Where Are Markets Today?

U.S. and European futures higher for first of the week as S&P 500 and Nasdaq futures up about 0.2%, and European indices 0.2% and 0.3% higher. Following new closing highs for the Nasdaq Composite and solid week-end close of the S&P 500 greatly fueled by recovery of shares of Apple. Positive mood is one of relief regarding coming data on inflation as well as renewed interest in high-level diplomatic meetings potentially significantly impacting world markets.

Motivating the sanguine mood is the U.S. inflationary environment. Marketplaces are looking for this week’s CPI reading and the median anticipates a +0.3% core CPI release and annualized core inflation of about 3.0%. Such a reading at or below expected levels will support a rate cut in September and one already factored out with better than a 90% chance following the ongoing growth worry. Politically, rumors of a Trump–Putin summit in Alaska and eventual relaxation of Ukraine sanctions have supported the mood with markets anticipating the potential ability for more global supply stability and trade flows.

Apart from geopolitics and inflation, corporate profit and trade are driving the pre-open optimism. Optimism that the August 12 U.S.–China trade truce expiry will be extended has eased concerns of a breakdown of trade tensions and lifted the mood among investors in U.S. and European markets. Moreover, the mega-cap and AI-related stocks’ strength thus far of stocks like Nvidia, AMD, Apple, Tesla, and Alphabet is still supporting market activity and a sign of leadership by industries of good earnings visibility and structural growth drivers.

Recent Market Conditions at Zaye Capital Markets With equities supported by benign inflation expectations, easing of geopolitical tensions, and strong earnings support, we also see room for further near-term progress. Valuations are still rich, though, and markets will still be vulnerable to any surprise inflation upside or diplomatic negotiation disappointments. Sustaining the advance will demand more widespread participation than mega-caps because shallow base for markets will trim resiliency if tech strength dissipates. Inflation data and geopolitical events later this week will tell whether prevailing euphoria will be converted into stronger advance.

Major Index Performance as of Monday, 11th of Aug., 2025

- Nasdaq Composite: 21,450, slightly higher.

- S&P 500: 6,389, marginally higher.

- Russell 2000: ~2,100, flat to slightly positive.

- Dow Jones: 44,176, modest gains.

The Great Seven and the S&P 500

We witness growing proof of “leadership fatigue.” Following disproportionate advances, mega-caps are being punished when guidance fails to extend far enough to support assumptions recommended by AI, when capex intensity anchors near-term free cash flows, and when tariff controversy muddles margin transparency. There is concentrated ownership and puts the S&P 500 tactically in the mercy of any one behemoth’s surprise; index strength over the long term probably will necessitate wider participation than the central seven.

Drivers Behind the Market Move – Monday, August 11, 2025

As markets start on a positive tone, we observe three overall directional drivers operative today:

1. Direction of Fed Policy Hinges on Inflation Data

Sentiment remains on U.S. CPI data on Tuesday. Investors anticipate an 89–90% probability of a September cut provided that inflation remains close to estimate. Any kind of deviation of this kind—specifically above expected core inflation—would ignite the Federal Reserve to put easing on the backburner and crush expectations of loosening money and injecting volatility.

2. Geopolitical Trends and Trade Policy

Latest President Trump comments, one of which being tariffs having a spectacularly positive effect on the stock market, still stimulate risk appetite. Increasing spillover expectations that the U.S.–China tariff truce that is set to expire on August 12 gets prolonged and minimizes near-term policy uncertainty roughly equates tariffs proponents’ pairing of tariffs and stocks. Speculation of Trump and Putin meeting each other in Alaska has also stimulated markets and come along with favorable expectations of sanctions relief and better energy and trade dynamics.

3. The Resilience of Earnings in the Case of Policy Uncertainty

In spite of trade war conflicts and macroeconomic setbacks, stock markets remained resilient and backed up by solid corporate earnings, specifically those of tech and AI pioneers. These have maintained market superiority and facilitated broader swings and ongoing investor excitement. For Zaye Capital Markets, markets these days come into view as carefully in place—the waiting game for signals from numbers on inflation, looking closely at trade and diplomatic action, and counting on earnings strength. Extending this rally will depend on breadth extension and affirmation of a constructive policy view on the part of the Federal Reserve.

Digesting Economic Data

The Trump Tweets and Their Implications

The string of recent statements from US president Trump has confirmed the administration’s assertive foreign and domestic policy policies. At home, his call for a deployment of police officers in Washington as a battle against crime is typical of a new focus on public stability and safety for America’s inner-cities. This program, deployed effectively, could potentially support investor sentiment towards urbanization schemes and municipal debt issues through a proof of faith in protection and control. Concurrently, it could also facilitate high spending on the part of the federation and thereby act on fiscal dynamics at an extraordinary sensitiveness on the markets towards pressure on the budget.

Economically, the government action of opening the window for Fannie Mae and Freddie Mac initial public offers selling 5%–15% of shares is a move towards more market exposure for two of America’s largest firms in the US mortgage finance industry. The action could add more depth in the mortgage-backed securities market and perhaps limit taxpayer exposure. But it carries another layer of risk because investor demand for these issues will hinge on the broad trend of mortgage interest rates and house affordability.

Cross-worldwide, Trump’s announcement that next week he and President Putin will sit down and White House announcement that recent Russia talks “went well,” heralds a probable easing of some U.S.–Russia relations. Any easing will spill over on energy markets, i.e., oil and gas, as geopolitical risk premiums re-price. All else being equal though, the overall geopolitical context is still strained and markets will probably remain anxious until tangible policy shifts materialize out of said meetings. Most striking of all is Trump’s claim that tariffs are having a “huge positive effect” on the stock market and news of the average U.S. tariff rate rising 20.1%, a record high since the 1910s. Short-run benefits of stock markets through perceived national industry protection are at the possible cost of tariffs fueling inflation, taxing global supply chains, and discouraging global trade flows. This dichotomy puts investors in a quandary of reconciling the near-term protectionism benefit of favored industries with the longer-term macroeconomic risk that it engenders.

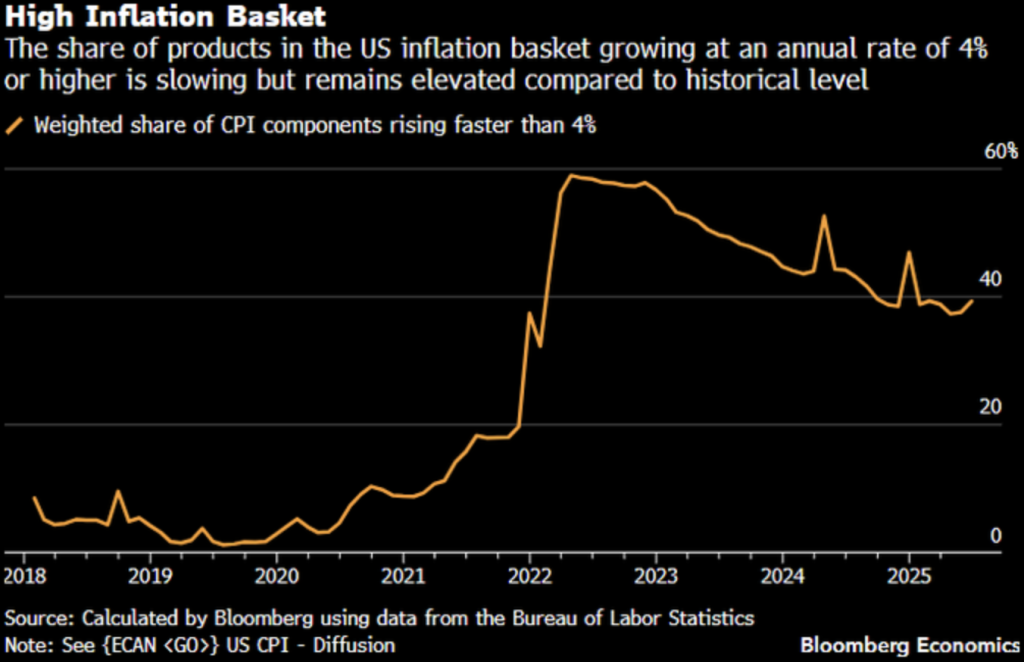

Inflation Cooling, But Structural Pressures Still A Risk

We see a significant moderation in U.S. inflation breadth, with the proportion of CPI components increasing more than 4% year-over-year declining from close to 60% in 2022 to about 40% in mid-2025. The moderation is a consequence of gradual dissipation of previous supply chain and energy price shocks. Nonetheless, underlying categories like housing and food persist in showing persistent price increases, continuing to exert upward pressure on the overall index notwithstanding the headline improvement.

Our research backs up the argument that these deep-seated sectors represent a formidable obstacle to long-term disinflation. Even as wider CPI measures moderate, such high-weight categories can provide a floor for general inflation. This threat is compounded by possible tariff actions debated during the 2024 U.S. presidential election, which the Federal Reserve Bank of Boston calculated would contribute 0.5–2.2% to core PCE inflation if implemented, which could undo recent gains.

In our view, this backdrop offers opportunity in consumer staples equities, where valuations have trailed earnings stability, rendering them undervalued. Analysts will want to watch the path of shelter and food inflation, along with policy indications on trade tariffs, to determine the longevity of the disinflation trend and front-run changes in interest rate expectations that would alter sector performance.

Home Ownership Drops to Six-Year Low as Affordability Crisis Deepens

We note a sharp decline in U.S. homeownership to 65% in Q2 2025, its lowest level since late 2019. The decline occurs amidst a sustained rise in interest rates and housing costs that have far exceeded wage growth, eroding affordability. While previous peaks above 69% in the early 2000s were a product of more accommodative credit conditions, today’s environment resembles post-2008 structural drags, with market access now increasingly constrained for first-time homebuyers.

The transition is underpinned by increasing rental demand, which jumped 15% in 2024, indicating a structural turn in housing need and preference. The shift has possible long-term socioeconomic ramifications, as falling ownership rates could impact wealth creation, social stability, and intergenerational opportunity, especially given studies connecting homeownership to better social and educational results.

We consider certain homebuilding and building material companies to be undervalued, especially those that have a concentration of affordable housing developments with robust order books. Analysts must monitor proposals for policy on mortgage lending criteria, incentives for housing supply, and interest rate movements, as these will be key to determining if ownership levels stabilise or carry on declining.

EARNINGS

Earnings – August 8, 2025

- Summit Therapeutics Inc.

While market attention was on Summit Therapeutics’ Q2 results, no official release had been made as of August 8. Consensus expectations pointed to a loss of ($0.10) per share, marginally better than the prior quarter’s ($0.09) loss. Investors maintained a cautious stance, awaiting confirmation of performance metrics and strategic updates in the forthcoming announcement.

- Lamar Advertising Company (REIT)

Lamar reported a steady quarter, with revenues rising 2.5% to roughly $579.3 million and net income increasing 12.7% year over year. Funds from operations reached $225.3 million, or $2.22 per share, supported by strength in national and local advertising and strategic acquisitions. However, rising costs remain a focal point for analysts monitoring margin sustainability.

- Plains All American Pipeline, L.P.

Plains posted an earnings beat despite a near 15% drop in revenue, driven by its $3.75 billion divestiture of the Canadian NGL business. This strategic asset optimisation helped offset top-line weakness and reflected management’s focus on maintaining profitability in a challenging midstream environment.

- Freedom Holding Corp.

Freedom Holding delivered 18% revenue growth to about $533.4 million in Q1 FY2026, boosted by a 60% surge in banking and an 18% rise in insurance revenue. However, net income declined 11.3% to $30.4 million, partly due to foreign exchange losses, prompting close watch on how currency volatility impacts profitability going forward.

Earnings – August 11, 2025

- Summit Therapeutics Inc.

Summit will not report earnings today; its Q2 release is now scheduled for August 12. Market sentiment is likely to build in the lead-up, as investors position ahead of the announcement.

- AST SpaceMobile, Inc.

AST SpaceMobile will post Q2 earnings after market close, followed by a 5:00 p.m. ET call. With no consensus estimates currently available, the focus will be on updates regarding adoption rates for its space-based broadband services and any operational milestones.

- Monday.com Ltd.

Monday.com reports this morning, with estimates at $0.84 EPS and around $293.6 million in revenue. Key watch points will be subscription growth trends, customer retention metrics, and margin trajectory in a competitive SaaS environment.

- Oklo Inc.

Oklo will release Q2 results after the close, with a 5:00 p.m. ET call. The previous quarter’s net loss of ($0.07) per share, significantly narrower than last year’s ($0.34), sets the tone for investor focus on capital efficiency, R&D allocation, and commercial rollout progress for its nuclear technology.

- United States Cellular Corporation

As of today, no official earnings details or estimates are available for U.S. Cellular. Investors will monitor corporate channels for updates and guidance on performance drivers.

Stock Market Wrap – Monday 11 August 2025

U.S. stocks start the week off on a cautious data-dependent note. Next day’s inflation report is near-term focus item that can re-make September rate cut likelihood as trade updates and top-level negotiations maintain geopolitics as a broad risk premium driver. Early signs indicate a slightly stronger risk appetite tone from tech, but breadth continues poor and headline hypersensitivity is high.

Stock Prices

Worldwide Politics and Economic Statistics

Three near-term drivers: (1) inflation—the consensus forecast is anticipating a robust core reading and that might influence September cut bets; (2) tariffs—the deadlines and enforcement talk continues to reverberate through the supply chains and margins; and (3) diplomacy—the this-week meeting in Alaska and push on Ukraine might influence the energy complex, the US dollar, and risk sentiment more broadly. A soft CPI will favor a string of expansion plays; a hotter print will risk a defensive rotation and higher real rates.

Latest Stock Updates

Following are the top 15 year-to-date 2025 performers and top indicating sector and company-specific strength:

$MP +377

$OKLO +255%

$PGY +209%

HOOD +208

$NBIS +148%

$PLTR +147%

$SYM +135

$CRCL +130%

$RBLX +123%

$ASTS +121%

HIMS +115

$JOBY +105%

$QBTS +101%

$CELH +97%

$NET +90

The Great Seven and the S&P 500

We witness growing proof of “leadership fatigue.” Following disproportionate advances, mega-caps are being punished when guidance fails to extend far enough to support assumptions recommended by AI, when capex intensity anchors near-term free cash flows, and when tariff controversy muddles margin transparency. There is concentrated ownership and puts the S&P 500 tactically in the mercy of any one behemoth’s surprise; index strength over the long term probably will necessitate wider participation than the central seven.

Major Index Performance as of Monday, 11th of Aug., 2025

- Nasdaq Composite: 21,450, slightly higher.

- S&P 500: 6,389, marginally higher.

- Russell 2000: ~2,100, flat to slightly positive.

- Dow Jones: 44,176, modest gains.

We will be selective—we pick quality on the balance sheet—at Zaye Capital Markets and will rebalance our exposure as tomorrow’s inflation print dictates the direction of rates and earnings multiples.

Gold Price – Monday 11 August 2025

The yellow metal is traded at $313.05 on the SPDR Gold Shares ETF and registering a mild withdrawal after recent gains. Market stays susceptible to recent updates and U.S. President Trump comments, including average U.S. increases in tariffs into 20.1% – highest since 1910s – and upcoming Russia’s President Putin trade meetings. These have been impacting gold as a geopolitical hedge to some extent as more tariffs tend to drive up prices and inflationary apprehension as well and also lead towards dislocation of supply chain. Unplanned data of the day on economy makes the traders more reliant on political news and trade policy anticipations as direction drivers of bullion prices.

Yesterday’s absence of economics data releases has preserved sentiment heavily driven through such geopolitical events as the market continues to be looking forward to tomorrow’s last reading on inflation. The confluence of high tariffs, diplomatic tensions, and subdued macro environment is underpinning the safe-haven stance of gold. Though the overall equity market is being underpinned through selective resilience in mega-caps, the underlying wariness in risk sentiment continues to underpin gold prices as investors position ahead of event risk of surprise on the higher end of inflation.

Oil Prices – Monday, August 11 2025

Brent stays near $66.00 per barrel and WTI near $63.30 both down as near-term supportive demand is overwhelmed by supply issues. OPEC+ Sept increases of 547,000 barrels per day and IEA forecasting weakest demand growth since 2009 has bolstered year-end supply surplus forecasts. This context combined with seasonally robust summer refinery runs is maintaining pressure on prices. Yesterday devoid of notable economics releases provided one-day respite during which sentiment became solidified as being very largely being driven almost entirely through fundamentals and geopolitical issues and left traders on the edge of their seats anticipating more market-sensitive releases.

Donald Trump’s remarks—including commenting on tariffs’ “huge positive effect” on the stock market and criticizing abrupt tariff increases on India for purchasing Russian oil and affirming meeting with Russia’s President that will materialize soon—are impacting oil on risk and demand sides. Flickers of pro-growth rhetoric provide support overall on market sentiment, though gigantic trade steps on major importers like India operate on future demand views, especially in Asia. With nothing significant in store on economics data for today, eyes look towards tomorrow U.S. inflation report capable of re-basing demand views: softer print has the ability of supporting prices of crudes through positivity on growth views while hotter reading has the ability of solidifying policy and capping upside saw on the energy market.

Bitcoin Prices – 11 August 2025 – Monday

Bitcoin is higher at $122,000 and powering August’s rally higher with a 7.4% advance thus far in the month. Institution buying is taking market share off available inventory and putting ongoing upside pressure on prices despite increasing mining costs following US Pres. Trump’s announcement of 100% tariffs on ASIC mining rigs that raise operating costs 21%. Policy change has the potential to squeeze miner margins and lead to slower near-term network and hash rate growth. Structural drivers of demand – supported by El Salvador’s announcement on rolling out world’s first Bitcoin bank and Coinbase’s announcement on enabling DEX trade for millions of assets – support adoption of Bitcoin as store-of-value and transactional currency and build increasing market and long-term adoption potential.

Lack of significant economic data yesterday retained the focus on crypto news and broader geopolitical themes. Trump’s call for tariffs’ “huge positive effect” on stocks and the average U.S. tariff rates increasing to 20.1% reflect a more protectionist trade climate, and this could initiate Bitcoin’s safe-haven theme among investors looking to own outside conventional fiat systems. Today, with minimal data release, traders will be searching for policy cues and the macro prints that will dictate the liquidity flows. A softer U.S. inflation print tomorrow will reduce real yields and provide more tailwinds to Bitcoin, and a hotter print will dampen speculative flows as risk assets reprice on tighter money expectations.

Eth Prices – Monday, 11 August 2025

Ethereum is up at $4,294.50 with intraday prices ranging between $4,171.87 and $4,324.59. Price action is being aided by historic whale and institutional buying volumes as over 1.03 million ETH worth ~$4.16 billion have been bought in the past 30 days. The buying spree has resulted in a 45% up move well and comfortably over the $4,000 barrier. ETF trades have also gone into overdrive as BlackRock’s iShares Ethereum Trust has seen $1.7 billion being invested over ten trade days as part of overall institutional inflows of over $7 billion over the past 30 days. This Whale and ETF buying partnership is aiding the classification of ETH as an Institution-level asset.

The positive swing is also sustained with continuous whale buys, including recent buys of another $667 million in value of ETH, which has taken the price through the resistance of $4,200. These flows reflect firm conviction of future adoption and usage of Ethereum and could be in the process of breaking higher into the $4,500–$5,000 zone subject to continued buys. But technical overbought levels suggest the trader needs to be alert to potential near-term corrections despite the overall trend.