investment, and balances of commerce demonstrates better health for the economy than foreseen with a decline global pattern. This kind of divergence is quite acute, more significant with European economies flat or limited growth wise, which more significantly increases a U.S. outperformance theme.

Forecast dispersion is also increasing very fast, with the gap between the high 10th and low 10th of economist forecasts widening by the first week of August. This type of gap in the past has been a signal for caution prior to large data reversions or business cycle turns occur. This type of very high reading for GDPNow defies the likelihood of the very popularized “soft landing” thesis even more because the underlying fundamentals-assumed consumer strength and policy-augmented demand-themselves are signaling an aggressive growth more than previously anticipated.

With this deviation existing, Walmart (WMT) appears undervalued relative to its potential upside. As consumer spending remains robust, a disproportionately favorable positioning for Walmart exists in essentials along with discount retailing. Retailers’ subsequent sales reports along with core PCE numbers should be carefully noted for confirmation of sustained strength in levels of demand. Detail breakdowns of GDP subcomponents, particularly inventories along with net exports, can help identify whether the same is being broad-based or policy-biased.

Service Sector Inflation Overshooting Economic Momentum

We see growing divergence for the U.S. services economy with the decline of the ISM Services PMI but a string of increasing rises for service prices, a divergence not seen since 2008 at the height of the financial panic. A look at the CPI Urban Consumers Services Less Energy Services index reveals inflationary pressure for the services economy isn’t falling relative to the level of overall economic activity. This divergence indicates inflation can potentially be sustained even with falling demand—a situation presenting a challenge for the dual mandate of the Federal Reserve.

In the past, such related phenomena have been succeeded by instability, and service inflation outbreaks have endured across slumps. The latest divergence bespeaks the possibility that monetary policy is perhaps too rough an instrument for non-cyclical supply-side induced inflation. The 2023 NBER findings reinforce this suspicion, attributing entrenched price increases in the service sector to supply chain inflexibilities rather than consumer appetite. When labour markets begin decelerating from an initial phase, service-inflation with such an origin can become a policy trap—contracting to fragility or relaxing to inflation.

Here, American Airlines Group (AAL) appears to be underpriced. As prices for service rise, restructuring-facilitated lean operations and pricing power create upside momentum within an inflation-sticky, low-demand recovery environment. Future ISM releases and employment cost indexes must be watched for signs of additional decouplings between expansion and service inflation to gauge implications of similar decouplings for other types of inflation. Supply shortages instead of demand may chart inflation patterns over the coming months.

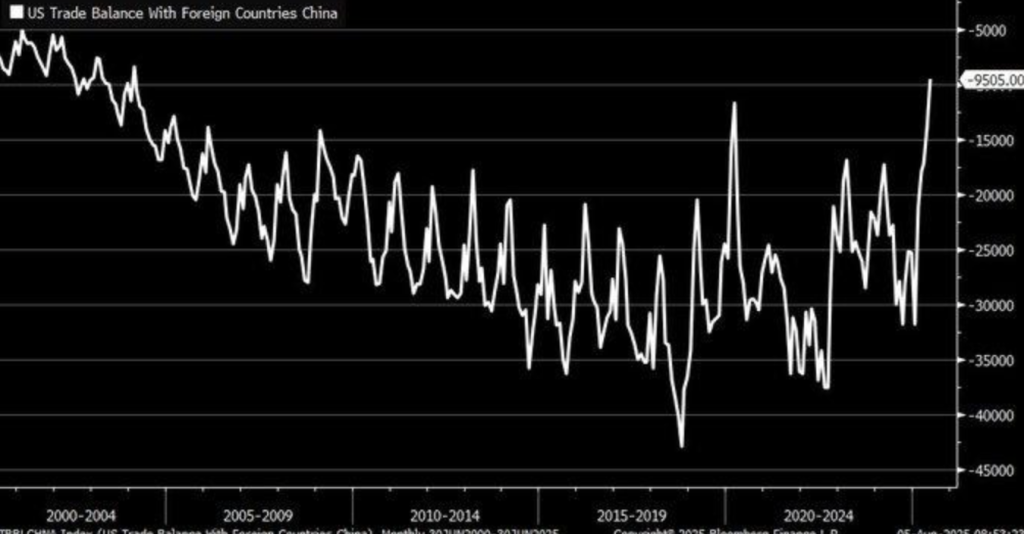

China Trade Gap Narrows, But Deficit Persists Through Shifted Supply Routes

We see a significant indicator because the US-China deficit drops to a low since February 2004 with a 5.7% increase in the overall trade deficit of goods in 2024 to $295.5 billion. It reflects a trend towards reorganization within a slowdown instead of a slowdown per se—custom intervention maybe stemmed direct China imports but reorganization of international trade reveals the same commodities coming in through other avenues but mostly Southeast Asia.

While the tariffs instituted since 2018 are accountable for a marginal 1.4% year-over-year decrease in direct China imports, the persistence of the deficit overall deflates the case for tariffs alone being accountable for reengineering trade deficits. Historical context indicates the previously similar decline in the China deficit after China’s accession to the WTO and subsequent escalation of export activity. This fall now is less a change in the structure of U.S. trade design than a strategic avoidance of tariffs upfront through transshipments through region’s allies.

Compared to such variable commerce map, Union Pacific Corporation (UNP) appears undervalued against its position in hauling freight to the interior and intermodal logistics. Need for perpetual merchandise movement—irrespective of origination—creates for growth in transitional supply chain reconfigurations. Shareholders are able to observe customs harmonization classification changes, Asian port volumes, and U.S. logistics demand shifts with a view to gauging whether policy triggers re-balancing—or relocations.

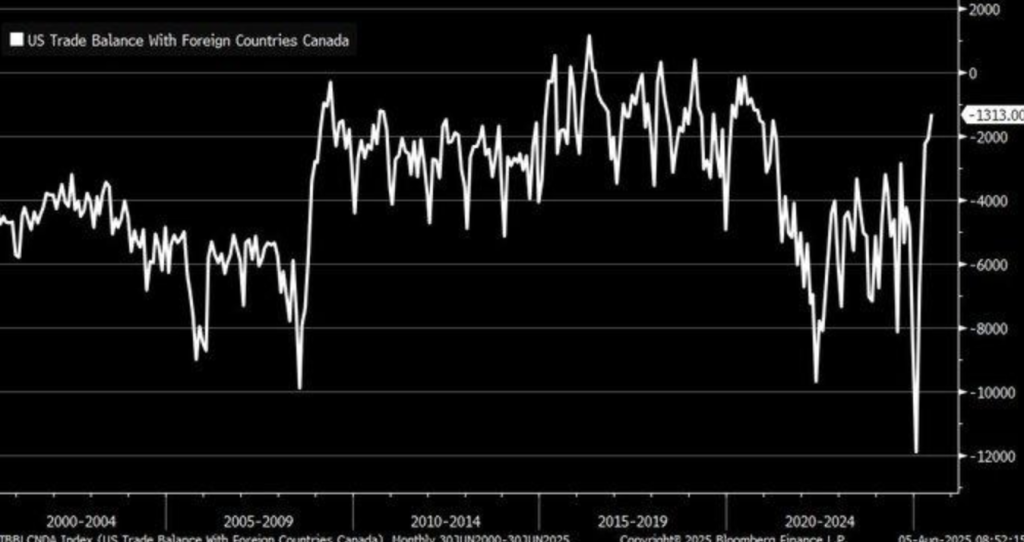

U.S.-Canada Trade Deficit Shrinks Amid Energy Realignment And Regional Shift

We observe a large trade reshuffling between North America with the U.S.-Canada trade deficit decreasing to approximately -$11.1 billion in July 2025—the October 2020 low. This 75% decrease from an estimated $45 billion in 2024 signals energy imports decreasing according to evolving supply chain rules. This trade reshuffling seems linked with decreasing oil prices as well as decreasing energy hunger, an historical U.S.-Canada trade driver.

De-globalization trends are also informing the shift. As American companies concentrate on regional value chains, the U.S.-Canada corridor has seen increased nearshoring along with decreased dependence on problematic transnational counterparts. This redefines North American integration and bucks long-term structural trade deficit expectations with principal allies itself. This kind of re-alignment of bilateral flows gets a boost from the recent softening of energy markets since 2023.

In this background, Enbridge Inc. (ENB) comes across as being undervalued. One of North America’s energy transport leaders, the infrastructure contributes to keeping regional energy commerce at moderate levels even beyond volume-decreasing phases. Investors would need to look at future energy inventory reports, transboundary pipeline levels along with reconfigurations of trade data in order to know more regarding whether this closing deficit is transitory or a continental trade policy change worthy indicator.

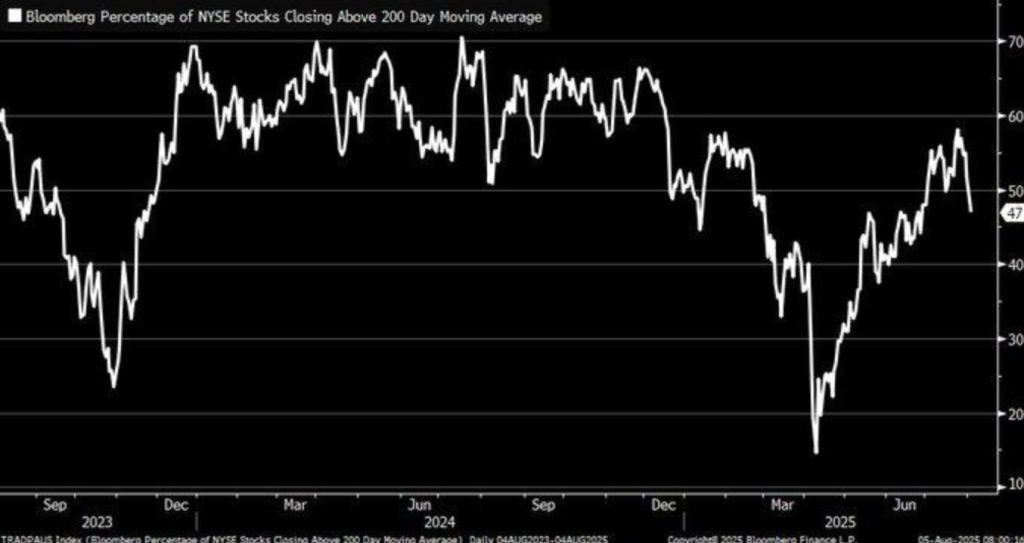

Market Breadth Narrows As Technical Signals Warn Of Underlying Fragility

We can gauge important equity market breadth weakening with a relatively modest 47% of stocks on the NYSE trading below their 200-day moving average on August 5 from a high of over 60% earlier in the year. This technical correction is a sign of waning momentum across the board and caution signs because historically these types of corrections have been followed by more significant corrections. This 200-day moving average is a sentiment indicator—a swift move below this line has been a signal of systemic revaluation of risk.

Breadth divergence is a major red flag, particularly where major indexes are solid but underlying participation is deteriorating. Research confirms bull markets powered by smaller sets of stocks pose a higher probability of a turn around. Making this vulnerability even more concerning is an aftershock effect of a recent disruption of the NYSE in the month of July which cleared but highlighted vulnerability within market structure at a point of heightened investor hypersensitivity. Coupled with global economic uncertainty, these technical indications point to escalating downside pressure.

With the background technically, SPDR S&P MidCap 400 ETF Trust (MDY) appears undervalued. Mid-caps trailing behind in breadth shedding but offer big potential for a bounce if breadth bottoms out in markets. Traders would be watching a continuation within breadth ratios, volatility indexes, along with sector leadership rotation moves for a sign about whether this is a constructive consolidation—a precursor for a more significant market correction.

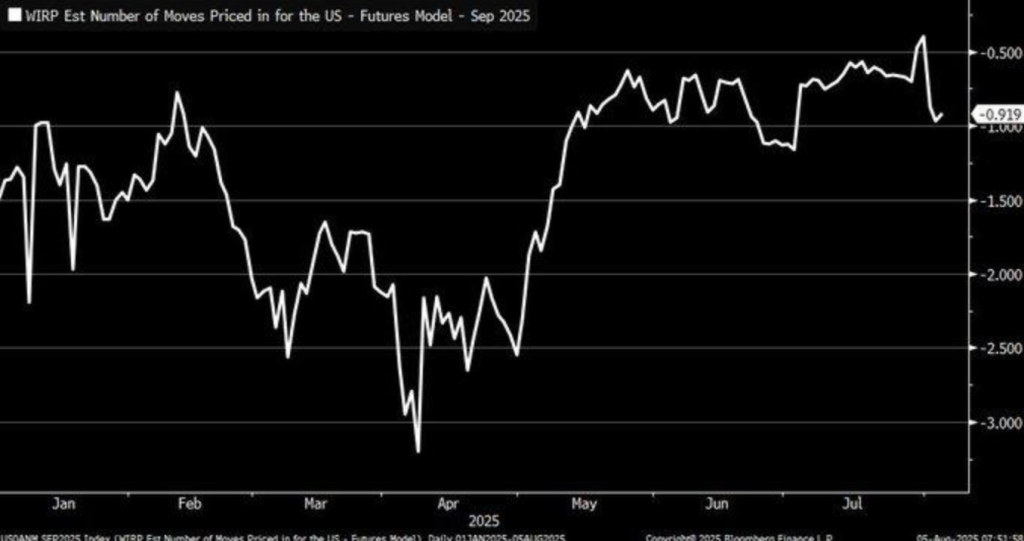

Rate-Cut Betting Eases As Futures Realign With Recession Signals

We see a re-calibration of rate expectation with U.S. futures markets now aiming for less in Federal Reserve easing than previously expected—reversing levels a month ago running as far out as August 2025. This re-balancing comes in the aftermath of dovish commentary along with weak labour data, which saw a worst-ever ADP employment report since March 2023. Reversion in markets from extreme easing calls is a sign of concern over the health of the recovery thesis for the economy.

Futur-implied odds now lean towards a 22% probability of a 50-basis-point cut in September. This reversal leans towards growing skepticism about Fed policy with signs of recession picking up over inflation alert. Looking at the past lends support to futures being worthy indicators of policy shifts once tempered with low non-farm payrolls. This conundrum between market pricing and weak macro fundamentals stokes questions over sustainability in present valuations across risk assets.

Here, Citigroup Inc. (C) seems underpriced here. As rate hopes fade, financials get hurt with margin squeeze but with Citigroup’s universal footprint and rate-sensitive product mix there can be a buffer possible. We will be keeping a very close eye on labour market rewrites, consumer credit, and Fed meeting minutes for a better gauge of how far recession expectation is shifting rate path assumptions.

Upcoming Economic Events

Quiet for Now, But Tomorrow’s Impetus Expands

Today’s economic calendar sees very few market-mover releases, which provide investors with a small amount of breathing room after a week of policy changes in monetary policy and mixed trade directions. But don’t confuse this breathing room with stability. While there’s no significant releases scheduled for today, market watchers are using this small moment of opportunity for a reset heading into the more significant indicator releases tomorrow.

We now turn to the fresh data set this Wednesday that can re-set expectations for levels of interest rates, inflation orientation, and industrial activity. Emerging at a time when macroeconomic tensions are still mounting—from labour markets imbalances to shifting trends of world trade flows—every data point matters.

We recommend waiting until tomorrow’s releases, when they may more clearly show whether the U.S. economy is on a path to soft landing—or continuing into contraction. Markets will react quickly, with rate-sensitive sectors, currency markets, and bond yields all set to react.

Earnings

Earnings Recap – August 5, 2025

- Advanced Micro Devices Inc. (AMD)

AMD posted second-quarter revenue of $7.7 billion, surpassing expectations driven by strength in its data center segment, which rose 14% year-over-year to $3.2 billion. Despite meeting EPS expectations at $0.48, the stock faced modest pressure as margins tightened due to elevated AI infrastructure investment. While the headline beat was encouraging, investor enthusiasm had already been priced in, prompting a muted post-report reaction.

- Caterpillar Inc. (CAT)

Caterpillar missed estimates as macro headwinds and tariff-related costs weighed on international demand, particularly in Asia. Though North American infrastructure projects provided support, order intake showed signs of deceleration. Markets responded cautiously, reflecting broader concerns about cyclicality and slowing global equipment sales.

- Amgen Inc. (AMGN)

Amgen delivered steady results with flat revenue growth, supported by new product uptake in oncology and inflammation. Despite ongoing biosimilar pressures, the company reaffirmed full-year guidance. Investors viewed the report as stable, with slight gains on confidence in its late-stage pipeline development and portfolio execution.

- Arista Networks Inc. (ANET)

While detailed reporting was limited, ANET’s consensus estimates pointed to strength in cloud and enterprise networking demand. With anticipated EPS near $0.65, investors are likely weighing expansion in AI infrastructure demand against margin sustainability in a competitive environment.

- Eaton Corporation PLC (ETN)

Eaton’s results were expected to be strong, with an EPS estimate of approximately $2.93. Market anticipation centered on backlog conversion in electrification and aerospace segments. Investor focus remained on forward guidance, as momentum in industrial demand remains a key valuation anchor.

- Fidelity National Information Services Inc. (FIS)

FIS disappointed on earnings, weighed down by delayed client rollouts in banking tech solutions. However, the merchant solutions division showed resilience, offering a partial offset. The stock came under pressure post-earnings as investors reassessed the pace of its recovery and margin trajectory.

Earnings Preview – August 6, 2025

- McDonald’s Corporation (MCD)

McDonald’s is projected to deliver Q2 EPS of $3.14 with revenue near $6.7 billion, driven by menu innovation and digital expansion. Investors will be focused on same-store sales growth, expected around 2.6%, and whether recent promotions have succeeded in countering inflation-driven traffic softness. Commentary on international performance and loyalty app adoption will be key catalysts for market reaction.

- The Walt Disney Company (DIS)

Disney’s earnings will be dissected for updates on streaming profitability, theme park margins, and developments around ESPN’s strategic future. Investors are also watching closely for cost-cutting execution and any clarity on studio output disruptions. Sentiment hinges on improving fundamentals in its direct-to-consumer segment.

- Uber Technologies Inc. (UBER)

Uber’s Q2 results are expected to highlight ride-hailing growth and margin expansion in delivery. Markets will scrutinise whether demand trends hold amid slowing consumer discretionary spending. Updates on Uber One subscription growth and mobility platform integrations will influence forward guidance expectations.

- Shopify Inc. (SHOP)

All eyes are on Shopify’s ability to sustain e-commerce momentum, with particular focus on subscription solutions and merchant services growth. Investor attention will also be on profitability metrics and whether elevated customer acquisition costs are being contained.

- AppLovin Corporation (APP)

AppLovin’s focus will be on mobile ad platform monetisation, especially on the demand-side network. With digital ad budgets still under scrutiny, investors will look for stable CPM growth and expanded partnerships to justify valuation multiples.

- Airbnb Inc. (ABNB)

Airbnb’s results will be dissected for insights into summer travel trends, booking strength, and host growth. Regulatory risks in major markets and updates on platform safety reforms will also factor into investor sentiment. Forward bookings and occupancy rates will be key indicators of momentum.

- Coca-Cola Euro-pacific Partners PLC (CCEP)

Currency headwinds and pricing dynamics across Europe will be in focus. Volume growth and regional sales composition will help determine if the company can maintain margin stability in an uncertain macro environment. Investor focus remains on cost discipline and product mix.

- Joby Aviation Inc. (JOBY)

As a pre-revenue company, investor interest will be on progress toward FAA certification and production milestones for its electric aircraft. Commentary on partnerships, commercial launch timelines, and government engagement will shape valuation sentiment.

- New York Times Company (NYT)

NYT’s report will be evaluated for digital subscriber growth, advertising recovery, and cost containment. Investors are particularly attentive to churn trends and the monetisation pace of newer content verticals. The outlook for Q3 media spend will likely steer market reaction.

- Blackstone Secured Lending Fund (BXSL)

BXSL’s loan portfolio will be reviewed for non-performing asset trends amid tightening credit. Interest rate sensitivity and updates on new originations will drive investor interest. Market focus will be on net investment income and commentary on portfolio health.

- Wix.com Ltd. (WIX)

Wix will be watched for updates on user growth, ARPU trends, and churn management. With competition heating up in the website-builder space, innovation in AI integration and customer retention strategies will be key for sustaining forward growth.

Stock Market Recap – August 6th, 2025

US shares commenced trading in a risk-averse mood today with investors hedging against increased trade tension from geopolitical origins and Fed remarks driven by expectations to boot. A sudden zig for semiconductor shares marked the beginning of the day’s most significant action with mega-cap technology again disappointing and cooling general market sentiment. In this context, concerns about the global economy and trade policy uncertainty dimmed investor expectations further.

Stock Prices

Economic Factors And Shift in Geopolitics

Markets responded negatively to fresh presidential threats of possible new chip import tariffs—a move which caught chip stocks off guard and a concern about rising trade tension. Meanwhile, weak manufacturing and labour hold near-term growth prospects in check, which contributes to speculation about a more tentative Fed approach towards rate easing. Sentiment for investors remains poor with heightened macro uncertainty.

Breaking Stock News:

Nvidia, Broadcom Fall Heavily Due to Donald Trump Tariffs That Happen

Semiconductor shares such as Broadcom Inc dropped following a tweet by President Trump announcing new tariffs this week in an attempt to increase chip production in America. That knocked the Philadelphia Semiconductor Index (SOX) off 1.1%, with the iShares Semiconductor (SOXX) down 0.7%. These shares were previously leading the SOX’s 11.7% year-to-date gain, and the unexpected change in expectation about trade policy sent a shiver down the tech sector’s spine.

The Magnificent Seven Plus S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet and Tesla—are exerting a large weight on the S&P 500 with AI-fueled growth sentiment deflating. 18%-plus retracements on averages off highs, the aggregation sellback in this select group—led by Nvidia—has had a large weight on the index. Index-level advances won’t resume durably without a stabilizing action in leadership.

Major Index Performance on Wednesday, August 6th 2025

- S&P 500: 5,829.41, down 0.3%, dragged lower by technology weakness.

- Nasdaq Composite: 18,106.55, -0.5%, as losses in semiconductors deepen.

- Dow Jones Industrial Average: Remains steady at 41,185.77, supported by industrial stocks and energy stocks.

- Russell 2000: Down 0.2% at 2,143.08, as small-caps react negatively to rate sensitivity and weak

We stay wary of sector turns and breadth indicators across the board in the market. Earnings season began and macro risk is high, which calls for a lean towards cash-flow strength stocks with operating earnings strength and pricing power. Position is defensive and select across the board until mega-cap leadership is firm and breadth improves.

Gold Price – 6th August 2025

Spot gold is at $3,381.10 an ounce, staying solid ground even amid an increasingly treacherous political climate. There being no actual economic data today has attracted investor attention solely towards politics with specific attention being directed towards President Trump’s overall remarks. Trump’s sacking of BLS chief, allegations of “rigged” labour data, threats of imposing major tariffs on India and the EU, and attacking the independence of the Federal Reserve have created market uncertainty. These acts and indications towards a dovish turn about for the Fed about institutional restructuring have driven investors towards gold for a safe-haven hedge. In a world where faith towards traditional indications from the economy is fast disappearing, gold’s non-yielding and inflation-hedged nature becomes more enticing.

In a directionless day for today’s non-firm data, sentiment remains constructed on yesterday’s breakdown in suspect labour stats. Loss of confidence in statistical integrity and policy direction is building a defensive booking across portfolios, which is fueling interest in hard assets such as gold. Zaye Capital Markets’ opinion is our bullish reason for gold’s action above $3,380 is a macro-stability anchor story piece. Together with escalation moves in tariffs, potential instability at the global central banks, fault lines in the geopolitics being stretched out, gold should maintain a bull firm bid formation at our estimate pending institutional credibility erosion for potential volatility continuation into the second half of Q3.

Oil Prices Wednesday, August 6 2025

Brent is $67.93 per barrel with WTI at about $65.44, a tad firmer for the day with markets reacting to fresh geopolitical tension along with mixed supply-demand indications. It regained recent lows after an OPEC+ pledge to increase 547,000 barrels per day of supply in September starting amid concerns about possible oversupply. But uncertainty still surrounds alliance’s ability to produce such a quantity. Meanwhile, even more caution has been brought about in the oil market with the IEA fresh world demand forecast—a reduction for 2025 for a small 730,000 b/d rise—to 730,000 b/d growth. But smaller U.S.-based inventories along with near-term Middle East risk premiums are operating together to maintain prices at or near $65 levels.

Volatility is being fanned by remarks of President Trump. Threats of placing large tariffs on India for re-exporting Russian oil have encouraged concern for possible trade dislocation in global flows of crude oil in favor of a soft risk premium. Underpinnings for allegations of manipulated labor data and of taking a swipe at the Federal Reserve have powered macro uncertainty in the meantime. No significant economy data are released today, so sentiment keeps being dictated today by these political bombshell headlines and the disappointing jobs report yesterday which derailed growth mania and raised questions about possible energy appetite. In our view at Zaye Capital Markets, the conflict between easing calls for near-term oil markets’ forecasts for demand will be oil’s near-term path defining characteristic, keeping it within a trading band barring policy shift or supply shock tipping the balance.

Bitcoin Price – Wednesday, August 6, 2025

Bitcoin is maintaining levels of $113,588 at present levels and remaining resolute against rising political uncertainty along with a changing regulatory landscape. SEC and CFTC’s latest appeals to enable spot trading of crypto on registered and regulated platforms have assisted in legitimizing the asset class, which in turn pushes institutional onboarding upwards even more. Hedge funds such as Fasanara Digital and Edge Capital remain outperformers with heightened confidence towards digitization of asset exposure. Market experts remain bullish about any correction over $100K being a bullish signal favoring Bitcoin’s long-term structural uptrend. Maintaining levels over $113K even with near-term volatility shows a sign of confidence in markets for Bitcoin as a new asset class amidst macro uncertainty.

President Trump’s aggressive rhetoric—from the dismissal of the BLS director and shaming labor data integrity to threatening enormous tariffs on India and the EU—has engendered a wider sense of distrust of traditional institutionality. This political debacle and the Fed’s autonomy issues are underpinning Bitcoin’s appeal as a decentralized policy risk hedge. Yesterday’s doctored labour data scare amplified investor fear, which is bolstering Bitcoin’s store of value image with institutional credibility issues on investors’ agendas. Without big economics data today, eyes are on recent politics and the evolving money terrain. Bitcoin’s present consolidation is perceived in Zaye Capital Markets’ opinion as a build towards more dependence on decentralized financial vehicle’s in the environment of institutional and geo-political uncertainty.

ETH Prices – Wednesday, August 6th 2025

Ethereum is currently at $3,580, still hovering high against murky market conditions with cross-currents to the ETFs. August 1 does mark the first 20-session net outflow day—losing an estimated $152 million—but institutional appetite remains. Last month alone over $5.4 billion witnessed Ethereum spot ETFs making gains with BlackRock’s ETHA accumulating $9.74 billion and holding a staggering 78% of the overall ETF market share. This sequential large institutional demand has been countered with whale action like a_record-large $300 million ETH purchase through Galaxy Digital representing continued belief in short- to longer-term worth of Ethereum. Speculators increasingly now expect ETH hitting a test of the $6,000 level by year-end pending market stability with additional institutional flows.

In keeping with disruptive policy rhetoric from President Trump—challenging the validity of economic data as well as menacing with dangerous trade war—is accelerating decentralized asset demand. Best positioned for the same stands Ethereum with investor skepticism in traditional institutions coupled with fiat policy protectionism. Without significant major economic data on the schedule for the day, market participants look to political activity coupled with capital flows for a signal. In our view in Zaye Capital Markets, ETH consolidation at the $3,500 region indicates macro hedge positioning coupled with robust ecosystem conviction underpinned with increasing ETF entry coupled with strategic whale buys. All this puts Ethereum a top institutional digital asset for trading through volatility coupled with positioning for integration over the longer term with decentralized finance.