Where Are Markets Today?

Equity futures start the day positively in the global arena, with US markets and European markets displaying an inclination towards risk-on trades. As of 24 October 2025, US stock futures are trading in positive territory but with low levels of enthusiasm. US traders continue to position themselves in anticipation of the September Core CPI, which is looked upon as a critical market-moving event for definition in terms of rate perspectives for the rest of the month. At the same time, European markets display weak positive bias due to positive overnight guidance from Wall Street but with a dampening effect from regional factors. Futures for the Stoxx 600 and the DAX display mild positivity with caution on traders’ part for venturing into risk territory in absence of macro definition.

The key catalyst behind such prudent optimism in US futures is the upcoming inflation reading, with the CPI/CPI Core prints wielding an outsize influence over assumptions on interest-rate paths. A strong number could spark a reset in Treasury yields with spillovers to technology and high-duration names, while a softer print could ignite a relief rally in equities, reinforcing notions of a dovish pivot in 2026. Meanwhile, market participants have had to incorporate a complex convergence of macro/political factors, with Trump’s escalation in tariff levels targeting China and military action in Venezuela bringing back tail risk, offsetting a technical futures buy program driven by the ongoing government shutdown/budget impasse.

Futures on the European markets are slightly higher but are range-bound. The traders on these markets are struggling with sticky region-wide inflation, the revival in the euro’s power, and fiscal policies in countries such as Germany, France, and Italy. Despite the trend in global rate cuts gaining momentum, the ECB’s stance is complex due to region-wide differentials in inflation, coupled with exposure to the energy markets. Further, with today’s Flash Manufacturing/Services PMIs in Germany, France, and the Eurozone actually scheduled for release, caution prevailed in market sentiment. Conversely, better-than-expected outcomes could boost equities; however, these would remain range-bound barring significant disinflation momentum. At Zaye Capital Markets, we view today’s futures markets in a global landscape characterized by a selective risk-on environment where volatility triggers are in evidence. There is a willingness to selectively re-engage with equities in Portfolio Construction but with extensive weighting on Macro Hedging strategies in place for now. Until there is clarity on Inflation, Central Bank Policy Directions, and sources of Global Geopolitical Risks, specifically regarding U.S.-China Trade Relations or EU Fiscal Harmonies, any futures market rallies would likely remain tactical rather than trend-anchoring in nature over the next 24-48 hours, critical in terms of sustaining Cautious Optimism versus likely shifts in Risk Appetite back to the Sidelines.

Major Index Performance on Friday, 24 October 2025

- Nasdaq Composite: Trading at ~22,942 (up ~0.9%)

- S&P 500: Trading at ~6,738 (up ~0.6%)

- Dow Jones Industrial Average: Trading at ~46,735 (up ~0.3%)

- Russell 2000: Trading at ~2,481 (up ~1.2%)

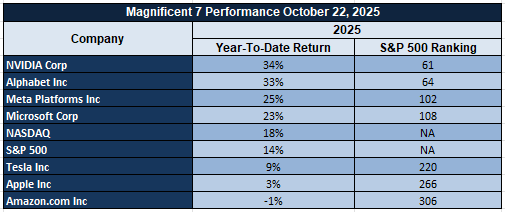

The Magnificent Seven and the S&P 500

“Magnificent Seven,” which comprises Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla, is facing renewed pressure in the ongoing week, which is an effect of margins, growth, and re-rating concerns on these stocks. As these stocks drive the S&P 500 heavily, their weakness is leading to an overall stagnation in the market. Until these stocks stabilize, the market is likely to face an upward constraint in November.

Drivers Behind the Market Move – Friday, October 24, 2025

At a time when U.S. and European market players are facing a rather fluid macro environment, market sentiment continues to remain in a state where it is evenly matched on either side. The factors influencing today’s market action include economically sensitive fundamentals, geopolitics from the U.S. administration, as well as structural issues in Europe.

1. U.S. Inflation Data Looms Over Risk Sentiment

All eyes are on today’s core/headline CPI numbers from the U.S., which represent a key pivot in influencing Federal Reserve expectations. Any potentially hot CPI number could drive yield curve volatility further and increase concerns over sustained tight-money policies, which would weigh on tech equities/high beta areas. Conversely, any softer number could serve as a positive equities-related catalyst in light of dampened aggressive rate views, which could be beneficial for growth names in particular. Against the ongoing U.S. government shutdown risk remaining unaddressed, today’s CPI number is a key influencing factor in terms of market momentum at the end of the month.

2. Trump’s Geopolitical Escalations Reignite Trade and Risk Premiums

The recent statements from President Trump, such as the confirmation that the tariff rate on Chinese imports would increase to 157% on November 1, frustration with Venezuela, and direct accusations against China on the issue of fentanyl smuggling, are reinserting the concept of geopolitical risk into financial markets. Despite the positive overture in the form of a meeting between President Trump and Chinese leader Xi, the tenor between these two governments has remained deliberately contentious on multiple fronts, making it more difficult for internationally integrated investments in equities, commodities, and other asset classes.

3. European Structural Headwinds Cap Optimism

The European markets are struggling to make way following the Wall Street trend of cautious optimism. The present Flash Manufacturing and Services PMIs in Germany, France, and the entire Eurozone are also likely to validate the state of economic stagnation due to persistent levels of inflation, coupled with their strong currencies. In addition, the uncertain policies implemented by the European Central Bank, together with the political disunity in major member nations in Europe, such as Italy and Germany, continue to obstruct an overall increase in market positivity.

In summary, it is a complex interplay between the presence of catalysts on the macro front versus political noise that is largely influencing market dynamics in today’s environment. At present, what is visible at Zaye Capital Markets is that investors continue to hedge their exposure ahead of inflation numbers while remaining vigilant on the geopolitics front.

Digesting Economic Data

The TRUMP Tweets and Their Implications

During the course of the last week, there has been a flood of so many press statements from the Trump administration, leading to uncertainty in the financial markets, mainly in terms of the volatile nature that could be adopted by policies in the coming global summits. Some of the major market-moving press statements made were on issues regarding China, Venezuela, and trade policies generally between the two nations, in which it is confirmed by Trump that the tariffs on Chinese imports would restart from November 1st. After the restart of tariffs on Chinese imports, it is apparent that it is happening at a time when supply chain risk is critical in many markets, including technology, petrochemicals, and manufacturing generally. Another issue mentioned in press statements is that Trump holds that “China is using Venezuela for the shipment of fentanyl,” with it being stated that that would be his “first question to President Xi in their meeting on Thursday.”

Threats of “land action in Venezuela” from Trump and his dissatisfaction with the Ukraine represent an escalation in worldwide tensions in geopolitics. Despite his disclaimers that B1 bombers were not operating off the Venezuelan coast, he did state that he could take direct military action with Congressional approval for supporting action on either land-based activities in alleged Venezuelan territory or for targeting drug cartels in that region, which could pose significant risks for regional instabilities within Latin America’s petroleum industry in terms of world-wide pricing for petroleum. At the same time, it has been acknowledged from the White House that any meeting between Trump and Putin has yet to be ruled out, so the tension between Eastern Europe is also likely to pose an ongoing risk for global geopolitics with ramifications for financial markets’ stability in gold, Treasuries, and defensive equities.

Domestically, other remarks from the “Shutdown Countdown,” including his views on the government shutdown, provided more clarity while also raising more questions. His assertion that $130 million in funds for military pay had been donated by a private source is an oddity that appears to underscore rising tensions in Congressional budget talks. He followed these with attacks on Democrats for “going totally crazy,” refusing an extension on federal pay, with the Senate rejecting a federal pay plan while rumors circulated on possible snap benefits for GOP lawmakers in an unprecedented display of federal fiscal system dysfunction potentially pressuring markets worried over consumption, government spending, and sovereign debt concerns. Other domestic legacy concerns from his term in office came from his challenge to reports on spending on ballroom construction costs in media accounts, claiming his budget perspectives were more prudent fiscal priorities in an apparent step likely to further politicize budget talks in markets in US markets. Possibly the most shocking and economically significant news is Trump’s pardon of Binance founder CZ (Changpeng Zhao) issued by the White House on grounds it is a constitutional issue, happening in the wake of overreach by the judiciary in the US system. It is an incredibly significant moment in the cryptocurrency industry—it is certainly one of the clearest displays of political support for the technology underlying the digital asset industry in recent years. It is a momentous day with potentially profound implications—it could serve to galvanize centralized exchanges in their practices, prompt a further relaxation in relations with the industry, and prompt renewed institutional interest in the asset class in aggregate. Clearly, in terms of its implications for the US, it is an economic positive in a significant way—it is a positive in terms of cryptocurrency industry sentiment compared to the overly chilly relations with seemingly every other administration in US history.

Kansas City Manufacturing Beats Expectations, Hints at Output-Led Momentum

The October 2025 Kansas City Fed Manufacturing Index also strengthened to +6, beating market forecasts of +2 as well as last month’s reading of +4. Behind the positive trend is the significant boost in industrial activities in the Tenth Federal Reserve District, which covers major manufacturing areas in eight states. Both production and shipments drove the jump in the headline series, rising to +15, its strongest level since April 2022. However, with new orders standing at +1, it is clear that the progress in these activities reflects a shift from optimism to action.

However, it is also pertinent to note that the jobs element declined from +7 to +1, thereby indicating that even though there is a positive gauge in terms of manufacturing output, it is not matched by an equivalent trend in terms of employment requirements. In other words, even if the trend in labor decouples from that in terms of manufacturing output, new opportunities in automation could offset labor costs, thereby making it an attractive proposition for businesses in such a scenario where clients could continue to face persisting challenges in terms of making informed hiring choices in view of rising labor costs in the vicinity of the last six months. Additionally, the level of optimism in terms of businesses improved to +14 in the six-month outlook.

Given these findings, it has been found that the company, Emerson Electric Co. (EMR), is undervalued. As a front-runner in industrial automation, process control solutions, and intelligent manufacturing infrastructure, the company is poised to capitalize on higher factory volumes without incurring costs associated with labor-intensive expansions. The company’s diversified customer base in industries like energy, chemical, and discrete manufacturing makes it better aligned with regional production volumes. Analysts need to monitor the capital spending outlook for the mid-stream industry players, book order trends, and forward-looking indicators in the durable goods industry to gauge the sustainability of the industrial cycle recovery period. However, industrial automation stocks with leaner labor footprints continue to make a strong case for the bulls with ongoing success in these areas.

Existing Home Sales Recover With Mortgage Rates, Real Estate Market Stabilizes Below Peak

Existing home sales in September improved by 1.5% on a monthly basis to a SAAR of 4.06 million units, pushing the trend in a positive direction following last month’s decline in sales. The improvement is in line with forecasts, indicating that buyers have started reacting to the slight decrease in mortgage interest rates, which dropped below 6.5% in recent weeks. Despite the improvement, it is apparent that sales levels continue to fall short of the peak levels experienced during the pandemic period, surpassing 6 million units.

The median sales price showed a 2.1% increase from last year to $415,200, indicating that the problem of unaffordability continues to persist. Also, the number of housing units on the market is unchanged at 4.6 months’ supply, continuing to ensure that the market trend remains favorable for sellers. Although unaffordability remains a problem, the unavailability of new homes in the market, together with an unwillingness on the part of existing homeowners to sell in a higher interest rate environment, is also sustaining prices at high levels.

Given these circumstances, it would seem that Lennar Corp (LEN) is undervalued. As one of the top builders in the country with favorable balance sheet flexibility, Lennar is well-poised to exploit the scarcity in existing homes and the trend towards new supply construction. Additionally, its ability to pass costs on could serve it well in terms of adapting to rising input costs challenges. Analysts would need to monitor weekly mortgage app %, builder survey indexes, and core CPI shelter indexes for leading indicators on the implications on housing-related equities and resultant inflation trends.

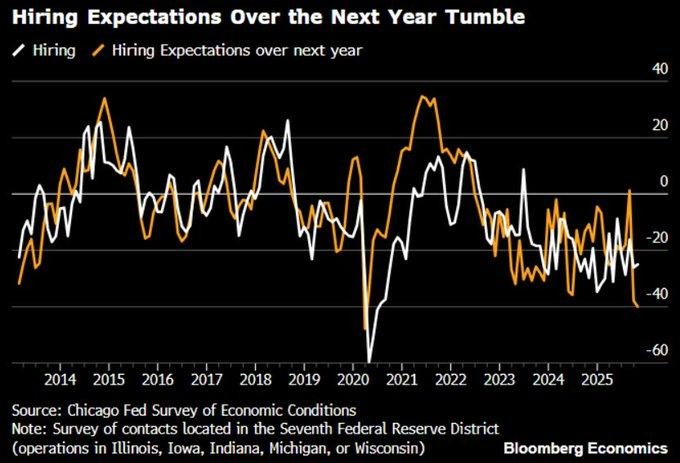

Midwest Hiring Outlook Shows 5-Year-Low Despite Overall Activity Bounce-Back

Labor hiring prospects in the Seventh Federal Reserve District dropped considerably in October, with the Survey of Economic Conditions from the Chicago Fed indicating a sharp fall to -40, indicating a level last seen during the 2020 low. The significant drop in labor market sentiment is quite ironic, considering that the overall activity index rose from -14 to +15 during the same period. There is an apparent critical juncture in the survey where businesses show improvement in activities but remain increasingly more pessimistic over labor hiring, perhaps due to enhanced labor productivity or caution in light of broader macroeconomic uncertainties.

The softer labor market prospect could represent a disinflationary influence, especially in core sectors where wages have been more sticky. As employment prospects continue to fall back, it is likely to mitigate labor costs’ upward pressure; hence, it could present an impression that the Federal Reserve doesn’t need to maintain a tight monetary policy stance. However, the stagflationary risk could arise if labor weakness is concurrently matched with ongoing supply-side-driven pricing tensions in areas such as the energy/housing indexes. At least for now, it appears there is a complex slowdown rather than a system-wide problem, but the marked deterioration in labor outlooks is something that deserves special attention.

In light of the factors mentioned, ADP (Automatic Data Processing, Inc.) is seen to be undervalued in the market today. As a company that is engaged in providing payroll services and workforce analytics, it remains resilient in terms of counter-cyclical labor management during times when hiring in the industry is slowing down. As more businesses opt for automation technology instead of hiring more employees in their HR departments, ADP’s subscription-based service is more defensive in nature for its shareholders.

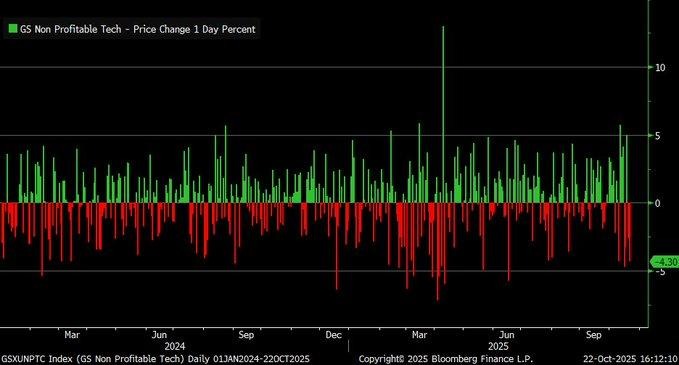

Non-Profitable Tech Basket Slumps 4.3% in a Day; Vulnerability in Sector Stirs Macro Worries

The GS Non-Profitable Tech Index, a proxy for high-growth, young technology companies in the US, dropped 4.3% on October 22, highlighting the subgroup’s sensitivity to changing macro trends. Despite the sharp decline, however, the index is up 8% for the month thus far, indicating the market’s conflicting forces between its belief in innovation for the long-term versus its concerns regarding valuations in the short-term, influenced by external factors such as high interest rates, trade tensions, and capital expenses in the artificial intelligence chain.

History shows that the risk profile for the group is high in a structural manner. The group’s stocks have performed 28 percentage points behind the S&P 500 from 2015 to 2020, highlighting their lagging nature during the time of tighter financial conditions. The recent fall in technology indexes with respect to tariffs and fiscal sensitivities in the area of artificial intelligence-related capital expenses has further pushed such speculative stocks, which rely more on their potential cash flows in the coming periods.

In light of these factors, it appears that Palo Alto Networks (PANW) is currently undervalued. Given its position within the industry in terms of being a leading company with its steady revenues, improving free cash flow generation, and its exposure to critical businesses for enterprises, Palo Alto is relatively defensive in the complex associated with technology in general. As it is neither part of the un-profitable group nor the fixed-target indexes, it remains an optimal hedge in terms of innovation-focused indexes in volatile cycles associated with capital rotations in high technology areas in general.

Mortgage Applications Fall for Fourth Week Despite Lower Rates, Signaling Cautious Buyer Sentiment

Mortgage applications in the US declined by 0.3% in the week ended October 17, registering the fourth successive fall in applications, according to MBA statistics. Despite the average 30-year fixed rate mortgage rate dipping to 6.37%, its lowest levels in over a year, the Mortgage Market Index continues its downtrend in terms of applications for the fourth successive week. Red flags continue to appear in the purchase category, with applications dipping to their lowest level since July, indicating that would-be purchasers continue to hold back in anticipation of further cuts in interest rates.

Though refinance volume surged 20% from last week, indicating some self-driven activities in the interest-rate sensitive housing market, core housing purchase demand is hampered by concerns over affordability. Factors such as home price escalation, scarcity, and persisting wage trends continue to discourage transaction volumes, especially for first-time buyers. The trend is seen in a bifurcated housing market, where refinance volume captures technical rate trends, while purchase volume is subject to more structural pressures, thus contributing little to near-term GDP even with easing financial conditions.

In these circumstances, it would appear that Zillow Group Inc. (ZG) is trading at a bargain valuation. As an integrated housing dataset and transaction platform company, it means that Zillow is well-poised to derive long-term leverage from a normalized housing cycle with durability from its rental marketplace exposure. Analysts need to watch for housing market metrics on a weekly basis, incentives offered by builders, as well as communication from the Fed on rate path.

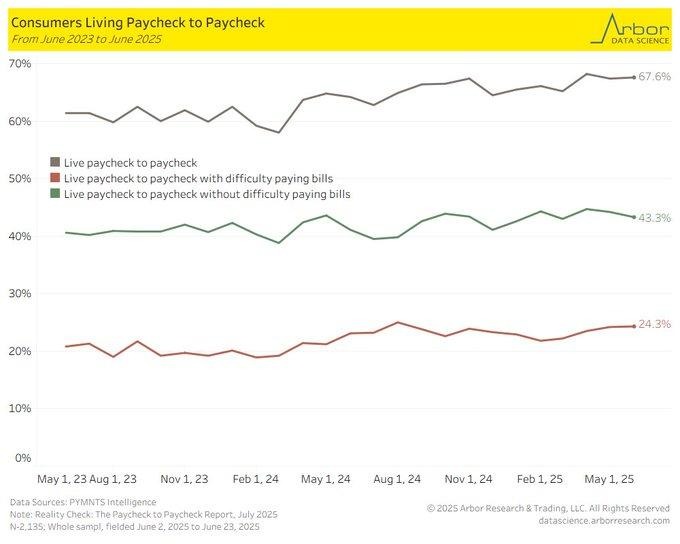

Two-Thirds of Americans Continue Living Paycheck to Paycheck Amidst Rising Housing Expenses

As of June 2025, 67.6% of U.S. consumers reported living paycheck-to-paycheck, according to PYMNTS Intelligence, marking only a slight improvement from May’s 68.4% high. While the marginal dip suggests some stabilization, the broader picture remains concerning: over two years of readings above 60% underscores persistent household vulnerability despite a cooling inflation backdrop and incremental wage gains. Nearly one in four respondents (24.3%) indicated they could not fully cover their bills, highlighting the inadequacy of nominal income growth relative to structural expenses like housing, healthcare, and debt servicing. Notably, even among higher-income cohorts, the data show elevated financial strain, challenging assumptions that earnings alone shield against liquidity stress.

Homeownership has emerged as a central pressure point. A growing segment—14% of owners or over 24 million individuals—attribute their budget fragility to home purchases, with rising monthly mortgage costs from adjustable-rate resets significantly tightening disposable income. This has led 42% of impacted households to reduce nonessential spending or increase reliance on credit, pushing up revolving balances and utilization rates across retail lending channels. The trend is particularly pronounced among younger households, many of whom entered the housing market during the rate-driven demand surge of 2021–2022 and now face unaffordable monthly outlays in a higher-for-longer rate regime. These dynamics risk dampening discretionary consumption through year-end and may pressure retail earnings in Q4 and Q1 2026.

In this kind of consumer environment, Synchrony Financial (SYF), in my view, is looking undervalued. By specializing in private-label and promotional lending, the company is well- suited to meet the growing need for credit, with its diversified retail businesses cushioned from industry-related fluctuations in performance. As a company with its core businesses in the area of credit cards and installment loans, Synchrony Financial is well-poised to capitalize on rising levels of revolving activity, but industry analysts would do well to pay strict attention to net charge-off ratios, loss provisioning in their portfolios, and the specific buckets for delinquencies within each tier of their lending portfolios.

Upcoming Economic Events

GBP Retail Sales, Eurozone & UK Flash PMIs, U.S. Flash PMIs, and CPI Readings

Global markets face a critical period ahead with a series of tight-packed pieces of macroeconomic information potentially reshaping entire sets of market views on growth, inflation, and policies alike. Given that key pieces of information are approaching on the UK, Eurozone, and US fronts, market positioning is set to ride the fence between economic durability and resultant fatigue from policies, with improvement/degradation in market sentiment principally dependent on these pieces of information versus market expectations. Below is what we watch at Zaye Capital Markets, alongside resultant market action.

GBP Retail Sales m/m – All That’s Required for a Resilient UK?

Retail sales would serve as an early indicator for the level of spending power in UK households with core inflation down but interest rates high.

- Should it test the consensus positively, it would imply that consumers have coped well with the prevailing Macro challenges, triggering an upbeat market in the pound, higher yields on short-term Gilts, and rising shares in the retail space. At the same time, it might cause the BoE to maintain high interest rates for an extended period, which could hamper economic growth in the medium-term.

- Weaker-than-expected print would confirm the slowdown in consumption, supporting the dovish trend in interest rate views, likely pressuring Sterling in the process. Expect areas to outperform in staples and defensives, with rising interest in BoE guidance on easing in early 2026.

Flash PMIs – Eurozone, UK, France, Germany: Growth or Stagnation?

The PMIs for Flash Manufacturing and Services in the Eurozone will give the first glimpse into regional economic activity in real time.

- Should these prints come in upbeat, more so in Germany and France, it could boost the value of the EUR and the GBP, dispel concerns over a possible recession, and trigger investment into cyclicals such as industrial goods, autos, and financials. If these industries show collective improvement in manufacturing and the services sectors, it could cause markets to reprice perceptions over the dovish policies adopted by the ECB and the BoE.

- However, Below-forecast data would only accentuate concerns that high interest rates and weak external demand remain major drags on European growth. This would trigger a bond rotation, a weakening euro, and subsequent underperformance in exporters and sensitive-rate industries. Do watch for the contradiction between services (which remain strong), on one hand, and manufacturing (which is weakening), on the other – a trend likely to increase policy disparities in early 2026.

U.S. Flash Manufacturing & Services PMIs – A Snapshot of Momentum

The US flash PMIs are highly informative in determining if the true economy is able to sustain momentum in the face of tight financial conditions.

- The positive surprise, especially in the service-related activities, would confirm that the economy is doing well even with the tight monetary policies adopted by the Federal Reserve. The implications would likely include an increase in Treasury yields, an increase in the value of the US dollar, and would also cause long-term equities to struggle.

- By contrast, softer-than-expected prints would imply that tighter policies are starting to dawn on the economy, leading to a bullish bond rally, a technology-driven stock market bounce, and rising prospects for a rate cut cycle in mid-2026. See if there is any decoupling in the sectors, with weak manufacturing and a dip in services casting a negative light on Q4 GDP figures.

U.S. CPI m/m, Core CPI m/m, CPI y/y – The Fed’s Inflation Pulse

These are the marquee data points of the week.

- If headline or core CPI print above forecast, it may prompt an aggressive hawkish repricing across rates markets. Expect 10Y yields to climb, USD strength, and pressure on tech and consumer discretionary names. Markets would likely push out rate cut bets and reintroduce chatter of potential re-tightening if services inflation proves sticky.

- A weaker-than-expected CPI, especially in core services ex-shelter, would be interpreted as validation that disinflation is regaining traction. That could trigger a broad-based equity rally, bull steepening in the yield curve, and softness in the dollar. Real yields would ease, benefiting gold, high-growth equities, and EM assets. Shelter and medical care inflation components will be particularly important as Fed officials weigh risks of over-tightening against lagged policy effects.

The coming week is likely to be critical in determining the tone for year-end positioning strategies as well as 2026 forecasts. Asset allocators need to brace for high levels of volatility in the following areas: forex majors (GBP/USD, EUR/USD), global rates, and value versus growth factor spreads. In the event that surprises come in on the positive side, a rotation from defensive to cyclical stocks, short-duration credits, and a more hawkish pricing for the major Developed Markets’ central banks is anticipated.

Stock Market Performance

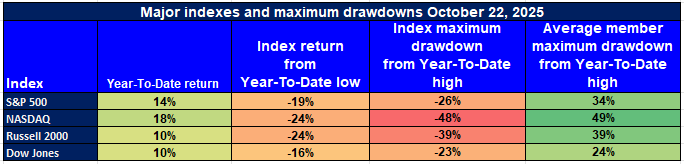

Indexes Rebound Sharply Since April, But Member-Level Pain Persists

The US indexes have made significant rallies since the market trough on April 8, 2025. But aside from the double-digit increases in the indexes, it is apparent that the average member draw-downs paint a more vulnerable picture in reality even with the resilience in the indexes.

Here is our revised categorization for major indexes:

S&P 500: Headline Strength vs. Silent Strain

YTD: +14% | +34% from April low | – 19% from YTD high | Avg. member: – 26%

The S&P 500 is up a strong 14% so far this year, with 34% from its April 8th closing low, but maximum draw-down levels at 19% from its year-td high levels and average portfolio member levels at 26% show strain nonetheless. There has also been little follow-through in breadth improvement.

NASDAQ: Big Gains, Deeper Cracks Beneath the Surface

YTD: +18% | +49% off April low | -24% from YTD high | Avg. member: -48%

The NASDAQ continues to lead in terms of performance, with the index gaining 18% so far in the year and closing in on 50% from its trough in April. Still, it is apparent that the technology-dominated index is vulnerable in terms of its structure, with an average member down 48% from its peak.

Russell 2000: Small-Caps Have Difficulty Maintaining Pace

YTD: +10% | +39% from April low | -24% from YTD high | Avg. member: -39%

The Russell 2000 is up 10% yr-to-date and 39% from April lows, yet small caps’ resilience remains uncertain. The 24% pull-back from 2025 highs coupled with a deep average portfolio company loss of 39% is indicative of selling in illiquid, interest-rate sensitive names, which is a function of overall caution on weaker balance sheets.

Dow Jones: Relative Stability, But Uneven Internals

YTD: +10% | +24% from April low | – 16% from YTD high | Avg. member: – 23% The defensive nature of the Dow has offered somewhat decent protection with its 10% return so far in the year and 24% gain from the April troughs. However, the fairly weak 16% index MG is somewhat contradicted by its average member MG of –23%.

At Zaye Capital Markets, we would also like to highlight the importance of risk-adjusted selectivity on a global basis. While the indexes have been strong, the level of underlying volatility is high. We would also like to highlight the need for quality names with strong earnings and strong cash flow, with a defensive industry footprint.

Earnings

Earnings Recap — October 23, 2025

- T-Mobile US, Inc.

T-Mobile delivered adjusted EPS of $2.41, slightly above the $2.40 consensus, with revenue rising 4% to approximately $21.95 billion. The company added over one million postpaid phone subscribers and 506,000 high-speed wireless broadband subscribers, demonstrating continued strength in its connectivity strategy. Importantly, T-Mobile raised its full-year guidance, signaling operational confidence. Investors should focus on subscriber momentum, broadband scale, margin impacts from 5G investments, and any updated commentary on competitive pricing strategies.

- Blackstone Inc.

Blackstone reported a 48% year-over-year increase in distributable earnings, reaching $1.52 per share, exceeding estimates of $1.23. The firm’s assets under management climbed to a record $1.24 trillion, driven by strong private-equity and credit performance. Key investor considerations include the pace of fund-raising, deployment capacity, resilience of credit strategies amid macro stress, and management’s commentary on asset valuations in a shifting rate environment.

- Intel Corporation

Intel posted an upside surprise with revenue of approximately $13.7 billion, up 3% from the prior year, and adjusted EPS of $0.23 versus a consensus of just $0.01. The return to profitability was driven by gross margin recovery to ~38%, compared to 15% a year ago. Strategic focus remains on AI compute opportunities, foundry execution, and further margin expansion. However, risks persist in scaling manufacturing and defending share in competitive segments.

- Honeywell International Inc.

Honeywell exceeded expectations with Q3 sales of $10.4 billion, up 7%, and adjusted EPS of $2.82, beating the $2.57 consensus. The company raised full-year EPS guidance to a range of $10.60–$10.70. Aerospace demand was a bright spot with 15% growth and a 22% jump in orders, reinforcing backlog strength. Key risks include execution around the upcoming Solstice spin-off and the trajectory of industrial automation demand.

- Union Pacific Corporation

Union Pacific reported adjusted EPS of $3.08, ahead of the $2.99 consensus, with revenue at approximately $6.24 billion. Bulk segment performance stood out, with 7% growth in coal and food grain transportation. Investors will be closely watching integration risks tied to the pending merger and any cost escalations, particularly given $41 million in merger-related charges this quarter. Commentary on intermodal competition and labor dynamics will also be key moving forward.

Earnings Preview — October 24, 2025

- The Procter & Gamble Company (PG)

Procter & Gamble is expected to report Q1 FY2026 results before the market opens. Investor focus should be on organic sales growth trends, gross margin dynamics amid raw material and transportation cost pressures, and the company’s ability to pass through pricing across its brand portfolio. Additionally, signals on inventory normalization and regional performance—particularly North America and emerging markets—will be critical in gauging full-year momentum.

- HCA Healthcare, Inc.

HCA Healthcare is set to report Q3 earnings, with Street estimates pointing to $5.72 EPS and $18.57 billion in revenue. The market will focus on trends in same-facility admissions, shifts in procedural mix, and wage-related cost pressures. Attention will also be on payer reimbursement trends and capacity constraints across the system. Regulatory updates and forward-looking guidance on operating leverage will guide healthcare positioning post-report.

- General Dynamics Corporation

General Dynamics is due to post Q3 results ahead of today’s open. The defense contractor will be evaluated based on its aerospace performance, backlog momentum across military programs, and cash flow generation. Export exposure, geopolitical developments, and defense budget commentary could influence sentiment, particularly as investors assess contract pipelines and supply chain resilience.

- Illinois Tool Works Inc.

Illinois Tool Works is also expected to report today. Key metrics will include demand trends in industrial capital equipment, geographic exposure between developed and emerging markets, and the balance between consumables and high-ticket equipment sales. Margin resilience under cost pressure and outlook revisions—if any—will be closely watched by institutional investors looking for clarity on the pace of industrial reacceleration.

Stock Market Overview – Friday, 24 Oct 2025

The US market started the day on a sour note, due to overstretched valuations, dominance by a select set of stocks, as well as rigid macro concerns. The dominance of the so-called “Magnificent Seven,” mega-cap tech names in the US market, continues to be an area of concern for us at Zaye Capital Markets. We continue to watch with caution before joining the bandwagon on a rallies thesis.

Stock Prices

Economic Factors and Geopolitics

The market sentiment is also driven by rising 10-year Treasury yields, in addition to concerns over inflation, leading to a re-valuation in terms of re-calculating discount rates in respect to estimates for the coming years. At the same time, market participants remain affected by implications from further escalation in trade tensions between the US and China, in respect to the latest escalation with regard to their rare earth exports. At the micro level, guidance on margins and capital expenditures remains increasingly less so from a catalyst perspective.

Latest Stock News

- $GOOGL has entered its first U.S. contract for carbon-capture natural gas to fuel its data centers in the Midwest, supporting its ambitions for 24/7 clean energy coverage in the face of rapidly growing AI-related workload volumes. That’s a profound acknowledgment that the existing grid is unscaleable for near-term volumes.

- At the same time, $GOOGL has secured a multi-billion-dollar commitment with Anthropic, launching the biggest ever increase in Tensor Processing Units (TPU). The $7 billion run rate is aligned with Google Cloud, supplemented with a gigawatt boost in compute power by 2026, making TPUs the profit center for its AI services segment.

- $NVDA is using real-world data from $UBER to train its more advanced Cosmos autonomy models. Having $UBER’s real-world data helps $NVDA’s models greatly in situations where traditional autonomy has failed – complex environments. Nvidia is positioning itself for success in commercial fleet autonomy solutions.

Meanwhile, the U.S. Commerce Department has stated that it is not in talks with companies such as $IONQ, $RGTI, $QBTS, or $QUBT at the moment, indicating a halt in immediate collaborations between the public and private entities on quantum computing initiatives.

The Magnificent Seven and the S&P 500

“Magnificent Seven,” which comprises Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla, is facing renewed pressure in the ongoing week, which is an effect of margins, growth, and re-rating concerns on these stocks. As these stocks drive the S&P 500 heavily, their weakness is leading to an overall stagnation in the market. Until these stocks stabilize, the market is likely to face an upward constraint in November.

Major Index Performance on Friday, 24 October 2025

- Nasdaq Composite: Trading at ~22,942 (up ~0.9%)

- S&P 500: Trading at ~6,738 (up ~0.6%)

- Dow Jones Industrial Average: Trading at ~46,735 (up ~0.3%)

- Russell 2000: Trading at ~2,481 (up ~1.2%)

At Zaye Capital Markets, we remain of the view that it is a “selective risk-on” environment at present. With mega-cap technology stocks weak, speculative stocks struggling, and interest rate sensitivity high, we continue to emphasize “free cash flow stalwarts,” pricing power leaders, and industry-driven stocks. We think more general participant engagement and recognition that the rally is sustainable only gets confirmed with improved breadth and reduced interest rate risks.

Gold Price

As of last Friday, 24 October 2025, the existing market prices for gold remain at US$ 4,140 for an ounce, temporarily retreating from its recent record-breaking levels that breached US$ 4,300, although well within key support levels. The temporary retreat is a readjustment in interest rate forecasts in light of today’s big-awaited macroeconomic reports, although the overall environment is generally friendly to gold futures. Some recent geopolitics on the back of a series of market-moving statements from Donald Trump are embedding layers of global risk premiums into markets. His subsequent reiteration on new taxes for China on November 1, views on Venezuelan connections with narcotics traffickers, threatening military action, and strong-worded warnings on Russia, Ukraine, and the flow of fentanyl into communities also combine in making the geopolitics rather volatile. At the same time, his meeting with Chinese President Xi and his Japanese counterpart, the new Japanese Prime Minster, is also on his agenda, making US foreign policies rather complex today.

Conversely, the next series of economic numbers, including UK retail sales, Eurozone manufacturing/services PMIs, and more broadly US CPI and flash PMIs, could also be pivotal in guiding the immediate gold price action pattern. As long as these numbers show upbeat surprises within either the inflation front or on the economic front, bond yields could edge higher, with the potential strengthening of the dollar likely to exert pressuring on gold prices. Conversely, any semblances of weakness within either the CPI numbers or economic indicators would reignite views for dovish policies, leading to renewed portfolio shifts to gold on its stagflation hedge benefits. Monday’s economic fundamentals were already set on a risk-off tone, with weakening labor market statistics coupled with weakening statistics within the overall consumer statistics leading to reduced equities with increased bond flows. All these statistics reemphasize the notion that the trend in subsequent levels of monetary increases is nearing its peak, making gold’s hedge role ideal in the trend. At Zaye Capital Markets, we perceive that the existing environment is ###At an Environmental Wherein Gold’s Support Trends Are Always Firm in Nature Despite Potentially Consolidating in the Short-Term.

Oil Prices

At present, as of Friday, 24 October 2025, the price for West Texas Intermediate (WTI) is US$61.61, with Brent settled at US$65.56. Both sets of prices have strengthened in recent days due to new rounds of renewed geopolitics and associated sanctions issued against Russia’s greatest exporters of petroleum products. As such, a risk premium has emerged in markets that initially were undermined by projections from the IEA on recent concerns over a global supply glut. According to Bloomberg’s Energy news aggregates, with further collaboration from Zero Hedge, it appears that the market is presently operating with two contrasting scenarios simultaneously: namely, supply scarcity driven by geopolitics, and dampening due to uncertain demand scenarios associated with mixed readings on global growth. Excess global supplies in Q1 2026 appear evidenced from reports coming from the IEA in the event that 2026’s weak demand accelerates, coinciding with no visible OPEC-indicator for any supplementary cuts following the recent 5.6% jump in WTI prices over the last month. The present market’s immediate level of sensitivity to today’s forthcoming economic readings – more specifically for US CPI and PMI – is critical in terms of ongoing petroleum futures pricing dynamics. Layered atop these dynamics are a series of sharply worded comments from Donald Trump that are directly influencing energy markets. His pledge to activate tariffs on China from 1 November, threats toward Venezuela over alleged drug-related activities, and mentions of military activity and sanctions reinforce fears of supply chain instability and geopolitical energy disruption. Trump’s remarks on China-Venezuela ties, fentanyl routes, and land action in Venezuela—all within the past 24 hours—have raised the perceived probability of U.S. interference in major oil-producing regions, which traders are increasingly pricing in as a geopolitical premium. Meanwhile, yesterday’s softer-than-expected labor and housing data added a note of caution, dampening growth sentiment and complicating the outlook for oil demand in the near term. At Zaye Capital Markets, we believe oil is navigating a volatile macro-geopolitical intersection: while short-term price gains are supported by rising tensions and sanctioned supply losses, sustainability will depend on how today’s economic data shapes the narrative around global consumption, Fed policy path, and overall energy demand resilience.

Bitcoin Price

As of Friday, 24 October 2025, Bitcoin is trading around US$109,000, recovering modestly from the week’s earlier lows near $108,000 and reclaiming ground following seven consecutive days of broader crypto market declines. While BTC briefly surged past $110,000 on short-covering and speculative bounce activity, structural pressures remain evident. The most notable driver of volatility this week has been the US$1.23 billion in aggregate outflows from spot Bitcoin ETFs over a five-day span, with daily outflows still exceeding US$100 million. These discharges have fueled concerns about waning institutional conviction and price fragility, especially as macro headwinds like a stronger dollar, elevated yields, and recessionary fear persist. Despite this, crypto-native data shows continued accumulation by long-term holders and strategic buyers, particularly as the pace of crypto ETP/ETF launches accelerates in global markets including the UK, Europe, and Asia. M&A activity within the space has also picked up, suggesting larger players are positioning for long-term infrastructure dominance amid short-term market chop. Analysts broadly agree that ETF flows and derivatives open interest will remain key volatility drivers heading into November. Overlaying this is a wave of politically charged developments that are influencing crypto sentiment at both retail and institutional levels. Donald Trump’s presidential pardon of Binance founder CZ (Changpeng Zhao)—framed as a rebuke of overreach by the previous administration—has been interpreted as a major moment of political support for the crypto industry. The move could create breathing room for centralized exchanges and signal a more accommodative stance toward digital asset infrastructure. However, this tailwind is complicated by Trump’s other remarks: threats of renewed tariffs on China beginning Nov. 1, growing military posturing toward Venezuela, and criticism of international trade dynamics have elevated geopolitical tension and contributed to broader risk-off flows. These remarks weigh on speculative appetite in crypto markets, as investors weigh the potential for macro instability and policy unpredictability. Yesterday’s weaker-than-expected U.S. data—particularly in labor and housing—further softened risk sentiment, pressuring BTC early before a modest bounce. As today’s U.S. CPI and flash PMI prints loom large, any inflation upside surprise could suppress crypto appetite via rising yields and a stronger dollar. Conversely, softer prints may breathe new life into the digital gold thesis and position Bitcoin for a break back above $110K, especially if ETF flows begin to stabilize.

Eth Prices

As of Friday, 24 October 2025, Ethereum (ETH) is trading in the range of US$3,820 – US$3,900, sustaining its ground following testing levels earlier in the week. Following this level is a period during which there has been mixed market sentiment, influenced by a strong discrepancy between institutional ETFs’ outflow and whale wallets’ activities. Specifically, on October 20, there were net outflows for ETH spot ETFs amounting to US$145.7 million, which is the third consecutive day with net outflows, sending a warning signal to today’s traders. Generally, the cryptocurrency market’s ETF is struggling to continue with its inflow following tighter global liquidity levels and risk-off sentiment in the asset class. Additionally, the derivatives’ open interest level for ETH is down somewhat, with a possible pause in placing leveraged bets, which is likely to dampen market volatility in the coming days.

In contrast to the Institutional Investor trend, Whales have been secretly hoarding Ethereum on a massive scale. During the last five trading days, Large Wallets netted over 200,000ETH, thereby registering their combined Whaly wallets over 22.31 million ETH, according to leading on-chain analytics sources. The trend deftly registering Outflow- cum- Inflow in Exchanges is indicative of long-term commitment to possibly awaiting better network activity, L2 facilitation benefits, or a DeFi-NFT ecosystem rebound. There is an obvious strategy mismatch between the Institutional Investor sellings in ETFs versus Whale Buying in the ETH markets, thereby presenting the following tactical dilemma within the ETH Markets: in the likely event of an Institutional Investor sentiment shift with reduced Inflation Metrics or improved Macro Liquidity Conditions, the existing Whale Buying trend might serve as the seedbed for an upward pivot back into the US$4,400-US$4,500 range in the near term. Conversely, in the event of continuing Institutional Investor sellings with worsened Macro Trends, the next downtrend in the ETH futures contracts could potentially target US$3,500 levels, provided Bitcoin Dominance strengthens, subject to an increase in Crypto-asset Volatility in coming trading cycles at global Exchanges. At Zaye Capital Markets, we would advise continuing to remain positive on the Mid-term to Long-term positioning within the Ethereum Marketspaces.