Where Are Markets Today?

Stock futures this Thursday are higher because investors feel confident about President Donald Trump’s grand 100% tax imposed upon foreign chips not including companies having existing or future US manufacture. Dow Jones futures are higher by around 40 points, whereas S&P 500 and Nasdaq 100 futures are higher 0.26% and 0.28%, respectively. In the European marketplace, the Euro Stoxx 50 is higher 0.2%, with market both digesting US semiconductor tax as well as imminent announcement regarding Bank of England (BOE) policy. Equities remain steady against the center stage shock of an imminent trade close, with carveouts protecting companies like Apple and Nvidia, who announced or are set about giant-scale US productions.

Mid-week remarks by President Trump shook futures markets when he promised to impose a 100% tariff on imported chips, directly hitting overseas semiconductor manufacture. Critical, however, was calming investor sentiment: firms “committed to building in the United States” would be exempted. That reassured markets that market-leading incumbents with domestic production, such as Apple—who also pledged an additional $100 billion of investment in US suppliers—would be excluded from the tariff sting. That exemption was sufficient to propel Apple shares up in after-hours trading by nearly 3%, in addition to its session 5% gain, and drove the reversal in Nasdaq futures. With European markets responding to money market sentiment, the BOE is slated to reduce rates later today. The committee will likely vote with a divide, reflecting intensifying inner resistance between risk of slowdown in growth vs. increased inflation. This transatlantic split between hawkish US trade policy vs. European monetary easing continues to underpin weak European equity gain, with both the DAX and CAC 40 both rising. Rate reductions will be beneficial to interest-rate sensitive sectors, offering further equity breathing room, particularly with weakening eurozone economic fundamentals.

In Zaye Capital Markets, what appears to be the bounce back in futures is evidence that wisely selecting policy shocks happen in markets. Exemption tariff plans and strategic firm announcement like that of Apple are throwing barely sufficient light under the cover under which risk appetite recovers. There are, however, far broader alarmist horizons. Threat of US-India tariff war, politicizing labor statistics, and change of tone by the BOE all have the potential to reinitiate volatility. For the moment, futures are up—but close attention must be kept for even a whisper at plans of reprisal or downgrades in earnings interwoven with supply-chain reweighting.

Major Index Performance on Thursday, August 7, 2025

- S&P 500: At 6,274.44, down 0.3 on the day

- Nasdaq Composite: 20,895.12, down 0.5%, led down by technology, chipmaking industry

- Dow Jones Industrial Average: 41,205.36, +0.2%, boosted by energy and the healthcare sector

- Russell 2000: At 2,171.23, unchanged to fractionally stronger, holds firm in small-cap

The Magnificent Seven and the S&P 500

The “Magnificent Seven” are under increased pressure–Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla. The group is down over 18% from recent highs with Tesla and Meta leading the decline. While AI stories propelled first-half gains, mood has swung to bearish with more constricted valuations alongside growing policy risk. The S&P 500 remains stuck around its late-July 6,389 high, loses breadth. The energy, financial, and industrial groups counter technology weakness but without mega-cap leadership, the index can’t find traction.

Drivers Behind the Market Move

Markets react to trade policy crosscurrents, intervention by the central banks, and subdued economic releases. Below are three key driving factors affecting US and European market sentiment today:

- Escalations Under Trump and Trade Indeterminacy

President Trump‘s announcement that he will impose 100% blanket tariff on semiconductor import, and 50% tariff on Indian import has once again intensified global trade tensions. While relief for companies with US domestic operations, like Apple, cushioned the impact for technology-biased indices, worries about supply chains getting disrupted pervasively are yet to dissipate. In addition, Trump’s warning about increasing tariffs against the European Union in case investment pledges are not delivered has contributed volatility, with investors fearing backlash, consequently delaying plans over corporate investment.

- Expectation of Monetary Easing by Bank of England

In the west, market attention has been concentrated on the Bank of England’s 25 basis point reduction this month. The reduction will be the fifth this year by the central bank and will be despite weakening readings in inflation and growth. The vote splitting among policymakers coupled with forward guidance in the Monetary Policy Summary has had markets most concentrated. The dovish tilt has been driving equity futures across the eurozone, with the interest-rate sensitive real estate, financial sectors having risen the most.

- U.S. Yield Decline Continues, By GDP, Inflation

In the US, below-proposed release of the ISM Services PMI and poor jobs market report generated hopes regarding Federal Reserve interest rate reductions. These releases point towards weakening services sector economy with relaxed wage pressure, thus generating hopes regarding monetary easing as early as the coming FOMC meeting. Despite the fact that Trump’s characterization of last week’s jobs report as “rigged” has introduced political background noise, macro outlook supports higher liquidity expectations, which are generating market stability.

Today’s move at Zaye Capital Markets constitutes a cautious balancing act between the escalating trade policy stand and dovish monetary perspectives. The market is balancing an optimistic note, albeit cautiously, given the reaction from central banks, but it remains cautious about disruptions that might ensue over tariff-backed geopolitics.

DIGESTING ECONOMIC DATA

The TRUMP Tweets and Their Implications

Recent spates of comments given by US President Donald Trump—spanning over economic accusations, aggressive trade rhetoric, etc.—have induced market volatility globally. His statement that jobs report issued last week was “rigged” along with his allegations regarding jobs statistics manipulation previously before presidential elections has induced doubt over US economic data adequacy. The aggressive rhetoric not only obliterates institutional credibility but also injects uncertainty into future policy path. Markets rely heavily upon faith in figures issued officially while coming to assets’ prices, and when faith withers, volatility takes its root. Threat given by Trump to appoint a “truly exceptional” person after the Bureau of Labor Statistics injects heightened politicization around economic tracking, an action that could boost investor risk sensitivity as well as precipitate safe-haven interest into assets like Bitcoin, gold.

Trade policy constitutes one of Trump’s legacy keys, as his warning of massive new tariffs against India—for its re-sale of Russian oil onto world markets—has increased geopolitical tensions. India has been called the “highest tariff nation” by Trump, with an implied policy of tough action that could result in outright trade retaliation. The implications of this risk could be significant: India, an important base location in the manufacture of pharmaceuticals as well as technology, could see its export competitive edge eroded under the impact of a new tariff regime. Such disruptions could inflate import prices in the US, raising fears about inflation, while making it difficult for the Federal Reserve to determine interest rates. For our part, Zaye Capital Markets considers these events as representing a possible headwind against global risk sentiment, particularly should retaliation be extended into other emerging markets. In addition to trade policy and data integrity, the president’s protracted feud with big banks produces another factor of systemic uncertainty. By accusing Bank of America and JPMorgan Chase, among others, directly of having discriminated against him and other conservatives, Trump directly challenges America’s largest pillars of finance. These remarks can fuel supervision over bank practice, catalyze action among regulators, and catalyze court cases, all of them drags upon financial sector shares. Additionally, the grievance that banks act adversarial to political opinion can catalyze flight into non-centralized ventures like Bitcoin, particularly among retail investors in search of financial infrastructures’ neutralization.

Last but not least, Trump’s foreign policy signals—a mention of progress on significant China trade agreement and direct diplomacy with such leaders as Xi Jinping and Zelenskiy—portend mixed result. While, on the one hand, markets will take relief from China de-escalation, thereby lifting fortunes of multinationals, on another hand, continued diplomatic stress with India, Brazil, and Russia portend turbulence-prone global politics. The signal sent from the White House on continued dialogue with Brazil’s team around tariffs and negotiation on policy framework at the Fed hint at bigger monetary adjustments, perhaps with direction of politics. We at Zaye Capital Markets watch closely how these signals play out across the currency landscape, commodities, and equity space as Trump’s remark continues to dictate expectations as well as financial flows.

Dollar Index Breakdown Reveals Shifting Global Hedging Strategies

We see intense mass reversal in the U.S. Dollar Index (DXY), plummeting from around 101,000 to its 98,500 range in early August of 2025. It maintains the bearish perspective born earlier in the year on its way to technical downside targets of 98.15. The fall indicates growing investor doubt regarding the prudence of U.S. economic policy after aggressive tariffs in April precipitated a $5 trillion equity pull-down. These policy changes had eroded confidence in the pound’s traditional role as an offshore safe haven.

The trend is also supported by enhanced central bank gold hoarding as it seeks to hedge against devaluation risk. The 10.8% H1 2025 fall in the dollar not only disrupts historic portfolio balancing but signifies structural policy rebalancing of the reserves. The dollar’s credibility is again questioned in the face of rising economic uncertainty as investors continue to unwind dollar positions into non-dollars. Further, the risk of protracted indecision at the Fed on cutting interest rates can still hold the dollar on the floor, with offshore flows increasingly preferring higher-yielding assets.

Against this background, Procter & Gamble Co. (PG) appears cheap during this phase. By having more than 50% revenue contribution from international geographies, repatriation of earnings increases with soft dollar, along with higher global pricing power. Analyst focus needs to be strictly concentrated upon euro-dollar parity, while protracted decline could be overestimating internationally exposed consumer staples’ earnings upgrades. Particular focus needs to be dedicated to upcoming US inflation releases along with G7 central bank cues around further FX volatility cues.

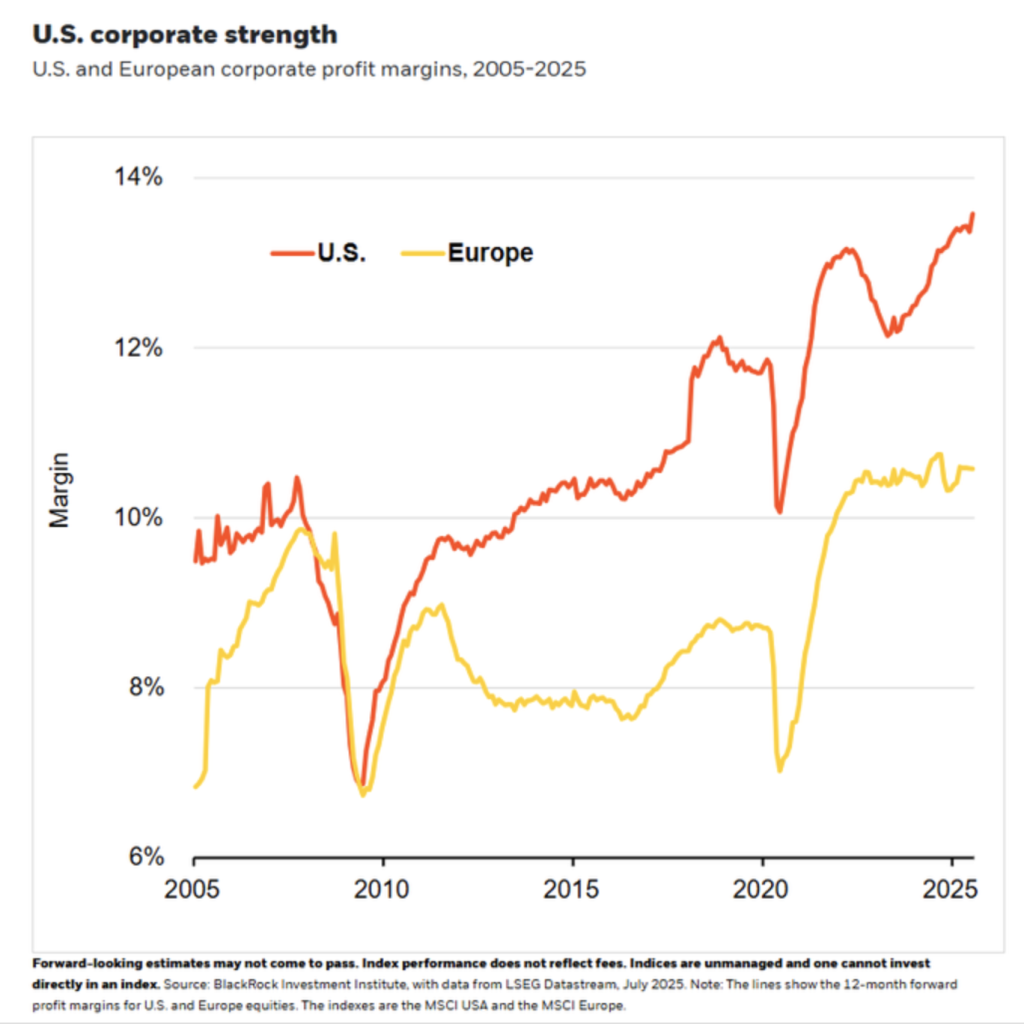

Profit Margin Gap Widens As US Technology Companies Outpace European Counterparts

A striking divergence has emerged between U.S. and European corporate profit margins, with U.S. margins climbing above 12% in 2025 while Europe remains subdued between 8–10%. The disparity stems largely from the outperformance of U.S. tech firms, which have disproportionately driven margin expansion due to scalable platforms, pricing power, and post-2020 fiscal advantages. Structural elements such as business-friendly tax incentives and accommodative federal policies have further lifted non-financial corporate profitability in the U.S., distinguishing it from the more constrained European regulatory landscape.

While U.S. margins benefit from persistent tech-led leverage, European firms are contending with headwinds. Eurostat data shows margins as a share of gross value-added have declined after peaking at 40.8%, pressured by rising labour costs and waning post-pandemic supply chain inefficiencies. The contrast challenges the perception of synchronised global recovery, instead highlighting regional disparities shaped by economic policy, sectoral composition, and wage rigidity. For investors, the margin gap underscores where operational resilience and profit reinvestment potential are currently concentrated.

In this context, we view Salesforce Inc. (CRM) as undervalued, given its expanding margins, global enterprise software demand, and limited European exposure. With digital transformation sustaining topline growth and high recurring revenue, it stands to benefit from this structural divergence. Analysts should focus on wage trend differentials across regions, EU fiscal responses to profit stagnation, and Q3 earnings commentary for margin trajectory clarity.

Homebuilding Index Rebounds Amid Interest Rate Headwinds

S&P 500 Sub-Industrial Construction hit a 2025 January peak, as sentiment flipped sharply around with an area-wide 6% year-to-date fall. The increase is a counter to the large-cap S&P 500’s 7% increase, indicating increasing optimism for home building demand. Despite macro headwinds like double-digit interest rates and increasing building input prices still tainting outlooks, current increase may be interpreted as investors both speculating in a soft-landing situation or even initial signs towards interest rate stability.

In the past, the building sector has been quite responsive to mortgage rates. Since policy rates are higher, slight adjustments in rate forecasts could result in sectoral adjustments. The 2024 real estate paper also concurred that raising mortgage rates by 1% would reduce home sales by 10% at most, in line with the sensitivity of the recovery. However, matched wage hikes, combined with minimal supply in residences, might be providing underlying support to demand, opposite expectations previously raised for sustained sector decline.

We think that D.R. Horton Inc. (DHI) is undervalued, adding leverage to any sustained increase in homepurchase activity. Scale advantage and land position position it well to benefit from even modest relaxation of lending terms. Analysts should consider watching for trends in future mortgage rates, Fed guidance on path for interest rates, and Q3 start of residences figures in gauging whether this bounce seems to suggest building momentum, or just a technical breather.

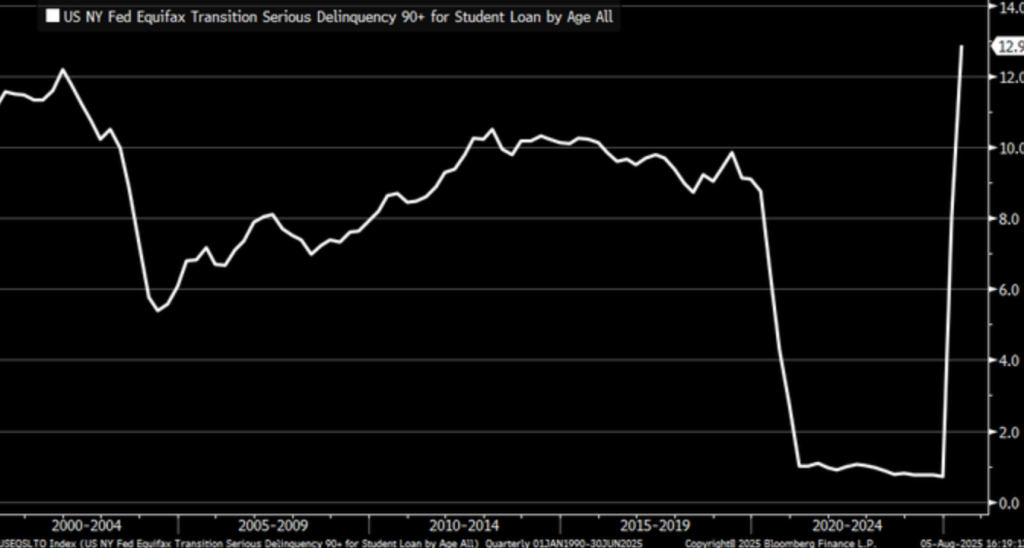

Student Loan Debts Rose, Casting What Worth Comes Out Of Investing

U.S. student loan delinquencies have increased to 12.9% in Q2 2025—its highest level in over two decades—marking a stark contrast to otherwise robust consumer credit conditions. Spiking due to delinquent balances accumulated between 2020 and 2024 that have just now entered credit reports, this increase is a lagged stress response as repayment obligations resumed. With auto and credit card debt, where delinquent levels are constant, student loans appear more prone to long-term structural imbalances.

The abnormal emphasis placed upon education debt is heightened with the astronomical $1.63 trillion outstanding amount paired with dubious employment prospects among non-technical degree holders. The researcher’s studies conducted over the past two years reinforce that the default risk among humanitiesdegree holders stands 40% higher than among STEM-degree holders, an indicator of rising student debt-cost gap instead of economic payback. In spite of government pronouncement over the past two years playing down the matter, the de-coupling of household debt trends signals student loans exhibit one fault line in an otherwise robust consumption landscape.

In this respect, Equifax Inc. (EFX) seems undervalued. Growing loan distress and tighter consumer credit conditions will both fuel heightened risk management and credit monitoring capacity demand. Analysts should also watchexpiration dates of repayment holds, graduate job trends sectorally, along with forthcoming commentary from the Fed concerning the health of the consumer credit.

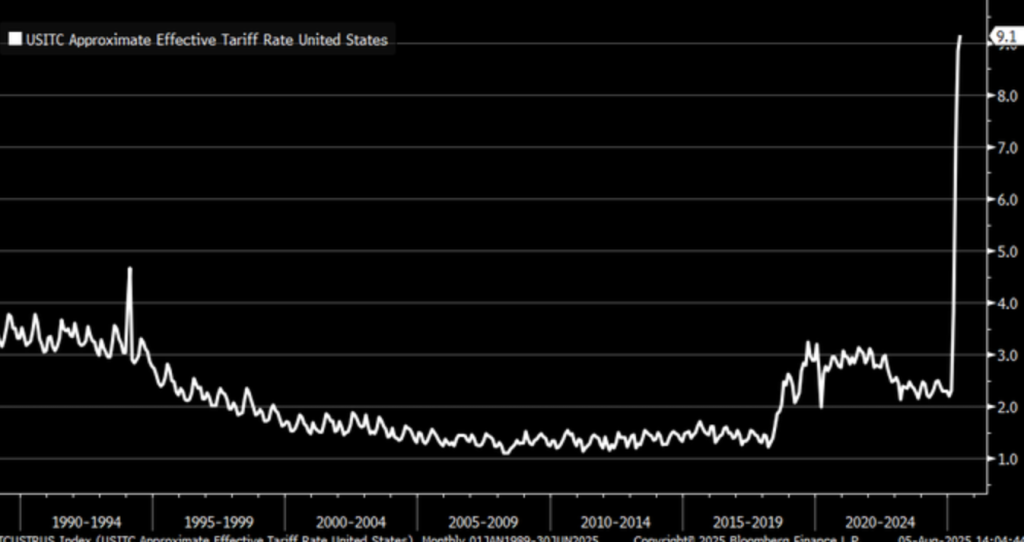

US Effective Tariff Rate Jumps To 9.1%, Raising Global Trade Alarm

Effective US tariff rate peaked 9.1% in June 2025, its three-decade high, signaling surging momentum in protectionist policy. The effective tariff had, hitherto, been in the 2–3% range, on average. The sharp jump signals the government’s tough reaction against retaliatory tariffs—their most notable targeting 25% tariff against India on their Russian oil import—the sector-specific tariffs, the foremost among them semiconductors. While some put tariff impact as large as 13.4% before trade substitution effects, the 9.1% measure gauges actual economic drags already being absorbed into international trade flows.

It’s not occurring in a vacuum. Retaliation threat against U.S. chip tariffs and general global friction are reconfiguring the post-pandemic trading landscape. Inflationary spillover reaches home consumers as higher costs feed into imported goods with producers taking on higher costs passed through. The GDP impact range estimate in 2025 as – 0.6% has the tariff path sounding alarm bells beyond exporters, into industries reliant on global supply chains, as well as raw import goods.

We view Caterpillar Inc. (CAT) as undertoned in this current situation with its cyclical risky nature and global coverage. The firm continues vulnerable to rising input prices and cross-border pressure, but medium-term non-area infra demand in the form of tariffs could cushion performance. The analysts should monitor future trade numbers, Q3 QGP guidance industrial exporting industries, and prospective adjustments in tariff width, mainly technology as well as import merchandise in energy.

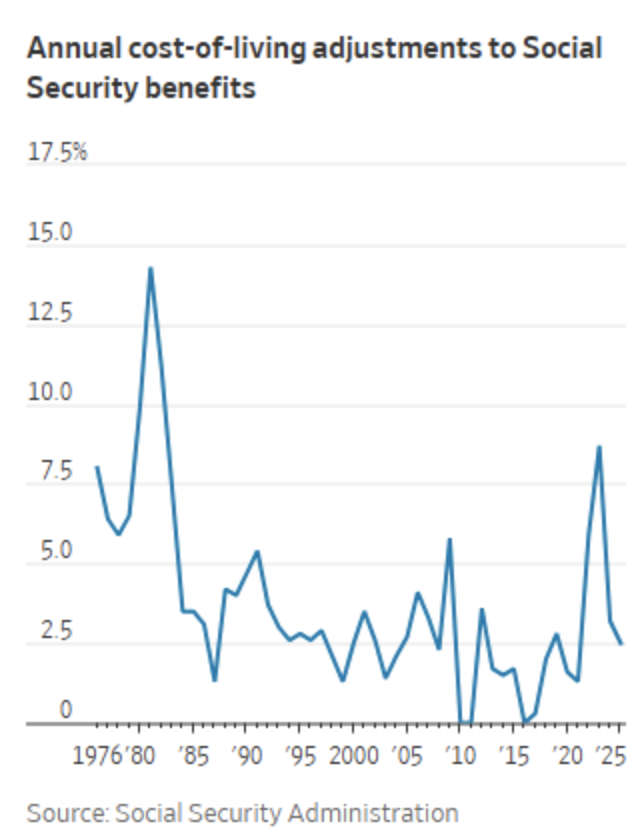

Inadequate Cola Adjustments Expose Retirees To Long-Term Inflation Risk

The Social Security Administration’s chart of history shows the dramatic 14.3% cost-of-living adjustment (COLA) in 1980, caused by double-digit inflation due to oil shocks and accommodative monetary policy. That adjustment is dwarfed by comparison to recent decades’ meager 1–3% COLA rates. Although inflation has been mostly kept under control, the specter of eroding purchasing power following increasing living costs has remained structurally present, especially for fixed-income retirees whose benefits do not keep up with real living cost increases.

Substantially fewer than a half of the U.S. state pension systems currently provide COLA, and those did experience the increases based on CPI-U, which increased only 2.9% in 2024. For most retired beneficiaries who do not receive the benefit boosts annually, rising health care costs—most notably within the IRMAA income levels—can be extremely effective in decreasing real income. Within a 20-year timeframe, the retiree’s benefit purchasing power could be decreased by as much as 30%, increasingly a problem as medical inflation continues its success and demographic pressure continues its success against entitlement programs.

We think UnitedHealth Group (UNH) is underpriced in this macro context. With rising healthcare expenses by retirees and real-cost health care inflation running ahead of fixed benefits, managed care and supplementary Medicare solution opportunities increase. Strategists will be interested to see future CPI medical care inflation readings, changes to Medicare premium structure, and budget proposals such as entitlement reform or CPI reweighting.

UPCOMING ECONOMIC EVENTS

Boe Policy Decisions, Bailey Speech & US Jobless Claims To Set Global Tone

It’s economic events calendar this week that contains a number of determinative events whose impact has the capacity to redefine market investor sentiment. In an era where it’s pressure upon the center banks not to inflate but without compromising expansion, key attention goes into this week’s interest rate decision, forward guidance, and recent US unemployment filings with the Bank of England (BOE). The releases coincide with equity markets searching for direction clarity, bond volatility, and monetary policy existing in an equilibrium equilibrium. The following are what to watch along with what it means if actuals go better/worse than est.

BOE Monetary Policy Overview & Official Bank Rate

BOE’s Official Bank Rate announcement will be setting the tone for sterling market sentiment and UK equity indices overall.

- If actual exceeds forecast, that would give an indication of a hawkish BOE bias, in confirmation it’s eager to snuff out inflation. That will be supportive of the British pound but negative for interest-rate sensitive sectors such as real estate, consumer lending, and homebuilding.

- Below forecast, however, will provide an indication of increased worries about UK economic stability and could precipitate sterling softness while lifting equity sectors most susceptible to home markets and spending by the consumer. The Monetary Policy Summary will be in the key role of providing color about inflation expectations and outlook for GDP, and possibly supporting sentiment weeks down the line in market sentiment.

MPC Official Bank Rate Votes & Monetary Policy Report

Apart from the major decision, MPC breakdown also helps to introduce some nuance.

- More members who are hawks, with even larger majorities, may be seen as confirmation that risk of higher inflation remains current—pushing gilt yields further up and testing equity valuations.

- Increasing dovish elements, meanwhile, may be seen as its own moment of flip in the cycle of rising interest rates, with consequent bond market rallying and comforting UK-domiciled risk assets. The Monetary Policy Report, and new forecasts for inflation and growth, will underpin the Q3 and Q4 expectations and has potential spillover into UK gilt positioning and into the FTSE 100.

BOE Governor Bailey Addresses

Tomorrow’s Governor Andrew Bailey’s address will offer live policy guidance.

- If Bailey indicates extended inflation watchfulness with a prolonged tightening cycle, it might lead to market volatility, pushing near-term gains while hardening speculation around another lift in rates this year.

- If dovish Bailey addressed, emphasizing weakening consumer demand/lay-offs, market expectations might reverse hoping policy easing over the coming year. The announcement will be big, especially, if it suggests imminent change in BOE’s policy framework in reaction to the decelerating world economy.

U.S. Unemployment Claims

Across the Atlantic, the weekly U.S. jobless claims data will offer a snapshot of real-time labour market health.

- Lower-than-expected claims will likely affirm continued strength in hiring and consumer demand, potentially reviving concerns over sticky wage inflation. That could raise the prospect of additional Federal Reserve tightening or extended higher-for-longer policy, pressuring equities while boosting the dollar and Treasury yields.

- In contrast, a higher-than-forecast figure would validate concerns that the labour market is cooling under elevated borrowing costs and trade friction. Such an outcome could drive investors into defensive sectors and increase bond demand, while tempering Fed rate expectations.

As we approach these key economic events, markets remain hypersensitive to macro signals. For investors, the interpretation of these releases will not just reflect near-term rate paths—but also broader confidence in global economic stability. At Zaye Capital Markets, we continue to monitor developments closely to identify tactical opportunities as the macro landscape evolves.

EARNINGS

Wednesday, August 6, 2025 – Reported Results

- McDonald’s Corporation

McDonald’s delivered stronger-than-expected results, supported by a 3.8% rise in same-store sales and an 11% increase in net profit. The company’s ability to navigate inflationary pressures through pricing power and international strength drove positive investor reaction, lifting the stock by approximately 3%. Its consistent global footprint remains a stabilising force amid consumer spending fluctuations.

- Walt Disney Company (The)

Disney topped earnings estimates and raised full-year profit guidance, buoyed by theme park strength and early streaming recovery. However, the stock dipped 2.7% as legacy media revenue—especially linear TV—continues to weigh on long-term growth visibility. Investors remain focused on profitability in its streaming segment and cost reduction momentum.

- Uber Technologies, Inc.

Uber impressed with a 34% year-over-year EPS growth to $0.63 and revenue reaching $12.65 billion. Despite unveiling a massive $20 billion buyback plan, shares slipped slightly due to investor scepticism around its robotaxi strategy and cost scaling in newer verticals. Nevertheless, mobility and delivery segments maintained solid momentum.

- Shopify Inc.

Shopify delivered a breakout quarter, surpassing revenue and earnings estimates. Shares jumped 22% as investor confidence surged around e-commerce resilience, margin expansion, and cross-border growth. The company’s execution on cost control and international logistics further positioned it as a clear standout in tech retail.

- AppLovin Corporation

AppLovin posted EPS of $2.39 versus an expected $1.96 and revenue of $1.26 billion, beating estimates across the board. Despite strong Q2 figures and raised Q3 guidance, shares fell slightly in after-hours trading, suggesting the rally may have priced in most of the upside ahead of earnings.

Other Reports

Additional earnings from Airbnb, Coca-Cola Europacific Partners, Joby Aviation, New York Times Company, Blackstone Secured Lending Fund, and Wix.com Ltd. were also released. While detailed numbers were limited at press time, early market reaction remained mixed, with some names reacting positively on guidance, while others lagged amid sector rotation.

Thursday, August 7, 2025 – Upcoming Earnings

- Eli Lilly and Company

Eli Lilly is set to report before the bell. Investors will focus on developments within its diabetes and weight-loss drug pipeline, especially following recent demand trends in GLP-1 treatments. Guidance will be key in confirming whether momentum continues into H2 2025.

- Gilead Sciences, Inc.

Gilead’s earnings will provide insight into antiviral drug performance and innovation within oncology. Key metrics to watch include R&D expenditure and expansion in international markets. Markets are expecting steady margins and pipeline progression updates.

- ConocoPhillips

As one of the largest U.S. energy producers, ConocoPhillips will be under close watch for its cash flow trends, capital expenditure discipline, and shareholder returns. With oil prices stabilising, its guidance on production growth and dividend policy will be critical for energy sentiment.

- Constellation Energy Corporation

Constellation’s results will shed light on demand dynamics in the utility and renewable energy space. Investors are particularly focused on its pricing structure, exposure to electricity trading markets, and forward cost of capital under regulatory constraints.

- Motorola Solutions, Inc.

Reporting after the close, Motorola is expected to show stable performance in public safety and communications. Analysts are watching closely for commentary on federal contracts, backlog strength, and progress in software integration, which supports its margin profile.

- Monster Beverage Corporation

Monster’s update will be dissected for beverage volume trends, distribution expansion, and competitive pricing in the non-alcoholic drinks space. Investors are also keen to assess whether global demand is holding steady amid shifting consumer preferences.

- Warner Bros. Discovery, Inc. – Series A

This earnings print will reveal how well the company is managing costs while growing streaming and core entertainment revenue. Subscriber metrics and advertising recovery remain front and centre, especially amid tightening content budgets across the industry.

- Rocket Lab Corporation

Rocket Lab will round out the day’s earnings, with focus on launch cadence, contract pipeline, and space infrastructure investment. The company’s commercial space position and financial burn rate will be closely examined for signs of sustainable scaling.

At Zaye Capital Markets, today’s lineup presents a multi-sector earnings cross-section, offering critical signals on healthcare resilience, energy capital flows, and the evolving media and tech outlook. We continue to monitor forward guidance closely as earnings remain the market’s main directional driver.

Stock Market Update – Thursday, August 7, 2025

U.S. equity markets opened Thursday trading cautiously as investors absorbed new tariff comments by President Donald Trump, another batch of earnings, and cross-purposes from the economic calendar. While the relative S&P 500 meandered close to recent highs, tech-driven volatility remains roil under the surface. The Nasdaq Composite has been weak early, dampened by sporadic action in megacap stocks and AI-exposed names. The Dow Jones index, however, is bucking this trend, along with the Russell 2000, assisted by defensives and rotation in the energy space.

Stock Prices

Financial Indicators and Geopolitical Trends

Market sentiment remains weak under policy uncertainty. President Trump’s most recent move to impose a 25% retaliatory duty on Indian imports in the energy and pharma trade balances presents new challenges to emerging market supply chains. In the meantime, Federal Reserve officials indicated caution on further rate action, emphasizing persistent labour market resilience but moderating wage expansion, while sustaining policy easing expectations.

Latest Share News

These 5 Stocks Are Leading The Day’s Activity

UBER | Uber Technologies

It fell about 2% despite the company’s strong earnings, with its $20B buyback program and double-digit top-line growth met with fears about its transition into autonomous drive.

$SHOP | Shopify

Shopify rallied 22% after blowing past 2Q expectations. Above-guidance gross margin along with cross-border leadership sent waves of optimistic Street analyst upgrades.

$AMD | Advanced Micro Devices

Even though it was well ahead of revenue estimates, AMD declined 1.4% after hours after missing by the slimmest of margins. Fear of Chinese export restrictions on AI chips is dragging it back.

$DIS | Walt Disney

Disney fell 2.7% even though it had topped estimates and also revised its forecast higher. Downfall in linear television and revenue headwinds in broadcast media maintains the bearish tone.

$APP | AppLovin

AppLovin posted an EPS beat and improved revision in its Q3 outlook, but after-hours volatility left investors questioning how much AI-ad momentum has been captured.

The Magnificent Seven and the S&P 500

The “Magnificent Seven” are under increased pressure–Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla. The group is down over 18% from recent highs with Tesla and Meta leading the decline. While AI stories propelled first-half gains, mood has swung to bearish with more constricted valuations alongside growing policy risk. The S&P 500 remains stuck around its late-July 6,389 high, loses breadth. The energy, financial, and industrial groups counter technology weakness but without mega-cap leadership, the index can’t find traction.

Major Index Performance on Thursday, August 7, 2025

- S&P 500: At 6,274.44, down 0.3 on the day

- Nasdaq Composite: 20,895.12, down 0.5%, led down by technology, chipmaking industry

- Dow Jones Industrial Average: 41,205.36, +0.2%, boosted by energy and the healthcare sector

- Russell 2000: At 2,171.23, unchanged to fractionally stronger, holds firm in small-cap

In Zaye Capital Markets, sector leadership, market internals, and earning momentum are closely held under our watch. As the macro narrative continues to shift, continued leadership beyond concentrated index leadership in large cap will be required in justified higher phase in US equities.

Gold Price

Today’s range has been between $3,378.80 and $3,392.50 per ounce, with more resilience with higher geopolitical as well as economic uncertainty. The spike is proof of increasing safety-demand with President Trump’s fresh threat of tariffs on India, jobs-data manipulation charges, as well as bank discrimination accusations imbuing volatility in marketplaces. His statements of having an apparent deal with China imminent, calling on the central bank to act adds policy-direction complexity. For both sides, today’s news of voting rates at the BOE as well as unemployment claims has heightened investor focus, with the BOE having to navigate its path with growth fears as well as inflationary pressure. These headlines, along with hints emanating from the White House on policy framework reshufflings with the Fed has worked on maintaining gold’s resilience under an uncertain macroclimate.

Yesterday’s economic reports—dovish ISM Services PMI and weak jobs prints—sparked fears of economic decline, pushing gold into the $3,380 level. With rate cuts imminent and confidence in government statistics undermined, gold continues to enjoy favor as an inflation hedge and policy uncertainty. This positioning is, in our view at Zaye Capital Markets, in play particularly with the global central banks on guard and news on tariffs adding to it. Without uncertainty, gold might attempt reaching the $3,500–$3,600 levels in the coming couple weeks, underpinning its positioning as the hedge of choice with poor trust in fiat policy instruments.

OIL PRICES

Crude oil prices are moderately reversing, with WTI crude at about $64.57 and Brent at about $67.09 per barrel, as markets process stronger-than-anticipated U.S. oil-demand gains and tighter-than-anticipated 3 million-barrel decline in crude inventories. Though this strength in demand driving this week’s reversal remains bullish, gains are capped, however, by tensions in the Middle East and new supply risks. OPEC+ has recently agreed higher September oil supply targets, injecting downside risk, while the IEA warns of thin inventories this coming winter. In the interim, President Trump’s escalation over tariffs against India—i.e., its Russian oil purchases—presents an achievable adjustment of global trade corridors, adding uncertainty over Middle East and Far East supply flows. His remark that Russian policy depends upon energy prices has also suggested an appeal for cheaper international oil prices, adding pressure upon crude markers.

Yesterday’s soft readings in the ISM Services PMI and new hopes for less aggressive monetary policy bolstered energy assets, with energy demand expectations picking up somewhat under assumptions of slowing interest rate hikes. The short term, however, remains heavily reliant on today’s interest rate decision from the BOE and US unemployment claims. Dovish bias from central banks, however, could bring support through economic optimism, and thus, oil prices, indirectly, while a development into tougher hawkish tone or weak labour market releases dampen energy demand prospects. We at Zaye Capital Markets watch closely real-time releases among IEA, OPEC+, and the central banks, as oil remains extremely sensitive to shifting narratives about inflation, trade sanctions, and supply discipline. In lack of clear resolution around tariffs, as well as macro policy direction, oil should remain volatile around $60–$70 per barrel.

BITCOIN PRICES

It’s trading between $114,728, with intraday volatility between $113,398, $115,678, as the market responds to skyrocketing institutional demand and macroeconomic uncertainty. The crypto space was greeted with some positive news as it became apparent that the SEC has made its determination that liquid staking activities won’t qualify under the securities category, removing regulatory threat and stoking enthusiasm to join decentralised finance. Also, Coinbase’s 30–35% convert premium in 2032 notes indicates investor optimism in crypto-backed debt remains. President Trump’s increasingly vitriolic rhetoric—the charges of “rigged” jobs data, impending tariffs against India, and discrimination claims against banks—has been an adder under the risk-off tone, with investors rotating into decentralised alternatives like Bitcoin. His continued rhetoric for reshuffling trade, as well as an active reallocation into digital reserves, confirms the script on Bitcoin as a geopolitical hedge.

Yesterday’s lack lustre ISM Services PMI and dovish labour market signaling gave booster to expectations of monetary ease, driving speculative interest into crypto assets once again. Bitcoin’s surge into the $115,000 level corresponds with this shift in sentiment, accompanied with the view that dovish, non-yielding assets are primed to gain relief policy conditions. Optimism, nonetheless, over the Fed’s next move and global tariff repercussions continues to obscure downside risk. The later release this week of BOE policy comments and US jobless claims are apt to catalyze sentiment further, most notably should they underpin slowing global economics, or market repricing of liquidity expectations. In Zaye Capital Markets, our case remains Bitcoin continues at a key technical and macro crossroads—between breaking higher into $120,000 should dovish cues endure, or correction into $110,000 should economic resilience regain.

ETH PRICES

Ethereum (ETH) trades at about $3,668, with intraday values at $3,573-$3,704, as an indication of investor interest with rising institutional buys. Importantly, an over 63,800 ETH sale worth about $232 million was conducted with FalconX and Galaxy Digital, exposing big players’ high-conviction holdings. The sale confirms other Mega whales’ accumulation over several days ago of near $300 million worth ETH, evidencing Bitcoin’s smart contract fundamental instrument. In the background, ETF flows into ETH products, exclusively via BlackRock, amount to $1.7 billion, further elucidating institutional belief in Ethereum’s longer-term value, regardless of market’s shorter-term volatiles.

Conversely, net taker volume has registered hard downtick pressure to –$418 million, one of the largest-ever sell-side imbalances on record. Although few ETFs seem to be losing small quantities, the size of repeated whale purchases indicates most of this supply has been absorbed, possibly resulting in supply squeeze. This ETF outflow/Deep-pocket accumulation tug-of-war may keep ETH range-bound in the near term, but fundamentals are bullish. In our view, at Zaye Capital Markets, this token has an imminent prospective breakout above $3,700–$4,000, precisely if regulatory clarity continues to enhance alongside macro conditions in general.