Where Are Markets Today?

U.S. and European stock futures move near unchanged early Friday, following a brisk session in which Wall Street measures set new all-time highs. Futures linked to the Dow Jones are moderately up by about 80 points (or 0.2%), and S&P 500 and Nasdaq 100 futures are up about 0.1% each. European indices are mirroring this nervous mood, with FTSE 100 and Euro Stoxx 50 futures only modestly in positive territory. Coming on the heels of yesterday’s Fed rate cut early this week, it sparked a risk-on session led by technology and smallcaps. Gains Thursday were broad-based and led by the Russell 2000 jumping 2.5%, closing at a new high first time since 2021. Markets today seem to be catching their breath and wondering whether upside momentum has further distance to travel—or whether short-term fatigue is already starting to set in.

The main propelling factor for this flat but upbeat futures tone is the dovish pivot by the Federal Reserve. The quarter-point reduction and statement indicating growing concern about softness in employment has re-set expectations for two additional rate cuts through year-end. That has helped to lift equity sentiment through rate-sensitive sectors, especially those with a growth and AI bias. Optimism is moderated by economic data indicating uneven progress, however. The drop below expectations for jobless claims is countered by soft housing and factory data and concerns regarding the underlying health of the economy. Investors are weighing relief from easier policy with doubt regarding whether the real economy is sturdy enough to support these valuation levels—especially with inflation remaining above goal. On the other side of the Atlantic, European futures are following U.S. leads, with advances for France’s CAC 40 and Germany’s DAX buoyed by hopes that eventually the ECB will follow the Fed’s path. Failing UK retail sales data and stuck eurozone industrial output are supporting views that monetary easing is farther ahead sooner than anticipated. Europe’s energy and metals sectors are gaining notice amidst global supply arguments and political tensions. At the same time, U.S. political news—especially from President Trump—appears to affect global sentiment. His remarks regarding oil, interfering with Fed policy decisions, and his scheduled phone discussion with Chinese President Xi are generating tailwinds and tail risks at once. Should the Trump–Xi discussion telegraph trade and/or technology policy breakthroughs, further advances by futures are possible. Should any escalation occur regarding global political tensions and monetary policy volatility reverse previous gains, it is possible.

The futures market, in both regions, is currently reflecting a battle between policy-driven optimism and structural macro concerns. With the Magnificent Seven tech stocks showing fatigue, broader participation will be key to maintaining new highs. Trump’s unpredictable remarks—ranging from calling wind energy a “disaster” to threatening action on TikTok, to pushing for more energy infrastructure—are adding complexity to sector expectations. At Zaye Capital Markets, we are watching this delicate balance closely. If today’s economic prints (such as U.K. retail sales and European inflation commentary) disappoint, it could reprice growth expectations and weigh on futures. But for now, markets are holding gains, and futures suggest a cautiously positive open—powered more by Fed liquidity hopes than by economic fundamentals. Whether that’s sustainable remains the question for the day.

Notable Index Performance to Friday, September 19, 2025

- Nasdaq: Higher trade, up by about 0.9%, with advances by technology and semiconductor stocks.

- S&P 500: Higher by around 0.5%– 0.6%, near all-time highs headed by large-cap technology.

- Russell 2000: Leading stocks, up 1.5% to 2.5%, benefiting from hopes for rate cuts and increasing small-cap demand.

- Dow Jones: Relatively stable rises by roughly 0.3%, defensive and industrial shares maintaining stability.

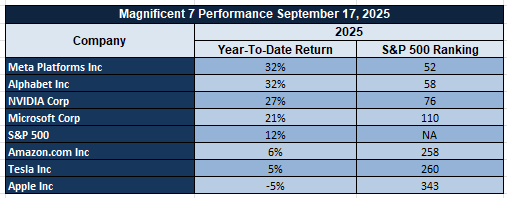

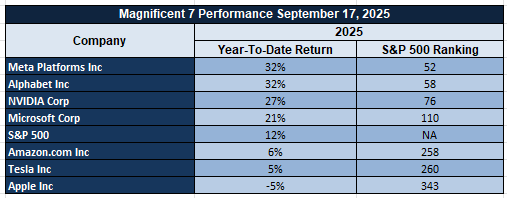

The Magnificent Seven and S&P 500 Indexes

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Meta, Alphabet, Amazon, and Tesla—continue at the forefront of index-level performance, but cracks are starting to form. Average drawdowns through the group are now over 18%, and markets are adjusting to hyperbolic valuations, particularly in technology fueled by AI-driven technology. Tesla and Meta have led the charge lower, while Nvidia has seen short-term benefit from the Intel partnership. The S&P 500 is extremely sensitive to this group’s direction, and until breadth picks up, sustained further momentum will be difficult to obtain. Rotation to energy, financials, and industrials can offer near-term relief, but new leadership by mega caps still resides at the forefront.

Drivers Behind the Market Move

1. Monetary Policy & Bank of England Slowdown in Tightening

One key driving factor is shifts in central bank policy. The Federal Reserve’s recent 25‑basis‑point rate cut and dovish rhetoric—mentioning weakness in the labour market—reshuffled gears to further easing later this year. Meanwhile, the Bank of England has aligned its policy rate at 4% and eased the pace of gilt sales (quantitative tightening) from £100 billion to £70 billion. The QT easing and less hawkish BoE stance are diminishing upward pressure on bond yields and thereby supporting equities—especially rate-sensitive sectors like technology and utilities. These are signs monetary tightening pressures are easing and sending a tailwind through markets.

2. Economic Softness & Consumer Cost Pressures Rise in UK

Softening data out of the UK is inducing caution among European investors. Weaker sales momentum, tax increases, regulatory challenges, and softening job markets are cited by retailers like Next to justify “anemic” future growth. Food inflation remains firm (about 4.9‑5%), especially for staples like meat and butter, despite a mild slowdown in other areas’ price increases. These strains hurt consumer spend hopes and drag discretionary spend-driven areas. Since UK is among large European economies, consumer sentiments here overflow to broader European futures.

3. Geopolitical Risk Premium & Political Messaging by Trump

President Trump’s latest public comments are creating layers of uncertainty that markets are absorbing. His approval of the Fed’s rate cut as ‘prudent’ while pushing to fire some Fed officials and press for quicker energy infrastructure injects political risk into central bank independence stories. On the foreign policy front, his demands for hostage release at Gaza, disagreement with Netanyahu, threats regarding immigration, and bolder positions towards foreign trade (China & TikTok) supply risk premiums. Investors view these as possible policy volatility sources—changes in tariffs, regulatory actions, shifts towards a different direction with respect to energy policy—and uncertainty like this tends to dampen broad risk-taking. These remarks account for why markets aren’t aggressively rallying in spite of favourable monetary signals; there’s instead a guarded optimism skewed by geopolitics and political risk.

Digesting Economic Data

TRUMP’s Tweets and their Implications

President Trump’s recent spate of public remarks—covering geopolitics to direct financial policy pressure—has added fresh volatility and speculation to financial markets. Perhaps most market-sensitive was messaging through the White House’s support of Federal Reserve’s recent 25-basis-point rate reduction, with Hassett declaring the Fed made a “prudent call.” This consistency implies a coordinated effort by fiscal and monetary authorities, at least superficially, and suggests the door is left open to further cuts. That said, Trump’s ongoing efforts to oust Fed Governor Lisa Cook through emergency Supreme Court petitions and his characterization of inflation and energy strategy imply a deeper discomfort with central bank independence. Markets see this as political interference and a wildcard for Fed credibility—bullish for gold and cryptos as alternate stores of value but CAUTIOUS towards long-duration assets dependent upon steady rate paths.

On the geopolitics side, Trump’s call for the “immediate release” of Gaza hostages and acknowledgment of a split with Israel’s Netanyahu bring new foreign policy unpredictability. His comments regarding Russia—stating oil price declines would have “no choice but to end the war” for Putin—and criticisms of other countries buying Russian oil add nuance to global energy diplomacy as well. These comments, and particularly when accompanied by his statement about not regretting an invitation to bring Putin to Alaska, signal a high-risk messaging approach to global oil and oil-related securities. Further, his plans to step up large-scale power initiatives to aid AI infrastructure show recognition of growing data center power demand. This can affect utilities, energy infrastructure stocks tied to grid upgrade efforts, and rare earth metals corresponding to grid modernization efforts. The political drive towards energy independence and centrally controlled U.S.-controlled power construction may direct investment funds away from green energy as well, as presaged by his “wind power is a disaster” statement.

Trump’s international economic stance is changing fast as well. His announcement of a phone call with Chinese President Xi, and his implication a TikTok agreement is near, is an effort to stabilize cross-Pacific trade relations. Describing TikTok as having “tremendous value,” and raising the specter of an extension, is a signal to markets that U.S.-China diplomacy is embarking upon a tactical reset mode. This would benefit Chinese technology equities and lower tariffs in certain sectors selectively and would be net beneficial to U.S. semiconductor and logistics players. The broader tone is still erratic—switching week to week from cooperative with Xi—to confrontational with Europe and the UK—such as when he told the UK Prime Minister to “use the military to stop immigration.” This unpredictability has a dampening effect upon global investor confidence through its impact upon international financial flows and risk-taking capacity. In Washington, Trump’s hardline posture continues to influence institutional behavior. His campaign to fire Lisa Cook and growing Republican pressure on the Federal Reserve to “curb financial fraud” signals increasing politicization of central bank decision-making. These developments could raise long-term concerns over the Fed’s operational independence—especially if rate cuts continue under political pressure. Such a shift would reverberate across fixed income markets and potentially weaken the dollar, giving gold, crypto, and energy-sensitive equities room to run. As we’ve seen historically, Trump’s words can have material impact on pricing, sentiment, and positioning. Whether discussing the Fed, energy, AI, or global diplomacy, the market no longer sees his tweets or comments as noise—they are strategic catalysts capable of moving billions in value. At Zaye Capital Markets, we are closely monitoring the velocity of Trump-driven narratives and their intersection with policy, asset rotation, and investor positioning.

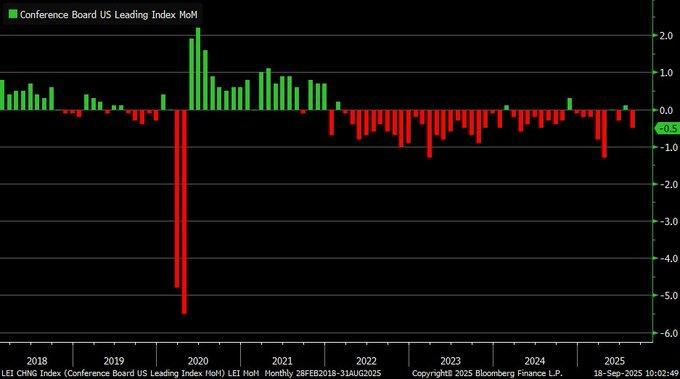

LEI Weakness Raises Recession Signals

Zaye Capital Markets notes the Conference Board Leading Economic Index dipped 0.5% during August 2025, steeper than predicted by -0.2%. The fall is continuation of a negative trend for much of the year and stirs recession risk fears, as conventionally the LEI has presaged economic contractions some seven months hence. True, there have been false signals by recent cycles and caution is required. However, the signal is clear: the risk profile to growth is altering and equity markets must allow for added fragility for domestic demand.

Our judgment is that the LEI’s decline is a symptom of structural headwinds—globalization shifts, technological change, and uneven industrial production—that are diminishing its forecasting reliability but still supporting a softening momentum narrative. Relative to other regions, global trade and infrastructure investments like those observed in emerging markets present a starker divergence: whereas the U.S. faces risks of cyclical slowdown, other economies are investing to build long-term resilience. For investors, this implies globally diversified exposures may mitigate purely U.S.-focused risks. From an equity standpoint, this is a more selective environment. Utilities are attractive as undervalued plays considering their cycle-end defensive stability, and healthcare is attractive with its price power and global earnings streams. Industrials with global exposure are also cheaper compared to peers and are a possible area to see upside if global demand stays strong. Analysts need to monitor inflation prints closely along with regional manufacturing surveys and global trade indicators to gauge and decide upon any reaction to the LEI’s continued weakness.

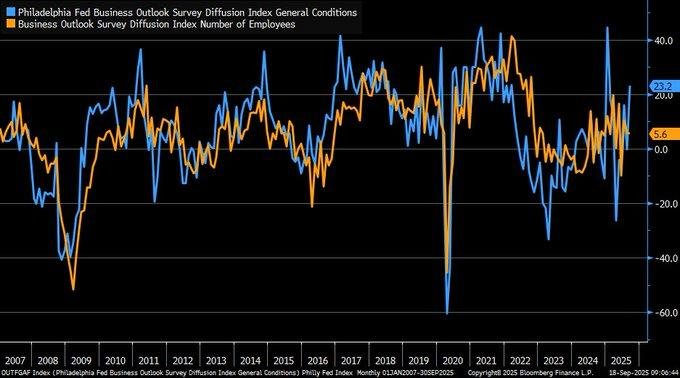

Manufacturing Surge Highlights Employment Strength

We at Zaye Capital Markets observe that the September 2025 Business Outlook Survey of the Philadelphia Fed revealed a sudden pick-up in factory activity with the main index jumping to +23.2 and employment up to +5.6, significantly above projections of +1.7. The bounce back is characteristic of the sector’s resilience and is consistent with longer-term research findings pointing to the capacity of manufacturing to bounce back once demand is stabilized. The pick-up in hiring further suggests working conditions in the industrial economy are tighter than headline jobless claims data are indicating and might provide a near-term cushioning factor to concerns about broader economic slowdown threats.

Our assessment is that this data stands in contrast to international trends, most notably the 1.1% contraction in UK manufacturing output for the same period. Such divergence underscores how domestic policy support and capital investment cycles are shaping outcomes differently across regions. While the U.S. benefits from steady demand and accommodative financial conditions, parts of Europe are struggling with weaker orders and supply chain frictions. For investors, this reinforces the importance of distinguishing between localized weakness and broader global resilience when allocating capital across geographies.

From an equity standpoint, undervalued industrial names are ones to benefit from this momentum, particularly those with high domestic exposure and operating leverage to factory demand. On a converse note, while the “prices paid” index jumping to +46.8 is a sign of continued inflationary pressure and is likely to increase chances of cost-sensitive segments like consumer discretionary experiencing margins headwinds. Analysts need to keep an eye towards near-term inflation releases, international PMI data and domestic employment surveys to see if U.S.-focused manufacturing strength can compensate global softness and steer future direction of interest-rate expectations.

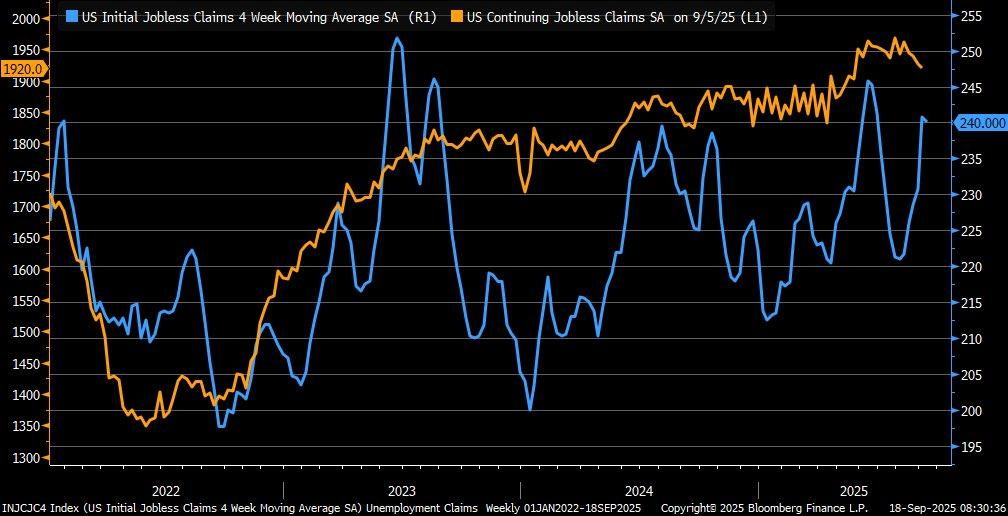

Jobless Claims Suggest Labor Market Stability

We at Zaye Capital Markets observe initial jobless claims dipped to 231,000 during the week ending September 12, 2025, and below the 240,000 consensus and previous week’s 264,000 as well. The 4-week moving average now reads 240,000, indicating stability at the labour front while the Federal Reserve recently reduced its policy rate range to 4.00%–4.25%. Continuing claims slipped by a notch to 1.920 million, a touch below expectations, indicating less long-term unemployed and furthering expectations of labour conditions being sturdier than anticipated.

Our assessment is that this strength offers a counterbalance to concerns over slowing growth, particularly as declines in jobless claims have historically preceded periods of expansion. Regional variations, however, illustrate the unevenness of the recovery: filings fell notably in Texas while ticking higher in New York, reflecting local industry dynamics and seasonal factors. Such disparities underline that while the national picture signals resilience, underlying pressures remain fragmented across states, and this could complicate the Fed’s balancing act as it monitors both inflation and employment risks.

From an equity standpoint, the resilience of the labor market favors undervalued financials, with firmer household employment usually driving credit demand and asset quality stability. Consumer discretionary shares with high wage-sensitive expenditure exposure may gain if confidence persists. Analysts need to pay attention to upcoming labor market updates, state surveys of employment, and the evolving Fed commentary to determine whether this stabilization is durable and durable or whether regionally based imbalances may re-emerge as broader risks to growth.

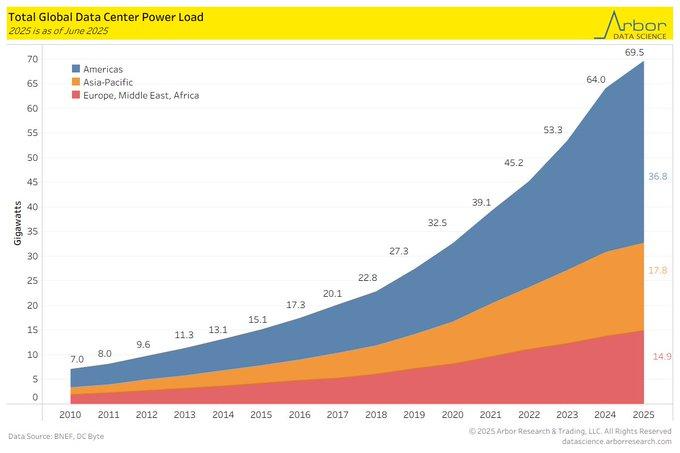

Data Center Power Surge Suggests Structural Energy Shift

We at Zaye Capital Markets note that global data center power demand has surged to 64.9 GW in 2025, up from just 7 GW in 2010, with the Americas accounting for 30.4 GW. This rapid climb, fueled by artificial intelligence and cloud computing adoption, exceeds prior energy use projections and challenges the narrative that data centers would remain a modest share of electricity consumption. Current levels suggest demand is structurally embedded in the global economy, raising questions over infrastructure adequacy and the scalability of current grids to support digital expansion.

Our view is that this trend is consistent with broader projections for increased energy intensity, including 75% global power demand growth by 2050 from data centers and electric transport. The intersection of digital infrastructure expansion and transport electrification illuminates a large capacity gap that has yet to meet corresponding generation and transmission investment. Unless there are significant upgrades, stresses on grids may lift volatility in energy prices and present risks and opportunities for sectors at large. Clean energy breakthroughs—spanning renewable integration to next-generation storage—are ever-more critical to avoid bottlenecks stalling economic development. From an equity standpoint, underappreciated utilities and energy infrastructure stocks are winners of this multi-year transition. Diversified renewable-powered utilities and grid transition plays seem especially well-placed to gain upside from accelerating demand. Industrials offering power equipment and storage solutions potentially re-rate to the upside as policy and capital redirect to energy resilience. Analysts will want to follow forward-looking energy policy landscapes, flows to renewables investment funds, and regulatory cues to determine by how much supply can meet the accelerating digital and electrification economy.

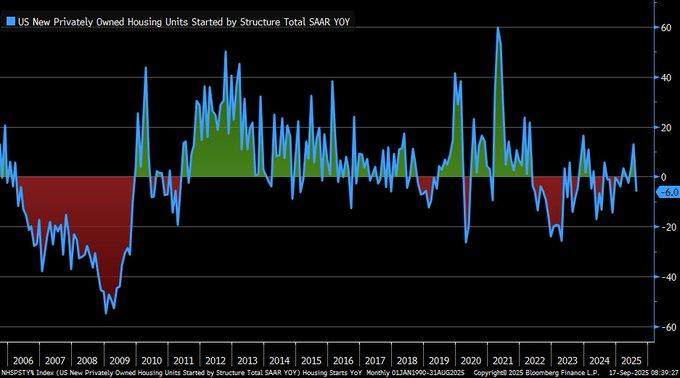

Building Permits Indicate Stress On Growth Prospects

Zaye Capital Markets notes U.S. private housing starts turned negative year-over-year during August 2025, snapping recent stability and stoking fears about a softening growth environment. The reversal occurred despite Q2 GDP growing at a 3.2% solid clip, itself registering how housing diverges from wider momentum. With construction costs rising 5.8% annually and borrowing costs high, pressures on fresh builds are growing. Comparative history tells us housing downturns have tended to precede broader contractions and thus this reversal is a prime red flag to monitor closely for investors.

Our view is that chronic affordability issues are now being compounded by high mortgage rates, around 6.5% at present, and causing a two-pronged drag on demand and supply side. Analysis argues that if financing is prohibitively expensive for much longer, housing activity will drop 10–15%, eroding confidence in the sector’s resilience. Local factors can accentuate this trend, with overheated segments set to experience steeper reversals, while those with more delicately matched supply-demand situations are likely to remain firmer. The broader threat is that softening residential construction drains over into ancillary areas, from construction materials to domestic furnishings, stiffening credit further.

From an equity perspective, underrated home improvement centers and select building materials distributors offer relative defensive appeal as maintenance and renovation activity is less cyclical than during new construction phases. Conversely, residential and commercial construction-related REITs can face valuation risks if the housing softness is extended. Analysts must track home price indexes, regional sales data, and construction pipeline formations to ascertain if this softness is cyclical or starting to reflect a broader structural adjustment within the RE space.

Fall in Mortgage Rates Provides Tenuous Relief

Zaye Capital Markets observes that the 30-year mortgage rate reduced by 45 basis points during the last two months, being the biggest fall in a year. This adjustment accompanies the recent Federal Reserve cue towards further easing in 2025 to reflect changing monetary policy expectations. As large as the reduction is, average mortgage rates are still high at around 6.7% this year, and thus affordability concerns in the residential space are hardly eliminated. The muted reaction in refinancing volumes supports that prevailing levels have yet to inject significant stimulus to dwelling demand.

Our read is that comparisons to history highlight the challenge: rates bottomed at 2.49% in September 2020, highlighting how far levels are from thresholds that significantly release demand. Studies show rates near 4% are needed to reaccelerate housing activity, and importantly, first-time buyer activity. For now, high borrowing rates will continue to hold back home sales and drag back new construction. That creates broader questions regarding housing’s contribution to total growth, and notably construction and real estate are key elements to cyclical momentum.

From an equity standpoint, underrated homebuilders with solid balance sheets and local diversification can offer selective opportunity since they can adjust through land tactics and price flexibility. Nevertheless, REITs at risk to residential and mortgage-backed segments are still vulnerable unless rates drop further. Analysts would want to keep tabs on Fed policy cues, affordability indexes for housing, and mortgage application trends to see whether this latest rate relief is an early inflection point or a brief reprieve during an otherwise stressful cycle for housing.

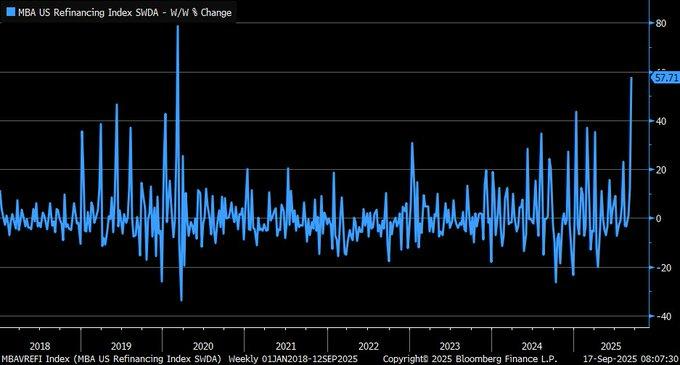

Surge Refinances Bode Market Confusion

Zaye Capital Markets observes that the Refinancing Index of MBA jumped 57.7% mid-month in September 2025 in one of its steepest gains over several years. This type of jump is unusual and was last seen when monetary policy eased aggressively during March 2020. Refinancing has historically tended to closely follow policy shifts and this move implies that households are adjusting to evolving rate expectations amidst some uncertainty over economic prospects.

Our read is that this refinancing surge is taking place amidst the rare environment of mildly higher refinancing rates, with 30-year fixed mortgages increasing 10 basis points to 6.75% through September 15, 2025. This scenario suggests many borrowers are rushing to secure terms out of fears of rate pressure once again, and not out of a response to lower cost of funds. This is a sign of increased policy sensibility and challenges the narrative that the housing market is gaining stability. Refinancing demand being sustained would further put lenders at risk for strain to deal with pipeline capacity and funding spread.

From an equity standpoint, undervalued financials and banks with excellent mortgage servicing businesses are set to gain from high refinancing volumes. Homebuilders are still vulnerable to affordability issues with volatility in rates posing difficulty to sales momentum and future planning. Analysts need to follow weekly refinancing flows, mortgage application series and Federal Reserve communications to gauge whether it is a fleeting rush or a starting point towards a bigger change in household credit behavior.

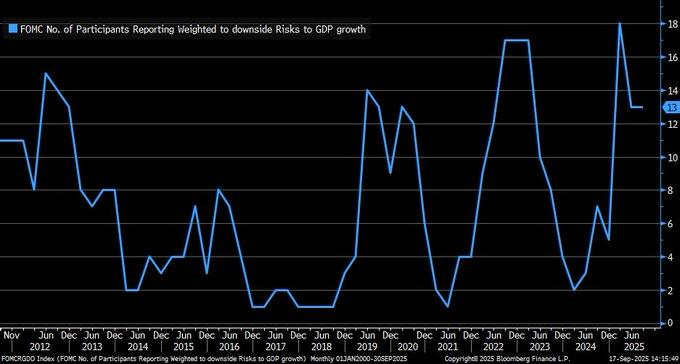

Persistent Downside Risks Weigh on Growth Outlook

Zaye Capital Markets observes that 13 FOMC officials have all singled out downside risks to GDP growth since June 2025, highlighting enduring caution around policy circles. This is a follow-on to prior expectations whereby almost all members cited comparable risks and raised concerns regarding expansion sustainability. Though the United States’ economy is ahead of G7 peers with its GDP at 13% above pre-pandemic figures by Q2 2025, policymakers are increasingly concerned with vulnerabilities to undermine momentum like softening in the labor market and stickiness in inflation.

Our assessment is that this contrast reflects rising stagflation fears—slow growth coupled with elevated price pressures—that have gained traction in recent weeks. Revised job growth data, including the sharp 911,000 downward adjustment in September, has only amplified unease around the durability of employment. Historical research shows that when downside risks are persistently flagged in FOMC projections, policy shifts often follow, raising the likelihood that additional easing measures may be deployed if growth indicators deteriorate further. The balance of risks is tilting toward defensive positioning as markets digest both strong headline GDP and weakening labor inputs.

From an equity standpoint, defensively undervalued segments like healthcare and consumer staples appear increasingly compelling based on their performance during stagflationary periods. Financials, however, risks being squeezed if further rate cuts squeeze margins without substantially increasing loan demand. Market participants will want to see close attention to upcoming inflation prints, revisions to the labor market and FOMC communications to see to what extent these downside risk views are reflected through policy shifts that can change the shape of the growth and equity environment.

Rate Cuts Hint at Caution Against Global Pressures

We at Zaye Capital Markets note that the Federal Funds Rate was reduced by 25 basis points to 4.25%–4.50% through December 2024. Even with this adjustment, however, the year-over-year drop in the Federal Funds Target Rate has continued to be negative since early 2025, a signal normally pointing to lasting economic strain. History suggests negative directional changes like this are generally correlated with discouragements in credit creation and investment demand and monetary easing will therefore fall short to compensate for structural weakness elsewhere throughout the broader economy.

Our read is that this dynamic is playing out against some significant global trends by complicating further the policy direction. Chinese GDP growth slowed to 4.7% during Q2 2025, highlighting how global circumstances are informing domestic policy decisions. As global growth momentum weakens, Federal Reserve’s deliberate pace of reduction looks to strike a balance between internal risk and external vulnerabilities to help keep inflation expectations contained while protecting against a steeper slowdown. The interplay serves to underscore financial markets’ growing interconnectivity, with cross-border movements of demand and capital flows weighing ever more significantly upon U.S. outcomes.

From an equity standpoint, undervalued infrastructure and utility stocks are opportunity plays since reduced rates favor funding environments for capital-intensive projects while defensive income stability is at center stage. However, cyclical stocks vulnerable to strong global demand like industrials related to trade may experience pressure on margins should international weakness prolong itself. Analysts need to monitor upcoming GDP reports, trends in credit markets and policy communications by the Federal Reserve to determine if cuts to rates will go deeper or stay calibrated to these multi-layered risks.

Upcoming Economic Events

GBP Retail Sales month/month

As we move deeper into a week shaped by shifting global growth narratives, attention in currency and equity markets will turn to the release of UK Retail Sales data. This indicator is a timely gauge of consumer spending—the backbone of the British economy—and has the potential to set the tone for GBP movements and cross-asset sentiment across Europe. With inflationary pressures and uneven growth trends already clouding the outlook, this print could either strengthen or undermine confidence in the UK’s near-term resilience.

GBP Retail Sales m/m

- If the data proves to come in stronger than predicted, it would confirm the scenario of durable consumer demand amidst firmer monetary conditions. Markets would see data as reinforcing the argument for the Bank of England to maintain its reticence regarding rate cuts, with policy remaining tighter for a bit longer. The pound might gain on fresh optimism regarding UK consumption, while equity sectors related to retail and discretionary segments may gain some near-term relief. Nevertheless, stronger data itself can foment fears regarding sticky inflation and cause gilt yields to edge up as rate expectations are reassessed by investors.

- If this number prints below expectations, it would reflect consumer vulnerability to high borrowing expenses and cost of living charges. The result would stoke hopes that the Bank of England will tilt towards policy loosening to prop up demand strains, depressing sterling along the way. There is scope for a dovish repricing benefit for UK bond markets and defensive equity areas like utilities and staples in anticipation of consumption slowing down. The main thing for analysts to watch will be whether this release provides evidence of stability for spending or signals vulnerabilities to compel policymakers to turn sooner than is priced by financial markets at present.

Stock Market Performance

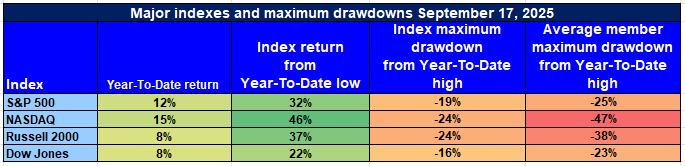

Indexes Recover from April Bottoms but Uncovering Underlying Vulnerability Continues

Zaye Capital Markets notes that U.S. equity markets have registered impressive gains since the bottom on April 8th, with key gauges registering sharp headline reversals and double-digit year-to-date gains. Yet beneath the radar screens, selloffs from annual highs and sharp constituent-level losses reflect that breadth is still weak throughout the marketplace. This divergence indicates that while indexes are registering enthusiasm related to expectations for monetary policy easing and fortified corporate profitability, the characteristic stock continuum is yet still subject to extreme volatility and thus it is crucial that investors are extremely selective with portfolio construction.

S&P 500: Strong Headline Gains, Narrow Participation

YTD: +12% | From 4/8/25 low: +32% | Highest loss below YTD high: -19% | Average peak loss per member: -25

The S&P 500 has jumped 32% since April and is 12% ahead for the year on support from large-cap leaders in technology, communications, and industrials. The index has however shed 19% off its high so far this year and its average component is 25% shy of peaks based on skewed sector performance. This is a sign of concentration in megacaps driving returns while cyclicals and mid-caps lag behind, putting broader market at risk of being buffeted by shifts in sentiment. Analysts will have to cover breadth of earnings because sustainability of gains depends on broader participation beyond select leaders.

NASDAQ: Tech Resurgence Masks Deep Pain

YTD: +15% | Since 4/8/25 low: +46% | Max drawdown from YTD high: -24% | Avg. member max drawdown: -47%

The NASDAQ enjoys the biggest rebound—a 46% jump since April and 15% so far this year—courtesy of AI euphoria, demand for cloud stocks and semiconductor momentum. Yet volatility is rampant: the index has suffered a 24% selloff to its peaks and the average membership is yet to recover by roughly half from its peaks. The divergence highlights that while growth sectors are propelling the performance of the index, the majority of its constituents are weak and testify to risks posed by valuations and weak investor sentiment. For investors, there is only one message: selective exposure to superior-quality and cash-rich innovators is necessary and speculative stocks are vulnerable to further pressure.

Russell 2000: Small-Cap Rally Lacks Conviction

YTD: +8% | Since 4/8/25 low: +37% | Max drawdown from YTD high: -24% | Avg. member max drawdown: -38% Small-caps have rebounded sharply, up 37% from the trough seen in April, but year-to-date performance is only at +8%, and drawdowns are still deep at -24% off YTD peaks. Average member decreases of -38% reflect how stressed less liquid and economic-sensitive stocks are and many are still susceptible to high borrowing cost and softening domestic demand. The gap shows reluctance among investors to factor full rebound for small-caps until further clarity is known regarding monetary policy and prospects for growth. Analysts will want to keep credit spreads and regional bank lending data close at hand as small-cap funding cost is still a crucial determinant of future performance.

Dow Jones: Defensive Tilt Provides Relative Refuge

YTD: +8% | Since 4/8/25 low: +22% | Max drawdown from YTD high: -16% | Avg. member max drawdown: -23% The Dow Jones, with its value tilt and defensive makeup, has rebounded 22% since April and resides +8% YTD, reflecting firmer stickiness compared to peers. The relatively modest 16% pullback from peaks highlights that consumer staples, diversified industrials, and traditional industries have provided some stability amidst volatility. Nevertheless, the average component still possesses a -23% loss from YTD peaks and shows that even defensives are susceptible to macro headwinds. Investors who are interested in quality income-generating stocks with price stickiness may find areas to like here, but sector rotation risks are present if economic trends continue to worsen.

At Zaye Capital Markets, our takeaway is that while indexes showcase strength, the story beneath reveals fragility. We continue to emphasize a barbell strategy: maintaining exposure to proven large-cap leaders that dominate index-level performance, while balancing with select undervalued defensives offering earnings stability and cash flow protection. Monitoring breadth indicators, earnings dispersion, and sector rotations will be critical to determining whether this rally broadens into a sustainable cycle or remains concentrated in narrow leadership.

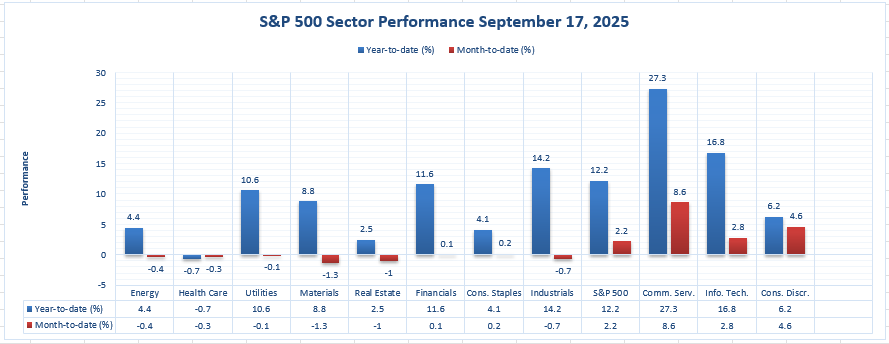

The Strongest Sector in All These Indices

We at Zaye Capital Markets interpret the sector tape as clearly dominated by Communication Services, strongest sector performer on both charts depicted. Year-to-date it’s up +27.3%, and month-to-date it leads at +8.6%—beating its own S&P 500 YTD +12.2% and MTD +2.2% performance. Lagging behind the leader is Information Technology at second with +16.8% YTD and +2.8% MTD, with Industrials completing the YTD podium at +14.2% (although -0.7% MTD evidences slowing momentum). Financials are still constructive at +11.6% YTD and +0.1% MTD, with Utilities at +10.6% YTD and -0.1% MTD.

Sector scoreboard (real numbers):

- Communication Services: +27.3% YTD | +8.6% MTD (strongest on both measures)

- Information Technology: +16.8% YTD | +2.

- Industrials: +14.2% YTD | -0.7% MTD

- Financials: +11.6% YTD | +0.1% MTD

- Utilities: +10.6% YTD | -0.1% MTD

- Materials: +8.8% YTD | -1.3% MTD

- Consumer Discretionary: +6.2% YTD | +4.6% MTD

- Energy: +4.4% YTD | -0

- Consumer Staples: +4.1% YTD | +0.2% MTD

- Real Estate: +2.5% YTD | -1.0% MTD

- Health Care: -0.7% YTD | -0.3% MTD

- S&P 500 (for reference): +12.2% YTD | +2

Our take: With Communication Services leading at +27.3% YTD and +8.6% MTD, leadership is clear; Information Technology (+16.8% / +2.8%) provides secondary strength. Mixed month-to-date prints—several sectors negative despite solid YTD gains—flag uneven momentum beneath the surface. We will continue to track whether the outperformance in the leaders broadens to Financials (+11.6% / +0.1%) and Industrials (+14.2% / -0.7%) or remains concentrated, as that breadth shift will determine durability of the current sector hierarchy.

Earnings

Earnings Recap — September 18, 2025 (Yesterday)

- FedEx Corporation

FedEx delivered stronger-than-expected earnings, with revenue of $22.24 billion versus forecasts near $21.66 billion and adjusted EPS of $3.83. Margins improved to roughly 5.8% on an adjusted basis, reflecting ongoing cost-cutting initiatives. Management reinstated full-year guidance, targeting revenue growth of 4–6% and EPS between $17.20 and $19.00 for fiscal 2026. Domestic package demand and yield management were key drivers, though international export volumes declined, highlighting the challenge of balancing global demand with operational efficiency.

- Lennar Corporation

Lennar reported disappointing results, with profits dropping nearly 46% year-over-year and revenue down about 8–9% to $8.25–$8.81 billion, missing estimates closer to $9 billion. EPS came in at $2.29, well below market expectations. Management pointed to affordability constraints driven by higher mortgage rates and construction costs as the main factors weighing on demand. Guidance for Q4 deliveries was softer than anticipated, underscoring the pressure on housing as financing conditions remain restrictive.

- Darden Restaurants, Inc.

Darden posted adjusted EPS of $1.97, slightly below consensus estimates, while revenue of $3.04 billion was largely in line and up roughly 10% year-over-year. Same-restaurant sales increased 4.7%, but cost inflation across food, labor, and imported goods, including proteins like beef and shrimp, weighed on margins. The company did, however, raise its fiscal 2026 sales growth outlook to 7.5–8.5%, signaling confidence in long-term demand despite ongoing expense headwinds.

- FactSet Research Systems, Inc.

FactSet was expected to post EPS of around $4.13–$4.14 on revenue near $593 million, with investors focused on its ability to maintain margins amid rising technology costs. Competitive pressure in financial analytics and platform investments remain areas of concern. Market participants will closely assess whether FactSet’s forward guidance provides enough reassurance about subscription growth and cost discipline going forward.

Earnings Preview — September 19, 2025 (Today)

- Golden Matrix Group, Inc.

Golden Matrix Group is set to report results today after posting a loss of $0.03 per share in its most recent update, missing expectations of breakeven. Revenue was also slightly below forecast. Investors will watch whether losses narrow and if momentum in gaming and casino products improves. Cost control, liquidity levels, and forward guidance will be critical factors in shaping sentiment, particularly given the company’s sensitivity to funding conditions.

- Anebulo Pharmaceuticals, Inc.

Anebulo’s upcoming release is expected to center on research and development progress, with investors focusing on clinical trial updates and cash burn rates. As a smaller-cap biotech, the company’s earnings themselves are less material than pipeline developments and regulatory news. Market reaction will depend on whether management provides clarity on trial timelines and funding outlook.

- MoneyHero Limited

MoneyHero’s report will provide insight into fintech adoption and regional financial services demand. Investors will pay close attention to revenue trends, user growth metrics, and customer acquisition costs. With profitability still a long-term target, commentary on monetization strategies and cost management will be especially relevant.

- Incannex Healthcare Inc.

Incannex is expected to highlight progress on its healthcare and cannabinoid-based therapy pipeline. Investors will look closely at R&D spending, clinical milestones, and balance sheet strength, given the capital-intensive nature of drug development. Any updates on regulatory submissions or trial data could drive the stock more than headline financials themselves.

Stock Market Summary – Friday, September 19, 2025

U.S. equity markets began today on the back of yesterday’s rate reduction boost, positivity in technology, and large headline announcements involving Intel and Nvidia. The mood is optimistically bullish—but with all eyes on how sustained the advances are set to be, particularly for large caps and growth stocks.

Stock Prices

Economic Indicators and Geopolitics Developments

The Federal Reserve lowered rates by 25 basis points and signaled additional easing is likely through year-end. That action boosted optimism through technology and semiconductors. Intel Corp. enjoyed its best day in decades following NVIDIA Corp.’s commitment to investing $5 billion in the company. Broader gauges—such as initial jobless claims falling—are furthering a soft-landing narrative. As rate-sensitive stocks react to dovish comments by the Fed, investor attention is shifting to sustainability of earnings and inflation pressure.

Recent News Shares

Top stories driving the market:

- Intel & Nvidia Deal: The investment by Nvidia in Intel is being seen as a huge vote of confidence in chipset infrastructure. Intel jumped close to 24%, boosting the overall technology complex.

- Rate Cut Implications: The Federal statement stressed data-dependency but rekindled hopes for further cuts later this year at its October and December meetings. That supports near-term liquidity but puts assumptions regarding economic strength at its core to the test.

The Magnificent Seven and S&P 500 Indexes

The “Magnificent Seven”—Apple, Microsoft, Nvidia, Meta, Alphabet, Amazon, and Tesla—continue at the forefront of index-level performance, but cracks are starting to form. Average drawdowns through the group are now over 18%, and markets are adjusting to hyperbolic valuations, particularly in technology fueled by AI-driven technology. Tesla and Meta have led the charge lower, while Nvidia has seen short-term benefit from the Intel partnership. The S&P 500 is extremely sensitive to this group’s direction, and until breadth picks up, sustained further momentum will be difficult to obtain. Rotation to energy, financials, and industrials can offer near-term relief, but new leadership by mega caps still resides at the forefront.

Notable Index Performance to Friday, September 19, 2025

- Nasdaq: Higher trade, up by about 0.9%, with advances by technology and semiconductor stocks.

- S&P 500: Higher by around 0.5%– 0.6%, near all-time highs headed by large-cap technology.

- Russell 2000: Leading stocks, up 1.5% to 2.5%, benefiting from hopes for rate cuts and increasing small-cap demand.

- Dow Jones: Relatively stable rises by roughly 0.3%, defensive and industrial shares maintaining stability.

Zaye Capital Markets is paying close attention to three main themes: continuation of Magnificent Seven strength, follow-through by Federal Reserve policy direction, and whether breadth from beyond the large technology group grows. The direction ahead depends upon corporate earnings strength, inflation continuation through Q4 and wider sector rotation.

Gold Price

Gold is currently trading around $3,645 per ounce, pulling back slightly after touching historic highs above $3,700 earlier this week. This cooling reflects a short-term bout of profit-taking amid a firmer U.S. dollar and climbing Treasury yields, both of which tend to put pressure on non-yielding assets like gold. Still, the broader backdrop remains highly supportive. The Federal Reserve’s quarter-point rate cut—paired with political messaging from the White House describing it as a “prudent call”—has reinforced the market’s belief that monetary policy is shifting into a more accommodative phase. At the same time, a barrage of comments from President Trump—ranging from calls to fire Fed Governor Lisa Cook to public pressure on global leaders over conflicts in Israel, Gaza, Russia, and China—has escalated geopolitical and institutional uncertainty. Markets are interpreting these moves as fresh catalysts for volatility and potential institutional fragility, boosting gold’s appeal as a hedge against both political unpredictability and central bank pressure. His upcoming call with President Xi and hints at extending trade arrangements with China further add an air of global economic recalibration—an environment in which gold historically outperforms due to its role as a stable store of value amid policy flux. The prior day’s better-than-anticipated initial jobless claims release (231,000 vs. 240,000 estimated), accompanied by declining continuing claims, indicated the U.S. labor market is staying strong while broader economic metrics soften. This subtle interpretation—of softness and not collapse—buttresses confidence that the Fed can keep easing gently without causing panic in financial markets, a consideration fortified by support for gold’s present positioning. Though dollar strength may cap near-term advances, gold is still propped up by stagflation fears persisting elsewhere, slower hiring patterns, and equity valuations moving to recalibrate. The “soft landing” scenario now embedded in financial markets provides gold leeway to digest above $3,600 as insurance against surprise inflation persistence elsewhere or geo-political shock impulses. In the weeks ahead, key data—particularly inflation releases and any sign from Trump’s China trade negotiations—will dictate whether gold regains its upward trajectory or takes a breather to absorb recent advances. For its part, however, at present gold is solidly rooted inside a bullish environment fueled by policy accommodation, geo-political tensions, and changing global leadership perspectives.

Oil Prices

Crude oil is trading around $67.40 per barrel for Brent and $63.50 per WTI barrel after a choppy week characterized by macro uncertainty and conflicting demand signals, and has stabilized there after digesting the Federal Reserve quarter-point rate reduction. Optimism is muted, however, as economic data persists with softness beneath its surface, and while generally a loosening monetary policy environment is supportive for commodities, oil’s response has been contained by growing U.S. distillate stocks, dollar buoyancy, and fears about global consumption trends. The recent drop in jobless claims and comparably decent U.S. labors data provide short-term supportive macro vibes, but weakening housing data and muted global retail activity—particularly throughout Europe and the UK—are dampening enthusiasm. In turn, while non-OPEC production has firmed and is set to trigger modest supply hikes by OPEC+ during Q4 has raised fears about impending oversupply risks at IEA and OPEC updates recently. The IEA’s long-term fear about lack of upstream investment is significant but not supportive to prices at present. Generally speaking, oil is stuck between weak but modest real-time demand and heavy product stocks and a fragile macro environment to justify aggressive bullish stands. President Trump’s recent statements are creating volatility for oil’s future. His statements regarding oil prices—that declining prices would whip up pressure on Russia to step back from its geopolitical aspirations—register an implicit preference for reduced energy expenses, interpreted by the market as political opposition to future supply cuts or strategic reserve purchases. Conversely, his vocal demands to release hostages in Gaza, criticisms of NATO and overseas leaders, and suggestions regarding military deployment to enforce immigration all elevate geopolitics-based tension premiums. The scale of this narrative maintains oil in suspense: there is a floor developing around global uncertainty and possible disruptions, yet ceilings are buttressed by growing inventories, soft retail signals like today’s GBP Retail Sales (the latter if soft will take another dent out of demand sentiment), and OPEC+ unwinding production restraint into a weak market. Markets are now adjusting to the notion that oil is less a simple economic commodity and more volatility barometer—reacting to headlines, policy changes, and supply chain disruptions as much as to sheer demand rehabilitation. Everyone is still awaiting Trump’s scheduled phone discussion with China’s Xi since any move towards fresh trade interaction or oil cooperation can invoke fresh waves through crude markets during subsequent sessions.

Bitcoin Prices

Bitcoin is currently trading around US $117,500, climbing higher after weathering short-term volatility triggered by the Federal Reserve’s 25-basis-point rate cut earlier this week. The digital asset has staged an impressive recovery from the US $111,000 range, propelled by a wave of bullish sentiment across the crypto ecosystem. One of the biggest catalysts has been the SEC’s introduction of new listing rules for crypto spot ETFs, effectively fast-tracking approvals and eliminating layers of prior red tape. This regulatory breakthrough has not only reignited institutional interest but also injected fresh liquidity into the market, leading to rallies across major exchanges. Additionally, Bahrain’s implementation of a comprehensive crypto regulation framework and new partnerships like DBS, Ripple, and Franklin Templeton’s tokenized money market fund initiative signal global momentum behind digital asset integration. Analysts are now projecting stronger capital inflows into Bitcoin as it inches closer to being granted the same asset classification as gold, a narrative gaining traction following inputs from major regulatory bodies. As macro conditions soften and central banks shift toward easing, Bitcoin’s store-of-value appeal is regaining strength—especially as investors seek decentralized alternatives to hedge against traditional financial risks. Politically, President Trump’s recent comments are stoking speculative fire. His endorsement of the Fed’s rate reduction as a “prudent call” is dovish-market friendly while his scheduled phone call with President Xi heightens risk for U.S.–China technology and trade stories—domains significantly correlated to digital currencies. His stance regarding regulatory authority combined with statements regarding national security issues, energy policy, and central bank power has furthered institutional curiosity regarding decentralized financial substitutes like Bitcoin. Yesterday’s decrease in jobless claims and tacit signals regarding a slowing labor space reinforce bets that the Fed will reduce rates prior to year-end. This change in rate path is constructive for Bitcoin, favoring environments with weak yields and abundant liquidity to thrive. Today’s economic releases—particularly UK Retail Sales—will determine risk sentiment throughout global financial centers. A weak consumer signal through Europe can cause capital to migrate towards Bitcoin as a hedge while any further weakness through traditional asset classes can expedite digital flight to safety protocols. For the present moment, Bitcoin resides at the confluence of macro easing, regulatory clarity, and expanding institutional demand—a powerful combination potentially driving price discovery through and beyond the US $120,000 threshold during sessions ahead.

ETH Prices

Ethereum (ETH) is valued at approximately $4,494 currently and steady following a week of volatility through which strong buying support was established at around the $4,450 level. The price action is typical of a consolidated market with ETH trading narrowly around $4,450 and $4,500 and shy of a crucial technical level at $4,800. On a successful breakout through this figure, Ethereum can re-test its level at $5,000 while protection to the downside at this stage is at around $4,400 and lower around $4,200 to $4,100. Overall, it is a constructive tone with support emanating from macro elements such as the recent rate cut by the Fed and weak economic data pointing to further dovish policy and growing adoption momentum through Ethereum’s DeFi and enterprise segments. On a sentiment basis, Ethereum has a edge through its first-mover advantage in the tokenization of real estate assets and NFT infrastructure and institutional-grade staking products and thus supporting its utility beyond speculative trading.

Most importantly, real-time data from the last couple of days shows whale accumulation and ETF inflows as being crucial to Ethereum’s strength. A single address bought 25,000 ETH (~US$112 million) at around US $4,493 in a solitary trade—one indicating high-conviction buying. At the same time, exchange data indicates large withdrawals of ETH from central exchanges, indicating long-term hold behavior instead of short-term selling pressure. On the institutional side, Ethereum ETFs saw inflows worth over US $360 million alone on September 15, one of the highest ever recorded single-day inflows in recent months. This sudden spurt in allocation of capital is interpreted as a message indicating Ethereum is being solidly added to structured financial portfolios alongside Bitcoin. As the ecosystem grows and confidence builds around regulatory clarity, institutional acceptance, and long-term scalability enhancements (such as proto-danksharding and rollups), ETH’s price is set to remain well-supported. Should today’s economic prints and global macro data continue to confirm a lower-rate scenario, Ethereum stands to further solidify its position as a yield-bearing, programmable asset during the next digital capital cycle.