Where Are Markets Today?

Global equity futures are pleasantly in the green this morning, with S&P 500 futures higher 0.94%, Nasdaq 100 futures higher 1.34%, and Dow Jones futures higher 132 points, or 0.3%. European futures also higher on last night’s U.S. tech gains and news of fading global trade tensions. Market participant response to the well-received news follows on the heels of the good news from the Microsoft and Meta Platforms earnings and the report from President Trump on trade revealing agreement reached with South Korea making the import tariffs 15%—down from the previously threatened 25%. This double catalyst of earnings strength and political easing is driving the futures higher on two continents.

U.S. tech progress is being spearheaded by entrenched “Magnificent Seven” members Microsoft and Meta, which gained 8% and 11% in after-hours trading. Microsoft’s Azure cloud unit surpassed the $75 billion annual revenue run rate and posted its all-time best cloud growth, and Meta posted higher-than-estimated third-quarter sales projections. These report numbers have soothed investor fears that cloud-driven innovation and the AI world continue to fuel leading-line growth in the world of mega-cap tech. With such players driving much of index weightings, resulting post-earnings strength is driving overall sentiment and support for the health of the tech world. As well as the earning excitement, the geopolitical concern is easing slightly. Trump’s last-minute move to lift South Korean tariffs to 15% from the 25% previously threatened has allayed trade-sensitive industries. The last-minute move on the much-hyped August 1 tariffs deadline is seen as a tactical reevaluation of not bringing critical supply chains into play. The move comes on the heels of reports the White House is optimistic on trade negotiating on China. The moves indicate market-friendly pragmatism is resurgent in U.S. trade policy and checking near-term geopolitical risk premia.

With futures in a bull trend of euphoria, the releases later today—headlined by Core PCE, the Employment Cost Index, the German CPI, and weekly jobless claims—will be the determiners of the next price action leg. Above-market inflation or wages have the potential to suffocate the existing risk appetite against the backdrop of fear the Fed will not deviate from its hawkish path. Soft prints will be able to prolong the existing rally on the back of further hopes of stability or even the relaxation of policy. Our forecast at Zaye Capital Markets is that the trading today will be the precursor to the all-critical next Friday tariff deadline and month-end flows and will be guided on two channels mainly—earnings and macroeconomic data.

Major Index Performance as of July 31, 2025

- S&P 500: Currently trading at 5,841.52 and down 0.4

- Nasdaq Composite: 18,220.78, down 0.6%, pulled lower by tech weakness.

- Dow Jones Industrial Average Advanced 0.2% to 41,182.34 on the back of gains in energy and financials.

- Russell 2000: Holding steady at 2,147.63, retreating from rate sensitivity in the small caps.

The Magnificent Seven and the S&P 500 Index

Despite on-time gains from a series of large-cap counters, the so-called “Magnificent Seven” of Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla are looking spent. The latest sector snapshot indicates the group has collectively shed more than 18% from recent highs, with the leaders in the pack being Tesla and Meta. This is a bout of valuation re-balancing, particularly from the AI-fueled growth narratives that have gotten too far ahead of fundamentals.

S&P 500 is still soft as the leadership of the tech weakens. Despite the support of the energy and industrials, the index would not have a big rally without again encountering the active participation of its key mega-cap leaders.

Drivers Behind the Market Movement

This is the accurate listing of the current top 3 drivers of the U.S. and European market:

1. Tech Earnings Momentum

Microsoft and Meta’s solid Q2 reports have raised a U.S. and European futures rally. Microsoft reported over $75 billion annually in sales at its Azure unit and Meta provided a brighter-than-expected sales forecast for Q3. Each surged after quarterly earnings reports 8% and 11% respectively and lifted market hopes for ongoing growth driven by the cloud and artificial intelligence. These reports have allayed the market’s concerns and provided underlying support through more universal equity indexes.

2. Trade Policy Tensions & Resolutions

President Trump’s new trade policy has given a boost to market confidence. The settlement of the 15% tariffs on the previously threatened 25% allayed the possibility of expanding trade sanctions. The same percentage on the EU soothed the waters further. But the market remains vigilant for the administration’s renewed efforts on the August 1 deadline on tariffs on Indian and copper-linked articles. Even as some settlement remains on the cards, indecision on India and Brazil continues to dent investor confidence.

3. Macro Data and Central Bank Signaling

Recent numbers such as healthier Q2 GDP growth in the U.S., robust payroll cost data and persistent inflation pressures also fueled declining hopes of September rate cut. The rate moves of the Federal Reserve to keep rates steady despite Trump’s loud calls for rate cuts further suggest its caution. Market observers anticipate releases such as Core PCE, German CPI and U.S. jobless claims next for more information on the direction of the Fed and inflationary direction.

Zaye Capital Markets foresees that resilience in the today’s market would be driven by the combination of optimistic earnings enthusiasm, rational trade policy results, and prudent monetary positioning. All of them combined direct the attention of the investors on the point of whether the economic information still maintains the trend or provides some volatility.

Digesting Economic Data

The TRUMP Tweets and Their Implications

President Trump’s newest spurt of comments, executive orders, and trade pronouncements shook financial markets to the core with implications well beyond political theater. Whether it is reaffirming the August 1 deadline for tariffs or vituperating the Federal Reserve out-and-out, Trump has redrafted the near-term macro landscape in effect. Announcing August 1 to be a “Great Day for America,” the President framed the prospect of a hard-hitting trade about-turn aimed directly and exclusively on India with 25% sanctions, 15% duty on South Korean exports, and 50% duty on copper—and literally excluding raw material inputs. The pronouncements come amidst rising trade deal-making and creating a chaotic world trade landscape just as the specter of inflation remains.

With his calls for rate cuts in his monetary policy, Trump doubled down on his public lobbying the Fed to cut rates even as the Fed was steadfast in our previous decision. His unmistakable political pressure injects volatility into a tense monetary context and risks central banking independence and stability in its policies. Concurrently the White House released its report on crypto policy advocating regulatory certainty—a report mercifully mum on the issue of Bitcoin reserves and international reserves invested in the digital unit—underscoring the administration’s indecision. Even as the administration refers to the Fed’s independence and adherence to the same, the White House economic commentary links the revenue from the tariffs directly to the reduction of the deficit and continues to blur the line between fiscal and monetary strategy. Other than the economic inputs, Trump’s moves to skirt the FDA on ousting vaccine regulator Vinay Prasad and hinting over the deal of $500 million with Harvard only add more fuel on the specter of executive overreach. The moves contribute further legal and policy volatility the market must process. Additionally, the internal narrative reset on the White House over the diversion of focus over the backlash over Epstein—presumably to take a break and gather pace before the August 1 deadline on tariffs—registers the distraction and gathering-momentum political gesture. The time and the tone of the moves themselves throw warning flags to the investor community who most respond to regulation intervention and political news.

These moves we view as a coordinaed attempt to construct policy primacy before the tariff launches later this week and potentially influence bond yields, volatility in equity marketplaces, and safety flows. The risks two-sided: near-term risk premia in geopolitically vulnerable commodities and FX marketplaces may increase as the credulity of U.S. monetary policy is questioned anew. That Trump continues to muddy the waters about trade, regulation, and political oratory leads us to recommend a defensive and flexible paradigm of portfolio positioning in order to offset headline-sensitive flows expected over the coming days.

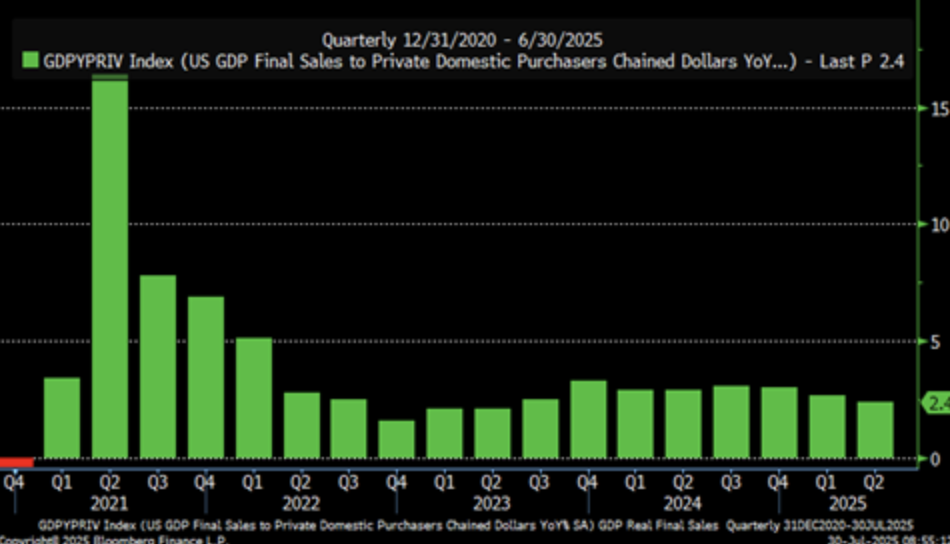

Production Outpacing Consumption: Is GDP Growth Misleading?

Q2 2025 GDP growth upgraded to 3.0% annualised well above consensus. But underlying the headline is a less rosy trend—Personal consumption growth plunged to 1.4%, while real sales to domestic end-buyers from end of production and inventories surged 2.4%. That change implies an increasingly supply and inventories restocking-driven rather than optimistic consumer spending-led economy. That discrepancy makes us wonder about the supportive growth prospects in the context of the ongoing consumer retrenchment in the face of inflation stickiness and credit wear.

Atlanta Fed’s GDPNow forecast, recasting Q2 growth to 2.9% last July 29th, exhibits the same structural profile: combinatory pressure motivated more by supply-side recovery and inventories building up than genuine demand strength. BEA goverment-purchase-adjusted final sales reinforces the argument that internal demand is still not capable of matching production—a warning indicator that must be monitored in evaluating healthy top-line growth.

We believe the industry and logistics business enterprises are coming in on the cheap in these circumstances, and home-base supply chain-backed companies are most likely positioned to gain in the near future. Shareholders must look to future PCE and inventories reports to determine if the producer-driven trend continues or is a short-term cycle. Any lasting discrepancy between consumption and 1.5% GDP growth—academic research warns—can indicate a demand-driven slowdown on the horizon.

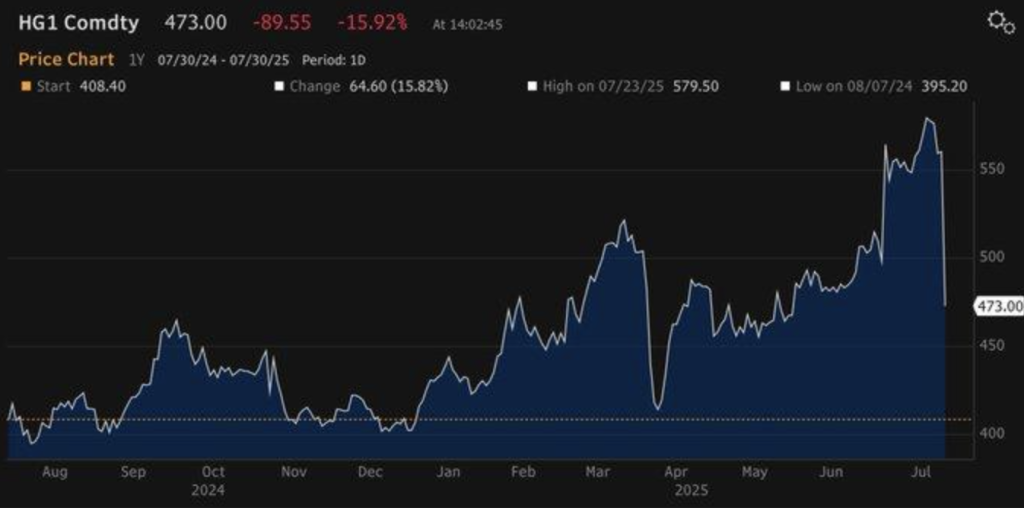

Copper Plunges 15% As Policy Reversal Rattles Metals Market

Copper fell 15.32% to $4.73 a pound on July 30, 2025, wiping out weeks of advance following the dramatic reversal of a 50% U.S. tariff on copper imports. The dramatic reversal dashed hopes for domestic premia and triggered a swift market response. The size of the sell-off—a parallel 18.38% decline on the spot market to $4.60—indicates more than recalibration; it is symptomatic of being over-sensitive to trade policy risk.

Structural demand for the metal remains intact even post-headline crash. For the forecasters, green infrastructure for clean sources of energy will drive demand for the metal 25% to 2025 and create a long-term basis for prices. History in the commodity market, such as the 2008 crash in the prices of the metal, suggests that once the market over-reacts rudely to radical policies then fundamentals reassert. This event seems no exception—temporary dislocation and not failure.

We find domestic recyclers and copper miners to be undervalued following this correction. These are the companies to benefit once copper global imbalances re-assert themselves. Chinese and European industrial order recovery indicators will be one thing that analysts will need to watch closely, traditionally correlated with the rebounds in the metal. Additional debate on the clear path of tariff policies will also be important in the short-term.

Pending Home Sales Drop As Strong Rates Weaken Demand Despite Healthy Inventory Supply

U.S. home market registered another fall in June 2025 as the Pending Home Sales Index decreased 0.8% from last month to stand at 72.0—at a near record low of 2001. Despite a 29% increase in supply over last year, stiffening mortgage rates averaging 6.82% have reduced affordability and dissuaded consumers from entering the market. The fall defied the 0.2% increase consensus forecast, providing further evidence that the monetary policy is still over-constricting the housing demand.

Even as regional marketplaces such as the Northeast posted modest increases, the home market continues to be stymied by the unaffordability, particularly the most threatened group of first-time home buyers who only accounted for 30% of sales last June. The average home price jumped 48% over five years away from the large pool of potential home buyers. The soft demand lifts the market from supply-low crisis scenario mode to pricey deadlock scenario mode, where sales growth is not greeted by supply growth.

Homebuilding supply companies and mortgage servicers look cheap, especially the most likely to gain in the future from rate reductions. Market players need to be versatile on the long-term yields and inflation measures. A cut in the mortgage rate to 6.0% as expected should significantly drive housing activity through 2026 under modelled assumptions of a 14% pending sales bounce based on a gain in affordability.

Tariff Escalation Targets India As Trade Deficit Widens

A 25% American duty on Indian importations beginning Aug. 1, 2025, is a radical shift in U.S. trade policy in an attempt to eliminate a $45.7 billion two-way trade deficit. It is the latest in a series of more generic rebalancings that have pushed U.S. average tariffs to 18.2%, the highest in nearly a century since pre-reciprocity times. The hike brings an end to decades of trade liberalization and rings a dissonant chord in the global supply chains and in investors’ minds.

India’s response thus far indicates retaliatory behavior on its part, and that would increase the risks to the downside of world growth. Economic theory and experience establish that tit-for-tat policy-making would shave off global GDP by 0.2% annually if retaliations are deep. Corporates relying on Indian raw materials and manufacturing goods could see cost pressures increase fast, especially among the pharmaceutical, textile, and IT hardware firms with insignificant supply diversification.

These American logistics companies with minimal Asia know-how are underpriced in the context of this evolving trade landscape. The export statistics post-August implementation must be tracked by the analysts, along with India’s retaliatory stance and cross-border procurement plan distortions. The breakdown in negotiations would most likely inject volatility into import-sensitive sectors and new market shares.

US Tariffs On India Signal Strategic Shift, Global Trade Risks Rise

Imposition of a 25% tariff on August 1, 2025, on Indian imports is an extreme measure in U.S. trade policy to keep the $45.7 billion trade deficit with India in check. The move is proof of an expansive policy approach that has raised the average U.S. tariff to 18.2%—its highest since the early 20th century. The move is an extreme departure from post-1934 tradition of tariff reciprocity and is raising structural questions on the long-term viability of multilateral trade cooperation.

India’s initial posturing on defending its interests poses the threat of retaliatory strike that would be disruptive to the crucial trade channels. Because all of the above industries like drug, chemicals, and electronics depend heavily on the bilateral trade, supply chains and input cost prices are now jeopardized. Prior modelling cautions that tit-for-tat tariff systems would decrease world GDP by 0.2% every year and contribute to a weak post-pandemic recovery outcome.

U.S. small-industrial stocks with minimal global exposure appear to us in this context as undervalued on the back of the potential domestic demand boost from tariff-assisted substitution. The forecasters need to be vigilant about the initial hints of margin squeeze from trade in the export policy of the U.S. and the input prices of the processing industry. Failure in trade talk has the potential to create fresh volatility in the global equity and currency marketplaces.

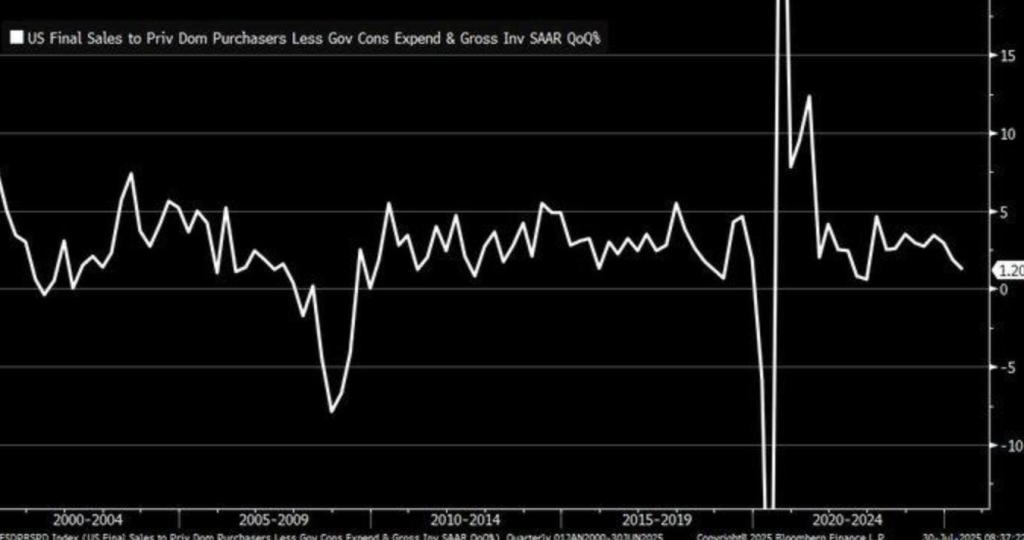

Demand Deceleration Raises Stagflation Concerns Despite GDP Growth

American economic growth actually further slows down in the background as last private domestic sales only grew 1.2% in Q2 2025—a dramatic flip from previous periods. This contrasts with the 3.0% top-line GDP growth and follows a Q1 decline of 0.5%, signs of a gap between aggregate production and true private demand. The flip implies most of the reported growth would be more likely the result of transitory retightening of inventories or consumption motivated by the state, and not the consumer spending.

Stagflation—troublesome inflation and weak growth—increasingly is the threat. Supply bottlenecks and trade friction in the form of higher tariffs are cost multipliers but deflate domestic demand in the worst-hit sectors—capital goods and consumer durables. The $109.6 billion drop in personal income for the month acts to reduce purchasing power and acts to highlight the reality that consumers are faced with rising restraints as prices are higher.

In this context, we think U.S. defensive shares—i.e., consumer staples and utilities—are cheap. Defensive shares offer coverage at the margin during weakness in growth and price pressures. The analysts have to remain vigilant on real income trends and policy signals from the Fed. In the event of monetary tightening against weakening demand, equity volatility could increase as the market re-evaluates growth projections.

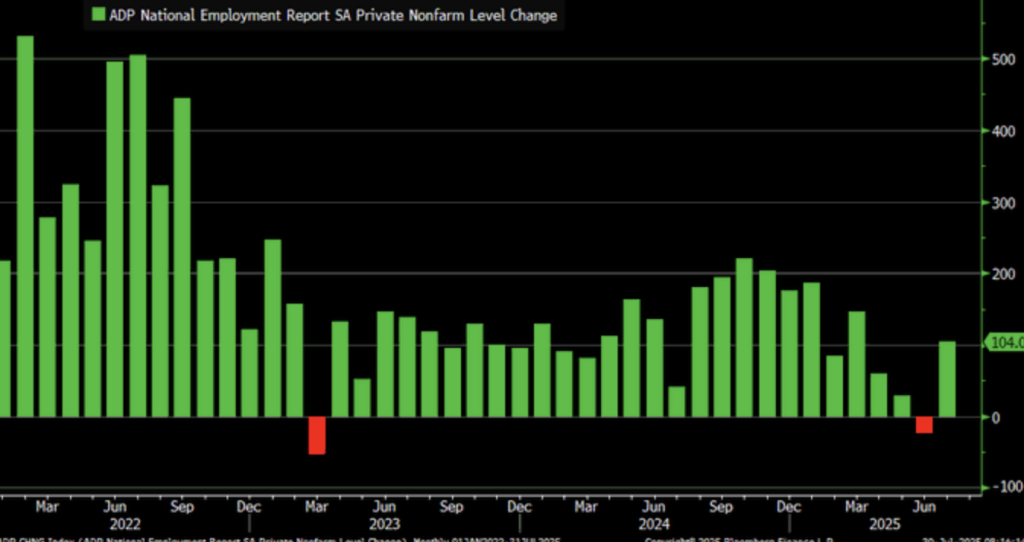

Private Payroll Surge Bodes Well For Job Market Despite Mixed Data

U.S. private payrolls increased 104,000 in July 2025 convincingly above market estimates of 76,000 and catching up for downward revised decline of 23,000 in June. The ADP National Employment Report data provides evidence of patchily resilient labour market on the whole. Advances in hospitality and financial services drove the gains and signal selective turnarounds in the style of digital economy themes.

So long as we are seeing volatility, the good shock resists stories of a weak labor market. The July rebound, combined with the less severe June contraction than initially estimated, is in sync with the possibility of underlying strength. Private sector payroll history is a leading indicator and, as history has indicated, precedes employer sentiment turning points ahead of overall economic indicator turning points. But discord among ADP and BLS readings warns analysis.

In undervalued names within the category, we highlight mid-cap staffing companies and payroll technology companies. Their models most stand to gain from sporadic recoveries in the hire, particularly the services component. The market awaits the next releases of the non-farm payrolls and wage growth numbers as a signal of convergence between datasets. Convergence between the two sets of datasets will offer support to a healthy macro labour case entering Q4.

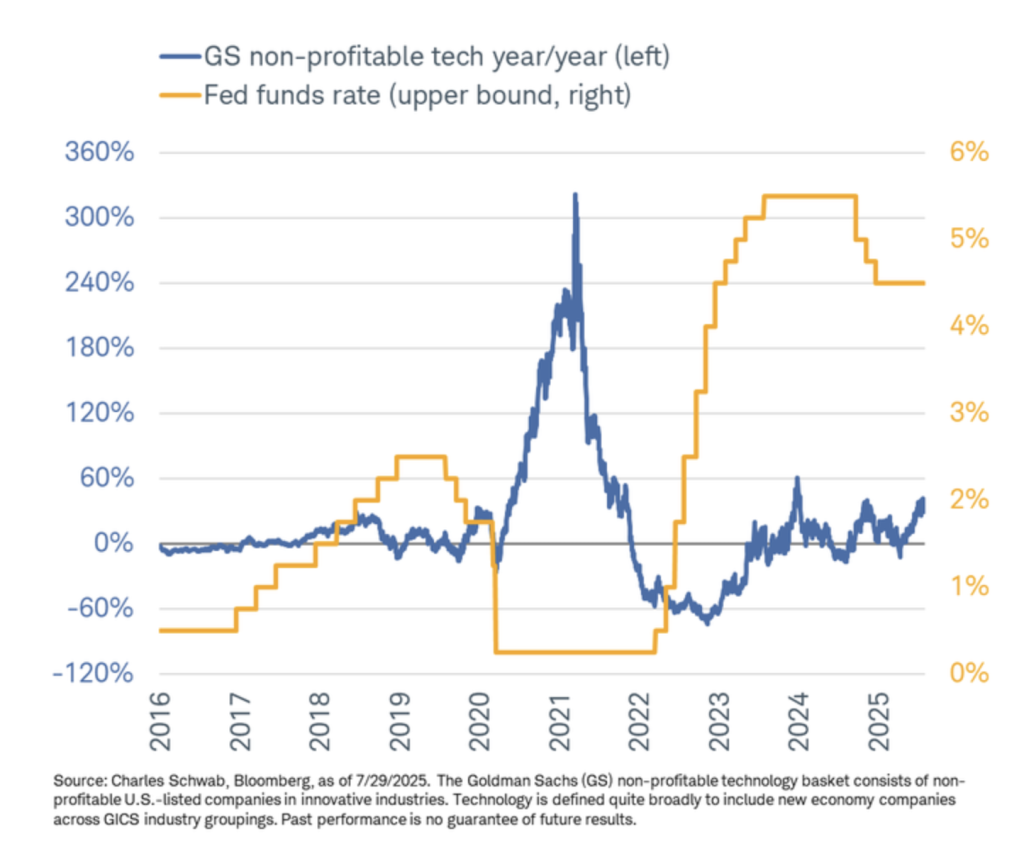

Speculative Tech Restraints Emerge Amid Higher Rates And Liquidity Decoupling

2021 speculative manias leader was the Goldman Sachs non-profitable technology index, its returns well over 300%, and it has gone on to retracement heavily—displaying much more modest growth profiles but still demand sought after in the world of innovation names. Relative to the 2021 craze, the present equity market is run on a federal fund rate over 4%, a precursor of much starker tighter monetary conditions that are restraining frenzied valuation growth.

This flip is similar to the 2000 dot-com collapse lessons, as unsustainable losses in tech stocks precipitated more than a 50% market correction. The distinction lies in policy: zero rates facilitated risk-taking in 2021, whereas the present higher rate regime makes for an automatic brake. Liquidity is still plentiful though—M2 money supply patterns reflect the still-easy availability of capital and therefore speculation maybe still lingering in the fringes but more discerning and cyclically induced.

We consider cash-flow-positive mid-cap tech stocks to be undervalued in this re-balanced world. Their operational strength shields them from policy mis-steps and valuation squeezes. The attention of the analysts is directed towards M2 velocity and credit extension to pick up the re-resumption of speculative activity. Without re-coupling of rates and liquidity, froth pockets would re-emerge and flourish particularly in frontier tech themes.

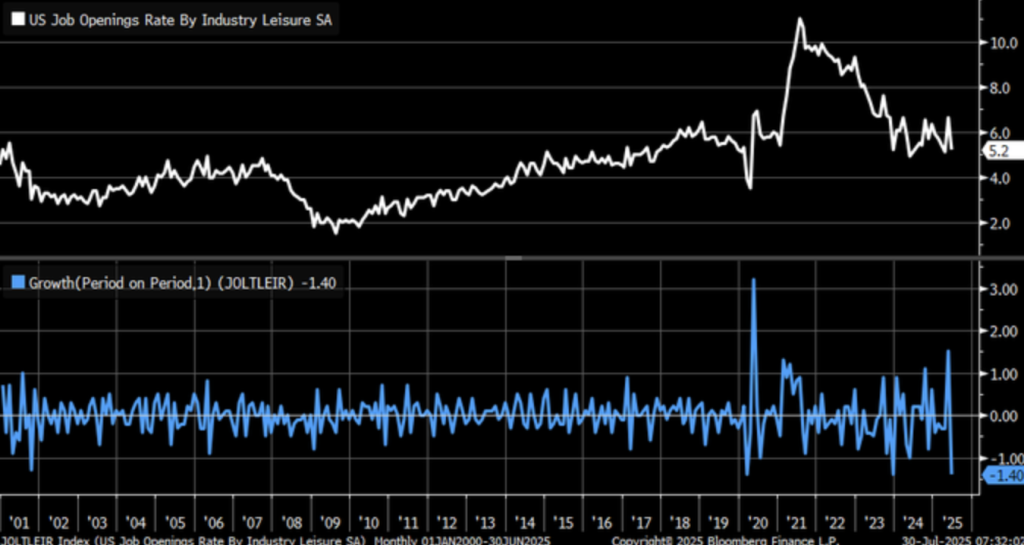

Leisure Job Openings Dip To Cyclical Lows Amid Consumer Spending Strains

US recreation industry employment available decreased 1.4% in June 2025 and hit the lowest points in December 2023 and March 2020. The fall from BLS labour turnover series portends falling demand on the most consumer-sensitive segment of the economy. The coincidence between thinner household pockets and inflationary intransience itself renders the industry’s labour demand also more cycle-sensitive and less growth-directed.

Sub-par Q2 performance from among the biggest hospitality brand names is further evidence of a slowdown. Downside earnings and traffic growth for the foodservice and lodging units respectively point towards a time of cautious discretionary spending. The downtick is a consequence of higher input prices and wages creating a margin squeeze on operators. Long-term outlooks for travel and tourism remain rosy—at 5.8% annual growth during the year 2032—yet the short-term remains highly volatile.

Local home hotel REITs and domestic travel technology platforms remain the undervalued calls on the pullback. The companies have minimal world volatility and demand normalization in the future. Leisure focus components of future CPIs, BLS employment patterns, and OECD series of sentiment need to remain on the analysts’ radar screens to test whether the fall is transitory or a consumption reshuffling.

Upcoming Economic Events

German Prelim CPI m/m, Core PCE Price Index m/m, Employment Cost Index q/q, Unemployment Claims

This week’s agenda includes a high-ticket run of inflation and labour market readings with global and domestic ramifications. In the wake of still-contagious rate nuance and consumer fatigue indicator signalling, each and every release can quite conceivably take the market either way—either confirming expectations of policy constricting or presaging relief for risk asset classes. Here’s an up-close preview ahead of what to watch for and also how each result impacts investor positioning and market direction:

German Prelim CPI m/m

Germany’s inflation’s first reading will give its initial glimpse on eurozone price dynamics.

- A hotter-than-projected print would be biased to bolster ECB hawks and re-fanned concerns about additional tightening, especially in the case of an energy and food-driven inflation. That would put European equities on the back foot and euro-denominated debt in focus.

- If the reading is weaker than expected then that would be taken to ease inflationary pressure and give authorities more room. European risk-sensitive assets would take the rally from the move and the world market take the news as the message that global inflation headwinds are fading.

Core PCE Price Index month/month

Perhaps the most important piece of data this week is the Core PCE as the Fed’s preferred inflation metric.

- A consensus-beating print would affirm ongoing stickiness in the inflationary faction—most pronounced in the services component—and would most likely solidify the case that the Fed needs to keep the rates higher for longer. Stocks, growth and technology names in particular, would most likely once again face selling pressure, whilst the benchmark tenors and the U.S. dollar would most likely benefit.

- A softer-than-consensus print would, however, affirm the “peak inflation” narrative and provide market participants confidence that tightening is largely complete. This scenario would unleash a more general equity rally and ease pressure on rate-sensitive names.

Employment Cost Index q/q

This quarter-to-quarter wage growth indicator reveals the degree to which labour costs are contributing to inflation.

- Such a fast acceleration as predicted would be driving a wage-led inflation spiral and would compel the Fed to leave the rate up for longer. Spillback would mean softness in the duration-sensitive sectors such as long-maturity Treasuries and growth sectors.

- A downside miss with the ECI would be interpreted as further evidence that labour market tightness is easing out, relief from some inflation pressure. Housing and consumer staples stocks would gain from the vision of moderating cost inputs.

Unemployment Claims

Weekly unemployment claims remain the best barometer of jobs hiring in real time.

- A decline short of consensus would mean the labour market remains snug, reinforcing the case for further consumer spending—albeit beneath support from holding inflation concerns. This could prompt markets to look for a more hawkish Fed policy.

- But unexpectedly sharp higher claims could be seen as proof of first chinks in the jobs wall reinforcing the slowing economy narrative. This would then prompt rotation out of cyclicals into defensives, gains in U.S. Treasury prices, and potentially a softer dollar as rate hike hopes recede.

Overall then, the inflation and wage prints of upside surprises will support a hawkish policy leaning and soft prints will simultaneously offer the first signal of the room for policy easing. To Zaye Capital Market analysts, the focus remains on the impact of such prints on the Fed’s forward guidance, the movement of the yield curve and the performance of the sector rotation on global portfolios.

EARNINGS

Earnings Recap: July 30, 2025

- Microsoft Corp.

Microsoft reported a blockbuster quarter, with revenue climbing to $76.4 billion, up 18% year-over-year and comfortably ahead of expectations. Net income rose to $27.2 billion, translating into an EPS of $3.65 versus the forecasted $3.37. The standout driver was Azure, which grew by 39%, propelling Intelligent Cloud revenue to $29.9 billion. With total cloud-related revenue reaching $46.7 billion, the results fuelled a post-market rally of over 9%, reaffirming Microsoft’s leadership in AI-driven enterprise growth and pushing its valuation toward the $4 trillion mark.

- Meta Platforms, Inc.

Meta delivered a major upside surprise, posting $47.52 billion in revenue—up 36% YoY and well above estimates near $44.8 billion. EPS reached $7.14, smashing the expected $5.89. Strength came from advertising recovery across Instagram Reels and WhatsApp Business, although engagement on legacy platforms like Facebook remained flat. Investors responded positively, driving shares up over 12% in after-hours trading, though sustainability of ad growth remains a key question.

- Qualcomm Incorporated

Qualcomm reported strong results driven by a rebound in its automotive and IoT segments, although handset revenues remained stagnant due to sluggish smartphone demand. The company’s share price slipped around 5% post-release, reflecting ongoing concerns about core mobile chip headwinds despite strength in diversification strategies.

- ARM Holdings PLC DR

ARM benefitted from surging demand in cloud infrastructure and AI-centric processors, outperforming both revenue and profit expectations. However, the company flagged increased licensing and operational costs, which may weigh on future margins. The stock traded sideways post-announcement, as investors digested near-term profitability concerns.

- Automatic Data Processing, Inc. (ADP)

ADP delivered steady, expectation-aligned results with continued growth in payroll and HR services. International markets supported topline resilience, although a marginal dip in margin performance was noted. Client retention remained strong, reinforcing ADP’s defensive qualities in a labour-sensitive environment.

- Robinhood Markets, Inc.

Robinhood fell short of revenue expectations, with weakness in crypto-related trading weighing on results. While net new funded accounts grew, the company’s reliance on transaction-based revenue continues to be challenged in a lower volatility environment. Shares rose 1% after hours, buoyed by long-term user growth, but near-term monetisation remains a concern.

- Ford Motor Co.

Ford exceeded profit expectations, driven by strong truck and EV sales, particularly in North America. However, executives flagged margin pressure from rising material and logistical costs. The stock dropped 4.6% post-earnings, as investors weighed robust top-line performance against the outlook for profitability under cost inflation.

- Morningstar, Inc.

Morningstar met earnings expectations, with modest growth in its subscription business offsetting weaker inflows into asset management products. While recurring revenue streams remain solid, market-sensitive products underperformed due to volatile fund flows. Investor response was muted, with attention fixed on forward commentary regarding capital allocation.

Earnings Preview: July 31, 2025

- Apple Inc. (AAPL)

Apple will report after the bell with investors focused on its services revenue trajectory and early signals around iPhone 18 demand. While growth is expected in App Store and wearables, any guidance cut on hardware could weigh on sentiment. Investors will also be watching for updates on AI integration and supply chain developments ahead of the product cycle.

- Amazon.com Inc. (AMZN)

Amazon is set to announce earnings that will likely highlight AWS performance and trends in e-commerce margins post-Prime Day. Advertising remains a growth lever, and market focus will be on cost optimisation progress in logistics. Any weakness in AWS guidance may raise concerns over enterprise IT spending softness.

- MicroStrategy Inc. (MSTR)

MicroStrategy’s results will be scrutinised more for its crypto exposure than software operations. Given recent Bitcoin price volatility, the market will focus on balance sheet implications and whether any impairment charges are recognised. Operationally, software growth remains secondary to crypto-linked balance risk.

- Southern Company (SO)

Southern is expected to post stable regulated utility earnings. Investors will seek clarity on grid infrastructure investments and cost recovery mechanisms amid elevated power demand and capital expenditure cycles. Regulatory outlook will be a key driver of sentiment in the earnings call.

- Cloudflare Inc. (NET)

Cloudflare is forecast to post solid revenue growth, but the market will zero in on margin expansion and operating efficiency. With valuation premiums priced into the stock, guidance quality and free cash flow metrics could be the swing factor for short-term price action.

- Exelon Corp. (EXC)

Exelon’s earnings will reflect base-load stability and grid reliability trends. With decarbonisation themes gaining traction, the market will evaluate Exelon’s long-term capital plans and its exposure to regulatory headwinds. Any miss on earnings or capex execution may pressure valuation multiples.

- Xcel Energy Inc. (XEL)

Xcel is likely to show consistent regulated utility performance with minimal surprises. However, commentary on renewables investment pipeline and rate base growth will be key. Investors will look for visibility on long-term infrastructure returns and inflation pass-through mechanisms.

Stock Markets– Thursday, July 31, 2025

Equity markets remain volatile with investors seeking to absorb a series of technology earnings, uncertain economic data, and new geopolitical tensions caused by shifts in U.S. tariff policy. Traders are weighing the Federal Reserve’s next move with signals of robust core inflation and labour market conditions. At the same time, President Trump’s recent comments on raising tariffs against India and regulation on tech leaders have added to the market uncertainty.

Stock Prices

Geopolitical Events and Economic Indicators

This meeting is also provoked following reports that pressures from inflation stand obstinate as the reads from the Core PCE indicate disinflation loses steam. Employment Cost Index releases on the brighter side also offer support to officials to take the initiative. Overseas, Trump’s renewed remarks about the 25% tariff on the import from India from today has shaken world markets and caused worries about New Delhi’s retaliations.

Geopolitically, there is concern over U.S. oil and technology trade corridors due to China and Brazil reinforcing U.S. sanctions. To respond, flows into defensive securities and fixed income safe-haven securities have accelerated but the market continues to be divided.

Stock News

Microsoft Corp. ($MSFT)

Microsoft stock continues to move forward following the Azure’s record performance. The cloud unit posted 39% year-on-year growth and added $4.3 billion of net new revenue—its largest-ever cloud pickup on record. Investors increasingly see Microsoft as the enterprise AI and cloud infrastructure leader and continue to feed optimism in the technology majors.

Robinhood Markets Inc. ($HOOD)

Robinhood rose more than 5% premaket today on earnings with near-term options market expecting further upside. CEO Vlad Tenev pointed out near 1 billion forecast contracts trading in Q2 indicating healthy retail demand. Aside from that retirement accounts doubled year over year to 1.5 million and the platform also holds $19 billion in assets under management setting the platform up for further institutional penetration and long-term asset growth.

The Magnificent Seven and the S&P 500 Index

Despite on-time gains from a series of large-cap counters, the so-called “Magnificent Seven” of Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla are looking spent. The latest sector snapshot indicates the group has collectively shed more than 18% from recent highs, with the leaders in the pack being Tesla and Meta. This is a bout of valuation re-balancing, particularly from the AI-fueled growth narratives that have gotten too far ahead of fundamentals.

S&P 500 is still soft as the leadership of the tech weakens. Despite the support of the energy and industrials, the index would not have a big rally without again encountering the active participation of its key mega-cap leaders.

Major Index Performance as of July 31, 2025

- S&P 500: Currently trading at 5,841.52 and down 0.4

- Nasdaq Composite: 18,220.78, down 0.6%, pulled lower by tech weakness.

- Dow Jones Industrial Average Advanced 0.2% to 41,182.34 on the back of gains in energy and financials.

- Russell 2000: Holding steady at 2,147.63, retreating from rate sensitivity in the small caps.

Zaye Capital Markets is paying close attention to sector activity and positioning plays during the ongoing earnings season. If top companies manage to sustain the earnings pace even amidst hardening policy direction will define the trend for the overall equity market during Q3.

Gold Price – Thursday, July 31st 2025

Gold currently stands at about $3,311 an ounce today after dropping 1% during Wednesday. The decline followed the better-than-projected U.S. economic data that solidified the market forecast the Federal Reserve would keep its rate stale and capped near-term gains on the metal. Nevertheless, political risk remains the foundation of the golden appeal. The latest trade actions of President Trump—of the imposition of a 50% duty on the importation of copper and 15% duties on South Korean exports and reimposition of sanctions on India—have shaken world markets. His demand on the Fed to cut interest rates and his pronouncements of a “great day for America” on the August 1 tariff deadline have only stoked investor concerns and raised the demand on the yellow metal as a political and monetary volatility hedge.

Follow-up releases later today—Core PCE, Employment Cost Index, German CPI, and jobless claims—will be key to the next gold direction. Any inflation or wage positive surprise would solidify a hawkish Fed theme and retain the yellow metal in its place. Otherwise, softer prints would, once again, spark dovish talk, especially with the rising rate-cut mission from Trump. In our view from Zaye Capital Markets, precious metal gold will still remain a stabilizing input in asset allocation against mixed macro signals and fiscal pressure. Economic releases yesterday, such as healthy GDP and firm labour market, clouded the landscape and kept the metal range-bound but well-supported amidst global indecision.

Bitcoin Prices – Thursday, 31 July 2025

The cryptocurrency also trades close to $117,833, even on a thin range after briefly breaking below the levels of $117,000 during the week. The move is a function of investor nervousness in the face of continued Fed policy, stubborn inflation data and short-term ambivalence in economic indicators. While yesterday’s robust GDP report and robust labour market figures briefly kept speculative asset prices in check, Bitcoin has so far remained fairly resolute on the back of favourable institutional flows and the positive vote from the U.S. SEC on in-kind creations and redemptions for Bitcoin ETFS. The regulatory reprieve makes the ETF more efficient, widens market liquidities and solidifies Bitcoin as a mainstream financial asset. The movement of the $447 million BTC being transferred by Galaxy further highlights the continued institutional demand on the horizon leading support prices.

Macro-politically, President Trump’s aggressive trade policy—most aggressively his tariff deployment against South Korea and India and against copper limits—has contributed to currency market and geopolitical uncertainty. His own public complaints against the Federal Reserve and rate cut lobbying prior to the August 1 deadline of the tariffs have also tightened risk appetite. Although the White House report on its crypto policies is one in favour of regulatory clarity, a dearth of detail on a Bitcoin strategic reserve still challenges investors to call for more substantial policy sign. Ahead of a hectic day of data releases including the Core PCE, the German CPI, and the U.S. jobless claims, the market holds on to a sign on the ease or otherwise of inflation. In our Zaye Capital Markets view, Bitcoin’s consolidation above the $117K level is a turning point inflection and today’s macro signal is to guide its breakout direction in the next few sessions.

ETH Prices – Thursday, July 31, 2025

Ethereum currently trades around $3,843 after gaining over 0.9% over the last 24 hours as it consolidates against key levels of resistance. Institution buying over the last few weeks has been tremendous and spot ETH ETFs received over $218 million in net inflows on July 29 and one-day net inflows of over $533 million last week. The aggregate of all ETF holdings reached over $9 billion and signifies building institutional confidence in the long-term value of Ethereum. Treasuries and whales buying aggressively on-chain mean that 220,000 ETH (~$850 million) has been bought in the last 48 hours—equalling roughly 23.5% of circulating supply—and a treasury wallet added 77,210 ETH equal to the monthly emission of Ethereum and creating a structural supply shock on the main chains.

This building pattern is an indication of rising pressure on exchange liquidity, suppressing supply and driving bullish demand throughout the ecosystem. Upside targets now in play range from $4,000 to $9,000 and center on ETF flows and decreasing sell-side supply. With long-term holders continuing to be lured in with institutional capital and whale demand, the price foundation continues to be built. In our coverage at Zaye Capital Markets, this stage is an underlying foundation building, and Ethereum’s depleted exchange reserves, firm ETF support, and surging corporate demand provide a solid foundation for further upwards movement—albeit barring macroeconomic stability and ongoing regulatory support.