U.S. and European stock futures are modestly lower to little changed in early trade, with market players in nervous anticipation of a wave of first-quarter reports from among the big U.S. banks, along with new inflation data. So far in early trade, Dow Jones futures have lost 30 points (-0.07%), while S&P 500 and Nasdaq 100 futures have declined around 0.1% each. In Europe, Euro Stoxx 50 and DAX futures are also broadly flat, in a similarly nervous overall tone on either side of the Atlantic. Markets seem to be taking a breATHER after Monday’s easy gains, as they digest renewed tariff threats from U.S. President Trump and watch for signals from today’s reading of CPI data and first-quarter reports releases.

This flat futures reaction comes after Trump threatened to impose a 30% tariff on Mexican and EU imports from Aug 1, a move that took world trade expectations by surprise. Investors recalibrate their perception of how tariffs would hurt profit margins as much as push up levels of prices, especially for trade-exposed areas of consumer and industrials. EU investors are also wary of themselves being retaliated against, with corporate leaders anticipating yet another spell of supply chain disruption as the continent is only just recovering from slowdowns in demand. Threats of retaliatory tit-for-tat trade measures cool optimism otherwise underpinned by strong macro fundamentals.

US attention is centered on proxy near-term Q2 bank revenues of financial giants JPMorgan, Wells Fargo, and Citigroup. In spite of bank margins being tightened further because of restricted credit as well as fluidizing rate outlooks, mixed earnings hopes await. However, there is ever-hope because there is speculation of good trading revenues as well as good consumer bank trends. This twinning of rising inflation optimism as well as hopefully upbeat earnings outlooks is maintaining futures flatish—but subject to bearish shocks.

For European markets, outside threats of tariff pressure aren’t only stemming defensive sentiment, but internal economic weakness is as well. Disappointing industrial soft output, weak retail sales, and energy supply risk are again in focus. Geopolitical risk convergence with Trump-led trade nervousness and uncertainty in this day’s inflation print is generating a nervous but paying-close-attention world futures market climate. Traders simply at the same time happen to be in defensive modes right now as they await further sign of whether this earnings season and this set of inflation reports have enough cred in sustaining market rallies seen in the past.

Major Index Performance as of Jul 15, 2025

- S&P 500: At 5,874.13, down 0.4% during the day

- Nasdaq Composite: At 13,725.42, down 0.6%

- Dow Jones Industrial Average: Near 38,520.75, down 0.2%

- Russell 2000: At 2,087.34, down 0.5%

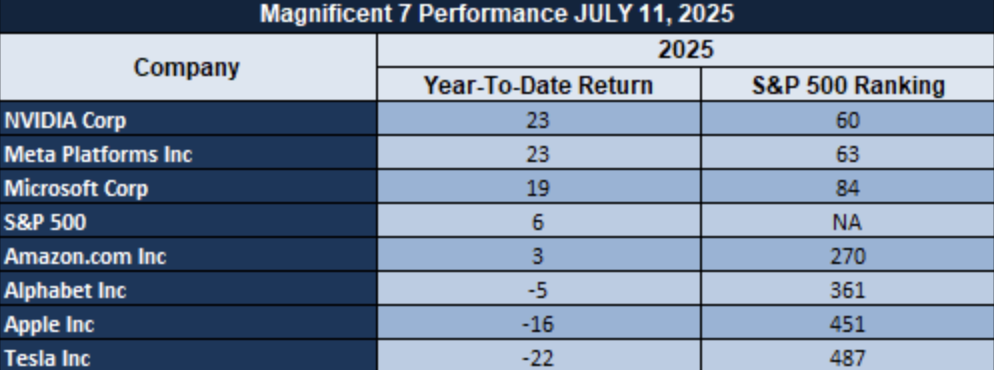

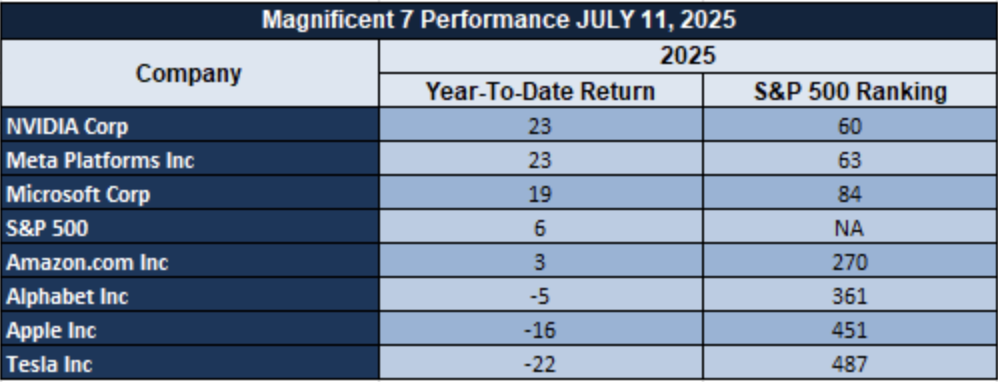

The Magnificent Seven and the S&P 500

The S&P 500 is faltering as key members of the “Magnificent Seven” struggle with profit-taking and policy risk. Both Tesla and Nvidia lagged, with Tesla bogged down by the weight of regulator uncertainty along with difficulties with pullbacks after staggering year-to-date gains for Nvidia. Both Apple and Amazon continued to lag with consumer-based indicators weakening, while Microsoft and Alphabet have remained in relatively solid ground. Concentration risk in these mega-cap stocks is in increasing focus, acting as fuel for thinner market breadth as well as defensive rotation.

Drivers Behind the Markets Transformation

With international markets entering on wobbly legs, investors are responding to a new set of events shaping U.S. and European sentiments. From geopolitics to market-transcending measures of inflation, these events are propelling risk appetite and sector rotations. Below are the three key market drivers today, as they relate to events of the previous 24 hours:

1. Trump’s Tariff Threats Fuel Trade Jitters

President Trump‘s threat to impose a 30% tariff on Mexican and European goods from and after August 1 has brought trade war nervousness back to world markets. His comments following Monday’s session have been at centre stage of multinational profit estimates, particularly in industrial, vehicle, and consumer companies. Retaliation plans have been reported as being under discussion among European leaders, with fear of an another 2018-2019 retaliatory cycle being at greater ease. Aggressive tone-plus commentary on “riling the market” as well as his criticisms of Fed Chairman Powell, is causing nervousness over independence of monetary policy and world trade diplomacy.

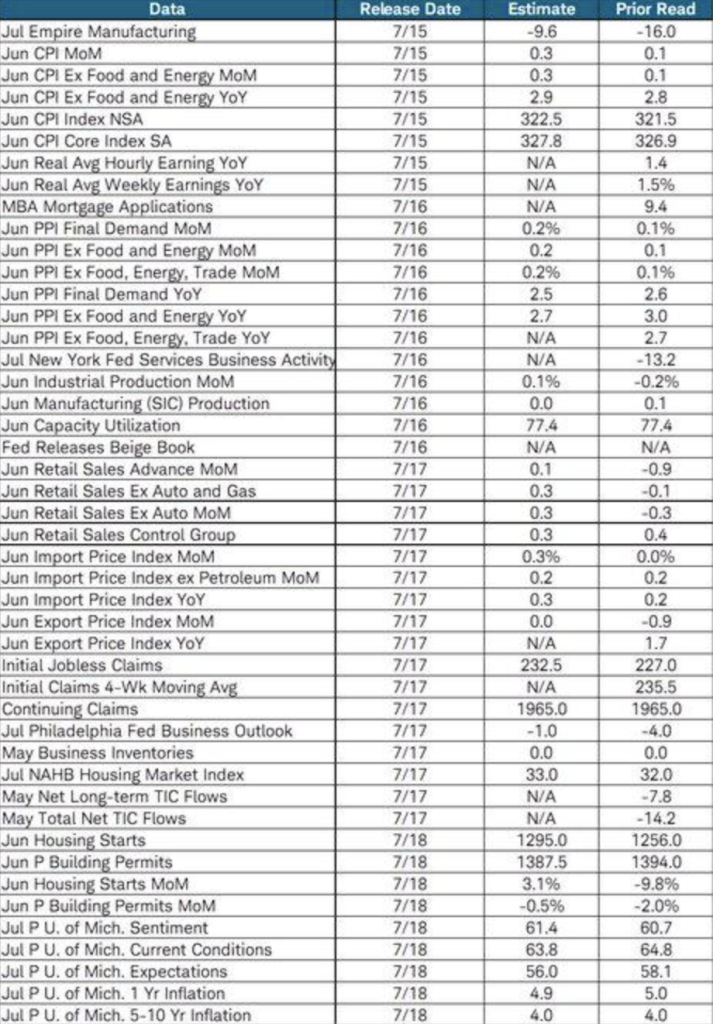

2. Waiting on Key U.S. Inflation Data

Markets are also firming in expectation of today’s inflation prints, including Core CPI m/m, CPI y/y, and CPI m/m. With persistence in yesterday’s economic data release in inflation, today’s prints feature prominently in rate expectations. A larger-than-anticipated print would force the Federal Reserve to extend its tight policy beyond markets had expected, in the wake of negative sentiment in stocks—indeed in growth stocks as well as tech stocks. A low number, on the other hand, can fuel expectations of soft landing and relief for rate sensitive assets.

3. Finance Industry’s Gains Cast a Shadow

Financials have remained in tight focus with today’s reports of JPMorgan, Wells Fargo, Citigroup, BlackRock, and BNY Mellon. With mixed messages elsewhere across the rest of the economy—i.e., improving credit card leverage and slowing loan growth—these reports will be watched tightly across credit quality, net interest income persistence, and trading revenue momentum. Because financials act as proxy indicators of the entirety of this earnings season, markets will be paying keen attention as to whether this latest bounce in equities is long-lasting or in need of reboot.

Digesting Economic Data

The TRUMP Tweets and Their Implications

At Zaye Capital Markets, we’re witnessing an unambiguous change in market sentiment in response to a range of comments from ex-US President Donald Trump—covering domestic economic policy through belligerent geopolitical posturing. His latest criticisms of US Fed Chair Jerome Powell, in support of would-be successor Kevin Hassett, has reinvigorated speculation around central bank independence as well as partisan control of direction of central bank policy. Markets already price potential less accommodative Fed leadership with Trump’s potential return to office, ideally in support of looser policy in response to cooling inflation. These hopes have already had effect on rate-sensitive products, with gold and Bitcoin recording small inflows as policy uncertainty hedge.

His own reported market impact—”I go on TV and rile the market”—isn’t exactly hot air. It is changing investor sentiment and volatility in asset classes. His daily trade commentary—such as favorable tariffs to allies and retaliatory tariffs against Russia unless there is a deal in 50 days—begins a new age of transactional diplomacy with the potential to disrupt global world supply chains. Such threats, in execution, would have a negative impact on industrial production as well as flows of raw materials, as well as inflate expectations of price increases in import-intensive companies. His trade commentary on Patriot deployment of batteries as well as military aid among others towards NATO signify a changing defence policy, likely boosting fiscal spend forecasts as well as defence industry valuations. On geopolitical front, there is unpredictable approach of Trump towards Vladimir Putin—addressing him as a “tough guy” but giving him space in order to facilitate talks— brings unpredictability in market impact of Ukraine-Russia tension. Some find it as diplomatic threats while others examine uncertainty of oil market uncertainty along with defence market repricing. His Russian interference in Ukraine’s grid sabotage adds further dread in susceptibility of eastern Europe’s energy market.

Furthermore, Trump’s emphasis on strategic sectors—the $70B AI & energy investiture with PLTR CEO in accompaniment—is reflective of a connected economic agenda with potential of speeding up sectors of artificial intelligence, defense, as well as alternative energy. Such sector emphasis can redirect capital flows into those companies regarded as sympathetic to policy goals of the Trump period. Generally, market impacts of such statements are not only defensive; they’re slowly rebalancing expectations on trade, inflation, tech, as well as monetary leadership into second half of 2025.

CPI Contradictions And Housing Weakness

Zaye Capital Markets is analyzing recent U.S. reports of inflation differences in recent 0.1% year-o-y decline in June CPI compared to overall trends of increasing inflation, in this instance UK’s 3.4% May increase. Single print is fueling concerns of data uncertainty, as it does in the wake of Bureau of Labor Statistics’ long-established tradition of averaging 0.3% revisions of CPI based on independent research. Uncertainty of ultimate measure of CPI either indicates one-off disinflation shock or lag in full data absorption, once again highlighting caution ahead of trading on initial estimates.

This is accompanied by overall weakness in key core macro indicators. Retail sales declined 0.9 as new housing starts declined to 126,280 units, posting a sustained downtrend. More significantly, building permits declined 5.2% year-on-year, backing pressure of residential investment policy tightness. These indicators support world downtrend reported among multilateral institutions, citing risk-off consumption patterns as well as poor private sector investmens. Inflation is sticky in certain markets, but structural cooling in housing reports subdued forward demand.

Of those in the spotlight, we think Lennar Corporation (LEN) is inexpensive, particularly as it continues to handle inventory carefully and focused on affordability in a soft housing market. Special attention is due next week’s mortgage apps and construction spending reports. These will provide good gauges of housing softness resilience as well as serve as an expectations reset in maintaining resilience in Q3 earnings.

Surging Retail Sentiment And Valuation Shifts

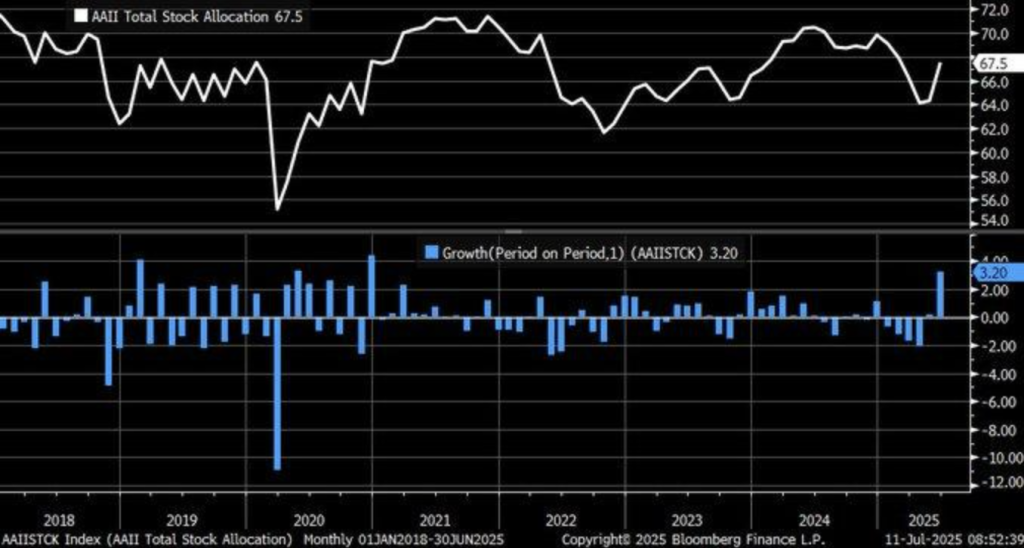

Zaye Capital Markets takes a look at the latest change of direction in sentiment in investors, a sudden 3.2% increase in privately owned investors’ equity allocation in June 2025, using long-term sentiment indicator data. It is the biggest monthly increase since with regards to December 2020 and can be seen as a behavioural correction towards risk-seeking. Bullishness in stocks is one of several pieces in a greater whole of stabilisation of the economy as a response towards a -0.3% decline in GDP in Q1 and is symptomatic of retail sentiment now changing as a response towards perceived market under-valuaiton.

Indeed, this earlier 3% market discount of the equity market vis-a-vis fair value—at May’s end—puts this retail rebalancing in perspective. Market participants seem to be rebalancing into stocks as volatility dips and macro indicators improve, testing in-vogue bearishness sentiment in Q2. We can’t help but wonder, though, that prior episodes of exuberant sentiment, especially those in long-run behavioural researches, have been subsequently followed in the near term with corrections as positioning gets ahead of fundamentals.

Here, Alphabet Inc. (GOOGL) looks to us as being undervalued. Though on the rise on sentiment, it is still below its intrinsic worth in comparison to sector comparables and enjoys greatly on upside potential in AI-revenues, and trends on ad spends. Technicians need to beware of retail inflow reports, valuation spreads against traditional norms, as well as upcoming changes in earnings. These will be key in deciding whether bullishness is founded on fundamentals or drawing a sentiment-driven retracement.

Housing Cools As Rates Bite Into Demand

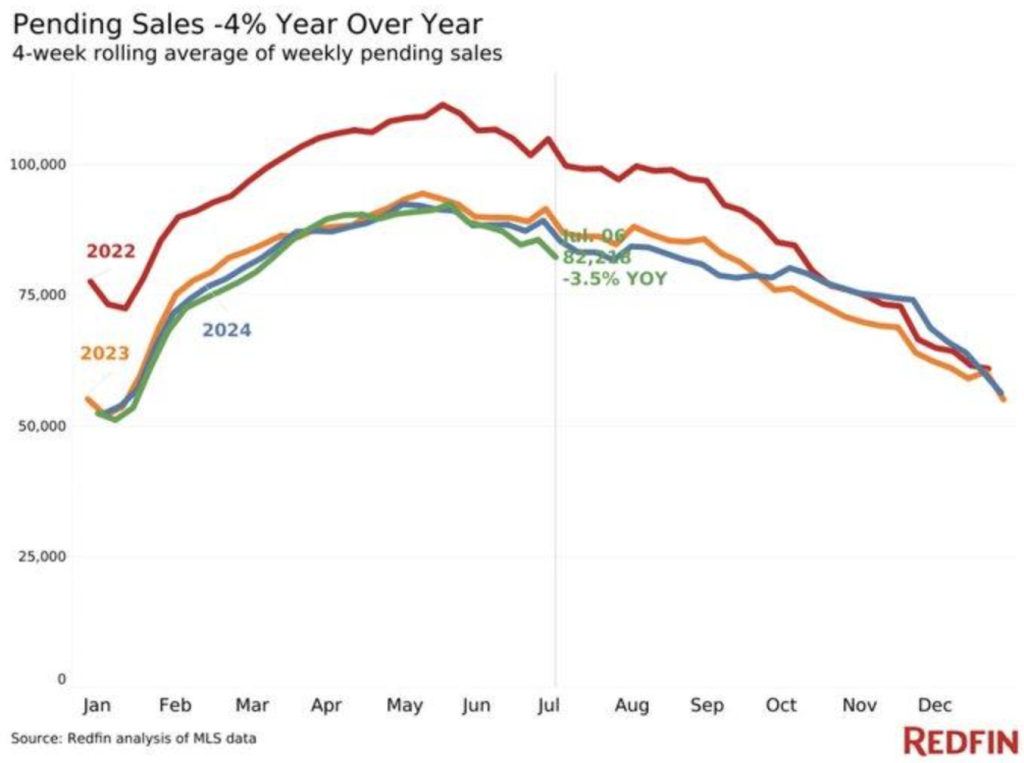

Here at Zaye Capital Markets, we take a second look at this latest 4% year-over-year drop inpending home purchases, reported in recently released housing market statistics. This greater fall—a greater one than in 2022–2024—a greater one with increasingly higher mortgage expenses evermore suppressing buying activity. With current 30-year fixed mortgage rates at some 6.7%, significantly higher than long-term average 5.5%, affordability squeeze accumulates, in spite of May’s modest 1.8% in-the-black pickup in purchases. It would seem markets have gone cyclical slowdown mode, driven no doubt in large measure due to unrelenting rates in combination with lofty residential prices.

This downtrend reflects overall economic indecision, as potential purchasers become increasingly hesitant in the face of doubt regarding future Federal Reserve policy. Threat of eventual rate cuts perhaps is stifling transactions, inducing a so-called “buyers strike” in which demand is delayed but not given up. So far, such indecision at mid-monetary-inflection points—a phenomenon substantiated in a series of studies of behavior—is usually a harbinger of cyclical bottoms in house flipping. In the near term at least, however, this is considered a market correction, not structural dislocation.

Here, in being substantially underpriced relative to its scaleable business along with price flexibilitiy, it is in good position to rebound once strengthening demand is observed. Mortgagemarket application levels, indicators of builder sentiment along with housingstarts statistics will need to be watched in an attempt to ascertain whether or not we have bottom in housing or pressure continues to build. These indicators will further lead housing-correlated equity exposures directions.

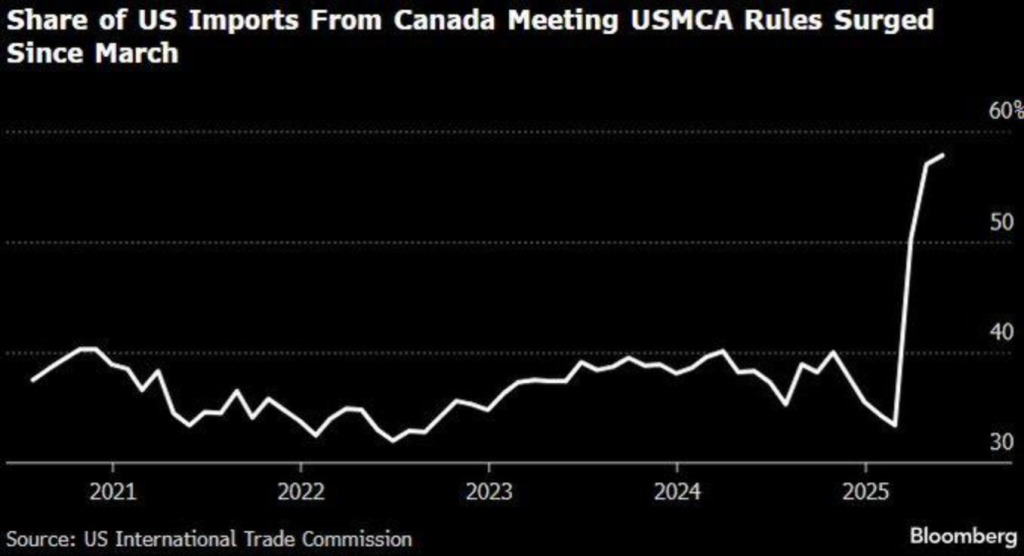

USMCA Compliance Triggers Signal Trade Rebalancing

We watch at Zaye Capital Markets with interest as imports of US products from Canada surge in response to USMCA rules of origin, rising from around 40% in March 2025 to over 60% in July, per some trade commission statistics recently assembled. The sudden influx would seem of a structural nature in trade flows in North America, likely due to redoubled enforcement or tactical rebalancing of export strategies in Canada in an effort to head off impending tariffs as well as maximize USMCA advantages. Both the auto as well as agri-sectors, long associated with complicated standards of compliance, seem at the forefront of such swift rebalancing.

This surge in USMCA-compliant imports is in response to a general US import retreat from Canada, decreasing 1.4% in 2024 to $412.7 billion. Rebalancing is likely due to Canadian export operators rerouting trade along compliant channels instead of diluting volumes across-the-board. Global trade tensions coupled with forthcoming tariff revisions—the most notable of them being the forthcoming 50% tariff on copper commencing Aug. 1—is probably rebalancing. Previous trade flows lie beneath direction: with policy risk build-up, export operators increase compliance as a way of entering under preferential trade agreements.

Against such rebalancing, Freeport-McMoRan Inc. (FCX) is cheap. In response to near-term volatility in copper trade, its long-term presence in compliant sourcing as well as North American base of operations make it a long-term winner of USMCA trade flows. In determining whose sectors will benefit in regulatory edge and how rebalancing of trade can accelerate in Q4, analysts will have to look towards customs compliance statistics, trends in port shipments, as well as primary sector breakdowns of imports by metal as well as autos.

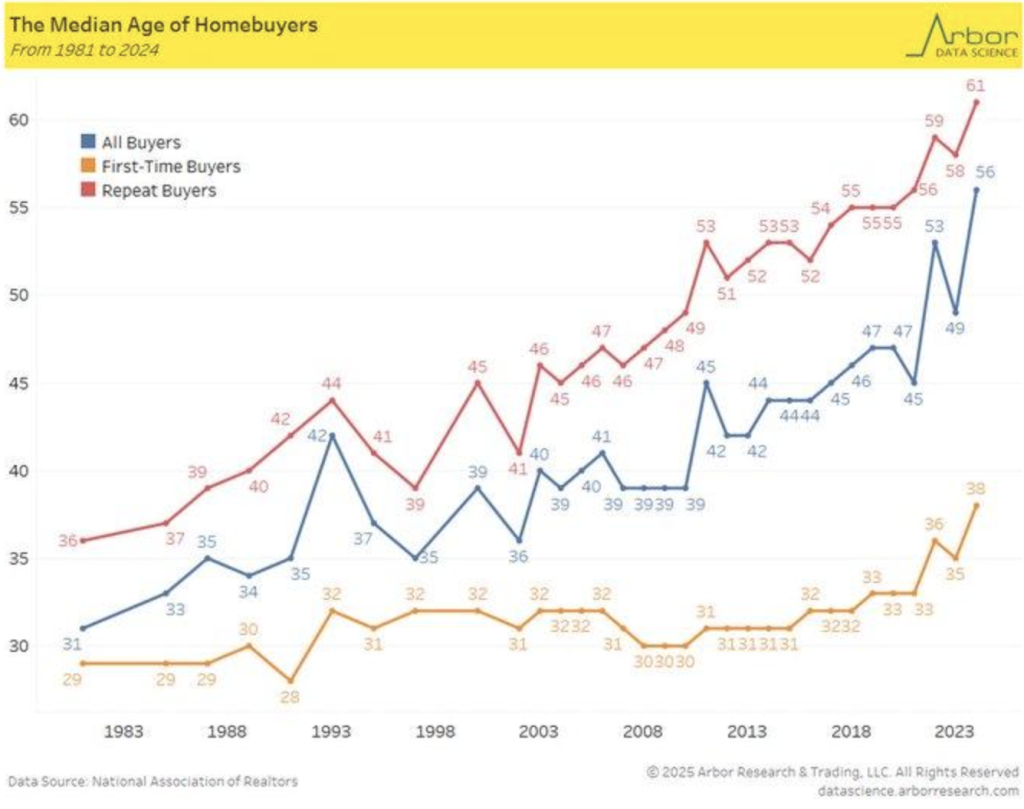

Rising First-Time Buyer Age Underscores Affordability Crisis

At Zaye Capital Markets, we view implications of constantly expanding first-time homebuyers median age of going up from 32 in 2000 through 38 in 2024, based on most recent statistics. As being an indicator of further points of entry in housing markets, it is caused mostly due to a 47% hike in house prices since 2019 along with average mortgage rates of 6.8% in 2024. On downward affordability, homeownership milestone has further been delayed in life, ever increasingly being the realm of older, wealthier, and better-financially insulated buyers.

First-time purchases fell 20% in the past decade, emblematic of a market driven as much by inequality of wealth as rising cost burden. With mixed emotions among citizens (76% of Americans believing affordability is deteriorating), structural problems abound nonetheless. As long as rate policy of the Federal Reserve is at work, actual pressure falls on scarce housing stocks, stagnant wages, and red-tape hurdles. Housing is thus no longer de fault accompaniment of adulthood but circumspectly obtained right of those with financial means.

Zillow Group Inc. (ZG) is considered to be undervalued right now. Focusing on data-driven lease platforms along with web-based residential services, it is in the best positions to take advantage of lagging buying trends combined with elevated long-term leasing demand. Signals of the character of leasing inflation rates, initial mortgage applications volume, as well as changes in buying demography, are to be monitored by analysts in order to gauge long-term orientation of housing market activity combined with probable alterations in real estate capital flows.

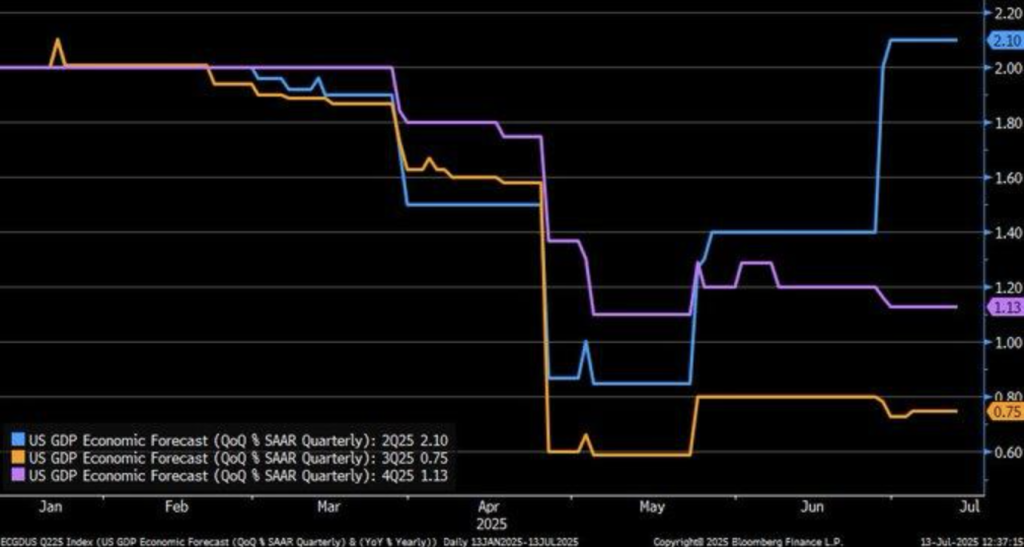

Gdp Growth Set To Fade As Tariff Tailwinds Erode

We’re following closely the reversing trend in U.S. GDP growth with recent estimates depicting a crescendo of about 2.5% in Q2 2025, returning to 1.5% at year-end. That forecast allows for sporadic surge from front-loading of import demand in early 2025 when companies front-run imports ahead of tariff hike. Such chretienic surge as this inflated headline growth is not on this ground on which long-term growth will be built. That trend is already unwinding because of tainted consumption as well as increased trade barriers.

Desirable slowdown is reflected in wider trends in global opinion, as a tariff-driven volatility has warped near-term numbers. Consumer expenditure onshore is retreating as inflation pressures persist and household incomes begin to appear fatigued. Tighter policy term and higher input prices pass through more and more into firm expectations, with forward movements growing more cautious by the day. It does nothing but fuel fears that GDP resilience in Q2 is a high-water mark and not a reference point for trends.

With this cooling climate, Procter & Gamble Co. (PG) looks cheap. Its price strength, worldwide distribution network, and defensive lineup of products are in good position to withstand consumption volatility as well as cost pressure. Real final sales, inventory contributions towards GDP, as well as tariff-adjusted trade flows in the coming months, will need tracking by analysts before they say whether underlying demand will be enough to justify current valuations—or whether further revisions lower in growth will push capital towards defensive equity exposures.

Declining Vix And Shifting Investor Risk Appetite

At Zaye Capital Markets, we examine rekindled same volatility of lower market volatility correlation to lower investor cash deployment. As volatility in the CBOE Volatility Index eased back in response to 2025’s high, there came an easing in AAII cash allocation as well, as a proxy of risk appetite’s return among retail investors in response to perceived market health. It continues as a behavioral proxy of rising bear market sentiment optimism in spite of persistent macro headwinds as well as policy uncertainty.

Historically, VIX served as a sentiment leading indicator of sentiment in markets—necessarily dropping before bull runs—but is context-dependent in its predictive capacity. Events such as the 2022 Ukraine-Russia crisis illustrated VIX’s limitations in periods of geopolitical tension, in this case, in response being less severe than expected. Cash allocation between 2010–2025 shows cash allocation is tactical rather than reactive in nature, with retail investors trading on volatility breakpoints rather than extremes of sentiment in fear.

In this sentiment-positive world, BlackRock Inc. (BLK) appears to be undervalued to this author. As the leader in asset management, it would stand to gain as capital flows out of cash and flows into products in equities and ETFs. VIX positioning, mutual fund flows, and AAII portfolio allocation changes will be primary in determining whether there is an extended risk-on cycle present or whether there is merely a temporary sentiment bounce susceptible to outside interference.

Upcoming Economic Events

Core CPI, Headline Inflation, Empire State Manufacturing, and Bank of England in Focus

With yet another critical period coming up in world markets, a string of world-class economic data will be at the forefront of guiding policy expectations and risk sentiment. From U.S. inflation readings to U.K. central bank commentary, every figure will be under analysts’ microscope as they look to them as harbingers of future monetary tightening, consumer endurance, as well as industrial strength. These are some of things we at Zaye Capital Markets will be watching, and how each event could inform asset prices in the days ahead:

Core CPI m/m, CPI m/m, CPI y/y

Inflation is front and center with three significant readouts: month-to-month core CPI, month-to-month headline CPI, and year-over-year CPI.

- If any of them print one or more of them higher than anticipated, markets would take it as further pressure of price inflation, and this would solidify expectations of a hawkish Fed. That will take a toll on equities—the stocks cocooned around growth—to the expense of U.S. Treasury yields as well as the dollar.

- If, however, data falls below expectations, it would solidify recent disinflation themes, and this would induce a rate-sensitive bounce in such stocks as techs as well as real estate, as well as maybe induce fresh Fed dovishness.

Empire State Manufacturing Index

This monthly first-of-the-month measure of Chinese factory health is an industrial momentum gauge in general.

- A print above expectations would be good news of rising business activity along with rebuilding stocks, positive cyclical stocks, as well as industrial sector strength.

- A soft first number below expectations, however, would be seen as damage done by wider credit spreads as well as soft global demand—triggering risk-off flows, especially small caps as well as in commodity-correlated names.

Bailey Speaks at Bank of England Meeting

Bailey’s commentary will have significant implications for sterling and U.K. rate expectations.

- If he sounds hawkish, particularly in view of intransigent British inflation, markets will price in further tightening—raising gilt yields and underpinning sterling.

- Alternatively, a dovish tone, referencing weaker growth or financial stability issues, will weaken sterling as well as underpin U.K. equities in expectation of policy stimulus. For overseas investors, his prognosis will have implications for central bank sentiment across the board in view of shared inflationary pressures.

STOCK MARKET PERFORMANCE

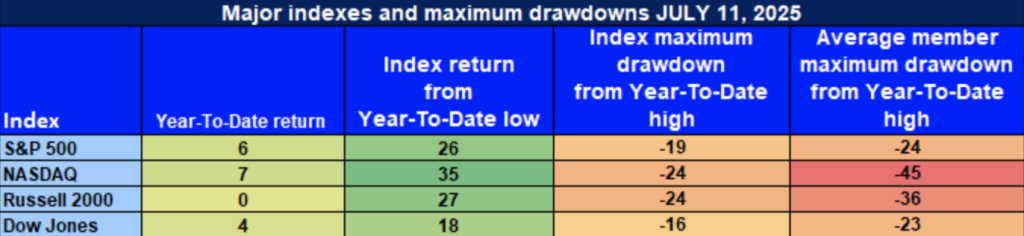

Markets bounce back from April lows but structural weakness persists

We’re observing closely at Zaye Capital Markets U.S. equity recovery from April 8 low. Headlines appear robustly recovered, yet constituent performance beneath headlines tells a highly broken tale. Although major gauges have been improving, member average drawdowns suggest limited leadership and continuing investor skittishness throughout industry.

Analysis of the big four indexes is as follows:

S&P 500: Accelerating Gain but Weak Breadth

S&P 500: +6% YTD | +26% from 4/8 low | -19% from YTD high | Avg. member: -24

The S&P 500 is 26% higher from the April low but only at 6% YTD return. Conversely, -19% below peak levels and -24% average member decline demonstrate that this rally is foundationally dependent on concentrated action. Overall membership is week, particularly in non-megacap groups.

NASDAQ: Solid Upday, But Internals Lag

NASDAQ: +7% YTD | +35% since 4/8 low | -24% vs YTD high | Avg. member: -45

NASDAQ best absolute rebound, but worst average member relative performance versus peers. 35% rebound from trough turns around -45% average member loss, characteristic of further damage in mid-grade as well as growth-oriented technology issues in still converging rate action.

Russell 2000: Failing Small Caps Find It Tough

Russell 2000: 0% YTD | +27% since 4/8 low | -24% from YTD high | Avg. member:-36%

Even with a 27% bounce back from its low, the Russell 2000 is unchanged this year. With its median member -36% slide, the index is a mirror of risk aversion in small companies, especially those with weaker balance sheets and limited price power with minimal credit.

Dow Jones: defensive anchor of stability

Dow Jones: +4% YTD | +18% since 4/8 low | -16% below YTD high | Avg. member: -23% The Dow Jones has faired reasonably well with assistance arriving in defensive as well as industrial exposures. Its 4% YTD return with lowest peak drawdown of -16% is indicative of relative strength. Nonetheless, average member declines of -23% solidifies in place that blue-chip stocks aren’t exempt of general macro headwinds.

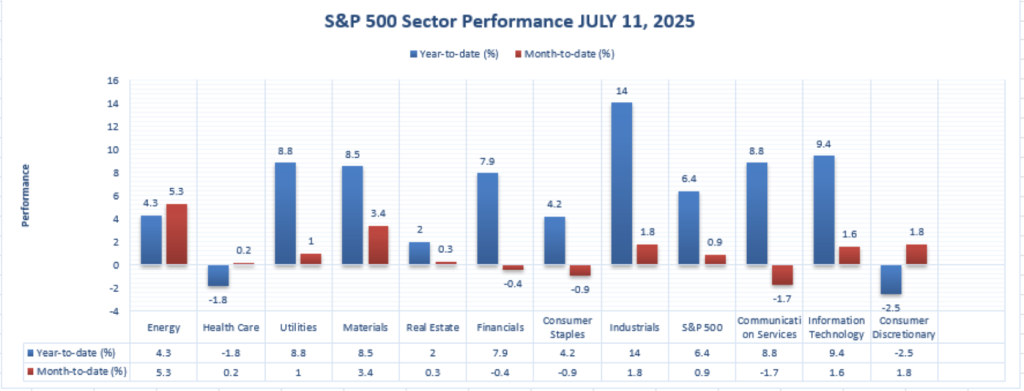

THE STRONGEST SECTOR IN ALL THESE INDICES

Industrials Lead the Charge as Larger Market Looks to Guidance

We are paying close attention to the dispersion at the sector level of the S&P 500, where strength is far from being evenly distributed across the 11 sector groups. Among the 11 sectors, Industrials have been the clear-cut strongest performer thus far in 2025, rising +14.0% year-to-date, ahead of all other groups. Such strength is mirrored in solid demand in the infrastructure, aerospace, and machinery units—segments with solid government contract-based and capex-related initiatives.

While also reporting strong YTD performances in other groups such as Information Technology (+9.4%), Communication Services (+8.8%), and Utilities (+8.8%), they lag Industrials in absolute performance as well as consistency as well. Industrials posted a +1.8% MTD gain as well, equalling Consumer Discretionary and Tech’s 1.6%, indicating persistent buying interest in the sector despite rising rate headwinds as well as geopolitical tensions.

From our perspective, Caterpillar Inc. (CAT) is seen as being undervalued in comparison with its industry peers. Its well-supported worldwide order book, its infrastructure-based energy-transition play, as well as its price power stability, place it in good standing for further appreciation. analysts will require forthcoming forward earnings commentary, new orders statistics, as well as shipments of capital goods data as watch points before it can confirm sector momentum sustainability before it gains entry into the second part of the year.

Earnings

Yesterday’s Releases – 14 Jul 2025

- Fastenal Company

Fastenal reported a good Q2 surprise, with EPS of $0.29, a fraction higher than the consensus estimate of $0.28. Revenue at Fastenal increased 8.6% year over year to $2.08 billion due to strong demand in industrial supplies as well as good execution in its contract channels. Margins also advanced, at 21.0%, due to better cost control as well as favorable supply chain trends. That is due to growing industrial sector confidence as well as the operating leverage of Fastenal as manufactured activity stabilizes after rebalancing.

- FB Financial Corporation

FB Financial posted $0.88 per share in earnings, short of estimates at $0.89. Revenue was up 7.2% from last year at $137 million. Bottom line was, however, marred by a $60 million loss on securities sales, damaging the net income overall, to $2.9 million. Even so, it was able to rise only its net interest margin to 3.68%, offering some relief. Shareholders will be keen to observe the interest rate risk of the institution as well as its balance sheet strategy against more sector headwinds ahead.

- WAFD, Inc. / Equity Bancshares, Inc. / Farmers & Merchants Bank Of Long

Even though there wasn’t any distinct definitive formal announcement of earnings due out at date of writing, preliminary showing is that such local banks have done thus: stable but under pressure net interest incomes, robust deposit franchises, and prudent provisioning. Shareholders will likely concentrate on loans quality, preservation of deposit base, as well as interest rate spread impact as these local banks report in full.

Today’s Expectations – July 15, 2025

- JP Morgan Chase & Co.

JPMorgan will guide consensus of $4.50 to $4.85 per share. Points of focus will be trading revenues, activity in the investment bank, as well as credit quality. Investors will be interested in learning whether there will be any discussion of loan growth as well as initial signs of distress in consumer or commercial books in a challenging rate environment.

- Wells Fargo & Company

Wells Fargo is expected to post the EPS in the level of $1.41, driven by consumer banking stability and net interest income growth. But greatest caution will be taken to factor in possible reserve additions or litigation expenses. The analysts will also factor in the performance of the bank with mortgage and credit card exposures, which remain vulnerable to rates and consumer spending.

- Blackrock, Inc.

BlackRock’s profit is expected between $10.58 and $10.78 a share, supported by rising assets under management combined with solid ETF flows. Investors will be keeping a close eye on how its latest acquisition of Preqin has affected it, as well as whether operating margins have withstood mixed fees.

- Citigroup, Inc.

Citigroup report is likely to have approximately $1.61 EPS, emphasizing its global presence, expanded trading desk, as well as capital base. As the company is vulnerable to emerging markets, investors will be eager to listen to news of international lending as well as currency risks. Any shred of news regarding restructuring and divestiture would further impact investor sentiment.

- The Bank Of New York Mellon Corporation

BNY Mellon will post a good quarter with $1.74 in EPS expected. The key drivers of performance will be custody revenue growth, enhanced asset management flows, as well as cost discipline. Capital markets will be interested in hearing trends in fee income, as well as institutional client demand expectations, against a changing macro backdrop.

Stock Market Summary – Tuesday, July 15, 2025

Markets trade with circumspection as investors navigate a trail of devoted readings of inflation, fresh fears of tariff, and risky reports of earnings. With core prints of CPI coming in at slight levels above estimate along with President Trump’s return of pressure of trade on China, risk appetite is withering away. These news events stoke rate path uncertainty of the Federal Reserve, central as it is entering onto Q3 of market sentiment.

Stock Prices

Financial Signals and Geostrategic Developments

The recent inflation print was a gentle positive surprise, particularly in core markets, in favor of longer-term disinflation. It has cooled speculation of a short-term rate cut, with an anxious tone across the equities markets. President Trump’s most recent remarks regarding possible tariff increases with China had fueled fresh fears of upending world trade, adding yet further pressure on investor confidence. Coupled with softened earnings surprises, these macro concerns are driving volatility and shaping near-term equities performance.

The Magnificent Seven and the S&P 500

The S&P 500 is faltering as key members of the “Magnificent Seven” struggle with profit-taking and policy risk. Both Tesla and Nvidia lagged, with Tesla bogged down by the weight of regulator uncertainty along with difficulties with pullbacks after staggering year-to-date gains for Nvidia. Both Apple and Amazon continued to lag with consumer-based indicators weakening, while Microsoft and Alphabet have remained in relatively solid ground. Concentration risk in these mega-cap stocks is in increasing focus, acting as fuel for thinner market breadth as well as defensive rotation.

Industry Trends: Oil and Technology in the Spotlight

Meta is fast scaling AI plans, with intentions of accumulating industry’s most talent-dense personnel as it develops multi-gigawatt AI clusters driven by NVIDIA’s GPUs. That in itself, combined with a shift towards proprietary AI models, is a flat-out monetisation approach shift. Palantir has remained in spotlights ever since it got top long-term upside ranking from Prospero, due to leadership in data analytics as well as defence contracts. Even oil stocks have been climbing due to mention of nuclear renaissance under re-elected Trump administration by SEC Chairman Chris Wright. CCJ, CEG, VRT, EOSE, as well as OKLO, are among risers. Further, Nvidia’s clearance of lifting bans on further sale of its H20 GPUs in China further shot its shares in overnight trade by over 3%. These sector gains have had significant impacts tech as well as energy leadership in Nasdaq, S&P 500, Russell 2000, as well as Dow Jones.

Major Index Performance as of Jul 15, 2025

- S&P 500: At 5,874.13, down 0.4% during the day

- Nasdaq Composite: At 13,725.42, down 0.6%

- Dow Jones Industrial Average: Near 38,520.75, down 0.2%

- Russell 2000: At 2,087.34, down 0.5%

With building momentum across earnings season, and changing inflation narratives, investors again will be selective with more attention to forward guidance, sector shifts, and geopolitical news. Stay data-driven in direction, but caution at this point is still bullish in market sentiment.

Gold Price – Tuesday, July 15, 2025

The gold price is trading at $3,346.85 per ounce, showing rising sensitivity to inflation, central bank, and rising geopolitical fears news. Yesterday’s modestly stronger-than-expected release of CPI has trimmed expectations of a quick Fed cuts as repeated core services price pressures cement policy direction expectations of a safer course. That has injected stocks markets with fresh uncertainty, summoning renewed focus towards gold as a defensive haven. Sentiment among investors is shifting towards safer havens as the direction of the Federal Reserve gets increasingly murkier and as inflation is considered tougher than expected.

Driving this momentum further, US President Donald Trump’s comments have injectedpolitical risk, in the guise of threats of harsh tariffs on Russia, criticisms of Fed Chairman Powell, as well as de facto support of an alternate candidate in the guise of Kevin Hassett—all stoking fears of policy revision. His statement, “I go on TV and rilethe market,” is a testament of sentiment-based action in this contemporary epoch. Meanwhile, this week’s planned economic releases—the e.g.,Empire State Manufacturing Index as well as BOE Governor Bailey’s comments —should go some way in determining gold’s direction. If this week’s readings of inflation surprise on the upside again, institutional buying of gold can gain momentum further, cementing its haven status further in response to uncertainty worldwide.

Oil Prices – Tuesday, 15 Jul 2025

Brent is currently about $69.16 a barrel and WTI around $66.89, a modest step back from recent highs. Oil markets are negotiating a knotty tug-of-war between escalating supply and ongoing demand tension. OPEC+ continues to increase production—Saudi Arabia alone will add more than some 2.5 million barrels a day to the market during the April-to-September period—while the IEA predicts a large supply surplus in the pipeline that will take its price toll by year-end. Meanwhile, Goldman has just raised its forecast, with Brent forecast to average $66 in the second half of 2025, on hopes of potential supply disruption and the tightening of OECD inventories. Monday’s CPI reading, which showed stickier inflation, also helped support oil, further solidifying that energy prices are still a big contributor in volatility pricing.

President Trump’s most recent comments are injecting further volatility in oil markets. His 50-day threat of action versus Russia in response to Ukraine, along with potential 30% EU, Mexican imports tariff, push crude prices higher in hopes of fresh geopolitical tensions and possible sanctions. But markets have since toned down as diplomatic solutions still cast long shadows. Threats of disruptions in oil supply channels—most prominently in the Middle East—once again act as a floor in oil prices. Release of economic indicators today in the guise of Core CPI, CPI y/y, along with the Empire State Manufacturing Index, will act as a determining force in oil’s near-term direction. Higher-than-expected inflation print can lower expectations of demand and push prices lower, while industrial strength indicators or geopolitical tensions can once again fuel bullish sentiment.

Bitcoin prices – Tuesday, 15 Jul 2025

Bitcoin is trading at $119,420, firming its bullish stance in spite of risk aversion in the macroeconomic landscape. Crypto overall sentiment is bullish in spite of huge institutional buying—Strategy’s $472.5 million buying of 4,225 BTCs and Bernstein’s $200,000 bullish take in this cycle have strengthened market sentiment. In the meantime, geopolitical developments with China and Russia uniting and suggestions of adoption of Bitcoin as store of financial value in either repressed or far-off economies has increased its strategic importance. Yesterday’s release of news on CPI coming out with stickier inflation only ignited the digital currency story as investors see non-mainstream store of values alternatives.

President Trump’s confrontational rhetoric—from tariff imposition on Russia to frank spat with Fed Chair Powell and succession speculation—has injected volatility into legacy markets. As he notoriously exclaimed, “I go on TV and rile the market,” testifying to how politicised monetary rhetoric is going to entrp institutional capital into decentralised markets such as in Bitcoin. Succession speculation of Kevin Hassett taking over as successor of Powell has injected uncertainty towards Fed policy expectations as well. In such environments, the “Digital Gold” thesis of Bitcoin is rising in stature. With scale build-up, large-ticket IPOs such as in Grayscale’s US SEC filing, as well as tech infra buildout such as XAI’s Grok integration towards govt deployment, ecosystem around Bitcoin increasingly sounds solid base.The ecosystem around Bitcoin increasingly sounds solid base. If there is a shock in today’s industrial or inflation data, bet on high correlation between crypto demand and macro instability as Bitcoin once again cements its status as a hedge against fiat weakness.

ETH Price – Tuesday, 15 Jul 2025

At $2,975.74, just shy of its intra-day high of $3,074. Having broken through critical resistance in the $2,800-$3,000 range, bullish pressure is being sustained through some $908 million of weekly ETF inflows, an all-time high since spot ETH ETFs have been available. Institutional buying has significantly drawn down on-exchange available stocks as coins are moved into custody, sparking a near 19% accumulation of whale balances over the week. Technically, Ethereum is considered broken out of key resistance in the $2,800-$3,000 range, with additional upside of some $3,500. Soaring DeFi activity, increasing staking activity, as well as bullish levels of RSI as well as MACD, overall point to a bullish path.

Whale action remains at the center of price action. An entity recently redeemed one of the large holders of over 6,989 ETH in Binance in a three-week span, an extremely powerful long-term accumulation and lower exchange liquidity indicator. A whale transferred another 20,300 ETH into varied DeFi protocols, absorbing additional supply. These tacticalactivities along with ETF-based buying pressure, further compress the market as well as ease sell-side risk. With macro news such as Core CPI as well as the Empire State Manufacturing Index unspooling today, further confirmation of rate cuts or inflation with a lag can further bolster Ethereum’s allure as an alternate yield-providing asset in a tightening financial world.