Where Are Markets Today?

U.S. and European stock futures are likely to open positively today with key indices in both bourses expected to open higher after encouraging inflation figures and strong rallies in key indices. The S&P 500 futures expect 1.08% rise, Dow Jones Industrial Average futures expect 1.06% rise, and Nasdaq-100 futures expect 1.27% rise. European futures are also expected to rise, with Euro STOXX 50 (+0.47%), FTSE 100 (+0.22%), DAX 30 (+0.52%), and CAC 40 (+0.71%) all expected to rise. The increases are indicative of the hopes after latest figures from U.S. inflation that eased, boosting hopes of a rate reduction eventually from the Federal Reserve this September.

Positive mood was led most of all by recent US Consumer Price Index (CPI) data, which revealed a less steeply rising increase in prices than was initially predicted. The 0.2% July rise, and a 0.3% rise in core CPI, assuaged concerns for runaway inflation and gave rise to expectations that the Federal Reserve would lower interest rates in an attempt to drive economic growth. A September cut from the Fed would likely give a shot in the arm to risk-sensitive markets, and technology would be one of its leading performers over recent months.

Tech shares are leading the way, heavy hitters including Nvidia and Microsoft holding firm, fueled by growth in artificial intelligence and use of cloud computing. That action of their stock is propelling overall markets upward with major indexes. Those market participants are especially bullish about that tech patch remaining atop amid fears that interest rates will be increased in months ahead. That specific sector’s action is once more being a determiner behind today’s optimism about U.S. and European shares.

Geopolitical news also provides foundation for optimism in markets. Although in the background are the trade tensions, President Trump’s recurring tariffs, and his probable meddling in Federal Reserve policy, all of this causes less short-term alarm than with earlier scenarios. Oil prices, which have become so contentious of late with geopolitical fears, are also comforting today, in that a slight price dip works to relieve pressure off sentiment in markets. As a result of today’s opening of markets, all of this is further compounded with positive inflation reports and positive major-sector performance, all of which works to fuel optimism.

Substantial Index Performance Up to August 12, 2025

- S&P 500: At 6,280.46, up 1.7% on the day.

- Nasdaq Composite: At present 21,681.90, up 1.4%, setting an all-time

- Russell 2000: Rose 3% to 1,913.16, its highest in about six months

- Dow Jones Industrial Average: Rose 1.1% to 41,182.34, boosted by increases in financial and oil shares.

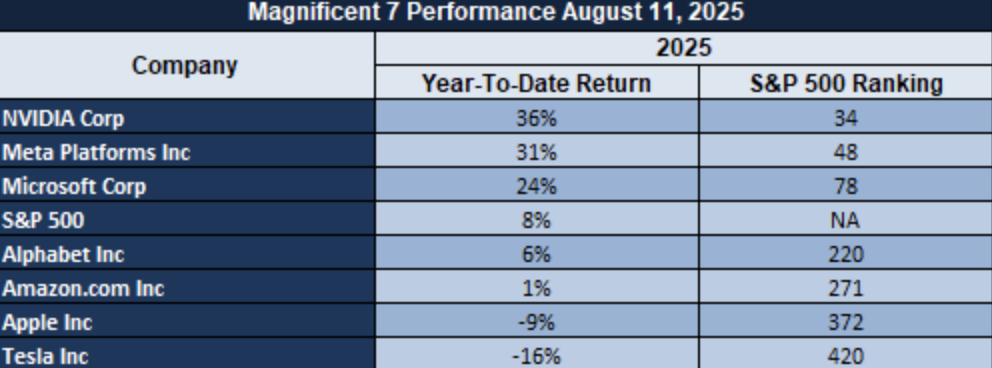

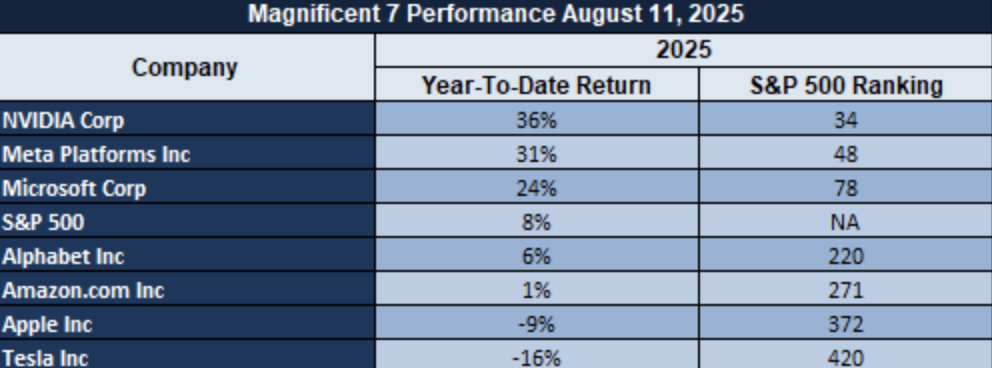

The Magnificent Seven and the S&P 500

Apple’s “Magnificent Seven” peers, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla, are beginning to tire. A sectoral breakdown another way reveals the group overall averaging a drawdown of more than 18% from their respective heights, led by Meta and Tesla. This is implying a recheck on valuations, in particular on AI growth narratives that have gotten out of control. The S&P 500 remains stuck below the whip of uncertainty in tech leadership. No conviction rally is possible, however, without its underlying mega-cap leaders re-engaging.

Drivers Behind the Market Move – August 13, 2025

With US and European markets opening today on higher grounds, investors’ sentiment is guided by three important facts:

- US Inflation Data and Federal Reserve Projections

US Consumer Price Index, July rose 0.2% and core CPI rose 0.3%. This has fueled hopes that interest rates would be reduced in September, after pressure on inflation eased. Market nerves are being driven by a number of different issues, first being that just 73,000 jobs were created in July in the US, much fewer than forecast. The announcement last week by President Trump that he was introducing tariffs on imports from several countries has also fueled fears of commerce, and markets have become choppy.

- Political and Trade Turbulences

Existing policy in international trade by US President Donald Trump, such as imposing tariffs and international trade with Brazil, continues to influence international trade performance trends. Fear of Trump’s politics, such as moves targeting Federal Reserve independence, continues to be a cause of worry for the market. Trump’s recent rants against significant financial institutions for their research on research of tariff research also continues to be a cause of disruption for investors.

- Sector-Specific Factors

Strong performance in big-tech names, such as Microsoft and Nvidia, that align with growth within AI and a rebound within earnings reporting continues to sustain markets. But re-emergent geopolitical fears, especially within Ukraine, and oil-price volatility are weakening sentiment within markets and volatility. Sectoral impulses, in this case, are dominating broad-based sentiment within markets as investors offset growth prospects against risks around geopolitical issues. These are creating a volatility-plagued market situation wherein investors equate politics, industry trends, and macroeconomic statistics.

Digesting Economic Data

The TRUMP Tweets and Its Implications

President Trump’s latest round of announcements and comments are echoing through both the political and financial spheres, carrying major implications for investor expectations and market sentiment. One of the most striking has been the proposal for a Trump-Putin summit in Alaska, described as a “listening exercise.” Although this summit might offer a chance for diplomatic exchange, especially over the current Ukraine-Russia standoff, the market’s response to such geopolitical overtures has typically been one of restraint. Geopolitical tensions, particularly over energy export and sanctions, have traditionally resulted in volatility across global markets, including oil prices and risk assets. Trump’s tone on trade and international diplomacy remains a driver of investor sentiment, especially within the context of energy markets and trade relations with major nations.

Also of concern are Trump’s remarks about the deployment of U.S. military forces. The California lawsuit against the Trump administration for deploying the military in Los Angeles on the grounds of violating the Posse Comitatus Act is another source of political risk. Such incidences can shift the market based on sentiment, particularly those sectors involved in defense and public infrastructure. However, the greater implication is the potential policy shifts that can arise from such legal standoffs. Investors can react by shifting to safe-haven assets or diversifying from sectors directly impacted by government regulatory policy changes or military-related policy.

Another fundamental development that may shape market action is Trump’s threat to sue Federal Reserve Chairman Jerome Powell over the management of a $2.5 billion renovation. The criticism of the Fed is symptomatic of longer-standing tensions between the executive and the central bank, with underlying fears about monetary policy and government intervention in economics. The Fed’s course of action has implications for long-term interest rates, inflation expectations, and broader market stability. If these tensions were to ratchet up, we could see further market volatility, especially in bond markets and interest rate-sensitive stocks.

Trump’s demand for a “land swap” solution to the Ukraine-Russia peace accord also adds to the geopolitical risk. Any shift in diplomatic stances has the potential to alter market expectations of European stability, energy security, and global trade relations. Investors are monitoring these developments closely, as these types of geopolitical risks have the potential to create volatility in commodity markets, particularly oil and gas, and impact the broader stock market, particularly industries like energy, defense, and tech. In the coming days, these political tensions, combined with Trump’s continued influence over economic policy, will most likely keep markets on edge.

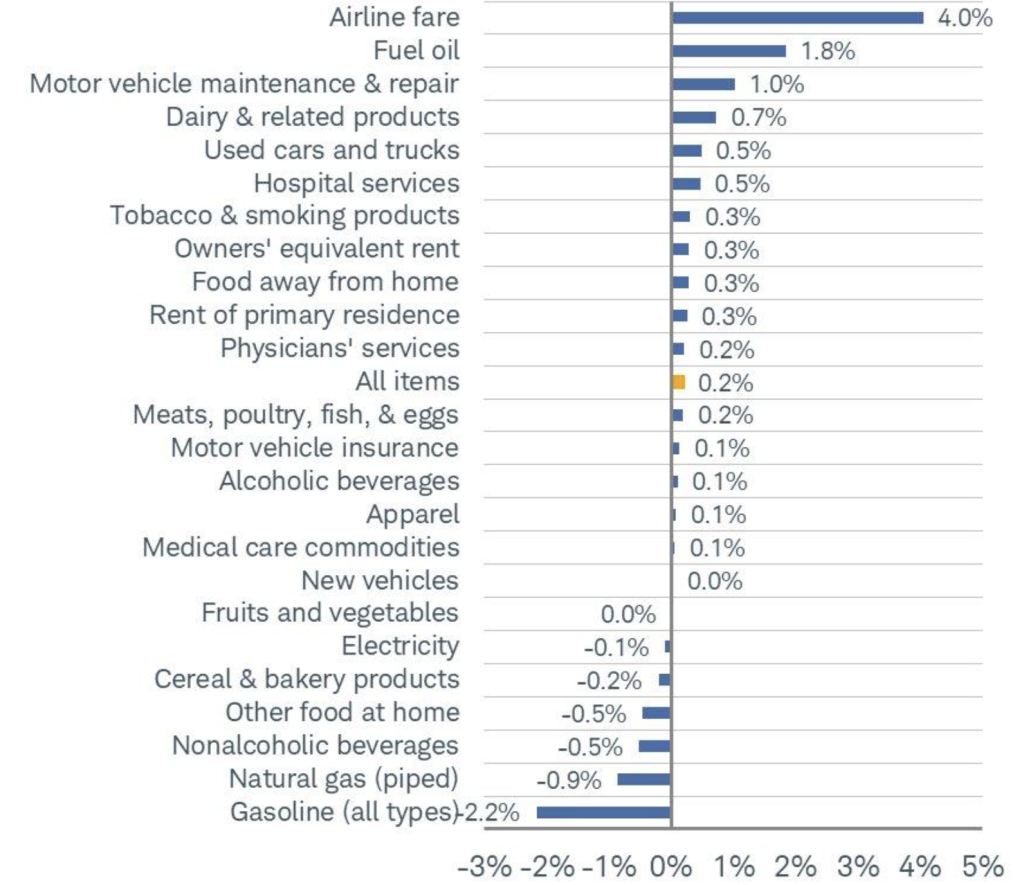

Airline Fares Outpace General Inflation Amid Rising Costs

TU.S. city consumer air prices jumped 4% during last month in July 2025 from the previous month, which was the largest month-on-month rise in May 2022, after a combination of healthy travel demand and all-time highs of jet fuel prices, which touched an all-time high of $2.85 a gallon, said the U.S. Energy Information Administration. Such a rise in relation to total 2.7% year-on-year rise in the Consumer Price Index (CPI) would indicate prices in the air are running ahead of total inflation. Such deviation is causing an inflationary issue which is unique to segments in travel and the transport sector.

Increased air prices also reflect supply deficiencies, especially a 15% world seat reduction from 2019, 2023 IATA reports state. Reduced flight capacity with increased demand has driven prices upwards. Through volatility inherent in this sector, with prices as high as 26.5% increases as recently as February 2023, there is skepticism that this increase is a transient burst in demand or is something deeper within this sector.

We believe Southwest Airlines (LUV) is an undervalued airline company. In spite of capacity restraints and surging fuel prices, Southwest has held its ground through admirable operating efficiency and an atmosphere of passenger delight. Analysts should be cautious regarding how it would strike a balance between surging ticket prices and keeping passenger traffic intact along with keeping its cost down. As sentiment around its markets continues to swing according to macroeconomic indicators, Southwest Airlines(LUV) is a good point of entry for investors that crave growth through industry Challenges. Analysts should be cautious regarding future directions of fuel prices and how intangible profit sustainability are despite altered market circumstances.

Global CPI Trends Indicate Inflationary Pressure Persists

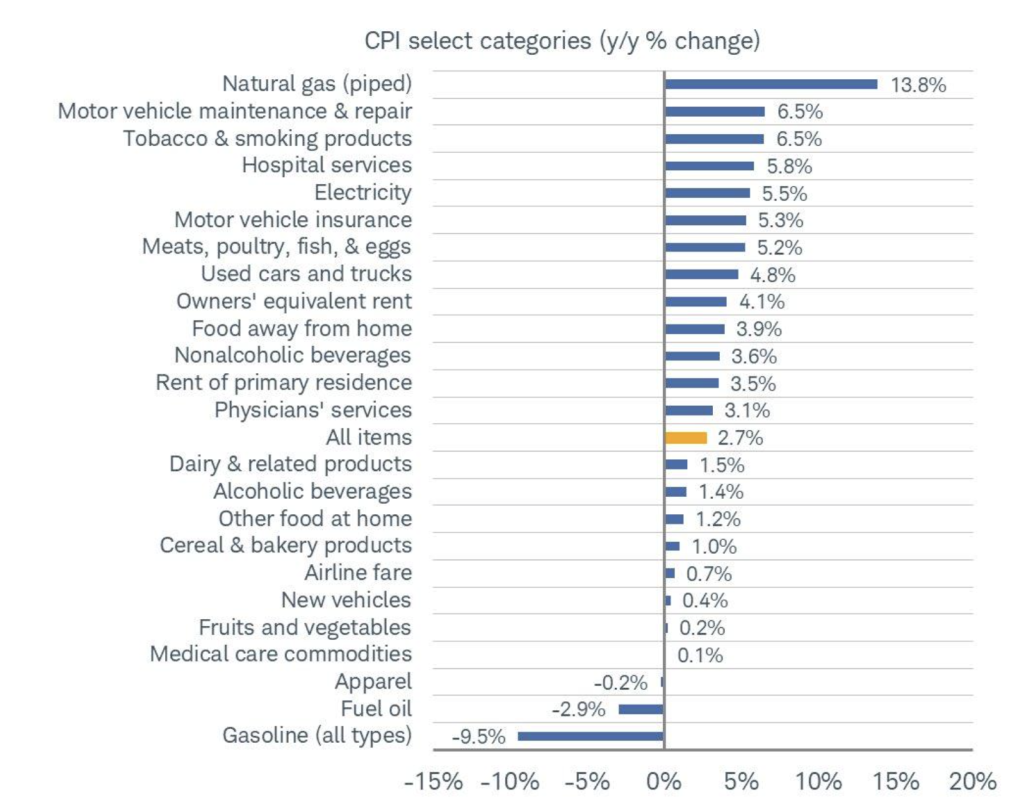

July 2025 U.S. Consumer Price Index (CPI) figures recorded a moderate 0.2% month-over-month increase in core staples like rent and meats, which indicates persistent inflationary pressures in fundamental household expenses. Gasoline prices, meanwhile, fell 2.2%, which reflected volatile energy impacts during a decline in global oil prices from $85 to $65 per barrel between July and September 2024. This only highlights the overall volatility in energy costs, which obscures the more stable inflation trends elsewhere. Investors must look beyond the energy price volatility to spot the core CPI components like housing and food for more selective economic indications.

Likewise, the UK’s recent CPI figures released by the Office for National Statistics (ONS) revealed a surprise 3.6% increase for June 2025. This ties in with inflationary pressures worldwide and indicates that inflation is not limited to a specific area. This international backdrop introduces complexity to the U.S. Federal Reserve’s 2.7% inflation target, and market players should be aware of how exogenous factors—like energy price volatility and geopolitical dynamics—can sometimes postpone the expected rate cuts, which would keep inflation expectations higher for longer.

Amidst these trends, McDonald’s (MCD) emerges as an undervalued consumer stock. Notwithstanding overall inflationary fears, McDonald’s strength in preserving profitability via menu price hikes and robust demand presents a strong argument for value investors. Analysts need to monitor the company’s success in managing ingredient cost hikes and rent increases while retaining its global clientele. Further, tracking overall energy trends and their effect on consumer spending will be important in assessing McDonald’s future earnings outlook.

Small Business Optimism Points To Economic Contradictions

The NFIB Small Business Optimism Index gained 1.7 points to 100.3 in July 2025, beating the 52-year average of 98. The increase is mostly due to better hiring plans and a better perception of expansion opportunities. This optimism is, however, moderated by a steep 8-point increase in the uncertainty index to 97, fueled by persistent tariffs and international conflicts. Small businesses, despite the positive sentiment, continue to worry about external factors affecting their stability, which indicates that the current recovery could be tenuous.

The NFIB survey also shows considerable challenges, with 11% of small business owners naming weak sales as their biggest problem—the most since February 2021. Moreover, 21% reported labor quality as an issue, a 5-point increase from June. Such issues indicate that even though optimism is increasing, structural issues remain, especially in labor markets and sales performance. The disconnect between optimism and fundamental issues indicates that small businesses operate in a complicated economic landscape that may affect future growth.

Against this background, Costco Wholesale (COST) stands out as a value stock in the retail industry. In spite of softness in the general economy, Costco has shown remarkable resilience, underpinned by its solid membership model and consistent consumer demand. Observers should pay close attention to how the company manages the effects of inflationary pressure and labor shortages on its value proposition. Seeing how Costco reacts to worldwide supply chain interruptions and tariff-driven cost rises will be key in evaluating its long-term potential.

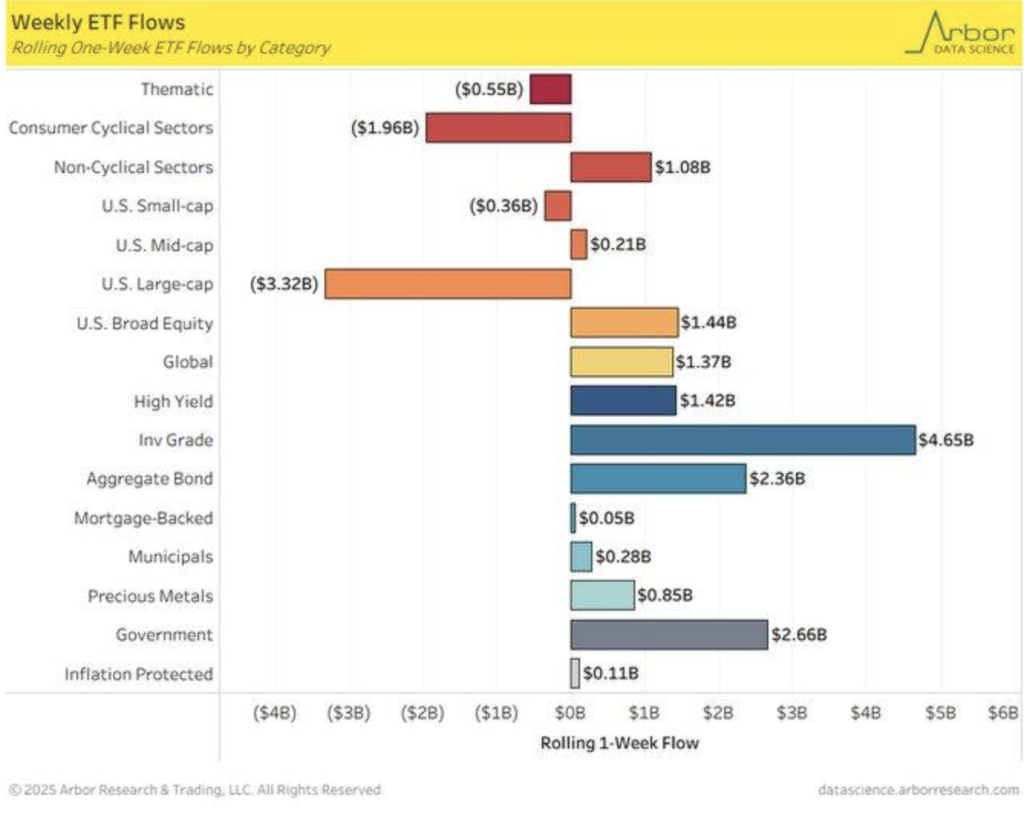

Shift Towards Bonds Signals Market Caution

The massive $4.68 billion inflow into investment-grade bond ETFs in the last week is a stark contrast to a $3.32 billion outflow from U.S. large-cap ETFs, reflecting a strong tilt towards safer assets as economic uncertainty increases. This is consistent with historical precedence, as investors tend to rotate into bonds when there’s volatility in equity markets. A 2023 Federal Reserve study concluded that investment-grade bonds tend to outperform equities by 2-3% per year during downturns, which implies that investors are looking for stability amid potential risks, especially in consumer cyclical sectors like retail and autos.

The bond rotation is also encouraged by the success of the $100 billion U.S. bond auction of August 6, 2025, which was greeted by robust demand as the allure of U.S. debt remained strong despite anxiety about increasing yields. This resilience in the bond market defies the theme of reducing U.S. debt attractiveness and indicates investors are positioning for Federal Reserve rate changes that may be on the horizon, which advises prudence in the wider market. The flows into bonds indicate demand for safer, income-yielding assets in the context of economic uncertainty.

Here, Vanguard Total Bond Market ETF (BND) presents itself as an undervalued investment. The recent run into bond ETFs indicates increasing demand for diversified bond exposure, and BND provides a wide portfolio of high-quality bonds that may rally from continued market trepidation. Future Federal Reserve action, inflation readings, and bond yields are worth watching by analysts to gauge how these may impact the performance of the bond market and if BND will persist in recording inflows in the rotation to fixed-income securities.

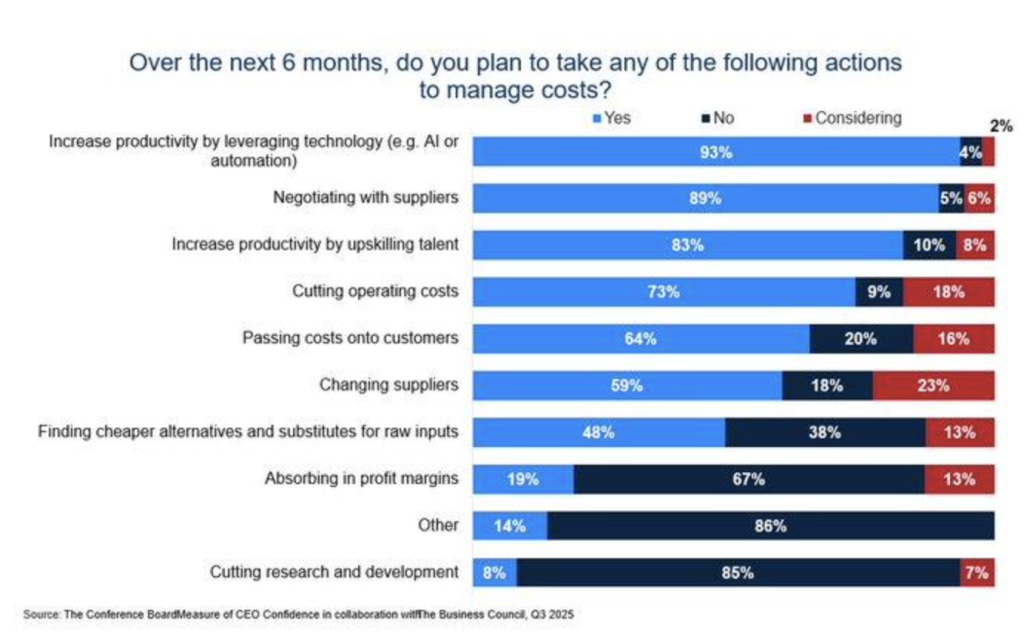

CEOs Adopt Tech To Boost Productivity Amid Cost Pressures

The Conference Board CEO survey of 2023 highlights that 93% of CEOs are planning to leverage technology, including AI and automation, to boost productivity in the subsequent six months. This strategy is consistent with a 2024 study by ISG, in which automation reduced the cost of manual intervention by optimizing inventory and workflow. By leveraging these technologies, companies aim to enhance operating efficiency and negate the impact of rising costs, reflecting long-term interest in innovation despite economic uncertainty.

However, only 64% of CEOs intend to pass on higher costs to consumers, which implies a more restrained reaction than the ones taken during previous inflationary cycles. A Reuters report in 2022 noted that while companies were in a position to pass on costs to consumers, it raised concerns about household affordability. This implies that while companies are focusing on productivity improvements, they are also cognizant of the potential for consumer backlash in an already strained economic environment. On the other hand, cutting research and development (R&D) expenditure is the lowest on the list of cost-reduction choices, with only 14% of CEOs supporting this measure. This contrasts with findings in a 2023 TK Associates study, in which 61% of CEOs felt they were unprepared for crises, meaning that R&D investment might be a long-shot risk in volatile markets. With companies prioritizing automation over innovation, there could be a potential trade-off in the development of new products and services, a point that would have to be closely monitored by analysts.

Microsoft (MSFT) is an undervalued tech stock considering its aggressive drive into AI and automation integration. The company’s sustained leadership in cloud services and AI use cases, which may be resilient in a cost-conscious market, should be followed by analysts. Its innovation pipeline and R&D investments, even in the face of economic uncertainty, will be instrumental in determining the company’s long-term growth trajectory.

U.S Retail Sales Display Resilience Amidst Volatile Trends

The Johnson Redbook Index, which monitors same-store retail sales, recently registered a significant jump to +6.5% year-over-year growth, mirroring sustained resilience in consumer spending amid a volatile trend since 2018. The growth stands in sharp contrast to the steep fall witnessed during the 2020 pandemic, when sales nosedived below -10%. The recent pickup indicates that consumers are returning to confidence and spending, which could be a harbinger of a recovery in retail activity as overall economic conditions stabilize.

This trend is supported by other recent retail data, including a 0.6% month-on-month U.S. retail sales increase for June 2025, as reported by TradingEconomics.com. Collectively, these data points suggest a potential correlation with a broader economic recovery, although studies like that in the Journal of Retailing (2023) caution that indices like the Redbook can overestimate demand due to seasonal adjustments. These factors would skew perceptions of the underlying health of consumer spending and require a more nuanced interpretation of such indicators.

In this environment, Target Corporation (TGT) is an overlooked retail stock that has slipped under the radar. In the midst of the broader retail boom, Target’s equity remains reasonably valued, which creates a buying opportunity. Whether the company can sustain its growing streak, particularly in the midst of potential seasonal volatility and economic shifts, is of interest to analysts. Monitoring consumer confidence, retail spending, and any macroeconomic shifts that will influence discretionary spending will be key to Target’s future success.

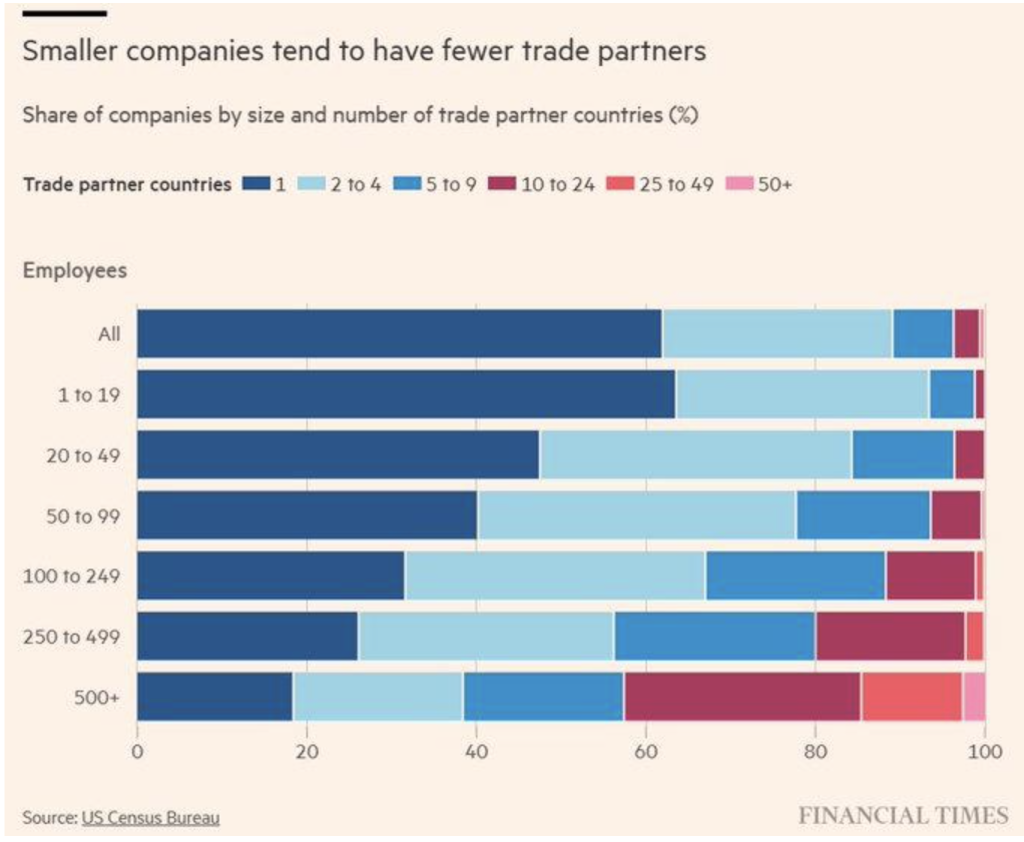

Small Firms’ Trade Dependency Increases Supply Chain Risks

U.S. Census Bureau data, which the Financial Times has brought to the forefront, indicates that small U.S. firms (1-19 employees) are disproportionately dependent upon a single trade partner, with more than 60% of those firms trading with only one country. This pattern weakens as the size of the firm gets larger, echoing resource limitations that constrain smaller firms from expanding globally. This reliance subjects smaller firms to considerable supply chain vulnerabilities, especially amidst geopolitical crises.

This concurs with a report in 2023 by the Journal of International Business Studies that determined that diversified trade networks can reduce supply chain risk by 35% during geopolitical tension. With the ongoing global uncertainty, such as the persistent effect of the Russia-Ukraine war, smaller firms with single market high dependency may be vulnerable to disruption, potentially leading to delays and rising costs. This vulnerability necessitates the diversification of global trade strategies for long-term stability.

Historical precedent from the 2008 financial crisis also backs up this assessment, with Federal Reserve data showing that firms with less diversified trade partners had recovery times 20% longer than their more diversified peers. This contradicts the idea that focus on a single market is always an efficiency strategy, especially during a time of elevated geopolitical risk. Small-cap manufacturing stocks like Nordson Corporation (NDSN) may offer investment potential, as their international footprint and diversified supply chains can afford them resilience in the face of rising trade risks. Analysts should monitor for evidence of supply chain disruption and any change in trade dynamics that could affect smaller companies’ recovery and growth.

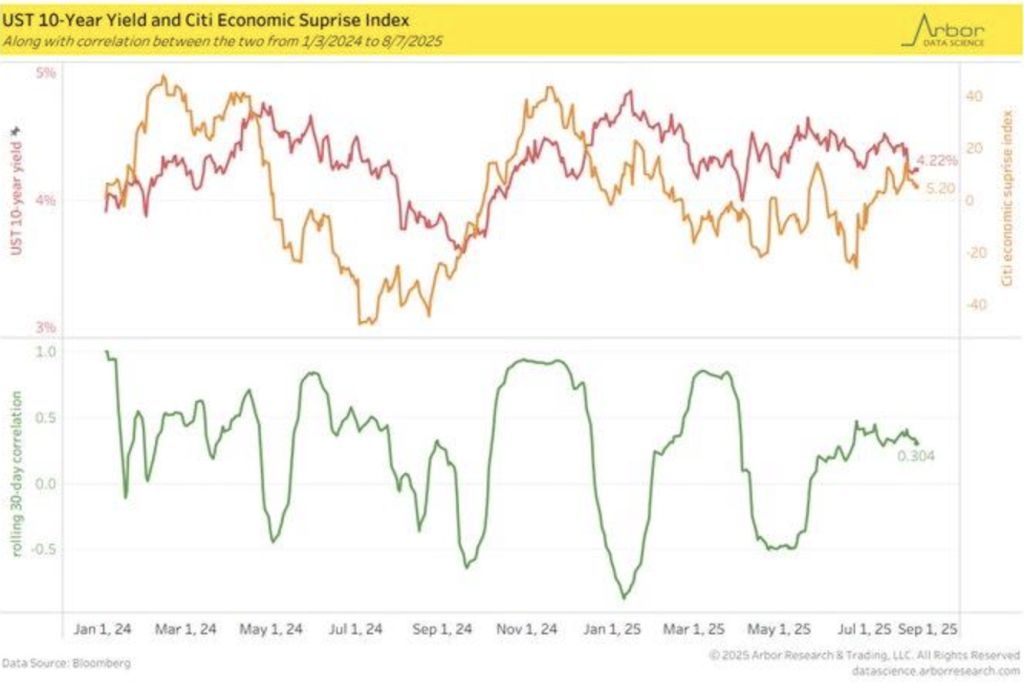

Treasury Yields And Economic Surprises Becoming Increasingly Linked

A rising positive correlation between the 10-year Treasury yield and the Citi U.S. Economic Surprise Index since mid-2025 suggests that surprise economic data is having a growing influence on long-term interest rates. This is supported by a 2023 Federal Reserve study, which estimated that yield sensitivity to economic surprises rose by 15% post-pandemic due to heightened market volatility. With economic data still surprising, Treasury yields are now apparently more sensitive to the shifts, amplifying the effect of surprise events on long-term interest rates.

The most recent iteration of this dynamic is the July 2025 Federal Reserve decision to postpone expected rate cuts, which was based on inflationary pressure from Trump-era tariffs, according to Jerome Powell. This decision is corroborated by Bureau of Labor Statistics data, which indicated a 3.2% inflationary surge in Q2 2025. Although the correlation between Treasury yields and economic surprises has attenuated from its peak last year, it is still considerable, indicating investor response to economic surprises and their effect on future interest rate expectations.

Historically, the same yield-surprise correlation during the 2008 financial crisis was followed by a 2% decline in bond yields within six months. This indicates the possibility of extensive market adjustments if present trends persist. Nevertheless, peer-reviewed research from the Journal of Finance (2024) warns that these types of correlations can become distorted due to geopolitical shocks, introducing an element of uncertainty. In this situation, Bonds of U.S. Treasury (TLT) continue to be an undervalued asset class. Analysts should keep track of the developing correlation between economic data surprises and Treasury yields, as additional changes could influence bond market performance and investor strategy.

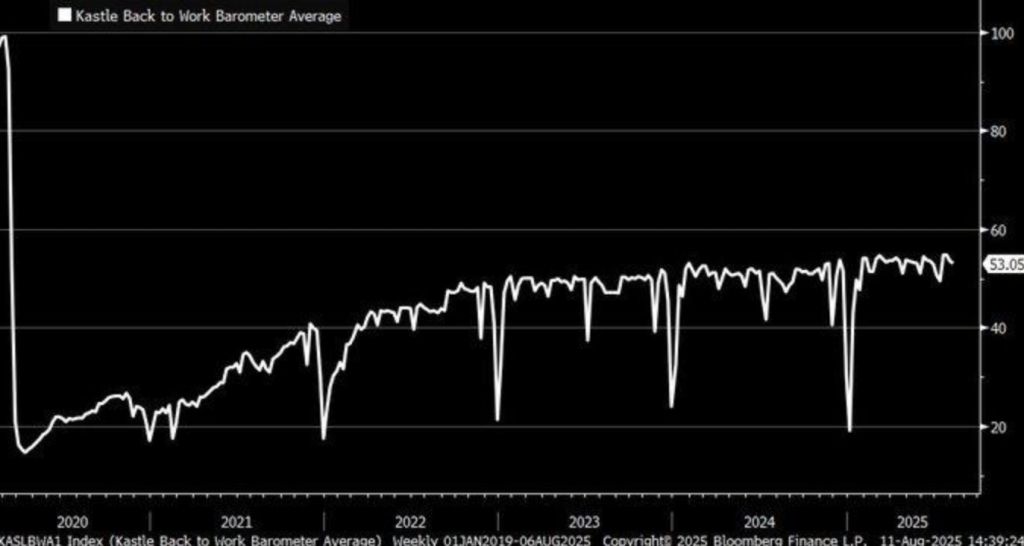

Post-Pandemic Office Occupancy Rises Amid Shift In Workplace Trends

Kastle Back to Work Barometer, an office utilization measure through security card scans, achieved a pandemic peak of roughly 50% in 2025, which showed a strong recovery of visits to offices. Consistent with other Nick Bloom’s survey statistics at Stanford, this also evidences return visits to office centers.

Kastle’s approach, which is based on anonymized information from 1.8 million international users, is more trustworthy than the conventional survey-based statistics, as a 2022 research study through Kastle uncovered that occupied buildings through law offices showed an additional 10% level of return compared to that of the total office industry.

This back-to-office jobs eliminates this remote working model utopia, inferring the employees and companies are traveling back to offices in order to develop collaborative work. One 2023 Gensler report claims that employees are choosing in-office interaction increasingly, fueled chiefly by pandemic-induced changes. It implies that the office face is changing, with workers choosing this hybrid format of remote and office work to develop innovation and collaborative endeavor.

Against this context, WeWork (WE) offers an undervalued business from the commercial property space. Rising office occupancy and runaway demand for flexspaces, WeWork’s value proposition of offering flexible office solutions has a bright long-term future. Its investors must be cautious about how it meets return-to-office trends that are present, but also reaps pent-up demand for hybrid offices. WeWork’s occupancy rates, its growth in its markets, and its resilience to withstand its profitability through office demand fluctuations shall be significant in estimating its growth prospects.

Stock Market Performance

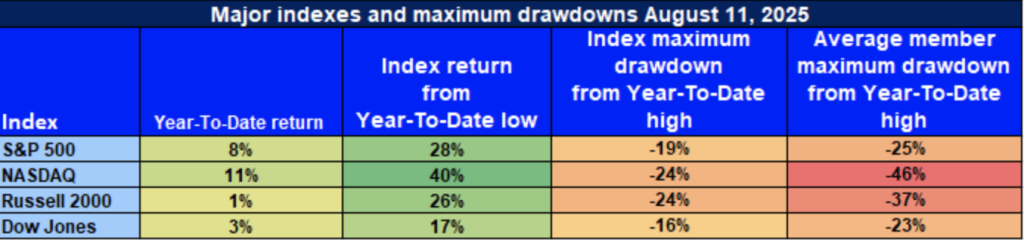

Indexes Have Recovered From Bottoms In April But Wider Volatility Persists

We stay watchful of sentiment in equity markets at Zaye Capital Markets. US indices finally showed a strong bounce back after hitting their bottom on 8th April 2025, but year-to-date returns are spotty. Larger drawdowns on a single security basis are a sign of underlying weakness, a convenient reminder of this market’s vulnerability even after its recent recovery.

Here is our latest assessment of key benchmark performance:

S&P 500: Strong Bounce Back, But Broad Participation

YTD: +8% | +28% below Apr low | -19% from YTD high | Avg. member: -25%

S&P 500 advanced 8% year-to-date and 28% from its April bottom. A 19% consolidation from its 2025 high and average 25% member drawdowns, however, register concentrated performance within individual large-cap issues, with broader participation being held in check.

NASDAQ: Technology Takes the Lead, But Member Weaknesses Are Raising Eyebrows

YTD: +11% | +40% off April low | -24% off YTD high | Avg. member: -46%

NASDAQ prints its biggest rebound at +40% from its bottom since April, and an 11% YTD. But that 24% correction from highs and huge 46% average drawdown indicate long-standing pain, particularly in growth-oriented tech names.

Small-Cap Gains in Russell 2000 Not Convincing

YTD: +1% | +26% below April low | -24% from YTD high | Avg. member: -37% Russell 2000 is up only 26% from its April low and just 1% YTD. The serial 24% drawdowns and higher average member losses confirm persistent investor wariness of small-cap stocks, which is not a positive sign for their resilience.

Dow Jones: Mild Advance despite Defensive Bias

YTD: +3% | +17% below low in April | -16% from YTD high | Avg. member: -23% The Dow, being more defensive in composition, is 3% YTD and 17% from its April lows. The 16% correction and 23% average member retreat, however, indicate even value segments stressed, and the market still exposed.

We, Zaye Capital Markets, pursue a cautious, risk-savvy strategy, aiming for quality exposure but vigilantly keeping volatility indicators and breadth leaders under surveillance across markets. Although as much recovery seems evident, our emphasis lies in availing ourselves of opportunity in areas of strength and maintaining capital through relentless volatility within the broader market.

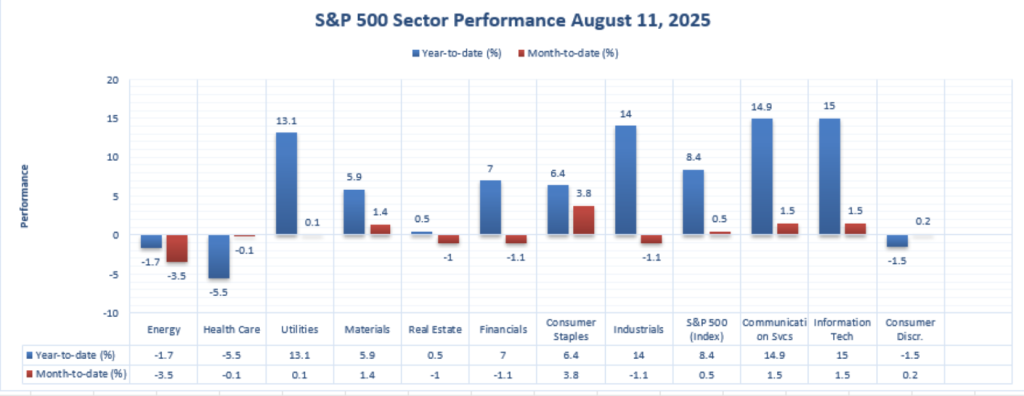

The Strongest Sector In All These Indices

Technology Is At Forefront Of 2025 Expansion As Sector Flows Support Expansion

At Zaye Capital Markets, we remain to monitor sector performance in the overall equity universe. Through August 11, 2025, to date, Information Technology has been the strongest sector in the S&P 500, reestablishing its leadership in a year of volatility and growth selectivity.

Here’s what statistics have to say:

Information Technology: The Unquestioned Champion

YTD Performance: +15.0% | MTD: +1.5%

Technology continues to be this year’s top-performing sector across the board, having returned 15.0% year-to-date and 1.5% months-to-date. The sector has support provided by secular structural themes, resilient earning growth, and robust investors’ demand for innovation-driven names. Technology remains poised to be a beneficiary of more shifting trends like artificial intelligence and cloud computing as companies continue their digitalization.

Communication Services: Serious Contender

YTD: +14.9% | MTD: +1.5% Then comes Communication Services, which rises 14.9% year-to-date, hand in hand with a concurrent 1.5% rise month-to-date. Gains come especially on the heels of large-cap media and platform titles, which are benefiting from robust ad revenues and additional moves towards digital consumption of content.

Industrials: Solid Cyclical Revival

YTD: +14.0% | MTD: -1.1% The Industrials have registered strong performance via 14.0% year-to-date growth driven by a cyclical recovery in transport, infrastructure, and manufacture. Month-to-date performance, however, has slowed down, albeit less steeply, which is an indication of investors’ caution as valuations rise, a sign that expansion within the sector is slowing despite the sector remaining strong.

Consumer Staples and Utilities: Defensive Resilient

Utilities YTD: +13.1% | Consumer Staples YTD: +6.4% Utilities have held their ground and are up 13.1% year-to-date, and Consumer Staples are 6.4% higher. Both are indicative of fear about wanting defensive names, as investors want stable markets regardless of what uncertainty there is outside. Both are good names that conservative investors want who want stable dividends and less volatility.

We prefer Information Technology exposure within quality names within Zaye Capital Markets. But be prepared to stay calm as rotation within sectors changes, that way, we can capture opportunities within a large universe of sectors as forces within markets change.

Earnings

Earnings Report: August 12, 2025

- Sea Limited (SE)

Sea Limited reported a significant 418.3% year-over-year increase in Q2 2025 earnings, reaching $414.2 million, driven by strong performances across its three core businesses. Revenue for the quarter rose to $5.26 billion, up from $3.81 billion in the same period last year. However, the company’s GAAP earnings per share (EPS) of $0.68 fell short of the adjusted guidance of $0.80. Despite this, the stock experienced a notable uptick, closing up nearly 20% on the day. Investors should focus on Sea’s ability to sustain growth in its key segments, especially in digital entertainment and e-commerce.

- CoreWeave, Inc. (CRWV)

CoreWeave reported Q2 2025 revenue of $1.21 billion, a 206% increase from the previous year, driven by accelerating demand for AI infrastructure. Despite the strong revenue growth, the company posted a net loss of $290.5 million, widening from a loss of $323.0 million in the same quarter last year. While the growth is impressive, the company’s operating income margin decreased to 2% from 20% in the previous year. Investors should keep an eye on CoreWeave’s ability to balance rapid expansion with cost control, particularly in the competitive AI infrastructure market.

- Cardinal Health, Inc. (CAH)

Cardinal Health reported Q4 2025 revenue of $60.2 billion, relatively flat compared to the same quarter last year. Excluding the impact of a previously communicated contract expiration, revenue increased by 21%. The company reported GAAP operating earnings of $428 million and GAAP diluted EPS of $1.00. Despite the profit surge, shares fell due to the revenue shortfall, and the focus is on how Cardinal Health will address the ongoing challenges in its distribution and services segment. Investors should watch for any strategic changes to improve revenue growth.

- Circle Internet Group, Inc. (CRCL)

Circle reported Q2 2025 revenue of $658 million, a 53% increase from the previous year, driven by reserves and institutional demand amid rising stablecoin adoption. Despite the loss reported for the quarter, shares rose by 5% post-earnings, reflecting investor optimism regarding the company’s long-term prospects in the digital asset space. Investors should focus on Circle’s role in the broader cryptocurrency ecosystem and its potential to capture further institutional demand amid regulatory developments.

- On Holding AG (ONON)

On Holding reported Q2 2025 results, with revenue growth driven by the brand’s global momentum. The company provided an updated full-year outlook, reflecting confidence in continued growth. However, detailed financial metrics were not disclosed in the available sources. Investors should focus on the company’s performance in international markets and its ability to maintain growth amidst competitive pressures in the athletic wear market.

Earnings Report: August 13, 2025

- JBS N.V. (JBS)

JBS is scheduled to report Q2 2025 earnings after the market close today. Analysts estimate earnings per share (EPS) of $0.39 and revenue of $21.47 billion. Investors will be focusing on the company’s performance in the meat processing sector and any updates on its global operations, especially in light of ongoing challenges in supply chains and global demand for protein products. Any commentary on its cost structure and pricing strategies will be key to assessing the company’s growth prospects.

- Performance Food Group Company (PFGC)

Performance Food Group is set to announce Q4 2025 earnings before market open today. The consensus EPS estimate is $1.46, with revenue expected to be $16.86 billion. Investors should pay attention to the company’s performance across its foodservice, Vistar, and Convenience segments, as well as any guidance provided for the upcoming quarters. The company’s ability to manage supply chain disruptions and labor shortages will likely be a major focus, especially in light of the current economic environment.

- StandardAero, Inc. (SARO)

StandardAero is scheduled to report Q2 2025 earnings after market close today. The consensus EPS estimate is $0.21, with expected revenue of $1.50 billion. Investors will be looking for insights into the company’s aerospace and defense services, particularly its ability to capitalize on increased defense spending. Any updates on contracts or operational performance improvements will be crucial to assess its future growth potential.

- Brinker International, Inc. (EAT)

Brinker International is set to report Q4 2025 earnings before market open today. Analysts will be focusing on same-store sales growth, cost management, and any strategic initiatives to drive traffic to its restaurant brands. The company’s efforts to improve customer experience and address labor costs in the competitive dining sector will be key factors to watch.

- Loar Holdings Inc. (LOR)

Loar Holdings is expected to announce Q2 2025 earnings today. Investors should monitor the company’s performance in its respective industry, focusing on key developments that may impact its financial outlook. Any updates on strategic initiatives, market share growth, and capital allocation will be important for assessing the company’s position in its sector.

Stock Market Summary – Wednesday, August 13, 2025

U.S. markets bounced back strongly on Tuesday, August 12, after renewed optimism among investors with the news of release of the Consumer Price Index report in July. S&P 500 and Nasdaq Composite registered all-time highs, and even the Russell 2000 registered its highest single-day gain in the last almost six months. The rally was across the board and was precipitated by hopes that maybe the Federal Reserve will be permitted to relax interest rates when its meeting in September comes around.

Stock Prices

Economic Developments and Geopolitical Developments

When the news of release of the CPI report, which rose 3.1% year on year, just above expectations but still compatible with falling inflation, was positively received from the market, it gave rise to speculation that monetary policy is going to be eased to sustain economic growth. As a result, equities have gained, wherein Nasdaq and S&P 500, which are tech-centric, were impacted the most through this speculation.

Stock Market News

On August 12, a number of issues shifted significantly:

- SE Sea Limited: Stock rose more than 19% after robust earnings.

- CoreWeave, Inc. (CRWV): As much as its revenue was through-the-roof, its stock declined following a wider-than

- Meta Platforms (META): Stock gained 3.15%, demonstrating strength after a breakout of a prior base.

- Lam Research (LRCX): Up 3.2%, recovering from a key technical level.

- Goldman Sachs (GS): 3.4% higher, still recovering from recent losses.

The Magnificent Seven and the S&P 500

Apple’s “Magnificent Seven” peers, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla, are beginning to tire. A sectoral breakdown another way reveals the group overall averaging a drawdown of more than 18% from their respective heights, led by Meta and Tesla. This is implying a recheck on valuations, in particular on AI growth narratives that have gotten out of control. The S&P 500 remains stuck below the whip of uncertainty in tech leadership. No conviction rally is possible, however, without its underlying mega-cap leaders re-engaging.

Substantial Index Performance Up to August 12, 2025

- S&P 500: At 6,280.46, up 1.7% on the day.

- Nasdaq Composite: At present 21,681.90, up 1.4%, setting an all-time

- Russell 2000: Rose 3% to 1,913.16, its highest in about six months

- Dow Jones Industrial Average: Rose 1.1% to 41,182.34, boosted by increases in financial and oil shares.

We are seeking rotation out of sectors and positioning strategies within this Q3 earnings season at Zaye Capital Markets. Language via leading players’ sustaining earning resilience through policy firming during Q3 shall decide broader equity markets’ direction.

Gold Price – Wednesday, August 13, 2025

As of the latest statistics, gold is selling at approximately $3,344 an ounce, down roughly 0.93% from the previous day’s close of $3,375.62. The drop follows a period of heightened volatility, driven by recent geopolitical tensions and U.S. data. President Trump’s comments regarding tariffs on gold bars imported eased some market anxieties, helping to ignite the short-lived retreat in gold prices. The July Consumer Price Index (CPI) statistics, slightly above expectations, reflected a slowing down in inflation, which may reduce the immediate need for aggressive interest rate cuts by the Federal Reserve. These have caused a recalibration in investor expectations, with some rotating out of gold as an inflation hedge.

Looking forward, the gold market continues to be vulnerable to movements in economic data and geopolitical tensions. Though the immediate tariff pressure has passed, persistent inflationary pressures and possible shifts in the Federal Reserve policy path will continue to drive gold’s attractiveness as a safe-haven asset. For now, investors are watching the inflation developments and the Fed’s future actions, with beliefs that gold could find support should inflation prove persistent. The capacity of the U.S. economy to sustain growth, alongside geopolitical risks, will ensure that gold stays in the limelight as an important asset for hedging against economic uncertainties.

Oil Prices – Wednesday, August 13, 2025

Brent crude is currently trading at approximately $66.15 per barrel, and West Texas Intermediate (WTI) is at $63.14 per barrel, posting a modest increase following recent weakness. The direction of oil prices is being determined by a series of factors that range from supply dynamics and geopolitical events to economic data. The latest American Petroleum Institute (API) report, which indicated a build of 1.52 million barrels in U.S. crude inventories, is indicative of potential weakness in demand. The International Energy Agency (IEA) and OPEC have both updated their outlooks, with the IEA reducing global oil demand growth and OPEC+ increasing production, further pressuring prices. Geopolitical uncertainty, particularly regarding tariffs on Russian oil imports and the recent invitation for a U.S.-Russia summit, is also muddying the waters. Trump’s statement about imposing tariffs on Russian oil and the potential for disruption to global trade relations is being watched closely, though the market is showing restraint, awaiting further clarity.

Looking forward, economic data today, specifically the Energy Information Administration’s (EIA) report on U.S. crude inventories, will be key in driving near-term price action. A decrease in inventories would be a sign of strong demand, which could underpin higher prices, while a build may reflect softer consumption, pressuring the market lower. Geopolitical tensions, including the ongoing risks in the Strait of Hormuz, remain a threat to oil supply security and could promote additional price volatility. As oil prices traverse this complex landscape, investors will need to remain sensitive to both economic data and geopolitical events in order to discern the direction of the broader market.

Bitcoin Prices – Wednesday, August 13, 2025

As of now, Bitcoin (BTC) is sitting at around $119,444, representing a slight increase of 0.3% from the last close. The crypto market is in the phase of consolidation, with Bitcoin remaining firm above the $118,000 level. This is happening in the context of rising institutional interest and regulatory clarity. Interestingly, Pantera Capital’s Bitcoin prediction for 2022 has come very close, with the price of the cryptocurrency tracking their projection closely, highlighting the confidence in Bitcoin’s long-term value.

Looking forward, the market is keeping a close eye on future economic reports, specifically the Consumer Price Index (CPI) report, which may have an impact on investor sentiment. A higher-than-expected CPI may reignite fears of inflation, which could push even more investors into Bitcoin as a hedge. On the other hand, a lower-than-expected CPI may ease fears of inflation, which could trigger a retreat in Bitcoin’s price. Geopolitical tensions and regulatory announcements will also continue to be key drivers of Bitcoin’s market action. Investors should remain aware of these events in order to successfully navigate the changing environment of cryptocurrency investing.

ETH Prices – Wednesday, August 13, 2025

Ethereum (ETH) is now trading at $4,615.98, a huge comeback from July’s low of approximately $2,380. The rally is mostly fueled by strong institutional demand and high whale activity. Spot Ethereum ETFs, such as investments by large companies BlackRock, Fidelity, and Grayscale, have together bought more than $1 billion in ETH, which has helped bring about an increase in ETH’s price and market cap. The heightened institutional demand, coupled with the high interest from big investors, is redefining the price action of Ethereum as it approaches its all-time high of $4,891.

Whale activity has been central to this price action. One major whale, “AguilaTrades,” flipped from a $3.7 million short position to a 15x leveraged long position, indicating a bullish sentiment. Moreover, an anonymous whale amassed $1.34 billion in ETH in eight days, adding to market optimism. The fact that institutional ETF buying and strategic whale accumulation are occurring in tandem points to increasing confidence in Ethereum’s long-term value, with analysts estimating ETH can hit price points of $6,000 to $7,000 by the end of 2025 if demand continues and market conditions remain favorable.