Where Are Markets Today?

Global futures are signaling a muted opening to the day of business, as U.S. and European indices move modestly as buyers look to developments in a possible U.S. government shutdown. Dow Jones Industrial Average futures fall 3 points, or 0.01%, while S&P 500 futures fall 0.02%, and Nasdaq 100 futures fall 0.03%. This muted market action occurs despite Monday having produced generally favorable follow-through as stocks closed higher across the board as a rebound in stocks associated with the field of artificial intelligence drove sentiment. In Europe, initial action shows modest losses, as Euro Stoxx 50 futures fall 0.11%, as do German DAX futures off 0.07%, and FTSE futures fall 0.06%. Investors look to how a government shutdown in the U.S. might have a ripple effect and a wider impact on world markets.

The big concern behind today’s jittery mood is the threat of a U.S. government shutdown. President Trump and lawmakers have yet to agree on funding as the new fiscal year starts on Wednesday, causing concern about a disruption to government services and business. This could lead to a delay in important economic data releases like this week’s September nonfarm payrolls report. This is one of the most highly anticipated measures of U.S. labor market health and is important to the Federal Reserve in its decision-making process. A delay to this report or its unavailability due to a shutdown could hinder a decision by the Fed to raise rates next October, causing further uncertainty to build in the market.

In spite of all these worries, a ray of optimism is provided by some new economic data and corporate earnings results. U.S. stock indexes closed higher on Monday as they were boosted by a good show from tech stocks, especially those that are connected to the artifcial intelligence business. Investors did seem to ignore the threat of shutdown as they paid heed to good earnings results from major players that exceeded most market projections. This market strength emerged even as more apprehension about a shutdown is growing and inflation fears persist. European stocks also made some gains and this is spurred by an improvement in UK-listed healthcare as well as tech stocks. These stocks are getting a good push from good earnings results and buoyant market mood but are yet to come to terms with all of the wider macroeconomic jitters that include a risk of a U.S. government shutdown. In the days ahead, this week’s economic data releases ranging from the German Preliminary Consumer Price Index (CPI) to ECB President Christine Lagarde’s speech and the Conference Board Consumer Confidence Index will most likely bring a clearer understanding of global economic growth. Results of these studies could affect investor attitudes in Europe as well as in the U.S. and even cause a shift in market perceptions. Barring such data indicating a slowdown or a dovish approach from central banks, it could cement the present bull run in equities. Yet stronger-than-anticipated growth rates or a hawkish stance from central banks could temper market exuberance as apprehensions of valuations of stocks, inflation, as well as higher interest rates, already affect investor sentiment. Eventually, an end to the U.S. government shutdown along with changing economic data would most probably guide markets in days to come.

Major Index Performance through Tuesday, September 30th 2025

- S&P 500: Trading at 6,630.44, up 0.14% on the day.

- Nasdaq Composite: Currently standing at 22,593.12, up 0.29%, as gains build.

- Dow Jones Industrial Average: 0.20% higher to 46,320.35, driven by firmer industrials and financial stocks.

- Russell 2000: Level at 2,436.20, exhibiting soft outperformance as small caps regain com.

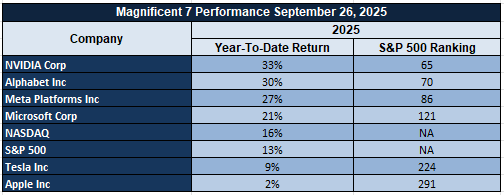

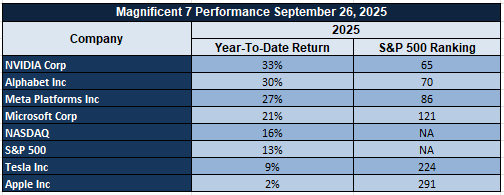

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—face headwinds again today. The group that has powered much of the S&P 500’s advance is tired, and sector-level drawdowns from recent highs average 18%. Nvidia stands alone with strong gains as enthusiasm about its AI-based business model fuels optimism. Meta and Tesla are hit hardest as investors reprice valuations amid deflating AI euphoria and tapering growth estimates. This relative weakness is a sign of a leadership change as investors move into less volatile sectors such as industry and energy. The S&P 500’s further rally potential is uncertain if these Goliath tech stocks do not regain their uptrends.

Drivers Behind the Market Move – Tuesday, Sept. 30, 2025

Global markets are navigating a complex landscape today, influenced by a mix of political developments, economic data, and investor sentiment. Key factors shaping the market’s direction include:

- US Government Shutdown Fears

The potential U.S. government shutdown is dampening market mood. President Trump and lawmakers have so far no agreed on funding as the fiscal year ends later today, raising the prospect of a shutdown that would delay some influential economic data releases such as the September nonfarm payrolls report. This is keeping investors on high alert and leading to sedate market action.

- Trump Trade Policies and Tariff Announcements

President Trump’s most recent tariff announcement, including a 100% tariff on foreign-produced films and a 30% tariff on foreign-made upholstered furniture, is having an impact on market sentiment. These are evoking market nerves about potential retaliation from trade partners and its effect on overall global flow of trade in general. Protectionist trends as such will have a beneficial effect on some sections of industry, but overall market sentiment is taking into account potential negative effects on global relations as well as supply chain flow.

- Upcoming Economic Data and Investor Expectations

Investors are awaiting near-term economic releases such as the German Preliminary Consumer Price Index (CPI), ECB President Christine Lagarde speech, and U.S. Conference Board’s Consumer Confidence Index. These releases will give a view of economic growth potential and central bank policy directions. These report results could affect investor attitudes as well as market direction in the U.S. as well as in Europe.

Over all, market developments on this day are driven by an array of political uncertainties, developments in trade policy, and economic data expectations. Investors are being cautious as they look forward to further developments on these fronts.

Digesting Economic Data

The TRUMP Tweets and Their Implications

In recent comments, President Donald Trump has struck a note of optimism and aggressiveness simultaneously that will have significant potential implications on not only geopolitical developments but also market sentiment. Trump has been especially bullish in comments about the economy of the U.S., repeating that “the economic numbers are great” — a tone that reinforces his optimism about a recovery in the economy. This positive perspective about the economy could have an impact on market activity by reinforcing investor optimism about U.S. growth — particularly in sectors linked to consumer spending as well as industrial production. Even as Trump’s emphasis about economic might could perk up market optimism itself, it is antithetical to current concern about inflation as well as tighter policy from the Fed that keeps riskier assets volatile.

At the same time, Trump’s comments regarding the situation in Gaza have added a new dimension of geopolitical risk. Comments that “looks like we’ll have a Gaza deal” and that he is “optimistic” about a breakthrough toward peace have offered optimism of an end to conflict, but uncertainty around specifics allows much room to speculate. A peace deal would eliminate some of the geopolitical risk that has long been a driver of market instability, especially in commodity sectors like oil. Yet given that such deals within the Middle East have frequently been complicated by difficulties, investors are apprehensive. Trump’s optimism about a deal and that he believes that Netanyahu as well as Hamas might accept his plan is a sign that his government would be considering active intervention in international peace negotiations and might have an effect on wider diplomatic relations and market reactions. Trump’s additional remarks, including his threat to put a 100% tariff on foreign films and his statements on Chinese, Indonesian, and Vietnamese control of the furniture industry, further suggest his protectionist approach, especially in trade. The implication of higher tariffs on foreign products could create uneasiness in global trade markets, having an impact on industry that is dependent on global supply chains. Trump’s past practice of tariffs, particularly Chinese imports, has in the past caused fluctuations in financial markets, and his renewed focus on trade limitations could create an additional risk layer, particularly to tech and manufacturing sectors that are sensitive to global trades. These remarks could provoke further worries from investors about such policy’s effect on corporate profit margins, particularly those having considerable foreign market exposure.

Finally, Trump’s ongoing pressure on inflation and the restrictive policy of the Fed might create further uncertainty in the investment environment. Trump’s remarks that inflation is a bigger threat than jobs reflect the stance of the current Fed and might result in a further tightening cycle. As a tightening of monetary policy aims to keep inflation in check, it might affect liquidity and pose a challenge to higher risk assets, such as tech stocks and cryptocurrencies. Market players will keep an eye on the action of the Fed and will closely look out for indications of a possible impact from Trump’s economic policies on general market conditions. Even as Trump optimism about economic robustness provides support to risk-on environment in the near term, a possibility of trade conflict, geopolitical risk, and tightening financial conditions might dampen market exuberance.

U.S. Real Estate Boom

The latest spike in U.S. pending sales of homes, which rose by 4% in August 2025, has been a subject of interest as it exceeded forecasted 0% growth. The driving force behind this spike seems to be a fall in mortgage rates to below 6.2%, a figure last witnessed in early 2025. This is an indication of a comeback of some sort in the real estate market that had been restricted due to restrictive mortgage rates and a scarcity of inventory. National Association of Realtors indicated a five-month high of contract signings as well, where a regional leader was recorded as having registered a tremendous 6.5% improvement. Nevertheless, even as this is a promising result, a limited inventory of only 4.1 months illustrates difficulties that persist in the market.

A new Federal Reserve survey reveals that cuts in rates, such as the Fed’s latest 25-basis-point cut, are capable of boosting housing demand in a time frame of 1-2 months. This is in line with the recent pick-up in housing sales and could imply that some life is being breathed into the housing market through the desired effect of the monetary policy of the Fed. Nevertheless, caution is necessary as August 2025 softening of labor market data could temper longer-term expectations and prevent sustained growth in housing markets. Analysts must keep an eye on further rate decisions of the Fed and examine if the good momentum in housing will last. From a standpoint of stock performance, real estate is a watch as a potential undervaluation could create opportunities. Stocks that have a connection to housing construction and homebuilding—particularly those that are set to benefit from regional variations in economic recovery—will benefit as the market recovers. Still, analysts would be well served to monitor inventory and shifting interest rate trends to better understand how strong the overall sector proves to be. Homebuilder and real estate investment trust (REIT) stocks could profit from such trends as long as supply constraint issues and general economic considerations are managed properly.

U.S. Economic Health Amid Global Volatility

The September 23-30, 2025, economic data released give a complete picture of the U.S. economy against a backdrop of ongoing global uncertainty. Worth mentioning is the September 4.3% job openings rate that reveals a slowing labor market. This is in line with anticipations that the Federal Reserve will come under increasing pressure to reconsider its interest rate policy. As much as the labor market earlier stoked economic overheating fears, this new shift in employment patterns indicates that inflationary pressures could now ease and push the Fed to a more cautious direction. Job openings-versus-economic-growth equation will be important to analysts as they weigh the central bank’s subsequent tightening of monetary policy decisions that could have large ramifications on the overall economy.

Similarly, other leading indicators such as the ISM Manufacturing Index, which came in at 52.0, and a 2.4% Durable Goods Orders increase demonstrate the strength of the U.S. factory floor. Even as world supply chain interruptions that began during the pandemic have persisted, these numbers indicate a steady ongoing recovery. As a bellwether of the American economy, the manufacturing industry appears to be faring well through all of the global volatility and seems to be a counter-narrative to recession rumors that have filled papers in months past. As supply lines solidify and goods demands remain steady, manufacturers will likely keep adding to economic growth in a positive way. Yet this segment of the economy as a whole is subject to how trends go internationally and is something to watch closely as a potential area of disruption. For investors, the trends point to opportunities in cyclical sectors like manufacturing, industrials, and durable goods. Those companies most set up to capitalize on a recovering manufacturing industry and dealing with global supply chain difficulties will stand to benefit. Stocks in such sectors could experience higher demand as a wider economy regains strength, yet analysts should be concerned about ongoing risk from international instability and changing monetary policy. The direction of interest rates set by the Fed will play a pivotal role in determining investment direction. As such, monitoring the Fed’s coming policy and its effect on inflation and employment information will come into sharp focus as a guide to where market trends will flow in subsequent months.

Cautious Economic Recovery and Capital Spending Prognosis

Current data from the Kansas City Fed’s September 2025 survey indicates a steady increase in the six-month capital spending (capex) forecast of service businesses, yet below the pre- and post-pandemic average. This is an indication that although a recovery trajectory is ongoing in the economy, it is cautious given that businesses remain apprehensive about supply chain interruptions on a global scale and wider market fluctuations. Since 2020, the capex forecast as a leading indicator of prospective business investment has remained muted, indicating a wait-and-see stance by businesses. This might mean that businesses are giving strategic priority to short-term survival and business stability rather than long-term business prospect development as they contend with ongoing uncertainties in the global economy.

Historical data and economic analyses reinforce this cautious outlook, with weak capex trends often correlating with slower job growth. A study from the National Bureau of Economic Research in 2023 linked declining capital expenditure in the service sectors to a 1.2% annual lag in employment, indicating that lower investment in expansion often results in stagnation in hiring. This slower growth trajectory could challenge the narrative of a robust economic rebound, suggesting that while some sectors are recovering, others are still struggling to regain momentum. Firms appear to be holding back on long-term investments, potentially signaling more conservative business strategies moving forward. This unwillingness to make firm capital investment commitments is an echo of past trends during recessionary periods like the 2008 financial crisis when capex recovery trailed GDP recovery by more than two years. This same dynamic might materialize in this recovery as well, as firms are hesitant to invest more in expansion and infrastructure even when a larger economy is improving. For analysts, such an important lesson is that this cautious approach might cull potential returns in some sectors that are most dependent upon strong capital expenditure like construction and manufacturing. Stocks from those sectors might suffer unless a larger commitment is made to long-term investment. Following employment data and trends in capex will be important to understanding a wider economy as well as potential risk to expansion.

Declining Savings and Shifting Consumer Behavior

The U.S. personal savings rate dropped to 4.6% in August 2025, marking a significant decline from the peak levels observed during the 2020 pandemic when stimulus checks propelled savings to over 32%. This decline signals a shift from forced savings to increased consumer spending, which has been largely driven by persistent inflation and a normalization of economic behavior. As consumers spend more amid inflationary pressures, the savings rate continues to edge lower, reflecting an adjustment to the economic environment and the gradual reduction in pandemic-induced financial buffers. The current savings rate suggests that consumers may be prioritizing immediate consumption over long-term savings, a behavior that may be sustained as inflation remains elevated.

Research from the National Bureau of Economic Research (NBER) suggests an inverse relationship between savings rates and consumer confidence. This aligns with data from the University of Michigan, showing sentiment levels similar to those seen in September 2008, which was marked by heightened economic uncertainty. The decline in savings, coupled with lower consumer confidence, indicates that households may be feeling more financially strained, possibly due to rising costs and the ongoing uncertainty in both domestic and global markets. Analysts should carefully monitor how these trends evolve, as changes in consumer sentiment and spending behavior will play a crucial role in shaping the economic landscape moving forward.

In addition to the immediate pressures from inflation, historical data from the Federal Reserve reveals another long-term factor contributing to the decline in savings rates: an aging population. As individuals reach retirement age, they begin to draw down their retirement funds, leading to lower overall savings. With an increasing number of individuals turning 73.5—approximately 3 million annually—this demographic shift is expected to contribute to a further decline in savings rates in 2025. For analysts, this trend highlights a potential challenge to future consumer spending, as the decline in savings could dampen the ability of retirees to maintain their pre-retirement spending levels. As such, sectors that rely on discretionary spending may face headwinds unless the overall economic situation improves. Monitoring savings trends and consumer behavior will be key for understanding how these factors influence broader market movements and investment opportunities.

Consumer Confidence Diverging from Labor Market Reality

The latest data from the University of Michigan consumer sentiment survey shows that “Buying Conditions for Large Household Durables” index has declined substantially from its earlier 2000s’ levels. Nevertheless, present data indicates that consumers are looking forward to some relief in prices that is most likely associated with softening trends in inflation. This development is consistent with reports including Atradius Collections’ 2025 forecast that anticipates a sales rise of 5.3% in consumer durables. Consumers appear to be hoping for some relief from price pressures that could foreshadow inflation might come down from its earlier feared status of being as entrenched. Optimism of this sort is going to have to be diluted by a grain of salt given that the wider economic situation is flashing signs of divergence that particularly exist between consumer sentiment and labor market realities.

The latest softening of the U.S. labor market complicates the story. In August 2025, just 22,000 jobs were added, and unemployment hit 4.3%, as reported by the U.S. Labor Department. These data indicate a possible slowdown in jobs creation and employment growth that would affect consumer confidence in the long run. This gap between promising consumer sentiment and softening labor market signals appears to be a late-cycle economic phase wherein confidence is just not matched by economic realities. As past analysis has revealed, such a phase tends to create uncertainty among consumer spending, particularly when employment insecurity is on the upswing although inflation is tapering down. Observing past trends in the “Buying Conditions of Large Household Durables” index from 1990 to 2025 reveals cyclical fluctuations correlated to shifts in economic policy as well as international trade tensions. As an example of this, U.S. tariffs against Chinese products have resulted in repressed demand without visible stimulation from sales efforts such as government-backed trade-in programs. Atradius’ forecast of 4%-5% per annum consumer durables growth against a background of growing protectionist risk serves to highlight how vulnerable consumer spending is in this industry. Analysts must interpret consumer optimism with some circumspection as exogenous events such as trade tensions and employment market trends may resulted in restricted growth among consumer durables if a deepening economic slowdown occurs. Tracking this aspect will be requisite to determining whether such a shift in consumer sentiment becomes a sustained source of growth.

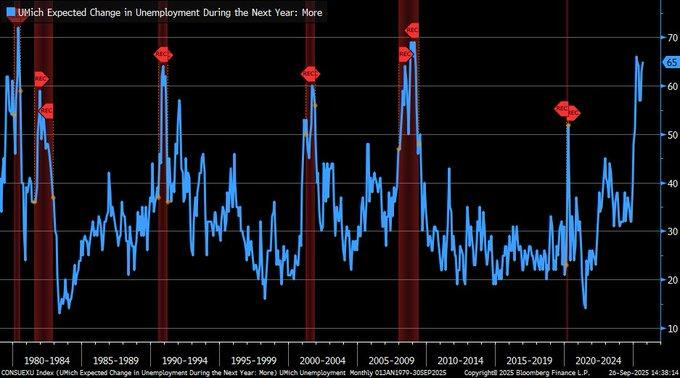

Rising Unemployment Expectations and Consumer Pessimism

The latest data from the University of Michigan’s consumer survey reveals a significant rise in consumer expectations for higher unemployment, with 65% of respondents anticipating job losses in 2025—an outlook not seen since the 2008 financial crisis. This sharp increase suggests potential economic unease that extends beyond the official labor market statistics. While the unemployment rate currently sits at 4.3%, this heightened expectation of job losses could signal deeper concerns about the economy. Consumer sentiment is increasingly pessimistic, which may impact spending behavior and consumer confidence, even if the official data does not yet fully reflect such concerns.

Historical evidence from the Bureau of Labor Statistics reveals that consumer anticipations of increasing unemployment frequently come just before actual unemployment increases. To illustrate this point, in 2007 when comparable spikes in the survey of the University of Michigan depicted more than 50% of consumers anticipating losses of jobs, the unemployment rate of the U.S. rose by 2%. This is an indication that a perception of the economy among its consuming class might be a precursory indicator of labor market trends as a self-fulfilling prophecy. When consumer confidence falls, lower spending could exert downward pressure on economic activity and thereby create the self-fulfilling prophecies that people harbor about prospective employment insecurity. This psychological change will have real life implications on an economy, especially those sectors that are sensitive to discretionary spending. In addition, a 2023 Journal of Economic Behavior & Organization paper discovered that AI-job displacement fears have a strong connection to amplified unemployment expectations. As AI implementation continues to expand, pessimism among consumers also increases, and a 10% jump in AI implementation is associated with a 1.5% spike in unemployment expectations. Present unemployment concern trends might thus be intensified by technological changes and automation, furthering consumer fears about work trends. For analysts, this increasing pessimism, if it persists, could prove problematic for consumer spending-dominated sectors as fears of job losses might prompt more cautiousness further dampening wider economic revivals. Tracking consumer sentiment shifts as well as automation trends will be important in determining potential trends in subsequent economic declines.

Services Sector Contraction and Threat of Inflation

The Kansas City Fed Services Index declined to -9 in September 2025, tying its cycle low, indicating a severe contraction in services activity in the U.S., which accounts for about 70% of GDP. Importantly, the employment component of the index hit its lowest reading since 2020, implying a possible freeze in the labor market amid regional economic pressure, especially in Plains states. This major decline in services activity reflects underlying vulnerabilities in one of the largest and most important parts of the economy. This is something that analysts have to watch very closely, as this sustained contraction in services could have far-reaching consequences in terms of overall economic growth in terms of lower consumer spending as well as losses of jobs.

This decline in the services sector is compounded by a 10% year-to-date drop in the Dollar Index (DXY), marking the worst performance since the 1973 oil shock. According to Federal Reserve models, this weakening of the dollar could add approximately 30 basis points to inflation, potentially pushing the economy into a stagflation scenario—where stagnant growth coincides with rising prices. This scenario, reminiscent of the 1970s, poses significant risks for both policymakers and investors. With inflationary pressures mounting while growth stagnates, the Federal Reserve may face difficult decisions on interest rates, as it balances the need to control inflation without further stalling economic recovery. The timing of these developments—taking place right before the holiday season—makes this outlook complicated. Seasonal employment during this time of year is a boon to employment numbers. Yet a 2023 National Able report explained that seasonal employment is once again at pre-pandemic levels, a sign of a more cautious economy. As unemployment is higher in some areas of the nation and economic uncertainty weighs on consumer spending patterns, Federal Reserve policy choices later in 2025 about interest rates will be important. Should inflation keep increasing yet weakness be developing in the labor market, the central bank will have to tighten policy again and could induce further slowdown in the economy. These macroeconomic signals will have to be closely watched by investors as they will have much to do with determining market trends’ direction in the months to come.

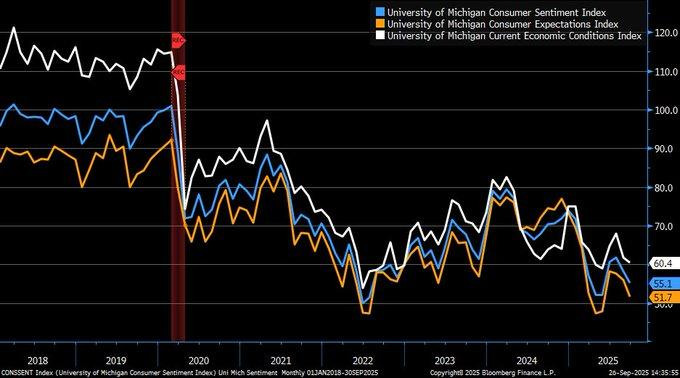

Declining Consumer Sentiment and Resilient Spending

The University of Michigan Consumer Sentiment Index declined to 55.1 in September 2025 following a 5% fall from August. This is a precipitous drop spurred by growing inflation fears and softer labor market prospects, as 44% of consumers named high prices as a huge financial problem by the university’s September 15, 2025 report. This fall in sentiment is an indication of increasing consumer anxiety as people feel pricing pressure from ongoing inflation and a labor market that no longer provides as much security as it used to do. Market analysts should keep an eye on whether such shifts in sentiment are a sign of a larger move to lower consumer confidence as such patterns may foreshadow slower spending growth in the near term.

In spite of the decline in sentiment, consumer spending has been unusually robust, a trend that might be accounted for by a lagged effect in consumer attitudes. According to a 2023 study prepared by the Federal Reserve, it is usually found that a 6-12 months’ gap exists between changes in consumer sentiment and concomitant changes in spending patterns. This lag effect might imply that although consumers are growing more apprehensive, their spending patterns have yet to fully reflect such attitudes. Analysts should therefore be circumspect about predicting an immediate fall in consumer spending because it might take a few months before such shifts in sentiment register as lower intake that is a main impetus of U.S. economic activity. To further complicate the forecast, international economic expectations in the IMF’s 2025 World Economic Outlook indicate a humble 3.0% worldwide rate of growth that could further escalate consumer apprehensiveness in the U.S. As tariff uncertainties and fiscal pressures reconstitute global trade patterns, especially against major U.S. trading partners, the economic landscape will potentially be less consumer-positive. American consumers already dealing with inflation and employment market worries may bear the additional burden of international economic instability, which could affect their buying decisions further. Market analysts must monitor closely how global economic considerations, paired with national sentiment patterns, will dictate consumer patterns in the coming months, especially as trade and fiscal policy uncertainties further materialize.

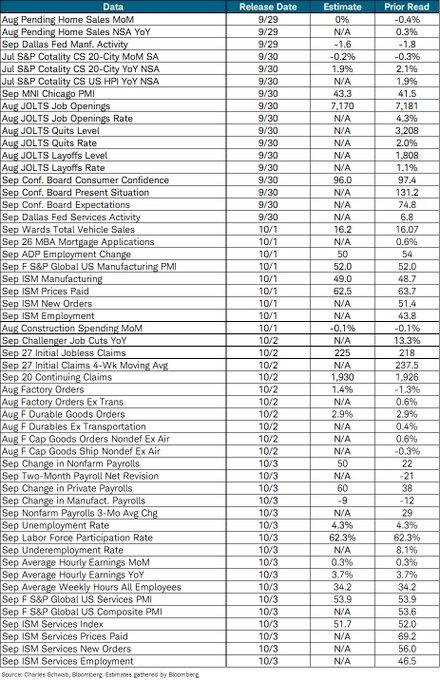

Upcoming Economic Events

German Prelim CPI m/m, ECB President Lagarde Speaks, JOLTS Job Openings, and CB Consumer Confidence

Heading into yet another pivotal week of economic releases from around the globe, a series of major economic events will come to a head in investor sentiment and have a broader effect on the market environment. From inflation data from Germany to Consumer Confidence from America, all of these economic indicators have the potential to jolt markets and provide additional insight into economic health worldwide and within each nation. Below is a list of those major data releases to watch this week, and how each is likely to move markets if actual numbers come in higher or lower than predicted:

German Prelim CPI m/m

September 2025 Germany preliminary Consumer Price Index (CPI) is a highly awaited publication that will give important information about trends in inflation in the largest economy of the Eurozone.

- If actual CPI is higher than expected, this could be interpreted as a build-up of inflationary pressure in Germany that might induce a more hawkish approach by the European Central Bank (ECB) in the near term. A higher-than-expected CPI would strengthen the Euro as market players re-price tighter monetary policy expectations that could lead to higher European bond yields. This development would put pressure on risk assets, such as stocks, as higher rates of interest threat usually undermines investor sentiment materially more in more growth-sensitive areas.

- However, if the German CPI figure is below market expectations or lower than forecasted, it might be interpreted by markets as evidence that inflationary pressures ease in the area. It could dampen worries of further tightening by the ECB and promote a dovish tone, which would result in a softer Euro as well as a risk asset rally such as stocks. Additionally, softer inflation data might stimulate some buying of bonds as investors aim to pre-buy lower yields even before it is possible that the ECB might move to a more accommodative stance.

ECB President Lagarde Speaks

The remarks of ECB President Christine Lagarde are extremely important, as her speeches give good indications of how inflation, economic activity, and monetary policy are faring from an ECB perspective.

- Should Lagarde turn more hawkish, expressing worries about increasing inflation or a further tightening of policy, we might witness a stronger Euro as price action reflects higher interest rates in the months to come. This would probably exert upward pressure on European bond yields as markets reprice the trajectory of ECB monetary policy. An even more forceful approach might also result in a spike of volatility in equity markets, especially in growth sectors, as higher rates tend to negatively affect the current-value of future earnings.

- However, if Lagarde’s intervention is dovish, suggesting concern about slow economic growth or ongoing European economy difficulties, this would lead to a depreciation of the Euro and a risk asset rally. Dovishness could imply that a sharp short-term tightening of interest rates is less probable from the ECB and accommodative monetary policy will be sustained. This would be favorable to equities, particularly risk-on sectors such as tech and consumer discretionary, as investors will be moving in search of higher returns when borrowing is lower.

JOLTS Job Vacancies

The JOLTS Job Openings is an important leading indicator of labor market health in America. The report presents an aggregate view of vacancies and employment trends within the economy.

- A higher-than-anticipated number of job openings would imply that firms are continuing to engage in hiring activity, which would indicate strength in America’s labor market. A stronger-than-anticipated reading could lift investor optimism about economy resilience, favoring sectors that drive growth like consumer discretionary and industrials. Additionally, strong job openings would most likely solidify a view that America’s economy continues to grow, which could push equities upwards and affirm the perspective of steady economic expansion.

- But a dismal JOLTS report that registers fewer job openings than anticipated could be an indication that companies are trimming their hiring plans, which will be an indicator of slow-down of economic activity. Less-than-anticipated job openings data would most likely create a risk-off mood in the markets as it would raise a question about labor market robustness. Such a trend would push investors into safe-haven assets such as bonds as well as gold. Cyclical sectors such as consumer discretionary as well as materials might come under selling pressure. A precipitous fall in the job openings report could create a negative perception regarding employment growth in the near term as well as give rise to perceptions of a potential slow-down of economic activity.

CB Consumer Confidence

The Conference Board (CB) Consumer Confidence Index is an important indicator of household sentiment and future spending in America.

- Better-than-expected reading could demonstrate that customers have better attitudes about their finances and overall economy, inducing higher consumer spending in major sectors of business like retail and services. When consumers are more optimistic, they will spend or even increase their spending rates, which is an engine of economic activity. Good confidence reading could buoy equities, particularly those that heavily depend on consumer spending like retail, tech, and travel.

- To the contrary, if the CB Consumer Confidence report is lower than anticipated, it might be an indication that consumers are becoming increasingly cautious given fears about inflation, interest rates, or job security. Slumping consumer confidence would result in less spending, especially across discretionary sectors, which will temper the overall growth forecast. Investors would then anticipate a move into safer sectors such as utilities, healthcare, and consumer staples. Risk assets such as high-growth stocks might come under pressure. Downbeat surprise in consumer sentiment might even invoke worries about a sustained recovery in the economy and could induce a shift in expectations about coming monetary policy.

As these pivotal economic developments play out, market players will be keeping a watchful eye on actual results compared to projections, as they might have a significant effect on asset prices. Whether indicating stronger economic activity or more conservative consumer spending, the ramifications of such data on monetary policy as well as sentiment will be significant. Investors will want to keep close attention on these important releases as an economy’s timing of data can provide discerning information regarding its future direction as well as that of the global economy.

Stock Market Performance

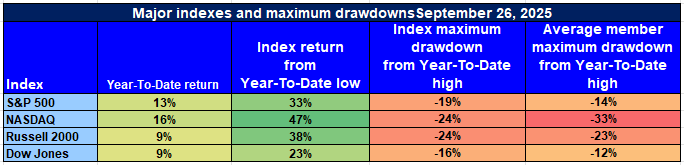

Indexes Bounce Back from Apr lows, But Narrow Breadth Predicts Ongoing Prudence

Equity markets in the U.S. have registered significant gains from the lows of April 8th but year-to-date have yielded mixed results as underlying drawdowns spell weakness hiding in plain view. Even as major indices have registered favorable momentum, a closer examination of average constituent action reveals that market breadth is thin and volatility is entrenched in the market’s fabric.

This is our summary of most recent performance of all top indexes:

S&P 500: Sturdy Headlines, Though Narrow Leadership

YTD: +13% | +33% lower than April low | -19% lower than YTD top | Avg. member: -14% | Avg. member drawdown from YTD top: -25%

The S&P 500 is robust year-to-date as it is up 13% in 2025 and has risen by 33% from the lows of April. But having a 19% decline from its top and an average member experiencing a 14% decline reveals that gains have been heavily concentrated in large-cap stocks and that a strong breadth of this rally is something that is lacking.

NASDAQ: Growth Struggles Amid Sharp Declines

YTD: +16% | +47% lower than April low | -24% lower than YTD high | Avg. member: -33% | Avg. member drawdown lower than YTD high: -48%

The NASDAQ has registered a good 16% YTD return, having rebounded by 47% from its Apr low. Yet a 24% drop from its YTD high and a stunning 33% average member decline indicate that weakness persists in the tech-dominated index. Notably, a 48% average member decline from its top reflects how volatile and delicate the sector remains.

Russell 2000: Small-Cap Gains Mask Underlying Struggles

YTD: +9% | +38% below April low | -24% below YTD high | Avg. member: -23% | Avg. member drawdown below YTD high: -38% Although the Russell 2000 has rallied 38% from its low in April, its 9% YTD return is evidence of a lack of conviction in small-cap stocks. Even with the rally, a 24% peak drawdown and a 23% average member drawdown, having an average 38% drawdown from YTD highs is evidence of extreme distress in smaller, economically sensitive stocks.

Dow Jones: Defensive Resilience Amidst Broader Weakness

YTD: +9% | +23% lower than April low | -16% lower than YTD high | Avg. member: -12% | Avg. member drawdown lower than YTD high: -23% The Dow Jones is also holding up well, up 9% year to date and 23% from the lows in April. A somewhat typical 16% correction from its high shows strength, yet average member corrections of 12% and 23% from peaks demonstrate even in defensively oriented sectors some areas of weakness.

At Zaye Capital Markets, we remain selective in our approach, focusing on high-quality stocks with robust balance sheets and stable earnings streams. We are monitoring market breadth closely to gauge whether the rally is broadening and becoming more sustainable. As volatility persists, we are cautious but continue to find attractive opportunities in more defensive sectors.

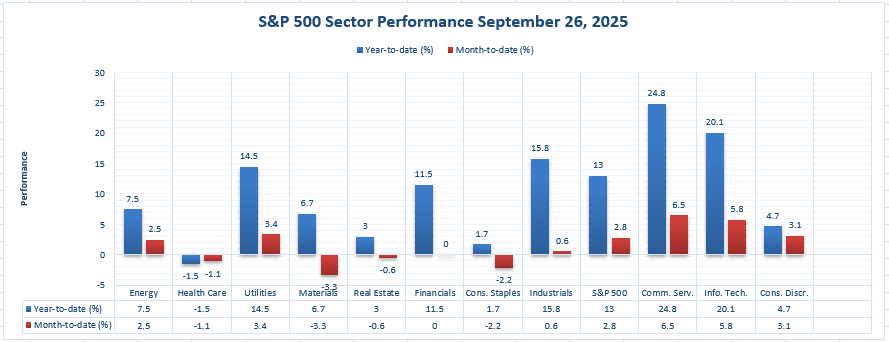

The Strongest Sector in All These Indices

Communication Services Leads the S&P 500 — Outperformance Driven by Growth, Momentum, and Digital Transformation

As of September 26th, 2025, Communication Services is currently the top-performing sector of the S&P 500, having a year-to-date return of 24.8% and a month-to-date return of 6.5%. Such a strong outperformance reflects the sector’s strong growth due to.digital media, entertainment, and a strong consumer desire to connect. Firms in this segment are benefiting from a sustained recovery in digital ads, streamed services, and online platforms that are driving better earnings growth and higher margins.

The relative strength of Communication Services across short- and long-term frames distinct it from others. Though Information Technology registered a healthy +20.1% YTD return and Industrials recorded a +15.8% YTD return, even those have not come close to emulating Communication Services’ rally in terms of distance or duration. Communication Services’ 6.5% month-to-date advance is close to 80 basis points ahead of Information Technology, its closest peer. Such a large outperformance is a good indicator of investor rotation into high-growth and high-margin businesses capable of faring well even against a difficult macro picture.

We’re optimistic about a handful of our top Communication Services picks, namely those that have leadership positions within digital infrastructure, content creation, and AI-powered advertising platforms. Revisions to Communication group earnings in Q3 will be of particular interest to analysts as margin guidance and trends in advertising expenditures will be a big determining factor of whether this group will be able to sustain this momentum into fourth quarter. Communication Services is a leader among absolute returns as well as risk-adjusted performance and is playing a significant role of this broader S&P 500 recovery narrative through 2025.

Earnings

Earnings Update – September 29, 2025

- Carnival Corporation (CCL)

Carnival Corporation reported a strong third-quarter performance, with earnings per share (EPS) of $1.43, surpassing estimates by 8.33%. Revenue reached $8.2 billion, exceeding expectations by 1.36%. The company achieved an all-time high net income of $1.9 billion and adjusted net income of $2.0 billion. This marks the tenth consecutive quarter of record revenues. Carnival raised its full-year 2025 adjusted net income guidance to a nearly 55% year-over-year increase, driven by improved net yields and effective cost management. The results reflect the company’s ability to navigate operational challenges and capitalize on strong consumer demand for cruises and leisure travel.

- Jefferies Financial Group Inc. (JEF)

Jefferies Financial Group reported Q3 2025 earnings of $1.01 per share, beating the estimated $0.59 by $0.42. Revenue for the quarter was $2.05 billion, a 21.6% increase year-over-year. The company’s net margin stood at 7.7%, with a return on equity of 6.59%. This performance reflects a strong rebound in Wall Street deals, contributing to Jefferies’ record quarterly financial results. The firm’s robust investment banking and wealth management services were the key drivers behind its performance, positioning it well for future growth despite market volatility.

- Vail Resorts Inc. (MTN)

Vail Resorts reported a Q4 2025 loss per share of $5.08, missing expectations. Revenue for the quarter was $271.29 million, a 2.2% increase from the previous year. The company cited challenges in the operating environment, including increased competition and reduced sales volume, which impacted profitability. The decline in skier visits due to unpredictable weather conditions and increased operating costs also weighed on the quarter’s results. Vail Resorts’ ability to adjust its strategy in response to these challenges will be crucial for its recovery in the coming quarters.

- Progress Software Corporation (PRGS)

Progress Software reported Q3 2025 earnings per share of $1.50, exceeding the estimated $1.38. Revenue for the quarter was $250 million, surpassing the forecasted $240.11 million and marking a 40% year-over-year increase. The company also raised its full-year guidance, reflecting strong demand for its AI-powered software solutions. This impressive performance was driven by robust growth in cloud offerings and strategic partnerships, which continue to position Progress Software as a key player in the enterprise software market.

Upcoming Earnings – September 30, 2025

- Nike, Inc. (NKE)

Nike is scheduled to report its Q2 2025 earnings today. Investors should focus on revenue growth, particularly in international markets, and any updates on the impact of global supply chain challenges. Nike’s digital sales and the performance of its Nike Direct segment will be key factors in understanding its ability to maintain its leadership position in the global athletic wear market. Additionally, insights into inventory management and demand trends in key regions like North America and China will provide a clearer picture of Nike’s operational health.

- Paychex, Inc. (PAYX)

Paychex is set to release its Q2 2025 earnings today. Key metrics to watch include revenue growth driven by demand for HR solutions and any updates on the integration of recent acquisitions. Investors should also look for guidance on the company’s outlook for the remainder of the fiscal year, especially in light of macroeconomic factors affecting small and medium-sized businesses. Paychex’s ability to maintain strong margins and customer retention will be critical as it navigates an evolving labor market.

- Lamb Weston Holdings, Inc. (LW)

Lamb Weston is expected to report its Q2 2025 earnings today. Investors should pay attention to revenue trends, particularly in the foodservice sector, and any updates on the company’s efforts to manage input costs and supply chain efficiencies. Lamb Weston’s strategic initiatives to drive growth in frozen potato products and expand into international markets will be key areas to watch. Additionally, guidance on the full-year outlook will provide insights into the company’s strategy to navigate a competitive food industry.

- United Natural Foods, Inc. (UNFI)

United Natural Foods is slated to release its Q2 2025 earnings today. Key areas of focus include revenue growth in the natural and organic products segment, improvements in operational efficiency, and any updates on the company’s efforts to reduce debt and enhance shareholder value. Investors should also look for guidance on the company’s strategy to address challenges in the grocery wholesale industry, especially as consumers continue to seek healthier and more sustainable food options. The company’s ability to manage rising input costs and maintain profit margins will be crucial in determining its long-term prospects.

Stock Market Report – Tuesday, September 30th, 2025

U.S. stocks have started the day cautiously as investors are dealing with a mix of economic data and lingering geopolitical tensions. Nasdaq and the S&P 500 are modestly higher due to gains in semiconductor matters, yet wider valuation fears, higher Treasury yields, and long-standing global trade tensions temper mood. Dow Jones and small-cap proxy Russell 2000 are modestly strong due to money rotation into defensively-positioned sectors and small-cap shares.

Stock Prices

Geopolitical Events and Economic Indicators

Today’s mixed tone in the market is being spurred by some factors such as worries of a U.S. government shutdown that could postpone some important economic data. Investor sentiment is further dampened by some remarks recently on how highly priced U.S. equities are and potential growth slowdown even as inflation cools down. Geopolitical risks that are mainly centered on China and worries about a slowdown in global economic activity are causing risk-off mood among some investors that have resulted in a scaling back of risk assets and selective seeking of safe haven positions in defensives.

Latest Stocks News

- $RKLB | Rocket Lab (RKLB) has been awarded 10 more dedicated electron missions from Synspective. This transaction cements leadership in satellite launch markets by Rocket Lab, especially as small satellite services continue on an uptrend spurred by growing commercial interest in global data infrastructure.

- $EOSE | Eos Energy Enterprises (EOSE) just became the 6th small-cap multi-bagger. It is a company that is capitalizing on its specialized focus of providing an alternative to legacy hardware that is struggling to keep up with growing electrification and AI demands.

- $OPENAI | OpenAI is testing an AI-enabled TikTok-like application that will incorporate AI-created video. Such an application would drastically revamp content creation and online media through a new wave of scale-able social media video production automation as yet another step in the rapid-evolutionary application of AI to media and entertainment.

- $HOOD | Robinhood’s prediction markets have now exceeded 4 billion event contracts. The site is quickly becoming an engine of volume that is among the most quickly growing as it shows more and more popularity among retail investors and can challenge traditional financial marketplaces.

The Magnificent Seven and the S&P 500

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—face headwinds again today. The group that has powered much of the S&P 500’s advance is tired, and sector-level drawdowns from recent highs average 18%. Nvidia stands alone with strong gains as enthusiasm about its AI-based business model fuels optimism. Meta and Tesla are hit hardest as investors reprice valuations amid deflating AI euphoria and tapering growth estimates. This relative weakness is a sign of a leadership change as investors move into less volatile sectors such as industry and energy. The S&P 500’s further rally potential is uncertain if these Goliath tech stocks do not regain their uptrends.

Major Index Performance through Tuesday, September 30th 2025

- S&P 500: Trading at 6,630.44, up 0.14% on the day.

- Nasdaq Composite: Currently standing at 22,593.12, up 0.29%, as gains build.

- Dow Jones Industrial Average: 0.20% higher to 46,320.35, driven by firmer industrials and financial stocks.

- Russell 2000: Level at 2,436.20, exhibiting soft outperformance as small caps regain com.

We have a “risk-on but cautious” approach at Zaye Capital Markets. Mega-cap tech health is once again pivotal to maintaining a rally. As long as earnings are decent and inflation continues to decline, a soft rebound is plausible. Elsewhere, less valuation-intensive areas may have firmer investment potential against this background.

Gold Price – Tuesday, September 30, 2025

Gold prices have spiked to new records, climbing to $3,842.76 per ounce as of this week, an impressive 11.4% September return and a stunning 45% year-to-date. This surge is mainly spurred by increasing safe-haven demand for gold as a result of escalating geopolitical tensions, mainly driven by this week’s ongoing conflict in Gaza and fears of a potential U.S. government shut-down. Market jitters persist as uncertainty around these developments continues to build, driving money into gold. Furthermore, gold is also boosted by speculations of potential interest rate decreases by the Federal Reserve as Treasury yields and inflationary pressures make assets that carry a yield less appealing. Though some optimism about President Trump suggesting a potential peace deal in Gaza this week has some optimism about this week’s developments, uncertainty about U.S. fiscal policy and the wider global economic outlook continues to drive safe-haven buying of gold. Investors remain optimistic yet cautious as they monitor developments that will dampen or drive this week’s safe-haven buying of precious metals. As we approach today’s economic data releases—German Preliminary Consumer Price Index (CPI), ECB President Christine Lagarde speech, U.S. Job Openings (JOLTS) and Conference Board Consumer Confidence Index—the attention is centered on how these numbers will affect investor sentiment and subsequently gold prices. If data reveals an economic slowdown or signals that central banks, especially the ECB and the Federal Reserve, will most likely keep dovish monetary policies in play, it would most likely solidify gold’s bullish momentum. Otherwise, stronger-than-anticipated economic data or central bank hawkish signals might dampen gold’s rallying bid as investors might again look to riskier assets that bear higher yields. Gold’s price action in the days ahead will depend on an interplay of these economic indicators, geopotential events, as well as market anticipations of subsequent monetary policy in the weeks to come. As it is now, the metal is a lead player in the larger investment universe and its price action is closely linked to an evolving global economy.

Oil Prices – Tuesday, September 30th 2025

Crude prices have recorded a marginal decline today as U.S. West Texas Intermediate (WTI) crude is quoting at $63.05 a barrel and Brent crude is quoting at $67.53 a barrel. This decline is a result of a series of supply-side events which have dampened the bullish momentum in the market. OPEC+ is likely to approve a production increase of 137,000 barrels a day in its next meeting as it attempts to recover market share following the sharp rise in oil prices in the past few days. Crude exports from Iraq’s Kurdistan to Turkey resumed recently following a hiatus of over two years and have injected additional supply into the global market. These events are putting pressure on prices from below as they bring along a possibility that when the market may not see as strong a demand as it would earlier have expected to see, its supply could surge. Additionally, geopolitical events, particularly from Gaza, are causing uncertainty in the oil arena. While President Trump’s recent statement about a potential breakthrough in peace in Gaza have injected some optimism into the market, complete implications of a deal are unclear and are keeping a firm grip on the market. Oil prices are living on a tight-rope as geopolitical events, supply additions and shifting expectations from demand keep a bearish grip on the overall direction. Most recent economic data such as the German Preliminary Consumer Price Index (CPI) and U.S. Job Openings (JOLTS) offered mixed signals that are causing uncertainty around oil prices. While CPI data revealed signs of sustained inflationary pressures in Europe, JOLTS data pointed to a softening U.S. labor market that could spell softer oil demand in the coming months. These economic prints combined with OPEC+’s output hike lead to a bearish view of oil prices in the short term. Market attention is focused on releases this week such as ECB President Christine Lagarde’s speech and the Conference Board Consumer Confidence Index as these might bring more clarity to global economic developments and affect estimates of oil demand. Economic growth staying soft or central bank signals of dovish monetary policy might bring additional losses to oil prices lower. Yet a surprise stronger set of economic prints or hawkish statements by central banks might reverse trends setting oil prices steady as market adjusts to new supply and demand balances. As a whole, the oil market itself is in flux as much as geopolitical tensions as well as economic prints along with supply developments all play important parts to guide price direction.

Bitcoin Prices – Tuesday, September 30, 2025

Bitcoin maintains its stunning rally, changing hands at $114,514 today as it recorded a 2.5% appreciation compared to yesterday. This stellar climb can be accounted for as a result of a myriad of factors that have been responsible for optimism across the market. Institutional demand continues to stay robust as a result of high-profile calls such as that made by Eric Trump stating that Bitcoin is set to have an “unbelievable” Q4 that has caused exuberance across the market. Additionally, such developments as Strive acquiring Semler Scientific that has now caused their Bitcoin reserves to hit above 10,900 BTC only serves to further prove increasing adoption of Bitcoin as a long-term store of value by institutions. Geopolitically, even Pakistan introducing a strategic Bitcoin reserve under the Pakistan Crypto Council has served to further improve market sentiment as it serves to exemplify growing acceptance of Bitcoin as a legitimate financial instrument on the world arena. As long as whale buying continues to offer support to it, Bitcoin has been able to keep above this crucial $113,000 threshold as a result of strong demand and enabling investor sentiment within the space of cryptocurrency. In spite of such optimism, Bitcoin price fluctuations continue to be affected by wider economic and geopolitical events, and potential volatility is driven by forthcoming economic data. Markets are monitoring major releases such as German Preliminary Consumer Price Index (CPI) due to be released today, ECB President Christine Lagarde speech tomorrow, U.S. Job Openings (JOLTS) tomorrow as well as Conference Board Consumer Confidence Index later this week. A show of further economic slowdown or dovish central bank action such as lower rates or inflation fears could cement Bitcoin’s upside rally as investors look to alternatives to traditional assets. Alternatively, if the economic data suggests stronger-than-anticipated growth or central bank hawkish action such as higher rates, the price of Bitcoin might come under pressure as investors move to safer assets. Simply put, Bitcoin price appreciation is a direct consequence of positive market sentiment, institutional buy-in as well as developments globally, but its future direction will remain closely correlated to wider economic developments as well as shifting tide of global monetary policy dynamics.

ETH prices – Tuesday, September 30, 2025

Ethereum (ETH) is now priced at $4,202.55, which is a 2.33% appreciation compared to its prior close. This is mainly due to increasing institutional buying interest and active whale activity. Very recently, Bitmine, a large Ethereum treasury holder, made it to headlines when it bought just over 252,000 ETH within a span of three days and now holds about 2.2 million ETH equal to $8.84 billion. This scale of buying is a strong indication of a long-term price appreciation of Ethereum as institutional investors keep on buying more of it. Moreover, whale activity is also ongoing to give a fillip to Ethereum’s bullish tone as over 15 whale wallets have collectively bought more than 406,000 ETH that are equal to about $1.6 billion. This is an indication that institutional and large-volume players have complete faith in Ethereum’s potential and this healthy buying activity will push its prices upwards in the long run. Even amid volatile markets, such large-volume activity by whales indicates that Ethereum is yet a highly valuable asset in the cryptocurrency universe. But Ethereum price dynamics are also being affected by how Ethereum ETFs are faring in the market. Spot Ethereum ETFs have witnessed tremendous outflows in the last week to the tune of nearly $800 million, which is largest such outflow across their life so far. This is causing some nervousness among investors as this could mean that institutional sentiment is weakening due to developments on the regulatory front or due to fears of short-term market volatility. Even as Ethereum’s price has been steady so far, this is only because of strong buy activity from whales. Contrast between growing whale buying and ETF outflow is a good indicator of mixed market sentiment as it shows that even as big investors remain upbeat about Ethereum’s long-term prospects, some of these investors are opting to exit through ETFs most likely as a result of short-term market volatility anticipated by them. Balance between these two countervailing factors—firm whale buying support and ETF outflow—will prove to be determinative of Ethereum’s price direction in weeks to come.