Where Are The Markets Today?

Up to Thursday morning, stock futures in Europe and the US are flat to down slightly, with US futures close to the flatline following yesterday’s strong rally in the S&P 500 and Nasdaq Composite, which reached new records. S&P 500 and Nasdaq 100 futures are flat, and this is because investors are cautiously optimistic after Wednesday’s record day. Dow Jones Industrial Average futures are up slightly by 13 points, or 0.03%, with modest changes. This flat start is because of a wait-and-watch environment as investors digest recent highs in the stock market and wait for future economic reports, which can decide the fate of the stock market.

This Conservative Outlook is driven by expectation of the Thursday reports on the economic side, specifically the Producer Price Index, and weekly unemployment claims for the week of August 9. Both of those reportings will be crucial to investors seeking to estimate inflationary pressure and overall economic conditions. Economists are projecting the PPI rising 0.2% in July after staying flat in the previous month of June. Any transgressions in those readings will have immediate impacts on the degree of expectation for Federal Reserve stimulus activity, specifically on the issue of the likelihood of a reduction in the interest rate in September.

Following on the expectation of the cut already, traders are patient and cautious and waiting for the affirmation of such by the figures. In addition to the main economic reports, U.S. futures are also showing overall sentiment after a strong day on the Street, with the S&P 500 and Nasdaq ending the day solidly in the green. The even start for the futures indicates the traders are staying in caution and are hedging the following economic reports before placing overly bullish wagers. While the initial strength in the U.S. futures is tempered by the recognition the strong momentum can easily turn in the latter half of the day on the release of the inflation and labor reports.

In Europe, caution is the order of the day with the investors waiting for the EU and the UK growth figures. European futures have come in mixed and relatively steady, with skepticism about the European economic growth remaining on the investor’s mind. Fears of European growth running into a slow down and the pressure of inflation have kept investors on the edge of their seats. With the market waiting on hold for major clues, European and U.S. futures indicate caution. Investors are on the cusp of clearer cues from the economic figures, with any large shocks in the figures able to swing the markets either way and have a possible impact on the overall sentiment on the European and the US stock markets.

Major Index Performance Through Thursday, August 14, 2025

- Nasdaq: at 21,713.14, higher by 0.14% on the day.

- S&P 500: At 6,466.58, up 0.32%.

- Russell 2000: 2,147.63, up 2% to a six-month high

- Dow Jones: to 44,922.27, up 1.04%.

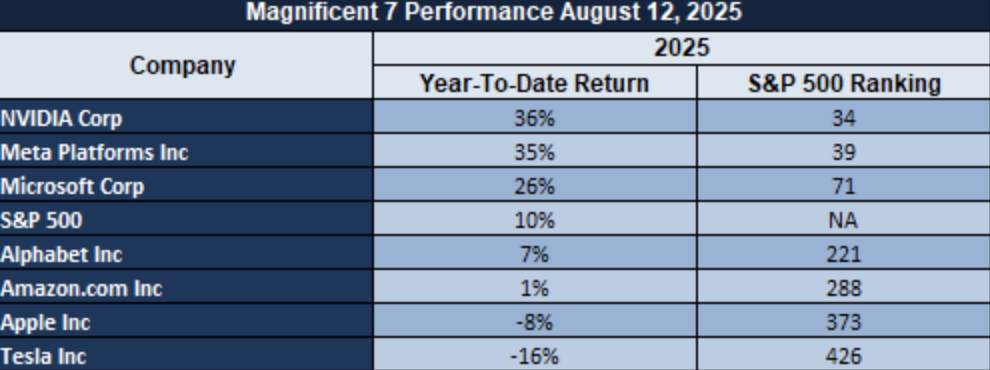

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are facing significant declines. On average, these stocks are down by over 18% from their recent highs, pointing to a potential market recalibration. This signals that the high valuations associated with AI-driven growth stocks may be unsustainable, putting pressure on broader market sentiment. As these stocks play such a pivotal role in the S&P 500, their underperformance continues to weigh on the index, and without a renewed push from these tech giants, the S&P 500’s ability to maintain its momentum will be challenged.

Drivers Behind the Market Move – Thursday, August 14, 2025

Thus far on Thursday morning, European and U.S. stock futures are even with U.S. futures hovering near the flatline after the healthy S&P 500 and Nasdaq Composite increase to new lifetime highs. S&P 500 and Nasdaq 100 futures are even, showing investors’ anxious optimism after the S&P’s new lifetime high on Wednesday. Dow Jones Industrial Average futures are slightly higher by 13 points, or 0.03%, showing modest gains. The even open is a sign of wait-and-see by investors taking in near-term levels of the top of the range and awaiting subsequent economic reports for guidance on the markets.

1. Expectations of Economic Data Release

The main reason for the conservative trend is anticipation of reports on Thursday, including the weekly jobless claims for the week ended August 9 and the Producer Price Index (PPI). Investors are focused on the reports so as to gauge the extent of inflation pressure and the state of the economy. Economists project a PPI of 0.2% in July after the flat lines in the month of June. Any shock in those figures will have a major effect on the extent of anticipation in the markets regarding moves by the Federal Reserve, for example, the reduction of interest rates in the September meeting. With the reduction of interest already on the cards in the market, traders are anticipating the validation by such reports.

2. Market sentiment impact of Trump President

Trump’s most recent comments have fogged the market atmosphere. His comments on the Federal Reserve and the nomination of a new chairman have fueled speculation about potential future monetary policy. Trump’s move to select a new Fed Chairman in advance—on the lines of 3-4 names—is an indicator of possible change in U.S. monetary policy. It has generated uncertainty, with markets eagerly awaiting to know whom would be selected and how this new leader would guide future rate decisions. Even the possibility of a more dovish or hawkish Fed under the new chairman has the ability to impact larger asset classes like equities, bonds, and commodities such as gold.

3. Blended European Market Sentiment

In Europe, the mood remains modestly risk-off in the leadup to critical growth figures for the EU and the UK. Though European futures have modestly firmed, the concern regarding economic growth in the continent has kept investors in a state of unease. Both of those factors, coupled with the universal impact of global inflationary pressure and the potential for monetary policy shifts, has the more defensive tone dominate European markets. The flattening of European and US futures is an indication of universal investor discomfort in the leadup to new economic cues which may determine the trajectory of equity markets in those areas.

Digesting Economic Data

The Trump Tweets and Their Implications

President Trump’s recent comments and tweets have had major effects on domestic policy and world markets in the recent past. His views on a number of issues like economic policy, law and order, and foreign relations have elicited quite substantial investor attention. Most notably, his comments on the Fed have created diverse speculations regarding future monetary policy. Trump’s move to reveal a new Fed Chairman in advance—is in the range of 3-4 candidates—gives rise to elevated potential for changes in U.S. monetary policy. It has raised alarm, with markets speculating nervously about who will be appointed and the new direction of movement for future action in the rate. A possible more hawkish or dovish Fed with new leadership has the potential to have implications on major asset classes like equities, fixed income like bonds, and commodities like gold.

Trump’s comments about the foreign policies of the U.S. with European leaders and with President Zelensky have made the geopolitics complicated. Trump’s comments about the requirement for “giving up territory” in the war in Ukraine and with Russia point toward a less diplomatic foreign policy approach, and such a move could lead to shifts in U.S. foreign policies. Such thinking will impact world markets, particularly energy and defense stocks, since any shift in the direction of waging peace or war in Ukraine would significantly impact the global oil price and defense budget. Investors must consider the direction in which the political processes are going to proceed and whether such moves can lead to more conflict or the potential de-escalation of conflict areas. On top of this complexity, Trump’s comments on national issues, including crime in the national capital, have raised concern about federal overreach. Calls by trump for a 30-day police takeover of Washington DC and a national template on combatting crime have added concern about overreach and the public perception of enhanced policing to the equation. The comments may have implications for the law enforcement, private security, and real estate sectors, especially in urban regions. While some investors interpret the comments as displaying effective leadership and stability, other investors may interpret the comments as a political farce subjecting civil liberties and local authority to possible upheaval in the domestic market.

In short, the latest remarks by President Trump have signaled the convergence of domestic and foreign policy overhauls with possible wide-ranging implications for financial markets. The President’s control over Fed leadership, geopolitics of Ukraine, and current controversies over domestic law enforcement policies will continue to be key concerns in investors’ minds in the future. We are monitoring closely the developments at Zaye Capital Markets as the latter can influence sentiment and dictate asset direction over the next several months.

Misery Index Hits 6.9% In July 2025: A Sign Of Economic Distress?

The U.S. misery index, the principal gauge which links inflation and unemployment together, in July 2025 reached 6.9%, a budget squeeze for consumers by and large. The 6.9%, the highest in the early 2000s, is the indicator of increased prices and deteriorating employment. The implication of increased inflation and deteriorating employment is the sign of possible economic limitation, yet the index remains significantly short of the 1980s’ stagflation peak of 21.9%.

Previous to this, a high misery index has accompanied reduced consumer spending, as noted in a 2023 report from the IMF. A blend of inflation and unemployment rates, the index can act as a leading indicator of downturns in the economy. With the IMF’s July 2025 World Economic Outlook that places the global growth in the 3.0% to 3.3% range, any significant shift could further strain domestic spending. Market commentators would do well to note closely changing consumer sentiment, that generally declines when the misery index is rising.

Based on economic indicators, part of the stocks look to be undervalued, i.e., consumer goods and discretionary companies, since they immediately come under the effect of a change in spending patterns. These stocks must be tracked by analysts, especially those with good fundamentals but susceptible to the ongoing pressure in the economy. Observe consumer spending trends and any indications of moderation in business earnings, which could further weigh on the stocks in these groups.

Decline In Demand For C&I Loans Signals Economic Slowdown Ahead

Net commercial and industrial (C&I) loan demand, as the recent graph depicts, has fallen by July 2025, and banks’ net percentage of increasing demand has fallen down to -28.0% for medium-size businesses. That is a very steep decline, in line with the level in the Federal Reserve’s Senior Loan Officer Opinion Survey, which registered the same in Q4 2024. Stalling of borrowing is the indication of businesses getting prepared for the economy to slow down and thus the growth outlook becomes cautious.

This fall is also reinforced by the National Bureau of Economic Research in the paper released in 2023, in which the authors calculated that higher interest levels, up to 2025, can cut business lending by 15-20% as companies have increased costs of capital. The next fall in borrowing can indicate business expansion and investment postponements and build up the risk of the whole economy slowing down. Market analysts should turn the attention to the credit conditions’ evaluation and the effects on the business activity.

While there have been previous precedents such as in the case of the 2008 financial crisis with the same drop in loan demand, the case is different in the case of repeated inflation above the Fed’s 2% tolerance level. Sustained inflation with sub-borrowing levels raised questions regarding the sustainability of the economy and is a sign of underlying weakness on the part of the economy. Cost of borrowing-sensitive and under-valued shares in the real estate and industrials sector are the probable losers.

Persistent Core Services Inflation Challenges Economic Slowdown Narrative

Core service inflation minus shelter rose 3.8% annually in July 2025, as the graph illustrates, indicating the consistent pressure of inflation, compared to the total CPI rise of 2.7%, which indicates the comparatively resilient character of service demand in the face of the declining housing factor. The disparity indicates the complexity of the inflationary processes in which services continue to push the prices higher even though some of the markets are experiencing relief.

This trend is consistent with the repeated concern of the Federal Reserve with the expansion of the core services as a signal bearer. National Bureau of Economic Research (NBER) evidence reveals that the removal of volatile shelter prices provides a clearer image of the underlying demands and hence plays a critical role in the July 2025 Fed decision to keep the federal funds range intact at 4.25%-4.50%. With the pressure still remaining in the services sector, the Fed remains cautious and keeps strict vigil on signs of inflation which time and again burst the scenario of the slow economy.

Unlike recent reservations about tariffs and softer jobs data, which had fueled hopes for rate cuts, stickiness in services inflation is the contrary, going against the script of a close-economic slowdown, at the benefit of the Fed’s prudence. On this premise, economists would have to closely observe the inflation-sensitive industries such as healthcare and consumer services, where ongoing squeeze on prices could signal likely overvaluation in the near term, and closely observe the Fed’s stance in the future.

Small Business Hiring Is Accelerating While Compensation Is Slowing: Is This A Labor Market Shift?

Smaller business hiring plans jumped in July 2025, said NFIB, but pay plans fell, indicating it to be a policy shift. The trend, aided by the U.S. Bureau of Labor Statistics release of the 4.1% unemployment rate, indicates that companies prefer bringing on employees rather than giving pay increases. Ease of labor market tightness seems to affect business strategy, potentially creating a more consistent stream of labor.

This trend is not like post-2020 recovery trends where the companies increased remuneration to hold on to employees amid the “Great Resignation,” according to the 2022 National Bureau of Economic Research working paper. The unforeseen acceleration in voluntary resignations by the scale of 47.8 million employees was a gauge of unprecedented workforce upheaval. The new trend could indicate the return to the relatively more stable workforce, or the likelihood of further offshoring as the companies respond to economic pressures.

If one goes back and examines history, such as the financial crisis of 2008, one can observe the same pattern of diverging hiring expansion and flat wages, examined in the 2010 paper in the Journal of Economic Perspectives. Thus, small companies may be mitigating the impact of economic uncertainty by emphasizing expansion of the workforce but using technological advances or offshoring to reduce wage expansion. Sensitive labor cost industries are those where observers must remain vigilant, as the pattern has the potential to impact probabilities and valuations, most notably in industries where flexible and low-cost labor forces are most prominent.

Bank Lending Standards Relaxed July 2025: Highlight Of A Credit Conditions Stabilization

In July 2025, the net percentage of banks increasing lending standards on commercial and industrial (C&I) loans fell markedly, by Federal Reserve figures. After a multiyear increase, the ease may indicate credit levels are returning to normal after unprecedented monetary tightening in 2023. The pattern may indicate a move away from crisis caution to more normal lending practice as the economy adapts to changing monetary policy.

Similar peaks in bank tightening of lending standards occurred during the 2008 financial crisis, so the recent relaxation of the tightening can be interpreted as going back to more stable and uniform credit conditions. The reversal of optimism in the banking and economy in general may be disguised by the banks’ relaxation of lending in the name of greater financial stability.

In research in 2022 for Journal of Financial Economics, there is correspondence of tighter lending policy with fewer loan applications when there are higher interest payments. Thus, the ease in recent months could signify better economic times than a policy decision made on whim. The investors will have to carefully observe credit-sensitive sectors like manufacturing and real estate in a bid to identify the net effect on business expansion and investment. Firms that use credit to expand can make use of the ease in credit policy.

Upcoming Economic Events

GDP, PPI, Jobless Claims, and President Trump Speech

In a critical week for the markets, Zaye Capital keeps a close eye on some economic data highlights throughout the week. With GDP growth announcements, inflation, initial jobless claims, and a first speech by President Trump, every announcement will reveal a lot about the economy and can have substantial impacts on investor attitudes and stock trading. Below is a more detailed explanation of what to look out for in each of the announcements and how the market should react based on the values ahead of or behind the expectation:

GDP m/m & Prelim GDP q/q

Release of the GDP numbers will provide a key indicator of economic activity and growth.

- A better-than-projected GDP reading will most likely translate into the American economy growing at a healthy rate. In such an event, risk assets can expect a boost, with stocks—particularly cyclical stocks—higher on the hope of positive expectation in business and consumer spending.

- Lower-than-forecast GDP reading, conversely, might spook investors regarding the potential slowing down of economic activity. In such an event, there will be a risk-off sentiment in the financial space with stocks underperforming and bonds benefiting on the back of investors’ flight to safe-haven instruments. That will also pressure the Federal Reserve into contemplation of dovish policy measures, including a reduction in interest rates.

Core PPI m/m & PPI m/m

The Producer Price Index (PPI) is the primary measure of the wholesale-level inflation, and a stronger than anticipated PPI has economy-wide implications.

- A stronger than anticipated PPI would most definitely validate the sticky inflation view most clearly seen on the production side of business and would have companies on the goods-producing side of town paying more cash. That would raise the expectation of the Fed maintaining the hawkish path and could push bond yields and the U.S. dollar higher. That would compress shares, led most clearly by the growth-sensitive component most sensitive to the spike in interest charges.

- A soft PPI print would validate the view of abating inflation pressure and one where the Fed would have greater leeway to adhere to current policies and even assume dovish policies. That would most definitely cause a shares rebound, led most clearly by the risk-sensitive component, and slice bond yields as investors overestimate the more benign inflation environment and the implications for even easier money policies down the road.

Unemployment Claims

Weekly unemployment claims is roughly as real-time of a measure of labor market health, and any miss of expectations will come under close scrutiny.

- A below-estimate unemployment claims release would inform us the labor market is healthy and bodes well for consumer spending optimism and the economy remains healthy. In this event, the stocks in cyclical sectors—consumer discretionary, financials, and industrials—would be healthy in light of increased levels of employment providing support for economic growth.

- But rising claim levels above estimate have the potential to signal labor market weakness, and concerns about diminished consumer optimism and slowing the economy would follow. In this event, a safety flight would follow, with investors moving into defensive sectors such as healthcare, utilities, and consumer staples, and bonds can participate in increased buying as the yield falls.

President Trump Speaks

President Trump’s speeches are often a market-moving event, especially given the ongoing economic and geopolitical uncertainties. In his speech,

- if President Trump signals aggressive trade policies or tariff hikes—particularly towards China or Europe—markets could react negatively, with equities falling as risk sentiment diminishes and the U.S. dollar strengthening on demand for haven assets. Any mention of tougher policies could further heighten concerns over inflation and global trade disruptions.

- On the other hand, if President Trump hints at policy easing, such as pursuing lower interest rates or de-escalating trade tensions, it could spark a relief rally in equities, with investors cheering a more favorable economic environment. In this case, we could see a broad-based rally across risk assets, with equities, particularly in the tech and consumer sectors, benefiting from an optimistic growth outlook.

With this pivotal week ahead of us, investors would do well to keep a close eye on those economic reports, and those will guide next move Fed expectations and garner essential insight into the state of the American economy. At Zaye Capital, we’ll keep a close eye on those events and their impact on asset prices and position ourselves optimally to react to new information in the markets.

Stock Market Performance

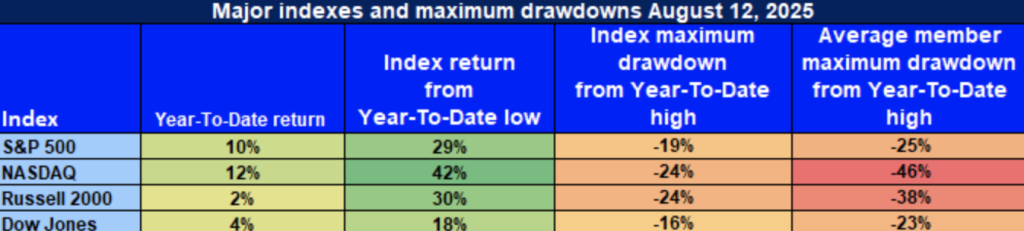

Indexes Rebound from April Lows, But Underlying Weakness Remains

At Zaye Capital Markets, we continue to monitor the recovery in the market since April 8th that has been underscored by large headline gains among major indices. Underneath the gains, however, a closer look reveals widespread drawdowns and negative breadth, demonstrating that volatility and selective leadership in the equity markets continue. As of August 12, 2025, the recovery remains uneven, and underlying market weakness continues.

S&P 500: Robust Rebound, Slim Participation

YTD: +10% | +29% off April low | -19% from YTD high | Avg. member: -25%

The S&P 500 has recorded a healthy 10% year-to-date advance but bounced 29% from April lows. The index, however, is still 19% below its YTD highs, with an average drawdown of -25% for its components. This means the rebound is focused in a limited group of large-cap names, which has left a lot of individual stocks in the red. Investors need to remain cautious because such narrow participation is a sign of danger to the wider market if leadership becomes less sturdy.

NASDAQ: Strong Gains Obscure Deeper Woes

YTD: +12% | +42% off April low | -24% from YTD high | Avg. member: -46%

The NASDAQ has been at the forefront of the rebound, rallying 42% from its April lows and posting 12% YTD returns. Yet, beneath this headline performance is considerable weakness. The index itself remains 24% off its YTD highs, and its average component has experienced a whopping -46% drawdown. These figures underpin risks in the tech-heavy NASDAQ, where growth stocks continue to languish, and overall market health remains concerning despite the rebound in individual stocks.

Russell 2000: Small Caps Rise, But Broad Pain Persists

YTD: +2% | +30% off April low | -24% from YTD high | Avg. member: -38% The Russell 2000 is up 30% from April lows, but only up a modest 2% YTD. Even with this bounce, the index is still 24% off of its YTD high, and the average drawdown among its constituents is -38%. This speaks to the unevenness of the recovery, as small-cap stocks—usually more economically sensitive—continue to struggle significantly.

Dow Jones: Defensive Tilt Provides Stability

YTD: +4% | +18% off April low | -16% from YTD high | Avg. member: -23% The Dow Jones has been more stable, showing a 4% YTD return and an 18% bounce from its April lows. Its drawdown from the YTD peak is the shallowest at -16%, and its average constituent has experienced a comparatively lighter -23% drawdown. This recovery, led by defensive and value-based sectors, is more balanced than that of the growth-laden indexes and indicates that conservative strategies might be better suited for today’s environment.

At Zaye Capital Markets, we maintain a cautious yet opportunistic stance, focusing on fundamentally strong companies. We are closely watching market breadth and volatility to navigate this selective and uneven market environment, ensuring we remain well-positioned for potential opportunities while managing risks effectively.

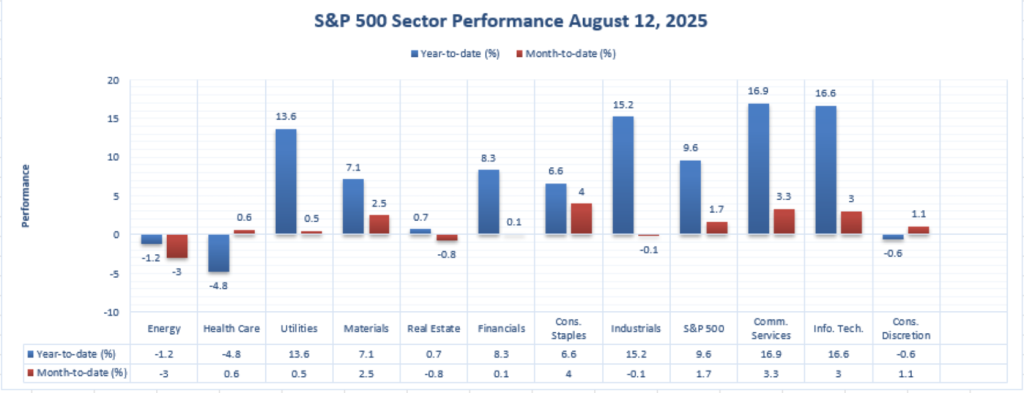

The Strongest Sector In All These Indices

Technology And Communication Services Continue To Lead Market Momentum

Up to August 12, 2025, S&P 500 sector performance testifies to overwhelming victory of the fast-growth and innovation-based sectors. In Zaye Capital Markets here, our research testifies to overwhelming victory of the Communication Services and of the Technology on top of the YTD leaders and still in the lead in the world and reclaiming the first spot in the new world economy.

Information Technology

YTD: +16.6% | MTD: +3.0%

Information Technology is still leading with a strong 16.6% year-to-date advance. That’s backed up by a 3.0% month-to-date increase, which is forecasting further strength. Leading drivers in the group are progress in AI, software, and semi conductor expansion. All of those sectors are still at the forefront of diversified investment attention, and technological advances are giving the group strong tailwind support.

Communication Services

YTD: +16.9% | MTD: +3.3%

Communication Services is ahead by a narrow margin of Information Technology with a 16.9% YTD increase. A 3.3% month-to-date increase is typical of the increased use of the internet-based media, platforms, and telecommunication. As more consumers make use of digitals services and media use increases, the industry has been driven by consistent growth in telecommunications services, advertising, and video streaming and thus continues to be a market-leading industry.

Both of these regions not only have surpassed the S&P 500’s aggregate YTD gain of 9.6% but have also displayed consistent momentum, beating most other groups on a month-to-month basis. In the eyes of Zaye Capital Markets, the consistent outperforming is seen as proof of broad-based leadership in tech-based industries in the securities markets. But caution is advised for the simple fact of the risks of over-torqued valuation and concentration in the regions under consideration. As with most things in life, selective stock selection still predominates in managing exposure in a marketplace still showing opportunities and risks in equal measure.

Earnings

Earnings Report: August 13, 2025

- JBS N.V. (JBSS)

JBS N.V. reported challenges in its beef segment, where it faced deeper losses due to the smallest U.S. cattle herd in decades. The company noted that increased costs and reduced margins in its largest operation were taking a toll. Despite these difficulties, JBS is focusing on strategic investments in emerging markets and operational efficiencies to navigate these challenges. Investors will be closely watching how the company manages these headwinds and whether it can sustain profitability in its other segments.

- Performance Food Group Company (PFGC)

Performance Food Group exceeded expectations for the fourth quarter of fiscal 2025, reporting adjusted earnings per share of $1.55, surpassing the forecast of $1.45. Revenue for the quarter was $16.9 billion, also above expectations. The company highlighted an increase in cash flow from operating activities, driven by higher cash-based operating income. This consistency in performance underscores its ability to leverage strategic initiatives effectively, providing confidence in its outlook.

- StandardAero, Inc. (SDA)

StandardAero posted stable second-quarter results with revenue of $1.53 billion, showing no year-over-year growth. The company expressed confidence in achieving its fiscal 2025 guidance, citing a strong first half of the year. Despite some market challenges, StandardAero’s resilience and its positive outlook for the remainder of the year reflect an underlying strength, particularly in its key service segments.

- Loar Holdings Inc. (LORL)

Loar Holdings reported robust second-quarter results, with net sales rising 26.9% to $123.1 million. Net income surged 118.7% year-over-year, reaching $16.7 million. The company raised its full-year 2025 adjusted earnings per share guidance, now expected to range between $0.83 and $0.88, up from previous estimates. Loar also announced the acquisition of Beadlight Limited, further expanding its product offerings and market reach, which could fuel future growth.

- Brinker International, Inc. (EAT)

Brinker International reported a 24% increase in comparable restaurant sales in the fourth quarter, leading to total revenues of $1.46 billion. Net income rose to $107 million, or $2.30 per share, marking a significant improvement from $57.3 million a year earlier. Chili’s performed exceptionally well with a 23.7% same-restaurant sales growth. The company also announced a $400 million stock buyback and provided a strong outlook for fiscal 2026.

Earnings Report: August 14, 2025

- Alibaba Group Holding Ltd. (BABA)

Alibaba is expected to announce its earnings for the fiscal quarter ending June 2025 on August 14, 2025. Investors will focus on updates regarding the company’s cloud computing segment and its international expansion efforts. Additionally, the performance of Alibaba’s e-commerce platforms and its ability to navigate regulatory challenges in China will be key points of interest. The company’s guidance and strategies for future growth will be closely watched.

- Applied Materials Inc. (AMAT)

Applied Materials will report its fiscal third-quarter 2025 results on August 14, 2025. The market will be watching for updates on its performance in the semiconductor equipment sector, particularly in AI chip manufacturing and advanced packaging technologies. Investors will also look for guidance on capital expenditure trends and any insights into how the company is positioning itself amid global supply chain challenges.

- Deere & Company (DE)

Deere is set to release its third-quarter fiscal 2025 results on August 14, 2025. Analysts expect earnings of $4.58 per share on $10.3 billion in sales, a decline from last year’s Q3 earnings of $6.29 per share on $11.4 billion in sales. Deere’s revised 2025 net income forecast, which was downgraded due to the impact of tariffs on steel and aluminum and lower farm income, will be closely scrutinized by investors for insights into the company’s outlook.

- NetEase Inc. (NTES)

NetEase is expected to report its second-quarter 2025 results on August 14, 2025. Investors will focus on the company’s performance in the online gaming sector, particularly in mobile and international markets. Updates regarding regulatory developments in China and their impact on NetEase’s operations will also be key points of interest. The company’s strategies for future growth and user engagement will be watched closely.

- Nu Holdings Ltd. (NU)

Nu Holdings is scheduled to release its second-quarter 2025 results on August 14, 2025. Analysts will look for updates on the company’s digital banking platform, customer acquisition metrics, and its expansion into new markets. Investors will also be keen on understanding any changes in credit risk profiles and the company’s progress towards profitability, especially in its rapidly growing digital banking segment.

- Quantum Computing Inc. (QUBT)

Quantum Computing is expected to report its second-quarter 2025 results on August 14, 2025. Investors will be watching for any advancements in quantum hardware and software, as well as partnerships with research institutions. The company’s progress towards the commercialization of quantum technologies and its ability to secure strategic partnerships will be key factors in its long-term outlook.

Stock Market Report – Thursday, August 14, 2025

American stock exchanges have opened for the day with the majors going up after keen expectations of the reduction in the interest rate by the Federal Reserve. Investor sentiment has also been boosted by recent cues of the economy demonstrating mild inflation and new demands by President Trump for relaxation in money supply. S&P 500 and Nasdaq Composite have established new all-time highs and the Russell 2000 index, the gauge of the small-cap stocks, has also given satisfactory returns.

Stock Prices

Economic Indicators and Geopolitical Developments

The American equity boom is owed to a mix of factors:

- Interest Rate Outlook: Traders are pricing in the full expectation of a 25 basis-point cut in the Fed interest in September, says the CME’s FedWatch Tool.

- Inflation Data: Consumer Price Index in July increased 0.2% in the month, as anticipated, and alleviated fears of rampant inflation.

- Presidential Leadership: The public declarations of President Trump showing support for reducing interest rates and guiding the economy have increased investor confidence.

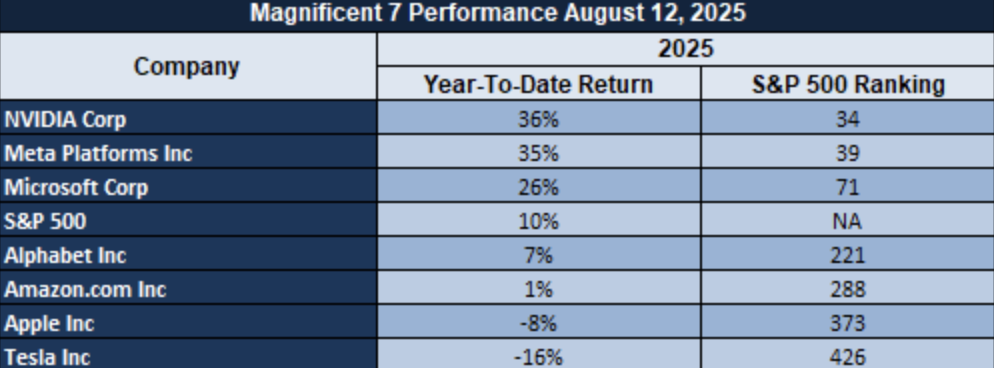

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—are facing significant declines. On average, these stocks are down by over 18% from their recent highs, pointing to a potential market recalibration. This signals that the high valuations associated with AI-driven growth stocks may be unsustainable, putting pressure on broader market sentiment. As these stocks play such a pivotal role in the S&P 500, their underperformance continues to weigh on the index, and without a renewed push from these tech giants, the S&P 500’s ability to maintain its momentum will be challenged.

Latest Share News

- $AAPL To Create Robots and Human-Like Siri in AI Drive

Apple is lining up for a massive foray into the AI space with fresh devices like the table robot companion in the pipeline for release in 2027. Apple also plans to upgrade Siri to make interacting with Siri much more natural, reviving the company’s goals in terms of innovation within AI. Shareholders are looking forward to the extent of improvement the new technologies have in the company’s product line and future growth opportunities.

- NVDA Reportedly Postponing Rubin To Review Before $AMD’s Launch Of MI450

Nvidia, by reports, has delayed introducing its Rubin AI chip in order to pre-empt the release of the MI450 by AMD. The strategic delay is evidence of the game of competition in the world of semiconductors where Nvidia is determined to maintain the hold on the AI and machine learning space. Investors are keenly observing the next move by Nvidia as it prepares to counter the recent releases by AMD.

- $AMZN Ad Business Is Very Real

Amazon’s advertising unit has expanded enormously, now generating almost 25% of the company’s e-commerce sales. This business, once insignificant to the company, is increasingly important as a growth driver for Amazon, acting as solid diversification to its classic retailing and cloud businesses. Investors should be paying close attention to how Amazon continues to gain from the explosive growth in the digital advertising space.

- U.S. Hides Trackers in Shipments of AI Chips to Catch Diversion to China

The U.S. government has apparently been slipping trackers into many AI chips, such as Dell and Super Micro Computer (SMCI) with processors from Nvidia and AMD, in an attempt to keep sensitive technology from reaching China. Attempts to enact the 2022 export controls might have supply chain implications for the chip and potentially larger regulations in the tech arena. Investors need to account for the potential disruptions the action might have in the global tech arena.

Major Index Performance Through Thursday, August 14, 2025

- Nasdaq: at 21,713.14, higher by 0.14% on the day.

- S&P 500: At 6,466.58, up 0.32%.

- Russell 2000: 2,147.63, up 2% to a six-month high

- Dow Jones: to 44,922.27, up 1.04%.

We are following sector rotation and positioning closely, and not just because the volatility in technology stock persists and persists, to position in front of the changing environment in the markets.

Gold Rate Today – Thursday, August 14, 2025

Gold prices have hit all-time highs as spot gold climbed to $3,367.53 an ounce, increasing by 0.4%, and December U.S. gold futures climbed 0.3% to settle at $3,416.70 an ounce. The surge is driven by a myriad of factors, including the weakening of the American currency and falling Treasuries yields as markets expect the probable Federal Reserve interest rate cut in September. Moreover, tensions in the geopolitical scene, including the war in Ukraine and U.S.-Russia diplomatic tensions, have boosted the purchase of gold as a safe-haven asset and pushed its prices up.

Bullish sentiment in the metals also got support from recent economic reports like initial unemployment filings and the Producer Price Index (PPI). These reports have encouraged investors to expect the Fed to go dovish with declining inflation pressure and have uplifted the spot prices of gold. But where there is improved-than-expected growth in the economic reports, interest-rate reduction expectations can have a dampening effect and spill over into the gold’s performance. At Zaye Capital Markets, such development is always on our radar in order for us to observe the possible risks and opportunities ahead of the gold in the short term.

Oil Prices – Thursday, August 14, 2025

Brent is currently valued at $65.91 a barrel and West Texas Intermediate (WTI) at $62.89 a barrel after recent declines and a combination of economic and political setbacks have prompted a modest back-and-forth bounce. Both are up in part on risk premiums in advance of President Trump’s upcoming summit with President Putin, and concerns about possible global oil supply changes. Threats by Trump of “severe consequences” in case the Ukraine war doesn’t stop, and changes in policy on sanctioning Venezuelan export of crude have caused oil complex volatility. Hopes of a cut in the Fed interest rate have added to the oil market volatility and have had implications on oil prices.

The financial news of yesterday also impacted sentiment within the market and the EIA reported the crude stocks up by 3.0 million barrels, suggesting possible supply excess problems. The IEA lifted the 2025 and 2026 world oil supply predictions based on higher OPEC+ and non-OPEC production, with weak global demand growth. This has increased the fears of supply overhang of the type that would pull oil prices lower. In the short term, economic news like claims for unemployment and GDP will have key roles in giving guidance for oil prices in the days to come. Positive information that is better than expected can buoy the oil prices and demand, but worse-than-expected information can continue to put the pressure as the fears about the growth in the economy continue to dominate the markets. At Zaye Capital Markets, we are aware and watching the developments for the effect on the oil market.

Bitcoin Prices – Thursday, August 14, 2025

Bitcoin has touched a new high of $124,002.49, fueled by rocketing institutional interest as well as favorable U.S. policies. With the crypto-friendly Trump policy, which has inducted the crypto assets into the 401(k) retirement plans and the formation of a Strategic Bitcoin Reserve, investor sentiment has improved significantly. Furthermore, the expectation of the interest rate cuts by the Federal Reserve, which have drained the value of the U.S. dollar, has also contributed to the spottiness of the alternative asset in the form of Bitcoin. The same upward trajectory of Bitcoin in the rest of the cryptocurrency space is being seen with Ethereum and other altcoins on the upswing as well.

The economic releases yesterday, including initial unemployment claims and the Producer Price Index, indicated soft labor and inflation and buoyed the likelihood of a dovish Fed turn. This favorable economic backdrop, together with positive regulation releases, has pushed Bitcoin to new heights. For us in the coming days ahead, the PPI and the day’s GDP will frame the path of sentiment in the markets definitively. Moderately better-than-anticipated readings may moderate the expectation of the rate cut and filter into the prevailing momentum in Bitcoin. At Zaye Capital Markets, we monitor the reports quite closely to determine their effect on Bitcoin and the general crypto environment.

ETH Prices – Thursday, August 14, 2025

The current spot price of Ethereum (ETH) is $4,771.49 with a price hike of 2.9% from the last session. This is being driven by aggressive buy demand by institutions with a new record injection into Ethereum ETFs and large whale trades. A group of whales, the “7 Siblings,” had sold ETH worth $88.2 million in the last 15 hours but another whale had sold ETH worth $50.6 million at a 20.2% premium from the prices, indicating a consistent switch back from profit-taking into strategic build-ups. This kind of activity is the hallmark of extremely volatile but dynamic markets where large investors and whales are intensely managing the swing in prices. Otherwise, Ethereum ETFs have seen inflows of more than $2.3 billion for the month, surpassing inflows into the ETFs of Bitcoin, indicating enhanced institutional confidence in Ethereum.

This institutional push fueled by positive regulatory advances and increased optimism about the scalability of Ethereum and the DeFi space has urged analysts to revise their ETH price forecasts upwards. Standard Chartered, for example, is targeting $7,500 by the year-end on the basis of expansion in Ethereum-based ETFs. But with ETH getting close to the critical levels of resistance, day traders have to keep short-term corrections in mind. Continued support to the current bull run still remains in the form of whale movement and institutional purchase, but the short-term movement can lose momentum as the forces of the market are in play.